LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- 1 Understand the uses and limitations of an income statement.

- 2 Understand the content and format of the income statement.

- 3 Prepare an income statement.

- 4 Explain how to report items in the income statement.

- 5 Identify where to report earnings per share information.

- 6 Explain intraperiod tax allocation.

- 7 Understand the reporting of accounting changes and errors.

- 8 Prepare a retained earnings statement.

- 9 Explain how to report other comprehensive income.

Financial Statements Are Changing

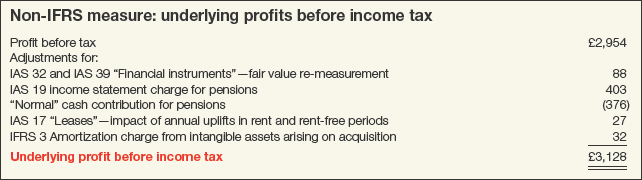

Tesco Group (GBR) recently presented the following additional supplemental information in its income statement.

The directors of Tesco commented in their report to shareholders that they believe the “Underlying profit before income tax” provides additional useful information to shareholders on company trends and performance. They note that these measures are used for internal performance analysis and that underlying profit as defined by IFRS may not be directly comparable with other companies' adjusted profit measures (sometimes referred to as pro forma measures). In addition, they state that it is not intended to be a substitute for, or superior to, IFRS measurements of profit.

Why do companies make these additional adjustments? One major reason is that companies believe the items on the income statement are not representative of operating results. Here is another example using Marks and Spencer plc (M&S) (GBR). M&S at one time reported in a separate schedule adjustments to net income for items such as strategic programme costs, restructuring costs, and impairment charges. All these adjustments made the adjusted income measure higher than reported income.

Skeptics of these practices note that these adjustments generally lead to higher adjusted net income. In addition, they note that it is difficult to compare these adjusted or pro forma numbers as one company may have a different view as to what it believes is fundamental to the business. In many ways, the pro forma reporting practices by Tesco and M&S represent implied criticisms of certain financial reporting standards, including how the information is presented on the income statement.

Recently, the IASB initiated a project on financial statement presentation to address users' concerns about these practices. Users believe too many alternatives for classifying and reporting income statement information exist. They note that information is often highly aggregated and inconsistently presented. As a result, it is difficult to assess the financial performance of the company and compare its results with other companies.

Take the income statement as an example. Some companies disaggregate product costs (such as materials and labor) as well as general and administrative costs (such as rent and utilities) in their income statements. Other companies simply report product costs and general and administrative costs in the aggregate. It is difficult to understand the nature of these costs (recurring or non-recurring, fixed or variable) if the costs are aggregated. In other words, two different companies can comply with existing standards for income statement presentation but vary considerably in the detail provided.

What is needed is a common set of principles to be followed when income statement information is presented. The IASB's work on financial statement presentation has been on the “back burner” as the Board focused instead on the major projects of revenue, leases, insurance, and financial instruments. However, input from IASB stakeholders indicate that the project on financial statement presentation and, in particular, income reporting should be a high priority. Hopefully, a restarted project on financial statement presentation will provide those necessary principles.

Sources: “Staff Draft of Exposure Draft: Financial Statement Presentation” (IASB: July 10, 2010); and H. Hoogervorst, “The Imprecise World of Accounting,” Speech to the International Association for Accounting Education and Research (June 20, 2012).

PREVIEW OF CHAPTER 4

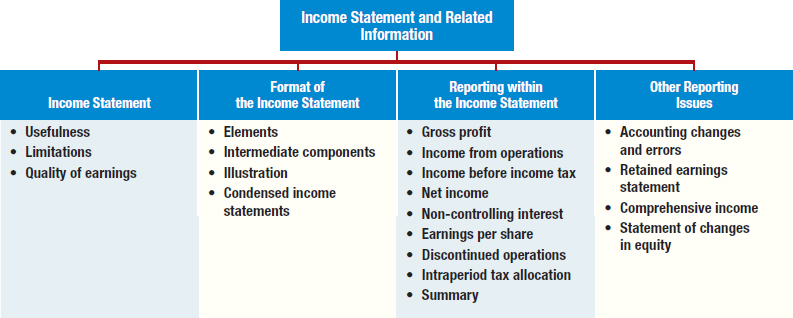

As indicated in the opening story, companies are attempting to provide income statement information they believe is useful for decision-making. Investors need complete and comparable information on income and its components to assess company profitability correctly. In this chapter, we examine the many different types of revenues, expenses, gains, and losses that affect the income statement and related information, as follows.

INCOME STATEMENT

LEARNING OBJECTIVE ![]()

Understand the uses and limitations of an income statement.

The income statement is the report that measures the success of company operations for a given period of time. (It is also often called the statement of income or statement of earnings.1) The business and investment community uses the income statement to determine profitability, investment value, and creditworthiness. It provides investors and creditors with information that helps them predict the amounts, timing, and uncertainty of future cash flows.

Usefulness of the Income Statement

The income statement helps users of financial statements predict future cash flows in a number of ways. For example, investors and creditors use the income statement information to:

- 1. Evaluate the past performance of the company. Examining revenues and expenses indicates how the company performed and allows comparison of its performance to its competitors. For example, analysts use the income data provided by Hyundai (KOR) to compare its performance to that of Toyota (JPN).

- 2. Provide a basis for predicting future performance. Information about past performance helps to determine important trends that, if continued, provide information about future performance. For example, General Electric (GE) (USA) at one time reported consistent increases in revenues. Obviously, past success does not necessarily translate into future success. However, analysts can better predict future revenues, and hence earnings and cash flows, if a reasonable correlation exists between past and future performance.

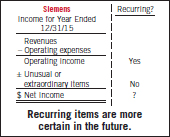

- 3. Help assess the risk or uncertainty of achieving future cash flows. Information on the various components of income—revenues, expenses, gains, and losses—highlights the relationships among them. It also helps to assess the risk of not achieving a particular level of cash flows in the future. For example, investors and creditors often segregate Siemens AG's (DEU) operating performance from discontinued operations because Siemens primarily generates revenues and cash through its operations. Thus, results from continuing operations have greater significance for predicting future performance than do results from discontinued operations.

In summary, information in the income statement—revenues, expenses, gains, and losses—helps users evaluate past performance. It also provides insights into the likelihood of achieving a particular level of cash flows in the future.

Limitations of the Income Statement

Because net income is an estimate and reflects a number of assumptions, income statement users need to be aware of certain limitations associated with its information. Some of these limitations include:

- 1. Companies omit items from the income statement that they cannot measure reliably. Current practice prohibits recognition of certain items from the determination of income even though the effects of these items can arguably affect the company's performance. For example, a company may not record unrealized gains and losses on certain investment securities in income when there is uncertainty that it will ever realize the changes in value. In addition, more and more companies, like L'Oréal (FRA) and Daimler AG (DEU), experience increases in value due to brand recognition, customer service, and product quality. A common framework for identifying and reporting these types of values is still lacking.

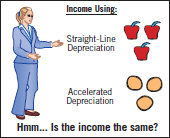

- 2. Income numbers are affected by the accounting methods employed. One company may depreciate its plant assets on an accelerated basis; another chooses straight-line depreciation. Assuming all other factors are equal, the first company will report lower income. In effect, we are comparing apples to oranges.

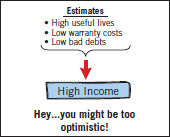

- 3. Income measurement involves judgment. For example, one company in good faith may estimate the useful life of an asset to be 20 years while another company uses a 15-year estimate for the same type of asset. Similarly, some companies may make optimistic estimates of future warranty costs and bad debt write-offs, which results in lower expense and higher income.

In summary, several limitations of the income statement reduce the usefulness of its information for predicting the amounts, timing, and uncertainty of future cash flows.

Quality of Earnings

So far, our discussion has highlighted the importance of information in the income statement for investment and credit decisions, including the evaluation of the company and its managers.2 Companies try to meet or beat market expectations so that the market price of their shares and the value of management's compensation increase. As a result, companies have incentives to manage income to meet earnings targets or to make earnings look less risky.

Regulators have expressed concern that the motivations to meet earnings targets may override good business practices. This erodes the quality of earnings and the quality of financial reporting. As a former regulator noted, “Managing may be giving way to manipulation; integrity may be losing out to illusion.”3

What is earnings management? It is often defined as the planned timing of revenues, expenses, gains, and losses to smooth out bumps in earnings. In most cases, companies use earnings management to increase income in the current year at the expense of income in future years. For example, they prematurely recognize sales in order to boost earnings. As one commentator noted, “... it's like popping a cork in [opening] a bottle of wine before it is ready.”

Companies also use earnings management to decrease current earnings in order to increase income in the future. The classic case is the use of “cookie jar” reserves. Companies establish these reserves by using unrealistic assumptions to estimate liabilities for such items as loan losses, restructuring charges, and warranty returns. The companies then reduce these reserves to increase reported income in the future.

Such earnings management negatively affects the quality of earnings if it distorts the information in a way that is less useful for predicting future earnings and cash flows. Markets rely on trust. The bond between shareholders and the company must remain strong. Investors or others losing faith in the numbers reported in the financial statements will damage capital markets.

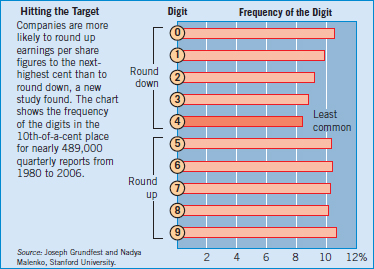

What do the numbers mean? FOUR: THE LONELIEST NUMBER

Managing earnings up or down adversely affects the quality of earnings. Why do companies engage in such practices? Some recent research concludes that many companies tweak quarterly earnings to meet investor expectations. How do they do it? Research findings indicate that companies tend to nudge their earnings numbers up by a 10th of a cent or two. That lets them round results up to the highest cent, as illustrated in the following chart.

What the research shows is that the number “4” appeared less often in the 10th's place than any other digit and significantly less often than would be expected by chance. This effect is called “quadrophobia.” For the typical company in the study, an increase of $31,000 in quarterly net income would boost earnings per share by a 10th of a cent. A more recent analysis of quarterly results for more than 2,600 companies found that rounding up remains more common than rounding down.

Another recent study reinforces the concerns about earnings management. Based on a survey of 169 public-company chief financial officers (and with in-depth interviews of 12), the study concludes that high-quality earnings are sustainable when backed by actual cash flows and “avoiding unreliable long-term estimates.” However, about 20 percent of firms manage earnings to misrepresent their economic performance. And when they do manage earnings, it could move EPS by an average of 10 percent.

Is such earnings management a problem for investors? It is if they cannot determine the impact on earnings quality. Indeed, the surveyed CFOs “believe that it is difficult for outside observers to unravel earnings management, especially when such earnings are managed using subtle unobservable choices or real actions.” What's an investor to do? The survey authors say the CFOs “advocate paying close attention to the key managers running the firm, the lack of correlation between earnings and cash flows, significant deviations between firm and peer experience, and unusual behavior in accruals.”

Sources: S. Thurm, “For Some Firms, a Case of ‘Quadrophobia’,” Wall Street Journal (February 14, 2010); and H. Greenberg, “CFOs Concede Earnings Are ‘Managed’,” www.cnbc.com (July 19, 2012). The study referred to is by I. Dichev, J. Graham, C. Harvey, and S. Rajgopal, “Earnings Quality: Evidence from the Field,” Emory University Working Paper (July 2012).

FORMAT OF THE INCOME STATEMENT

Elements of the Income Statement

LEARNING OBJECTIVE ![]()

Understand the content and format of the income statement.

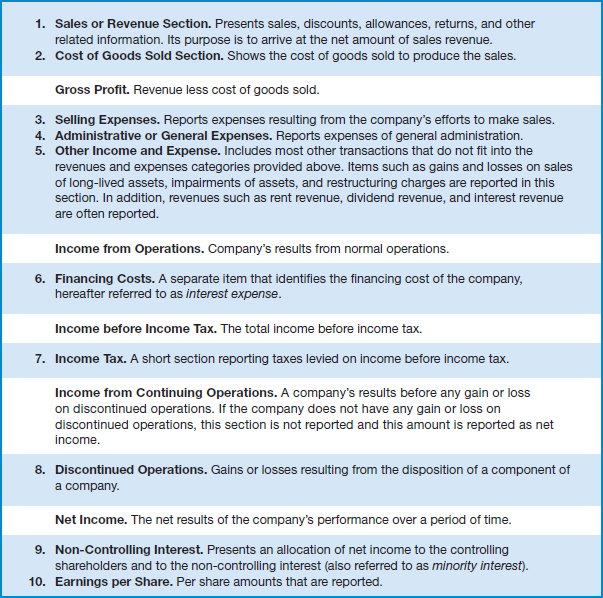

Net income results from revenue, expense, gain, and loss transactions. The income statement summarizes these transactions. This method of income measurement, the transaction approach, focuses on the income-related activities that have occurred during the period.4 The statement can further classify income by customer, product line, or function; by operating and non-operating; and by continuing and discontinued. The two major elements of the income statement are as follows.

ELEMENTS OF FINANCIAL STATEMENTS

INCOME. Increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in equity, other than those relating to contributions from shareholders.

EXPENSES. Decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in equity, other than those relating to distributions to shareholders.[1]

![]() See the Authoritative Literature section (page 162).

See the Authoritative Literature section (page 162).

The definition of income includes both revenues and gains. Revenues arise from the ordinary activities of a company and take many forms, such as sales, fees, interest, dividends, and rents. Gains represent other items that meet the definition of income and may or may not arise in the ordinary activities of a company. Gains include, for example, gains on the sale of long-term assets or unrealized gains on trading securities.

The definition of expenses includes both expenses and losses. Expenses generally arise from the ordinary activities of a company and take many forms, such as cost of goods sold, depreciation, rent, salaries and wages, and taxes. Losses represent other items that meet the definition of expenses and may or may not arise in the ordinary activities of a company. Losses include losses on restructuring charges, losses related to sale of long-term assets, or unrealized losses on trading securities.5

When gains and losses are reported on an income statement, they are generally separately disclosed because knowledge of them is useful for assessing future cash flows. For example, when McDonald's (USA) sells a hamburger, it records the selling price as revenue. However, when McDonald's sells land, it records any excess of the selling price over the book value as a gain. This difference in treatment results because the sale of the hamburger is part of McDonald's regular operations. The sale of land is not.

We cannot overemphasize the importance of reporting these elements. Most decision-makers find the parts of a financial statement to be more useful than the whole. As we indicated earlier, investors and creditors are interested in predicting the amounts, timing, and uncertainty of future income and cash flows. Having income statement elements shown in some detail and in comparison with prior years' data allows decision-makers to better assess future income and cash flows.6

Intermediate Components of the Income Statement

Companies generally present some or all of the following sections and totals within the income statement, as shown in Illustration 4-1 (on page 140).

ILLUSTRATION 4-1

Income Statement Format

Illustration

LEARNING OBJECTIVE ![]()

Prepare an income statement.

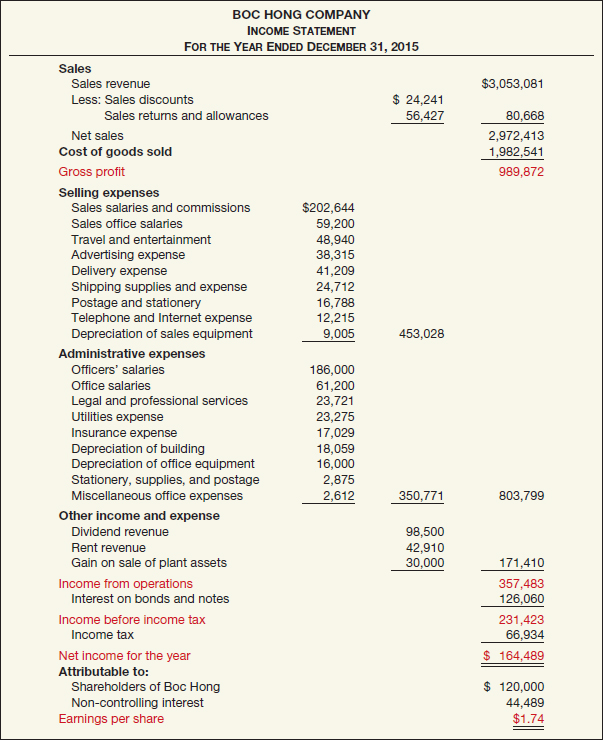

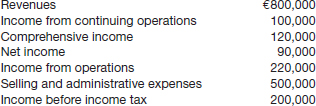

Illustration 4-2 presents an income statement for Boc Hong Company. Boc Hong's income statement includes all of the major items in the list above, except for discontinued operations. In arriving at net income, the statement presents the following subtotals and totals: gross profit, income from operations, income before income tax, and net income.

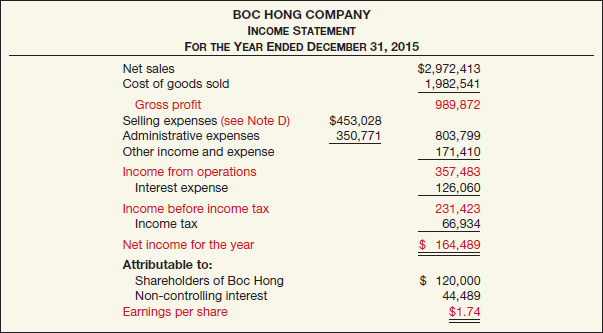

Condensed Income Statements

In some cases, an income statement cannot possibly present all the desired expense detail. To solve this problem, a company includes only the totals of components in the statement of income. It then also prepares supplementary schedules to support the totals. This format may thus reduce the income statement itself to a few lines on a single sheet. For this reason, readers who wish to study all the reported data on operations must give their attention to the supporting schedules.

ILLUSTRATION 4-2

Income Statement

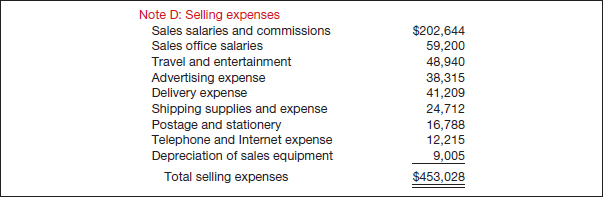

For example, consider the income statement shown in Illustration 4-3 (on page 142) for Boc Hong Company. This statement is a condensed version of the more detailed income statement presented in Illustration 4-2. It is more representative of the type found in practice. Illustration 4-4 (on page 142) shows an example of a supporting schedule, cross-referenced as Note D and detailing the selling expenses.

How much detail should a company include in the income statement? On the one hand, a company wants to present a simple, summarized statement so that readers can readily discover important factors. On the other hand, it wants to disclose the results of all activities and to provide more than just a skeleton report. As a result, the income statement always includes certain basic elements, but companies can present them in various formats.

ILLUSTRATION 4-3

Condensed Income Statement

ILLUSTRATION 4-4

Sample Supporting Schedule

What do the numbers mean? YOU MAY NEED A MAP

Many companies increasingly promote their performance through the reporting of various “pro forma” earnings measures. A recent study of the top 40 New Zealand companies documented an increase in pro forma reporting from just 10 percent of companies in 2004 to 45 percent in 2010. A similar study of French companies showed that 79 percent of the sample companies reported pro forma numbers that are higher than unadjusted (IFRS) numbers, suggesting that managers have significant motives for reporting a profit that would be higher than under IFRS-based numbers and higher than in analysts' forecasts.

A good example is that of Vivendi Universal (FRA), which has been announcing its annual earnings on a pro forma basis for a few years. The corporation then reconciles its pro forma and IFRS earnings in its financial statements. Its pro forma earnings measures, called “adjusted net income, group share,” are systematically higher than earnings computed under IFRS. The most astonishing point is the type of items excluded. The reconciliation statement included in the annual report conspicuously excluded important operational and economic expenses such as “non-recurring expenses,” “gains/losses on disposals,” “financial provisions,” and even “goodwill amortization and income tax.”

One regulator calls such earnings measures EBS—“Everything but Bad Stuff.” Indeed, public companies in the United States are required to reconcile non-U.S. GAAP financial measures to U.S. GAAP, thereby giving investors a roadmap to analyze adjustments companies make to their U.S. GAAP numbers to arrive at pro forma results. This provides investors a more complete picture of company profitability, not the story preferred by management. A similar rule might be in order internationally.

Sources: Gaynor B, “Crisis of Accounting's Double Standards,” The New Zealand Herald (November 27, 2010); and F. Aubert, “The Relative Informativeness of GAAP and Pro Forma Earnings Announcements in France,” Journal of Accounting and Taxation, Vol. 2(1) (June 2010), pp. 1–14. See also SEC Regulation G, “Conditions for Use of Non-GAAP Financial Measures,” Release No. 33–8176 (March 28, 2003).

REPORTING WITHIN THE INCOME STATEMENT

Gross Profit

![]() LEARNING OBJECTIVE

LEARNING OBJECTIVE

Explain how to report items in the income statement.

Boc Hong Company's gross profit is computed by deducting cost of goods sold from net sales. The disclosure of net sales is useful because Boc Hong reports regular sales revenue as a separate item. It discloses unusual or incidental revenues in other income and expense. As a result, analysts can more easily understand and assess trends in revenue from continuing operations.

Similarly, the reporting of gross profit provides a useful number for evaluating performance and predicting future earnings. Statement readers may study the trend in gross profits to understand how competitive pressure affected profit margins.

Income from Operations

Boc Hong Company determines income from operations by deducting selling and administrative expenses as well as other income and expense from gross profit. Income from operations highlights items that affect regular business activities. As such, it is a metric often used by analysts in helping to predict the amount, timing, and uncertainty of future cash flows.

Expense Classification

Companies are required to present an analysis of expenses classified either by their nature (such as cost of materials used, direct labor incurred, delivery expense, advertising expense, employee benefits, depreciation expense, and amortization expense) or their function (such as cost of goods sold, selling expenses, and administrative expenses).

An advantage of the nature-of-expense method is that it is simple to apply because allocations of expense to different functions are not necessary. For manufacturing companies that must allocate costs to the product produced, using a nature-of-expense approach permits companies to report expenses without making arbitrary allocations.

The function-of-expense method, however, is often viewed as more relevant because this method identifies the major cost drivers of the company and therefore helps users assess whether these amounts are appropriate for the revenue generated. As indicated, a disadvantage of this method is that the allocation of costs to the varying functions may be arbitrary and therefore the expense classification becomes misleading.

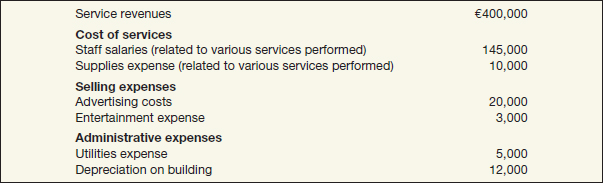

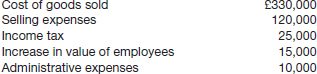

To illustrate these two methods, assume that the accounting firm of Telaris Co. performs audit, tax, and consulting services. It has the following revenues and expenses.

If Telaris Group uses the nature-of-expense approach, its income statement presents each expense item but does not classify the expenses into various subtotals. This approach is shown in Illustration 4-5 (on page 144).

ILLUSTRATION 4-5

Nature-of-Expense Approach

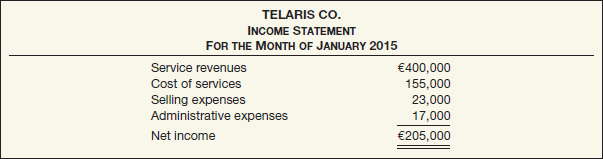

If Telaris uses the function-of-expense approach, its income statement is as follows.

ILLUSTRATION 4-6

Function-of-Expense Approach

The function-of-expense method is generally used in practice although many companies believe both approaches have merit. These companies use the function-of-expense approach on the income statement but provide detail of the expenses (as in the nature-of-expense approach) in the notes to the financial statements. For example, Boc Hong's condensed income statement, shown in Illustrations 4-3 and 4-4, indicates how this information might be reported.7 The IASB-FASB discussion paper on financial statement presentation also recommends the dual approach used in the Boc Hong illustrations. For homework purposes, use the function-of-expense approach shown in the Boc Hong example in Illustration 4.3 (on page 142), unless directed otherwise.

Gains and Losses

What should be included in net income is controversial. For example, should companies report gains and losses, and corrections of revenues and expenses of prior years, as part of retained earnings? Or, should companies first present them in the income statement and then carry them to retained earnings?

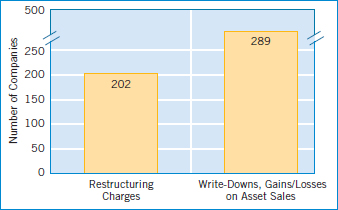

This issue is extremely important because the number and magnitude of these items are substantial. For example, Illustration 4-7 identifies the most common types and number of gains and losses reported in a survey of 500 large companies. Notice that more than 40 percent of the surveyed firms reported restructuring charges, which often contain write-offs and other one-time items. A survey of 200 IFRS adopters indicates that about 27 percent of the surveyed firms reported a discontinued operation charge.8

ILLUSTRATION 4-7

Number of Unusual Items Reported in a Recent Year by 500 Large Companies

As our opening story discusses, we need consistent and comparable income reporting practices to avoid “promotional” information reported by companies. Developing a framework for reporting these gains and losses is important to ensure reliable income information.9 Some users argue that the most useful income measure reflects only regular and recurring revenue and expense elements. Unusual, non-recurring items do not reflect a company's future earning power.

In contrast, others warn that a focus on income that excludes these items potentially misses important information about a company's performance. Any gain or loss experienced by the company, whether directly or indirectly related to operations, contributes to its long-run profitability. As one analyst notes, “write-offs matter.... They speak to the volatility of past earnings.”10

In general, the IASB takes the position that both revenues and expenses and other income and expense should be reported as part of income from operations. For example, it would be inappropriate to exclude items clearly related to operations (such as inventory write-downs and restructuring and relocation expenses) because they occur irregularly or infrequently, or are unusual in amount. Similarly, it would be inappropriate to exclude items on the grounds that they do not involve cash flows, such as depreciation and amortization expenses. However, companies can provide additional line items, headings, and subtotals when such presentation is relevant to an understanding of the entity's financial performance.

IFRS indicates additional items that may need disclosure on the income statement to help users predict the amount, timing, and uncertainty of future cash flows. Examples of these unusual items are as follows.

- Losses on write-downs of inventories to net realizable value or of property, plant, and equipment to recoverable amount, as well as reversals of such write-downs.

- Losses on restructurings of the activities of a company and reversals of any provisions for the costs of restructuring.

- Gains or losses on the disposal of items of property, plant, and, equipment or investments.

- Litigation settlements.

- Other reversals of liabilities.

Most companies therefore report these items as part of operations and disclose them in great detail if material in amount. Some, for example, simply show each item as a separate item on the income statement before income from operations. Others use the caption Other income and expense and then itemize them in this section or in the notes to the financial statements. For homework purposes, itemize gains, losses, revenues, and expenses that are not reported as part of the revenue and expense sections of the income statement in the “Other income and expense” section.

What do the numbers mean? ARE ONE-TIME CHARGES BUGGING YOU?

It is an age-old question: which number—net income or income from operations—should an analyst use in evaluating companies that have unusual items? Some argue that operating income better represents what will happen in the future. Others note that special items are often no longer special. For example, one study noted that in 2001, companies in the Standard & Poor's 500 index wrote off items totaling $165 billion—more than in the prior five years combined.

A more recent study indicates that companies continue to make adjustments for one-time or unusual items. And the trend is increasing, with 36 percent of large companies making adjustments for one-time or unusual items in 2012 compared to 20 percent in 2011.

A study by Multex.com and the Wall Street Journal indicated that analysts should not ignore these charges. Based on data for companies taking unusual charges, the study documented that companies reporting the largest unusual charges had more negative share price performance following the charge, compared to companies with smaller charges. Thus, rather than signaling the end of bad times, these unusual charges indicated poorer future earnings.

In fact, some analysts use these charges to weed out companies that may be headed for a fall. Following the “cockroach theory,” any charge indicating a problem raises the probability of more problems. Thus, investors should be wary of the increasing use of restructuring and other one-time charges, which may bury expenses that signal future performance declines.

Sources: Adapted from J. Weil and S. Liesman, “Stock Gurus Disregard Most Big Write-Offs, but They Often Hold Vital Clues to Outlook,” Wall Street Journal Online (December 31, 2001); and R. Walters, “Exceptional Costs Becoming Business as Usual for Tech Groups,” Financial Times (November 14, 2013).

Income before Income Tax

Boc Hong computes income before income tax by deducting interest expense (often referred to as financing costs) from income from operations. Under IFRS, companies must report their financing costs on the income statement. The reason for this requirement is to differentiate between a company's business activities (how it uses capital to create value) and its financing activities (how it obtains capital).

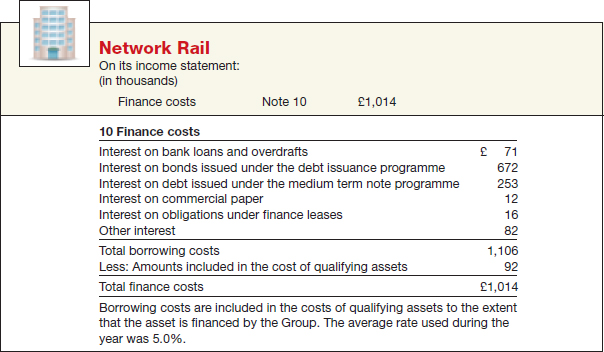

In most cases, the financing costs involve interest expense. In other situations, companies offset against interest expense, items such as interest revenue. Illustration 4-8 indicates how Network Rail (GBR) presents its financing costs involving only interest expense.

ILLUSTRATION 4-8

Presentation of Finance Costs

As indicated, some companies offset interest revenue and interest expense, and identify it as either finance costs or interest expense and interest revenue, net. For homework purposes, consider only interest expense as financing costs. Interest revenue (income) should be reported as part of “Other income and expense.”

Net Income

Boc Hong deducts income tax from income before income tax to arrive at net income. Net income represents the income after all revenues and expenses for the period are considered. It is viewed by many as the most important measure of a company's success or failure for a given period of time.

Income tax is reported on the income statement right before net income because this expense cannot be computed until all revenues and expenses are determined. In practice, an understanding of how the company arrived at the income tax for the period is important. For example, some of the revenue items may have different tax rates associated with them. In other cases, expense items may not be deductible for income tax purposes. Understanding these situations enables users to better predict what the future holds for the company. As a result, there is often extensive disclosure related to how the number for income tax expense is determined. Chapter 19 discusses this subject in detail.

Allocation to Non-Controlling Interest

A company like Siemens (DEU) owns substantial interests in other companies. Siemens generally consolidates the financial results of these companies into its own financial statements. In these cases, Siemens is referred to as the parent, and the other companies are referred to as subsidiaries. Non-controlling interest is then the portion of equity (net assets) interest in a subsidiary not attributable to the parent company.

To illustrate, assume that Boc Hong acquires 70 percent of the outstanding shares of LTM Group. Because Boc Hong owns more than 50 percent of LTM, it consolidates LTM's financial results with its own. Consolidated net income is then allocated to the controlling (Boc Hong) and non-controlling shareholders' percentage of ownership in LTM. In other words, under this arrangement, the ownership of LTM is divided into two classes: (1) the majority interest represented by shareholders who own the controlling interest and (2) the non-controlling interest (sometimes referred to as the minority interest) represented by shareholders who are not part of the controlling group. When Boc Hong prepares a consolidated income statement, IFRS requires that net income be allocated to the controlling and non-controlling interest. This allocation is reported at the bottom of the income statement, after net income. An example of how Boc Hong reports its non-controlling interest is shown in Illustration 4-9.

ILLUSTRATION 4-9

Presentation of Non-Controlling Interest

These amounts are to be presented as allocations of net income or net loss, not as an item of income or expense.

Earnings per Share

LEARNING OBJECTIVE ![]()

Identify where to report earnings per share information.

A company customarily sums up the results of its operations in one important figure: net income. However, the financial world has widely accepted an even more distilled and compact figure as the most significant business indicator—earnings per share (EPS).

The computation of earnings per share is usually straightforward. Earnings per share is net income minus preference dividends (income available to ordinary shareholders), divided by the weighted average of ordinary shares outstanding.11

To illustrate, assume that Lancer, Inc. reports net income of $350,000. It declares and pays preference dividends of $50,000 for the year. The weighted-average number of ordinary shares outstanding during the year is 100,000 shares. Lancer computes earnings per share of $3, as shown in Illustration 4-10.

ILLUSTRATION 4-10

Equation Illustrating Computation of Earnings per Share

Note that EPS measures the number of dollars earned by each ordinary share. It does not represent the dollar amount paid to shareholders in the form of dividends.

Prospectuses, proxy material, and annual reports to shareholders commonly use the “net income per share” or “earnings per share” ratio. The financial press and securities analysts also highlight EPS. Because of its importance, companies must disclose earnings per share on the face of the income statement.

Many corporations have simple capital structures that include only ordinary shares. For these companies, a presentation such as “Earnings per share” is appropriate on the income statement. In many instances, however, companies' earnings per share are subject to dilution (reduction) in the future because existing contingencies permit the issuance of additional shares. [3]12

In summary, the simplicity and availability of EPS figures lead to their widespread use. Because of the importance that the public, even the well-informed public, attaches to earnings per share, companies must make the EPS figure as meaningful as possible.

Discontinued Operations

As Illustration 4-7 (on page 145) shows, one of the most common types of unusual items is discontinued operations. The IASB defines a discontinued operation as a component of an entity that either has been disposed of, or is classified as held-for-sale, and:

- 1. Represents a major line of business or geographical area of operations, or

- 2. Is part of a single, co-coordinated plan to dispose of a major line of business or geographical area of operations, or

- 3. Is a subsidiary acquired exclusively with a view to resell. [4]

To illustrate a component, Unilever plc (GBR) manufactures and sells consumer products. It has several product groups, each with different product lines and brands. For Unilever, a product group is the lowest level at which it can clearly distinguish the operations and cash flows from the rest of the company's operations. Therefore, each product group is a component of the company. If a component were disposed of, Unilever would classify it as a discontinued operation.

Here is another example. Assume that Softso Inc. has experienced losses with certain brands in its beauty-care products group. As a result, Softso decides to sell that part of its business. It will discontinue any continuing involvement in the product group after the sale. In this case, Softso eliminates the operations and the cash flows of the product group from its ongoing operations, and reports it as a discontinued operation.

On the other hand, assume Softso decides to remain in the beauty-care business but will discontinue the brands that experienced losses. Because Softso cannot differentiate the cash flows from the brands from the cash flows of the product group as a whole, it cannot consider the brands a component. Softso does not classify any gain or loss on the sale of the brands as a discontinued operation.

Companies report as discontinued operations (in a separate income statement category) the gain or loss from disposal of a component of a business. In addition, companies report the results of operations of a component that has been or will be disposed of separately from continuing operations. Companies show the effects of discontinued operations net of tax as a separate category, after continuing operations.

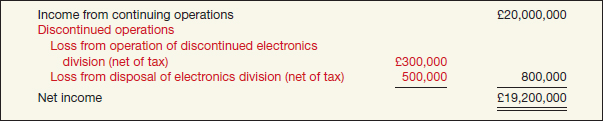

To illustrate, Multiplex Products, Inc., a highly diversified company, decides to discontinue its electronics division. During the current year, the electronics division lost £300,000 (net of tax). Multiplex sold the division at the end of the year at a loss of £500,000 (net of tax). Illustration 4-11 shows the reporting of discontinued operations for Multiplex.

ILLUSTRATION 4-11

Income Statement Presentation of Discontinued Operations

Companies use the phrase “Income from continuing operations” only when gains or losses on discontinued operations occur.13

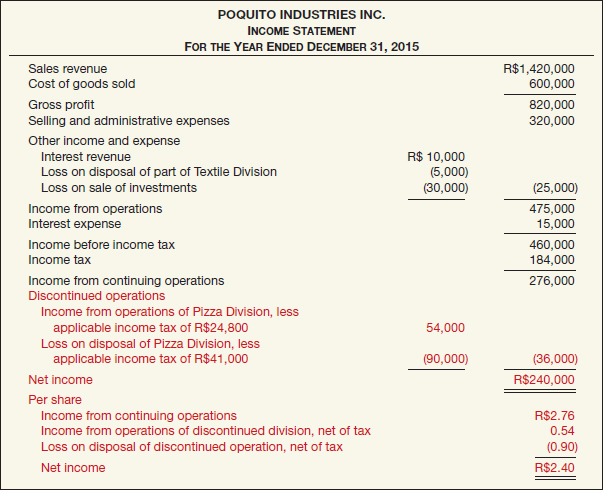

A company that reports a discontinued operation must report per share amounts for the line item either on the face of the income statement or in the notes to the financial statements. [5] To illustrate, consider the income statement for Poquito Industries Inc., shown in Illustration 4-12 (on page 150). Notice the order in which Poquito shows the data, with per share information at the bottom. Assume that the company had 100,000 shares outstanding for the entire year. The Poquito income statement, as Illustration 4-12 shows, is highly condensed. Poquito would need to describe items such as “Other income and expense” and “Discontinued operations” fully and appropriately in the statement or related notes.

ILLUSTRATION 4-12

Income Statement

Intraperiod Tax Allocation

LEARNING OBJECTIVE ![]()

Explain intraperiod tax allocation.

Companies report discontinued operations on the income statement net of tax. The allocation of tax to this item is called intraperiod tax allocation, that is, allocation within a period. It relates the income tax expense (sometimes referred to as the income tax provision) of the fiscal period to the specific items that give rise to the amount of the income tax provision.

Intraperiod tax allocation helps financial statement users better understand the impact of income taxes on the various components of net income. For example, readers of financial statements will understand how much income tax expense relates to “income from continuing operations.” This approach should help users to better predict the amount, timing, and uncertainty of future cash flows. In addition, intraperiod tax allocation discourages statement readers from using pretax measures of performance when evaluating financial results, and thereby recognizes that income tax expense is a real cost.

Companies use intraperiod tax allocation on the income statement for the following items: (1) income from continuing operations and (2) discontinued operations. The general concept is “let the tax follow the income.”

To compute the income tax expense attributable to “Income from continuing operations,” a company would find the income tax expense related to both the revenue and expense transactions as well as other income and expense used in determining this income subtotal. (In this computation, the company does not consider the tax consequences of items excluded from the determination of “Income from continuing operations.”) Companies then associate a separate tax effect (e.g., for discontinued operations). Here, we look in more detail at calculation of intraperiod tax allocation for discontinued gain or discontinued loss.

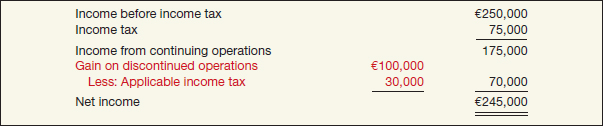

Discontinued Operations (Gain)

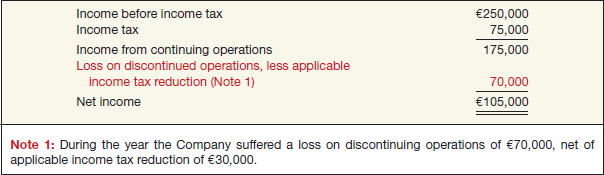

In applying the concept of intraperiod tax allocation, assume that Schindler Co. has income before income tax of €250,000. It has a gain of €100,000 from a discontinued operation. Assuming a 30 percent income tax rate, Schindler presents the following information on the income statement.

ILLUSTRATION 4-13

Intraperiod Tax Allocation, Discontinued Operations Gain

Schindler determines the income tax of €75,000 (€250,000 × 30%) attributable to “Income before income tax” from revenue and expense transactions related to this income. Schindler omits the tax consequences of items excluded from the determination of “Income before income tax.” The company shows a separate tax effect of €30,000 related to the “Gain on discontinued operations.”

Discontinued Operations (Loss)

To illustrate the reporting of a loss from discontinued operations, assume that Schindler Co. has income before income tax of €250,000. It suffers a loss from discontinued operations of €100,000. Assuming a 30 percent tax rate, Schindler presents the income tax on the income statement as shown in Illustration 4-14. In this case, the loss provides a positive tax benefit of €30,000. Schindler, therefore, subtracts it from the €100,000 loss.

ILLUSTRATION 4-14

Intraperiod Tax Allocation, Discontinued Operations Loss

Companies may also report the tax effect of a discontinued item by means of a note disclosure, as illustrated below.

ILLUSTRATION 4-15

Note Disclosure of Intraperiod Tax Allocation

Summary

Illustration 4-16 (on page 152) provides a summary of the primary income items.

ILLUSTRATION 4-16

Summary of Income Items

As indicated, companies report all revenues, gains, expenses, and losses on the income statement and, at the end of the period, close them to Income Summary. They provide useful subtotals on the income statement, such as gross profit, income from operations, income before income tax, and net income. Companies classify discontinued operations of a component of a business as a separate item in the income statement, after “Income from continuing operations.” Companies present other income and expense in a separate section, before income from operations. Providing intermediate income figures helps readers evaluate earnings information in assessing the amounts, timing, and uncertainty of future cash flows.

What do the numbers mean? DIFFERENT INCOME CONCEPTS

As indicated in the opening story, the IASB is working on a project related to presentation of financial statements. In 2008, the IASB (and FASB) issued an exposure draft that presented examples of what these new financial statements might look like. Recently, they conducted field tests on two groups: preparers and users. Preparers were asked to recast their financial statements and then comment on the results. Users examined the recast statements and commented on their usefulness.

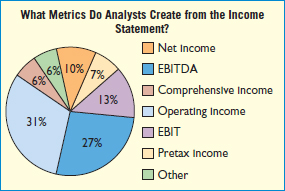

One part of the field test asked analysts to indicate which primary performance metric they use or create from a company's income statement. They were provided with the following options: (a) Net income; (b) Pretax income; (c) Income before interest and taxes (EBIT); (d) Income before interest, taxes, depreciation, and amortization (EBITDA); (e) Operating income; (f) Comprehensive income; and (g) Other. Presented below is a chart that highlights their responses.

As indicated, Operating income (31%) and EBITDA (27%) were identified as the two primary performance metrics that respondents use or create from a company's income statement. A majority of the respondents identified a primary performance metric that uses net income as its foundation (pretax income would be in this group). Clearly, users and preparers look at more than just the bottom line income number, which supports the IFRS requirement to provide subtotals within the income statement.

Source: “FASB-IASB Report on Analyst Field Test Results,” Financial Statement Presentation Informational Board Meeting (September 21, 2009).

OTHER REPORTING ISSUES

![]() LEARNING OBJECTIVE

LEARNING OBJECTIVE

Understand the reporting of accounting changes and errors.

In this section, we discuss reporting issues related to (1) accounting changes and errors, (2) retained earnings statement, (3) comprehensive income, and (4) statement of changes in equity.

Accounting Changes and Errors

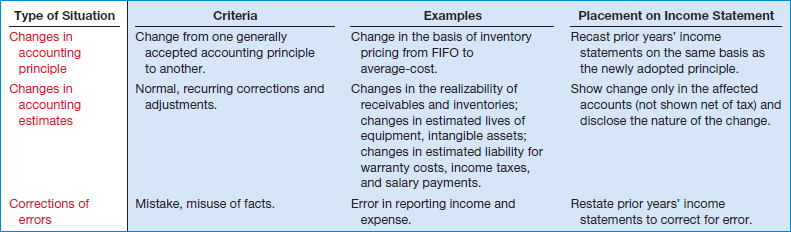

Changes in accounting principle, changes in estimates, and corrections of errors require unique reporting provisions.

Changes in Accounting Principle

Changes in accounting occur frequently in practice because important events or conditions may be in dispute or uncertain at the statement date. One type of accounting change results when a company adopts a different accounting principle. Changes in accounting principle include a change in the method of inventory pricing from FIFO to average-cost, or a change in accounting for construction contracts from the percentage-of-completion to the completed-contract method. [6]14

A company recognizes a change in accounting principle by making a retrospective adjustment to the financial statements. Such an adjustment recasts the prior years' statements on a basis consistent with the newly adopted principle. The company records the cumulative effect of the change for prior periods as an adjustment to beginning retained earnings of the earliest year presented.

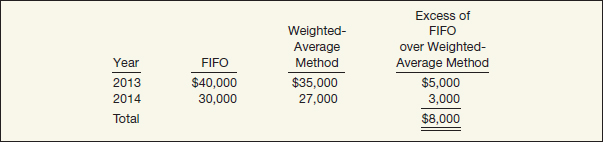

To illustrate, Gaubert Inc. decided in March 2015 to change from FIFO to weighted-average inventory pricing. Gaubert's income before income tax, using the new weighted-average method in 2015, is $30,000. Illustration 4-17 presents the pretax income data for 2013 and 2014 for this example.

ILLUSTRATION 4-17

Calculation of a Change in Accounting Principle

Illustration 4-18 shows the information Gaubert presented in its comparative income statements, based on a 30 percent tax rate.

ILLUSTRATION 4-18

Income Statement Presentation of a Change in Accounting Principle

Thus, under the retrospective approach, the company recasts the prior years' income numbers under the newly adopted method. This approach therefore preserves comparability across years.

Changes in Accounting Estimates

Changes in accounting estimates are inherent in the accounting process. For example, companies estimate useful lives and residual values of depreciable assets, uncollectible receivables, inventory obsolescence, and the number of periods expected to benefit from a particular expenditure. Not infrequently, due to time, circumstances, or new information, even estimates originally made in good faith must be changed. A company accounts for such changes in the period of change if they affect only that period, or in the period of change and future periods if the change affects both.

To illustrate a change in estimate that affects only the period of change, assume that DuPage Materials Corp. consistently estimated its bad debt expense at 1 percent of credit sales. In 2015, however, DuPage determines that it must revise upward the estimate of bad debts for the current year's credit sales to 2 percent, or double the prior years' percentage. The 2 percent rate is necessary to reduce accounts receivable to net realizable value. Using 2 percent results in a bad debt charge of CHF240,000, or double the amount using the 1 percent estimate for prior years. DuPage records the bad debt expense and related allowance at December 31, 2015, as follows.

![]()

DuPage includes the entire change in estimate in 2015 income because the change does not affect future periods. Companies do not handle changes in estimate retrospectively. That is, such changes are not carried back to adjust prior years. (We examine changes in estimate that affect both the current and future periods in greater detail in Chapter 22.) Changes in estimate are not considered errors.

Corrections of Errors

Errors occur as a result of mathematical mistakes, mistakes in the application of accounting principles, or oversight or misuse of facts that existed at the time financial statements were prepared. In recent years, many companies have corrected for errors in their financial statements. The errors involved such items as improper reporting of revenue, accounting for share options, allowances for receivables, inventories, and other provisions.

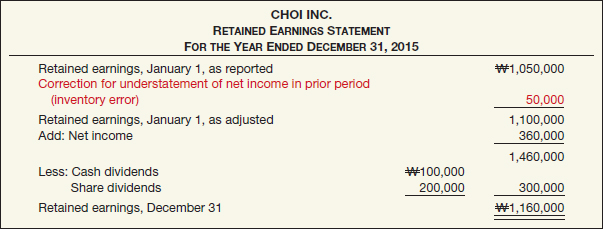

Companies correct errors by making proper entries in the accounts and reporting the corrections in the financial statements. Corrections of errors are treated as prior period adjustments, similar to changes in accounting principles. Companies record a correction of an error in the year in which it is discovered. They report the error in the financial statements as an adjustment to the beginning balance of retained earnings. If a company prepares comparative financial statements, it should restate the prior statements for the effects of the error.

To illustrate, in 2015, Tsang Co. determined that it incorrectly overstated its accounts receivable and sales revenue by NT$100,000 in 2014. In 2015, Tsang makes the following entry to correct for this error (ignore income taxes).

![]()

Retained Earnings is debited because sales revenue, and therefore net income, was overstated in a prior period. Accounts Receivable is credited to reduce this overstated balance to the correct amount.

Summary

The impact of changes in accounting principle and error corrections are debited or credited directly to retained earnings, if related to a prior period. Illustration 4-19 summarizes the basic concepts related to these two items, as well as the accounting and reporting for changes in estimates. Although simplified, the chart provides a useful framework for determining the treatment of special items affecting the income statement.

ILLUSTRATION 4-19

Summary of Accounting Changes and Errors

Retained Earnings Statement

![]() LEARNING OBJECTIVE

LEARNING OBJECTIVE

Prepare a retained earnings statement.

Net income increases retained earnings. A net loss decreases retained earnings. Both cash and share dividends decrease retained earnings. Changes in accounting principle (generally) and prior period adjustments may increase or decrease retained earnings. Companies charge or credit these adjustments (net of tax) to the opening balance of retained earnings.

Companies may show retained earnings information in different ways. For example, some companies prepare a separate retained earnings statement, as Illustration 4-20 shows.

ILLUSTRATION 4-20

Retained Earnings Statement

The reconciliation of the beginning to the ending balance in retained earnings provides information about why net assets increased or decreased during the year. The association of dividend distributions with net income for the period indicates what management is doing with earnings: It may be “plowing back” into the business part or all of the earnings, distributing all current income, or distributing current income plus the accumulated earnings of prior years.

Restrictions of Retained Earnings

Companies often restrict retained earnings to comply with contractual requirements, board of directors' policy, or current necessity. Generally, companies disclose in the notes to the financial statements the amounts of restricted retained earnings. In some cases, companies transfer the amount of retained earnings restricted to an account titled Appropriated Retained Earnings. The retained earnings section may therefore report two separate amounts: (1) retained earnings free (unrestricted) and (2) retained earnings appropriated (restricted). The total of these two amounts equals the total retained earnings.

Comprehensive Income

LEARNING OBJECTIVE ![]()

Explain how to report other comprehensive income.

Companies generally include in income all revenues, expenses, and gains and losses recognized during the period. These items are classified within the income statement so that financial statement readers can better understand the significance of various components of net income. Changes in accounting principle and corrections of errors are excluded from the calculation of net income because their effects relate to prior periods.

In recent years, use of fair values for measuring assets and liabilities has increased. Furthermore, possible reporting of gains and losses related to changes in fair value has placed a strain on income reporting. Because fair values are continually changing, some argue that recognizing these gains and losses in net income is misleading. The IASB agrees and has identified a limited number of transactions that should be recorded directly to equity. One example is unrealized gains and losses on non-trading equity securities.15 These gains and losses are excluded from net income, thereby reducing volatility in net income due to fluctuations in fair value. At the same time, disclosure of the potential gain or loss is provided.

Companies include these items that bypass the income statement in a measure called comprehensive income. Comprehensive income includes all changes in equity during a period except those resulting from investments by owners and distributions to owners. Comprehensive income, therefore, includes the following: all revenues and gains, expenses and losses reported in net income, and all gains and losses that bypass net income but affect equity. These items—non-owner changes in equity that bypass the income statement—are referred to as other comprehensive income.

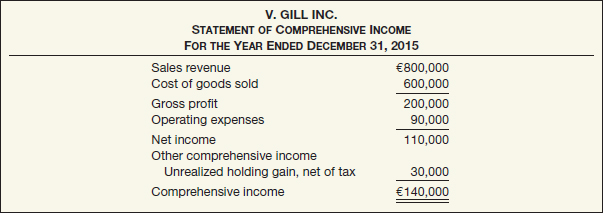

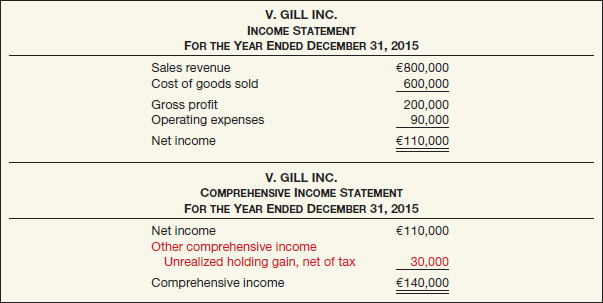

Companies must display the components of other comprehensive income in one of two ways: (1) a single continuous statement (one statement approach) or (2) two separate but consecutive statements of net income and other comprehensive income (two statement approach). The one statement approach is often referred to as the statement of comprehensive income. The two statement approach uses the traditional term income statement for the first statement and the comprehensive income statement for the second statement.

Under either approach, companies display each component of net income and each component of other comprehensive income. In addition, net income and comprehensive income are reported. Companies are not required to report earnings per share information related to comprehensive income.16

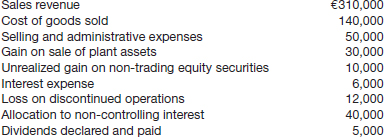

We illustrate these two alternatives in the next two sections. In each case, assume that V. Gill Inc. reports the following information for 2015: sales revenue €800,000, cost of goods sold €600,000, operating expenses €90,000, and an unrealized holding gain on non-trading equity securities of €30,000, net of tax.

One Statement Approach

In this approach, the traditional net income is a subtotal, with total comprehensive income shown as a final total. The combined statement has the advantage of not requiring the creation of a new financial statement. However, burying net income as a subtotal on the statement is a disadvantage. Illustration 4-21 shows the one statement format for V. Gill.

ILLUSTRATION 4-21

One Statement Format: Comprehensive Income

Two Statement Approach

Illustration 4-22 shows the two statement format for V. Gill. Reporting comprehensive income in a separate statement indicates that the gains and losses identified as other comprehensive income have the same status as traditional gains and losses.

ILLUSTRATION 4-22

Two Statement Format: Comprehensive Income

![]() Evolving Issue INCOME REPORTING

Evolving Issue INCOME REPORTING

As indicated in the chapter, information reported in the income statement is important to meeting the objective of financial reporting. However, there is debate over income reporting practices, be it the controversy over pro forma reporting or whether to report comprehensive income in a one statement or a two statement format. In response to these debates and to differences between income reporting under U.S. GAAP and IFRS, standard-setters are working on a project to improve the usefulness of the income statement.

Work to date has resulted in two core principles for financial statement presentation (for the income statement, balance sheet, and the statement of cash flows) based on the objective of financial reporting:

- 1. Disaggregate information so that it is useful in predicting an entity's future cash flows. Disaggregation means separating resources by the activity in which they are used and by their economic characteristics.

- 2. Portray a cohesive financial picture of a company's activities. A cohesive financial picture means that the relationship between items across financial statements is clear and that a company's financial statements complement each other as much as possible.

Cohesiveness will be addressed by using the same classifications across the three primary statements; the two classifications currently under consideration are referred to as business and financing. Thus, this proposal is consistent with some current income reporting practices. However, agreeing on a standard level of disaggregation in the income statement may be difficult, given the current controversies surrounding pro forma reporting, extraordinary items, and comprehensive income reporting.

The statement presentation project is currently inactive on the Boards' joint agenda (http://www.ifrs.org/Current-Projects/IASB-Projects/Financial-Statement-Presentation/Pages/Financial-Statement-Presentation.aspx), but it is expected to restart once the projects on financial instruments, revenue, and leases are completed.

Statement of Changes in Equity

In addition to a statement of comprehensive income, companies are also required to present a statement of changes in equity. Equity is generally comprised of share capital—ordinary, share premium—ordinary, retained earnings, and the accumulated balances in other comprehensive income. The statement reports the change in each equity account and in total equity for the period. The following items are disclosed in this statement.

- 1. Accumulated other comprehensive income for the period.

- 2. Contributions (issuances of shares) and distributions (dividends) to owners.

- 3. Reconciliation of the carrying amount of each component of equity from the beginning to the end of the period.

Companies often prepare the statement of changes in equity in column form. In this format, they use columns for each account and for total equity.

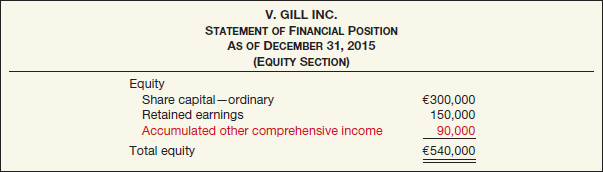

To illustrate, assume the same information for V. Gill as shown in Illustration 4-22 (on page 157). The company had the following equity account balances at the beginning of 2015: Share Capital—Ordinary €300,000, Retained Earnings €50,000, and Accumulated Other Comprehensive Income €60,000, related to unrealized gains on non-trading equity securities. No changes in the Share Capital—Ordinary account occurred during the year. Cash dividends during the period were €10,000. Illustration 4-23 shows a statement of changes in equity for V. Gill.

Total comprehensive income is comprised of net income of €110,000 added to retained earnings and €30,000 related to the unrealized gain. Separate columns are used to report each additional item of other comprehensive income.17 Thus, this statement is useful for understanding how equity changed during the period.

ILLUSTRATION 4-23

Statement of Changes in Equity

Regardless of the display format used, V. Gill reports the accumulated other comprehensive income of €90,000 in the equity section of the statement of financial position as follows.18

ILLUSTRATION 4-24

Presentation of Accumulated Other Comprehensive Income in the Statement of Financial Position

By providing information on the components of comprehensive income, as well as accumulated other comprehensive income, the company communicates information about all changes in net assets.19 With this information, users will better understand the quality of the company's earnings.

INCOME STATEMENT

Standards issued by the FASB (U.S. GAAP) are the primary global alternative to IFRS. As in IFRS, the income statement is a required statement for U.S. GAAP. In addition, the content and presentation of the U.S. GAAP income statement is similar to the one used for IFRS. A number of U.S. GAAP standards have been issued that provide guidance on issues related to income statement presentation.

Relevant Facts

Following are the key similarities and differences between U.S. GAAP and IFRS related to the income statement.

Similarities

- Both U.S. GAAP and IFRS require companies to indicate the amount of net income attributable to non-controlling interest.

- Both U.S. GAAP and IFRS follow the same presentation guidelines for discontinued operations, but IFRS defines a discontinued operation more narrowly. Both standard-setters have indicated a willingness to develop a similar definition to be used in the joint project on financial statement presentation.

- Both U.S. GAAP and IFRS have items that are recognized in equity as part of other comprehensive income but do not affect net income. Both U.S. GAAP and IFRS allow a one statement or two statement approach to preparing the statement of comprehensive income.

Differences

- Presentation of the income statement under U.S. GAAP follows either a single-step or multiple-step format. IFRS does not mention a single-step or multiple-step approach. In addition, under U.S. GAAP, companies must report an item as extraordinary if it is unusual in nature and infrequent in occurrence. Extraordinary-item reporting is prohibited under IFRS.

- The U.S. SEC requires companies to have a functional presentation of expenses. Under IFRS, companies must classify expenses by either nature or function. U.S. GAAP does not have that requirement.

- U.S. GAAP has no minimum information requirements for the income statement. However, the U.S. SEC rules have more rigorous presentation requirements. IFRS identifies certain minimum items that should be presented on the income statement.

- U.S. SEC regulations define many key measures and provide requirements and limitations on companies reporting non-U.S. GAAP information. IFRS does not define key measures like income from operations.

- U.S. GAAP does not permit revaluation accounting. Under IFRS, revaluation of property, plant, and equipment, and intangible assets is permitted and is reported as other comprehensive income. The effect of this difference is that application of IFRS results in more transactions affecting equity but not net income.

About the Numbers

The terminology used in the IFRS literature is sometimes different than what is used in U.S. GAAP. For example, here are some of the differences related to this chapter.

| IFRS | U.S. GAAP |

| Equity or shareholders' equity | Shareholders' equity or stockholders' equity |

| Share capital—ordinary | Common stock |

| Share capital—preference | Preferred stock |

| Ordinary shares | Common shares |

| Preference shares | Preferred shares |

| Share premium—ordinary | Premium on common stock or Paid-in capital in excess of par—common |

| Share premium—preference | Premium on preferred stock or Paid-in capital in excess of par—preferred |

| Reserves | Retained earnings and accumulated other comprehensive income |

| Statement of financial position | Balance sheet or Statement of financial position |

| Profit or loss | Net income or Net loss |

On the Horizon

The IASB and FASB are working on a project that would rework the structure of financial statements. One stage of this project will address the issue of how to classify various items in the income statement. A main goal of this new approach is to provide information that better represents how businesses are run. In addition, this approach draws attention away from just one number—net income.

KEY TERMS

accumulated other comprehensive income, 159

Appropriated Retained Earnings, 156

capital maintenance approach, 138 (n)

changes in accounting estimates, 154

changes in accounting principle, 153

comprehensive income, 156

discontinued operation, 148

earnings management, 137

earnings per share, 148

function-of-expense method, 143

income statement, 136

intraperiod tax allocation, 150

nature-of-expense method, 143

other comprehensive income, 156

Other income and expense, 146

prior period adjustments, 154

quality of earnings, 137

statement of changes in equity, 158

statement of comprehensive income, 136 (n)

transaction approach, 138

SUMMARY OF LEARNING OBJECTIVES

![]() Understand the uses and limitations of an income statement. The income statement provides investors and creditors with information that helps them predict the amounts, timing, and uncertainty of future cash flows. Also, the income statement helps users determine the risk (level of uncertainty) of not achieving particular cash flows. The limitations of an income statement are as follows. (1) The statement does not include many items that contribute to general growth and well-being of a company. (2) Income numbers are often affected by the accounting methods used. (3) Income measures are subject to estimates.

Understand the uses and limitations of an income statement. The income statement provides investors and creditors with information that helps them predict the amounts, timing, and uncertainty of future cash flows. Also, the income statement helps users determine the risk (level of uncertainty) of not achieving particular cash flows. The limitations of an income statement are as follows. (1) The statement does not include many items that contribute to general growth and well-being of a company. (2) Income numbers are often affected by the accounting methods used. (3) Income measures are subject to estimates.

![]() Understand the content and format of the income statement. Net income results from revenue, expense, gain, and loss transactions. This method of income measurement, the transaction approach, focuses on the income-related activities that have occurred during a given period. Instead of presenting only a net change in net assets, it discloses the components of the change.

Understand the content and format of the income statement. Net income results from revenue, expense, gain, and loss transactions. This method of income measurement, the transaction approach, focuses on the income-related activities that have occurred during a given period. Instead of presenting only a net change in net assets, it discloses the components of the change.

The following sections are generally shown on an income statement: sales or revenue, cost of goods sold, selling expense, administrative or general expense, financing costs, and income tax. If present, a company also reports discontinued operations (net of tax). Earnings per share is reported, and an allocation of net income or loss to the non-controlling interest is also presented, where applicable.

![]() Prepare an income statement. Companies determine net income by deducting expenses from revenues but also classify various revenues and expenses in order to report useful subtotals within the income statement. These subtotals are gross profit, income from operations, income before income tax, and a final total, net income.

Prepare an income statement. Companies determine net income by deducting expenses from revenues but also classify various revenues and expenses in order to report useful subtotals within the income statement. These subtotals are gross profit, income from operations, income before income tax, and a final total, net income.

![]() Explain how to report items in the income statement. Companies generally provide some detail on revenues and expenses on the face of the income statement but may prepare a condensed income statement with details on various components presented in the notes to the financial statements. Companies are required to classify expense either by nature or by function. Unusual and non-recurring items should be reported in income from operations, but financing costs are reported separate from operating revenues and expenses. Companies report the effects of discontinued operations of a component of a business as a separate item, after income from continuing operations.

Explain how to report items in the income statement. Companies generally provide some detail on revenues and expenses on the face of the income statement but may prepare a condensed income statement with details on various components presented in the notes to the financial statements. Companies are required to classify expense either by nature or by function. Unusual and non-recurring items should be reported in income from operations, but financing costs are reported separate from operating revenues and expenses. Companies report the effects of discontinued operations of a component of a business as a separate item, after income from continuing operations.

![]() Identify where to report earnings per share information. Companies must disclose earnings per share on the face of the income statement. A company that reports a discontinued operation must report per share amounts for these line items either on the face of the income statement or in the notes to the financial statements.

Identify where to report earnings per share information. Companies must disclose earnings per share on the face of the income statement. A company that reports a discontinued operation must report per share amounts for these line items either on the face of the income statement or in the notes to the financial statements.

![]() Explain intraperiod tax allocation. Companies should relate the tax expense for the year to specific items on the income statement to provide a more informative disclosure to statement users. This procedure, intraperiod tax allocation, relates the income tax expense for the fiscal period to the following items that affect the amount of the tax provisions for (1) income from continuing operations and (2) discontinued operations.

Explain intraperiod tax allocation. Companies should relate the tax expense for the year to specific items on the income statement to provide a more informative disclosure to statement users. This procedure, intraperiod tax allocation, relates the income tax expense for the fiscal period to the following items that affect the amount of the tax provisions for (1) income from continuing operations and (2) discontinued operations.

![]() Understand the reporting of accounting changes and errors. Changes in accounting principle and corrections of errors are adjusted through retained earnings. Changes in accounting estimates are a normal part of the accounting process. The effects of these changes are handled prospectively, with the effects recorded in income in the period of change and in future periods without adjustment to retained earnings.

Understand the reporting of accounting changes and errors. Changes in accounting principle and corrections of errors are adjusted through retained earnings. Changes in accounting estimates are a normal part of the accounting process. The effects of these changes are handled prospectively, with the effects recorded in income in the period of change and in future periods without adjustment to retained earnings.

![]() Prepare a retained earnings statement. The retained earnings statement should disclose net income (loss), dividends, adjustments due to changes in accounting principles, error corrections, and restrictions of retained earnings.

Prepare a retained earnings statement. The retained earnings statement should disclose net income (loss), dividends, adjustments due to changes in accounting principles, error corrections, and restrictions of retained earnings.

![]() Explain how to report other comprehensive income. Companies report the components of other comprehensive income in one of two ways: (1) a combined statement of comprehensive income (one statement format) or (2) in a second statement (two statement format).

Explain how to report other comprehensive income. Companies report the components of other comprehensive income in one of two ways: (1) a combined statement of comprehensive income (one statement format) or (2) in a second statement (two statement format).

Authoritative Literature References

[1] The Conceptual Framework for Financial Reporting, “Chapter 4: The Framework (1989): The Remaining Text” (London, U.K.: IASB, 2010), par. 4.25.

[2] International Accounting Standard 1, Presentation of Financial Statements (London, U.K.: IASB, 2007), par. 82.

[3] International Accounting Standard 33, Earnings per Share (London, U.K.: IASB, 2003).

[4] International Financial Reporting Standard 5, Non-current Assets Held for Sale and Discontinued Operations (London, U.K.: IASB, 2004).

[5] International Accounting Standard 33, Earnings per Share (London, U.K.: IASB, 2003).

[6] International Accounting Standard 8, Accounting Policies, Changes in Accounting Estimates and Errors (London, U.K.: IASB, 2003).

[7] International Accounting Standard 1, Presentation of Financial Statements (London, U.K.: International Accounting Standards Committee Foundation, 2007), paras. 90–91.

[8] International Accounting Standard 1, Presentation of Financial Statements (London, U.K.: International Accounting Standards Committee Foundation, 2007), paras. 81–82.

![]()

- What kinds of questions about future cash flows do investors and creditors attempt to answer with information in the income statement?

- How can information based on past transactions be used to predict future cash flows?

- Identify at least two situations in which important changes in value are not reported in the income statement.

- Identify at least two situations in which application of different accounting methods or accounting estimates results in difficulties in comparing companies.

- Explain the transaction approach to measuring income. Why is the transaction approach to income measurement preferable to other ways of measuring income?

- What is earnings management?

- How can earnings management affect the quality of earnings?

- Why should caution be exercised in the use of the net income figure derived in an income statement? What are the objectives of IFRS in their application to the income statement?

- A Wall Street Journal article noted that MicroStrategy (USA) reported higher income than its competitors by using a more aggressive policy for recognizing revenue on future upgrades to its products. Some contend that MicroStrategy's quality of earnings is low. What does the term “quality of earnings” mean?

- What is the major distinction between income and expenses under IFRS?

- Do the elements of financial statements, income and expense, include gains and losses? Explain.

- What are the sections of the income statement that comprise (1) gross profit and (2) income from operations?

- Ahold (NLD), in its consolidated income statement, reported “settlement of securities class action” €803 million loss. In what section of the income statement is this amount reported?

- Explain where the following items are reported on the income statement: (1) interest expense and (2) income tax.

- Explain the difference between the “nature-of-expense” and “function-of-expense” classifications.

- Discuss the appropriate treatment in the income statement for the following items:

- (a) Loss on discontinued operations.

- (b) Non-controlling interest allocation.

- (c) Earnings per share.

- (d) Gain on sale of equipment.

- Discuss the appropriate treatment in the financial statements of each of the following.

- (a) Write-down of plant assets due to impairment.

- (b) A delivery expense on goods sold.

- (c) Additional depreciation on factory machinery because of an error in computing depreciation for the previous year.

- (d) Rent received from subletting a portion of the office space.

- (e) A patent infringement suit, brought 2 years ago against the company by another company, was settled this year by a cash payment of NT$725,000.

- (f) A reduction in the Allowance for Doubtful Accounts balance, because the account appears to be considerably in excess of the probable loss from uncollectible receivables.

- Indicate where the following items would ordinarily appear on the financial statements of Boleyn, Inc. for the year 2015.

- (a) The service life of certain equipment was changed from 8 to 5 years. If a 5-year life had been used previously, additional depreciation of £425,000 would have been charged.

- (b) In 2015, a flood destroyed a warehouse that had a book value of £1,600,000.

- (c) In 2015, the company wrote off £1,000,000 of inventory that was considered obsolete.

- (d) Interest expense for the year was £45,000.