CHAPTER 4

Murabaha

INTRODUCTION TO MURABAHA

Conventional banking treats money and commodities and their trading as the same. As discussed in earlier chapters, Islam views money differently from commodities. Money is only a medium of exchange with no intrinsic value, and on its own it does not satisfy any need. Meanwhile commodities have intrinsic value and satisfy some need. Commodities have differing qualities and can be identified by specifications when they are traded. A new or a used car of the same model are not the same, or of the same value, but a new or an old bank note are the same. As such, money cannot be treated as a commodity. Hence, pure lending of money and earning a fixed return on it, which is interest, is prohibited. Islamic finance requires each financial transaction to be linked to a real asset. When commodities are traded for credit, an excess can be charged according to the majority of Muslim scholars. The seller can charge a different price for a cash sale or a credit sale, where the credit sale price would be higher.

According to Shariah rule, a sales contract can be executed only when the item already exists, is owned by the seller at the time of sale and is in the physical or constructive possession of the seller. Two exceptions to this rule are the contracts of Salam and Istisna, to be covered in Chapters 8 and 9, respectively.

In Islamic commerce, sales can be classified according to delivery and payment as:

- Immediate delivery with spot payment.

- Immediate delivery with deferred payment.

- Immediate payment with deferred delivery.

Sales can also be classified based on disclosure of cost to the customer as:

- Musawama or bargain sale. In this sale, the seller and buyer agree upon a price without any reference to the cost, because a seller is not obliged to reveal it. When we buy something from a shop we are aware of the price but do not know the cost. We either decide to buy at the given price or try to bargain on the price.

- Murabaha or trust sale. Murabaha is the simplest Islamic banking instrument and is a widely used product. Islam prohibits charging fixed interest on money, but permits charging fixed profit on sale of goods. Islamic banks therefore use a sale-based transaction – Murabaha – instead of a term loan for financing. Murabaha is a sales contract where profit is made by selling at a cost-plus basis. It is an agreement where the bank purchases a specified item at the request of the customer, adds a pre-agreed profit to it and sells it to them at the marked-up price.

Murabaha is also called trust sales, since the distinguishing feature of Murabaha from regular sales is that the seller discloses the cost to the buyer and a known profit is added; the buyer puts their trust in the seller to buy the required item and to disclose to the client the quality or specification of the item and the actual cost as well as the markup added. If there is any storage, transportation or other cost incurred by the seller in delivering the item to the buyer, that will be added to the cost. The markup can either be a lump sum or a percentage of the price of the goods. The delivery of the goods is immediate. The client can pay on spot or pay deferred. Sales mostly is on deferred payment, so credit is extended, and this is used as a method of finance when the customer requires funds to buy goods. Deferred payment also has the option of the full amount at a deferred period or in instalments, the latter being more common. Thus, Murabaha provides the customer with the advantage of acquiring and using the asset, earning profit from it and using this profit to repay in deferred instalments. Murabaha is a Shariah-compliant instrument since the bank first acquires the asset for resale at profit along with the risk associated with purchase and resale, so an asset is sold for money and the transaction is not an exchange of money for money. There are two types of Murabaha.

- Ordinary Murabaha. The client asks the bank to acquire an asset that they would like to purchase without making any promise to buy it.

- Murabaha sale with a promise (also called Murabaha to the purchase order). The client makes a promise to buy the item once the bank acquires it. This type is more common as Islamic banks want to guarantee that the client will buy what they asked the bank to acquire for them.

In Murabaha with a promise the client has the risk of the goods not being delivered as per specification and at contracted time, while in the case of ordinary Murabaha the entire non-delivery risk is with the bank.

So, Murabaha is a sale and purchase agreement between the bank and its client. The bank sometimes may not prefer to buy the item itself due to legal restrictions, or because it does not have sufficient knowledge, and appoints the client as an agent to make the purchase. In such a situation, the client may take delivery of the item but the ownership will go to the bank. The bank may take security as a mortgage, guarantee, charge or lien to protect itself against default of the deferred payments. In case of default the bank may sell the security and recover its dues, but will make no profit and any excess remaining from the sale of the security will be returned to the client. Under Shariah rulings Islamic banks cannot charge a late payment fee, or if they do charge the bank cannot benefit from it and it is given away to charity. On the other hand, Islamic banks can charge for any costs they incur to recover the payments from the client.

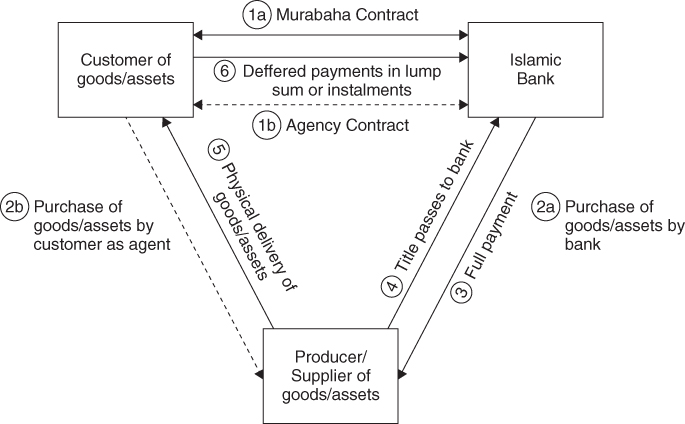

Figure 4.1 is an overview of a Murabaha contract.

FIGURE 4.1 Murabaha contract

CONDITIONS RELATED TO MURABAHA

Murabaha contracts executed between an Islamic bank and a client are characterized by various conditions.

- Conditions of sale contract. Murabaha from an Islamic bank is not a loan in exchange for interest payment as in a conventional bank, but the sale of a good or service. As such, Murabaha needs to fulfil the Shariah requirements of a valid sale – that is, the item of sale must exist at the time of the sale and be owned by and in the physical or constructive possession of the seller at the time of the sale.

- Goods subject to Murabaha contract. These items need to be legal and Halal, having real commercial value. The items can be tangibles like vehicles, machinery, equipment and intangibles like brand name, trademark, copyright, patent, royalties, etc. Currencies and other mediums of exchange, like gold or silver, cannot be traded by Murabaha as they cannot be exchanged on a deferred basis.

- Costs related to the Murabaha item. All direct and indirect costs, including the original cost of the item plus all other costs (e.g. packaging, transportation, delivery, installation and any agency costs), need to be identified and both the buyer and the seller should be aware of them and mutually agree to them.

- Markup or profit. This can be a fixed amount or a percentage of the cost of the Murabaha item. This amount will constitute the Islamic bank's profit and for the Murabaha client or buyer it is the extra cost incurred for the advantage of deferred payment. The markup or profit will be clearly stated and mutually agreed by the bank and the client and cannot be changed later.

- Third-party seller. The seller of the good or service in a Murabaha needs to be a third party, besides the client and the Islamic bank.

- Client's promise. To reduce its risk, the bank may require the client to sign a unilateral promise to buy the goods once they have been acquired by the bank and in Western jurisdictions like the UK or the USA, this promise is binding. This is called Murabaha with a promise.

- Binding promise. In Murabaha, when the two parties contract it is morally binding on both. However, if the bank – while relying on the promise – takes the necessary steps to acquire the property then the promise becomes legally binding.

- Defects in the item. If there are any defects in the Murabaha item, the seller needs to inform the buyer or else it would be a betrayal and the buyer can demand compensation or the sale can be cancelled. Moreover, any risk of loss of the asset before delivery, or risk related to any concealed defects in the asset, are borne by the bank.

- Ownership of the item. Murabaha is Shariah compliant because the bank needs to acquire the ownership and physical or constructive possession of the asset, thus assuming that all risks associated with it before reselling to the client; in contrast, the conventional bank simply lends the money to the client to acquire the asset without taking any risk related to the asset.

- Advance payment or deposit. The client may be required, or want, to make an advance payment or a deposit, which is part of the price and is adjusted from the price during repayment. This is allowed by Shariah.

- Delivery of the item. This is immediate, and after delivery the client bears the risk of the item as the sale has concluded.

- Repayment. This can be spot or deferred, made in a lump sum or in instalments. The payment schedule and sequence of transactions should be mutually agreed upon before Murabaha is concluded.

- Security. The Islamic bank may ask the client to provide some security or guarantee, or sign a promissory note to fall back on in case of non-repayment. The asset purchased via the Murabaha transaction can serve as the collateral.

- Delayed repayment. If repayments are delayed, then conventional banks charge interest on interest but Islamic banks cannot increase the price or the markup. This may sometimes motivate customers to delay payments. To discourage this, Shariah scholars allow the Islamic bank to charge a penalty for delayed payment, but they cannot benefit from this money and it is donated to charity.

- Failure to repay. According to Shariah rulings, if a solvent debtor deliberately delays or fails to repay, then legal action can be taken; if the debtor is insolvent, leniency in repayment is recommended.

CALCULATION OF MURABAHA PROFIT

The Arabic root word Ribh means gain or profit and is the foundation for the term Murabaha. Murabaha is an Islamic banking contract of sale, where the bank purchases an item at the request of the client and resells it to the client at a mutually agreed profit or markup. Outwardly the critics of Islamic banking find Murabaha markup to seem the same as interest, especially since the markup amount is fixed. The markup amount can be calculated in two ways. It is either a lump sum amount or it can be a percentage of the cost of the item of sale. For example, a client may purchase a car worth £100,000 and the markup may be decided as a lump sum amount of £8,000 or it could be decided as 8% of the original cost of the item, making the final sale price £108,000. In both cases the client and the bank are both aware and mutually agree to the original cost and the markup method and amount. A Murabaha contract and the markup added to the cost of the item of sale are both Shariah compliant because the Islamic bank is required to buy, own and bear all ownership risk of the item before selling it to the client. To compare: in the case of a conventional bank it sells the funds to the client at the price of interest, which is the time value of money; in the case of an Islamic bank it sells the asset to the client at a marked-up price and hence is Shariah compliant as this is not the same as selling the money. The deferred instalments of repayment of Murabaha usually include in proportion both the cost and the markup of the item of sale. The margin of profit, or net margin, is a ratio calculated by dividing net profits by sales and in case of the Murabaha it is calculated by dividing the markup amount by the sales price and it shows the degree of profit made in the contract.

In case of deliberate delay or failure to repay the due instalments by the Murabaha clients, as per Shariah rulings a penalty can be charged, to discourage clients from delaying, but the penalty cannot benefit the Islamic bank and is required to be distributed to charity. Moreover, legal proceedings and court action can also be taken against the client. In the case of insolvency of the client, the Islamic bank does not have the authority to charge the client with a penalty.

THE MURABAHA PROCESS

The steps involved in an ordinary Murabaha contract are as below:

- A prospective client or buyer requests the Islamic bank to buy a specific item or asset, promising to buy it from the bank for a profit. According to Shariah scholars this is an invitation by the client to the bank to enter a contract, but not a commitment yet.

- If the bank accepts this invitation they are required to source the item or asset as per client specifications, pay for the item and buy and own it with all ownership-related risks.

- The bank then makes the formal offer to the prospective buyer.

- The prospective buyers have the option to accept the offer and buy the item or asset or go back on their word. If they accept the offer a Murabaha contract is executed.

This leaves the bank with a major risk of being left with items or assets that were purchased for prospective clients who finally did not buy them. Since the bank is not a retailer of commodities, this can cause major problems. To avoid this, Shariah scholars have allowed banks to accept requests from clients tied up with a promise to buy. In contemporary Islamic banking, most Murabaha contracts are executed on this basis and the steps to be followed for a Murabaha with a promise contract are as below.

- The client approaches the bank with a request to purchase a specific item or asset.

- The Islamic bank sources the appropriate vendor for the item and identifies the total relevant cost.

- The bank then negotiates with the client on the item, its costs and the applicable markup.

- If the client agrees to the above conditions, it makes a request with a promise to buy.

- The bank and the client sign a joint agreement, by which the bank agrees to buy the specified item and sell it to the client at the cost plus an agreed markup and the client promises to buy the item once the bank has acquired it. Alternately, the bank may assign the client as the agent to buy the asset on behalf of the bank, especially if the client has some experience, skill or other advantages with the vendor or in purchase of the asset. In this case, a separate agency or Wakala contract would be drawn up between the bank and the client.

- Whether the bank buys directly from the vendor or buys via the agent, the client, a sales contract is executed between the bank and the vendor.

- The bank or its agent, the client, then purchases the asset from the vendor, pays the original price and all other relevant costs.

- A Murabaha contract is drawn up between the bank and the client for purchase of the asset at the original price, plus all other relevant costs, and a markup. The contract also clearly details the repayment schedule.

- The bank delivers the asset to the client, or the client takes delivery directly from the vendor and is in physical possession of the asset, but the ownership title passes to the bank.

- The client next accepts the Murabaha contract and the sale is executed between the bank and the client and ownership of the asset is transferred to the client.

- The client pays the bank over the contract period either as a lump sum in the future or in instalments over the deferred period.

Three parties are involved in completing the Murabaha contract involving the purchase and sale – the bank, the vendor and the client. The Murabaha contract may include an advance deposit called the Arbun. This is an amount of money that the client pays to the bank in advance when signing the agreement but before the bank purchases the asset. Arbun is paid on request by the bank and it ensures the client's commitment and seriousness in acquiring the asset. If the client completes the Murabaha contract, the Arbun will be considered as part payment against the agreed price of the asset. If the client does not fulfil the Murabaha contract, the Arbun would be treated differently, depending on the type of Murabaha contract. If the contract was binding as in the Murabaha with a promise, and the client later refuses to purchase the asset, the bank can use the Arbun amount to cover any loss it incurred in purchasing the asset and not being able to sell it. If the Arbun is not sufficient to cover the bank's loss, it can demand the balance from the client. On the other hand, if the Murabaha contract is not binding (it is an ordinary Murabaha), the Arbun needs to be returned to the client.

PRACTICAL APPLICATIONS OF MURABAHA

Being a simple cost-plus sale with deferred repayment, Murabaha is widely used by Islamic banks. Some common uses of the Murabaha are as follows.

- Retail finance. Includes home financing, vehicle financing, other personal durables financing for households, to finance their medium and long-term needs for assets like cars, homes, household furniture, equipment, etc.

- Working capital financing. Businesses purchase raw materials and meet other working capital and short-term needs with Murabaha.

- Business medium and long-term financing. Businesses use Murabaha to purchase land, buildings, equipment, machinery and vehicles with medium and long-term repayment schedules.

- Syndicated loans. When the financing needs of the business are large, or the project is too risky for one Islamic bank, two or more Islamic banks come together for a joint Murabaha financing, called a syndicate. One of these banks, called the lead bank, is appointed to manage the Murabaha contract and liaise with the client.

- Trade finance. This includes imports, exports, bills of exchange and letters of credit. The process of letter of credit (L/C) financing using the Murabaha contract involves:

- The importer or customer asks the Islamic bank to open a L/C to import goods and provides all necessary information.

- The bank checks the application and documents, secures the necessary guarantees and then opens the L/C in favour of the customer.

- Copies of the L/C are sent to the correspondent bank and the exporter.

- A Murabaha with a promise contract is signed between the Islamic bank and the importer, where both parties mutually agree on the costs of the goods and all other delivery costs and conditions.

- The exporter ships the goods and hands over the shipping documents to the correspondent bank.

- The correspondent bank sends the shipping documents to the Islamic bank.

- The Islamic bank's ownership of the goods is confirmed once it accepts the documents.

- The Islamic bank finally sells the goods to the importer on a cost plus markup basis.

- The importer pays the bank on a deferred basis – lump sum or instalments as per the mutually agreed schedule.

TAWARRUQ, REVERSE MURABAHA OR COMMODITY MURABAHA

Tawarruq or reverse Murabaha is a financial instrument where the client purchases a commodity from a seller, via an Islamic bank, on a deferred payment basis and then the client appoints the Islamic bank to sell the commodity to a third party on a spot payment basis. In a practical sense, the client raises immediate cash and will repay it in the future in instalments. Tawarruq is used by retail customers to raise personal finance and for businesses to raise short-term liquidity as well as working capital. Islamic banks themselves use Tawarruq to manage their short-term cash shortage or surplus. This provides an alternative to the conventional interbank liquidity market.

As in any Murabaha contract it involves a sale with deferred payment in instalments. Usually, to provide this short-term financing, a base metal is used as the underlying asset, and as such this product is also called commodity Murabaha. The price of the commodity, the markup amount or percentage, the purchase date and the repayment schedule are all mutually decided between the two parties. Once purchased via Murabaha on deferred payment, the Islamic bank sells the commodity on spot in the market and thus raises short-term funds for its own liquidity management or as an agent for its client. The commodities suitable for Tawarruq are those that are widely available, unique and not perishable. As per Shariah restrictions, commodities previously used as money (gold, silver, barley, wheat, etc.) cannot be used for Tawarruq. A disadvantage of Tawarruq is that some cost is involved for both the buy and sell part of the transaction.

From the Shariah-compliance perspective Tawarruq is a controversial product, since the client does not purchase the commodity for their use and the transaction is not linked to any real economic activity, so some scholars believe it is just raising cash and thus creates Riba. Other scholars permit it since it involves two Shariah-compliant contracts, the first being a Murabaha and the second being pure sales, and provided that clear ownership transfer of commodity happens and purchase and sales transactions are independent of each other. The AAOIFI has also permitted Tawarruq and developed a set of standards for Tawarruq. This product is used more in South-East Asian countries, rather than in GCC countries.

Tawarruq is allowed if built as a hybrid sale, where the customer buys the item (usually a commodity) from the bank on deferred instalment payments, then sells the commodity to a third party for immediate cash. Controversy exists about Tawarruq since on the surface it appears that money is currently being exchanged for money that will be paid later. Some Islamic scholars consider Tawarruq acceptable if the client requires the money for themselves and not to lend it to someone else, have no other cash financing option available, the sale has no link to Riba and the client takes possession of the item, physically or constructively, before selling it again.

CHALLENGES AND PROBLEMS ASSOCIATED WITH MURABAHA

Even though Murabaha is the simplest of the Islamic banking products being used today, and is widely used, it is not without criticism or issues. Some of the frequently discussed challenges and problems faced by Murabaha are listed below.

- Murabaha assets. A Murabaha contract can only be executed for a permissible Halal asset.

- Appears like interest. Outwardly, to someone not very familiar with the construction of Islamic banking products, the fixed repayment instalments may appear like interest, which can cause doubts amongst Muslim customers or be the reason for criticism from those who do not agree that Islamic banking is any different from conventional banking. In reality, the markup is determined as a lump sum amount or as a percentage of the cost of the item and added to the cost to derive the Murabaha price that is repaid, deferred in fixed instalments. Both parties are aware of and mutually agree to the cost as well as the markup.

- Interest-based benchmark. One of the challenges for Islamic banks related to Murabaha is to decide the markup. Whether to use a lump sum amount or a percentage of the cost of the item. In case of a percentage, what percentage should be used? Due to the absence of an internationally accepted Islamic profit benchmark, and to stay competitive with conventional banks, most Islamic banks use the LIBOR as a benchmark to decide the markup. For example, the markup could be LIBOR +3%. This practice is not against the Shariah according to scholars, since interest is not being used, it only serves as a guideline for choosing a markup that will be competitive with the conventional banks, while all other Murabaha conditions are followed. The use of an interest-based benchmark to identify market acceptability of the Islamic banking profit does not make the Murabaha contract invalid.

- Uncertainty or Gharar. LIBOR is a variable interest rate and using it to decide the Murabaha markup can introduce uncertainty or Gharar, which is prohibited in the contract according to some critics. Meanwhile other scholars opine that both parties agree on the LIBOR benchmark in advance, thus there is no uncertainty. To remove this doubt further, Islamic banks sometimes use the LIBOR to identify the markup at the onset of the contract only, add it to the cost and calculate fixed repayments over the deferred period. There is then no uncertainty, as the variability of LIBOR over the period of the Murabaha does not affect it.

- Risk of ordinary non-binding Murabaha. In case of an ordinary Murabaha, once the bank acquires the asset, the client may refuse to buy it from them. The bank would then be left with an asset for which it may not be able to find another buyer soon, thus incurring other costs for holding the asset. To avoid this risk, Islamic banks mostly execute the Murabaha with a promise which is binding on the client once the asset has been acquired.

- Legal implications of the Murabaha with a promise. The Islamic Fiqh Academy's opinion is that any commercial promise is binding on the promisor when the promise is one-sided as it is in Murabaha. When, due to this promise, the second party buys something and if the promisor goes back on their word, then the second party is liable to loss. In this case the Shariah courts can enforce the purchase of the asset or require the promisor to compensate the second party.

- Ownership risk. When the bank acquires the Murabaha asset, any risk related to ownership is the bank's risk till the sales contract is completed and the asset is delivered to the client. The asset may have defects, or the quantity may be less, and these are all the bank's risks. The bank needs to provide acceptable quality and required quantity of the asset to the client as per the specifications in the Murabaha contract.

- Rescheduling of payments or rollover. Conventional banks usually have no issues with rescheduling or rolling over loans, since they charge interest as the time value of money and with the expansion of the repayment period they earn more interest, and may even apply a new interest rate for the new period. Islamic banks cannot rollover Murabaha since it is a sale and not a loan, and the ownership has already passed to the client. If, considering the client's inability to repay on time, they allow rollover, they cannot increase the markup amount as this will be tantamount to the time value of money and prohibited in Shariah.

- Deliberate delay in payments. Murabaha is a sales transaction with deferred payments, and as such Islamic banks cannot increase the sales price or markup amount in case of delayed payments, unlike conventional banks that charge additional interest. Dishonest clients sometimes take advantage of this. To reduce or avoid this tendency, Shariah scholars allow charging of a penalty for delayed payment or default to discourage unnecessary delay in payments. As per Shariah requirements though, Islamic banks cannot benefit from this penalty and are required to give it away to charity.

- Collateral or guarantee. Contemporary Shariah scholars have allowed Islamic banks to ask the client to provide some sort of security, for example a mortgage on the asset purchased by the Murabaha or any other kind of lien, to provide some protection to the bank against default or deferred payments. Security can be taken from the customer only after the sales transaction has happened in Murabaha and the client has a liability to repay, but the details of the security can be provided earlier. Moreover, third-party guarantees are also allowed in case of Murabaha under certain specific conditions, where the guarantor is required to make the deferred payments if the client fails to do so.

- Early payment discount. This is allowed in conventional banking, but in case of Islamic banking a compulsory discount, if the client pays before the scheduled date, is not permissible and as such cannot be part of the Murabaha contract. The bank may voluntarily pay the client some discount for early payment.

- Buy-back arrangement. These are prohibited in Shariah as such Murabaha contracts cannot be implemented for assets already owned by the client, where the client first sells to the bank and then buys back.

- Tax implications and ownership issues in non-Muslim jurisdictions. The two levels of sales transactions – between vendor and bank and then between bank and client – involve two tax events, thus causing double taxation, which makes Murabaha transactions more expensive than conventional loans in Western jurisdictions. Moreover, the markup may also be viewed as a capital gain, leading to capital gains tax in non-Muslim jurisdictions that do not formally recognize Islamic banking. Another challenge in these jurisdictions is that Western banks are not allowed to act as principles in taking title to properties and this can cause major problems in Murabaha where the Shariah requires the bank to take title to the asset and then sell it to the client.

- Securitization of Murabaha. Murabaha cannot be securitized as a negotiable instrument like Sukuk and traded in the secondary market, the reason being that once the Murabaha sale has been implemented the client owns the asset and also has a liability for deferred payments to the bank. This constitutes a certain amount of money, which cannot be traded as this amount is fixed and cannot be traded at a higher or lower price.

COMPARISON OF MURABAHA WITH CONVENTIONAL LOANS

A Murabaha contract is most commonly compared with regular loans from conventional banks. Table 4.1 highlights the most common differences between these.

TABLE 4.1 Differences between Murabaha and conventional loans

| Factors | Murabaha | Conventional loan |

| Type of contract | Sales contract. | Loan contract. |

| Product description | The client requests the bank to acquire and sell an asset to it. The bank buys and resells the asset to the client at the cost and markup price, where both the original cost and markup are known to both parties and mutually agreed. | The client asks the bank for a loan and the bank lends the agreed amount of money, charging interest at a fixed or variable rate on the principal amount. |

| Repayment | Repayment is specified in a schedule and is most often deferred, either as a lump sum or as instalments. | Repayment is specified in a schedule. If interest is fixed, the schedule will be unchanged over the period. If interest is variable, the schedule will also be variable. |

| Relationship of the bank with the asset | A major requirement of Murabaha is for the bank to own the asset, physically or constructively, and then resell to the client. In summary, the bank sells the asset. | Conventional banks only lend the funds and have no relationship to the asset. In summary, the bank sells money. |

| Profit margin for the bank | The bank has a fixed margin since the cost plus the markup is decided at the onset of the contract. | The bank usually has a variable margin, since most often the interest rate is variable. Even if the rate is fixed, it is usually fixed for a limited period and then becomes variable. |

| Risk related to the asset for the bank | If the asset delivered by the vendor has any defect or deficiency, the bank bears the risk and cost as owner. | The bank only provides the funds; the client is the owner of the asset and bears all risk or cost of defect or deficiency in the asset delivered by the vendor. |

| Extension of repayment | The bank may extend the repayment dates but no additional markup or penalty can be charged. | Repayment date extension is technically an extension of the loan and will lead to an increase in interest. |

| Early payment discount | An early payment discount cannot be built into the Murabaha contract as per Shariah rulings and cannot be mandatory. The bank may provide some discount voluntarily. | In most loan contracts, an early payment discount is built in and early payment also leads to less interest expense. |

| In case of default | The bank can sue the client and demand payment. | The bank can sue and demand payment as well as additional charges. |

KEY TERMS AND CONCEPTS

- Binding promise

- Markup or profit

- Murabaha or trust sale

- Murabaha process

- Murabaha sale with a promise

- Ordinary Murabaha

CHAPTER SUMMARY

Murabaha is one of the simplest and most widely used Islamic banking products. It is an alternative to conventional loans. In the Murabaha contract the bank purchases the asset required by its customer and then resells at a marked-up price. Important conditions related to the Murabaha contract are that it needs to meet the Shariah requirements of a valid sale, be only for Halal items and all direct and indirect costs related to the item and the lump sum or percentage of markup should be known to both parties. Other conditions are that the original seller of the item needs to be a third party, the bank may demand a promise to buy from the client, all risk of the item prior to sale to the client is the bank's, the bank may ask for an advance deposit or collateral from the client, delivery is immediate while repayment is spot or deferred, as a lump sum or in instalments.

The ordinary Murabaha process involves a client requesting the bank to acquire and resell to it any specific asset without a concrete promise to buy, leading to significant risk for the bank. In contrast, the more commonly used Murabaha sale with a promise includes a binding promise by the client to buy the asset once the bank has acquired it, thus significantly reducing bank risk. Murabaha is widely used for both retail and corporate customers as well as in trade finance and syndicated financing. Controversially, reverse Murabaha is used as personal finance or short-term financing for corporates or as a liquidity management instrument for the banks themselves.

Despite its simplicity, Murabaha faces challenges related to being applicable for Halal assets only, the markup appearing like interest, LIBOR being used as a benchmark, variability of LIBOR causing Gharar or uncertainty, ownership risk of the bank for defects in the item, delay or default in repayment and, unlike conventional finance, that Murabaha does not allow a compulsory early payment discount, buy-back arrangement, rescheduling of repayments, etc. Murabaha also faces tax issues in non-Muslim jurisdictions, since the markup is not treated with tax exemption as is interest for conventional loans.

Murabaha and conventional loans though are used as alternatives in the industry; they differ from each other in relation to the type of contract created, the relationship and risks of the bank related to the asset, early repayment, delayed payment or default and, of course, the contrast of interest versus markup.

END OF CHAPTER QUESTIONS AND ACTIVITIES

Discussion Questions

- What are the three requirements of a Shariah-compliant sales contract?

- Define Musawama.

- What does a Murabaha contract mean?

- What are the types of Murabaha contract? Describe them all.

- Which kind of Murabaha contract is more commonly used by the banks? Why?

- Write down any 10 conditions related to a valid Murabaha.

- How is the Murabaha profit calculated?

- Describe the process for ordinary Murabaha.

- Describe the process for a Murabaha sale with promise.

- Discuss some practical applications of the Murabaha contract in modern Islamic banking.

- What is Tawarruq? Discuss the controversy related to this product.

- Discuss the challenges and problems related to the Murabaha contract in modern Islamic banking.

- Compare the Murabaha contract with a conventional bank loan.

- Suppose that bank A buys a car for client B, and resells the car to the client. The bank and the client are both aware of the sales price to the client and mutually agree, but the cost of the car to the client is not disclosed to the client and is known only to the bank and the car dealer. Does this transaction meet the requirements of a valid Murabaha contract? Explain your answer.

Multiple Choice Questions

Circle the letter next to the most accurate answer.

- Which one below is not a Shariah requirement for Murabaha?

- Existence of the asset

- Existence of a sales contract

- Sales price to be specified later

- Sales is on deferred payment

- Murabaha is executed when:

- Money is sold for money

- A good or service is sold for money

- A commodity is sold for a commodity

- A commodity is sold for a service

- Which restriction below is not applicable for Murabaha:

- No rollover is allowed

- No late penalty can be paid to the bank for its income

- No price renegotiation is allowed

- No profit can be charged on the asset sold by the bank

- Tangible and non-tangible goods subject to Murabaha must be:

- Halal

- Real

- Have commercial value

- All of the above

- Which statement below is most applicable for a Murabaha?

- Murabaha is a sale of items at a price including cost of purchase minus profit margin, mutually agreed by buyer and seller

- Murabaha is a sale of items at a price including cost of purchase plus profit margin, mutually agreed by buyer and seller

- Murabaha is rent of an asset

- Murabaha is a loan of funds

- A Murabaha transaction is considered as Shariah compliant if:

- It deals with either tangible or intangible goods

- The buyer is aware of the original cost of the goods and any additional costs incurred in the process of procuring the goods

- The margin of profit on the goods is mutually agreed between the buyer and seller at the beginning of the contract

- All of the above

- If the buyer defaults:

- The bank can renegotiate the price

- The bank can charge late payment fees

- The buyer pays a penalty that is donated to charity

- The bank can do nothing

- Eman wants to purchase a car, priced at (Qatari rial) QAR100,000 with a Murabaha contract from Q Bank. The bank's required markup is 5%. How much will Eman pay each month if the total repayment period is 5 years?

- QAR2,500

- QAR1,750

- QAR1,500

- QAR1,250

- A customer needs financing to purchase a machine for their factory and plans to use a Murabaha. Which structure below appears most accurate?

- A Murabaha is structured between the Islamic bank, the manufacturer of the machine and the customer and the manufacturer sells the machine directly to the customer while the bank pays the manufacturer directly

- A Murabaha is structured between the Islamic bank, the manufacturer of the machine and the customer, creating two sales contracts: one where the manufacturer sells to the bank and the second where the bank sells to the customer

- A Murabaha is structured between the Islamic bank, the manufacturer of the machine and the customer such that the bank lends money to the manufacturer to build the machine and then the bank sells it to the customer

- A Murabaha is structured between the Islamic bank, the manufacturer of the machine and the customer such that the bank lends money to the manufacturer to build the machine and then rents the machine to the customer

- A corporation contracted with an Islamic bank using the Murabaha contract to purchase a fleet of trucks from a manufacturer. Is it allowed for the corporation to take delivery of the trucks directly from the manufacturer?

- Allowed, if legal title to the trucks passes to the bank prior to delivery to the corporation

- Allowed, if legal title to the trucks passes to the bank after delivery to the corporation

- Not allowed, because the bank must take both legal title and physical possession of the trucks before delivering them to the corporation

- Not allowed, because the bank must take physical possession of the trucks before delivering them to the corporation, while legal title can pass directly to the corporation

True/False Questions

Write T for true and F for false next to the statement.

- Musawama and Ijara are two types of Murabaha.

- Murabaha is usually a deferred credit sale.

- Murabaha profit is mutually agreed between bank and client.

- The bank acts as a middleman in Murabaha.

- In Murabaha, the client is informed of the cost of the asset, the markup is not required to be disclosed.

- In Murabaha, the price of goods is decided later.

Calculation Problems

- Bintang has arranged to purchase a house costing (Indonesian rupiaya) IDR2 million on a Murabaha basis from Indonesia Islamic Bank. All other indirect costs of acquiring the property are IDR50,000. The bank agreed on a reasonable profit rate of 8%. The repayment will be made monthly over 20 years. How much will the price of the house be to Bintang? How much will Bintang have to pay each month?

- Shamma wants to purchase a Nissan Patrol SUV, priced at (Pakistani rupee) PKR360,000 at Pak Automobiles. She wants to finance the car on a Murabaha basis from Pak Islamic Bank. The bank's required profit markup for the car finance is 3.5% per annum for a repayment period of 5 years. Compute the total cost of the car with the markup. How much will the monthly payment on this Murabaha auto-financing be?

- Adam approaches the Islamic Bank of Arlington in the USA to finance the purchase of an industrial washer-dryer for his laundry business at USD10,000. The bank agrees to purchase the machine from the manufacturer and then sell it to Adam for USD12,000, which is to be paid by Adam in equal instalments over the next 3 years. What type of Islamic financing is being offered by the bank to Adam and how much is the monthly instalment?