Chapter 4

Operational Safety Decision-making and Economics

4.1 Economic Theories and Safety Decisions

4.1.1 Introduction

Making a decision is often difficult because of the uncertainties involved and the risks these uncertainties entail. A balance needs to be struck between different alternatives and the corresponding consequences. The decision therefore depends in part on how a choice problem is defined and the value that is attached to the pros and cons of an alternative. However, this involves a lot of uncertainty, as people can never be completely sure of the exact consequences of the chosen course of action [1].

Much research on decision-making has already been carried out in different disciplines. Various models and theories can be found in the literature that describe decision-making under conditions of uncertainty and which attempt to explain the phenomena observed. The first theory, developed as early as the seventeenth century, is the “expected value theory” (see also Chapter 2). According to this theory, people take decisions by maximizing the expected value.

However, the St. Petersburg paradox – which is a paradox related to probability and decision theory – made it clear that the expected value theory would not hold in real situations. The paradox is based on a particular (theoretical) lottery game that leads to a random variable with an infinite expected value (i.e., infinite expected payoff) but that nevertheless seems to be worth only a very small amount to the participants. The St. Petersburg paradox is a situation where a naïve decision criterion, which takes only the expected value into account, predicts a course of action that no actual person would be willing to take (see also Section 4.1.2). The St. Petersburg paradox therefore made a more accurate model necessary, and Bernoulli developed a new theory, the “expected utility theory.” This theory states that people attempt to maximize not the expected value, but the expected utility, when making decisions (see also Chapters 3, 7, and 8). People assess the utility of each outcome based on probabilities and then choose the alternative with the highest sum of weighted outcomes.

Kahneman and Tversky then developed a theory that took into account the human factor: the “prospect theory.” This theory was very successful as it included the psychological aspects of human behavior. In this theory, a choice problem is defined relative to a reference point. Depending on coding in terms of gains and losses, people will show more risk-averse or risk-seeking behavior [2–5].

People are constantly taking decisions, consciously or unconsciously. It is therefore not surprising that the subject of decision-making is studied in various disciplines, from mathematics and statistics to economy and political science, to sociology and psychology.

4.1.2 Expected Utility Theory

As described in the introduction, the first universally applicable decision-making theory was the “expected value theory,” developed as early as the seventeenth century. According to this theory, people take decisions based on maximization of the expected (monetary) value. However, this theory was repudiated by the St. Petersburg paradox. In the St. Petersburg paradox, a coin is tossed until “heads” appears. If “heads” appears on the first toss, the casino pays €1, otherwise it doubles the payout each time “heads” appears. What price would you be prepared to pay to enter this game? This paradox describes a gamble with an infinite expected value. Even so, most people intuitively feel that they should not pay a large price to take part in the game [3, 6].

To solve the St. Petersburg paradox, Bernoulli developed a new theory. He suggested that people want to maximize not the expected value, but the expected utility. As a result, the utility of wealth is not linear, but concave. After all, an increase in wealth of €1000 is worth more if the initial wealth is lower (e.g., from €0 to €1000) than if it is higher (e.g., from €10 000 to €11 000). This theory is called the expected utility theory in the literature. It is a theory about decision-making under conditions of risk in which each alternative results in a set of possible outcomes and in which the probability of each outcome is known. Individuals attempt to maximize the expected utility in their risky choices. They calculate the utility of each outcome using probabilities and choose the alternative with the highest sum of weighted outcomes. The attitude of an individual to risk is defined by the form of a utility function. For a risk-averse individual, the function is concave; for a risk-neutral individual, the function is linear; and for a risk-seeking individual, the function is convex. Given a choice between a certain outcome with a utility y and a gamble with the same utility y, a risk-averse individual will choose a certain outcome, a risk-seeking individual the gamble, and a risk-neutral individual will treat the two outcomes equally [3–5, 7–9].

4.1.3 Prospect Theory

The expected utility theory has been considered for a long time the most applicable method but, despite its strengths, it has encountered several problems as a descriptive model for decision-making under conditions of risk and uncertainty. After all, it requires that the decision-maker has access to all the information describing the whole of the situation. Clearly, this information requirement is far too rigorous for most practical applications, in which the probabilities cannot be calculated exactly, or the decision-maker does not yet know what he or she wants, or the series of alternatives is not fully determined, and so on. In addition, there is plenty of experimental evidence to suggest that individuals often fail to behave in the manner defined in the expected utility theory. In fact, the choices made by individuals consistently deviate from those predicted by the model, as is made clear in the experiments of Allais and Ellsberg.1 The so-called Allais paradox shows that individuals are sensitive to differences in probabilities. Experiments show that an individual's willingness to choose an uncertain outcome depends not only on the level of the uncertainty, but also on the source. People show dependence on a source when they are prepared to choose a proposition from source A but not the same proposition from source B. Regarding the so-called Ellsberg paradox, there are different versions of Ellsberg's experiment. In one version there are two urns, one containing 50 black and 50 red balls, and the other containing 100 balls about which it is only known that they are either red or black. People must choose an urn and a color, then draw a ball from the chosen urn. If the ball matches the color chosen, the subject wins a prize. Ellsberg noted that people display a strong preference for the urn with an equal number of red and black balls, despite the fact that economic analysis suggests that there is no reason to prefer one urn or the other. Ellsberg's classic study therefore shows that people attach a higher value to bets with known probabilities (risk) than to bets with unknown probabilities (uncertainty). This preference is called “ambiguity aversion.” The Ellsberg experiment shows that it is possible that decision-makers will not follow the usual rules of probability if they cannot act based on subjective probability. As a result, in such situations the theory of expected utility does not accurately predict behavior. For a more positive appreciation of expected utility theory see Chapter 7. An alternative theory was therefore required to describe the observed empirical deviations [3–5, 7–20].

Kahneman and Tversky's [4] prospect theory is considered an alternative to the expected utility theory and one of the principal theories for decision-making under conditions of risk. According to this theory, individuals are more likely to assess outcomes based on change from a reference point than on an intrinsic value. After all, people tend to think in terms of losses and gains rather than intrinsic values and therefore make choices based on changes relative to a certain reference point. The reference point is often, but not always, the status quo. Assuming that the reference point is zero, gains are represented by positive outcomes and losses by negative outcomes. The concept of a reference point means that people deal with losses differently from gains. Because people code outcomes in terms of a reference point and deal with losses and gains differently, the definition of this reference point or construction of the choice problem is crucial. How people approach the problem – i.e., in terms of losses or gains – affects the preferences independently of the mathematical equality between the two choice problems. Most decision problems take the form of a choice between maintaining the status quo and accepting an alternative, which may be more advantageous in some respects and less advantageous in others. The advantages of an outcome are then assessed as gains and the disadvantages as losses. Individuals usually give more weight to losses than to comparable gains and display more risk-averse behavior in the case of gains and more risk-seeking behavior in the case of losses [2–5, 10, 21–28].

According to prospect theory, each individual attempts to maximize the utility function, defined not in absolute terms but in terms of losses and gains relative to a reference point. This function is usually concave for gains and convex for losses, reflecting the risk-averse behavior for gains and risk-seeking behavior for losses, as shown in Figure 4.1 [2, 3, 8, 10, 21, 24, 27–30].

Figure 4.1 Utility function of prospect theory.

(Source: Wikipedia, 2016 [31].)

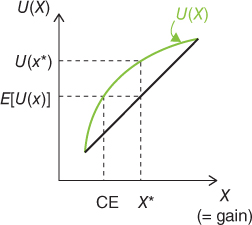

Risk-averse behavior for gains is seen in the fact that people choose certain gains rather than uncertain, but larger, gains. In Figure 4.2, a certain gain is shown as CE and the uncertain, larger, gain as x*. Due to risk-averse behavior, the expected value of the uncertain gain E[U(x)] is lower than the actual utility for this gain U(x*). The utility function of a risk-averse individual is therefore concave. Risk-seeking behavior in the case of losses, on the other hand, is expressed by the fact that people choose uncertain, higher losses rather than certain, but lower losses. Finally, in the case of risk-neutral behavior, the expected value, E[U(x)], will be equal to the actual utility U(x*), and the utility function will be linear. These findings can be readily applied to operational safety by inserting the safety utility function Su in the place of the utility function (see also Figure 3.6).

Figure 4.2 Utility function for gains (risk-averse behavior).

These findings show that the preference for prospects relating to losses only are the mirror image of preference for prospects relating to gains only. Kahneman and Tversky [4] call this the “reflection effect” around the reference point. This means that the sensitivity to change decreases with increasing distance from the reference point [2, 3, 8, 10, 21, 24, 27–30].

An aversion to risk is reflected in the observed behavior, i.e., people are more sensitive to losses than to gains. The utility function for losses is therefore steeper than that for gains, as shown in Figure 4.3. A loss of €5000 results in a value of −€4000, whereas a gain of €5000 only results in a value of €3000. In absolute terms, therefore, people attach a higher value to a loss than to an equivalent gain. This means that a reduction in loss has a much higher value than an increase in gain of the same amount, so that people express more risk-seeking behavior in the case of losses and more risk-averse behavior in the case of gains. The convex curve for losses and concave curve for gains therefore give a typical utility function an S-form [2, 3, 8, 10, 21, 24, 27–30].

Figure 4.3 The utility function curve.

(Source: Reproduced with permission of LessWrong [32].)

People treat gains differently from losses based on two aspects. The first of these is the reflection effect, as discussed earlier, and the second is “loss aversion.” Loss aversion explains why losses weigh more heavily than gains. It implies that people prefer the status quo, or other reference point, to a 50/50 chance of positive and negative alternatives with the same absolute value. The negative utility of giving up a good is therefore experienced as greater than the utility of acquiring a good, so that people often choose the status quo rather than a change. This phenomenon reflects the observed greater sensitivity to losses than to gains. The result is a utility function that is steeper for losses than for gains. One implication of loss aversion is that individuals have a strong tendency to remain in the status quo, as the disadvantages of leaving the status quo weigh more heavily than the advantages. Loss aversion also implies that people place a higher value on a good that they own than on a similar good that they do not own. This overvaluing of property is called the “endowment effect.” The process of acquiring a good increases its value. This even applies to trivial goods such as sweets or coffee mugs. One consequence of this phenomenon is that people often ask for more to give up a good than they are prepared to pay for it. This means that the selling price is always higher than the buying price, as the highest price a buyer is prepared to pay to acquire a good will be lower than the minimum compensation required to give up the same good [2, 4, 5, 10, 21, 24, 26–28, 33–36]. Translated into safety language, this means that safety management is not inclined to change existing company safety measures and policies, even if the new safety measures and policies would prove to be better at the same price. Therefore, a minimum safety increase premium (see Section 4.2.5) may be needed to convince safety management to change an existing safety situation.

In addition to the reflection effect, loss aversion, and the endowment effect, the prospect theory also makes use of other effects to describe and explain behavior during decision-making processes. First of all, it is possible to deduce from a number of empirical observations that individuals weigh certain outcomes more heavily than possible outcomes. This is called the “certainty effect.” People also weigh small probabilities more heavily, and attach too little weight to average and high probabilities. As a result, highly probable but uncertain outcomes are often treated as if they were certain. This effect is called the “pseudo-certainty effect.” Consequently, changes in probability that approach 0 or 1 have a larger impact on preferences than comparable changes in the middle of the range of probability. This effect can be clarified using the following example: during a hypothetical game of Russian roulette, people are prepared to pay more to reduce the number of bullets in the revolver from one to zero than from four to three. There is also the “immediacy effect,” which refers to a preference for outcomes that are experienced immediately. Finally, prospect theory also describes a “magnitude effect.” This effect refers to the following pattern: people are risk-seeking in the case of small gains and become strongly risk-averse as the size of the gain increases, and people are risk-averse in the case of very small losses and become more risk-seeking as the size of the losses increases [5, 8, 10, 21, 24, 25, 27].

4.1.4 Bayesian Decision Theory

The Bayesian decision theory can be seen as the newest theory, further advancing insights beyond prospect theory, and aims to resolve the consistency problems with, on the one hand, predictive risk analysis and expected utility theory and, on the other, common-sense considerations of risk acceptability in some well-constructed counter-examples in experiments like the ones by Allais and Ellsberg which are typically brought forth by the behavioral economists. This neo-Bernoullian decision theory is a direct reaction to Kahneman and Tversky's prospect theory [27], which was felt to put too high a premium on the sterile empiricism of hypothetical betting experiments, while at the same time failing to appeal to the need for compelling and rational first principles. The Bayesian decision theory differs from the expected utility theory in that an alternative position measure which captures the worst-case, most likely, and best-case scenarios is maximized, rather than the traditional criterion of choice where the expected values are maximized.

It can be demonstrated that this simple adjustment of the criterion of choice accommodates (non-trivially) the Allais paradox and the common-sense observation that type II events are more risky than type I events, as well as (very trivially, as the Ellsberg paradox is arguably not that paradoxical) the Ellsberg paradox (see Sections 7.3 and 7.4, respectively). Moreover, it can be shown that the proposed alternative criterion of choice relative to the traditional criterion of choice leads to a more realistic estimation of hypothetical benefits of type II risk barriers (see Section 8.12).

4.1.5 Risk and Uncertainty

The world that we live in is a world full of uncertainties in which, in most cases, we are unable to predict future events. Nevertheless, people are forced to make predictions given that suitable management responses are required when facing uncertainties, particularly in the field of operational safety. To explain how people deal with uncertainty when making a choice between different alternatives, use has traditionally been made of either formal models or rational analyses. Two types of models are used. The first of these is used mainly in economics and in research into decision-making: a numerical value is assigned to each alternative and the choice characterized by maximization of this value. In doing this, people mainly make use of normative models, such as the expected utility theory, or descriptive models, such as the prospect theory. The second type of model is usually used in law and politics. This approach identifies different reasons and arguments for why a certain decision should be taken. When making a decision, people weigh up the reasons for and the reasons against a certain alternative. A decision therefore depends in part on the value attached to the pros and cons of a particular alternative [1, 37].

A distinction should be made between “uncertainty” and “(negative) risk.” The difference between risk and uncertainty is that, in the case of uncertainty, the probability is not fully known. Risk is characterized by an objective probability distribution, while uncertainty bears no relation to statistical analysis [5, 38, 39].

In the modern world, (negative) risk takes two fundamental forms. Risk as a feeling refers to the quick, instinctive, and intuitive response of an individual to danger. Risk as analysis results in logic, reasoning, and scientific deliberation, as applied in risk management. People generally make decisions involving risk by constructing qualitative arguments that support their choice. During a decision-making process, a distinction is made between risky and risk-free choices. Risky choices are made with no prior knowledge of the consequences. As the consequences of such actions depend on uncertainties, this choice can also be regarded as a kind of gamble that results in certain outcomes with varying probabilities. However, the same choice can be described in different ways. For example, the possible outcomes of a gamble can be described as gains and losses compared with the status quo or the initial position. An example of decision-making involving risk is the acceptability of a gamble that results in a certain monetary outcome with a specific chance. A typical risk-free decision concerns the acceptability of a transaction in which a good or service is exchanged for money or labor. Most people will choose certainty in preference to a gamble, even though a gamble has, mathematically speaking, a higher expected value. This preference for certainty is an example of risk-averse behavior. As indicated before, a general preference for certainty rather than a gamble with a higher expected value is called risk aversion, and rejection of certainty for a gamble with the same or a lower expected value is called risk-seeking behavior. Furthermore, as also previously mentioned, people usually display risk-averse behavior when faced with improbable gains and risk-seeking behavior when faced with improbable losses [4, 38–41].

In addition to decision-making under conditions of risk, decision-making under conditions of uncertainty is also possible. Uncertainty describes a situation in which the decision-maker does not have access to any required statistical information. Various definitions of uncertainty are given in the literature. Whichever definition is used, uncertainty is not static, due to the dependence on knowledge. For example, if the amount of available information increases, the uncertainty will be reduced (e.g., going from domain B toward domain D in Figure 2.5). The term uncertainty is mainly used to describe the uncertainty resulting from the consequences of actions that are unknown because of their dependence on future events. This is often called “external uncertainty,” as it concerns the uncertainty of ambient conditions beyond the control of the decision-maker. Internal uncertainty refers to uncertainties in the preferences of the decision-maker, the definition of the problem, and the vagueness of the information [38, 42–50].

There are in fact two types of uncertainty – objective and subjective. Objective uncertainty relates to the information about the probabilities, whereas subjective uncertainty relates to the attitude of the decision-maker. There are two aspects with respect to this attitude of decision-makers: their attitude to the gain and their attitude to the negative risk. The attitude of a person to risk is traditionally – in accordance with expected utility theory – defined in terms of marginal utility or the form of the utility function. If a decision-maker is not risk-neutral, then the subjective and objective probabilities will not be equal [5, 49].

Decision-making under conditions of uncertainty takes place either if the prior information is incomplete or if the outcomes of the decisions are unclear. The best strategy for dealing with uncertainty in decision-making is to reduce or completely remove this uncertainty. Uncertainty can be reduced by collecting more information before making a decision or by delaying a decision. If no further information is available, uncertainty can be reduced by extrapolating the available information. Statistical techniques can be used to predict the future based on information relating to current or past events. Another technique is to form assumptions. Assumptions enable experienced decision-makers to take quick and efficient action within their domain of expertise, even if there is a lack of information. If it is considered to be unfeasible or overly expensive to reduce the uncertainty, this uncertainty can be acknowledged in two ways: by taking it into account when selecting an alternative, or by preparing to avoid or face the possible risk involved [42, 46, 48, 50].

If a decision is to be made under conditions of uncertainty, use can be made of various decision strategies, including MaxMin strategy, MaxMax strategy, and the Hurwicz criterion strategy. The choice of model depends on the attitude of the decision-maker. Three different attitudes are described in the literature: pessimistic, optimistic, and neutral. In the case of a pessimistic attitude, the decision-maker only considers the worst case for each alternative. He therefore makes use of the MaxMin strategy, and the alternative with the highest gain in the worst case will be selected. In the case of an optimistic attitude, decision-makers only consider the best case for each alternative. They therefore select the alternative with the highest gain in the best case, using the so-called MaxMax strategy (not to be confused with the so-called “Maxmax hypothetical benefits” – see later in this chapter). The third type is the neutral attitude. In this case, the decision-maker considers each case in the same way and the evaluation value of each alternative is determined by the general conditions. A combination of an optimistic and pessimistic attitude is called the Hurwicz method [45, 47, 49].

It should be noted that the uncertainties involved in making decisions increase in size and impact if decisions need to be made concerning the risks related to type II risks. After all, high-impact, low-probability (HILP) events are characterized by low probabilities and large, extensive, and possibly irreversible consequences. Type II risks are not always well understood, with the result that people do not always know how to deal with them. It is not possible to increase knowledge through experimentation, given that the risks are effectively irreversible in a normal time frame. The classic theories, based on expected utility, therefore do not always work and results should be interpreted with great caution, as the models tend to underestimate events with low probabilities [46, 51], as is demonstrated in Section 7.5.

4.1.6 Making a Choice Out of a Set of Options

When making a decision, a choice usually needs to be made from a set of possible options. This choice is not made randomly. An attempt is made to make a choice that provides the best answer to a number of criteria: the optimum choice. Each choice results in a gain of a certain value, so that the choice is selected with the largest gain. However, in most cases, the gains resulting from a choice are affected by variables of unknown value. It is traditional to assume that, if a rational choice needs to be made between two alternatives that involve uncertainties, the uncertainty is described using probability and the different alternatives are ordered based on the expected utility of the consequences of these alternatives. Selection of one alternative is therefore based on the probability and potential value of a possible outcome [47, 52, 53].

There are two phases involved in making a choice. The first phase involves various mental operations that simplify the choice problem by transforming the representation of outcomes and probabilities. Coding involves the identification of the reference point and the framing of outcomes as deviations from this reference point, and this affects orientation toward risk. After all, a difference between two alternatives will always have a larger impact if it is seen as a difference between two disadvantages rather than a difference between two advantages. The decision can therefore be made to allow the disadvantages of a deviation to weigh more heavily than the advantages. In addition, common elements to the various alternatives or irrelevant alternatives are also often eliminated. This “isolation effect” can result in different preferences, as there are different ways of separating prospects into shared and distinctive elements. This can result in a reversal in preferences and inconsistency. The second phase is the evaluation phase [5, 36].

The traditional utility function assumes that an individual has a well-organized and stable system of preferences and good calculation skills. However, such an assumption is unrealistic in many contexts. In response to this problem, Simon [54] developed the theory of bounded rationality. This implies that, due to the expense and impracticalities involved in choosing between all possible alternatives to achieve the optimum choice, people usually look for the first satisfactory alternative that meets a set of predetermined objectives. The implication is therefore that human behavior should be modeled as satisfying rather than optimizing. Such an approach has several appealing qualities, as working with objectives is, in most cases, very natural [47, 54, 55].

Evaluation of the outcomes is susceptible to framing effects due to the non-linear utility function and people's tendency to compare outcomes with a reference point. The decision frame used to analyze a decision refers to the perception of the decision-maker regarding a possible outcome of a risky decision in terms of gains and losses. Whether or not a certain outcome is seen as a loss or a gain depends on the reference point used to evaluate possible outcomes. The framing effect is seen whenever the same outcome can be considered a loss or a gain, depending on the reference point used. For example, if a company is faced with an accident cost of €5000, which was expected to be €10 000, is this experienced as a loss or a gain? The answer depends, for example, on whether the previous accident cost or the expected value is used as a reference point. Whether or not a decision is considered in terms of a loss or a gain is very important, because people display risk-seeking behavior when faced with losses and more risk-averse behavior when faced with gains [4, 8, 56].

It is therefore clear that emotions play an important role in social and economic decision-making. Individuals, including people who need to make decisions on safety budgets – such as safety managers and middle and top managers – evaluate alternatives subjectively and emotions influence these evaluations. People generally try to control these emotions and to anticipate the emotional impact on future decisions, as emotions can affect such decisions. The impact of emotions is of particular importance when assigning a value to different perspectives [8, 57].

4.1.7 Impact of Affect and Emotion in the Process of Making a Choice between Alternatives

Traditional economic theory assumes that most decision-making involves the rational maximization of the expected utility. Such an approach assumes that people have access to unlimited knowledge, time, and information-processing skills. In the 1970s and 1980s, researchers identified several phenomena that systematically violated the normative principles of economic theory. In the 1990s, emotions were shown to play a significant role in various forms of decision-making, in particular concerning decisions that involved a high level of risk and uncertainty [40, 58–60].

According to Epstein and Pacini [61], people understand reality through two interactive, parallel processing systems. The rational system is a deliberative, analytical system that functions using established rules of logic and evidence (such as the prospect theory). This system makes it possible for individuals to consciously seek knowledge, develop ideas, and analyze. On the other hand, the experiential, emotional system codes reality in images, metaphors, and narratives to which affective feelings are attached. This system enables individuals to learn from experience without consciously paying attention. Individuals differ in the extent to which the rational and experiential systems influence their decision-making. The balance between these two processes is influenced by various factors, such as age and cognitive load, both of which result in a greater dependence on affect. By affect, the “faint whisper of emotion” that influences decisions directly is meant, and is not simply an answer to a prior analytical evaluation [41, 60, 62].

People therefore base their judgment on a certain activity, not just on what they think, but also on what they feel. If they have a good feeling about a certain activity, they assess the risk as low and the benefit as high. However, if they do not have a good feeling, they will judge the risk as high and the benefit as low. This is called “affect heuristic” in the literature. If the consequences are highly affective, as in the case of the lottery or cancer, there is little variation. For example, research by Loewenstein and Prelec [8] showed that people expressed the same feelings regarding winning the lottery whether the chance was 1 in 10 million or 1 in 10 000 [41, 59, 60].

In any case, it is clear that emotions, which can be interpreted and expressed as moral principles, should be much more considered in risk indexing and risk calculations than is the case today. Section 4.10.4 therefore suggests an approach to calculate risks, where both rational and moral factors are taken into account.

4.1.8 Influence of Regret and Disappointment on Decision-making

People always wish that they had made a different decision if the decision they made turns out to have negative consequences. This feeling is even stronger if it turns out that the alternative would have resulted in a more favorable outcome. In such situations, people experience a feeling of regret. Regret is a psychological response to the making of a wrong decision. A “wrong” decision is defined based on the actual outcome and not on the information available at the moment the decision was made. Regret can result from comparison of an outcome with an outcome that would have resulted from making a different decision. Regret therefore has much in common with opportunity cost (see Chapter 5).

Regret can affect people in two ways. First of all, it can lead people to try to undo the consequences of their regretted choice after the decision has been made. Second, if they anticipate the regret they would later feel, it can influence the choice they make before the decision is taken. A new decision-making model was developed based on this anticipatory aspect of regret – the “regret theory.” Whereas classical theories assume that the expected utility of a choice depends only on the possible pain or pleasure associated with the outcome of that choice, in regret theory utility also depends on the feelings caused by the outcome of the rejected choices. Regret theory is based on two fundamental assumptions. The first is that people compare the real outcome with the outcome that would have resulted from making a different choice. As result of this, people experience certain feelings: regret, if the choice that they did not make would have resulted in a more favorable outcome; and pleasure, if the choice made has produced the best possible outcome. The second assumption of the regret theory is that the emotional consequences of the decision are anticipated and taken into account when making that decision. Different experiments have shown that such behavior results in a more risk-averse attitude. However, this is not always the case. Although most people do their best to avoid regret, this does not only result in more risk-averse behavior, but can also lead people to display more risk-seeking behavior. An aversion to regret can therefore result in choosing an outcome with the lowest (negative) risk as well as in choosing an outcome with the highest (negative) risk. Experiencing regret and disappointment also has another consequence, which is that avoiding feedback so as not to experience regret and disappointment means that people do not learn from their experiences [3, 13, 59, 63].

As well as regret and pleasure, people can also experience disappointment when making a choice between alternatives. Disappointment is a psychological response to an outcome that does not correspond to expectations. When people make a decision, they can experience these feelings when comparing uncertain alternatives. However, it is not always possible to compare the outcome of a chosen alternative and the outcome of an alternative that was not chosen. Imagine that a choice needs to be made between a certain alternative and an uncertain one. If an alternative is chosen with outcome characteristics with some probability, it is always clear what the result of the other (certain) alternative would be. However, if the certain alternative is chosen, it is not always possible to determine whether this choice resulted in a more favorable outcome or not, because one does not know whether the uncertain alternative would have been realized or not [3, 13, 59, 63].

It is possible to translate the principle of regret theory into industrial practice by using expected hypothetical benefits (see also Section 4.2.4) to aid decision-making. To this end, later in this book, expected hypothetical benefits are explained in greater depth and they are used in cost-benefit analysis (see Chapter 5) and cost-effectiveness analysis (see Chapter 6) approaches for decision-making purposes.

4.1.9 Impact of Intuition on Decision-making

The accuracy of decision-making is often inversely proportional to the speed with which decisions need to be made. To explain the fact that people are able to make high-quality decisions relatively quickly, most researchers focus on intuition. Individuals mainly make use of intuition when they are faced with severe time constraints. After all, intuition is based on our innate ability to synthesize information rapidly and effectively and could therefore be essential in successfully solving complex tasks in a short space of time. However, intuitively making decisions does not always result in accurate decisions, as applying intuition only results in speed, sometimes at the expense of accuracy [62, 64].

4.1.10 Other Influences while Making Decisions

In addition to emotions, there are also other factors that influence decision-making. The knowledge available within the decision context also determines an individual's behavior when choosing between alternatives. Research shows that individuals who are not experts are typically overconfident. They overestimate the quality of their abilities and knowledge and perceive extreme probabilities as not so extreme. Experts and more qualified people, on the other hand, are more sensitive to the risk associated with a hypothetical gamble and display more risk-averse behavior, as shown in the research of Donkers et al. [65]. Second, age also has an impact on the decision-making process. The older an individual, the more experience they have and the more capable they are of curtailing overconfidence and therefore responding like an expert. Older people have a more accurate idea of their knowledge and the limits of that knowledge [66, 67].

Finally, gender also plays a large role in decision-making. Many studies have highlighted the fact that men are more risk-seeking than women. The reasons for this difference in approach to risk have already been investigated in various research areas. They can be caused by nature or nurture, or a combination of the two. For example, (young) boys are expected to take risks when participating in competitive sports, whereas (young) girls are often encouraged to be careful. The high-risk choices that men make may therefore be the result of the way in which they were raised by their parents. The same applies to women's risk aversion. Another possible explanation for gender differences is that the way in which risk is experienced relates to the cognitive and non-cognitive differences between men and women. It should be pointed out that women who acquire more competences, become more confident or obtain more knowledge show increased risk-seeking behavior when making decisions. However, such factors have an opposite effect on men, who display more risk-averse behavior with increasing expertise and confidence. Finally, the framing of a decision problem strongly influences the way in which a man makes a decision, but not a woman [14, 66, 68, 69].

4.2 Making Decisions to Deal with Operational Safety

4.2.1 Introduction

In the previous section, the way in which people make decisions and choices, and all the accompanying influencing psychological principles, was discussed. It is obvious that decision theory and making choices under uncertainty are not at all easy to model. The very nature of operational safety management, safety being defined as “a dynamic non-event,” makes it very hard to develop a decision-supporting model. Nonetheless, safety managers need to make such decisions, based on their emotions, their intuition, and the available information and its accompanying uncertainty and/or variability. Making decisions to deal with operational safety should be as accurate as feasible, rational, cost-effective, simple yet not over-simplified, no-nonsense and pragmatic, and, most importantly, as effective as possible (so that there are as many non-events as possible). To this end, a number of possible decision-making approaches may be worked out and will be elaborated upon and explained in the remainder of this book. The decision process should lead to adequate and optimized (according to the company's safety management characteristics) risk treatment. The concept of “risk treatment” should be explained at this point. There are several possible ways to treat risks:

- 1. Risk treatment option 1: risk reduction

- a. Risk avoidance

- b. Risk control.

- 2. Risk treatment option 2: risk acceptance

- a. Risk retention

- b. Risk transfer.

Organizations basically have two main options to deal with risks: they can either accept the risks, or they can reduce the risks. Risk reduction options involve technological, organizational/procedural, and human factor prevention and mitigation measures in order to decrease the risk level. Risk acceptance options, on the other hand, encompass measures that reduce the financial impact of the risks on the organization. There are two sub-options available within each of the two main options [70]. For risk reduction these are risk avoidance and risk control, whereas for risk acceptance, these are risk retention and risk transfer.

4.2.2 Risk Treatment Option 1: Risk Reduction

Risk avoidance and risk control can be achieved in an optimal way by inherent safety or design-based safety. There are five principles of design-based safety. The possible implementation of these five principles is explained for the case of the chemical industry, illustrated in Figure 4.4.

Figure 4.4 Five principles of design-based safety implemented in the chemical industry.

(Source: Kletz [71, 72]. Reproduced with permission from Taylor & Francis.)

As explained by Meyer and Reniers [73], techniques of risk reduction aim to minimize the likelihood of occurrence of an unwanted event and/or the severity of potential losses as a result of the event, or aim to make the likelihood or outcome more predictable. They are applied to existing processes and situations and can be listed as:

- Substitution – by replacing substances and procedures by less hazardous ones, by improving construction work, and so on. Care should be taken that there is not simply a replacement of risk.

- Elimination of risk exposure – this consists in not creating or completely eliminating the condition that could give rise to the exposure to risk.

- Prevention – combines techniques to reduce the likelihood/frequency of potential losses.

- Protection/mitigation – these are techniques whose goal is to reduce the severity of accidental losses before/after an accident occurs.

- Segregation – summarizes the techniques used to minimize the overlapping of losses from a single event. This possibility may imply very high costs:

- Segregation by separation of high-risk units

- Segregation by duplication of high-risk units.

Using principles such as elimination, substitution, moderation, and attenuation in the design phase is always better than to use them in an existing situation/process. In the former case, the approach is called design-based safety (as already explained), and in the latter case it is called “add-on safety.” Design-based safety is known to be much more cost-effective than add-on safety, certainly in the long term. Hence, from an economic viewpoint, design-based safety should always be preferred.

4.2.3 Risk Treatment Option 2: Risk Acceptance

Risk retention and risk transfer, both sub-options of risk acceptance, only differ in the financial consequences of a risk turning into an accident. Risk retention concerns intentionally or unintentionally retaining the responsibility for a specified risk. Intentional retention is referred to as “risk retention with knowledge” and can be seen as a manner of self-insurance or auto-financing, finance planning of potential losses by an organization's own resources. Unintentional retention is referred to as “risk retention without knowledge,” which is caused by inadequate hazard identification and insufficient risk assessment and management.

Usually, self-insurance will only be an option for large organizations able to set up and administrate an insurance fund. It is important to understand that only those losses that are predictable through statistical calculations, thus mainly type I risks, should be retained within an organization. Companies should avoid those risks (of mainly type II), possibly resulting in a major catastrophe or bankruptcy. The advantage of self-insurance is that insurance premiums should be lower, as there are no intermediaries expecting payments for costs, profits, or commissions. In such cases, the insured party also receives the benefit of investment income from the insurance fund that has been established, and keeps any profit accrued from it. Hence, there is an incentive for an organization to practice good risk management principles. However, there is also a downside to auto-financing: a self-insured organization will usually establish its insurance fund based on a statistical normal distribution of losses, being calculated over an extended time period. Hence, as company losses for some insurable type II risks may occur within 20 years but also the next day, there may be insufficient funds accrued to cope with certain losses, especially during the early years of the insurance fund.

Risk transfer involves shifting the responsibility for a specified risk to a third party. Insurance represents an important option for an organization to deal with risks. Risks can – in total or in part – be transferred to external agents, and hence the organization may carry out its business with the reassurance that if an accident occurs that is insured, the insurance company will provide an indemnity.

As risk transfer provides little incentive for a company to significantly reduce risk levels, there used to be a time when “risk management” was considered by company management as “insurance management.” This period is rightfully a long time ago. Companies nowadays realize that not all risks are insurable, and that for those risks that are insured, there are often large uninsured consequences, besides those that are insured and that will be compensated. Risks that are typically covered by insurance include employer's liability, public liability, product liability, fire, and transport. Uninsured risks typically include equipment repairs, employee sick pay, loss of production, staff replacement, damage to corporate image, and accident investigations. A more elaborated list of incident and accident costs is given in Section 4.3 and also further in Chapter 5 on cost-benefit analysis.

4.2.4 Risk Treatment

Risk treatment is the selection and implementation of appropriate options for dealing with risk. It includes choosing among risk avoidance, risk reduction, risk transfer, and/or risk retention, or a combination thereof. Often, there will be residual risk which cannot be removed totally as it is not cost-effective to do so. Risk treatment thus involves identifying the range of options for treating risks, assessing these options financially and preparing and implementing treatment plans. The risk management treatment measures may be summarized as:

- avoid the risk – decide not to proceed with the activity likely to generate risk;

- reduce the likelihood of harmful consequences occurring;

- reduce the consequences occurring;

- transfer the risk – cause another party to share or bear the risk;

- retain the risk – accept the risk and be prepared if an accident occurs.

Risk treatment should be looked at from an economic viewpoint. Financial aspects can play a pivotal role in advocacy and decision-making on risk treatment by demonstrating the financial and economic value of the different treatment options.

Some new concepts need to be defined to be able to develop an approach to decide between different risk treatment options, i.e., the concepts of variability, normalized variability, and hypothetical benefit.

Variability can be defined as the maximum variation between the possible costs of every risk treatment option. Variability can thus be calculated as the difference between the maximum cost and the minimum cost of risk treatment, and doing this for every risk treatment option. As the possible costs per risk treatment option really are different depending on the scenario, variability does not depend on the measurement process used to estimate the costs.

The following formula can be used to determine the variability:

The normalized variability can then be determined by:

The hypothetical benefit of the risk treatment option can be defined in two ways:

- Definition (i) – as the difference between the highest possible costs of an accident in the current situation and those of an accident after applying the treatment measure; hence:

- Definition (ii) – as the difference between the costs of retention when doing nothing (taking no action) and those of the possible accident after applying the treatment measure; hence:

Based on the risk attitude of the decision-maker, one of both hypothetical benefit definitions may be preferred and chosen.

Notice that uncertainty is not the same as variability (as previously explained in this book). Uncertainty is the result of not having sufficient information. It can be considered the result of not being able to measure with sufficient precision, and hence, simply put, it is the result of imprecise methods of measurement [74]. As all measurement methods are imprecise, at least to some degree, all information is accompanied by a high or a low amount of uncertainty. This is the basis of the notion of “risk” and leads to the knowledge that every aspect of decision-making in life is accompanied by risk (see also Chapter 1). It also leads to the distinction between the two types of risk: risks with a lot of information available and hence a low amount of uncertainty (so-called type I risks), and risks with a paucity of information and thus a high amount of uncertainty (so-called type II risks). Risk treatment calculations such as those suggested and illustrated in this section should only be carried out if adequate financial information is available. This relates to type I risks and the more common type II risks.

In the case of definition (i), calculation of the Maxmax hypothetical benefits, emphasis is placed on the consequences of an event, irrespective of the probabilities. In the case of definition (ii), calculation of the expected hypothetical benefits, probabilities are considered. Therefore, definition (i) may be interesting for decision-makers putting more emphasis on consequences (or in case there is a lack of probability information, such as with some type II risks), while definition (ii) would probably be more interesting for decision-makers taking consequences as well as probabilities into consideration (and disposing over the probability information).

It should be noted by the reader that, besides the choice of the definition to determine the hypothetical benefits, which can be rather subjective, the risk treatment calculations approach explained in this section is highly rational and only financial considerations are used to make the calculations and recommendations. No moral aspects, such as equity, justification of the risk, and other ethical aspects, are taken into account in this approach. Therefore, if used, it should be applied with this knowledge in mind. Ethical aspects will be discussed later in this chapter.

4.2.5 The “Human Aspect” of Making a Choice between Risk Treatment Alternatives

Different factors play a role when taking decisions and making choices between various alternatives. The decision-making process becomes even more complicated in an organizational context. Managers need to make decisions concerning issues that affect not only their personal lives, but also the company they work for, its employees, its surroundings, and more. The majority of management problems of any enterprise, including safety investment portfolio management, is characterized by uncertainties and lack of necessary information. The difficulty in predicting future parameter values and future events has an impact on the evaluation of safety investment projects. Uncertainty, or the lack of information, thus obviously hampers managerial decisions. To decrease the level of uncertainty, managers may use historic data, trends, statistical information, qualitative expert judgments, past achievements, and all other information available to the company [37, 75].

Managerial behavior and decision-making sometimes have little affinity with real skills and available resources. The way people think and people behave is much more linked to situational perception and the ability to control processes and potential results. Managers may make different decisions in a similar situation as a result of a different interpretation and evaluation of the situation at hand. Decisions can be divided into two groups: opportunities and threats. Managers usually view controllable situations as opportunities and uncontrollable ones as threats. However, what is interpreted as “controllable” and as “uncontrollable” depends entirely on the person, and varies strongly from manager to manager. Therefore, it is possible that one manager sees a situation characterized by a certain level of uncertainty as an opportunity, while another manager sees the same situation as a threat [75–77].

4.2.5.1 Safety Increase Premium

Preferences toward safety can be described (as already indicated in Chapter 3), by a safety utility function and provide, for example, an idea of the safety state difference one is willing to suffer to leave the person indifferent between an uncertain (but higher) safety state (point B in Figure 4.6) and a certain (but lower) safety state (point A in Figure 4.6). “Uncertain” in this regard indicates that management feels less certain about the effectiveness of the higher safety situation than that of the lower safety situation, and asks, “Is it worth the trouble or money?”

Figure 4.6 Safety increase premium determination.

The safety increase premium can then be calculated as the extra budget that is required to cover the difference between safety state x** and x*, because a certain safety situation x* delivers the same expected utility as the uncertain safety situation x** and its corresponding expected value. Hence, the safety premium can be regarded as the amount of money that safety management needs to invest to get into a higher safety situation (but one perceived as more uncertain with respect to its effectiveness). It is the minimum amount that risk-averse management (cf. the shape of the safety utility function) would need to spend on safety to leave it indifferent between the uncertain and the certain safety situations.

4.3 Safety Investment Decision-making – a Question of Costs and Benefits

4.3.1 Costs and Hypothetical Benefits

Accidents do bear a cost – and often not a small one. An accident can be linked to a variety of direct and indirect costs. Table 4.1 gives a non-exhaustive list of potential costs that might accompany accidents.

Table 4.1 Non-exhaustive list of quantifiable and non-quantifiable socioeconomic consequences of accidents

| Interested parties | Non-quantifiable consequences of accidents | Quantifiable consequences of accidents |

| Victim(s) | Pain and suffering | Loss of salary and bonuses |

| Moral and psychic suffering | Limitation of professional skills | |

| Loss of physical functioning | Time loss (medical treatment) | |

| Loss of quality of life | Financial loss | |

| Health and domestic problems | Extra costs | |

| Reduced desire to work | ||

| Anxiety | ||

| Stress | ||

| Colleagues | Bad feeling | Time loss |

| Anxiety or panic attacks | Potential loss of bonuses | |

| Reduced desire to work | Heavier workload | |

| Anxiety | Training and guidance of temporary employees | |

| Stress | ||

| Organization | Deterioration of social climate | Internal investigation |

| Poor image, bad reputation | Transport costs | |

| Medical costs | ||

| Lost time (informing authorities, insurance company, etc.) | ||

| Damage to property and material | ||

| Reduction in productivity | ||

| Reduction in quality | ||

| Personnel replacement | ||

| New training for staff | ||

| Technical interference | ||

| Organizational costs | ||

| Higher production costs | ||

| Higher insurance premiums | ||

| Administrative costs | ||

| Sanctions imposed by parent company | ||

| Sanctions imposed by the government | ||

| Modernization costs (ventilation, lighting, etc.) after inspection | ||

| New accident indirectly caused by accident (due to personnel being tired, inattentive, etc.) | ||

| Loss of certification | ||

| Loss of customers or suppliers as a direct consequence of the accident | ||

| Variety of administrative costs | ||

| Loss of bonuses | ||

| Loss of interest on lost cash/profits | ||

| Loss of shareholder value |

Meyer and Reniers [73]. Reproduced with permission from De Gruyter.

Hence, by implementing a sound safety policy and by adequately applying operational risk management, substantial costs can be avoided, namely all costs related to accidents that have never occurred (i.e., the non-events), the so-called “hypothetical benefits.” However, in current practice, companies place little or no importance on the “hypothetical benefit” concept due to its complexity. In Section 4.2.4 an attempt has been made to make the concept more tangible. In Section 8.12 the concept is explored even more in depth, as hypothetical benefits are equated and modeled as a maximum investment willingness.

Non-quantifiable costs are highly dependent on non-generic data such as individuals' characteristics, a company's culture and/or the company as a whole and even socio-economic circumstances. Rather, the costs assert themselves when the actual costs supersede the quantifiable costs. In economics (e.g., in environment-related predicaments) monetary evaluation techniques are often used to specify non-quantifiable costs, among them the contingent valuation method and the conjoint analysis or hedonic methods. In the case of non-quantifiable accident costs, various studies have demonstrated that these form a multiple of the quantifiable costs [73].

The quantifiable socioeconomic accident costs (see Table 4.1) can be divided into direct and indirect costs. Direct costs are visible and obvious, while indirect costs are hidden and not immediately evident. In a situation where no accidents occur, the direct costs result in direct hypothetical benefits, whilst the indirect costs result in indirect hypothetical benefits. The resulting indirect hypothetical benefits comprise, for example, not having sick leave or absence from work, not having staff reductions, not experiencing labor inefficiency and not experiencing change in the working environment. Figure 4.7 illustrates this reasoning.

Figure 4.7 Analogy between total accident costs and hypothetical benefits.

(Source: Meyer and Reniers [73]. Reproduced with permission from De Gruyter.)

Although hypothetical benefits seem to be rather theoretical and conceptual, they are nonetheless important if you are to fully understand safety economics. Hypothetical benefits resulting from non-occurring accidents or “non-events” can be divided into different categories at the organizational level, depending on the preferences and characteristics of the organization and its safety management. Meyer and Reniers [73], for example, mention five classes of hypothetical benefits. The first category concerns the non-loss of work time and includes the non-payment of the employee who at the time of the accident adds no further value to the company (if payment were to continue, this would be a pure cost). The non-loss of short-term assets forms the second category and can include, for example, the non-loss of raw materials. The third category involves long-term assets, such as the non-loss of machines. Various short-term benefits, such as non-transportation costs and non-fines, constitute the fourth category. The fifth category consists of non-loss of income, non-signature of contracts or non-price reductions. In Chapter 5, hypothetical benefits are elaborated in greater depth. Independent of the number of classes or categories used, the visible or direct hypothetical benefits generated by the avoidance of costs resulting from non-occurring accidents only make up a small portion of the factors responsible for the total hypothetical benefits resulting from non-occurring accidents.

Next to tangible benefits, intangible benefits might exist. Intangible benefits may manifest themselves in different ways, e.g., non-deterioration of image, avoidance of lawsuits, and the fact that an employee, thanks to the safety policy and the non-occurrence of accidents, does not leave the organization. If an employee does not leave the organization, the most significant benefit arises from work hours that other employees do not have to make up. Management time is consequently not given over to interviews and routines surrounding the termination of a contract. The costs of recruiting new employees can, for example, prove considerable if the company has to replace employees with experience and company-specific skills. Research into the reasons that form the basis of recruitment of new staff reveals a difference between, on the one hand, the recruitment of new employees due to the expansion of a company and, on the other hand, the replacement of staff who have resigned due to poor safety policies.

4.3.2 Prevention Benefits

An accident that does not occur in an enterprise, thanks to the existence of an efficient safety and prevention policy within the company, was referred to as a non-occurring accident or a non-event. Non-occurring accidents (in other words, the prevention of accidents) result in the avoidance of a number of costs and thus create hypothetical benefits, as explained previously. An estimation of the amount of input and output of the implementation of a safety policy is thus clearly anything but simple. It is impossible to specify the costs and benefits of one exceptional measure. The effectiveness (and the costs and benefits) of a safety policy must be regarded as a whole.

Hence, if an organization is interested in knowing the efficiency and the effectiveness of its safety policy and its prevention investments, in addition to identifying all kinds of prevention costs, it is also worth calculating the hypothetical benefits that result from non-occurring accidents. By taking all prevention costs and all hypothetical benefits into account, the true prevention benefits can be determined.

4.3.3 Prevention Costs

In order to obtain an overview of the various kinds of prevention costs, it is appropriate to distinguish between fixed and variable prevention costs, on the one hand, and direct and indirect prevention costs on the other.

Fixed prevention costs remain constant irrespective of changes in a company's activities. One example of a fixed cost is the purchase of a fireproof door. This is a one-off purchase and the related costs are not subject to variation in accordance with production. Variable costs, in contrast to fixed costs, vary proportionally in accordance with a company's activities. The purchase of safety gloves can be regarded as a variable cost due to the fact that the gloves have to be replaced sooner when used more frequently or more intensively due to increased productivity levels.

Variable prevention costs have a direct link with production levels. Fixed prevention costs, by contrast, are not directly linked to production levels. A safety report, for example, will state where hazardous materials must be stored, but this will not have a direct effect on production. The development of company safety policy includes not only direct prevention costs, such as the application and implementation of safety material, but also indirect prevention costs such as development and training of employees and maintenance of the company safety management system.

A non-exhaustive list of prevention costs is as follows:

- staffing costs of company HSE department;

- staffing costs for the rest of the personnel (time needed to implement safety measures, time required to read working procedures and safety procedures, etc.);

- procurement and maintenance costs of safety equipment (e.g., fire hoses, fire extinguishers, emergency lighting, cardiac defibrillators, pharmacy equipment);

- costs related to training and education with respect to working safely;

- costs related to preventive audits and inspections;

- costs related to exercises, drills, simulations with respect to safety (e.g., evacuation exercises, etc.);

- a variety of administrative costs;

- prevention-related costs for early replacements of installation parts, and so on;

- maintenance of machine park, tools, and so on;

- good housekeeping;

- investigation of near-misses and incidents.

In contrast to quantifying hypothetical benefits, companies are usually very experienced in calculating direct and indirect (non-hypothetical) costs of preventive measures.

4.4 The Degree of Safety and the Minimum Overall Cost Point

As Fuller and Vassie [70] indicate, the overall (or total) cost of a company safety policy will be directly related to an organization's standards for health and safety, and thus its degree of safety. The higher the company's health and safety standards and its degree of safety, the greater the prevention costs, and the lower the accident costs within the company. Prevention costs will rise exponentially as the degree of safety increases, because of the law of diminishing returns, which describes the difficulties of trying to achieve the last small improvements in performance. If a company has already made huge prevention investments, and the company is thus performing very well on health and safety, it becomes ever more difficult to further improve its health and safety performance with one extra “unit” (in economics also called “marginal” improvement). On the contrary, the accident costs will decrease exponentially as the degree of safety improves because, as the accident rate is reduced, and hence accident costs are decreased, there is ever less potential for further (accident reduction) improvements (see Figure 4.8).

Figure 4.8 Prevention costs and accident costs as a function of the degree of safety (qualitative figure).

From a purely microeconomic viewpoint, a cost-effective company will choose to establish a degree of safety that allows it to operate at the minimum total cost point. Figure 4.8 illustrates this reasoning. At this point, the prevention costs are balanced by the accident costs, and at first sight the “optimal safety policy” (from a microeconomic point of view) is realized. It is important that for this exercise to deliver results that are as accurate as possible, the calculation of both prevention costs and accident costs should be as complete as possible, and all direct and indirect, visible and invisible, costs should be taken into account. However, Figure 4.8 indicates that, in an optimal cost-effective situation, one should not strive for a zero-accident situation. But is this really always the case? As will be explained further, this is possibly not always the case.

As it happens, an observation is that companies who have aspired to zero accidents globally over very long periods are still in business, and indeed even highly profitable. Their safety and profitability records are usually better than those with fatalistic beliefs that some accidents are inevitable and that they should/can be considered part of the cost-effectiveness policy of the company. Figure 4.8 was actually first produced in the quality management context and originally looked like Figure 4.9. Despite the reasoning that an optimum overall cost point is not at zero accident level, many manufacturers that did aim for zero quality defects (no matter the theory) largely achieved their aims, despite what is shown in Figure 4.9.

Figure 4.9 Conventional cost-benefit analysis for determining the tolerable accident level in quality management.

Panopoulos and Booth [78] sought to challenge the conclusions drawn from Figure 4.9, namely that zero accidents could “never” be the optimum outcome. To this end, they assumed that the starting point of prevention costs for a safety minimum overall cost graph needs to be zero accidents, achieved at finite cost, not infinite cost (as this must also be true in real industrial practice). From that initiating point, the trends in accident and prevention costs as accident numbers increase may be explored. It should be noted that the novel presentation method is not profound. Its key purpose is to challenge the existing ideas regarding the minimum overall cost curve (cf. Booth [79]).

Figures 4.10 and 4.11 present graphical minimum overall cost curves, assuming finite values of prevention costs for zero accidents.

Figure 4.10 Conventional cost-benefit analysis (Figure 4.9 redrawn) showing zero accidents as not the optimum case.

Figure 4.11 Conventional cost-benefit analysis showing zero accidents as the optimum case.

Figure 4.11 shows the case where zero accidents offer the cheapest option. Everything turns on the relationship between accident and preventive costs as the number of accidents goes up, and where the minimum overall cost lies.

What, then, are the factors that determine whether Figure 4.10 or 4.11 applies? Figure 4.10 is identical to Figure 4.9 but drawn in a different way, as in the latter the cost of each accident is relatively modest, and prevention costs rise dramatically as zero is approached. This might typically be where safety expenditure is not cost-effective. In contrast, Figure 4.11 shows zero accidents as the optimum case. Here each accident is more expensive than shown in Figure 4.10, and the costs of moving from a small number of accidents to zero are relatively modest. A question that arises is: what are the practical circumstances where zero accidents is the minimum cost option?

As Booth [79] explains, the arguments for zero quality defects provides the clue, but also the challenge. Frequent, albeit minor, quality defects threaten sales (and product safety, where the effects can be catastrophic). Moreover, quality management was revolutionized when the change was made from rectifying defects “at the end of the production line” to the more cost-effective approach of quality checks being incorporated into every task – so achieving zero defects at the end of the line via a dramatically better preventive approach. Returning to accidents, zero accidents are more likely to offer the best business case where the costs of an accident are high, as with type II events. Hence, Figure 4.11 provides a good argument for zero type II events or zero major accidents, while the pursuit of zero type I events or zero occupational accidents should be treated like Figure 4.10. In summary, using a cost-benefit analysis to determine a minimum overall cost is only suitable for one type of risk (type I risks) and not for other risks (type II). But the cost-benefit exercise results will still be largely improvable, and the next paragraph and section explain why and how.

Earlier in this section, the phrase “from a microeconomic point of view” was mentioned, due to the fact that victim costs and societal costs should, in principle, also be taken into account in the overall/total costs calculations. If only microeconomic factors are important for an organization, only accident costs related to the organization are considered by the company, and not the victim and societal costs. Hence, even if all direct and indirect accident costs are determined by an organization, there will be an underestimation of the full economic costs, due to individual and macroeconomic costs. True accident costs are composed of the organizational costs, as well as the costs to the victim and to society.

Organizations should thus make a distinction between the different types of risk, and between real accident costs and hypothetical benefits. Costs of accidents that happened (“accident costs”) and costs of accidents that were avoided and never happened (“hypothetical benefits” due to non-events) are completely different in nature: many more non-events happen than accidents. Nonetheless, their analogy is clear and therefore they are easily confused when making safety cost-benefit considerations. Curves such as those in Figure 4.8 are only valid for type I risks, as the curve of “accident costs” (displaying the costs related to a certain degree of safety) can only be empirically determined if a large number of accidents happened, and thus if sufficient data are available. It is impossible to determine empirically the costs of disasters linked to a certain degree of safety, simply because not that many catastrophes happen, which would be necessary to obtain sufficient information to draw such a curve. Hence, the curves displayed in Figure 4.8 cannot be drawn – and should not be used – for type II risks. At best, a thought experiment can be conducted, with a resulting Figure 4.11 being applicable to type II events.

4.5 The Type I and Type II Accident Pyramids

Heinrich [80], Bird [81], and James and Fullman [82], among other researchers, mentioned the existence of a ratio relationship between the numbers of incidents with no visible injury or damage, and those with property damage, those with minor injuries, and those with major injuries. This accident ratio relationship is known as “the accident pyramid” or “the safety triangle.” Figure 4.12 illustrates such an accident pyramid (or safety triangle). Accident pyramids unambiguously indicate that accidents with higher consequences are “announced” by accidents with lesser consequences. Hence the importance of, among other things, awareness and incident analyses for safety managers.

Figure 4.12 The Bird accident pyramid (“Egyptian”).

Studies [80–82] found different ratios (varying from 1 : 300 to 1 : 600), depending on the industrial sector, the area of research, cultural aspects, and so on. Although the statistical relationship between the different levels of the pyramid has never been proven, the existence of the accident pyramid obviously has merits from a qualitative point of view. From a qualitative interpretation of the pyramid, it could be possible to prevent serious accidents by taking preventive measures aimed at near misses, minor accidents, and so on. Hence, these “classic” accident pyramids clearly provide an insight into type I accidents, where a lot of data are at hand. In brief, the assumptions of the “old” safety paradigm emanating from the accident pyramid (see Figure 4.12) hold that:

- 1. As injuries increase in severity, their number decreases in frequency.

- 2. All injuries of low severity have the same potential for serious injury.

- 3. Injuries of differing severity have the same underlying causes.

- 4. One injury reduction strategy will reach all kinds of injuries equally (i.e., reducing minor injuries by 20% will also reduce major injuries by 20%).

Using injury statistics, Krause [83] indicated that while minor injuries may decline in companies, serious injuries can remain the same, hence casting credible doubts on the validity of the safety pyramid concept. In fact, research indicated that only some 20% (21% to be precise) of the type I incidents have the potential to lead to a serious type I accident. This finding implies that if one focuses only on “the other 80%” of the type I incidents (i.e., the 80% of the incidents that are unlikely to lead to serious injury), the causative factors that create potential serious accidents will continue to exist and so will the serious accidents themselves.

Therefore, Krause [83] proposed a “new” safety paradigm with the following assumptions:

- 1. All minor injuries are not the same in their potential for serious injury or fatality. A subset of low severity injuries come from exposures that act as a precursor to serious accidents.

- 2. Injuries of differing severity have differing underlying causes.

- 3. Reducing serious injuries requires a different strategy than reducing less serious injuries.

- 4. The strategy for reducing serious injuries should use precursor data derived from accidents, injuries, near misses, and exposure.

Based on research by Krause [83] on the different types of uncertainties/risks available, and on several disasters (such as the BP Texas City Refinery disaster of 2005), the classic pyramid shape thus needed to be refined and improved. Instead of an “Egyptian” pyramid shape, such as the classic accident pyramid studies suggest, the shape should rather be a “Mayan” one, as illustrated in Figure 4.13.

Figure 4.13 Mayan accident pyramid shape.

(Source: Meyer and Reniers [73]. Reproduced with permission from De Gruyter.)