5

Administration Selling and Distribution Overheads

LEARNING OBJECTIVES

After studying this chapter you should be able to:

Understand the concept of administration expenses.

Know the features of administrative overheads.

Determine administrative expenses and quote prices.

Know how to control administration expenses.

Understanding the meaning of selling and distribution overheads.

Apply the stages involved in accounting process of ascertaining selling and distribution overheads.

Distinguish between production overhead and selling and distribution overhead.

Explain certain important key terms.

Administration expenses (overheads) have no direct relationship with existing production activities. Also they bear a remote relationship to the selling and distribution activities. Administration overheads are not tangible and not easy to quantify. They are dealt with as period costs. They are not affected by any variation in volume of output or sales. Such expenses are often linked to cost objects while reporting costs for the process of making decisions. This chapter aims at explaining the nature, special features, accounting treatment and control of administration, selling and distribution overheads in detail.

5.1 ADMINISTRATION OVERHEADS

Administration overhead may be defined as the aggregate of the costs of formulating the policy, directing the organisation, and controlling the operations of an undertaking which is not directly related to production, selling, distribution and research or development or any other function. It is clear that the cost of administering production activities is not included in administration overhead. They are treated as production overhead and included in it.

Administration provides support to production, selling, distribution and research and development functions. Despite this factor, direct relationship cannot be established between these functions and the administration overhead. It may also be said that administration overhead has no influence on the present existing operations. On the other hand, it bears relationship with the activities that determine the future plan and activities of an organization.

Administration overheads include salary of office staff, directors’ remuneration, rent, rates and taxes of office buildings, office lighting, healing, depreciation of office furniture and fixtures, repair and maintenance of office building, insurance premium for office building, postage, courier, fax, email charges, legal expenses, printing and stationery expenses, audit fees and bank charges.

5.2 ACCOUNTING FOR ADMINISTRATION OVERHEAD

There are a number of approaches for accounting for administration overheads. They are:

5.2.1 Separate Cost Item

Under this method, administration is considered as an independent activity. Administration overhead is treated as a separate item of cost in respect of finished goods sold. Accordingly, a cost analysis sheet is prepared on a periodical basis showing separately production costs, administration costs, selling costs and distribution costs.

The major task involved in accounting treatment is the choice of an equitable base for the allotment of administration costs to units produced or sold. Some of the important bases used for the allotment of administration overhead are as follows:

Manufacturing or factory costs

Number of units manufactured

Net sales value

Number of units sold

Selling Costs

Gross profit on sales

The overhead application rate is computed by using the base selected as under.

Base: Manufacturing or factory cost

Base: Number of units produced

Base: Net sales value

- Base: Number of units sold

- Base: Conversion cost

- Conversion cost means that cost of direct labour, direct expenses and factory overheads are all included.

- Gross profit means the profit before administration, selling and distribution overheads.

- The bases which lay emphasis on the selling function, namely “Net saeles value”, “Selling costs” and “Number of units sold” are more equitable than the other bases. A predetermined overhead absorption rate can be used.

- It is important to note that administration overhead must not be added to the cost of units in stock (finished goods or work-in-progress).

- It must be added to the cost of units sold.

5.2.2 Apportionment of Administration Overhead to Manufacturing, Selling and Distribution Functions

Under this approach, administration overhead is to be apportioned between manufacturing and selling activities, equitable. This method is based on the assumption that administration overhead renders benefit to two major functions of an organization, namely, manufacturing and selling. As the entire administrative overheads are apportioned to manufacturing and selling activities, it loses its identity.

This method treats as product cost that portion of administration overhead which has been apportioned to manufacturing activities. The remaining part so apportioned to selling and distribution activities is to be debited to costing profit and loss account.

5.2.3 Transferring Administration Overhead to Costing Profit and Loss Account

Under this approach, total administration overhead is transferred to costing profit and loss account. This approach is based on the conception of following factors:

- Administration is an independent activity.

- Administrative functions are important.

- There is no direct relationship between administration overhead and the products manufactured and sold.

- The administration overhead is fixed.

- It is considered as period cost and therefore to be charged to costing profit and loss account.

Illustration 5.1

The following information has been gathered for a company doing jobbing work only for 2009

| Rs. | |

|---|---|

Materials consumed |

1,00,000 |

Direct labour |

75,000 |

Factory overheads |

60,000 |

Office and administrative expenses |

23,500 |

Sales |

|

The company has to quote for a job to be undertaken in March 2010. It is estimated that the job will require materials costing Rs. 40,000 and direct wages for it will be Rs. 50,000. What should be the quotation?

[C.S. (Inter). Modified]

Solution

First, profit has to be ascertained by preparing cost sheet for 2009 as follows:

| Particulars | Rs. |

|---|---|

Step 1 → Materials consumed |

1,00,000 |

Step 2 → Direct labour |

75,000 |

Step 3 → PRIME COST (Step 1 + Step 2) |

1,75,000 |

Step 4 → Factory overheads |

60,000 |

Step 5 → WORKS COST (Step 3 + Step 4) |

2,35,000 |

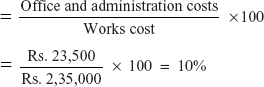

Step 6 → Administration and office expenses |

23,500 |

Step 7 → TOTAL COST (Step 5 + Step 6) |

2,58,500 |

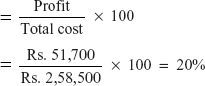

Step 8 → PROFIT (Step 9 – Step 7) (Bal. Fig.) |

51,700 |

Step 9 → Sales (Given) |

3,10,200 |

STAGE II: Following percentages have to be calculated in order to quote the job for 2010:

- Percentage of factory overheads to direct labour:

- Percentage of office and administration expenses to works cost:

- Percentage of profit to total cost

Based on these percentages, price to be quoted is calculated as follows:

STAGE III:

| Particulars | Rs. |

|---|---|

Step 1 Materials |

40,000 |

Step 2 Direct labour |

50,000 |

Step 3 PRIME COST (Step 1 + Step 2) |

90,000 |

Step 4 Factory overheads (Ref: Stage II: (i)- Factory overheads to direct labour percentage is 80%. 80% of Rs. 50,000 = Rs. 40,000) |

40,000 |

Step 5 WORKS COST (Step 3 + Step 4) |

1,30,000 |

Step 6 Office and administration expenses (Ref: Stage II-(ii)-Percentage of administration expenses to works cost is 10% of Rs. 1,30,000 = Rs. 13,000) |

13,000 |

Step 7 TOTAL COST (Step 5 + Step 6) |

1,43,000 |

Step 8 Profit (Ref: Stage II (iii) – Percentage of profit to total cost = 20%; 20% of Rs. 1,43,000 = Rs. 28,600) |

28,600 |

Step 9 ∴ PRICE TO BE QUOTED (Add : Step 7 + Step 8) |

1,71,600 |

5.3 CONTROL OF ADMINISTRATION OVERHEAD

Administration overhead is first collected under cost account numbers with respect to each administration department. These cost account numbers are account code numbers allotted to administration, selling and distribution expenses after allocation and apportionment to different administration departments. After having collected, a comparison has to be made by applying some norms, which are (i) last year’s actual overheads, (ii) budgeted overheads and (iii) standards.

5.3.1 Last Year’s Actual Overheads

Comparison with past data will not yield desired results. Inefficiencies of past year are included in last year’s actual overheads.

Last year’s records do not consider intervening changes that have taken place. Hence, control reports may be prepared separately and the past results are to be compared with.

5.3.2 Budgeted Overheads

Budgeted overheads is another criterion for undertaking evaluation. Administration overheads budget forms part of the master budget and should be prepared during the annual or half-yearly budget preparation work. Actual overheads are to be compared with the overheads given in the administration overheads budget. In the modified form, flexible budgets are prepared for each item of administration overheads and comparisons are made periodically and corrective measures are undertaken in case of variances.

5.3.3 Standards

Another way of controlling administration overheads is setting standards. Measurement of performance can be done against standards. But it is very difficult to set standards for each item of administration overhead. Applying standard cost accounting principles will not yield the desired results effectively.

All the three approaches that have been explained above show that the comparison will result in or show variances. The variances should be ascertained, investigated and analysed by causes and responsibility centres. They must be reported to appropriate level to take corrective action.

Administration overheads are generally fixed in nature. Once the volume of activity increases, it is very difficult to control increase in administration overhead in such situations. Hence, it is very difficult to understand, allocate, apportion and control administration overheads and the management must have a constant vigil over this constantly.

5.4 SELLING AND DISTRIBUTION OVERHEAD

5.4.1 Selling Overheads

Selling Overheads is the cost of creating sales and retaining customers. Overhead expenses which are incurred for the purpose of promoting the marketing and sales of different products are called selling overhead. Selling Overhead is the aggregate of indirect materials, indirect wages and indirect expenses incurred for creating and stimulating demand for a firm’s products, securing and executing the orders. But the costs associated with manufacture and distribution of products are not included in selling overhead. Examples of selling overhead are advertisement and publicity expenses, salary commission and benefits of sales force, technical representatives, bad debts, showroom costs, costs of catalogue and price lists, commission and brokerage to third parties.

5.4.2 Distribution Overheads

Distribution overhead is the cost of servicing and maintaining demand. Distribution overhead is the aggregate of indirect materials, indirect wages and indirect expenses incurred for moving finished products to central and local storage, moving finished products to customers, making the empty packages reusage etc. Distribution overheads is the cost of making a firm’s products available to customers. Examples of distribution overheads are warehousing expenses, carriage and freight outwards, wastage of finished goods, cost of secondary packing, insurance premium for finished goods, all expenses incurred in maintenance of delivery vehicles etc.

Even though the functions differ and vary, both selling and selling and distribution overheads are grouped together for the purpose of cost accounting.

5.4.3 Accounting for Selling and Distribution Overheads

Following are the important stages involved in the process of accounting for selling and distribution overheads:

5.4.3.1 Stage I

The first step involved in this process of accounting is the collection of expenses relating to selling and distribution under clearly defined cost account numbers. These cost account numbers reveal the nature of expenditure and the causes for their occurrence. Account headings have to be properly codified and arranged. In this stage, the necessity arises to classify selling and distribution overheads into (1) variable, (2) semi-variable and (3) fixed.

5.4.3.2 Stage II

The next important stage in the process of accounting for selling and distribution overhead in the allocation for selling and distribution overhead is the allocation and apportionment of these expenses to different functions and territories. The different functions may be grouped into important headings as under:

- Direct selling

- Advertisement and sales promotion

- Credit and collections

- Warehousing and storage

- Transportation

Grouping of functions may differ from one organization to another.

- Individual groups are to be treated as independent cost centres. Allocation and apportionment of expenses are similar to production overheads procedure.

- Then, these expenses are distributed to the central marketing organization and sales territories by way of allocation and apportionment.

- The bases that are used for distributing selling overheads to the functions and sales territories are:

| Selling Overheads | Basis |

|---|---|

Depreciation |

Capital value of assets |

Advertisement expenses |

Sales value |

Insurance premium |

Value of property |

Catalogue cost |

Sales value |

Credit and collection |

Cash collected or number of orders |

Direct selling |

Allocation |

General administration |

Number of orders |

- It is also possible to record many of the expenses with respect to each function and territory separately, which can facilitate direct allocation.

5.4.3.3 Stage III

In this stage, selling and distribution overheads are analysed by products or product groups. Expenses are segregated into variable and fixed. It is important to note that variable selling and distribution overheads occur at the time of sale of a product only. They consist of specific amount for each unit of product sold. Such overheads can be allotted by way of a direct charge. But the difficulty arises for apportioning fixed costs. “Sales value of goods” may be considered a reasonable basis for apportionment of fixed overheads. However, the best method is to find out the relationship between each item of such overhead and the benefits received by different products sold and then allocate the expenses using a proper equitable basis.

5.4.4 Control of Selling and Distribution Overheads

Selling and distribution expenses may be controlled by using the methods mentioned as follows:

- Comparison with past performance

- Installation of budgetary control system

- Standard costing and analysis of variances

- Profitability analysis

5.4.5 Distinction between Production Overhead and Selling and Distribution Overhead

| Basis of Distinction | Production Overhead | Selling and Distribution Overhead |

|---|---|---|

1. Treatment of overhead cost |

Production overhead is treated as a product cost. |

Selling and distribution overhead is treated as period cost |

2. Managerial control |

Management control can be exercised to a great extent. |

Management control cannot be exercised here. |

3. Change in techniques |

Manufacturing techniques may not undergo frequent changes. |

Marketing techniques undergo frequent changes in tune with marketing conditions. |

4. Cause and effect relationship |

In manufacturing process, there is a direct cause and effect relationship. |

In marketing process, there exists no direct cause and effect relationship. |

5. Time lag |

Time lag between incurrence of expense and result is very short. |

Time lag is comparatively large in this case. |

Illustration 5.2

The works cost of a certain article is Rs. 500 and the selling price is Rs. 1,000. The following selling and distribution (direct) expenses were incurred:

| Rs. | |

|---|---|

Freight and carriage |

50 |

Insurance |

15 |

Commission |

45 |

Packing cases |

15 |

The estimated fixed selling and distribution expenses for the year were Rs. 50,000, and the estimated value of sales for the year were Rs. 2,00,000.

You are required to set out the final cost of the article using the method of percentage on sales to recoup fixed selling and distribution expenses.

Solution

Step 1: The percentage of fixed selling and distribution expenses to the estimated value of sales is calculated as follows:

Step 2: Final cost of the article is computed using the method of percentage on sales as follows:

| Particulars | Rs. | Rs. |

|---|---|---|

Step 1: Works cost (given) |

|

500 |

Step 2: Selling and distribution expenses (direct) variable: |

|

|

(i) Freight and carriage |

50 |

|

(ii) Insurance |

15 |

|

(iii) Commission |

45 |

|

(iv) Packing |

15 |

|

15 |

||

Step 3: Fixed: 25% of selling price (25% of 1,000) |

250 |

375 |

Step 4: Total cost (Step 1 + Step 2 + Step 3) |

875 |

|

Step 5: Profit (Step 6 − Step 4) |

125 |

|

Step 6: Selling price (given) |

1,000 |

Illustration 5.3

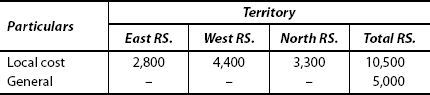

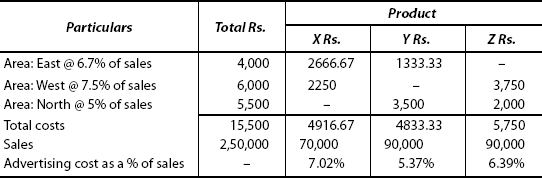

A Company is producing three types of products X, Y and Z. The sales territory of the company is divided into three areas: East, West and North. The estimated sales for the year 2009 are as follows:

The budgeted advertising cost is as follows:

You are required to find the percentage of advertising cost on sales for each area and product showing how you will present the statement to the management.

Solution

-

Total sales =

East: Rs. 60,000

West: Rs. 80,000

North: Rs. 1,10,000

Total: Rs. 2,50,000

- General cost (given): Rs. 5,000

Based on the above two values, advertising cost as a percentage of sales is computed as follows:

Apportionment and allocation of advertising cost area-wise

Apportionment of Advertisement Cost Product-wise

Illustration 5.4

A company is supplying its products to the ultimate consumers through the wholesalers to retailers. The managing director thinks that if they sell through retailers or to the consumer direct, they can increase their sales, earn better prices and make profit. As a cost accountant of the company, you are required to advise the managing director in selecting the channels of distribution from the following information:

Cost of Production:

Variable cost @ Rs. 8 per unit

Fixed cost Rs. 6,00,000

In selecting the channels of distribution what factors besides cost would you consider?

Solution

NOTE 1:

Fixed cost: |

Rs.6,00,000 |

|

|

|

|

|

|

2. Factors that require in choosing the channel besides cost are:

- Nature of product

- Nature of market condition

- Nature of competition

- Nature of demand

- Substitutes available

- Credit collection

- Managerial policy decision

Statement of Profitability

The result shows that channel II (To retailer direct) gives the highest profit. So the management is advised to select the selling process through the retailers as it makes high profit.

Illustration 5.5

VRV Co. Ltd, a manufacturing company, having an extensive marketing net work across the country, sells its products through four zones, viz. East, West, South and North. The budgeted expenditure for the year is given below:

| Rs. | Rs. | |

|---|---|---|

Sales manager’s salary |

|

60,000 |

Expenses relating to sales manager’s office |

|

40,000 |

Travelling salesmen’s salaries |

|

1,60,000 |

Travelling expenses |

|

18,000 |

Advertisement |

|

15,000 |

Godown Rent: |

|

|

East Zone: |

7,500 |

|

West Zone: |

12,600 |

|

South Zone: |

4,900 |

|

North Zone: |

9,000 |

|

|

|

34,000 |

|

Rs. |

Insurance on Inventories |

10,000 |

Commission on sales @ 5% on sales |

3,00,000 |

Further particulars:

Based on the above details, you are required to compute zone-wise selling overheads as a percentage to sales.

Solution

Allocation and Apportionment of Selling Overhead

Zonal-wise Selling Overheads as Percentage of sales

Illustration 5.6

LMN Ltd decided to analyse its selling and distribution costs for products X, Y and Z in order to provide management with more effective information for cost control and to guide the salesmen’s efforts towards the sale of the products with the highest potential net profit.

The income statement of the company for the past year is as follows:

| Rs. | Rs. | |

|---|---|---|

Sales |

|

2,60,000 |

Cost of goods sold |

|

1,25,000 |

Gross profit on sales |

|

1,35,000 |

Selling and distribution costs |

|

|

Salesmen’s salaries |

12,250 |

|

Salesmen’s commission |

13,750 |

|

Advertising |

32,500 |

|

Transport and delivery |

4,200 |

|

Credit and collection |

2,050 |

|

Packing |

2,800 |

|

Warehouse |

2,250 |

|

Sales office expenses |

7,400 |

|

Bad debts |

4,705 |

|

|

81,905 |

|

General and administration expenses |

20,625 |

1,02,530 |

Net profit |

|

32,470 |

Additional Information:

Sales office expenses: Allocated in the same ratio as in packing General and administrative expenses: Allocated on the basis of sales

You are required to prepare a statement showing the analysis of the selling and distribution costs for management’s guidance.

Solution

Each item is to be allocated on the respective basis and income statement is prepared in the comparative form for each product.

Results are tabulated in the following table:

Comparative Income Statement

(Analysis of selling and distribution overhead)

Illustration 5.7

A company has five salesmen working in its Chennai branch. The following information is available in the branch office record for the month of March 2010. In assessing the performance of each salesman, branch office costs of Rs. 30,000 are apportioned as a percentage of cost of goods sold. The results of salesmen Q and T are not satisfactory and their discharge is recommended. Do you consider the method of apportionment equitable and support the recommendation? You are required to prepare comparative salesmen’s profit and loss statement showing contribution margin and net profit.

[I.C.W.A. Modified]

Solution

Most of the branch office costs are of fixed nature. Hence, fixed office expenses are not to be apportioned to ascertain the efficiency of salesmen. On the other hand, they should be deducted from the total contributions. Accordingly assessment should be based on contributions made by salesmen.

- Contribution = Sales – Total variable costs

These two concepts have been explained in detail in Chapter 16 comprising marginal costing, and cost volume profit analysis, later in this book. Students, after learning such concepts, may revert again and be able to solve this problem. At present, apply the formula to ascertain contribution and P/V ratio.

Branch Profit and Loss Statement

- The table reveals that the performance of salesmen Q and T are comparatively less.

- Contribution of Q = Rs. 4,800

Contribution of T = Rs. 2,800

- Their P/V ratios are also less: For Q = 6 per cent

For T = 7 per cent

- The reason for such low contribution and P/V ratio is the variable costs of goods sold by them are high.

- Recommendations:

- Variable costs should be brought down instead of discharging the two salesmen.

- Total contribution by Q and T = Rs. 7,600. If they are discharged total contribution will be reduced to (Rs. 34,400 – Rs. 7,600) = Rs. 26,800. This will be inadequate to recover the branch office costs (fixed) Rs. 30,000, which may result in a loss of Rs. (30,000 = 26,800) 3,200.

For these two reasons, salesman Q and T should not be discharged from their jobs.

Summary

Administration Overheads: Administration overhead is the aggregate of the costs of formulating the policy, directing the organisation and controlling the operations of a business firm. However, it should not be directly related to production, selling distribution and research or development or any other activities.

Accounting for Administration Overhead: Selecting a suitable base for the allotment of administration costs to units produced or sold is the major task. Some of the important bases are: Manufacturing or factory costs, Number of units produced, Net sales value, Number of units sold, Selling costs, and Gross profit on sales. Here, it is treated as a separate item of cost with respect to finished goods sold.

Another approach is to apportion administration overhead between manufacturing and selling activities equally.

This approach is not recommended because administration costs lose their identity as they are merged with manufacturing and selling activities.

Another approach is to transfer administration overheads to costing profit and loss account.

Selling and Distribution Overheads: There are three important stages in the process of accounting for selling and distribution overheads: (1) Classifying them into variable, semi-variable and fixed; (2) Allocation and apportionment of these expenses into different functions and territories and (3) Expenses are segregated into variable and fixed and analysed by products or product groups.

Administration and selling and distribution overheads are analysed and apportioned in illustrations 5.1 to 5.7.

QUESTION BANK

Objective Questions

I. State whether the following statements are True or False

- Administration, selling and distribution overheads have no direct relationship with existing production activities.

- The costs of administrating production activities are included in administration overhead.

- Administration overheads can influence the firm’s future operations.

- Administration overheads bear close relationship with sales.

- Administration overheads should be added to the cost of units in stock (cost of inventory).

- Administration overheads are mainly variable in nature.

- There exists no relationship between cost of goods sold and fixed selling and distribution overheads.

- Selling and distribution overhead is treated as a product cost.

- Bad debt of normal nature is treated as selling and distribution overhead, and forms part of product cost.

- Abnormal bad debt is included in cost accounts.

Answers:

1. True |

2. False |

3. True |

4. True |

5. False |

6. False |

7. True |

8. False |

9. True |

10. False. |

|

|

II. Fill in the blanks with suitable word(s)

- Administration, selling and distribution overheads are treated as _____ cost.

- Administration productive activities are treated as _____.

- Existing production activities bear no relationship with ____.

- Administration overhead should not be added to the cost of ____.

- Administration overhead renders benefit to two functions: (1) ____ and (2) ____.

- Administration overheads are ____ in nature.

- Selling overhead is the cost of ____.

- Selling and distribution cost is treated as ____ cost as per GAPP.

- Sales is influenced by ____ mix.

- Abnormal bad debt is ____ to costing profit and loss account.

Answers:

- period

- production overhead

- administration, selling and distribution overhead

- inventory

- manufacturing and selling

- fixed

- creating sales and retaining customers

- period

- marketing mix

- debited

III. Multiple Choice Questions Choose the best answer:

- Administration overheads are allotted to cost units based on

- number of units sold

- direct materials

- direct labour

- machine hours

- Generally administration overheads are treated as

- product costs

- period costs

- committed costs

- opportunity costs

- Insurance premium paid for office equipment represents

- production overhead

- selling overhead

- administration overhead

- distribution overhead

- Cost of fancy packing is included in

- production overhead

- selling overhead

- administration overhead

- all of the above

- Which one of the following is the cost of executing the orders

- administration cost

- production cost

- selling cost

- distribution cost

- Which one of the following bases not used for allotment of administration overhead

- manufacturing costs

- net sales value

- number of staff

- number of units manufactured

- Selling and distribution overhead (fixed) are apportioned using one of the following bases:

- cost of goods sold

- number of units manufactured

- Direct labour hours

- number of salesmen

- Bad debt of normal nature is treated as

- administration overhead

- production overhead

- selling and distribution overhead

- excluding from cost accounts.

Answers:

1. (a) |

2. (b) |

3. (c) |

4. (b) |

5. (d) |

6. (c) |

7. (a) |

8. (d) |

|

|

Short Answer Questions

- Define “Administration Overhead”.

- Give examples of administration overheads.

- Name the bases used for allotting administration costs.

- Name the norms applied for making a comparison of overheads collected.

- How would you treat administration overheads in cost accounts?

- Define “selling and distribution overhead”.

- How selling and distribution overheads may be classified for accounting purpose?

- What do you mean by “direct allocation”?

- Name the bases used for apportioning of selling and distribution (fixed) overheads.

- How can you control the selling and distribution overheads? Name four methods.

- Distinguish between production overhead and selling and distribution overhead.

- How would you treat the following items in cost accounts

- Research and development cost

- Bad debts

- Advertisement expenses

- How would you classify the following items of expenses?

- Market research

- Commission paid to salesman

- Showroom expenses

Essay Questions

- Enumerate in detail the number of approaches that you would use in order to account for administration overhead.

- Explain how will you control administration overhead?

- Explain in detail the various stages that are involved in accounting for selling and distribution overheads.

- Discuss the various methods which are used for controlling selling and distribution overheads.

- Investment of men, money and materials in various research and development projects both in the public and in the private sectors in India is on the increase. The urge to invest more in this area has been accelerated because of the increasing tax incentive offered by the government. Suggest a method for controlling the expenditure in research and development and measuring its efficiency.

Exercises

1. A company is producing three types of products: A, B and C. The sales territory is divided into three areas X, Y and Z.

The estimated sales and the advertising cost for the next year are as follows:

You are required to prepare a statement showing territory-wise advertising cost expressed as a percentage of sales. The allocation of advertising cost should be based on sales as given above.

[I.C.W.A. (Inter)]

[Ans: X: 12 per cent; Y: 14 per cent; Z: 11 per cent]

2. Following data are available relating to a company for a certain month:

The company adopts sales basis and quantity basis for application of selling and distribution costs respectively. Compute (a) the territory-wise overhead recovery rates separately for selling and distribution costs and (b) the amounts of selling and distribution costs chargeable to a consignment of 2,000 units of a product, sold in each territory at Rs. 4-50 per unit.

[I.C.W.A. (Inter)]

3. A manufacturer has shown an amount of Rs. 16,190 in his books as “Establishment” which really includes the following expenses:

(1) Agent’s commission, Rs. 5,750, (2) Warehouse wages, Rs. 1,800, (3) Warehouse repairs, Rs. 510, (4) Lighting of office, Rs. 70, (5) Office salaries, Rs. 1,130, (6) Director’s remuneration, Rs. 1,400, (7) Travelling expenses of a salesman, Rs. 760, (8) Rent rates and insurance of warehouse, Rs. 310, (9) Rent, rates and insurance of office, Rs. 230, (10) Lighting of warehouse, Rs. 270, (11) Printing and stationery, Rs. 1,500, (12) Trade magazine, Rs. 70, (13) Donation, Rs. 150, (14) Bank charges, Rs. 100, (15) Discount allowed, Rs. 1,970, (16) Bad debts, Rs. 170.

From the information, prepare a statement showing in separate totals (a) Selling expenses, (b) Distribution expenses, (c) Administration expenses and (d) Expenses which you disregard in estimating costs.

[I.C.W.A. (Inter)]

[Ans: (a) Rs. 6,680; (b) Rs. 2,890 (c) Rs. 4,500 and (d) Rs. 2,120]

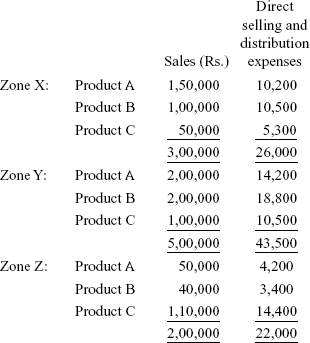

4. A company is making a study of the relative profit-ability of the two products A and B in addition to direct costs, indirect selling and distribution costs to be allocated between the two products, which are provided as follows:

Rs. |

|

Insurance coverage for inventory (finished) |

78,000 |

Storage costs |

1,40,000 |

Packing and forwarding charges |

7,20,000 |

Salesman salaries |

8,50,000 |

Invoicing costs |

4,50,000 |

Other details are given here:

|

Product A |

Product B |

Selling price per unit (Rs.) |

500 |

1,000 |

Cost per unit (inclusive of indirect selling & distribution costs) |

300 |

600 |

Annual sales (in units) |

10,000 |

8,000 |

Average inventory (units) |

1,000 |

800 |

Number of Invoices |

2,500 |

2,000 |

One of the product A requires a storage space twice as much as product B. The cost of packing and forward one unit is the same for both the products. Salesmen are paid salary plus commission @ 5 per cent on sales and equal ammount of efforts are put forth on the sales of each of the products

Required: (1) Set up a schedule showing the apportionment of indirect selling and distribution costs between the two products. (2) Prepare a statement showing the relative profitability of the two products

[C.A. (Inter)].

[Ans.:(i): |

(a)Rs. 14,55,000; |

(b)Rs. 14,33,000 |

(ii): |

(a)Rs. 5,45,000; |

(b)Rs. 17,67,000 |

|

(a)10.9% |

(b)22.08%] |

5. A match factory sells its goods in four direct zones – South, North, East and West. You have been given the following particulars in respect of each zone

The following are the expenses of the previous year:

|

Rs. |

Sales manager and his establishment |

1,24,000 |

Travelling representatives’ salaries |

72,000 |

Travelling representatives’ travelling allowances |

24,000 |

Advertising |

48,000 |

Godown rent at outstations:

|

Rs. |

|

South zone |

15,000 |

|

North zone |

21,000 |

|

East zone |

9,600 |

|

West zone |

7,200 |

52,800 |

Insurance on inventories at outstations |

24,400 |

Commission on sales @ 2½ |

62,500 |

Transportation charges outward |

72,000 |

|

4,79,700 |

You are required to compute selling overhead rates as a percentage of sales.

[Ans: South: 21.9 per cent; North: 16.72 per cent

East: 21.91 per cent; West: 22.6 per cent]

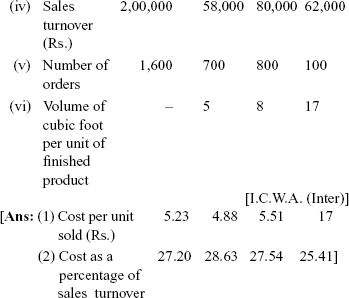

6. A company produces a single product in three sizes A, B and C. Prepare a statement showing the selling and distribution expenses apportioned over the three sizes applying the appropriate basis for such apportionment in each case from the particulars indicated. Express the total of the cost so apportioned to each size as:

- Cost per unit sold (nearest paise)

- A percentage of sales turnover (nearest to two places of decimal)

Expenses |

Amount |

Basis of |

|

Rs. |

apportionment |

Sales salaries |

10,000 |

Direct charge |

Sales commission |

6,000 |

Sales turnover |

Sales office expenses |

2,096 |

Number of orders |

Advertising: General |

5,000 |

Sales turnover |

Advertising: Specific |

22,000 |

Direct charge |

Packing |

3,000 |

Total volume in cubic foot of products sold |

Delivery expenses |

4,000 |

Total volume in cubicfoot of products sold |

Warehouse expenses |

1,000 |

|

Credit collection |

1,296 |

Number of orders |

expenses |

54,397 |

|

Data available to three sizes are as follows:

[I.C.W.A. (Inter)]

7. Progressive Company Ltd. manufactures three products A, B and C and sells directly through their own sales force in three zones X, Y, Z. The overall control of distribution and sales is taken care of at the headquarters, responsible also for sales promotion.

You are presented with the following data for the year ended 31 March 2010.

Selling and sales promotion expenses at the headquarters are:

Selling expenses |

Rs. 18,000 |

Administration expenses |

Rs. 20,000 |

Other expenses |

Rs. 24,000 |

While Advertisement expenses are allocated to zones and production on the basis of sales, the other two types of expenses are allocated equally to zones and products.

Cost of sales should be taken as following percentage of sales:

Product A |

80% |

Product B |

75% |

Product C |

70% |

You are required to tabulate the above information to present comparative profit and loss statements for each zone and for each product.

[I.C.W.A. Modified]

[Ans: Zone-wise profit: Zone X: Rs. 24,000; Y: 52,500;

Z: Rs. 13,000

Product-wise profit: Product A: Rs. 29,400;

B: 31,500; C: Rs. 38,600]

8. Cosmos Ltd. manufactures three types of products A, B and C. The sales territory of the company is divided into three areas: North, South and Central. The estimated sales for the year are as follows:

Budgeted advertising cost is as follows:

|

Rs. |

North |

6,400 |

South |

9,000 |

Central |

7,800 |

Common |

11,600 |

You are required to work out the advertising cost per cent on sales for each product and each territory and prepare a suitable statement for presentation to management.

[I.C.W.A. (Inter)]

[Ans: A: 6-29 per cent B: 5-45 per cent C: 6-36 per cent North: 6 per cent South: 7 per cent and Central 5-25 per cent]

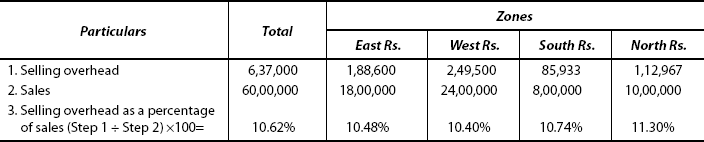

9. XYZ Ltd, a manufacturing company, having an extensive marketing network throughout the country, sells its products through four zonal offices, viz. A, B, C and D. The budgeted expenditure for the year is given below:

|

Rs. |

Sales manager’s salary |

1,20,000 |

Expenses relating to sales |

80,000 |

manager’s office |

|

Travelling salesmen’s salaries |

3,20,000 |

Travelling expenses |

36,000 |

Advertisements |

30,000 |

Godown Rent: |

|

Zone A – Rs. 15,000 |

|

Zone B – Rs. 25,200 |

|

Zone C – Rs. 9,800 |

|

Zone D – Rs. 18,000 |

68,000 |

Insurance on inventories |

20,000 |

Commission on sales at 5% on sales |

6,00,000 |

The Following Particulars are Available:

Based on above details, compute zone-wise selling overheads as a percentage to sales

[I.C.W.A. (Inter)]

[Ans: A: 10.48 per cent; B: 10.40 per cent; C: 10.74 per cent; D: 11.30 per cent Total: 10.62 per cent]