Chapter 5

Reporting Financial Condition

In This Chapter

![]() Reporting financial condition in the balance sheet

Reporting financial condition in the balance sheet

![]() Reading the balance sheet

Reading the balance sheet

![]() Categorizing business transactions

Categorizing business transactions

![]() Connecting revenue and expenses with their assets and liabilities

Connecting revenue and expenses with their assets and liabilities

![]() Examining where businesses go for capital

Examining where businesses go for capital

![]() Understanding balance sheet values

Understanding balance sheet values

This chapter explores one of the three primary financial statements reported by businesses — the balance sheet, which is also called the statement of financial condition and the statement of financial position. This financial statement is a summary at a point in time of the assets of a business on the one hand, and the liabilities and owners’ equity sources of the business on the other hand. It’s a two-sided financial statement, which is condensed in the accounting equation:

Assets = Liabilities + Owners’ equity

The balance sheet may seem to stand alone — like an island to itself — because it’s presented on a separate page in a financial report. But keep in mind that the assets and liabilities reported in a balance sheet are the results of the activities, or transactions, of the business. Transactions are economic exchanges between the business and the parties it deals with: customers, employees, vendors, government agencies, and sources of capital. Transactions are the stepping stones from the start-of-the year to the end-of-the-year financial condition.

In contrast to the income statement, which I explain in Chapter 4, the balance sheet does not have a natural bottom line, or one key figure that is the focus of attention. The balance sheet reports various assets, liabilities, and sources of owners’ equity. Cash is the most important asset but other assets are important as well. Short-term liabilities are compared against cash and assets that can be converted into cash quickly. The balance sheet, as I explain in this chapter has to be read as a whole — you can’t focus only on one or two items in this financial summary of the business.

Presenting the Balance Sheet

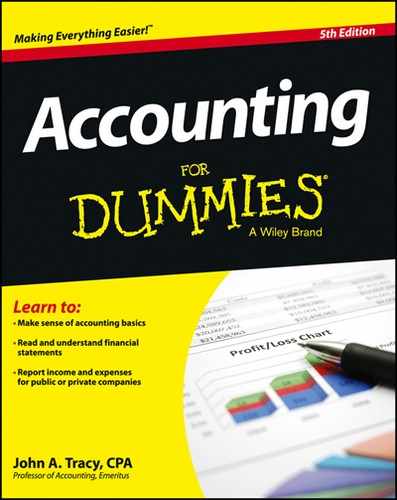

Figure 5-1 presents a two-year, comparative balance sheet for the product business example that I introduce in Chapter 4. The balance sheet is at the close of business, December 31, 2012 and 2013. In most cases financial statements are not completed and released until a few weeks after the balance sheet date. Therefore, by the time you read this financial statement it’s already somewhat out of date, because the business has continued to engage in transactions since December 31, 2013. When significant changes have occurred in the interim between the closing date of the balance sheet and the date of releasing its financial report, a business should disclose these subsequent developments in the footnotes to the financial statements.

The balance sheet in Figure 5-1 is reported in the vertical, or portrait, layout with assets on top and liabilities and owners’ equity on the bottom. Alternatively, a balance sheet may be presented in the horizontal or landscape mode with liabilities and owners’ equity on the right side and assets on the left.

If a business does not release its annual financial report within a few weeks after the close of its fiscal year, you should be alarmed. There are reasons for such a delay, and the reasons are all bad. One reason might be that the business’s accounting system is not functioning well and the controller (chief accounting officer) has to do a lot of work at year-end to get the accounts up to date and accurate for preparing its financial statements. Another reason is that the business is facing serious problems and can’t decide on how to account for the problems. Perhaps a business may be delaying the reporting of bad news. Or the business may have a serious dispute with its independent CPA auditor that has not been resolved.

If a business does not release its annual financial report within a few weeks after the close of its fiscal year, you should be alarmed. There are reasons for such a delay, and the reasons are all bad. One reason might be that the business’s accounting system is not functioning well and the controller (chief accounting officer) has to do a lot of work at year-end to get the accounts up to date and accurate for preparing its financial statements. Another reason is that the business is facing serious problems and can’t decide on how to account for the problems. Perhaps a business may be delaying the reporting of bad news. Or the business may have a serious dispute with its independent CPA auditor that has not been resolved.

The balance sheet presented in Figure 5-1 includes a column for changes in the assets, liabilities, and owners’ equity over the year (from year end 2012 through year end 2013). Including these changes is not required by financial reporting standards, and in fact most businesses do not include the changes. It certainly is acceptable to report balance sheet changes; but because it’s not mandated most companies don’t. I include the changes for ease of reference in this chapter. Transactions generate changes in assets, liabilities, and owners’ equity, which I summarize later in the chapter (see the section “Understanding That Transactions Drive the Balance Sheet”).

The balance sheet presented in Figure 5-1 includes a column for changes in the assets, liabilities, and owners’ equity over the year (from year end 2012 through year end 2013). Including these changes is not required by financial reporting standards, and in fact most businesses do not include the changes. It certainly is acceptable to report balance sheet changes; but because it’s not mandated most companies don’t. I include the changes for ease of reference in this chapter. Transactions generate changes in assets, liabilities, and owners’ equity, which I summarize later in the chapter (see the section “Understanding That Transactions Drive the Balance Sheet”).

Figure 5-1: Typical comparative balance sheet for a product business at the end of its two most recent years (in vertical, or portrait format).

Doing a preliminary read of the balance sheet

Now suppose you own the business whose balance sheet is shown in Figure 5-1. (More likely you would not own 100 percent of the ownership shares of the business; you would own the majority of shares, which gives you working control of the business.) You’ve already digested your most recent annual income statement (refer to Figure 4-1), which reports that you earned $1,690,000 net income on annual sales of $26,000,000. What more do you need to know? Well, you need to check your financial condition, which is reported in the balance sheet.

Is your financial condition viable and sustainable to continue your profit making endeavor? The balance sheet helps answer this critical question. Perhaps you are on the edge of going bankrupt even though you are making a profit. Your balance sheet definitely is where to look for telltale information about possible financial troubles.

In reading through a balance sheet such as the one shown in Figure 5-1, you may notice that it doesn’t have a punch line like the income statement does. The income statement’s punch line is the net income line, which is rarely humorous to the business itself but can cause some snickers among analysts. You can’t look at just one item on the balance sheet, murmur an appreciative “ah-ha,” and rush home to watch the game. You have to read the whole thing (sigh) and make comparisons among the items. Chapters 13 and 16 offer more information on interpreting financial statements.

On first glance you might be somewhat alarmed that your cash balance decreased $110,000 during the year (refer to Figure 5-1). Didn’t you make a tidy profit? Why would your cash balance go down? Well, think about it. Many other transactions affect your cash balance. For example, did you invest in new long-term operating assets (called property, plant and equipment in the balance sheet)? Yes you did, as a matter of fact: These fixed assets increased $1,275,000 during the year (again, see Figure 5-1).

Overall your total assets increased $1,640,000 (see Figure 5-1 again). All assets except cash increased during the year. One big reason is the $940,000 increase in your retained earnings owners’ equity. I explain in Chapter 4 that earning profit increases retained earnings. Profit was $1,690,000 for the year but retained earnings increased only $940,000. Therefore, part of profit was distributed to the owners, which decreases retained earnings. I discuss these things and other balance sheet interpretations as we move through the chapter. For now, the preliminary read of the balance sheet does not indicate any serious, earth-shaking financial problems facing your business.

The balance sheet of a service business looks pretty much the same as a product business (see Figure 5-1) — except a service business does not report an inventory of products held for sale. If it sells on credit, a service business has an accounts receivable asset, just like a product company that sells on credit. The size of its total assets relative to annual sales revenue for a service business varies greatly from industry to industry, depending on whether the service industry is capital intensive or not. Some service businesses, such as airlines, for-profit hospitals, and hotel chains, for example, need to make heavy investments in long-term operating assets. Other service businesses do not.

The balance sheet of a service business looks pretty much the same as a product business (see Figure 5-1) — except a service business does not report an inventory of products held for sale. If it sells on credit, a service business has an accounts receivable asset, just like a product company that sells on credit. The size of its total assets relative to annual sales revenue for a service business varies greatly from industry to industry, depending on whether the service industry is capital intensive or not. Some service businesses, such as airlines, for-profit hospitals, and hotel chains, for example, need to make heavy investments in long-term operating assets. Other service businesses do not.

The balance sheet is unlike the income and cash flow statements, which report flows over a period of time (such as sales revenue that is the cumulative amount of all sales during the period). The balance sheet presents the balances (amounts) of a company’s assets, liabilities, and owners’ equity at an instant in time. Notice the two quite different meanings of the term balance. As used in balance sheet, the term refers to the equality of the two opposing sides of a business — total assets on the one side and total liabilities and owners’ equity on the other side, like a scale with equal weights on both sides. In contrast, the balance of an account (asset, liability, owners’ equity, revenue, and expense) refers to the amount in the account after recording increases and decreases in the account — the net amount after all additions and subtractions have been entered. Usually, the meaning of the term is clear in context.

An accountant can prepare a balance sheet at any time that a manager wants to know how things stand financially. Some businesses — particularly financial institutions such as banks, mutual funds, and securities brokers — need balance sheets at the end of each day, in order to track their day-to-day financial situation. For most businesses, however, balance sheets are prepared only at the end of each month, quarter, and year. A balance sheet is always prepared at the close of business on the last day of the profit period. In other words, the balance sheet should be in sync with the income statement.

Kicking balance sheets out into the real world

The statement of financial condition, or balance sheet, shown earlier in Figure 5-1 is about as lean and mean as you’ll ever read. In the real world many businesses are fat and complex. Also, I should make clear that Figure 5-1 shows the content and format for an external balance sheet, which means a balance sheet that is included in a financial report released outside a business to its owners and creditors. Balance sheets that stay within a business can be quite different.

Internal balance sheets

For internal reporting of financial condition to managers, balance sheets include much more detail, either in the body of the financial statement itself or, more likely, in supporting schedules. For example, just one cash account is shown in Figure 5-1, but the chief financial officer of a business needs to know the balances on deposit in each of the business’s checking accounts.

As another example, the balance sheet shown in Figure 5-1 includes just one total amount for accounts receivable, but managers need details on which customers owe money and whether any major amounts are past due. Greater detail allows for better control, analysis, and decision-making. Internal balance sheets and their supporting schedules should provide all the detail that managers need to make good business decisions. See Chapter 14 for more detail on how business managers use financial reports.

External balance sheets

Balance sheets presented in external financial reports (which go out to investors and lenders) do not include a whole lot more detail than the balance sheet shown in Figure 5-1. However, external balance sheets must classify (or group together) short-term assets and liabilities. These are called current assets and current liabilities, as you see in Figure 5-1. For this reason, external balance sheets are referred to as classified balance sheets.

Let me make clear that the CIA does not vet balance sheets to keep secrets from being disclosed that would harm national security. The term classified, when applied to a balance sheet, does not mean restricted or top secret; rather, the term means that assets and liabilities are sorted into basic classes, or groups, for external reporting. Classifying certain assets and liabilities into current categories is done mainly to help readers of a balance sheet more easily compare current assets with current liabilities for the purpose of judging the short-term solvency of a business.

Judging Liquidity and Solvency

Solvency refers to the ability of a business to pay its liabilities on time. Delays in paying liabilities on time can cause very serious problems for a business. In extreme cases, a business can be thrown into involuntary bankruptcy. Even the threat of bankruptcy can cause serious disruptions in the normal operations of a business, and profit performance is bound to suffer. The liquidity of a business is not a well-defined term; it can take on different meanings. However, generally it refers to the ability of a business to keep its cash balance and its cash flows at adequate levels so that operations are not disrupted by cash shortfalls. For more on this important topic check out the book that my son, Tage, and I coauthored, Cash Flow For Dummies (Wiley, 2012).

If current liabilities become too high relative to current assets — which constitute the first line of defense for paying current liabilities — managers should move quickly to resolve the problem. A perceived shortage of current assets relative to current liabilities could ring alarm bells in the minds of the company’s creditors and owners.

Therefore, notice the following points in Figure 5-1 (dollar amounts refer to year-end 2013):

![]() The first four asset accounts (cash, accounts receivable, inventory, and prepaid expenses) are added to give the $8,815,000 subtotal for current assets.

The first four asset accounts (cash, accounts receivable, inventory, and prepaid expenses) are added to give the $8,815,000 subtotal for current assets.

![]() The first four liability accounts (accounts payable, accrued expenses payable, income tax payable, and short-term notes payable) are added to give the $4.03 million subtotal for current liabilities.

The first four liability accounts (accounts payable, accrued expenses payable, income tax payable, and short-term notes payable) are added to give the $4.03 million subtotal for current liabilities.

![]() The total interest-bearing debt of the business is separated between $2.25 million in short-term notes payable (those due in one year or sooner) and $4 million in long-term notes payable (those due after one year).

The total interest-bearing debt of the business is separated between $2.25 million in short-term notes payable (those due in one year or sooner) and $4 million in long-term notes payable (those due after one year).

The following sections offer more detail about current assets and liabilities.

Current assets and liabilities

Short-term, or current, assets include:

![]() Cash

Cash

![]() Marketable securities that can be immediately converted into cash

Marketable securities that can be immediately converted into cash

![]() Assets converted into cash within one operating cycle, the main components being accounts receivable and inventory

Assets converted into cash within one operating cycle, the main components being accounts receivable and inventory

The operating cycle refers to the repetitive process of putting cash into inventory, holding products in inventory until they are sold, selling products on credit (which generates accounts receivable), and collecting the receivables in cash. In other words, the operating cycle is the “from cash — through inventory and accounts receivable — back to cash” sequence. The operating cycles of businesses vary from a few weeks to several months, depending on how long inventory is held before being sold and how long it takes to collect cash from sales made on credit.

Short-term, or current, liabilities include non-interest-bearing liabilities that arise from the operating (sales and expense) activities of the business. A typical business keeps many accounts for these liabilities — a separate account for each vendor, for instance. In an external balance sheet you usually find only three or four operating liabilities, and they are not labeled as non-interest-bearing. It is assumed that the reader knows that these operating liabilities don’t bear interest (unless the liability is seriously overdue and the creditor has started charging interest because of the delay in paying the liability).

The balance sheet example shown in Figure 5-1 discloses three operating liabilities: accounts payable, accrued expenses payable, and income tax payable. Be warned that the terminology for these short-term operating liabilities varies from business to business.

In addition to operating liabilities, interest-bearing notes payable that have maturity dates one year or less from the balance sheet date are included in the current liabilities section. The current liabilities section may also include certain other liabilities that must be paid in the short run (which are too varied and technical to discuss here).

Current and quick ratios

The sources of cash for paying current liabilities are the company’s current assets. That is, current assets are the first source of money to pay current liabilities when these liabilities come due. Remember that current assets consist of cash and assets that will be converted into cash in the short run. To size up current assets against total current liabilities, the current ratio is calculated. Using information from the company’s balance sheet (refer to Figure 5-1), you compute its year-end 2013 current ratio as follows:

$8,815,000 current assets ÷ $4,030,000 current liabilities = 2.2 current ratio

Generally, businesses do not provide their current ratio on the face of their balance sheets or in the footnotes to their financial statements — they leave it to the reader to calculate this number. On the other hand, many businesses present a financial highlights section in their financial report, which often includes the current ratio.

The quick ratio is more restrictive. Only cash and assets that can be immediately converted into cash are included, which excludes accounts receivable, inventory, and prepaid expenses. The business in our example does not have any short-term marketable investments that could be sold on a moment’s notice. So, only cash is included for the ratio. You compute the quick ratio as follows (refer to Figure 5-1):

$2,165,000 quick assets ÷ $4,030,000 current liabilities = .54 quick ratio

Folklore has it that a company’s current ratio should be at least 2.0 and its quick ratio 1.0. However, business managers know that acceptable ratios depend a great deal on general practices in the industry for short-term borrowing. Some businesses do well with current ratios less than 2.0 and quick ratios less than 1.0, so take these benchmarks with a grain of salt. Lower ratios do not necessarily mean that the business won’t be able to pay its short-term (current) liabilities on time. Chapters 13 and 16 explain solvency in more detail.

Understanding That Transactions Drive the Balance Sheet

A balance sheet is a snapshot of the financial condition of a business at an instant in time — the most important moment in time being at the end of the last day of the income statement period. If you read Chapter 4, you noticed that I continue using the same example in this chapter. The fiscal, or accounting, year of the business ends on December 31. So its balance sheet is prepared at the close of business at midnight December 31. (A company should end its fiscal year at the close of its natural business year or at the close of a calendar quarter — September 30, for example.) This freeze-frame nature of a balance sheet may make it appear that a balance sheet is static. Nothing is further from the truth. A business does not shut down to prepare its balance sheet. The financial condition of a business is in constant motion because the activities of the business go on nonstop.

Transactions change the makeup of a company’s balance sheet — that is, its assets, liabilities, and owners’ equity. The transactions of a business fall into three basic types:

![]() Operating activities, which also can be called profit-making activities: This category refers to making sales and incurring expenses, and also includes accompanying transactions that lead or follow the recording of sales and expenses. For example, a business records sales revenue when sales are made on credit, and then, later, records cash collections from customers. The transaction of collecting cash is the indispensable follow-up to making the sale on credit. For another example, a business purchases products that are placed in its inventory (its stock of products awaiting sale), at which time it records an entry for the purchase. The expense (the cost of goods sold) is not recorded until the products are actually sold to customers. Keep in mind that the term operating activities includes the associated transactions that precede or are subsequent to the recording of sales and expense transactions.

Operating activities, which also can be called profit-making activities: This category refers to making sales and incurring expenses, and also includes accompanying transactions that lead or follow the recording of sales and expenses. For example, a business records sales revenue when sales are made on credit, and then, later, records cash collections from customers. The transaction of collecting cash is the indispensable follow-up to making the sale on credit. For another example, a business purchases products that are placed in its inventory (its stock of products awaiting sale), at which time it records an entry for the purchase. The expense (the cost of goods sold) is not recorded until the products are actually sold to customers. Keep in mind that the term operating activities includes the associated transactions that precede or are subsequent to the recording of sales and expense transactions.

![]() Investing activities: This term refers to making investments in assets and (eventually) disposing of the assets when the business no longer needs them. The primary examples of investing activities for businesses that sell products and services are capital expenditures, which are the amounts spent to modernize, expand, and replace the long-term operating assets of a business. A business may also invest in financial assets, such as bonds and stocks or other types of debt and equity instruments. Purchases and sales of financial assets are also included in this category of transactions.

Investing activities: This term refers to making investments in assets and (eventually) disposing of the assets when the business no longer needs them. The primary examples of investing activities for businesses that sell products and services are capital expenditures, which are the amounts spent to modernize, expand, and replace the long-term operating assets of a business. A business may also invest in financial assets, such as bonds and stocks or other types of debt and equity instruments. Purchases and sales of financial assets are also included in this category of transactions.

![]() Financing activities: These activities include securing money from debt and equity sources of capital, returning capital to these sources, and making distributions from profit to owners. Note that distributing profit to owners is treated as a financing transaction. For instance when a business corporation pays cash dividends to its stockholders the distribution is treated as a financing transaction. The decision whether or not to distribute some of its profit depends on whether the business needs more capital from its owners, to grow the business or to strengthen its solvency. Retaining part or all of profit for the year is one way of increasing the owner’s equity in the business. I discuss this topic later in the chapter (see “Financing a Business: Sources of Cash and Capital” later in the chapter).

Financing activities: These activities include securing money from debt and equity sources of capital, returning capital to these sources, and making distributions from profit to owners. Note that distributing profit to owners is treated as a financing transaction. For instance when a business corporation pays cash dividends to its stockholders the distribution is treated as a financing transaction. The decision whether or not to distribute some of its profit depends on whether the business needs more capital from its owners, to grow the business or to strengthen its solvency. Retaining part or all of profit for the year is one way of increasing the owner’s equity in the business. I discuss this topic later in the chapter (see “Financing a Business: Sources of Cash and Capital” later in the chapter).

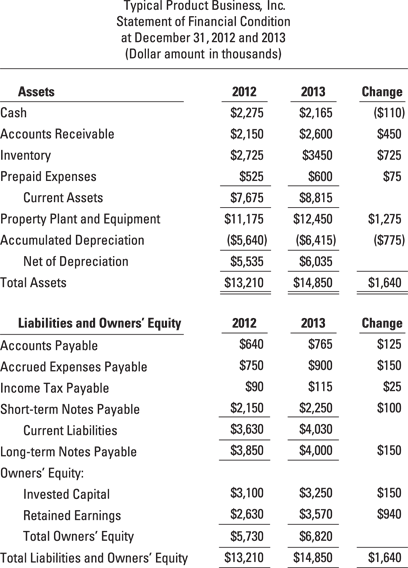

Figure 5-2 presents a summary of changes in assets, liabilities, and owners’ equity during the year for the business example I introduce in Chapter 4. Notice the middle three columns in Figure 5-2, for each of the three basic types of transactions of a business. One column is for changes caused by its revenue and expenses and their connected transactions during the year, which collectively are called operating activities (although I prefer to call them profit-making activities). The second column is for changes caused by its investing activities during the year. The third column is for the changes caused by its financing activities.

Note: Figure 5-2 does not include subtotals for current assets and liabilities. (The formal balance sheet for this business is presented in Figure 5-1). Businesses do not report a summary of changes in their assets, liabilities, and owners’ equity such as Figure 5-2. (Personally I think that such a summary would be helpful to users of financial reports.) The purpose of Figure 5-2 is to demonstrate how the three major types of transactions during the year change the assets, liabilities, and owner’s equity accounts of the business during the year.

The 2013 income statement of the business is shown in Figure 4-1 in Chapter 4. You may want to flip back to this financial statement. On sales revenue of $26 million, the business earned $1.69 million bottom-line profit (net income) for the year. The sales and expense transactions of the business during the year plus the associated transactions connected with sales and expenses cause the changes shown in the operating activities column in Figure 5-2. You can see in Figure 5-2 that the $1.69 million net income has increased the business’s owners’ equity–retained earnings by the same amount.

The operating activities column in Figure 5-2 is worth lingering over for a few moments because the financial outcomes of making profit are seen in this column. In my experience, most people see a profit number, such as the $1.69 million in this example, and stop thinking any further about the financial outcomes of making the profit. This is like going to a movie because you like its title, but you don’t know anything about the plot and characters. You probably noticed that the $1,515,000 increase in cash in this column differs from the $1,690,000 net income figure for the year. The cash effect of making profit (which includes the associated transactions connected with sales and expenses) is almost always different than the net income amount for the year. Chapter 6 on cash flows explains this difference.

Figure 5-2: Summary of changes in assets, liabilities, and owners’ equity during the year according to basic types of transactions.

The summary of changes presented in Figure 5-2 gives a sense of the balance sheet in motion, or how the business got from the start of the year to the end of the year. It’s very important to have a good sense of how transactions propel the balance sheet. A summary of balance sheet changes, such as shown in Figure 5-2, can be helpful to business managers who plan and control changes in the assets and liabilities of the business. They need a clear understanding of how the three basic types of transactions change assets and liabilities. Also, Figure 5-2 provides a useful platform for the statement of cash flows, which I explain in Chapter 6.

Coupling the Income Statement and Balance Sheet

Chapter 4 explains that sales and expense transactions change certain assets and liabilities of a business. (These changes are summarized in Figure 5-2.) Even in the relatively straightforward business example introduced in Chapter 4, we see that cash and four other assets are involved, and three liabilities are involved in the profit-making activities of a business. I explore these key interconnections between revenue and expenses and the assets and liabilities of a business here. It turns out that the profit-making activities of a business shape a large part of its balance sheet.

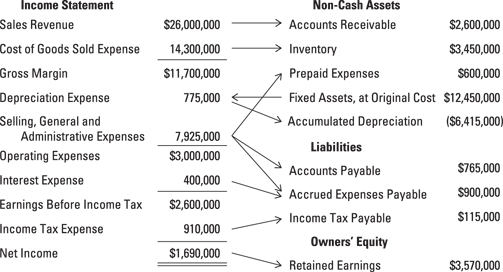

Figure 5-3 shows the vital links between sales revenue and expenses and the assets and liabilities that are driven by these profit-seeking activities. Note that I do not include cash in Figure 5-3. Sooner or later, sales and expenses flow through cash; cash is the pivotal asset of every business. Chapter 6 examines cash flows and the financial statement that reports the cash flows of a business. Here I focus on the noncash assets of a business, as well as its liabilities and owners’ equity accounts that are directly affected by sales and expenses. You may be anxious to examine cash flows, but as we say in Iowa, “Hold your horses.” I’ll get to cash in Chapter 6.

The income statement in Figure 5-3 continues the same business example I introduce in Chapter 4. It’s the same income statement but with one modification. Notice that the depreciation expense for the year is pulled out of selling, general, and administrative expenses. We need to see depreciation expense on a separate line.

Figure 5-3 highlights the key connections between particular assets and liabilities and sales revenue and expenses. Business managers need a good understanding of these connections to control assets and liabilities. And outside investors and creditors should understand these connections to interpret the financial statements of a business (see Chapters 13 and 16).

Figure 5-3: The connections between sales revenue and expenses and the noncash assets, liabilities, and owners’ equity driven by these profit-making activities.

Sizing up assets and liabilities

Although the business example I use in this chapter is hypothetical, I didn’t make up the numbers at random. For the example, I use a medium-sized business that has $26 million in annual sales revenue. The other numbers in its income statement and balance sheet are realistic relative to each other. I assume that the business earns 45 percent gross margin ($11.7 million gross margin ÷ $26 million sales revenue = 45 percent), which means its cost of goods sold expense is 55 percent of sales revenue. The sizes of particular assets and liabilities compared with their relevant income statement numbers vary from industry to industry, and even from business to business in the same industry.

Based on its history and operating policies, the managers of a business can estimate what the size of each asset and liability should be, which provide useful control benchmarks against which the actual balances of the assets and liabilities are compared, to spot any serious deviations. In other words, assets (and liabilities, too) can be too high or too low relative to the sales revenue and expenses that drive them, and these deviations can cause problems that managers should try to remedy.

For example, based on the credit terms extended to its customers and the company’s actual policies regarding how aggressively it acts in collecting past-due receivables, a manager determines the range for the proper, or within-the-boundaries, balance of accounts receivable. This figure is the control benchmark. If the actual balance is reasonably close to this control benchmark, accounts receivable is under control. If not, the manager should investigate why accounts receivable is smaller or larger than it should be.

The following sections discuss the relative sizes of the assets and liabilities in the balance sheet that result from sales and expenses (for the fiscal year 2013). The sales and expenses are the drivers, or causes, of the assets and liabilities. If a business earned profit simply by investing in stocks and bonds, it would not need all the various assets and liabilities explained in this chapter. Such a business — a mutual fund, for example — would have just one income-producing asset: investments in securities. This chapter focuses on businesses that sell products on credit.

Sales revenue and accounts receivable

In Figure 5-3 annual sales revenue for the year 2013 is $26 million. The year-end accounts receivable is one-tenth of this, or $2.6 million. So the average customer’s credit period is roughly 36 days: 365 days in the year times the 10 percent ratio of ending accounts receivable balance to annual sales revenue. Of course, some customers’ balances are past 36 days, and some are quite new; you want to focus on the average. The key question is whether a customer credit period averaging 36 days is reasonable.

Suppose that the business offers all customers a 30-day credit period, which is fairly common in business-to-business selling (although not for a retailer selling to individual consumers). The relatively small deviation of about 6 days (36 days average credit period versus 30 days normal credit terms) probably is not a significant cause for concern. But suppose that, at the end of the period, the accounts receivable had been $3.9 million, which is 15 percent of annual sales, or about a 55-day average credit period. Such an abnormally high balance should raise a red flag; the responsible manager should look into the reasons for the abnormally high accounts receivable balance. Perhaps several customers are seriously late in paying and should not be extended new credit until they pay up.

Cost of goods sold expense and inventory

In Figure 5-3 the cost of goods sold expense for the year 2013 is $14.3 million. The year-end inventory is $3.45 million, or about 24 percent. In rough terms, the average product’s inventory holding period is 88 days — 365 days in the year times the 24 percent ratio of ending inventory to annual cost of goods sold. Of course, some products may remain in inventory longer than the 88-day average, and some products may sell in a much shorter period than 88 days. You need to focus on the overall average. Is an 88-day average inventory holding period reasonable?

The “correct” average inventory holding period varies from industry to industry. In some industries, especially heavy equipment manufacturing, the inventory holding period is very long — three months or longer. The opposite is true for high-volume retailers, such as retail supermarkets, that depend on getting products off the shelves as quickly as possible. The 88-day average holding period in the example is reasonable for many businesses but would be too high for some businesses.

The managers should know what the company’s average inventory holding period should be — they should know what the control benchmark is for the inventory holding period. If inventory is much above this control benchmark, managers should take prompt action to get inventory back in line (which is easier said than done, of course). If inventory is at abnormally low levels, this should be investigated as well. Perhaps some products are out of stock and should be immediately restocked to avoid lost sales.

Fixed assets and depreciation expense

As Chapter 4 explains, depreciation is a relatively unique expense. Depreciation is like other expenses in that all expenses are deducted from sales revenue to determine profit. Other than this, however, depreciation is very different from other expenses. When a business buys or builds a long-term operating asset, the cost of the asset is recorded in a specific fixed asset account. Fixed is an overstatement; although the assets may last a long time, eventually they are retired from service. The main point is that the cost of a long-term operating or fixed asset is spread out, or allocated, over its expected useful life to the business. Each year of use bears some portion of the cost of the fixed asset.

The depreciation expense recorded in the period does not require any further cash outlay during the period. (The cash outlay occurred when the fixed asset was acquired, or perhaps later when a loan is secured for part of the total cost.) Rather, depreciation expense for the period is that quota of the total cost of a business’s fixed assets that is allocated to the period to record the cost of using the assets during the period. Depreciation depends on which method is used to allocate the cost of fixed assets over their estimated useful lives. I explain different depreciation methods in Chapter 7.

The higher the total cost of its fixed assets (called property, plant, and equipment in a formal balance sheet), the higher a business’s depreciation expense. However, there is no standard ratio of depreciation expense to the cost of fixed assets. The annual depreciation expense of a business seldom is more than 10 to 15 percent of the original cost of its fixed assets. Either the depreciation expense for the year is reported as a separate expense in the income statement (as in Figure 5-3), or the amount is disclosed in a footnote.

Because depreciation is based on the gradual charging off or writing-down of the cost of a fixed asset, the balance sheet reports not one but two numbers: the original (historical) cost of its fixed assets and the accumulated depreciation amount (the total amount of depreciation that has been charged to expense from the time of acquiring the fixed assets to the current balance sheet date). The purpose isn’t to confuse you by giving you even more numbers to deal with. Seeing both numbers gives you an idea of how old the fixed assets are and also tells you how much these fixed assets originally cost.

In the example we’re working with in this chapter, the business has, over several years, invested $12,450,000 in its fixed assets (that it still owns and uses), and it has recorded total depreciation of $6,415,000 through the end of the most recent fiscal year, December 31, 2013. (Refer to the balance sheet presented in Figure 5-1.) The business recorded $775,000 depreciation expense in its most recent year. (See its income statement in Figure 5-3.)

You can tell that the company’s collection of fixed assets includes some old assets because the company has recorded $6,415,000 total depreciation since assets were bought — a fairly sizable percent of original cost (more than half). But many businesses use accelerated depreciation methods that pile up a lot of the depreciation expense in the early years and less in the back years (see Chapter 7 for more details), so it’s hard to estimate the average age of the company’s assets. A business could discuss the actual ages of its fixed assets in the footnotes to its financial statements, but hardly any businesses disclose this information — although they do identify which depreciation methods they are using.

Operating expenses and their balance sheet accounts

Take another look at Figure 5-3 and notice that sales, general, and administrative (SG&A) expenses connect with three balance sheet accounts: prepaid expenses, accounts payable, and accrued expenses payable. The broad SG&A expense category includes many different types of expenses in making sales and operating the business. (Separate detailed expense accounts are maintained for specific expenses; depending on the size of the business and the needs of its various managers, hundreds or thousands of specific expense accounts are established.)

Many expenses are recorded when paid. For example, wage and salary expenses are recorded on payday. However, this record-as-you-pay method does not work for many expenses. For instance, insurance and office supplies costs are prepaid, and then released to expense gradually over time. The cost is initially put in the prepaid expenses asset account. (Yes, I know that “prepaid expenses” doesn’t sound like an asset account, but it is.) Other expenses are not paid until weeks after the expenses are recorded. The amounts owed for these unpaid expenses are recorded in an accounts payable or in an accrued expenses payable liability account.

For more detail regarding the use of these accounts in recording expenses you might want to refer to Chapter 4. Remember that the accounting objective is to match expenses with sales revenue for the year, and only in this way can the amount of profit be measured for the year. So expenses recorded for the year should be the correct amounts, regardless of when they’re paid.

What about cash?

A business’s cash account consists of the money it has in its checking accounts plus the money that it keeps on hand. Cash is the essential lubricant of business activity. Sooner or later, virtually all business transactions pass through the cash account. Every business needs to maintain a working cash balance as a buffer against fluctuations in day-to-day cash receipts and payments. You can’t really get by with a zero cash balance, hoping that enough customers will provide enough cash to cover all the cash payments that you need to make that day.

At year-end 2013, the cash balance of the business whose balance sheet is presented in Figure 5-1 is $2,165,000, which equals a little more than four weeks of annual sales revenue. How large a cash balance should a business maintain? This question has no simple answer. A business needs to determine how large a cash safety reserve it’s comfortable with to meet unexpected demands on cash while keeping the following points in mind:

![]() Excess cash balances are unproductive and don’t earn any profit for the business.

Excess cash balances are unproductive and don’t earn any profit for the business.

![]() Insufficient cash balances can cause the business to miss taking advantage of opportunities that require quick action — such as snatching up a prized piece of real estate that just came on the market or buying out a competitor.

Insufficient cash balances can cause the business to miss taking advantage of opportunities that require quick action — such as snatching up a prized piece of real estate that just came on the market or buying out a competitor.

Intangible assets and amortization expense

Although our business example does not include these kinds of assets, many businesses invest in intangible assets. Intangible means without physical existence, in contrast to buildings, vehicles, and computers. For example:

![]() A business may purchase the customer list of another company that is going out of business.

A business may purchase the customer list of another company that is going out of business.

![]() A business may buy patent rights from the inventor of a new product or process.

A business may buy patent rights from the inventor of a new product or process.

![]() A business may buy another business lock, stock, and barrel and may pay more than the total of the individual assets of the company being bought are worth — even after adjusting the particular assets to their current values. The extra amount is for goodwill, which may consist of a trained and efficient workforce, an established product with a reputation for high quality, or a very valuable location.

A business may buy another business lock, stock, and barrel and may pay more than the total of the individual assets of the company being bought are worth — even after adjusting the particular assets to their current values. The extra amount is for goodwill, which may consist of a trained and efficient workforce, an established product with a reputation for high quality, or a very valuable location.

Only intangible assets that are purchased are recorded by a business. A business must expend cash, or take on debt, or issue owners’ equity shares for an intangible asset in order to record the asset on its books. Building up a good reputation with customers or establishing a well-known brand is not recorded as an intangible asset. You can imagine the value of Coca-Cola’s brand name, but this “asset” is not recorded on the company’s books. (However, Coca-Cola protects its brand name with all the legal means at its disposal.)

The cost of an intangible asset is recorded in an appropriate asset account, just like the cost of a tangible asset is recorded in a fixed asset account. Whether or when to allocate the cost of an intangible asset to expense has proven to be a very difficult issue in practice, not easily amenable to accounting rules. At one time the cost of most intangible assets were charged off according to some systematic method. The fraction of the total cost charged off in one period is called amortization expense. Currently, however, the cost of an intangible asset is not charged to expense unless its value has been impaired. Testing for impairment is a very messy process. I do not go into the technical details here; because our business example doesn’t include any intangible assets, there is no amortization expense.

Debt and interest expense

Look back at the balance sheet shown in Figure 5-1. Notice that the sum of this business’s short-term (current) and long-term notes payable at year-end 2013 is $6.25 million. From its income statement in Figure 5-3 we see that its interest expense for the year is $400,000. Based on the year-end amount of debt, the annual interest rate is about 6.4 percent. (The business may have had more or less borrowed at certain times during the year, of course, and the actual interest rate depends on the debt levels from month to month.)

For most businesses, a small part of their total annual interest is unpaid at year-end; the unpaid part is recorded to bring interest expense up to the correct total amount for the year. In Figure 5-3, the accrued amount of interest is included in the accrued expenses payable liability account. In most balance sheets you don’t find accrued interest payable on a separate line; rather, it’s included in the accrued expenses payable liability account. However, if unpaid interest at year-end happens to be a rather large amount, or if the business is seriously behind in paying interest on its debt, it should report the accrued interest payable as a separate liability.

Income tax expense and income tax payable

In Figure 5-3, earnings before income tax — after deducting interest and all other expenses from sales revenue — is $2.6 million. The actual taxable income of the business for the year probably is different than this amount because of the many complexities in the income tax law. In the example, I use a realistic 35 percent tax rate, so the income tax expense is $910,000 of the pretax income of $2.6 million.

A large part of the federal and state income tax amounts for the year must be paid before the end of the year. But a small part is usually still owed at the end of the year. The unpaid part is recorded in the income tax payable liability account, as you see in Figure 5-3. In the example, the unpaid part is $115,000 of the total $910,000 income tax for the year, but I don’t mean to suggest that this ratio is typical. Generally, the unpaid income tax at the end of the year is fairly small, but just how small depends on several technical factors.

Net income and cash dividends (if any)

The business in our example earned $1.69 million net income for the year (see Figure 5-3). Earning profit increases the owners’ equity account retained earnings by the same amount, which is indicated by the line of connection from net income to retained earnings in Figure 5-3. The $1.69 million profit (here I go again using the term profit instead of net income) either stays in the business or some of it is paid out and divided among the owners of the business.

During the year the business paid out $750,000 total cash distributions from its annual profit. This is included in Figure 5-2’s summary of transactions — look in the financing activities column on the retained earnings line. If you own 10 percent of the shares you would receive one-tenth, or $75,000 cash, as your share of the total distributions. Distributions from profit to owners (shareholders) are not expenses. In other words, bottom-line net income is before any distributions to owners. Despite the importance of distributions from profit you can’t tell from the income statement or the balance sheet the amount of cash dividends. You have to look in the statement of cash flows for this information (which I explain in Chapter 6).

Financing a Business: Sources of Cash and Capital

To run a business, you need financial backing, otherwise known as capital. In broad overview, a business raises capital needed for its assets by buying things on credit, waiting to pay some expenses, borrowing money, getting owners to invest money in the business, and making profit that is retained in the business. Borrowed money is known as debt; capital invested in the business by its owners and retained profits are the two sources of owners’ equity.

How did the business whose balance sheet is shown in Figure 5-1 finance its assets? Its total assets are $14,850,000 at year-end 2013. The company’s profit-making activities generated three liabilities — accounts payable, accrued expenses payable, and income tax payable — and in total these three liabilities provided $1,780,000 of the total assets of the business. Debt provided $6,250,000, and the two sources of owners’ equity provided the other $6,820,000. All three sources add up to $14,850,000 million, which equals total assets, of course. Otherwise, its books would be out of balance, which is a definite no-no.

Accounts payable, accrued expenses payable, and income tax payable are short-term, non-interest-bearing liabilities that are sometimes called spontaneous liabilities because they arise directly from a business’s expense activities — they aren’t the result of borrowing money but rather are the result of buying things on credit or delaying payment of certain expenses.

It’s hard to avoid these three liabilities in running a business; they are generated naturally in the process of carrying on operations. In contrast, the mix of debt (interest-bearing liabilities) and equity (invested owners’ capital and retained earnings) requires careful thought and high-level decisions by a business. There’s no natural or automatic answer to the debt-versus-equity question. The business in the example has a large amount of debt relative to its owners’ equity, which would make many business owners uncomfortable.

Debt is both good and bad, and in extreme situations it can get very ugly. The advantages of debt are:

![]() Most businesses can’t raise all the capital they need from owners’ equity sources, and debt offers another source of capital (though, of course, many lenders are willing to provide only part of the capital that a business needs).

Most businesses can’t raise all the capital they need from owners’ equity sources, and debt offers another source of capital (though, of course, many lenders are willing to provide only part of the capital that a business needs).

![]() Interest rates charged by lenders are lower than rates of return expected by owners. Owners expect a higher rate of return because they’re taking a greater risk with their money — the business is not required to pay them back the same way that it’s required to pay back a lender. For example, a business may pay 6 percent annual interest on its debt and be expected to earn a 12 percent annual rate of return on its owners’ equity. (See Chapter 13 for more on earning profit for owners.)

Interest rates charged by lenders are lower than rates of return expected by owners. Owners expect a higher rate of return because they’re taking a greater risk with their money — the business is not required to pay them back the same way that it’s required to pay back a lender. For example, a business may pay 6 percent annual interest on its debt and be expected to earn a 12 percent annual rate of return on its owners’ equity. (See Chapter 13 for more on earning profit for owners.)

The disadvantages of debt are:

![]() A business must pay the fixed rate of interest for the period even if it suffers a loss for the period or earns a lower rate of return on its assets.

A business must pay the fixed rate of interest for the period even if it suffers a loss for the period or earns a lower rate of return on its assets.

![]() A business must be ready to pay back the debt on the specified due date, which can cause some pressure on the business to come up with the money on time. (Of course, a business may be able to roll over or renew its debt, meaning that it replaces its old debt with an equivalent amount of new debt, but the lender has the right to demand that the old debt be paid and not rolled over.)

A business must be ready to pay back the debt on the specified due date, which can cause some pressure on the business to come up with the money on time. (Of course, a business may be able to roll over or renew its debt, meaning that it replaces its old debt with an equivalent amount of new debt, but the lender has the right to demand that the old debt be paid and not rolled over.)

If a business defaults on its debt contract — it doesn’t pay the interest on time or doesn’t pay back the debt on the due date — it faces some major unpleasantness. In extreme cases, a lender can force it to shut down and liquidate its assets (that is, sell off everything it owns for cash) to pay off the debt and unpaid interest. Just as you can lose your home if you don’t pay your home mortgage, a business can be forced into involuntary bankruptcy if it doesn’t pay its debts. A lender may allow the business to try to work out its financial crisis through bankruptcy procedures, but bankruptcy is a nasty affair that invariably causes many problems and can really cripple a business.

Recognizing the Hodgepodge of Values Reported in a Balance Sheet

In my experience, the values reported for assets in a balance sheet can be a source of confusion for business managers and investors, who tend to put all dollar amounts on the same value basis. In their minds, a dollar is a dollar, whether it’s in accounts receivable, inventory, property, plant and equipment, accounts payable, or retained earnings. But as a matter of fact, some dollars are much older than other dollars.

The dollar amounts reported in a balance sheet are the result of the transactions recorded in the assets, liabilities, and owners’ equity accounts. (Hmm, where have you heard this before?) Some transactions from years ago may still have life in the present balances of certain assets. For example, the land owned by the business that is reported in its balance sheet goes back to the transaction for the purchase of the land, which could be 20 or 30 years ago. The balance in the land asset is standing in the same asset column, for example, as the balance in the accounts receivable asset, which likely is only 1 or 2 months old.

Book values are the amounts recorded in the accounting process and reported in financial statements. Do not assume that the book values reported in a balance sheet equal the current market values. Generally speaking, the amounts reported for cash, accounts receivable, and liabilities are equal to or are very close to their current market or settlement values. For example, accounts receivable will be turned into cash for the amount recorded on the balance sheet, and liabilities will be paid off at the amounts reported in the balance sheet. It’s the book values of fixed assets, as well as any other assets in which the business invested some time ago that are likely lower than their current replacement values.

Also, keep in mind that a business may have “unrecorded” assets. These off balance sheet assets include such things as a well-known reputation for quality products and excellent service, secret formulas (think Coca-Cola here), patents that are the result of its research and development over the years, and a better trained workforce than its competitors. These are intangible assets that the business did not purchase from outside sources, but rather accumulated over the years through its own efforts. These assets, though not reported in the balance sheet, should show up in better than average profit performance in its income statement.

The current replacement values of a company’s fixed assets may be quite a bit higher than the recorded costs of these assets, in particular for buildings, land, heavy machinery, and equipment. For example, the aircraft fleet of United Airlines, as reported in its balance sheet, is hundreds of millions of dollars less than the current cost it would have to pay to replace the planes. Complicating matters is the fact that many of its older planes are not being produced any more, and United would replace the older planes with newer models.

Businesses are not permitted to write up the book values of their assets to current market or replacement values. (Well, investments in marketable securities held for sale or available for sale have to be written up, or down, but this is an exception to the general rule.) Although recording current market values may have intuitive appeal, a market-to-market valuation model is not practical or appropriate for businesses that sell products and services. These businesses do not stand ready to sell their assets (other than inventory); they need their assets for operating the business into the future. At the end of their useful lives, assets are sold for their disposable values (or traded in for new assets).

Don’t think that the market value of a business is simply equal to its owners’ equity reported in its most recent balance sheet. Putting a value on a business depends on several factors in addition to the latest balance sheet of the business. My son, Tage, and I discuss business valuation in our book Small Business Financial Management Kit For Dummies (John Wiley & Sons).