CHAPTER 8

Salam

INTRODUCTION TO SALAM

Under Islamic Shariah law, to be valid, all sales contracts need to meet certain conditions. These are that the asset, which is the subject of the contract, needs to exist at the time of the contract. Moreover, the asset should be owned by the seller and be in physical or constructive possession of the seller. Islam allows practical flexibility in its rules, as needed by the community to perform various business transactions legally and conveniently. Salam and Istisna are the two Islamic finance products that do not follow these Shariah regulations, and they are the permitted exceptions.

In the case of a Salam contract, the payment is made fully in advance at the time of the contract and the delivery of the asset is deferred to a specific time in the future. A Salam contract is like a forward sale contract in conventional finance, with advance payment and deferred delivery. The buyer of the asset is called the Muslam, the seller is the Muslam Ileihi, the payment for the asset is called the Ras al Maal and the purchased asset or commodity is the Muslam Fihi.

Most Salam contracts are short term, though they can be for the medium or long term, and are used for production finance. As such, Salam is more of a trade contract and not a loan. Salam contracts are most suitable for homogenous goods, which have commodity-like characteristics and are freely available in the market, like sugar, coffee, oil, cotton, etc. Any assets that have unique characteristics (farm animals, precious stones, etc.) are not suitable for Salam contracts. Though the asset or commodity does not exist at the time of the contract, a detailed description, quality and quantity needs to be specified in the contract. Salam contracts are suitable and commonly used to finance transactions in agriculture, trade, construction, manufacturing, project finance and working capital.

In the Murabaha contract as elaborated in Chapter 4, the asset is delivered in spot while the payment is a deferred lump sum or instalments and the price includes a markup, and thus is higher than the spot price. A Salam contract is the opposite of Murabaha, where the payment is made in spot in advance and delivery is in the future. The price paid with Salam is often a discounted price, which is less than the price if delivery is made in spot.

IMPORTANT CHARACTERISTICS OF THE SALAM CONTRACT

Goods suitable for Salam. Not every asset or good is suitable for Salam. Goods that are homogenous in character and which are traded by counting, measuring or weighing according to usage and the customs of trade are more suitable for Salam. These goods should normally be expected to be available at the time of delivery. Commodities like oil, wheat, sugar, etc. can be transacted easily using Salam, and as such it is commonly used for agriculture and trade financing. Goods whose quality or quantity cannot be determined by exact specifications cannot be sold through the contract of Salam. Also, goods that are not the same cannot be sold using Salam. For example, farm animals which are each different, precious stones which are each of distinct size, shape, clarity, etc.

Clear specifications of the goods, including description, quantity and quality, should be provided to avoid any uncertainty or Gharar. When goods are sold by Salam, it is essential to clearly specify the attributes of the contracted goods, but none of these goods can be directly tied up to any specific source of supply, like a specific farm for an animal, a specific tree for fruit or a particular oil field for oil. Any source should be acceptable if the goods meet the required specifications. Salam cannot be used for items that are termed Ribawi items (money-like items), which can be exchanged only at spot – for example gold and silver.

Price of the Salam contract. The buyer pays the price fully in advance at the time of the contract. If the full amount is not paid in advance, then the debt of future payment is exchanged for the debt of supply of goods in the future, and this is tantamount to a sale of debt against debt and thus is prohibited. The price in Salam is most often set at a level lower than the price of the same commodities delivered at spot; the difference between the two prices is the benefit for the buyer.

Delivery date and place. The exact date and place of the delivery needs to be mutually agreed between the seller and the buyer, and should be clearly specified in the contract. On that date in the future and at the designated place, the seller commits to supply a specific quantity and quality of certain goods to the buyer, who has already paid the price in full in advance at the time the sales contract was made. The date and place of delivery can only be changed by mutual consent of the two parties. For the contract to be completed, there should be actual delivery of the goods. A Salam contract cannot be executed for items which must be delivered on spot and not in the future. Moreover, the goods should be such that they are readily available on the date of delivery.

Buy-back condition. In a Salam contract, the buyer cannot demand a buy-back condition from the seller, which would require the seller to buy back the goods delivered. Shariah ruling does not allow the buyer to sell back the commodity to the original seller. However, some scholars opine that once the buyer has taken delivery of the items, with physical or constructive possession, the buyer can enter into a separate sales contract with the original seller which is completely independent of the original Salam contract.

Security and guarantee. It is permitted in a Salam contract for the buyer to ask the seller to provide security to ensure timely delivery of the commodity. Acceptable securities could be a guarantee, a mortgage, a hypothecation or a performance bond. A Salam contract is not a liability of money but is a debt obligation of the contracted goods. If the seller fails to deliver the commodity as per specifications on the assigned delivery date, and at the assigned delivery place, the buyer may reject the contract and execute the performance bond, or may sell a mortgaged asset or the hypothecated items to recover their original price and any other incidental loss, or may require the guarantor to pay the requisite amount. Since a Salam contract is a debt obligation of goods not money, it is permissible to take a guarantee or security up to the value of the goods. Guarantees, security or performance bonds can be taken to ensure delivery on the due date, failure of which can lead to cancellation of the contract and exercise of the security.

Penalty. A penalty can be agreed upon in the Salam contract at the onset which is liable on the seller if there is any delay in delivery of the contracted commodity to the buyer. The seller may also be liable to pay a penalty for delayed delivery, calculated as a percentage per day of delay, but this penalty needs to be donated to charity. The buyer can also approach the relevant courts for an award of damages, at the discretion of the courts and determined based on all direct and indirect costs incurred, but excluding any time value of money. The courts may also provide permission to sell the security provided by the seller to recover the losses of the buyer.

Termination. Once the Salam contract has been signed, none of the parties can revoke it unilaterally. Termination can only be executed with mutual consent of both parties.

HISTORY OF THE SALAM CONTRACT AND ITS SHARIAH ACCEPTABILITY

During the time of the Prophet, Salam contracts were used in agriculture. When the Prophet migrated to Medina, it was common for people there to pay in advance the price of fruits to be delivered later. The Prophet specifically said that whoever pays in advance for dates, to be delivered later, should have a contract that clearly specifies the weight and measure of the dates.

A Salam contract was allowed by the Prophet subject to certain conditions. The main utility of the Salam contract was to meet the needs of small farmers who needed money to pay for the expenses of growing their crops, especially dates, and to provide for their families till the harvest period. With the advent of Islam, when Riba or interest was declared prohibited, these farmers could not accept any interest-based loans. As such, they were permitted to sell their agricultural produce before they harvested it. During the same time, Arabian traders were involved in exports of certain commodities from their home country to other places and imports of other goods from those places to their own country. These traders were also in need of funds to conduct their export and import business and were not able to approach the interest-based money lenders. Salam financing was applicable for the traders also. Salam is a kind of debt, since the seller is liable to provide for the contracted goods, at the specific date. To remove all uncertainty, the Prophet said that all who sell based on Salam must sell a specific volume and a specific weight, on a specific due date.

The delivery date is very important in the Salam contract, since the asset needs to be delivered to the buyer on that date, and if the seller has not been able to acquire or produce by the contracted date, they may have to purchase it from the open market and deliver on the due date. Both the buyer and the seller are aware of the price and the date of delivery of the contract. Moreover, the seller is taking the risk of not delivering on the due date and being required to pay a higher price in the open market, while the buyer takes the risk of the asset being cheaper in the spot market on the contracted future delivery date. Since both parties assume risk and are aware of all details, the Salam contract is free of Gharar and Maisir.

BENEFITS OF THE SALAM CONTRACT

The Salam contract along with Istisna, to be introduced in Chapter 9, are the two exceptions to the Shariah conditions of a valid sales contract of the asset being in existence, owned and in physical or constructive possession of the seller at the time of the contract. This flexibility in the Shariah rules is beneficial when executing various business transactions where the seller requires advance payment to produce or acquire the asset to sell. A Salam contract is beneficial to the sellers because they receive the price for the commodity in advance and can utilize it as a Shariah-compliant financing alternative, and are able to avoid any involvement with interest-based financing.

A Salam contract also benefits the purchasers by providing assets or goods at a discounted price, since the advance price is lower than the spot price. This is possible since the purchaser is willing to pay in advance and thus is providing financing for the business venture producing or acquiring the asset or commodity, which encourages the seller to offer a price discount. Usually, the Salam buyer expects the price to increase in the future.

ROLE OF ISLAMIC BANKS IN SALAM AND THE PARALLEL SALAM CONTRACT

Salam contracts are gaining in popularity amongst the modern Islamic banks operating around the world. Islamic banks can provide Salam financing by entering into two separate Salam contracts: the first is called a Salam contract and the second is called a parallel Salam contract. A second way for Islamic banks is to participate in one Salam contract and then in an instalment sales contract, like Murabaha.

The Islamic bank acts as the buyer of the asset or commodity in the first Salam contract and then enters into the second Salam contract, the parallel Salam, as a seller of the acquired asset or commodity from the first Salam contract that it will now sell and deliver to the buyer in the parallel Salam. Shariah rules require these two Salam contracts to be completely independent of each other. There must be two different and independent contracts, they cannot be tied up and the performance of one should not be contingent on the other. Parallel Salam is allowed with a third party only. Any liability arising from either contract would not affect the other contract.

The Salam and parallel Salam contracts together would involve three parties, the bank being the common party in both contracts. In the Salam contract the bank would commit to buy a certain quantity and quality of the asset or commodity from the supplier or manufacturer that will be delivered in the future at a specific date and place, and pay the full contracted price in advance upfront. This price is usually less than the spot price at the time of the contract. The bank then enters the parallel Salam contract as a seller of the exact same quantity and quality of the asset or commodity it purchased earlier in the Salam contract; the other party in this contract is the client, the buyer, who pays the full price in advance to the bank for delivery at a date and place which is the same as in the Salam contract.

The actual sequence of events is that the client first approaches the bank to buy the asset using Salam financing and, based on this application, the bank then contracts with the supplier or manufacturer on one side in the Salam contract and with the client on the other side in the parallel Salam contract. The specifications of the asset or commodity, the delivery date and place of both contracts, are identical. The objective of the bank in entering the Salam contract is to be able to fulfil the parallel Salam contract only. The period of the parallel Salam contract is much shorter and usually the price would be higher, compared with the original Salam contract with a longer period and lower price. The bank pays the supplier a lower advance price but pays it much earlier in time compared with when the client pays the bank the full price in advance, which is slightly higher. The difference between the two prices constitutes the profit earned by the bank. When an Islamic bank gets involved in a Salam contract it is basically providing purchase finance or forward finance to the client.

Islamic banks have the choice of also purchasing the commodity with a Salam contract executed with the supplier/manufacturer. Then, instead of entering a parallel Salam contract with the client, it may decide to use a Murabaha contract, resell the commodity with a markup and provide the client with the opportunity to pay in deferred instalments, thus technically providing purchase finance.

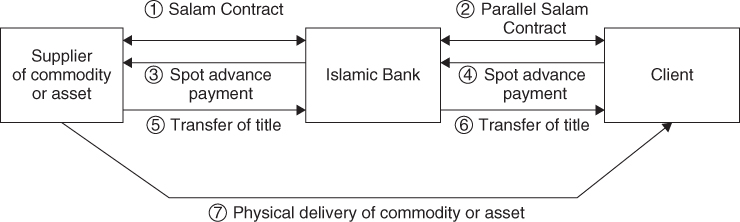

SALAM AND PARALLEL SALAM DIAGRAM AND PROCESS

A diagram of the Salam process is shown in Figure 8.1.

FIGURE 8.1 Salam and parallel Salam contracts

- The client approaches the bank for financing the purchase of a specific quantity and quality of a commodity or asset.

- The bank agrees and the client completes the application.

- The bank signs a Salam contract with the relevant supplier or manufacturer for the commodity or asset for a specific date and place, where the bank is the buyer, the supplier is the seller, based on the client's application.

- In the parallel Salam contract signed with the client as buyer and the bank as seller, the quantity, quality and specifications are exactly the same as in the Salam contract.

- The duration of the Salam contract is much longer than the parallel Salam contract.

- The bank orders the supplier and pays in advance, on behalf of the client, the required asset or commodity.

- The client makes the advance payment for the parallel Salam much later while the delivery date and place are the same, thus technically the client is receiving purchase finance from the bank.

- Often the bank only receives the ownership title and then passes it on to the client, while the physical delivery of the asset is made directly to the client.

PRACTICAL APPLICATION OF SALAM

Salam is used where the asset is not ready, and payment can be made in advance. Salam contracts are most commonly used for financing agriculture, natural resources and international trade, providing advance funds to farmers, miners and exporters to finance their activities. It can also be used as working capital finance for businesses.

A Practical Example

Alpha Superstore (A) approaches Big Bank (B) on 1 September to purchase 10,000 boxes of candy using the parallel Salam to be delivered on 31 December of this year, while the payment of USD50,000 will be made on 1 November as the contract is signed. B enters into the Salam contract for the exact same 10,000 boxes of candy with manufacturer Candy Maker (C) on 2 September, paying on spot USD45,000 in advance with delivery to be on 31 December. On the delivery date, physical delivery is directly from C to A, though actually legally two sales contracts were implemented from C to B and then from B to A. B makes the payment earlier and at a lesser amount. The price difference is the bank's profit. The customer needs to pay later and thus gets purchase funding indirectly.

The parallel Salam delivery to A from B is not conditional on C delivering to B. If C does not deliver in time or of the required quality, quantity or specification, B needs to buy from the market and deliver to A and thus bears the risk of making a loss. A, B and C need to be three independent parties.

PROBLEMS RELATED TO SALAM CONTRACTS

Credit risk – seller's default. The supplier manufacturer in the Salam contract may not deliver on the specified date and at the specified place, and this could force the bank to purchase from the market to deliver to its client in the parallel Salam contract.

Market risk. The price of the commodity may change in the market and the bank can lose, either if it is forced to buy at a higher price from the market or if the price goes below the price at which the bank buys from the manufacturer in the Salam contract.

Mismatch of quality and quantity. If the commodities specified in the Salam and parallel Salam contracts do not match completely, or the delivered goods do not match with the specifications, the supplier or manufacturer would be in default with the bank, but the bank still has to supply to the client by purchasing from the open market.

COMPARISON OF SALAM CONTRACT WITH CONVENTIONAL BANKING

As discussed in Chapter 3, the main difference between Islamic banking and conventional banking comes from the differences in financial intermediation applied in the two systems, and this is carried into the application of various Islamic banking products vis à vis conventional bank loans. As explained earlier in Chapter 3, conventional bank depositors provide their funds to the bank against a fixed interest rate. The conventional bank applies these funds to finance various loans on fixed interest again. The borrower may earn less or more but will pay the fixed amount to the bank, which in turn pays a fixed amount to the depositors. The bank shares no risk with the borrower and similarly the depositors share no risk with the bank. In contrast, in the Islamic bank, the depositors share the profit and loss earned by the bank, while in case of the Salam contract the bank buys the good by paying in advance and resells it to the client at a higher price and thus earns a profit which it shares pro-rata with its depositors.

KEY TERMS AND CONCEPTS

- Buy-back condition

- Mismatch of quality and quantity

- Muslam

- Muslam Fihi

- Muslam Ileihi

- Parallel Salam

- Ras al Maal

- Ribawi

- Salam

- Seller's default

CHAPTER SUMMARY

Salam is one of the two Islamic finance products that are the exception to the Shariah requirement of a valid sales contract – that the asset should exist, be owned by and be in the physical or constructive possession of the seller. In Salam, the buyer makes the full payment in advance to the seller for a specific amount of good, to be delivered at a specific future date.

Goods with homogenous characteristics, that can be counted, measured or weighed, rather than those with unique characteristics, are suitable for Salam. The price, delivery date and place need to be clearly stipulated. No buy-back condition is allowed, though security or guarantee is permitted, and a penalty can be charged for delay of delivery but needs to be donated to charity. Termination of the contract is only allowed with mutual consent.

The Salam contract was used during the time of the Prophet, especially in agriculture and trade. It benefits the seller in the form of advance funding to produce, while the buyer benefits from a discounted price. In modern Islamic banking the banks play middlemen by contracting with the original manufacturer in the Salam contract and with the original buyer in the parallel Salam contract.

Some problems related to Salam contracts are the credit risk or seller's default, market risk and mismatch of quality and quantity. Salam differs from conventional banking financial intermediation, where the bank receives deposits and gives loans on fixed interest and earns from the margin of the two interest rates. In Salam the bank as buyer pays in advance to the manufacturer, and in parallel Salam the bank as seller receives advance payment from the client buyer. Usually the Salam contract has longer duration and less advance price compared with parallel Salam, thus the bank provides purchase finance and earns profit from the difference in price.

END OF CHAPTER QUESTIONS AND ACTIVITIES

Discussion Questions

- Define the Islamic banking instrument of Salam.

- What are the various parties in a Salam contract?

- Discuss the characteristics of a Salam contract.

- How was Salam used during the time of the Prophet?

- What benefits do the buyers and sellers in Salam derive?

- Discuss the role of Islamic banks in Salam.

- Explain how an Islamic bank gets involved in a Salam and a parallel Salam contract, discuss the parties and the differences of these two contracts.

- Explain and draw the process of Salam and parallel Salam.

- What problems do Salam contracts face?

- Compare Salam with conventional banking.

Multiple Choice Questions

Circle the letter next to the most accurate answer.

- Which of the following is a characteristic of the Salam contract?

- The buyer pays the seller part of the price of the asset in advance

- The buyer pays the seller the full price of the asset in advance

- The asset is delivered at the time the contract is signed

- The goods must exist at the time of signing the contract

- Which of the following is not a characteristic of the Salam contract?

- The goods must be homogenous or identical

- Quality and quantity must be determined at the time of contract signing

- Salam cannot be tied to the produce from a specific farm, field or tree

- Date and place of delivery is determined later, not at the time of the contract signing

- Which statement below is true about the Salam contract?

- The seller will provide a specific commodity to the buyer, with delivery and payment both in the future

- The seller will provide a specific commodity to the buyer, with delivery in the future and payment in advance today

- The seller will provide a specific commodity to the buyer, with delivery now and payment in the future

- The seller will provide a specific commodity to the buyer, with delivery and payment both today

- The Salam contract resembles which conventional finance product?

- Loan contract

- Forward contract

- Options contract

- Swap contract

- Under the Salam contract the seller is at risk:

- For the entire period of the contract

- For a very short period at the beginning of the contract

- For a very short period towards the end of the contract

- At no point during the contract

- The two Islamic banking products that are exceptions to the Shariah rules of goods being in existence and possession of the seller are:

- Salam and Murabaha

- Mudaraba and Musharaka

- Ijara and Murabaha

- Salam and Istisna

- In a Salam contract the Muslam is:

- The buyer

- The seller

- The goods under contract

- The payments made during the contract

- In a Salam contract the Muslam Ileihi is:

- The buyer

- The seller

- The goods under contract

- The payments made during the contract

- In a Salam contract the Ras al Maal is:

- The buyer

- The seller

- The goods under contract

- The payments made during the contract

- In a Salam contract the Muslam Fihi is:

- The buyer

- The seller

- The goods under contract

- The payments made during the contract

- In which Islamic banking contract is the purchase and sale of a commodity done for deferred delivery in exchange for immediate payment?

- Istisna

- Salam

- Ijara

- Musawama

True/False Questions

Write T for true and F for false next to the statement.

- Salam is a sales contract where the seller supplies specific goods to the buyer in the future against full advance payment on spot.

- The deferred delivery for immediate payment in Salam is an exception allowed by Shariah.

- In Salam the seller is exposed to a total loss of capital.

- In a Salam contract delivery of the goods on the due date is a must.

- Using a Salam contract, an exporter can be paid in advance and can use these funds to buy the raw material to manufacture the items of the export contract.

- In a Salam contract, the seller can decide to sell their goods to a different buyer if the sales price increases in the future.

- A Salam contract can be cancelled unilaterally with due notice.

- The buyer of a Salam contract pays, on spot, the full price in advance for future delivery of the goods, expecting the price to be less in the future.

- Salam can only be used for goods that are very standardized.