CHAPTER 5

Accounting for Merchandising Operations

FEATURE STORY

Who Doesn’t Shop?

Carrefour, headquartered in France, is the largest retailer in Europe and the second largest retailer in the world. While 40% of its sales are in France, it operates stores under a variety of names in 32 countries in Europe, Asia, and Latin America, such as Carrefour Express, Dity, Ed, Minipreco, and Promocash. Its nearly 10,000 stores employ 471,000 people and generate sales of €112 billion.

Becoming an international titan hasn’t always been easy. Carrefour has enjoyed some successful mergers and acquisitions. But, it has also experienced setbacks, including a failed effort to acquire a giant Brazilian retailer. It has had some success in increasing market share in emerging markets. But, by far the largest share of its sales are in Europe, which has experienced low consumer confidence in recent years due to the recession and debt crisis. As a result, Carrefour’s increases in emerging markets have only served to offset declines in Europe.

Management has experienced upheaval, with three new chief executive officers during a seven-year period. Investors in recent years have withdrawn support for the company, resulting in a drop in Carrefour’s share price of two-thirds in less than five years. At times, the company has struggled strategically. Recently, it decided to quit using temporary price cuts to promote products. Instead, Carrefour sets prices low on certain key items. It also decided to not set its prices as low as those of bargain stores, such as E.Leclerc (FRA). Carrefour’s management felt that the additional services the company provides would enable it to charge slightly higher prices than bargain stores without losing customers. However, poor economic conditions made consumers extremely price-conscious. As a result, the company has seen a significant drop in customer traffic.

Nobody said retailing is easy, but at number two in the world, Carrefour has no intention of throwing in the towel. The company recently launched a makeover of 500 superstores in Europe, and it continues to look for expansion opportunities in countries that have good growth opportunities. Recently, the company opened its first store in India. Lars Olofsson, CEO of Carrefour, declared: “The opening of this first store marks Carrefour’s entry into the Indian market and will be followed shortly by the opening of other Cash & Carry stores. This first step is essential to allow the Carrefour teams to fully understand the specificities of the Indian market and then build our presence in other formats.”

PREVIEW OF CHAPTER 5

Merchandising is one of the largest and most influential industries in the world. It is likely that a number of you will work for a merchandiser. Therefore, understanding the financial statements of merchandising companies is important. In this chapter, you will learn the basics about reporting merchandising transactions. In addition, you will learn how to prepare and analyze a commonly used form of the income statement. The content and organization of the chapter are as follows.

Merchandising Operations

Learning Objective 1

Identify the differences between service and merchandising companies.

Metro (DEU), Carrefour (FRA), and Tesco (GBR) are called merchandising companies because they buy and sell merchandise rather than perform services as their primary source of revenue. Merchandising companies that purchase and sell directly to consumers are called retailers. Merchandising companies that sell to retailers are known as wholesalers. For example, retailer Walgreens (USA) might buy goods from wholesaler Grupo Casa SA de CV (MEX). Retailer Office Depot (USA) might buy office supplies from wholesaler Corporate Express (NLD). The primary source of revenues for merchandising companies is the sale of merchandise, often referred to simply as sales revenue or sales. A merchandising company has two categories of expenses: cost of goods sold and operating expenses.

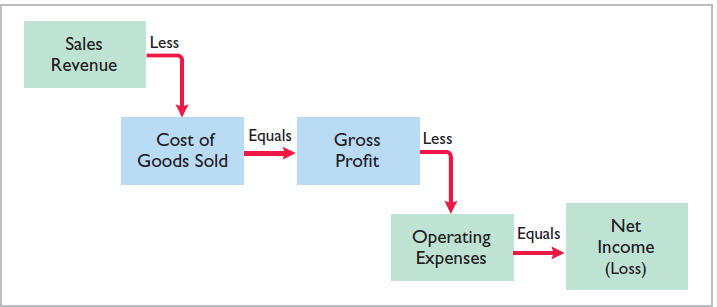

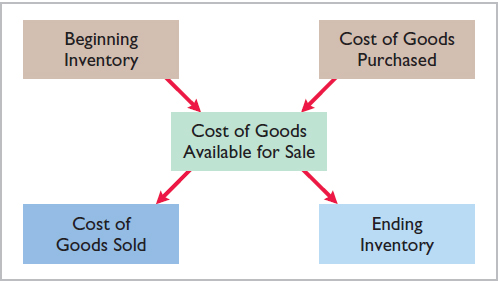

Cost of goods sold is the total cost of merchandise sold during the period. This expense is directly related to the revenue recognized from the sale of goods. Illustration 5-1 shows the income measurement process for a merchandising company. The items in the two blue boxes are unique to a merchandising company; they are not used by a service company.

Illustration 5-1 Income measurement process for a merchandising company

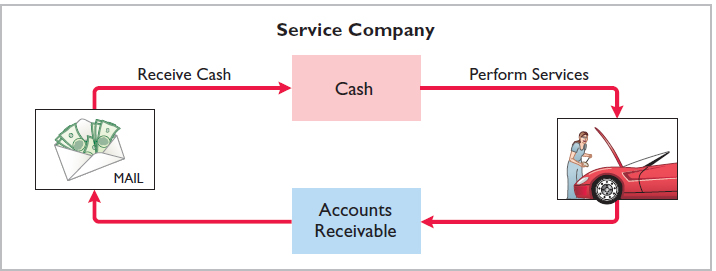

Operating Cycles

The operating cycle of a merchandising company ordinarily is longer than that of a service company. The purchase of merchandise inventory and its eventual sale lengthen the cycle. Illustration 5-2 shows the operating cycle of a service company.

Illustration 5-2 Operating cycle for a service company

Illustration 5-3 shows the operating cycle of a merchandising company.

Illustration 5-3 Operating cycle for a merchandising company

Note that the added asset account for a merchandising company is the Inventory account. Companies report inventory as a current asset on the statement of financial position.

Flow of Costs

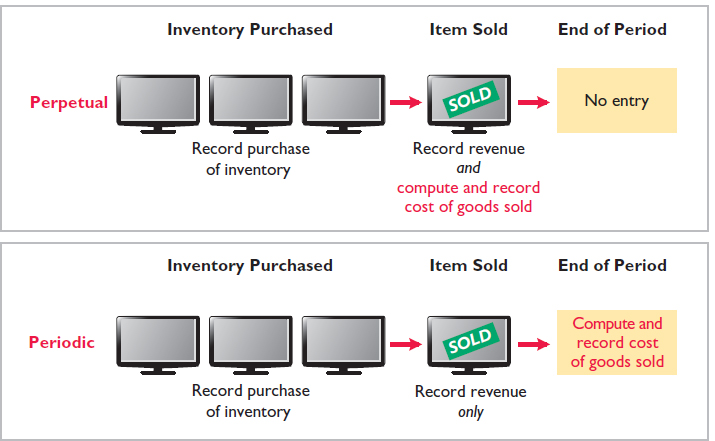

The flow of costs for a merchandising company is as follows. Beginning inventory plus the cost of goods purchased is the cost of goods available for sale. As goods are sold, they are assigned to cost of goods sold. Those goods that are not sold by the end of the accounting period represent ending inventory. Illustration 5-4 describes these relationships. Companies use one of two systems to account for inventory: a perpetual inventory system or a periodic inventory system.

Illustration 5-4 Flow of costs

• HELPFUL HINT

For control purposes, companies take a physical inventory count under the perpetual system even though it is not needed to determine cost of goods sold.

PERPETUAL SYSTEM

In a perpetual inventory system, companies keep detailed records of the cost of each inventory purchase and sale. These records continuously—perpetually—show the inventory that should be on hand for every item. For example, a Toyota (JPN) dealership has separate inventory records for each automobile, truck, and van on its lot and showroom floor. Similarly, a Morrisons (GBR) grocery store uses bar codes and optical scanners to keep a daily running record of every box of cereal and every jar of jelly that it buys and sells. Under a perpetual inventory system, a company determines the cost of goods sold each time a sale occurs.

PERIODIC SYSTEM

In a periodic inventory system, companies do not keep detailed inventory records of the goods on hand throughout the period. Instead, they determine the cost of goods sold only at the end of the accounting period—that is, periodically. At that point, the company takes a physical inventory count to determine the cost of goods on hand.

To determine the cost of goods sold under a periodic inventory system, the following steps are necessary:

- Determine the cost of goods on hand at the beginning of the accounting period.

- Add to it the cost of goods purchased.

- Subtract the cost of goods on hand at the end of the accounting period.

Illustration 5-5 graphically compares the sequence of activities and the timing of the cost of goods sold computation under the two inventory systems.

Illustration 5-5 Comparing perpetual and periodic inventory systems

ADVANTAGES OF THE PERPETUAL SYSTEM

Companies that sell merchandise with high unit values, such as automobiles, furniture, and major home appliances, have traditionally used perpetual systems. The growing use of computers and electronic scanners has enabled many more companies to install perpetual inventory systems. The perpetual inventory system is so named because the accounting records continuously—perpetually—show the quantity and cost of the inventory that should be on hand at any time.

A perpetual inventory system provides better control over inventories than a periodic system. Since the inventory records show the quantities that should be on hand, the company can count the goods at any time to see whether the amount of goods actually on hand agrees with the inventory records. If shortages are uncovered, the company can investigate immediately. Although a perpetual inventory system requires both additional clerical work and expense to maintain the subsidiary records, a computerized system can minimize this cost.

Some businesses find it either unnecessary or uneconomical to invest in a computerized perpetual inventory system. Many small merchandising businesses find that basic accounting software provides some of the essential benefits of a perpetual inventory system. Also, managers of some small businesses still find that they can control their merchandise and manage day-to-day operations using a periodic inventory system.

Because of the widespread use of the perpetual inventory system, we illustrate it in this chapter. We discuss and illustrate the periodic system in Appendix 5B.

Recording Purchases of Merchandise

Learning Objective 2

Explain the recording of purchases under a perpetual inventory system.

Companies purchase inventory using cash or credit (on account). They normally record purchases when they receive the goods from the seller. Every purchase should be supported by business documents that provide written evidence of the transaction. Each cash purchase should be supported by a canceled check or a cash register receipt indicating the items purchased and amounts paid. Companies record cash purchases by an increase in Inventory and a decrease in Cash.

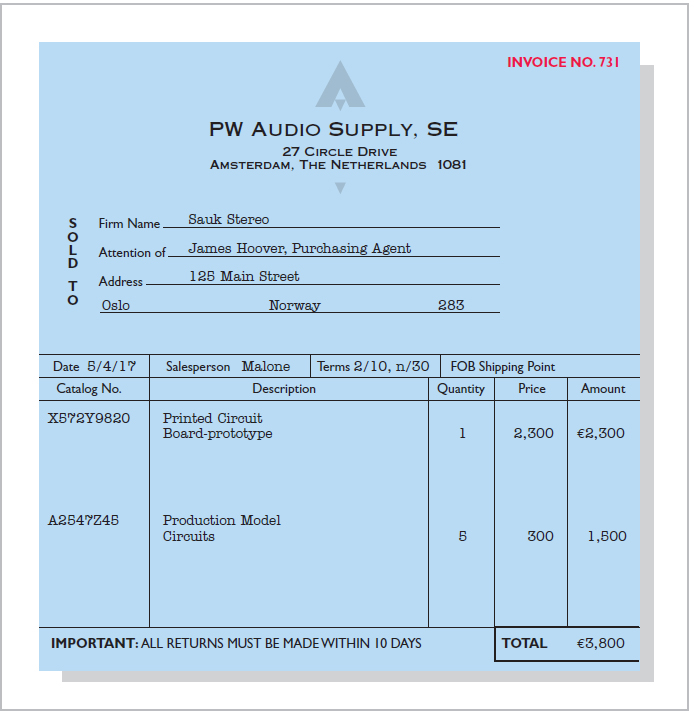

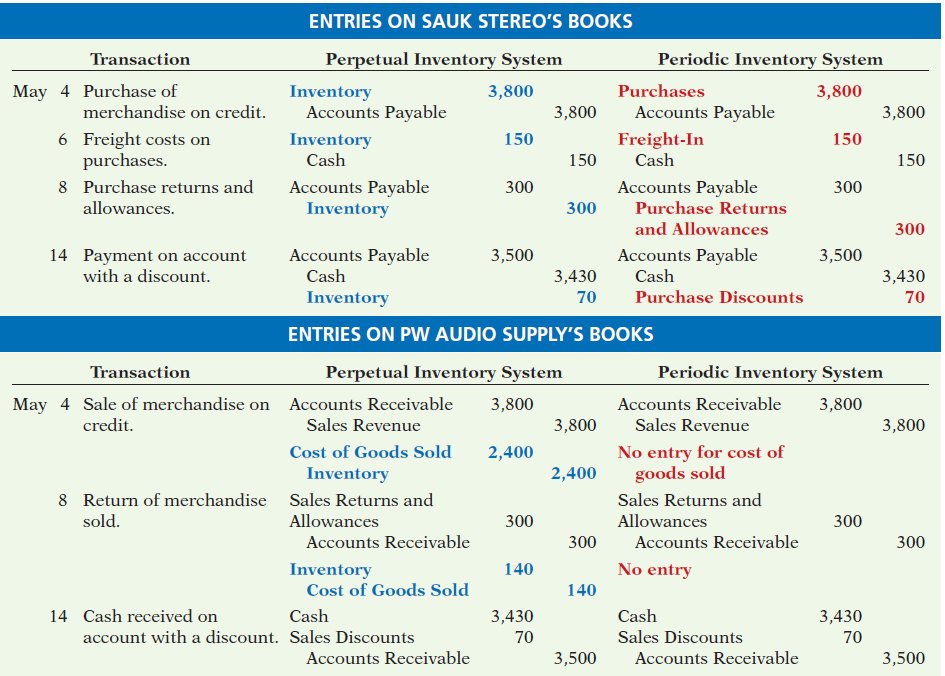

A purchase invoice should support each credit purchase. This invoice indicates the total purchase price and other relevant information. However, the purchaser does not prepare a separate purchase invoice. Instead, the purchaser uses as a purchase invoice a copy of the sales invoice sent by the seller. In Illustration 5-6, for example, Sauk Stereo (the buyer) uses as a purchase invoice the sales invoice prepared by PW Audio Supply, SE (the seller).

Illustration 5-6 Sales invoice used as purchase invoice by Sauk Stereo

• HELPFUL HINT

To better understand the contents of this invoice, identify these items:

- Seller

- Invoice date

- Purchaser

- Salesperson

- Credit terms

- Freight terms

- Goods sold: catalog number, description, quantity, price per unit

- Total invoice amount

Sauk Stereo makes the following journal entry to record its purchase from PW Audio Supply. The entry increases (debits) Inventory and increases (credits) Accounts Payable.

Under the perpetual inventory system, companies record purchases of merchandise for sale in the Inventory account. Thus, Carrefour would increase (debit) Inventory for clothing, sporting goods, and anything else purchased for resale to customers.

Not all purchases are debited to Inventory, however. Companies record purchases of assets acquired for use and not for resale, such as supplies, equipment, and similar items, as increases to specific asset accounts rather than to Inventory. For example, to record the purchase of materials used to make shelf signs or for cash register receipt paper, Carrefour would increase (debit) Supplies.

Freight Costs

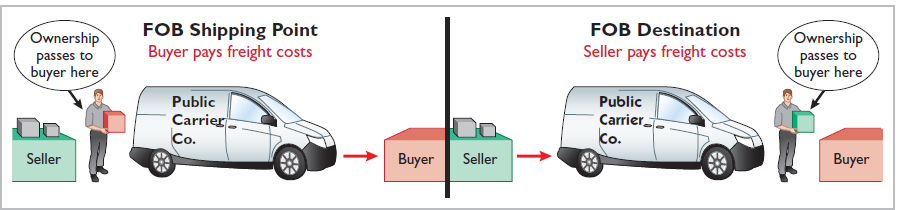

The sales agreement should indicate who—the seller or the buyer—is to pay for transporting the goods to the buyer’s place of business. When a common carrier such as a railroad, trucking company, or airline transports the goods, the carrier prepares a freight bill in accord with the sales agreement.

Freight terms are expressed as either FOB shipping point or FOB destination. The letters FOB mean free on board. Thus, FOB shipping point means that the seller places the goods free on board the carrier, and the buyer pays the freight costs. Conversely, FOB destination means that the seller places the goods free on board to the buyer’s place of business, and the seller pays the freight. For example, the sales invoice in Illustration 5-6 indicates FOB shipping point. Thus, the buyer (Sauk Stereo) pays the freight charges. Illustration 5-7 illustrates these shipping terms.

Illustration 5-7 Shipping terms

FREIGHT COSTS INCURRED BY THE BUYER

When the buyer incurs the transportation costs, these costs are considered part of the cost of purchasing inventory. Therefore, the buyer debits (increases) the Inventory account. For example, if Sauk Stereo (the buyer) pays Acme Freight Company €150 for freight charges on May 6, the entry on Sauk Stereo’s books is:

Thus, any freight costs incurred by the buyer are part of the cost of merchandise purchased. The reason: Inventory cost should include all costs to acquire the inventory, including freight necessary to deliver the goods to the buyer. Companies recognize these costs as cost of goods sold when the inventory is sold.

FREIGHT COSTS INCURRED BY THE SELLER

In contrast, freight costs incurred by the seller on outgoing merchandise are an operating expense to the seller. These costs increase an expense account titled Freight-Out (sometimes called Delivery Expense). For example, if the freight terms on the invoice in Illustration 5-6 had required PW Audio Supply (the seller) to pay the freight charges, the entry by PW Audio Supply would be:

When the seller pays the freight charges, the seller will usually establish a higher invoice price for the goods to cover the shipping expense.

Purchase Returns and Allowances

A purchaser may be dissatisfied with the merchandise received because the goods are damaged or defective, of inferior quality, or do not meet the purchaser’s specifications. In such cases, the purchaser may return the goods to the seller for credit if the sale was made on credit, or for a cash refund if the purchase was for cash. This transaction is known as a purchase return. Alternatively, the purchaser may choose to keep the merchandise if the seller is willing to grant an allowance (deduction) from the purchase price. This transaction is known as a purchase allowance.

Assume that Sauk Stereo returned goods costing €300 to PW Audio Supply on May 8. The following entry by Sauk Stereo for the returned merchandise decreases (debits) Accounts Payable and decreases (credits) Inventory.

Because Sauk Stereo increased Inventory when the goods were received, Inventory is decreased when Sauk Stereo returns the goods (or when it is granted an allowance).

Suppose instead that Sauk Stereo chose to keep the goods after being granted a €50 allowance (reduction in price). It would reduce (debit) Accounts Payable and reduce (credit) Inventory for €50.

Purchase Discounts

The credit terms of a purchase on account may permit the buyer to claim a cash discount for prompt payment. The buyer calls this cash discount a purchase discount. This incentive offers advantages to both parties: The purchaser saves money, and the seller is able to shorten the operating cycle by converting the accounts receivable into cash.

• HELPFUL HINT

The term net in “net 30” means the remaining amount due after subtracting any sales returns and allowances and partial payments.

Credit terms specify the amount of the cash discount and time period in which it is offered. They also indicate the time period in which the purchaser is expected to pay the full invoice price. In the sales invoice in Illustration 5-6 (page 224), credit terms are 2/10, n/30, which is read “two-ten, net thirty.” This means that the buyer may take a 2% cash discount on the invoice price less (“net of”) any returns or allowances, if payment is made within 10 days of the invoice date (the discount period). Otherwise, the invoice price, less any returns or allowances, is due 30 days from the invoice date.

Alternatively, the discount period may extend to a specified number of days following the month in which the sale occurs. For example, 1/10 EOM (end of month) means that a 1% discount is available if the invoice is paid within the first 10 days of the next month.

When the seller elects not to offer a cash discount for prompt payment, credit terms will specify only the maximum time period for paying the balance due. For example, the invoice may state the time period as n/30, n/60, or n/10 EOM. This means, respectively, that the buyer must pay the net amount in 30 days, 60 days, or within the first 10 days of the next month.

When the buyer pays an invoice within the discount period, the amount of the discount decreases Inventory. Why? Because companies record inventory at cost, and by paying within the discount period, the buyer has reduced its cost. To illustrate, assume Sauk Stereo pays the balance due of €3,500 (gross invoice price of €3,800 less purchase returns and allowances of €300) on May 14, the last day of the discount period. The cash discount is €70 , and Sauk Stereo pays €3,430 . The entry Sauk Stereo makes to record its May 14 payment decreases (debits) Accounts Payable by the amount of the gross invoice price, reduces (credits) Inventory by the €70 discount, and reduces (credits) Cash by the net amount owed.

If Sauk Stereo failed to take the discount and instead made full payment of €3,500 on June 3, it would debit Accounts Payable and credit Cash for €3,500 each.

A merchandising company usually should take all available discounts. Passing up the discount may be viewed as paying interest for use of the money. For example, passing up the discount offered by PW Audio Supply would be comparable to Sauk Stereo paying an interest rate of 2% for the use of €3,500 for 20 days. This is the equivalent of an annual interest rate of approximately 36.5% . Obviously, it would be better for Sauk Stereo to borrow at prevailing bank interest rates of 6% to 10% than to lose the discount.

Summary of Purchasing Transactions

The following T-account (with transaction descriptions in red) provides a summary of the effect of the previous transactions on Inventory. Sauk Stereo originally purchased €3,800 worth of inventory for resale. It then returned €300 of goods. It paid €150 in freight charges, and finally, it received a €70 discount off the balance owed because it paid within the discount period. This results in a balance in Inventory of €3,580.

Recording Sales of Merchandise

Learning Objective 3

Explain the recording of sales revenues under a perpetual inventory system.

In accordance with the revenue recognition principle, companies record sales revenue when the performance obligation is satisfied. Typically, the performance obligation is satisfied when the goods transfer from the seller to the buyer. At this point, the sales transaction is complete and the sales price established.

Sales may be made on credit or for cash. A business document should support every sales transaction, to provide written evidence of the sale. Cash register documents provide evidence of cash sales. A sales invoice, like the one shown in Illustration 5-6 (page 224), provides support for a credit sale. The original copy of the invoice goes to the customer, and the seller keeps a copy for use in recording the sale. The invoice shows the date of sale, customer name, total sales price, and other relevant information.

The seller makes two entries for each sale. The first entry records the sale: The seller increases (debits) Cash (or Accounts Receivable, if a credit sale), and also increases (credits) Sales Revenue. The second entry records the cost of the merchandise sold: The seller increases (debits) Cost of Goods Sold, and also decreases (credits) Inventory for the cost of those goods. As a result, the Inventory account will show at all times the amount of inventory that should be on hand.

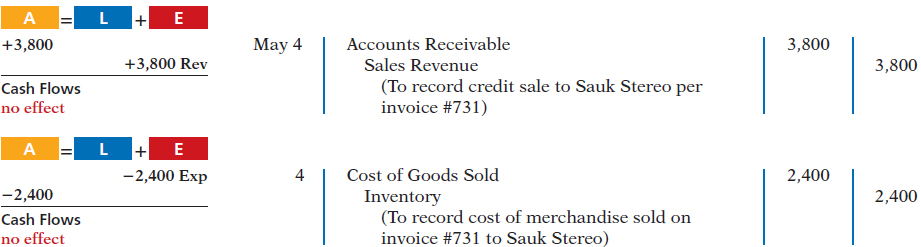

To illustrate a credit sales transaction, PW Audio Supply records its May 4 sale of €3,800 to Sauk Stereo (see Illustration 5-6) as follows (assume the merchandise cost PW Audio Supply €2,400).

For internal decision-making purposes, merchandising companies may use more than one sales account. For example, PW Audio Supply may decide to keep separate sales accounts for its sales of TVs, Blu-ray players, and headsets. Carrefour might use separate accounts for sporting goods, children’s clothing, and hardware—or it might have even more narrowly defined accounts. By using separate sales accounts for major product lines, rather than a single combined sales account, company management can more closely monitor sales trends and respond more strategically to changes in sales patterns. For example, if TV sales are increasing while Blu-ray player sales are decreasing, PW Audio Supply might reevaluate both its advertising and pricing policies on these items to ensure they are optimal.

On its income statement presented to outside investors, a merchandising company normally would provide only a single sales figure—the sum of all of its individual sales accounts. This is done for two reasons. First, providing detail on all of its individual sales accounts would add considerable length to its income statement. Second, most companies do not want their competitors to know the details of their operating results. However, Microsoft (USA) at one point expanded its disclosure of revenue from three to five types. The reason: The additional categories will better enable financial statement users to evaluate the growth of the company’s consumer and Internet businesses.

Sales Returns and Allowances

We now look at the “flip side” of purchase returns and allowances, which the seller records as sales returns and allowances. These are transactions where the seller either accepts goods back from the buyer (a return) or grants a reduction in the purchase price (an allowance) so the buyer will keep the goods. PW Audio Supply’s entries to record credit for returned goods involve (1) an increase (debit) in Sales Returns and Allowances (a contra account to Sales Revenue) and a decrease (credit) in Accounts Receivable at the €300 selling price, and (2) an increase (debit) in Inventory (assume a €140 cost) and a decrease (credit) in Cost of Goods Sold, as shown below (assuming that the goods were not defective).

If Sauk Stereo returns goods because they are damaged or defective, then PW Audio Supply’s entry to Inventory and Cost of Goods Sold should be for the fair value of the returned goods, rather than their cost. For example, if the returned goods were defective and had a fair value of €50, PW Audio Supply would debit Inventory for €50, and would credit Cost of Goods Sold for €50.

What happens if the goods are not returned but the seller grants the buyer an allowance by reducing the purchase price? In this case, the seller debits Sales Returns and Allowances and credits Accounts Receivable for the amount of the allowance. An allowance has no impact on Inventory or Cost of Goods Sold.

Sales Returns and Allowances is a contra revenue account to Sales Revenue. This means that it is offset against a revenue account on the income statement. The normal balance of Sales Returns and Allowances is a debit. Companies use a contra account, instead of debiting Sales Revenue, to disclose in the accounts and in the income statement the amount of sales returns and allowances. Disclosure of this information is important to management: Excessive returns and allowances may suggest problems—inferior merchandise, inefficiencies in filling orders, errors in billing customers, or delivery or shipment mistakes. Moreover, a decrease (debit) recorded directly to Sales Revenue would obscure the relative importance of sales returns and allowances as a percentage of sales. It also could distort comparisons between total sales in different accounting periods.

Sales Discounts

As mentioned in our discussion of purchase transactions, the seller may offer the customer a cash discount—called by the seller a sales discount—for the prompt payment of the balance due. Like a purchase discount, a sales discount is based on the invoice price less returns and allowances, if any. The seller increases (debits) the Sales Discounts account for discounts that are taken. For example, PW Audio Supply makes the following entry to record the cash receipt on May 14 from Sauk Stereo within the discount period.

Like Sales Returns and Allowances, Sales Discounts is a contra revenue account to Sales Revenue. Its normal balance is a debit. PW Audio Supply uses this account, instead of debiting Sales Revenue, to disclose the amount of cash discounts taken by customers. If Sauk Stereo does not take the discount, PW Audio Supply increases (debits) Cash for €3,500 and decreases (credits) Accounts Receivable for the same amount at the date of collection.

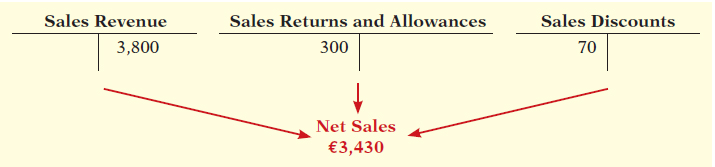

The following T-accounts summarize the three sales-related transactions and show their combined effect on net sales.

Completing the Accounting Cycle

Learning Objective 4

Explain the steps in the accounting cycle for a merchandising company.

Up to this point, we have illustrated the basic entries for transactions relating to purchases and sales in a perpetual inventory system. Now we consider the remaining steps in the accounting cycle for a merchandising company. Each of the required steps described in Chapter 4 for service companies apply to merchandising companies. Appendix 5A to this chapter shows the use of a worksheet by a merchandiser (an optional step).

Adjusting Entries

A merchandising company generally has the same types of adjusting entries as a service company. However, a merchandiser using a perpetual system will require one additional adjustment to make the records agree with the actual inventory on hand. Here’s why: At the end of each period, for control purposes, a merchandising company that uses a perpetual system will take a physical count of its goods on hand. The company’s unadjusted balance in Inventory usually does not agree with the actual amount of inventory on hand. The perpetual inventory records may be incorrect due to recording errors, theft, or waste. Thus, the company needs to adjust the perpetual records to make the recorded inventory amount agree with the inventory on hand. This involves adjusting Inventory and Cost of Goods Sold.

For example, suppose that PW Audio Supply, SE has an unadjusted balance of €40,500 in Inventory. Through a physical count, PW Audio Supply determines that its actual merchandise inventory at December 31 is €40,000. The company would make an adjusting entry as follows.

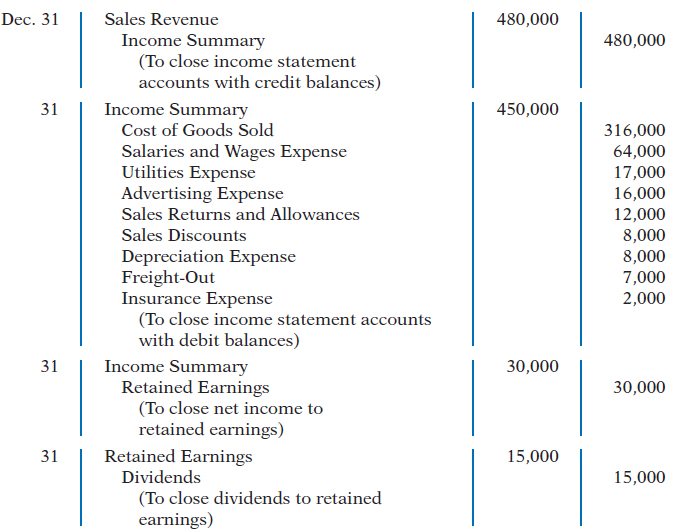

Closing Entries

A merchandising company, like a service company, closes to Income Summary all accounts that affect net income. In journalizing, the company credits all temporary accounts with debit balances, and debits all temporary accounts with credit balances, as shown below for PW Audio Supply. Note that PW Audio Supply closes Cost of Goods Sold to Income Summary.

• HELPFUL HINT

The easiest way to prepare the first two closing entries is to identify the temporary accounts by their balances and then prepare one entry for the credits and one for the debits.

After PW Audio Supply has posted the closing entries, all temporary accounts have zero balances. Also, Retained Earnings has a balance that is carried over to the next period.

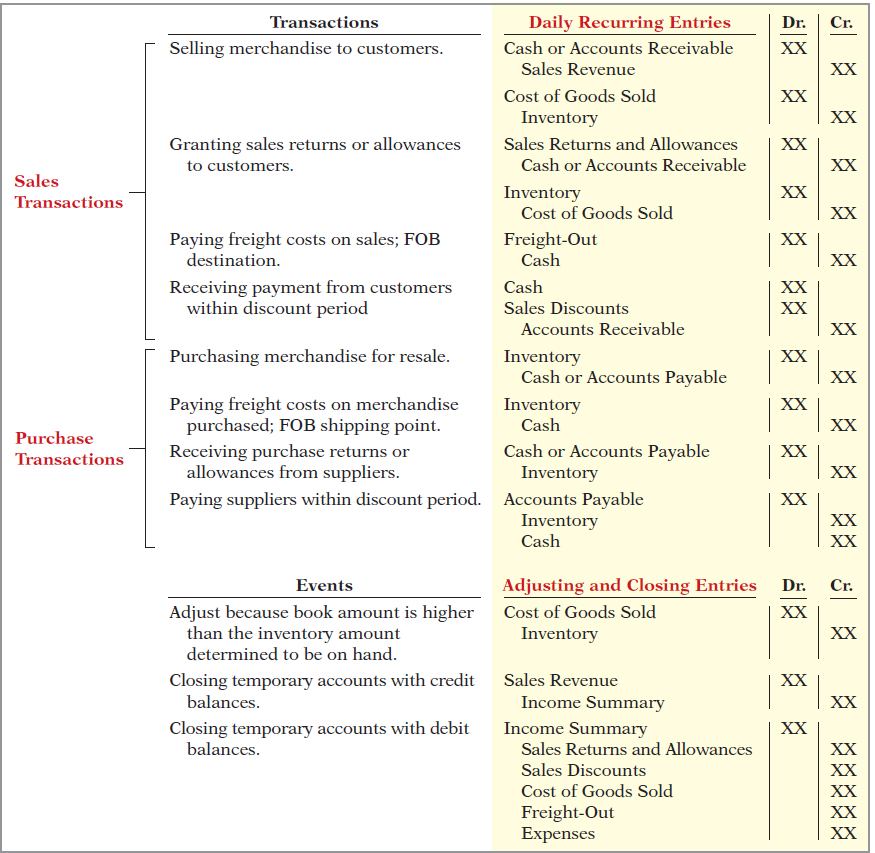

Summary of Merchandising Entries

Illustration 5-8 summarizes the entries for the merchandising accounts using a perpetual inventory system.

Illustration 5-8 Daily recurring and adjusting and closing entries

Forms of Financial Statements

Learning Objective 5

Prepare an income statement for a merchandiser.

Merchandising companies widely use the classified statement of financial position introduced in Chapter 4. This section explains an income statement used by merchandisers.

Income Statement

The income statement is a primary source of information for evaluating a company’s performance. The format is designed to differentiate between the various sources of income and expense.

INCOME STATEMENT PRESENTATION OF SALES

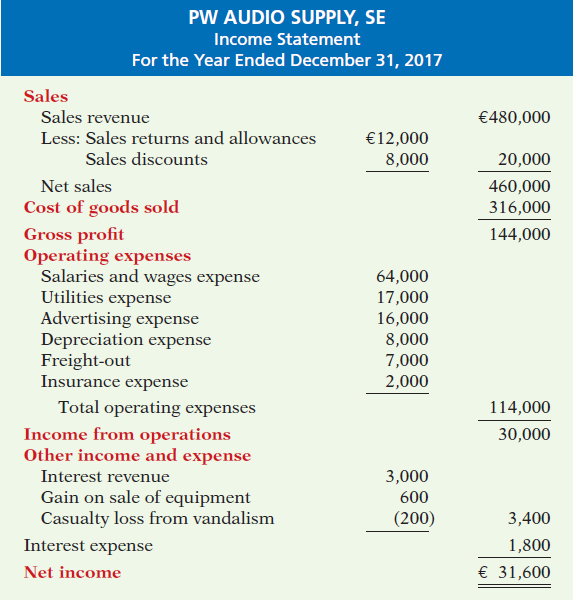

The income statement begins by presenting sales revenue. It then deducts contra revenue accounts—sales returns and allowances and sales discounts—from sales revenue to arrive at net sales. Illustration 5-9 presents the sales section for PW Audio Supply, using assumed data.

Illustration 5-9 Computation of net sales

| PW AUDIO SUPPLY, SE Income Statement (partial) |

||||

| Sales | ||||

| Sales revenue | €480,000 |

|||

| Less: Sales returns and allowances | €12,000 |

|||

| Sales discounts | 8,000 |

20,000 |

||

| Net sales | €460,000 |

|||

This presentation discloses the key data about the company’s principal revenue-producing activities.

GROSS PROFIT

From Illustration 5-1 (page 220), you learned that companies deduct cost of goods sold from sales revenue in order to determine gross profit. For this computation, companies use net sales (which takes into consideration Sales Returns and Allowances and Sales Discounts) as the amount of sales revenue. On the basis of the sales data in Illustration 5-9 (net sales of €460,000) and cost of goods sold under the perpetual inventory system (assume €316,000), PW Audio Supply’s gross profit is €144,000, computed as follows.

Illustration 5-10 Computation of gross profit

| Net sales | €460,000 |

| Cost of goods sold | 316,000 |

| Gross profit | €144,000 |

We also can express a company’s gross profit as a percentage, called the gross profit rate. To do so, we divide the amount of gross profit by net sales. For PW Audio Supply, the gross profit rate is 31.3%, computed as follows.

Illustration 5-11 Gross profit rate formula and computation

Analysts generally consider the gross profit rate to be more useful than the gross profit amount. The rate expresses a more meaningful (qualitative) relationship between net sales and gross profit. For example, a gross profit of €1,000,000 may sound impressive. But if it is the result of a gross profit rate of only 7% when others in the industry get 20%, it is not so impressive. The gross profit rate tells how much of each euro of sales go to gross profit.

Gross profit represents the merchandising profit of a company. It is not a measure of the overall profitability, because operating expenses are not yet deducted. But managers and other interested parties closely watch the amount and trend of gross profit. They compare current gross profit with amounts reported in past periods. They also compare the company’s gross profit rate with rates of competitors and with industry averages. Such comparisons provide information about the effectiveness of a company’s purchasing function and the soundness of its pricing policies.

OPERATING EXPENSES

Operating expenses are the next component in the income statement of a merchandising company. They are the expenses incurred in the process of earning sales revenue. Many of these expenses are similar in merchandising and service companies. At PW Audio Supply, operating expenses were €114,000. This €114,000 includes costs that were incurred for salaries, utilities, advertising, depreciation, freight-out, and insurance. The presentation of operating expenses is shown in Illustration 5-12.

Illustration 5-12 Operating expenses

| Operating expenses | |||

| Salaries and wages expense | € 64,000 |

||

| Utilities expense | 17,000 |

||

| Advertising expense | 16,000 |

||

| Depreciation expense | 8,000 |

||

| Freight-out | 7,000 |

||

| Insurance expense | 2,000 |

||

| Total operating expenses | €114,000 |

||

Illustration 5-12 provides an opportunity to discuss two different presentation formats allowed by IFRS: presentation by nature and presentation by function. Presentation by nature provides very detailed information, with numerous line items, that reveal the nature of costs incurred by the company. In Illustration 5-12, the detailed information regarding costs incurred for salaries and wages, utilities, advertising, depreciation, freight-out, and insurance demonstrates presentation by nature.

Presentation by function aggregates costs into groupings based on the primary functional activities in which the company engages. For example, at PW Audio Supply, operating expenses are those costs incurred to perform the operating functions of a merchandising business. If PW Audio Supply chose to present strictly by function, it would present its operating expenses as a single line item of €114,000. However, if a presentation by function is used, IFRS requires disclosure of additional details regarding the nature of certain expenses that were included in the functional grouping. For example, depreciation and salary and wage costs are items specifically required to be disclosed.

Illustration 5-12 combines both a presentation by function and by nature to present operating expenses. It uses a functional grouping of operating expenses but also presents in detail the nature of the costs included in that functional grouping. In your homework, you should use this approach.

OTHER INCOME AND EXPENSE

Other income and expense consists of various revenues and gains and expenses and losses that are unrelated to the company’s main line of operations. Illustration 5-13 lists examples of each.

Illustration 5-13 Examples of other income and expense

| Other Income |

|

Interest revenue from notes receivable and marketable securities. Dividend revenue from investments in ordinary shares. Rent revenue from subleasing a portion of the store. Gain from the sale of property, plant, and equipment. |

| Other Expense |

|

Casualty losses from such causes as vandalism and accidents. Loss from the sale or abandonment of property, plant, and equipment. Loss from strikes by employees and suppliers. |

Merchandising companies report other income and expense in the income statement immediately after the company’s primary operating activities. Illustration 5-14 shows this presentation for PW Audio Supply.

INTEREST EXPENSE

Financing activities, which result in interest expense, represent distinctly different types of cost to a business. In evaluating the performance of a business, it is important to monitor its interest expense. As a consequence, interest expense, if material, must be disclosed on the face of the income statement. PW Audio Supply incurred interest expense of €1,800. Illustration 5-14 presents a complete income statement for PW Audio Supply. Use this format when preparing your homework.

Illustration 5-14 Income statement

COMPREHENSIVE INCOME

Chapter 1 discussed the fair value principle. IFRS requires companies to mark the recorded values of certain types of assets and liabilities to their fair values at the end of each reporting period. In some instances, the unrealized gains or losses that result from adjusting recorded amounts to fair value are included in net income. However, in other cases, these unrealized gains and losses are not included in net income. Instead, these excluded items are reported as part of a more inclusive earnings measure, called comprehensive income. Examples of such items include certain adjustments to pension plan assets, gains and losses on foreign currency translation, and unrealized gains and losses on certain types of investments. As shown in Chapter 1, items that are excluded from net income but included in comprehensive income are either reported in a combined statement of net income and comprehensive income, or in a separate schedule that reports only comprehensive income. Illustration 5-15 shows how comprehensive income is presented in a separate comprehensive income statement. Use this format when preparing your homework.

Illustration 5-15 Separate statement of net income and comprehensive income

| PW AUDIO SUPPLY, SE Comprehensive Income Statement For the Year Ended December 31, 2017 |

||||

| Net income | €31,600 | |||

| Other comprehensive income | ||||

| Unrealized holding gain on investment securities | 2,300 |

|||

| Comprehensive income | €33,900 |

|||

Inventory Presentation in the Classified Statement of Financial Position

In the statement of financial position, merchandising companies report inventory as a current asset immediately above accounts receivable. Recall from Chapter 4 that companies generally list current asset items in the reverse order of their closeness to cash (liquidity). Inventory is less close to cash than accounts receivable because the goods must first be sold and then collection made from the customer. Illustration 5-16 presents the assets section of a classified statement of financial position for PW Audio Supply.

Illustration 5-16 Assets section of a classified statement of financial position

| PW AUDIO SUPPLY, SE Statement of Financial Position (Partial) December 31, 2017 |

||||

| Assets | ||||

| Property, plant, and equipment | ||||

| Equipment | €80,000 |

|||

| Less: Accumulated depreciation—equipment | 24,000 |

€ 56,000 |

||

| Current assets | ||||

| Prepaid insurance | 1,800 |

|||

| Inventory | 40,000 |

|||

| Accounts receivable | 16,100 |

|||

| Cash | 9,500 |

67,400 |

||

| Total assets | €123,400 |

|||

• HELPFUL HINT

The €40,000 is the cost of the inventory on hand, not its expected selling price.

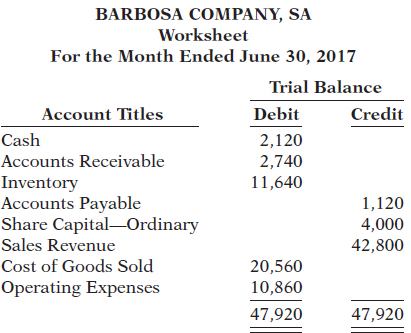

APPENDIX 5A Worksheet for a Merchandising Company

Learning Objective *6

Prepare a worksheet for a merchandising company.

Using a Worksheet

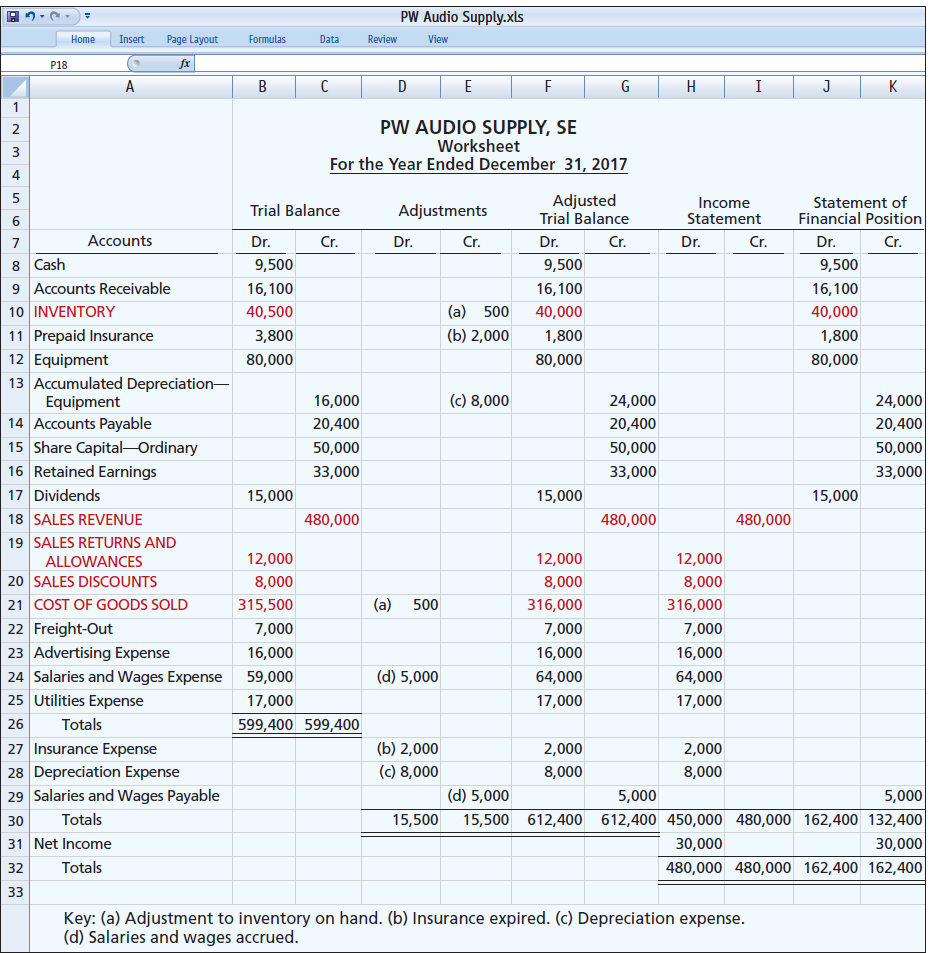

As indicated in Chapter 4, a worksheet enables companies to prepare financial statements before they journalize and post adjusting entries. The steps in preparing a worksheet for a merchandising company are the same as for a service company (see pages 162–165). Illustration 5-17 shows the worksheet for PW Audio Supply (excluding non-operating items). The unique accounts for a merchandiser using a perpetual inventory system are shown in capital red letters. This worksheet assumes that the company did not have comprehensive income.

Illustration 5A-1 Worksheet for merchandising company

TRIAL BALANCE COLUMNS

Data for the trial balance come from the ledger balances of PW Audio Supply at December 31. The amount shown for Inventory, €40,500, is the year-end inventory amount from the perpetual inventory system.

ADJUSTMENTS COLUMNS

A merchandising company generally has the same types of adjustments as a service company. As you see in the worksheet, adjustments (b), (c), and (d) are for insurance, depreciation, and salaries and wages. Yazici Advertising A.Ş., as illustrated in Chapters 3 and 4, also had these adjustments. Adjustment (a) was required to adjust the perpetual inventory carrying amount to the actual count.

After PW Audio Supply enters all adjustments data on the worksheet, it establishes the equality of the adjustments column totals. It then extends the balances in all accounts to the adjusted trial balance columns.

ADJUSTED TRIAL BALANCE

The adjusted trial balance shows the balance of all accounts after adjustment at the end of the accounting period.

INCOME STATEMENT COLUMNS

Next, the merchandising company transfers the accounts and balances that affect the income statement from the adjusted trial balance columns to the income statement columns. PW Audio Supply shows sales of €480,000 in the credit column. It shows the contra revenue accounts Sales Returns and Allowances €12,000 and Sales Discounts €8,000 in the debit column. The difference of €460,000 is the net sales shown on the income statement (Illustration 5-14, page 237).

Finally, the company totals all the credits in the income statement column and compares those totals to the total of the debits in the income statement column. If the credits exceed the debits, the company has net income. PW Audio Supply has net income of €30,000. If the debits exceed the credits, the company would report a net loss.

STATEMENT OF FINANCIAL POSITION COLUMNS

The major difference between the statements of financial position of a service company and a merchandiser is inventory. PW Audio Supply shows the ending inventory amount of €40,000 in the statement of financial position debit column. The information to prepare the retained earnings statement is also found in these columns. That is, the retained earnings beginning balance is €33,000. Dividends are €15,000. Net income results when the total of the debit column exceeds the total of the credit column in the statement of financial position columns. A net loss results when the total of the credits exceeds the total of the debit balances.

APPENDIX 5B Periodic Inventory System

Learning Objective *7

Explain the recording of purchases and sales of inventory under a periodic inventory system.

As described in this chapter, companies may use one of two basic systems of accounting for inventories: (1) the perpetual inventory system or (2) the periodic inventory system. In the chapter, we focused on the characteristics of the perpetual inventory system. In this appendix, we discuss and illustrate the periodic inventory system. One key difference between the two systems is the point at which the company computes cost of goods sold. For a visual reminder of this difference, refer back to Illustration 5-5 (on page 222).

Determining Cost of Goods Sold Under a Periodic System

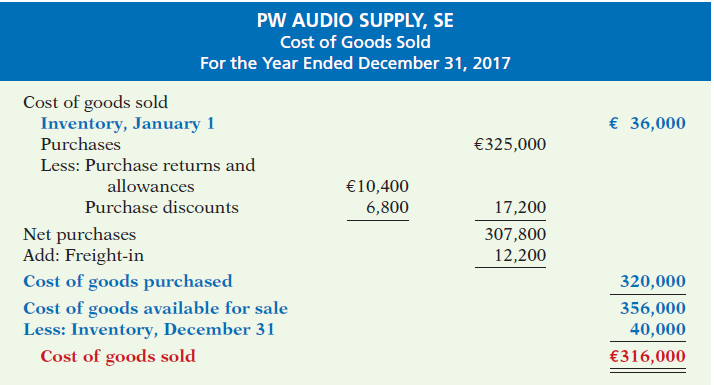

Determining cost of goods sold is different when a periodic inventory system is used rather than a perpetual system. As you have seen, a company using a perpetual system makes an entry to record cost of goods sold and to reduce inventory each time a sale is made. A company using a periodic system does not determine cost of goods sold until the end of the period. At the end of the period the company performs a count to determine the ending balance of inventory. It then calculates cost of goods sold by subtracting ending inventory from the cost of goods available for sale. Goods available for sale is the sum of beginning inventory plus cost of goods purchased, as shown in Illustration 5-18.

Illustration 5B-1 Basic formula for cost of goods sold using the periodic system

Another difference between the two approaches is that the perpetual system directly adjusts the Inventory account for any transaction that affects inventory (such as freight costs, returns, and discounts). The periodic system does not do this. Instead, it creates different accounts for purchases, freight costs, returns, and discounts. These various accounts are shown in Illustration 5-19, which presents the calculation of cost of goods sold for PW Audio Supply using the periodic approach.

Illustration 5B-2 Cost of goods sold for a merchandiser using a periodic inventory system

• HELPFUL HINT

The far right column identifies the primary items that make up cost of goods sold of €316,000. The middle column explains cost of goods purchased of €320,000. The left column reports contra purchase items of €17,200.

Note that the basic elements from Illustration 5-18 are highlighted in Illustration 5-19. You will learn more in Chapter 6 about how to determine cost of goods sold using the periodic system.

The use of the periodic inventory system does not affect the form of presentation in the statement of financial position. As under the perpetual system, a company reports inventory in the current assets section.

Recording Merchandise Transactions

In a periodic inventory system, companies record revenues from the sale of merchandise when sales are made, just as in a perpetual system. Unlike the perpetual system, however, companies do not attempt on the date of sale to record the cost of the merchandise sold. Instead, they take a physical inventory count at the end of the period to determine (1) the cost of the merchandise then on hand and (2) the cost of the goods sold during the period. And, under a periodic system, companies record purchases of merchandise in the Purchases account rather than the Inventory account. Also, in a periodic system, purchase returns and allowances, purchase discounts, and freight costs on purchases are recorded in separate accounts.

To illustrate the recording of merchandise transactions under a periodic inventory system, we will use purchase/sales transactions between PW Audio Supply, SE and Sauk Stereo, as illustrated for the perpetual inventory system in this chapter.

Recording Purchases of Merchandise

On the basis of the sales invoice (Illustration 5-6, shown on page 224) and receipt of the merchandise ordered from PW Audio Supply, Sauk Stereo records the €3,800 purchase as follows.

• HELPFUL HINT

Be careful not to debit purchases of equipment or supplies to a Purchases account.

Purchases is a temporary account whose normal balance is a debit.

FREIGHT COSTS

When the purchaser directly incurs the freight costs, it debits the account Freight-In (or Transportation-In). For example, if Sauk Stereo pays Acme Freight Company €150 for freight charges on its purchase from PW Audio Supply on May 6, the entry on Sauk Stereo’s books is:

Like Purchases, Freight-In is a temporary account whose normal balance is a debit. Freight-In is part of cost of goods purchased. The reason is that cost of goods purchased should include any freight charges necessary to bring the goods to the purchaser. Freight costs are not subject to a purchase discount. Purchase discounts apply only to the invoice cost of the merchandise.

• Alternative Terminology

Freight-in is also called transportation-in.

PURCHASE RETURNS AND ALLOWANCES

Sauk Stereo returns €300 of goods to PW Audio Supply and prepares the following entry to recognize the return.

Purchase Returns and Allowances is a temporary account whose normal balance is a credit.

PURCHASE DISCOUNTS

On May 14, Sauk Stereo pays the balance due on account to PW Audio Supply, taking the 2% cash discount allowed by PW Audio Supply for payment within 10 days. Sauk Stereo records the payment and discount as follows.

Purchase Discounts is a temporary account whose normal balance is a credit.

Recording Sales of Merchandise

The seller, PW Audio Supply, records the sale of €3,800 of merchandise to Sauk Stereo on May 4 (sales invoice No. 731, Illustration 5-6, page 224) as follows.

SALES RETURNS AND ALLOWANCES

To record the returned goods received from Sauk Stereo on May 8, PW Audio Supply records the €300 sales return as follows.

SALES DISCOUNTS

On May 14, PW Audio Supply receives payment of €3,430 on account from Sauk Stereo. PW Audio Supply honors the 2% cash discount and records the payment of Sauk Stereo’s account receivable in full as follows.

COMPARISON OF ENTRIES—PERPETUAL VS. PERIODIC

Illustration 5-20 summarizes the periodic inventory entries shown in this appendix and compares them to the perpetual-system entries from the chapter. Entries that differ in the two systems are shown in color.

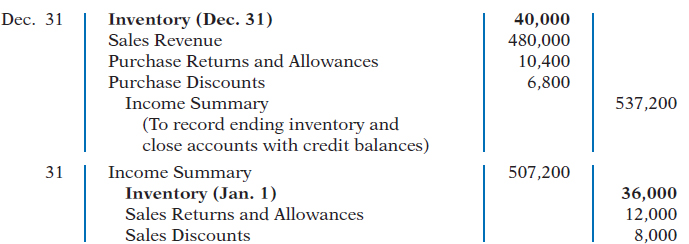

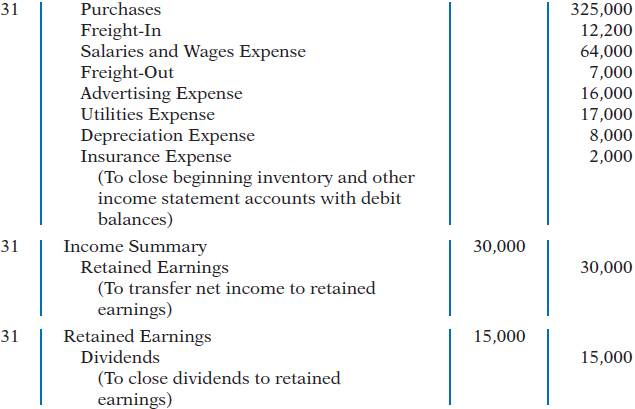

Journalizing and Posting Closing Entries

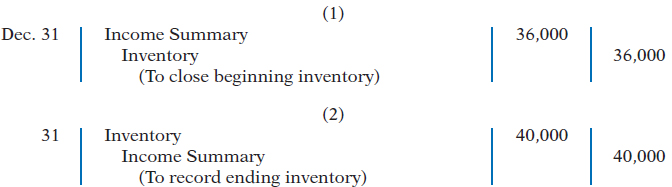

For a merchandising company, like a service company, all accounts that affect the determination of net income are closed to Income Summary. Data for the preparation of closing entries may be obtained from the income statement columns of the worksheet. In journalizing, all debit column amounts are credited, and all credit columns amounts are debited. To close the merchandise inventory in a periodic inventory system:

- The beginning inventory balance is debited to Income Summary and credited to Inventory.

- The ending inventory balance is debited to Inventory and credited to Income Summary.

The two entries for PW Audio Supply are as follows.

Illustration 5B-3 Comparison of entries for perpetual and periodic inventory systems

After posting, the Inventory and Income Summary accounts will show the following.

Illustration 5B-4 Posting closing entries for merchandise inventory

Often, the closing of Inventory is included with other closing entries, as shown on the next page for PW Audio Supply. (Close Inventory with other accounts in homework problems unless stated otherwise.)

• HELPFUL HINT

Except for merchandise inventory, the easiest way to prepare the first two closing entries is to identify the temporary accounts by their balances and then prepare one entry for the credits and one for the debits.

After the closing entries are posted, all temporary accounts have zero balances. In addition, Retained Earnings has a credit balance of €48,000: .

Using a Worksheet

As indicated in Chapter 4, a worksheet enables companies to prepare financial statements before journalizing and posting adjusting entries. The steps in preparing a worksheet for a merchandising company are the same as they are for a service company (see pages 162–165).

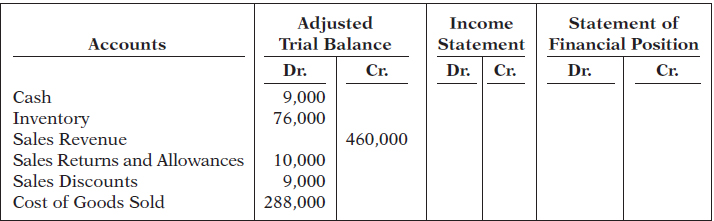

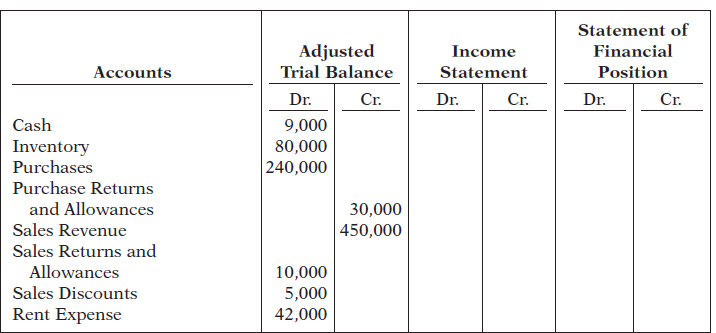

TRIAL BALANCE COLUMNS

Data for the trial balance come from the ledger balances of PW Audio Supply at December 31. The amount shown for Inventory, €36,000, is the beginning inventory amount from the periodic inventory system.

ADJUSTMENTS COLUMNS

A merchandising company generally has the same types of adjustments as a service company. As you see in the worksheet in Illustration 5-22, adjustments (a), (b), and (c) are for insurance, depreciation, and salaries and wages. These adjustments were also required for Yazici Advertising A.Ş., as illustrated in Chapters 3 and 4. The unique accounts for a merchandiser using a periodic inventory system are shown in capital red letters. Note, however, that the worksheet excludes non-operating items.

After all adjustment data are entered on the worksheet, the equality of the adjustment column totals is established. The balances in all accounts are then extended to the adjusted trial balance columns.

INCOME STATEMENT COLUMNS

Next, PW Audio Supply transfers the accounts and balances that affect the income statement from the adjusted trial balance columns to the income statement columns. The company shows Sales Revenue of €480,000 in the credit column. It shows the contra revenue accounts, Sales Returns and Allowances of €12,000 and Sales Discounts of €8,000, in the debit column. The difference of €460,000 is the net sales shown on the income statement (Illustration 5-9, page 234). Similarly, Purchases of €325,000 and Freight-In of €12,200 are extended to the debit column. The contra purchase accounts, Purchase Returns and Allowances of €10,400 and Purchase Discounts of €6,800, are extended to the credit columns.

Illustration 5B-5 Worksheet for merchandising company—periodic inventory system

The worksheet procedures for the Inventory account merit specific comment:

- The beginning balance, €36,000, is extended from the adjusted trial balance column to the income statement debit column. From there, it can be added in reporting cost of goods available for sale in the income statement.

- The ending inventory, €40,000, is added to the worksheet by an income statement credit and a statement of financial position debit. The credit makes it possible to deduct ending inventory from the cost of goods available for sale in the income statement to determine cost of goods sold. The debit means the ending inventory can be reported as an asset on the statement of financial position.

These two procedures are specifically illustrated below:

Illustration 5B-6 Worksheet procedures for inventories

The computation for cost of goods sold, taken from the income statement column in Illustration 5-22, is as follows.

Illustration 5B-7 Computation of cost of goods sold from worksheet columns

• HELPFUL HINT

In a periodic system, cost of goods sold is a computation—it is not a separate account with a balance.

Finally, PW Audio Supply totals all the credits in the income statement column and compares these totals to the total of the debits in the income statement column. If the credits exceed the debits, the company has net income. PW Audio Supply has net income of €30,000. If the debits exceed the credits, the company would report a net loss.

STATEMENT OF FINANCIAL POSITION COLUMNS

The major difference between the statements of financial position of a service company and a merchandising company is inventory. PW Audio Supply shows ending inventory of €40,000 in the statement of financial position debit column. The information to prepare the retained earnings statement is also found in these columns. That is, the retained earnings beginning balance is €33,000. Dividends are €15,000. Net income results when the total of the debit column exceeds the total of the credit column in the statement of financial position columns. A net loss results when the total of the credits exceeds the total of the debit balances.

GLOSSARY REVIEW

- Comprehensive income

- An income measure that includes gains and losses that are excluded from the determination of net income. (p. 237).

- Contra revenue account

- An account that is offset against a revenue account on the income statement. (p. 230).

- Cost of goods sold

- The total cost of merchandise sold during the period. (p. 220).

- FOB destination

- Freight terms indicating that the seller places the goods free on board to the buyer’s place of business, and the seller pays the freight. (p. 225).

- FOB shipping point

- Freight terms indicating that the seller places goods free on board the carrier, and the buyer pays the freight costs. (p. 225).

- Gross profi t

- The excess of net sales over the cost of goods sold. (p. 235).

- Gross profi t rate

- Gross profi t expressed as a percentage, by dividing the amount of gross profi t by net sales. (p. 235).

- Net sales

- Sales revenue less sales returns and allowances and less sales discounts. (p. 234).

- Operating expenses

- Expenses incurred in the process of earning sales revenue. (p. 235).

- Periodic inventory system

- An inventory system under which the company does not keep detailed inventory records throughout the accounting period but determinesthe cost of goods sold only at the end of an accounting period. (p. 222).

- Perpetual inventory system

- An inventory system under which the company keeps detailed records of the cost of each inventory purchase and sale, and the records continuously show the inventory that should be on hand. (p. 221).

- Purchase allowance

- A deduction made to the selling price of merchandise, granted by the seller so that the buyer will keep the merchandise. (p. 226).

- Purchase discount

- A cash discount claimed by a buyer for prompt payment of a balance due. (p. 226).

- Purchase invoice

- A document that supports each credit purchase. (p. 224).

- Purchase return

- A return of goods from the buyer to the seller for a cash or credit refund. (p. 226).

- Sales discount

- A reduction given by a seller for prompt payment of a credit sale. (p. 230).

- Sales invoice

- A document that supports each credit sale. (p. 228).

- Sales returns and allowances

- Purchase returns and allowances from the seller’s perspective. See Purchase return and Purchase allowance, above. (p. 229).

- Sales revenue (Sales)

- The primary source of revenue in a merchandising company. (p. 220).

PRACTICE MULTIPLE-CHOICE QUESTIONS

Gross profit will result if:

- operating expenses are less than net income.

- sales revenues are greater than operating expenses.

- sales revenues are greater than cost of goods sold.

- operating expenses are greater than cost of goods sold.

Under a perpetual inventory system, when goods are purchased for resale by a company:

- purchases on account are debited to Inventory.

- purchases on account are debited to Purchases.

- purchase returns are debited to Purchase Returns and Allowances.

- freight costs are debited to Freight-Out.

The sales accounts that normally have a debit balance are:

- Sales Discounts.

- Sales Returns and Allowances.

- Both (a) and (b).

- Neither (a) nor (b).

A credit sale of NT$7,500 is made on June 13, terms 2/10, net/30. A return of NT$500 is granted on June 16. The amount received as payment in full on June 23 is:

- NT$7,000.

- NT$6,860.

- NT$6,850.

- NT$6,500.

Which of the following accounts will normally appear in the ledger of a merchandising company that uses a perpetual inventory system?

- Purchases.

- Freight-In.

- Cost of Goods Sold.

- Purchase Discounts.

To record the sale of goods for cash in a perpetual inventory system:

- only one journal entry is necessary to record cost of goods sold and reduction of inventory.

- only one journal entry is necessary to record the receipt of cash and the sales revenue.

- two journal entries are necessary: one to record the receipt of cash and sales revenue, and one to record the cost of goods sold and reduction of inventory.

- two journal entries are necessary: one to record the receipt of cash and reduction of inventory, and one to record the cost of goods sold and sales revenue.

The steps in the accounting cycle for a merchandising company are the same as those in a service company except:

- an additional adjusting journal entry for inventory may be needed in a merchandising company.

- closing journal entries are not required for a merchandising company.

- a post-closing trial balance is not required for a merchandising company.

- an income statement is required for a merchandising company.

The income statement for a merchandising company shows each of the following features except:

- gross profit.

- cost of goods sold.

- a sales section.

- investing activities section.

If sales revenues are €400,000, cost of goods sold is €310,000, and operating expenses are €60,000, the gross profit is:

- €30,000.

- €90,000.

- €340,000.

- €400,000.

- In a worksheet using a perpetual inventory system, Inventory is shown in the following columns:

- adjusted trial balance debit and statement of financial position debit.

- income statement debit and statement of financial position debit.

- income statement credit and statement of financial position debit.

- income statement credit and adjusted trial balance debit.

- In determining cost of goods sold in a periodic system:

- purchase discounts are deducted from net purchases.

- freight-out is added to net purchases.

- purchase returns and allowances are deducted from net purchases.

- freight-in is added to net purchases.

- If beginning inventory is HK$600,000, cost of goods purchased is HK$3,800,000, and ending inventory is HK$500,000, cost of goods sold is:

- HK$3,900,000.

- HK$3,700,000.

- HK$3,300,000.

- HK$4,200,000.

- When goods are purchased for resale by a company using a periodic inventory system:

- purchases on account are debited to Inventory.

- purchases on account are debited to Purchases.

- purchase returns are debited to Purchase Returns and Allowances.

- freight costs are debited to Purchases.

Solutions

PRACTICE EXERCISES

Prepare purchase and sales entries.

- On June 10, Vareen Company purchased £8,000 of merchandise from Harrah Company, FOB shipping point, terms 3/10, n/30. Vareen pays the freight costs of £400 on June 11. Damaged goods totaling £300 are returned to Harrah for credit on June 12. The fair value of these goods in £70. On June 19, Vareen pays Harrah Company in full, less the purchase discount. Both companies use a perpetual inventory system.

Instructions

- Prepare separate entries for each transaction on the books of Vareen Company.

- Prepare separate entries for each transaction for Harrah Company. The merchandise purchased by Vareen on June 10 had cost Harrah £4,800.

Solution

Prepare an income statement.

- In its income statement for the year ended December 31, 2017, Sun Company Ltd. reported the following condensed data.

| Interest expense | NT$ 70,000 |

Net sales | NT$2,200,000 |

| Operating expenses | 725,000 |

Interest revenue | 25,000 |

| Cost of goods sold | 1,300,000 |

Loss on disposal of plant assets | 17,000 |

Instructions

Prepare an income statement.

Solution

PRACTICE PROBLEM

Prepare an income statement.

The adjusted trial balance columns of Falcetto Company SpA’s worksheet for the year ended December 31, 2017, are as follows. (All amounts are in euros.)

| Debit | Credit | ||

| Cash | 14,500 |

Accumulated Depreciation—Equipment | 18,000 |

| Accounts Receivable | 11,100 |

||

| Inventory | 29,000 |

Notes Payable | 25,000 |

| Prepaid Insurance | 2,500 |

Accounts Payable | 10,600 |

| Equipment | 95,000 |

Share Capital—Ordinary | 50,000 |

| Dividends | 12,000 |

Retained Earnings | 31,000 |

| Sales Returns and Allowances | 6,700 |

Sales Revenue | 536,800 |

| Sales Discounts | 5,000 |

Interest Revenue | 2,500 |

| Cost of Goods Sold | 363,400 |

673,900 |

|

| Freight-Out | 7,600 |

||

| Advertising Expense | 12,000 |

||

| Salaries and Wages Expense | 56,000 |

||

| Utilities Expense | 18,000 |

||

| Rent Expense | 24,000 |

||

| Depreciation Expense | 9,000 |

||

| Insurance Expense | 4,500 |

||

| Interest Expense | 3,600 |

||

673,900 |

Instructions

Prepare an income statement for Falcetto Company SpA.

Solution

| FALCETTO COMPANY SpA Income Statement For the Year Ended December 31, 2017 |

|||||

| Sales | |||||

| Sales revenue | €536,800 |

||||

| Less: Sales returns and allowances | € 6,700 |

||||

| Sales discounts | 5,000 |

11,700 |

|||

| Net sales | 525,100 |

||||

| Cost of goods sold | 363,400 |

||||

| Gross profit | 161,700 |

||||

| Operating expenses | |||||

| Salaries and wages expense | 56,000 |

||||

| Rent expense | 24,000 |

||||

| Utilities expense | 18,000 |

||||

| Advertising expense | 12,000 |

||||

| Depreciation expense | 9,000 |

||||

| Freight-out | 7,600 |

||||

| Insurance expense | 4,500 |

||||

| Total operating expenses | 131,100 |

||||

| Income from operations | 30,600 |

||||

| Other income and expense | |||||

| Interest revenue | 2,500 |

||||

| Interest expense | 3,600 |

||||

| Net income | € 29,500 |

||||

WileyPLUS

Brief Exercises, DO IT! Review, Exercises, and Problems, and many additional resources are available for practice in WileyPLUS.

NOTE: Asterisked Questions, Exercises, and Problems relate to material in the appendices to the chapter.

QUESTIONS

- “The steps in the accounting cycle for a merchandising company are different from the accounting cycle for a service company.” Do you agree or disagree?

- Is the measurement of net income for a merchandising company conceptually the same as for a service company? Explain.

Why is the normal operating cycle for a merchandising company likely to be longer than for a service company?

- How do the components of revenues and expenses differ between merchandising and service companies?

- Explain the income measurement process in a merchandising company.

How does income measurement differ between a merchandising and a service company?

When is cost of goods sold determined in a perpetual inventory system?

Distinguish between FOB shipping point and FOB destination. Identify the freight terms that will result in a debit to Inventory by the buyer and a debit to Freight-Out by the seller.

Explain the meaning of the credit terms 2/10, n/30.

Goods costing £2,500 are purchased on account on July 15 with credit terms of 2/10, n/30. On July 18, a £200 credit memo is received from the supplier for damaged goods. Give the journal entry on July 24 to record payment of the balance due within the discount period using a perpetual inventory system.

Karen Lloyd believes revenues from credit sales may be recorded before they are collected in cash. Do you agree? Explain.

- What is the primary source document for recording (1) cash sales, (2) credit sales.

- Using XXs for amounts, give the journal entry for each of the transactions in part (a).

A credit sale is made on July 10 for €700, terms 2/10, n/30. On July 12, €100 of goods are returned for credit. Give the journal entry on July 19 to record the receipt of the balance due within the discount period.

Explain why the Inventory account will usually require adjustment at year-end.

Prepare the closing entries for the Sales Revenue account, assuming a balance of €180,000 and the Cost of Goods Sold account with a €125,000 balance.

What merchandising account(s) will appear in the post-closing trial balance?

Regis Co. has sales revenue of HK$1,090,000, cost of goods sold of HK$700,000, and operating expenses of HK$230,000. What is its gross profit and its gross profit rate?

Kim Ho Company reports net sales of ¥800,000, gross profit of ¥570,000, and net income of ¥240,000. What are its operating expenses?

Identify the distinguishing features of an income statement for a merchandising company.

Identify the sections of an income statement that relate to

- operating activities, and

- non-operating activities.

-

Indicate the columns of the worksheet in which

- inventory and

- cost of goods sold will be shown using a perpetual inventory system.

-

Identify the accounts that are added to or deducted from Purchases to determine the cost of goods purchased using a periodic inventory system. For each account, indicate whether it is added or deducted.

-

Goods costing NT$60,000 are purchased on account on July 15 with credit terms of 2/10, n/30. On July 18, a NT$6,000 credit was received from the supplier for damaged goods. Give the journal entry on July 24 to record payment of the balance due within the discount period, assuming a periodic inventory system.

BRIEF EXERCISES

Compute missing amounts in determining net income.

BE5-1 Presented below are the components in Clearwater Company, Ltd.’s income statement. Determine the missing amounts.

| Sales Revenue | Cost of Goods Sold | Gross Profit | Operating Expenses | Net Income | |

| (a) | £78,000 | ? | £30,000 | ? | £10,800 |

| (b) | £108,000 | £55,000 | ? | ? | £29,500 |

| (c) | ? | £83,900 | £79,600 | £39,500 | ? |

Journalize perpetual inventory entries.

BE5-2 Giovanni Company buys merchandise on account from Gordon Company. The selling price of the goods is €780, and the cost of the goods is €560. Both companies use perpetual inventory systems. Journalize the transaction on the books of both companies.

Journalize sales transactions.

BE5-3 Prepare the journal entries to record the following transactions on Benson Company, Ltd.’s books using a perpetual inventory system.

- On March 2, Benson Company sold £800,000 of merchandise to Edgebrook Company, terms 2/10, n/30. The cost of the merchandise sold was £620,000.

- On March 6, Edgebrook Company returned £120,000 of the merchandise purchased on March 2. The cost of the returned merchandise was £90,000.

- On March 12, Benson Company received the balance due from Edgebrook Company.

Journalize purchase transactions.

BE5-4 From the information BE5-3, prepare the journal entries to record these transactions on Edgebrook Company’s books under a perpetual inventory system.

Prepare adjusting entry for merchandise inventory.

BE5-5 At year-end, the perpetual inventory records of Federer Company showed merchandise inventory of CHF98,000. The company determined, however, that its actual inventory on hand was CHF96,100. Record the necessary adjusting entry.

Prepare closing entries for accounts.

BE5-6 Orlaida Company has the following account balances: Sales Revenue €192,000, Sales Discounts €2,000, Cost of Goods Sold €105,000, and Inventory €40,000. Prepare the entries to record the closing of these items to Income Summary.

Prepare sales section of income statement.

BE5-7 Yangtze Company, Ltd. provides the following information for the month ended October 31, 2017 (amounts in Chinese yuan): sales on credit ¥280,000, cash sales ¥100,000, sales discounts ¥5,000, sales returns and allowances ¥22,000. Prepare the sales section of the income statement based on this information.

Explain presentation in an income statement.

BE5-8 ![]() Explain where each of the following items would appear on an income statement: (a) gain on sale of equipment, (b) interest expense, (c) casualty loss from vandalism, (d) cost of goods sold, and (e) depreciation expense.

Explain where each of the following items would appear on an income statement: (a) gain on sale of equipment, (b) interest expense, (c) casualty loss from vandalism, (d) cost of goods sold, and (e) depreciation expense.

Compute net sales, gross profit, income from operations, and gross profit rate.

BE5-9 Assume Jose Company has the following reported amounts: Sales revenue €506,000, Sales returns and allowances €13,000, Cost of goods sold €342,000, Operating expenses €110,000. Compute the following: (a) net sales, (b) gross profit, (c) income from operations, and (d) gross profit rate. (Round to one decimal place.)

Identify worksheet columns for selected accounts.

*BE5-10 Presented below is the format of the worksheet presented in the chapter.

Indicate where the following items will appear on the worksheet: (a) Cash, (b) Inventory, (c) Sales revenue, and (d) Cost of goods sold.

Example:

Cash: Trial balance debit column; Adjusted trial balance debit column; and Statement of financial position debit column.

Compute net purchases and cost of goods purchased.

*BE5-11 Assume that Kowloon Company uses a periodic inventory system and has these account balances (in thousands): Purchases ![]() 430,000; Purchase Returns and Allowances

430,000; Purchase Returns and Allowances ![]() 13,000; Purchase Discounts

13,000; Purchase Discounts ![]() 8,000; and Freight-In

8,000; and Freight-In ![]() 16,000. Determine net purchases and cost of goods purchased.

16,000. Determine net purchases and cost of goods purchased.

Compute cost of goods sold and gross profit.

*BE5-12 Assume the same information as in BE5-11 and also that Kowloon Company has beginning inventory (in thousands) of ![]() 60,000, ending inventory of

60,000, ending inventory of ![]() 86,000, and net sales of

86,000, and net sales of ![]() 680,000. Determine the amounts to be reported for cost of goods sold and gross profit.

680,000. Determine the amounts to be reported for cost of goods sold and gross profit.

Journalize purchase transactions.

*BE5-13 Prepare the journal entries to record these transactions on Huntington Company’s books using a periodic inventory system.

- On March 2, Huntington Company purchased £900,000 of merchandise from Saunder Company, terms 2/10, n/30.

- On March 6, Huntington Company returned £184,000 of the merchandise purchased on March 2.

- On March 12, Huntington Company paid the balance due to Saunder Company.

Prepare closing entries for merchandise accounts.

*BE5-14 A. Hall Company has the following merchandise account balances: Sales Revenue $180,000, Sales Discounts $2,000, Purchases $120,000, and Purchases Returns and Allowances $30,000. In addition, it has a beginning inventory of $40,000 and an ending inventory of $30,000. Prepare the entries to record the closing of these items to Income Summary using the periodic inventory system.

Identify worksheet columns for selected accounts.

*BE5-15 Presented below is the format of the worksheet using the periodic inventory system presented in Appendix 5B.

Indicate where the following items will appear on the worksheet: (a) Cash, (b) Beginning inventory, (c) Accounts payable, and (d) Ending inventory.

Example:

Cash: Trial balance debit column; Adjustment trial balance debit column; and Statement of financial position debit column.

EXERCISES

Answer general questions about merchandisers.

E5-1 Mr. Soukup has prepared the following list of statements about service companies and merchandisers.

- Measuring net income for a merchandiser is conceptually the same as for a service company.

- For a merchandiser, sales less operating expenses is called gross profit.

- For a merchandiser, the primary source of revenues is the sale of inventory.

- Sales salaries and wages is an example of an operating expense.

- The operating cycle of a merchandiser is the same as that of a service company.

- In a perpetual inventory system, no detailed inventory records of goods on hand are maintained.

- In a periodic inventory system, the cost of goods sold is determined only at the end of the accounting period.

- A periodic inventory system provides better control over inventories than a perpetual system.

Instructions

Identify each statement as true or false. If false, indicate how to correct the statement.

Journalize purchase transactions.

E5-2 Information related to Duffy Co., Ltd. is presented below.

- On April 5, purchased merchandise from Thomas Company, Ltd. for £25,000, terms 2/10, net/30, FOB shipping point.

- On April 6, paid freight costs of £900 on merchandise purchased from Thomas.

- On April 7, purchased equipment on account for £26,000.

- On April 8, returned damaged merchandise to Thomas and was granted a £2,600 credit for returned merchandise.

- On April 15, paid the amount due to Thomas in full.

Instructions

- Prepare the journal entries to record these transactions on the books of Duffy Co., Ltd. under a perpetual inventory system.

- Assume that Duffy Co., Ltd. paid the balance due to Thomas Company, Ltd. on May 4 instead of April 15. Prepare the journal entry to record this payment.

Journalize perpetual inventory entries.

E5-3 On September 1, Moreau Office Supply SA had an inventory of 30 calculators at a cost of €22 each. The company uses a perpetual inventory system. During September, the following transactions occurred.

| Sept. | 6 |

Purchased with cash 90 calculators at €20 each from Roux Co. SA, terms 2/10, n/30. |

9 |

Paid freight of €180 on calculators purchased from Roux Co. | |

10 |

Returned 3 calculators to Roux Co. for €66 credit (including freight) because they did not meet specifications. | |

12 |

Sold 28 calculators costing €22 (including freight) for €33 each to Village Book Store, terms n/30. | |

14 |

Granted credit of €33 to Village Book Store for the return of one calculator that was not ordered. | |

20 |

Sold 40 calculators costing €22 for €35 each to Holiday Card Shop, terms n/30. |

Instructions

Journalize the September transactions.

Prepare purchase and sales entries.

E5-4 On June 10, York Company Ltd. purchased £7,600 of merchandise from Bianchi Company, FOB shipping point, terms 2/10, n/30. York pays the freight costs of £400 on June 11. Damaged goods totaling £300 are returned to Bianchi for credit on June 12. The fair value of these goods is £70. On June 19, York pays Bianchi Company in full, less the purchase discount. Both companies use a perpetual inventory system.

Instructions

- Prepare separate entries for each transaction on the books of York Company, Ltd.

- Prepare separate entries for each transaction for Bianchi Company. The merchandise purchased by York on June 10 had cost Bianchi £4,300.

Journalize sales transactions.

E5-5 Presented below are transactions related to Li Company, Ltd.

- On December 3, Li sold HK$580,000 of merchandise to South China Co., Ltd. terms 1/10, n/30, FOB shipping point. The cost of the merchandise sold was HK$364,800.

- On December 8, South China was granted an allowance of HK$28,000 for merchandise purchased on December 3.

- On December 13, Li received the balance due from South China.

Instructions

- Prepare the journal entries to record these transactions on the books of Li Company, Ltd. using a perpetual inventory system.

- Assume that Li Company, Ltd. received the balance due from South China Co., Ltd. on January 2 of the following year instead of December 13. Prepare the journal entry to record the receipt of payment on January 2.

Prepare sales section and closing entries.

E5-6 The adjusted trial balance of Mendoza Company SLU shows the following data pertaining to sales at the end of its fiscal year October 31, 2017: Sales Revenue €820,000, Freight-Out €16,000, Sales Returns and Allowances €28,000, and Sales Discounts €13,000.

Instructions

- Prepare the sales section of the income statement.

- Prepare separate closing entries for (1) sales, and (2) the contra accounts to sales.

Prepare adjusting and closing entries.

E5-7 Hezir Company A.Ş. had the following account balances at year-end: Cost of Goods Sold ![]() 60,000, Inventory

60,000, Inventory ![]() 15,000, Operating Expenses

15,000, Operating Expenses ![]() 29,000, Sales Revenue

29,000, Sales Revenue ![]() 117,000, Sales Discounts

117,000, Sales Discounts ![]() 1,300, and Sales Returns and Allowances

1,300, and Sales Returns and Allowances ![]() 1,700. A physical count of inventory determines that merchandise inventory on hand is

1,700. A physical count of inventory determines that merchandise inventory on hand is ![]() 14,200.

14,200.

Instructions

- Prepare the adjusting entry necessary as a result of the physical count.

- Prepare closing entries.

Prepare adjusting and closing entries.

E5-8 Presented below is information related to Poulsen Industries, A/S for the month of January 2017.

| Ending inventory per perpetual records | € 21,600 |

Insurance expense | € 12,000 |

| Rent expense | 20,000 |

||

| Ending inventory actually on hand | 21,000 |