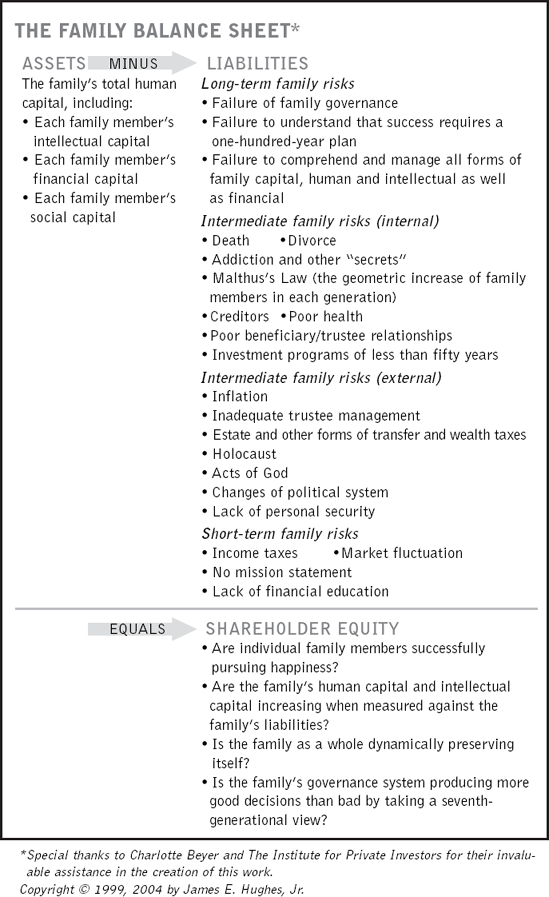

The family balance sheet and family income statement are key tools for measuring the health of a family's long-term wealth preservation business. As with any business, the shareholders— in this case, family members—need to know how the enterprise is doing, so they need a way of measuring the business's progress. These measurements allow shareholders to instruct the directors, managers, and trustees of the family business on the tasks of running it and to determine how well these managers are fulfilling their roles.

The traditional balance sheet attempts to measure the state of well-being of a business at a certain point in time. Such balance sheets contain statements of assets, liabilities, and shareholder equity as a reflection of the business's financial status. The family balance sheet also lists assets, liabilities, and shareholder equity but expands what each category measures. Because successful long-term family wealth preservation is achieved by enhancing the well-being of individual family members over a long period of time, the family balance sheet measures human and intellectual capital as well as financial capital. The family balance sheet is an attempt to measure how well a family is managing its human capital.

A family balance sheet is an addition to, not a substitute for, a family financial statement. A family wealth management business, like every other financial organization, must know its financial capacity to carry on its mission.

Business balance sheets reflect a point in time, but when combined with previous balance sheets, they can reveal short- and long-term trends. Most company balance sheets report results backward and forward over specific time periods in order to measure trends and to show the business's progress. Business defines two years as short-term, five years as intermediate, and ten years as long-term. Families assess their wealth preservation with an analogous system and for the same purposes but use different time periods. Unfortunately, very few families have understood how long-term their measurement has to be to know if they are successful. They look at time periods that are much too short—five years, or ten, perhaps. But families attempting to overcome the "Shirtsleeves to shirtsleeves in three generations" proverb should define short-term as twenty years, or one generation; intermediate as fifty years, or two generations; and long-term as one hundred years, or three generations. This difference of view profoundly affects the nature of the assets and liabilities being measured. It also enforces very long-term planning. A family balance sheet should report to its shareholders the historic results of the family's long-term wealth preservation business using these longer time periods.

When families create a family balance sheet in this form, they quickly appreciate the actual position of the family vis-à-vis the shirtsleeves proverb. Applying the state of the family as reflected on the family balance sheet to the mission of the family as stated in its family mission statement, the family can begin to do the required long-term strategic planning. With this tool each family member can learn to act as a shareholder of the family business and understand his or her role in it.

Ordinary businesses use annual income statements to reflect profits and losses over a single year. Family businesses need to compile analogous documents, called family income statements. When used with the family balance sheet, the family income statement measures the increase or decrease in the family's human and intellectual capital during the year in question, and thus measures the family's annual performance in managing its human and intellectual capital. Family leaders collect and review family members' résumés and individual mission statements, as described in Chapter 2, to assess gains and losses in human and intellectual capital. I recommend to families as a "best practice" for successful family governance that they obtain an updated résumé and personal mission statement from each member annually. This practice gives the family governance leaders a clear impression of how the individual family members who form the assets on the family balance sheet are doing in their individual pursuits of happiness. It will also tell them whether the family as a whole has increased or decreased its human and intellectual capital during the year being measured.

When a family holds financial assets in trust, the family income statement should also include a summary by the family's governance leaders of two other sets of reports:

annual reports by family members of themselves as beneficiaries, based on beneficiary best practices (see Chapter 10); and

annual reports by family trustees on their performance in light of trustee best practices (see Chapter 11).

The results of these reviews alert the family leaders to current and future liabilities on the family balance sheet. They offer the leaders an opportunity to address these issues as they emerge so they can be managed before they turn into serious problems.

Families who create a family balance sheet and family income statement are amazed at how rich they are in human and intellectual capital. They are even more amazed at how much better they do financially within two to three years of implementing these practices. Why are their results so rewarding? If the family leaders know what their human and intellectual capital is, they can engage each family member as a shareholder in the mission of the family business: long-term wealth preservation. Once family members are engaged in this process, the overall risk profile of the family declines.