CHAPTER 8

Accounting for Receivables

FEATURE STORY

Are You Going to Pay Me—or Not?

What is the only thing harder than making a sale? Answer: Collecting the cash. Just ask a banker, virtually any banker. Bankers around the world have been awash in “doubtful” loans for years. And, it may be many years before the mess is finally cleaned up.

If your business sells most of its goods on credit or is in the business of making loans, then accurately recording your receivables is one of your most important accounting tasks. At the end of every accounting period, companies are required to estimate how many of their receivables are “uncollectible.” A significant decline in the amount of estimated doubtful loans can send a company’s share price soaring. For example, BNP Paribas (FRA) reported a decline in the estimated provision for doubtful loans of more than 50%. The market reacted very favorably, with the company’s share price rising by 5.3% in one day.

On the other hand, when a company announces an unexpected increase in its estimated doubtful loans, the securities market often reacts severely. For example, BBVA (ESP) announced that it was increasing its estimated provision for doubtful loans by €164 million. Its share price fell by 6% in a single day.

No bank is spared scrutiny of its estimated doubtful loans. In fact, it is likely that no number in a bank’s financial statements receives more careful investigation by financial analysts and investors. Nearly three years after the beginning of the financial crisis, Bank of America’s (USA) share price was still in single digits (after hitting a high of $54 per share) primarily because of investor concern regarding its provision for doubtful loans. And, on the other side of the globe, in Iran, one banker suggested that as many as 20% of the loans held by that country’s banks are doubtful.

Sources: Ben Hall, “Fall in Bad Loans Boosts BNP Paribas,” Financial Times Online (FT.com) (August 2, 2010); Tracy Alloway, “BBVA, an Exercise in Spanish Banking Losses,” Financial Times Online (FT.com) (February 3, 2011); and Najmeh Bozorgmehr, “Private Banks Open to Assist Tehran Insiders,” Financial Times Online (FT.com) (May 9, 2011).

PREVIEW OF CHAPTER 8

As indicated in the Feature Story, receivables are a significant asset for banks. Because a large portion of sales are credit sales, receivables are important to companies in other industries as well. As a consequence, companies must pay close attention to their receivables and manage them carefully. In this chapter, you will learn what journal entries companies make when they sell products, when they collect cash from those sales, and when they write off accounts they cannot collect.

The content and organization of the chapter are as follows.

The Navigator

The Navigator

Types of Receivables

Learning Objective 1

Identify the different types of receivables.

The term receivables refers to amounts due from individuals and companies. Receivables are claims that are expected to be collected in cash. The management of receivables is a very important activity for any company that sells goods or services on credit.

Receivables are important because they represent one of a company’s most liquid assets. For many companies, receivables are also one of the largest assets. Illustration 8-1 lists receivables as a percentage of total assets for five well-known companies in a recent year.

Illustration 8-1 Receivables as a percentage of assets

| Company | Receivables as a Percentage of Total Assets |

| adidas (DEU) | 16% |

| Hyundai (KOR) | 5 |

| Samsung (KOR) | 13 |

| Nestlé (CHE) | 41 |

| China Mobile Limited (HKG) | 2 |

The relative significance of a company’s receivables as a percentage of its assets depends on various factors: its industry, the time of year, whether it extends long-term financing, and its credit policies. To reflect important differences among receivables, they are frequently classified as (1) accounts receivable, (2) notes receivable, and (3) other receivables.

Accounts receivable are amounts customers owe on account. They result from the sale of goods and services. Companies generally expect to collect accounts receivable within 30 to 60 days. They are usually the most significant type of claim held by a company.

Notes receivable are a written promise (as evidenced by a formal instrument) for amounts to be received. The note normally requires the collection of interest and extends for time periods of 60–90 days or longer. Notes and accounts receivable that result from sales transactions are often called trade receivables.

Other receivables include non-trade receivables such as interest receivable, loans to company officers, advances to employees, and income taxes refundable. These do not generally result from the operations of the business. Therefore, they are generally classified and reported as separate items in the statement of financial position.

Accounts Receivable

Learning Objective 2

Explain how companies recognize accounts receivable.

Recognizing Accounts Receivable

Recognizing accounts receivable is relatively straightforward. A service organization records a receivable when it performs a service on account. A merchandiser records accounts receivable at the point of sale of merchandise on account. When a merchandiser sells goods, it increases (debits) Accounts Receivable and increases (credits) Sales Revenue.

The seller may offer terms that encourage early payment by providing a discount. Sales returns also reduce receivables. The buyer might find some of the goods unacceptable and choose to return the unwanted goods.

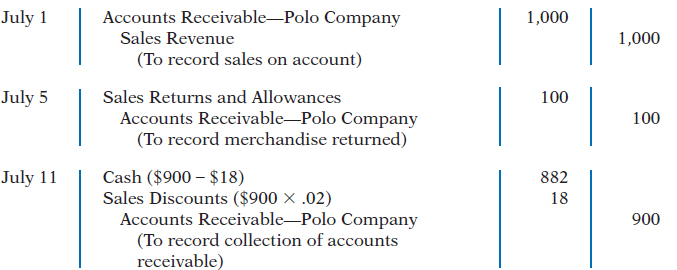

To review, assume that Hennes & Mauritz (SWE) on July 1, 2017, sells merchandise on account to Polo Company for $1,000, terms 2/10, n/30. On July 5, Polo returns merchandise with a sales price of $100 to Hennes & Mauritz. On July 11, Hennes & Mauritz receives payment from Polo Company for the balance due. The journal entries to record these transactions on the books of Hennes & Mauritz are as follows. (Cost of goods sold entries are omitted.)

• HELPFUL HINT

These entries are the same as those described in Chapter 5. For simplicity, we have omitted inventory and cost of goods sold from this set of journal entries and from end-of-chapter material.

Some retailers issue their own credit cards. When you use a retailer’s credit card (JCPenney (USA), for example), the retailer charges interest on the balance due if not paid within a specified period (usually 25–30 days).

To illustrate, assume that you use your JCPenney credit card to purchase clothing with a sales price of $300 on June 1, 2017. JCPenney will increase (debit) Accounts Receivable for $300 and increase (credit) Sales Revenue for $300 (cost of goods sold entry omitted) as follows.

Assuming that you owe $300 at the end of the month, and JCPenney charges 1.5% per month on the balance due, the adjusting entry that JCPenney makes to record interest revenue of $4.50 on June 30 is as follows.

Interest revenue is often substantial for many retailers.

Learning Objective 3

Distinguish between the methods and bases companies use to value accounts receivable.

Valuing Accounts Receivable

Once companies record receivables in the accounts, the next question is: How should they report receivables in the financial statements? Companies report accounts receivable on the statement of financial position as an asset. But determining the amount to report is sometimes difficult because some receivables will become uncollectible.

Each customer must satisfy the credit requirements of the seller before the credit sale is approved. Inevitably, though, some accounts receivable become uncollectible. For example, a customer may not be able to pay because of a decline in its sales revenue due to a downturn in the economy. Similarly, individuals may be laid off from their jobs or faced with unexpected hospital bills. Companies record credit losses as debits to Bad Debt Expense (or Uncollectible Accounts Expense). Such losses are a normal and necessary risk of doing business on a credit basis. Recently, when home prices in many parts of the world fell, home foreclosures rose and lenders experienced huge increases in their bad debt expense.

• Alternative Terminology

You will sometimes see Bad Debt Expense called Uncollectible Accounts Expense.

Two methods are used in accounting for uncollectible accounts: (1) the direct write-off method and (2) the allowance method. The following sections explain these methods.

DIRECT WRITE-OFF METHOD FOR UNCOLLECTIBLE ACCOUNTS

Under the direct write-off method, when a company determines a particular account to be uncollectible, it charges the loss to Bad Debt Expense. Assume, for example, that Warden Ltd. writes off as uncollectible M. E. Doran’s HK$1,600 balance on December 12. Warden’s entry is as follows.

Under this method, Bad Debt Expense will show only actual losses from uncollectibles. The company will report accounts receivable at its gross amount.

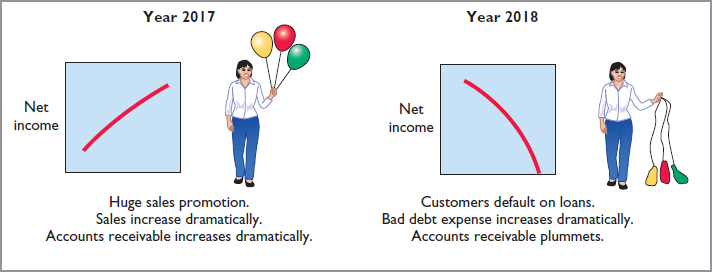

Although this method is simple, its use can reduce the usefulness of both the income statement and statement of financial position. Consider the following example. Assume that in 2017, Quick Buck Computer Ltd. decided it could increase its revenues by offering computers to college students without requiring any money down and with no credit-approval process. On campuses across the country, it distributed one million computers with a selling price of HK$6,400 each. This increased Quick Buck’s revenues and receivables by HK$6,400 million. The promotion was a huge success! The 2017 statement of financial position and income statement looked great. Unfortunately, during 2018, nearly 40% of the customers defaulted on their loans. This made the 2018 income statement and statement of financial position look terrible. Illustration 8-2 shows the effects of these events on the financial statements if the direct write-off method is used.

Illustration 8-2 Effects of direct write-off method

Under the direct write-off method, companies often record bad debt expense in a period different from the period in which they record the revenue. The method does not attempt to match bad debt expense to sales revenue in the income statement. Nor does the direct write-off method show accounts receivable in the statement of financial position at the amount the company actually expects to receive. Consequently, unless bad debt losses are insignificant, the direct write-off method is not acceptable for financial reporting purposes.

ALLOWANCE METHOD FOR UNCOLLECTIBLE ACCOUNTS

The allowance method of accounting for bad debts involves estimating uncollectible accounts at the end of each period. This provides better matching on the income statement. It also ensures that companies state receivables on the statement of financial position at their cash (net) realizable value. Cash (net) realizable value is the net amount the company expects to receive in cash.1

IFRS requires the allowance method for financial reporting purposes when bad debts are material in amount. This method has three essential features:

• HELPFUL HINT

In this context, material means significant or important to financial statement users.

- Companies estimate uncollectible accounts receivable. They match this estimated expense against revenues in the same accounting period in which they record the revenues.

- Companies debit estimated uncollectibles to Bad Debt Expense and credit them to Allowance for Doubtful Accounts through an adjusting entry at the end of each period. Allowance for Doubtful Accounts is a contra account to Accounts Receivable.

- When companies write off a specific account, they debit actual uncollectibles to Allowance for Doubtful Accounts and credit that amount to Accounts Receivable.

RECORDING ESTIMATED UNCOLLECTIBLES To illustrate the allowance method, assume that Hampson Furniture has credit sales of €1,200,000 in 2017. Of this amount, €200,000 remains uncollected at December 31. The credit manager estimates that €12,000 of these sales will be uncollectible. The adjusting entry to record the estimated uncollectibles increases (debits) Bad Debt Expense and increases (credits) Allowance for Doubtful Accounts, as follows.

Hampson reports Bad Debt Expense in the income statement as an operating expense (usually as a selling expense). Thus, the estimated uncollectibles are matched with sales in 2017. Hampson records the expense in the same year it made the sales.

Allowance for Doubtful Accounts shows the estimated amount of claims on customers that the company expects will become uncollectible in the future. Companies use a contra account instead of a direct credit to Accounts Receivable because they do not know which customers will not pay. The credit balance in the allowance account will absorb the specific write-offs when they occur. As Illustration 8-3 shows, the company deducts the allowance account from accounts receivable in the current assets section of the statement of financial position.

Illustration 8-3 Presentation of allowance for doubtful accounts

| HAMPSON FURNITURE Statement of Financial Position (partial) |

||||

| Current assets | ||||

| Supplies | € 25,000 |

|||

| Inventory | 310,000 |

|||

| Accounts receivable | €200,000 |

|||

| Less: Allowance for doubtful accounts | 12,000 |

188,000 |

||

| Cash | 14,800 |

|||

| Total current assets | €537,800 |

|||

The amount of €188,000 in Illustration 8-3 represents the expected cash realizable value of the accounts receivable at the statement date. Companies do not close Allowance for Doubtful Accounts at the end of the fiscal year.

• HELPFUL HINT

Cash realizable value is sometimes referred to as accounts receivable (net).

RECORDING THE WRITE-OFF OF AN UNCOLLECTIBLE ACCOUNT Companies use various methods of collecting past-due accounts, such as letters, calls, and legal action. When they have exhausted all means of collecting a past-due account and collection appears impossible, the company should write off the account. In the credit card industry, for example, it is standard practice to write off accounts that are 210 days past due. To prevent premature or unauthorized write-offs, authorized management personnel should formally approve each write-off. To maintain segregation of duties, the employee authorized to write off accounts should not have daily responsibilities related to cash or receivables.

To illustrate a receivables write-off, assume that the financial vice president of Hampson Furniture authorizes a write-off of the €500 balance owed by R. A. Ware on March 1, 2018. The entry to record the write-off is as follows.

Bad Debt Expense does not increase when the write-off occurs. Under the allowance method, companies debit every bad debt write-off to the allowance account rather than to Bad Debt Expense. A debit to Bad Debt Expense would be incorrect because the company has already recognized the expense when it made the adjusting entry for estimated bad debts. Instead, the entry to record the write-off of an uncollectible account reduces both Accounts Receivable and Allowance for Doubtful Accounts. After posting, the general ledger accounts appear as shown in Illustration 8-4.

Illustration 8-4 General ledger balances after write-off

A write-off affects only statement of financial position accounts—not income statement accounts. The write-off of the account reduces both Accounts Receivable and Allowance for Doubtful Accounts. Cash realizable value in the statement of financial position, therefore, remains the same, as Illustration 8-5 shows.

Illustration 8-5 Cash realizable value comparison

| Before Write-Off | After Write-Off | |

| Accounts receivable | € 200,000 |

€ 199,500 |

| Less: Allowance for doubtful accounts | 12,000 |

11,500 |

| Cash realizable value | €188,000 |

€188,000 |

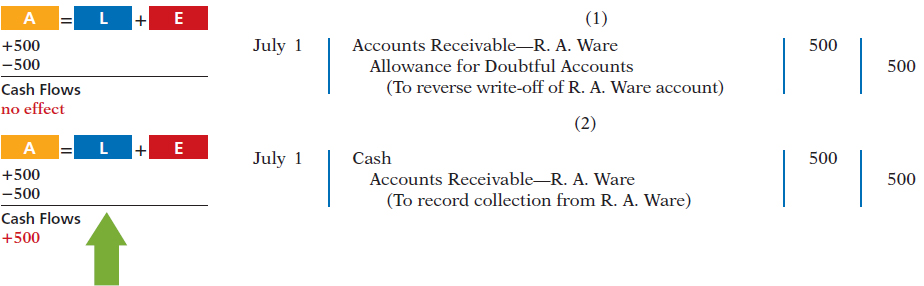

RECOVERY OF AN UNCOLLECTIBLE ACCOUNT Occasionally, a company collects from a customer after it has written off the account as uncollectible. The company makes two entries to record the recovery of a bad debt. (1) It reverses the entry made in writing off the account. This reinstates the customer’s account. (2) It journalizes the collection in the usual manner.

To illustrate, assume that on July 1, R. A. Ware pays the €500 amount that Hampson had written off on March 1. Hampson makes the following entries.

Note that the recovery of a bad debt, like the write-off of a bad debt, affects only statement of financial position accounts. The net effect of the two entries above is a debit to Cash and a credit to Allowance for Doubtful Accounts for €500. Accounts Receivable and the Allowance for Doubtful Accounts both increase in entry (1) for two reasons. First, the company made an error in judgment when it wrote off the account receivable. Second, after R. A. Ware did pay, Accounts Receivable in the general ledger and Ware’s account in the subsidiary ledger should show the collection for possible future credit purposes.

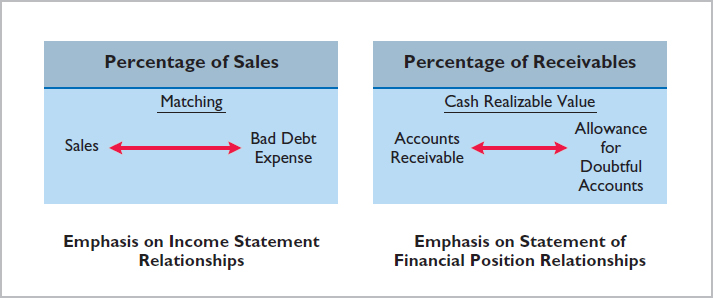

ESTIMATING THE ALLOWANCE For Hampson Furniture in Illustration 8-3, the amount of the expected uncollectibles was given. However, in “real life,” companies must estimate that amount when they use the allowance method. One of two bases is used to determine this amount: (1) percentage of sales or (2) percentage of receivables. Both bases are generally accepted. The choice is a management decision. It depends on the relative emphasis that management wishes to give to expenses and revenues on the one hand or to cash realizable value of the accounts receivable on the other. The choice is whether to emphasize income statement or statement of financial position relationships. Illustration 8-6 compares the two bases.

Illustration 8-6 Comparison of bases for estimating uncollectibles

The percentage-of-sales basis results in a better matching of expenses with revenues—an income statement viewpoint. The percentage-of-receivables basis produces the better estimate of cash realizable value—a statement of financial position viewpoint. Under both bases, the company must determine its past experience with bad debt losses.

Percentage-of-Sales. In the percentage-of-sales basis, management estimates what percentage of credit sales will be uncollectible. This percentage is based on past experience and anticipated credit policy.

The company applies this percentage to either total credit sales or net credit sales of the current year. To illustrate, assume that Gonzalez SA elects to use the percentage-of-sales basis. It concludes that 1% of net credit sales will become uncollectible. If net credit sales for 2017 are €800,000, the estimated bad debt expense is €8,000 . The adjusting entry is as follows.

After the adjusting entry is posted, assuming the allowance account already has a credit balance of €1,723, the accounts of Gonzalez SA will show the following.

Illustration 8-7 Bad debt accounts after posting

This basis of estimating uncollectibles emphasizes the matching of expenses with revenues. As a result, Bad Debt Expense will show a direct percentage relationship to the sales base on which it is computed. When the company makes the adjusting entry, it disregards the existing balance in Allowance for Doubtful Accounts. The adjusted balance in this account when netted against accounts receivable should be a reasonable approximation of the realizable value of the receivables. If actual write-offs differ significantly from the amount estimated, the company should modify the percentage for future years.

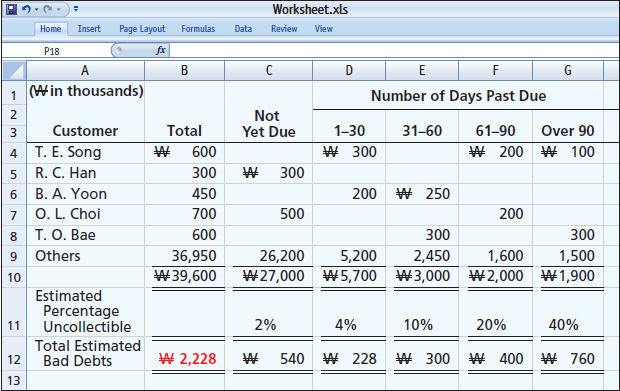

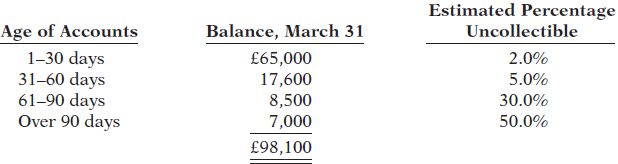

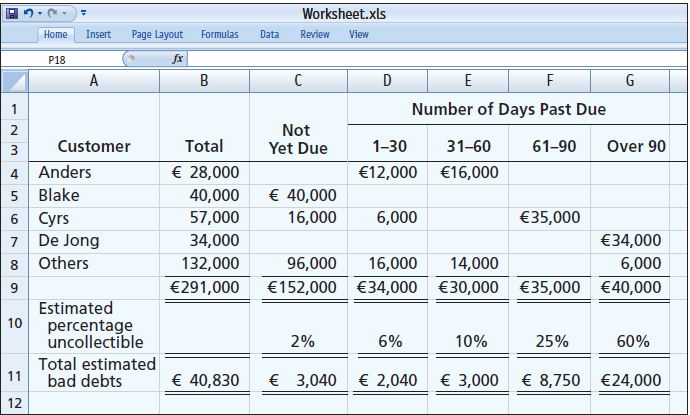

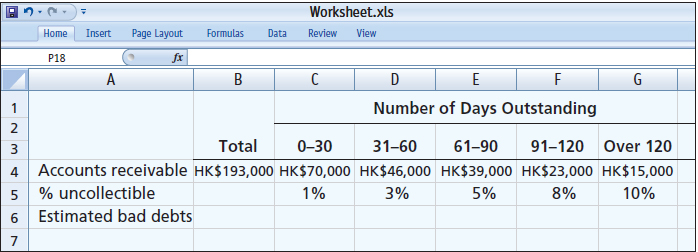

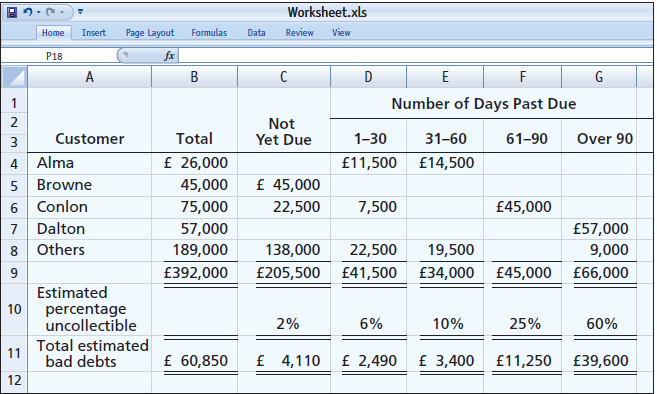

Percentage-of-Receivables. Under the percentage-of-receivables basis, management estimates what percentage of receivables will result in losses from uncollectible accounts. The company prepares an aging schedule, in which it classifies customer balances by the length of time they have been unpaid. Because of its emphasis on time, the analysis is often called aging the accounts receivable.

• HELPFUL HINT

Where appropriate, the percentage-of-receivables basis may use only a single percentage rate.

After the company arranges the accounts by age, it determines the expected bad debt losses. It applies percentages based on past experience to the totals in each category. The longer a receivable is past due, the less likely it is to be collected. Thus, the estimated percentage of uncollectible debts increases as the number of days past due increases. Illustration 8-8 (page 392) shows an aging schedule for Dart Company Ltd. Note that the estimated percentage uncollectible increases from 2% to 40% as the number of days past due increases.

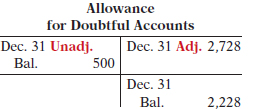

Total estimated bad debts for Dart (![]() 2,228,000) represent the amount of existing customer claims the company expects will become uncollectible in the future. This amount represents the required balance in Allowance for Doubtful Accounts at the statement of financial position date. The amount of the bad debt adjusting entry is the difference between the required balance and the existing balance in the allowance account. If the trial balance shows Allowance for Doubtful Accounts with a credit balance of

2,228,000) represent the amount of existing customer claims the company expects will become uncollectible in the future. This amount represents the required balance in Allowance for Doubtful Accounts at the statement of financial position date. The amount of the bad debt adjusting entry is the difference between the required balance and the existing balance in the allowance account. If the trial balance shows Allowance for Doubtful Accounts with a credit balance of ![]() 528,000, the company will make an adjusting entry for

528,000, the company will make an adjusting entry for ![]() 1,700,000 (

1,700,000 (![]() 2,228,000 −

2,228,000 − ![]() 528,000), as shown here (

528,000), as shown here (![]() in thousands).

in thousands).

Illustration 8-8 Aging schedule

• HELPFUL HINT

The older categories have higher percentages because the longer an account is past due, the less likely it is to be collected.

After Dart posts its adjusting entry, its accounts will appear as follows (![]() in thousands).

in thousands).

Illustration 8-9 Bad debt accounts after posting

Occasionally, the allowance account will have a debit balance prior to adjustment. This occurs when write-offs during the year have exceeded previous provisions for bad debts. In such a case, the company adds the debit balance to the required balance when it makes the adjusting entry. Thus, if there had been a ![]() 500,000 debit balance in the allowance account before adjustment, the adjusting entry would have been for

500,000 debit balance in the allowance account before adjustment, the adjusting entry would have been for ![]() 2,728,000 (

2,728,000 (![]() 2,228,000 +

2,228,000 + ![]() 500,000) to arrive at a credit balance of

500,000) to arrive at a credit balance of ![]() 2,228,000. The percentage-of-receivables basis will normally result in the better approximation of cash realizable value.

2,228,000. The percentage-of-receivables basis will normally result in the better approximation of cash realizable value.

Disposing of Accounts Receivable

Learning Objective 4

Describe the entries to record the disposition of accounts receivable.

In the normal course of events, companies collect accounts receivable in cash and remove the receivables from the books. However, as credit sales and receivables have grown in significance, the “normal course of events” has changed. Companies now frequently sell their receivables to another company for cash, thereby shortening the cash-to-cash operating cycle.

Companies sell receivables for two major reasons. First, they may be the only reasonable source of cash. When money is tight, companies may not be able to borrow money in the usual credit markets. Or, if money is available, the cost of borrowing may be prohibitive.

A second reason for selling receivables is that billing and collection are often time-consuming and costly. It is often easier for a retailer to sell the receivables to another party with expertise in billing and collection matters. Credit card companies such as MasterCard (USA) and Visa (USA) specialize in billing and collecting accounts receivable. MasterCard and Visa credit cards are issued by banks around the world, including ICBC (CHN), BNP Paribas (FRA), and Barclays (GBR).

SALE OF RECEIVABLES

A common sale of receivables is a sale to a factor. A factor is a finance company or bank that buys receivables from businesses and then collects the payments directly from the customers. Factoring is a multibillion dollar business.

Factoring arrangements vary widely. Typically, the factor charges a commission to the company that is selling the receivables. This fee ranges from 1–3% of the amount of receivables purchased. To illustrate, assume that Tsai Furniture factors NT$600,000 of receivables to Federal Factors. Federal Factors assesses a service charge of 2% of the amount of receivables sold. The journal entry to record the sale by Tsai Furniture on April 2, 2017, is as follows.

If the company often sells its receivables, it records the service charge expense (such as that incurred by Tsai) as a selling expense. If the company infrequently sells receivables, it may report this amount in the “Other income and expense” section of the income statement.

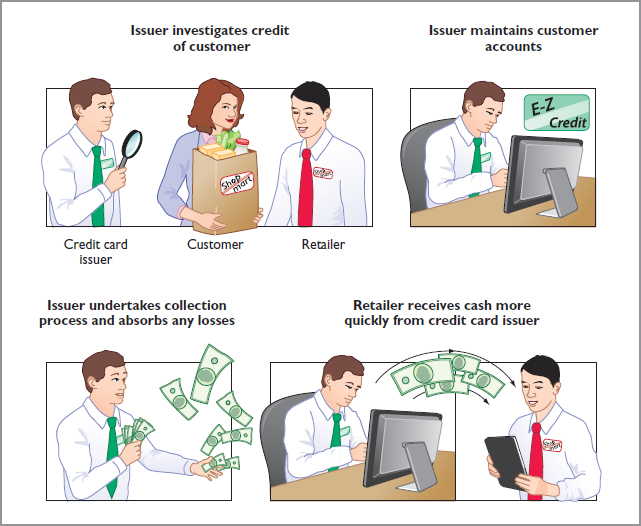

CREDIT CARD SALES

Credit card use is becoming widespread around the world. ICBC is among the largest credit card issuers in the world. Visa and MasterCard are the credit cards that most individuals use. Three parties are involved when credit cards are used in retail sales: (1) the credit card issuer, who is independent of the retailer; (2) the retailer; and (3) the customer. A retailer’s acceptance of a national credit card is another form of selling (factoring) the receivable.

Illustration 8-10 (page 394) shows the major advantages of credit cards to the retailer. In exchange for these advantages, the retailer pays the credit card issuer a fee of 2–6% of the invoice price for its services.

ACCOUNTING FOR CREDIT CARD SALES The retailer generally considers sales from the use of credit card sales as cash sales. The retailer must pay to the bank that issues the card a fee for processing the transactions. The retailer records the credit card slips in a similar manner as checks deposited from a cash sale.

Illustration 8-10 Advantages of credit cards to the retailer

To illustrate, Lee Co. Ltd. purchases NT$6,000 of music downloads for its restaurant from Yang Music, using a Visa First Bank Card. First Bank charges a service fee of 3%. The entry to record this transaction by Yang Music on March 22, 2018, is as follows.

Notes Receivable

Learning Objective 5

Compute the maturity date of and interest on notes receivable.

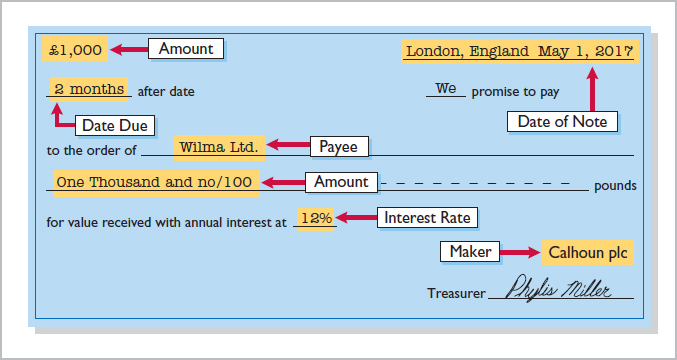

Companies may also grant credit in exchange for a formal credit instrument known as a promissory note. A promissory note is a written promise to pay a specified amount of money on demand or at a definite time. Promissory notes may be used (1) when individuals and companies lend or borrow money, (2) when the amount of the transaction and the credit period exceed normal limits, or (3) in settlement of accounts receivable.

In a promissory note, the party making the promise to pay is called the maker. The party to whom payment is to be made is called the payee. The note may specifically identify the payee by name or may designate the payee simply as the bearer of the note.

In the note shown in Illustration 8-11, Calhoun plc is the maker, and Wilma Ltd. is the payee. To Wilma Ltd., the promissory note is a note receivable. To Calhoun plc, it is a note payable.

Illustration 8-11 Promissory note

• HELPFUL HINT

For this note, the maker, Calhoun plc, debits Cash and credits Notes Payable. The payee, Wilma Ltd., debits Notes Receivable and credits Cash.

Notes receivable give the holder a stronger legal claim to assets than do accounts receivable. Like accounts receivable, notes receivable can be readily sold to another party. Promissory notes are negotiable instruments (as are checks), which means that they can be transferred to another party by endorsement.

Companies frequently accept notes receivable from customers who need to extend the payment of an outstanding account receivable. They often require such notes from high-risk customers. In some industries (such as the pleasure and sport boat industry), all credit sales are supported by notes. The majority of notes, however, originate from loans.

The basic issues in accounting for notes receivable are the same as those for accounts receivable:

- Recognizing notes receivable.

- Valuing notes receivable.

- Disposing of notes receivable.

On the following pages, we look at these issues. Before we do, however, we need to consider two issues that do not apply to accounts receivable: determining the maturity date and computing interest.

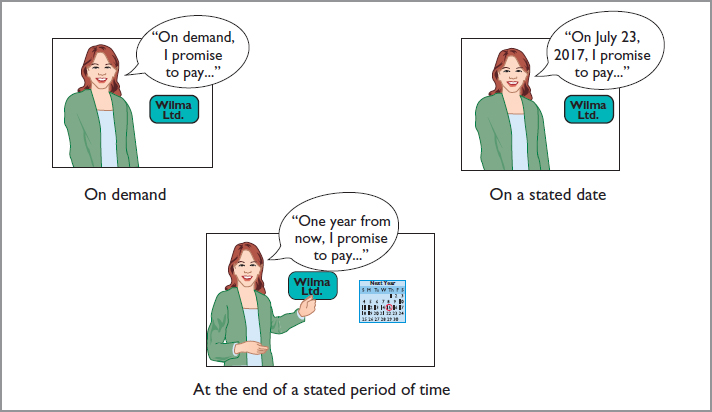

Determining the Maturity Date

When the life of a note is expressed in terms of months, you find the date when it matures by counting the months from the date of issue. For example, the maturity date of a three-month note dated May 1 is August 1. A note drawn on the last day of a month matures on the last day of a subsequent month. That is, a July 31 note due in two months matures on September 30.

When the due date is stated in terms of days, you need to count the exact number of days to determine the maturity date. In counting, omit the date the note is issued but include the due date. For example, the maturity date of a 60-day note dated July 17 is September 15, computed as follows.

Illustration 8-12 Computation of maturity date

| Term of note | 60 days | |

| July (31–17) | 14 | |

| August | 31 | 45 |

| Maturity date: September | 15 |

Illustration 8-13 shows three ways of stating the maturity date of a promissory note.

Illustration 8-13 Maturity date of different notes

Computing Interest

Illustration 8-14 gives the basic formula for computing interest on an interest-bearing note.

Illustration 8-14 Formula for computing interest

The interest rate specified in a note is an annual rate of interest. The time factor in the formula in Illustration 8-14 expresses the fraction of a year that the note is outstanding. When the maturity date is stated in days, the time factor is often the number of days divided by 360. When counting days, omit the date that the note is issued but include the due date. When the due date is stated in months, the time factor is the number of months divided by 12. Illustration 8-15 shows computation of interest for various time periods.

• HELPFUL HINT

The interest rate specified is the annual rate.

Illustration 8-15 Computation of interest

There are different ways to calculate interest. For example, the computation in Illustration 8-15 assumes 360 days for the length of the year. Most financial instruments use 365 days to compute interest. For homework problems, assume 360 days to simplify computations.

Recognizing Notes Receivable

Learning Objective 6

Explain how companies recognize notes receivable.

To illustrate the basic entry for notes receivable, we will use Calhoun plc’s £1,000, two-month, 12% promissory note dated May 1. Assuming that Calhoun plc wrote the note to settle an open account, Wilma Ltd. makes the following entry for the receipt of the note.

The company records the note receivable at its face value, the amount shown on the face of the note. No interest revenue is reported when the note is accepted because the revenue recognition principle does not recognize revenue until the performance obligation is satisfied. Interest is earned (accrued) as time passes.

If a company lends money using a note, the entry is a debit to Notes Receivable and a credit to Cash in the amount of the loan.

Valuing Notes Receivable

Learning Objective 7

Describe how companies value notes receivable.

Valuing short-term notes receivable is the same as valuing accounts receivable. Like accounts receivable, companies report short-term notes receivable at their cash (net) realizable value. The notes receivable allowance account is Allowance for Doubtful Accounts. The estimations involved in determining cash realizable value and in recording bad debt expense and the related allowance are done similarly to accounts receivable.

Disposing of Notes Receivable

Learning Objective 8

Describe the entries to record the disposition of accounts receivable.

Notes may be held to their maturity date, at which time the face value plus accrued interest is due. In some situations, the maker of the note defaults, and the payee must make an appropriate adjustment. In other situations, similar to accounts receivable, the holder of the note speeds up the conversion to cash by selling the receivables. The accounting entries for the sale of notes receivable are left for a more advanced class.

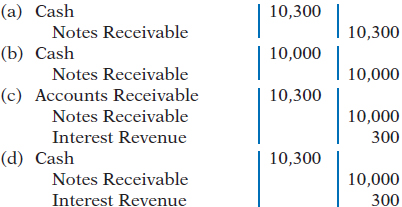

HONOR OF NOTES RECEIVABLE

A note is honored when its maker pays in full at its maturity date. For each interest-bearing note, the amount due at maturity is the face value of the note plus interest for the length of time specified on the note.

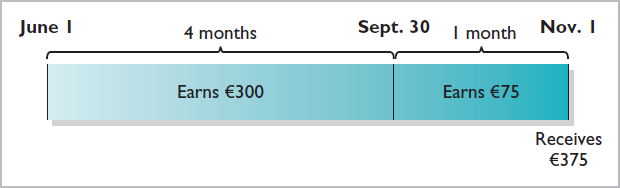

To illustrate, assume that Wolder Co. lends Higley Co. €10,000 on June 1, accepting a five-month, 9% interest note. In this situation, interest is €375 . The amount due, the maturity value, is €10,375 . To obtain payment, Wolder (the payee) must present the note either to Higley Co. (the maker) or to the maker’s agent, such as a bank. If Wolder presents the note to Higley Co. on November 1, the maturity date, Wolder’s entry to record the collection is as follows.

ACCRUAL OF INTEREST RECEIVABLE

Suppose instead that Wolder Co. prepares financial statements as of September 30. The timeline in Illustration 8-16 presents this situation.

Illustration 8-16 Timeline of interest earned

To reflect interest earned but not yet received, Wolder must accrue interest on September 30. In this case, the adjusting entry by Wolder is for four months of interest, or €300, as shown below.

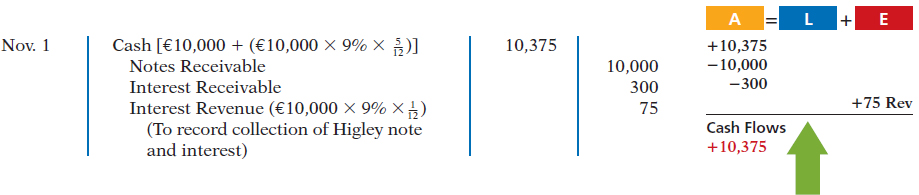

At the note’s maturity on November 1, Wolder receives €10,375. This amount represents repayment of the €10,000 note as well as five months of interest, or $375, as shown below. The €375 is comprised of the €300 Interest Receivable accrued on September 30 plus €75 earned during October. Wolder’s entry to record the honoring of the Higley note on November 1 is as follows.

In this case, Wolder credits Interest Receivable because the receivable was established in the adjusting entry on September 30.

DISHONOR OF NOTES RECEIVABLE

A dishonored (defaulted) note is a note that is not paid in full at maturity. A dishonored note receivable is no longer negotiable. However, the payee still has a claim against the maker of the note for both the note and the interest. Therefore, the note holder usually transfers the Notes Receivable account to an Accounts Receivable account.

To illustrate, assume that Higley Co. on November 1 indicates that it cannot pay at the present time. The entry to record the dishonor of the note depends on whether Wolder Co. expects eventual collection. If it does expect eventual collection, Wolder Co. debits the amount due (face value and interest) on the note to Accounts Receivable. It would make the following entry at the time the note is dishonored (assuming no previous accrual of interest).

If instead on November 1 there is no hope of collection, the note holder would write off the face value of the note by debiting Allowance for Doubtful Accounts. No interest revenue would be recorded because collection will not occur.

Statement Presentation and Analysis

Learning Objective 9

Explain the statement presentation and analysis of receivables.

Presentation

Companies should identify in the statement of financial position or in the notes to the financial statements each of the major types of receivables. Short-term receivables appear in the current assets section of the statement of financial position. Short-term investments appear after short-term receivables because these investments are more liquid (nearer to cash). Companies report both the gross amount of receivables and the allowance for doubtful accounts.

In an income statement, companies report bad debt expense and service charge expense as selling expenses in the operating expenses section. Interest revenue appears under “Other income and expense” in the non-operating activities section of the income statement.

Analysis

Investors and corporate managers compute financial ratios to evaluate the liquidity of a company’s accounts receivable. They use the accounts receivable turnover to assess the liquidity of the receivables. This ratio measures the number of times, on average, the company collects accounts receivable during the period. It is computed by dividing net credit sales (net sales less cash sales) by the average net accounts receivable during the year. Unless seasonal factors are significant, average net accounts receivable outstanding can be computed from the beginning and ending balances of net accounts receivable.

For example, in a recent year Lenovo Group (CHN) (which reported in U.S. dollars) had net sales of $38,707 million for the year. It had a beginning accounts receivable (net) balance of $2,885 million and an ending accounts receivable (net) balance of $3,171 million. Assuming that Lenovo’s sales were all on credit, its accounts receivable turnover is computed as follows.

Illustration 8-17 Accounts receivable turnover and computation

The result indicates an accounts receivable turnover of 12.8 times per year. The higher the turnover, the more liquid the company’s receivables.

A variant of the accounts receivable turnover that makes the liquidity even more evident is its conversion into an average collection period in terms of days. This is done by dividing the turnover into 365 days. For example, Lenovo’s turnover of 12.8 times is divided into 365 days, as shown in Illustration 8-18, to obtain approximately 28.5 days. This means that it takes Lenovo on average 28.5 days to collect its accounts receivable.

Illustration 8-18 Average collection period for receivables formula and computation

Companies frequently use the average collection period to assess the effectiveness of a company’s credit and collection policies. The general rule is that the collection period should not greatly exceed the credit term period (that is, the time allowed for payment).

GLOSSARY REVIEW

- Accounts receivable

- Amounts owed by customers on account. (p. 384).

- Accounts receivable turnover

- A measure of the liquidity of accounts receivable; computed by dividing net credit sales by average net accounts receivable. (p. 401).

- Aging the accounts receivable

- The analysis of customer balances by the length of time they have been unpaid. (p. 391).

- Allowance method

- A method of accounting for bad debts that involves estimating uncollectible accounts at the end of each period. (p. 387).

- Average collection period

- The average amount of time that a receivable is outstanding; calculated by dividing 365 days by the accounts receivable turnover. (p. 401).

- Bad Debt Expense

- An expense account to record uncollectible receivables. (p. 386).

- Cash (net) realizable value

- The net amount a company expects to receive in cash. (p. 388).

- Direct write-off method

- A method of accounting for bad debts that involves expensing accounts at the time they are determined to be uncollectible. (p. 387).

- Dishonored (defaulted) note

- A note that is not paid in full at maturity. (p. 399).

- Factor

- A finance company or bank that buys receivables from businesses and then collects the payments directly from the customers. (p. 393).

- Maker

- The party in a promissory note who is making the promise to pay. (p. 395).

- Notes receivable

- Written promise (as evidenced by a formal instrument) for amounts to be received. (p. 384).

- Other receivables

- Various forms of non-trade receivables, such as interest receivable and income taxes refundable. (p. 384).

- Payee

- The party to whom payment of a promissory note is to be made. (p. 395).

- Percentage-of-receivables basis

- Management estimates what percentage of receivables will result in losses from uncollectible accounts. (p. 391).

- Percentage-of-sales basis

- Management estimates what percentage of credit sales will be uncollectible. (p. 390).

- Promissory note

- A written promise to pay a specified amount of money on demand or at a definite time. (p. 395).

- Receivables

- Amounts due from individuals and other companies. (p. 384).

- Trade receivables

- Notes and accounts receivable that result from sales transactions. (p. 384).

PRACTICE MULTIPLE-CHOICE QUESTIONS

Receivables are frequently classified as:

- accounts receivable, company receivables, and other receivables.

- accounts receivable, notes receivable, and employee receivables.

- accounts receivable and general receivables.

- accounts receivable, notes receivable, and other receivables.

Buehler Company Ltd. on June 15 sells merchandise on account to Chaz Co. for HK$10,000, terms 2/10, n/30. On June 20, Chaz returns merchandise worth HK$3,000 to Buehler. On June 24, payment is received from Chaz for the balance due. What is the amount of cash received?

- HK$7,000.

- HK$6,800.

- HK$6,860.

- None of the above.

Which of the following approaches for bad debts is best described as a statement of financial position method?

- Percentage-of-receivables basis.

- Direct write-off method.

- Percentage-of-sales basis.

- Both percentage-of-receivables basis and direct write-off method.

Hughes plc has a credit balance of £5,000 in its Allowance for Doubtful Accounts before any adjustments are made at the end of the year. Based on review and aging of its accounts receivable at the end of the year, Hughes estimates that £60,000 of its receivables are uncollectible. The amount of bad debt expense which should be reported for the year is:

- £5,000.

- £55,000.

- £60,000.

- £65,000.

Use the same information as in Question 8-12, except that Hughes has a debit balance of £5,000 in its Allowance for Doubtful Accounts before any adjustments are made at the end of the year. In this situation, the amount of bad debt expense that should be reported for the year is:

- £5,000.

- £55,000.

- £60,000.

- £65,000.

Net sales for the month are

800,000,000 and bad debts are expected to be 1.5% of net sales. The company uses the percentage-of-sales basis. If Allowance for Doubtful Accounts has a credit balance of 15,000,000 before adjustment, what is the balance after adjustment?

800,000,000 and bad debts are expected to be 1.5% of net sales. The company uses the percentage-of-sales basis. If Allowance for Doubtful Accounts has a credit balance of 15,000,000 before adjustment, what is the balance after adjustment?- 15,000,000.

- 27,000,000.

- 23,000,000.

- 31,000,000.

In 2017, Roso Carlson Ltd. had net credit sales of NT$7,500,000. On January 1, 2017, Allowance for Doubtful Accounts had a credit balance of NT$180,000. During 2017, NT$300,000 of uncollectible accounts receivable were written off. Past experience indicates that 3% of net credit sales become uncollectible. What should be the adjusted balance of Allowance for Doubtful Accounts at December 31, 2017?

- NT$100,500.

- NT$105,000.

- NT$225,000.

- NT$405,000.

An analysis and aging of the accounts receivable of Prince Ltd. at December 31 reveals the following data.

Accounts receivable £800,000Allowance for doubtful accounts per books before adjustment 50,000Amounts expected to become uncollectible 65,000The cash realizable value of the accounts receivable at December 31, after adjustment, is:

- £685,000.

- £750,000.

- £800,000.

- £735,000.

Which of the following statements about Visa credit card sales is incorrect?

- The credit card issuer makes the credit investigation of the customer.

- The retailer is not involved in the collection process.

- Two parties are involved.

- The retailer receives cash more quickly than it would from individual customers on account.

Blinka Retailers accepted €50,000 of Citibank Visa credit card charges for merchandise sold on July 1. Citibank charges 4% for its credit card use. The entry to record this transaction by Blinka Retailers will include a credit to Sales Revenue of €50,000 and a debit(s) to:

One of the following statements about promissory notes is incorrect. The incorrect statement is:

- The party making the promise to pay is called the maker.

- The party to whom payment is to be made is called the payee.

- A promissory note is not a negotiable instrument.

- A promissory note is often required from high-risk customers.

Foti Co. accepts a $1,000, 3-month, 6% promissory note in settlement of an account with Bartelt Co. The entry to record this transaction is as follows.

Ginter Co. Ltd. holds Kolar plc’s €10,000, 120-day, 9% note. The entry made by Ginter when the note is collected, assuming no interest has been previously accrued, is:

Accounts and notes receivable are reported in the current assets section of the statement of financial position at:

- cash (net) realizable value.

- net book value.

- lower-of-cost-or-net realizable value.

- invoice cost.

Oliveras Company Ltd. had net credit sales during the year of HK$8,000,000 and cost of goods sold of HK$5,000,000. The balance in accounts receivable at the beginning of the year was HK$1,000,000, and the end of the year it was HK$1,500,000. What were the accounts receivable turnover and the average collection period in days?

- 4.0 and 91.3 days.

- 5.3 and 68.9 days.

- 6.4 and 57 days.

- 8.0 and 45.6 days.

Solutions

PRACTICE EXERCISES

Journalize entries to record allowance for doubtful accounts using two different bases.

- The ledger of J.C. Cobb Company at the end of the current year shows Accounts Receivable $150,000, Sales Revenue $850,000, and Sales Returns and Allowances $30,000.

Instructions

- If J.C. Cobb uses the direct write-off method to account for uncollectible accounts, journalize the adjusting entry at December 31, assuming J.C. Cobb determines that M. Jack’s $1,500 balance is uncollectible.

- If Allowance for Doubtful Accounts has a credit balance of $2,400 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1.5% of net sales, and (2) 10% of accounts receivable.

- If Allowance for Doubtful Accounts has a debit balance of $200 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 0.75% of net sales and (2) 6% of accounts receivable.

Solution

Journalize entries for notes receivable transactions.

- Troope Supply SA has the following transactions related to notes receivable during the last 3 months of 2017.

| Oct. | 1 |

Loaned €16,000 cash to Juan Vasquez on a 1-year, 10% note. |

| Dec. | 11 |

Sold goods to A. Palmer, A/S, receiving a €6,750, 90-day, 8% note. |

16 |

Received a €6,400, 30-day, 9% note in exchange for J. Nicholas’s outstanding accounts receivable. | |

31 |

Accrued interest revenue on all notes receivable. |

Instructions

- Journalize the transactions for Troup Supply.

- Record the collection of the Vasquez note at its maturity in 2018.

Solution

PRACTICE PROBLEM

Prepare entries for various receivables transactions.

The following selected transactions relate to Dylan plc.

| Mar. | 1 |

Sold £20,000 of merchandise to Potter plc, terms 2/10, n/30. |

11 |

Received payment in full from Potter plc for balance due. | |

12 |

Accepted Juno Ltd.’s £20,000, 6-month, 12% note for balance due on existing accounts receivable. | |

13 |

Made Dylan plc credit card sales for £13,200. | |

15 |

Made Visa credit card sales totaling £6,700. A 3% service fee is charged by Visa. | |

| Apr. | 11 |

Sold accounts receivable of £8,000 to Harcot Factor. Harcot Factor assesses a service charge of 2% of the amount of receivables sold. |

13 |

Received collections of £8,200 on Dylan plc credit card sales and added finance charges of 1.5% to the remaining balances. | |

| May | 10 |

Wrote off as uncollectible £16,000 of accounts receivable. Dylan uses the percentage-of-sales basis to estimate bad debts. |

| June | 30 |

Credit sales recorded during the first 6 months total £2,000,000. The bad debt percentage is 1% of credit sales. At June 30, the balance in the allowance account is £3,500 before adjustment. The company prepares financial statements on a semiannual basis. |

| July | 16 |

One of the accounts receivable written off in May was from J. Simon, who pays the amount due, £4,000, in full. |

Instructions

Prepare the journal entries for the transactions.

Solution

WileyPLUS

Brief Exercises, DO IT! Review, Exercises, and Problems, and many additional resources are available for practice in WileyPLUS.

QUESTIONS

What is the difference between an account receivable and a note receivable?

What are some common types of receivables other than accounts receivable and notes receivable?

Texaco Oil Company (USA) issues its own credit cards. Assume that Texaco charges you $40 interest on an unpaid balance. Prepare the journal entry that Texaco makes to record this revenue.

What are the essential features of the allowance method of accounting for bad debts?

Roger Holloway cannot understand why cash realizable value does not decrease when an uncollectible account is written off under the allowance method. Clarify this point for Roger Holloway.

Distinguish between the two bases that may be used in estimating uncollectible accounts.

Borke Ltd. has a credit balance of NT$320,000 in Allowance for Doubtful Accounts. The estimated bad debt expense under the percentage-of-sales basis is NT$370,000. The total estimated uncollectibles under the percentage-of-receivables basis is NT$580,000. Prepare the adjusting entry under each basis.

How are bad debts accounted for under the direct write-off method? What are the disadvantages of this method?

Freida ASA accepts both its own credit cards and national credit cards. What are the advantages of accepting both types of cards?

An article recently appeared in the Wall Street Journal indicating that companies are selling their receivables at a record rate. Why are companies selling their receivables?

WestSide Textiles decides to sell HK$8,000,000 of its accounts receivable to First Factors Ltd. First Factors assesses a service charge of 3% of the amount of receivables sold. Prepare the journal entry that WestSide Textiles makes to record this sale.

Your roommate is uncertain about the advantages of a promissory note. Compare the advantages of a note receivable with those of an account receivable.

How may the maturity date of a promissory note be stated?

Indicate the maturity date of each of the following promissory notes:

Date of Note Terms (a) March 13 one year after date of note (b) May 4 3 months after date (c) June 20 30 days after date (d) July 1 60 days after date Compute the missing amounts for each of the following notes.

Principal Annual Interest Rate Time Total Interest (a) ? 9% 120 days € 450 (b) €30,000 10% 3 years ? (c) €60,000 ? 5 months €3,000 (d) €45,000 8% ? €1,200 In determining interest revenue, some financial institutions use 365 days per year and others use 360 days. Why might a financial institution use 360 days?

Jana Company dishonors a note at maturity. What are the options available to the lender?

General Motors Corporation (USA) has accounts receivable and notes receivable. How should the receivables be reported on the statement of financial position?

The accounts receivable turnover is 8.14, and average net accounts receivable during the period is £400,000. What is the amount of net credit sales for the period?

BRIEF EXERCISES

Identify different types of receivables.

BE8-1 Presented below are three receivables transactions. Indicate whether these receivables are reported as accounts receivable, notes receivable, or other receivables on a statement of financial position.

- Sold merchandise on account for 64,000,000 to a customer.

- Received a promissory note of 57,000,000 for services performed.

- Advanced 8,000,000 to an employee.

Record basic accounts receivable transactions.

BE8-2 Record the following transactions on the books of Galaxy Co.

- On July 1, Galaxy Co. sold merchandise on account to Kingston Inc. for $17,200, terms 2/10, n/30.

- On July 8, Kingston Inc. returned merchandise worth $3,800 to Galaxy Co.

- On July 11, Kingston Inc. paid for the merchandise.

Prepare entry for allowance method and partial statement of financial position.

BE8-3 During its first year of operations, Energy Company SE had credit sales of €3,000,000; €600,000 remained uncollected at year-end. The credit manager estimates that €28,000 of these receivables will become uncollectible.

- Prepare the journal entry to record the estimated uncollectibles.

- Prepare the current assets section of the statement of financial position for Energy Company. Assume that in addition to the receivables it has cash of €90,000, inventory of €118,000, and prepaid insurance of €7,500.

Prepare entry for write-off; determine cash realizable value.

BE8-4 At the end of 2017, Endrun Ltd. has accounts receivable of £700,000 and an allowance for doubtful accounts of £54,000. On January 24, 2018, the company learns that its receivable from Marcello is not collectible, and management authorizes a write-off of £6,200.

- Prepare the journal entry to record the write-off.

- What is the cash realizable value of the accounts receivable (1) before the write-off and (2) after the write-off?

Prepare entries for collection of bad debt write-off.

BE8-5 Assume the same information as BE8-4. On March 4, 2018, Endrun Ltd. receives payment of £6,200 in full from Marcello. Prepare the journal entries to record this transaction.

Prepare entry using percentage-of-sales method.

BE8-6 Hamblin Co. elects to use the percentage-of-sales basis in 2017 to record bad debt expense. It estimates that 2% of net credit sales will become uncollectible. Sales revenues are $800,000 for 2017, sales returns and allowances are $38,000, and the allowance for doubtful accounts has a credit balance of $9,000. Prepare the adjusting entry to record bad debt expense in 2017.

Prepare entry using percentage-of-receivables method.

BE8-7 Shenzhen Ltd. uses the percentage-of-receivables basis to record bad debt expense. It estimates that 1% of accounts receivable will become uncollectible. Accounts receivable are £420,000 at the end of the year, and the allowance for doubtful accounts has a credit balance of £1,280.

- Prepare the adjusting journal entry to record bad debt expense for the year.

- If the allowance for doubtful accounts had a debit balance of £740 instead of a credit balance of £1,280, determine the amount to be reported for bad debt expense.

Prepare entries to dispose of accounts receivable.

BE8-8 Presented below are two independent transactions.

- Fiesta Restaurant accepted a Visa card in payment of a €175 lunch bill. The bank charges a 4% fee. What entry should Fiesta make?

- St. Pierre AG sold its accounts receivable of €70,000. What entry should St. Pierre make, given a service charge of 3% on the amount of receivables sold?

Compute interest and determine maturity dates on notes.

BE8-9 Compute interest and find the maturity date for the following notes.

| Date of Note | Principal | Interest Rate (%) | Terms | |

| (a) | June 10 | £80,000 | 6% | 60 days |

| (b) | July 14 | £64,000 | 7% | 90 days |

| (c) | April 27 | £12,000 | 4% | 75 days |

Determine maturity dates and compute interest and rates on notes.

BE8-10 Presented below are data on three promissory notes. Determine the missing amounts.

| Date of Note | Terms | Maturity Date | Principal | Annual Interest Rate | Total Interest | |

| (a) | April 1 | 60 days | ? | €600,000 |

5% | ? |

| (b) | July 2 | 30 days | ? | 90,000 |

? | €600 |

| (c) | March 7 | 6 months | ? | 120,000 |

10% | ? |

Prepare entry for notes receivable exchanged for account receivable.

BE8-11 On January 10, 2017, Wilfer Ltd. sold merchandise on account to Elgin Co. for HK$80,400, n/30. On February 9, Elgin Co. gave Wilfer Ltd. a 7% promissory note in settlement of this account. Prepare the journal entry to record the sale and the settlement of the account receivable.

Compute ratios to analyze receivables.

BE8-12 The financial statements of Minnesota Mining and Manufacturing Company (3M) (USA) report net sales of $20.0 billion. Accounts receivable (net) are $2.7 billion at the beginning of the year and $2.8 billion at the end of the year. Compute 3M’s accounts receivable turnover. Compute 3M’s average collection period for accounts receivable in days.

EXERCISES

Journalize entries related to accounts receivable.

E8-1 Presented below are selected transactions of Federer AG. Federer sells in large quantities to other companies and also sells its product in a small retail outlet.

| March | 1 |

Sold merchandise on account to Lynda Co. for CHF3,800, terms 2/10, n/30. |

3 |

Lynda Co. returned merchandise worth CHF600 to Federer. | |

9 |

Federer collected the amount due from Lynda Co. from the March 1 sale. | |

15 |

Federer sold merchandise for CHF200 in its retail outlet. The customer used his Federer credit card. | |

31 |

Federer added 1.5% monthly interest to the customer’s credit card balance. |

Instructions

Prepare journal entries for the transactions on page 410.

Journalize entries for recognizing accounts receivable.

E8-2 Presented below are two independent situations.

- On January 6, Bennett Co. sells merchandise on account to Jackie Ltd. for £7,000, terms 2/10, n/30. On January 16, Jackie Ltd. pays the amount due. Prepare the entries on Bennett’s books to record the sale and related collection.

- On January 10, Connor Bybee uses his Sheridan Co. credit card to purchase merchandise from Sheridan Co. for £9,000. On February 10, Bybee is billed for the amount due of £9,000. On February 12, Bybee pays £6,000 on the balance due. On March 10, Bybee is billed for the amount due, including interest at 2% per month on the unpaid balance as of February 12. Prepare the entries on Sheridan Co.’s books related to the transactions that occurred on January 10, February 12, and March 10.

Journalize entries to record allowance for doubtful accounts using two different bases.

E8-3 The ledger of Elburn ASA at the end of the current year shows Accounts Receivable €110,000, Sales Revenue €840,000, and Sales Returns and Allowances €28,000.

Instructions

- If Elburn uses the direct write-off method to account for uncollectible accounts, journalize the adjusting entry at December 31, assuming Elburn determines that T. Thum’s €1,500 balance is uncollectible.

- If Allowance for Doubtful Accounts has a credit balance of €2,500 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 1% of net sales, and (2) 10% of accounts receivable.

- If Allowance for Doubtful Accounts has a debit balance of €200 in the trial balance, journalize the adjusting entry at December 31, assuming bad debts are expected to be (1) 0.75% of net sales and (2) 6% of accounts receivable.

Determine bad debt expense; prepare the adjusting entry for bad debt expense.

E8-4 Leland Ltd. has accounts receivable of £98,100 at March 31. Credit terms are 2/10, n/30. At March 31, Allowance for Doubtful Accounts has a credit balance of £900 prior to adjustment. The company uses the percentage-of-receivables basis for estimating uncollectible accounts. The company’s estimate of bad debts is shown below.

Instructions

- Determine the total estimated uncollectibles.

- Prepare the adjusting entry at March 31 to record bad debt expense.

Journalize write-off and recovery.

E8-5 At December 31, 2016, Crawford Ltd. had a credit balance of £15,000 in Allowance for Doubtful Accounts. During 2017, Crawford wrote off accounts totaling £14,100. One of those accounts (£1,800) was later collected. At December 31, 2017, an aging schedule indicated that the balance in Allowance for Doubtful Accounts should be £17,800.

Instructions

Prepare journal entries to record the 2017 transactions of Crawford Ltd.

Journalize percentage-of-sales basis, write-off, recovery.

E8-6 On December 31, 2016, Russell NV estimated that 2% of its net sales of €360,000 will become uncollectible. The company recorded this amount as an addition to Allowance for Doubtful Accounts. On May 11, 2017, Russell NV determined that the B. Vetter account was uncollectible and wrote off €1,100. On June 12, 2017, Vetter paid the amount previously written off.

Instructions

Prepare the journal entries on December 31, 2016, May 11, 2017, and June 12, 2017.

Journalize entries for the sale of accounts receivable.

E8-7 Presented below and on page 412 are two independent situations.

- On March 3, Pusan Appliances sells 620,000,000 of its receivables to Universal Factors Ltd. Universal Factors assesses a finance charge of 4% of the amount of receivables sold. Prepare the entry on Pusan Appliances’ books to record the sale of the receivables.

- On May 10, Taejeon Ltd. sold merchandise for 3,200,000 and accepted the customer’s America Bank MasterCard. America Bank charges a 5% service charge for credit card sales. Prepare the entry on Taejeon’s books to record the sale of merchandise.

Journalize entries for credit card sales.

E8-8 Presented below are two independent situations.

- On April 2, Julie Keiser uses her JCPenney Company credit card to purchase merchandise from a JCPenney store for $1,500. On May 1, Keiser is billed for the $1,500 amount due. Keiser pays $900 on the balance due on May 3. On June 1, Keiser receives a bill for the amount due, including interest at 1.0% per month on the unpaid balance as of May 3. Prepare the entries on JCPenney Co.’s books related to the transactions that occurred on April 2, May 3, and June 1.

- On July 4, Avalon Restaurant accepts a Visa card for a $200 dinner bill. Visa charges a 3% service fee. Prepare the entry on Avalon’s books related to this transaction.

Journalize credit card sales.

E8-9 Hong Kong Stores accepts both its own and national credit cards. During the year, the following selected summary transactions occurred.

| Jan. | 15 |

Made Hong Kong credit card sales totaling HK$17,000. (There were no balances prior to January 15.) |

20 |

Made Visa credit card sales (service charge fee 2%) totaling HK$4,800. | |

| Feb. | 10 |

Collected HK$11,000 on Hong Kong credit card sales. |

15 |

Added finance charges of 1.5% to Hong Kong credit card account balances. |

Instructions

Journalize the transactions for Hong Kong Stores.

Journalize entries for notes receivable transactions.

E8-10 Reeves Supply plc has the following transactions related to notes receivable during the last 2 months of 2017. The company does not make entries to accrue interest except at December 31.

| Nov. | 1 |

Loaned £15,000 cash to Norma Jeanne on a 12-month, 9% note. |

| Dec. | 11 |

Sold goods to Bob Sharbo, receiving a £6,750, 90-day, 8% note. |

16 |

Received a £4,400, 180-day, 12% note in exchange for Richard Russo’s outstanding accounts receivable. | |

31 |

Accrued interest revenue on all notes receivable. |

Instructions

- Journalize the transactions for Reeves Supply.

- Record the collection of the Jeanne note at its maturity in 2018.

Journalize entries for notes receivable.

E8-11 Record the following transactions for Taylor Co. in the general journal.

| 2017 | ||

| May | 1 |

Received a €7,500, 12-month, 8% note in exchange for Len Monroe’s outstanding accounts receivable. |

| Dec. | 31 |

Accrued interest on the Monroe note. |

| Dec. | 31 |

Closed the interest revenue account. |

| 2018 | ||

| May | 1 |

Received principal plus interest on the Monroe note. (No interest has been accrued in 2018.) |

Prepare entries for note receivable transactions.

E8-12 Bieber Ltd. had the following select transactions.

| May | 1, 2017 |

Accepted Crane plc’s 12-month, 12% note in settlement of a £16,000 account receivable. |

| July | 1, 2017 |

Loaned £25,000 cash to Sam Howard on a 9-month, 10% note. |

| Dec. | 31, 2017 |

Accrued interest on all notes receivable. |

| Apr. | 1, 2018 |

Sam Howard dishonored its note; Bieber expects it will eventually collect. |

| May | 1, 2018 |

Received principal plus interest on the Crane note. |

Instructions

Prepare journal entries to record the transactions. Bieber prepares adjusting entries once a year on December 31.

Journalize entries for dishonor of notes receivable.

E8-13 On May 2, Nanjing Ltd. lends ¥7,600,000 to Cortland Ltd., issuing a 3-month, 7% note. At the maturity date, August 2, Cortland indicates that it cannot pay.

Instructions

- Prepare the entry to record the issuance of the note.

- Prepare the entry to record the dishonor of the note, assuming that Nanjing expects collection will occur.

- Prepare the entry to record the dishonor of the note, assuming that Nanjing does not expect collection in the future.

Compute accounts receivable turnover and average collection period.

E8-14 Lashkova A/S had accounts receivable of €100,000 on January 1, 2017. The only transactions that affected accounts receivable during 2017 were net credit sales of €1,000,000, cash collections of €920,000, and accounts written off of €30,000.

Instructions

- Compute the ending balance of accounts receivable.

- Compute the accounts receivable turnover for 2017.

- Compute the average collection period in days.

PROBLEMS: SET A

Prepare journal entries related to bad debt expense.

P8-1A At December 31, 2016, Cafu SA reported the following information on its statement of financial position.

| Accounts receivable | R$960,000 |

| Less: Allowance for doubtful accounts | 66,000 |

During 2017, the company had the following transactions related to receivables.

| 1. Sales on account | R$3,315,000 |

| 2. Sales returns and allowances | 50,000 |

| 3. Collections of accounts receivable | 2,810,000 |

| 4. Write-offs of accounts receivable deemed uncollectible | 88,000 |

| 5. Recovery of bad debts previously written off as uncollectible | 29,000 |

Instructions

- Prepare the journal entries to record each of these five transactions. Assume that no cash discounts were taken on the collections of accounts receivable.

- Enter the January 1, 2017, balances in Accounts Receivable and Allowance for Doubtful Accounts, post the entries to the two accounts (use T-accounts), and determine the balances.

- Prepare the journal entry to record bad debt expense for 2017, assuming that an aging of accounts receivable indicates that expected bad debts are R$125,000.

- Compute the accounts receivable turnover for 2017, assuming the expected bad debt information presented in (c).

Compute bad debt amounts.

P8-2A Information related to Hamilton plc for 2017 is summarized below.

| Total credit sales | £2,500,000 |

| Accounts receivable at December 31 | 970,000 |

| Bad debts written off | 66,000 |

Instructions

- What amount of bad debt expense will Hamilton report if it uses the direct write-off method of accounting for bad debts?

- Assume that Hamilton estimates its bad debt expense to be 3% of credit sales. What amount of bad debt expense will Hamilton record if it has an Allowance for Doubtful Accounts credit balance of £4,000?

- Assume that Hamilton estimates its bad debt expense based on 7% of accounts receivable. What amount of bad debt expense will Hamilton record if it has an Allowance for Doubtful Accounts credit balance of £3,000?

- Assume the same facts as in (c), except that there is a £3,000 debit balance in Allowance for Doubtful Accounts. What amount of bad debt expense will Hamilton record?

What is the weakness of the direct write-off method of reporting bad debt expense?

What is the weakness of the direct write-off method of reporting bad debt expense?

Journalize entries to record transactions related to bad debts.

P8-3A Presented below is an aging schedule for Sycamore AG.

At December 31, 2017, the unadjusted balance in Allowance for Doubtful Accounts is a credit of €9,200.

Instructions

- Journalize and post the adjusting entry for bad debts at December 31, 2017.

- Journalize and post to the allowance account the following events and transactions in the year 2018.

- On March 31, a €1,000 customer balance originating in 2017 is judged uncollectible.

- On May 31, a check for €1,000 is received from the customer whose account was written off as uncollectible on March 31.

- Journalize the adjusting entry for bad debts on December 31, 2018, assuming that the unadjusted balance in Allowance for Doubtful Accounts is a debit of €1,100 and the aging schedule indicates that total estimated bad debts will be €31,600.

Journalize transactions related to bad debts.

P8-4A Hú Ltd. uses the allowance method to estimate uncollectible accounts receivable. The company produced the following aging of the accounts receivable at year-end.

Instructions

- Calculate the total estimated bad debts based on the information on page 414.

- Prepare the year-end adjusting journal entry to record the bad debts using the aged uncollectible accounts receivable determined in (a). Assume the current balance in Allowance for Doubtful Accounts is a HK$3,000 debit.

- Of the above accounts, HK$5,000 is determined to be specifically uncollectible. Prepare the journal entry to write off the uncollectible account.

- The company collects HK$5,000 subsequently on a specific account that had previously been determined to be uncollectible in (c). Prepare the journal entry(ies) necessary to restore the account and record the cash collection.

- Comment on how your answers to (a)–(d) would change if Hú Ltd. used 3% of total accounts receivable, rather than aging the accounts receivable. What are the advantages to the company of aging the accounts receivable rather than applying a percentage to total accounts receivable?

Journalize entries to record transactions related to bad debts.

P8-5A At December 31, 2017, the trial balance of Roberto SpA contained the following amounts before adjustment.

| Debit | Credit | |

| Accounts Receivable | €385,000 | |

| Allowance for Doubtful Accounts | € 800 |

|

| Sales Revenue | 918,000 |

Instructions

- Based on the information given, which method of accounting for bad debts is Roberto using—the direct write-off method or the allowance method? How can you tell?

- Prepare the adjusting entry at December 31, 2017, for bad debt expense under each of the following independent assumptions.

- An aging schedule indicates that €12,400 of accounts receivable will be uncollectible.

- The company estimates that 1% of sales will be uncollectible.

- Repeat part (b) assuming that instead of a credit balance there is an €960 debit balance in Allowance for Doubtful Accounts.

- During the next month, January 2018, a €3,000 account receivable is written off as uncollectible. Prepare the journal entry to record the write-off.

- Repeat part (d) assuming that Roberto uses the direct write-off method instead of the allowance method in accounting for uncollectible accounts receivable.

- What type of account is Allowance for Doubtful Accounts? How does it affect how accounts receivable is reported on the statement of financial position at the end of the accounting period?

Prepare entries for various notes receivable transactions.

P8-6A Hilo Ltd. closes its books monthly. On September 30, selected ledger account balances are:

| Notes Receivable | £31,000 |

| Interest Receivable | 170 |

Notes Receivable include the following.

| Date | Maker | Face | Term | Interest |

| Aug. 16 | Demaster Ltd. | £ 8,000 |

60 days | 8% |

| Aug. 25 | Skinner Co. | 9,000 |

60 days | 10% |

| Sept. 30 | Almer Ltd. | 14,000 |

6 months | 9% |

Interest is computed using a 360-day year. During October, the following transactions were completed.

| Oct. | 7 |

Made sales of £6,300 on Hilo credit cards. |

12 |

Made sales of £1,200 on MasterCard credit cards. The credit card service charge is 3%. | |

15 |

Added £460 to Hilo customer balance for finance charges on unpaid balances. | |

15 |

Received payment in full from Demaster Ltd. on the amount due. | |

24 |

Received notice that the Skinner note has been dishonored. (Assume that Skinner is expected to pay in the future.) |

Instructions

- Journalize the October transactions and the October 31 adjusting entry for accrued interest receivable.

- Enter the balances at October 1 in the receivable accounts. Post the entries to all of the receivable accounts.

- Show the statement of financial position presentation of the receivable accounts at October 31.

Prepare entries for various receivable transactions.

P8-7A On January 1, 2017, Derek Co. had Accounts Receivable €139,000, Notes Receivable €30,000, and Allowance for Doubtful Accounts €13,200. The note receivable is from Kaye Noonan Ltd. It is a 4-month, 9% note dated December 31, 2016. Derek prepares financial statements annually at December 31. During the year, the following selected transactions occurred.

| Jan. | 5 |

Sold €24,000 of merchandise to Zwingle SE, terms n/15. |

20 |

Accepted Zwingle’s €24,000, 3-month, 6% note for balance due. | |

| Feb. | 18 |

Sold €8,000 of merchandise to Gerard AG and accepted Gerard’s €8,000, 6-month, 7% note for the amount due. |

| Apr. | 20 |

Collected Zwingle note in full. |

30 |

Received payment in full from Kaye Noonan on the amount due. | |

| May | 25 |

Accepted Isabella Ltd.’s €4,000, 3-month, 7% note in settlement of a past-due balance on account. |

| Aug. | 18 |

Received payment in full from Gerard on note due. |

25 |

The Isabella note was dishonored. Isabella is not bankrupt; future payment is anticipated. | |

| Sept. | 1 |

Sold €10,000 of merchandise to Fernando Co. and accepted a €10,000, 6-month, 8% note for the amount due. |

Instructions

Journalize the transactions.

PROBLEMS: SET B

Prepare journal entries related to bad debt expense.

P8-1B At December 31, 2016, Globe Trotter Imports reported the following information on its statement of financial position.

| Accounts receivable | €220,000 |

| Less: Allowance for doubtful accounts | 15,000 |

During 2017, the company had the following transactions related to receivables.

| 1. Sales on account | €2,400,000 |

| 2. Sales returns and allowances | 45,000 |

| 3. Collections of accounts receivable | 2,250,000 |

| 4. Write-offs of accounts receivable deemed uncollectible | 10,600 |

| 5. Recovery of bad debts previously written off as uncollectible | 2,000 |

Instructions

- Prepare the journal entries to record each of these five transactions. Assume that no cash discounts were taken on the collections of accounts receivable.

- Enter the January 1, 2017, balances in Accounts Receivable and Allowance for Doubtful Accounts. Post the entries to the two accounts (use T-accounts), and determine the balances.

- Prepare the journal entry to record bad debt expense for 2017, assuming that an aging of accounts receivable indicates that estimated bad debts are €21,400.

- Compute the accounts receivable turnover for the year 2017, assuming the expected bad debt information presented in (c).

Compute bad debt amounts.

P8-2B Information related to Izmir A.Ş. for 2017 is summarized below.

| Total credit sales | |

| Accounts receivable at December 31 | 369,000 |

| Bad debts written off | 23,400 |

Instructions

- What amount of bad debt expense will Izmir report if it uses the direct write-off method of accounting for bad debts?

- Assume that Izmir decides to estimate its bad debt expense to be 3% of credit sales. What amount of bad debt expense will Izmir record if Allowance for Doubtful Accounts has a credit balance of

3,000?

3,000? - Assume that Izmir decides to estimate its bad debt expense based on 7% of accounts receivable. What amount of bad debt expense will Izmir record if Allowance for Doubtful Accounts has a credit balance of 4,000?

- Assume the same facts as in (c), except that there is a 2,000 debit balance in Allowance for Doubtful Accounts. What amount of bad debt expense will Izmir record?