7

Single Costing*

LEARNING OBJECTIVES

After studying this chapter you should be able to:

Understand the meaning and features of output costing.

Distinguish between the historical cost sheet and the estimated cost sheet.

Understand the significance of cost sheet.

Prepare a cost sheet and a production account.

Comprehend the special treatment of stock.

Differentiate between a cost sheet and a production account.

Explain the meaning of certain key terms.

7.1 UNIT COSTING

Unit costing is a method of costing. This method is used:

- In industries producing identical products or a single article on a large scale

- Where manufacturing process (i.e. production) is uniform

- Where cost units are having identical costs

Ascertainment of cost per unit is to be arrived at by dividing total cost by number of units. Unit costing is suitable for industries manufacturing homogeneous products like sugar, bricks, cement works, collieries and breweries.

7.2 FEATURES OF OUTPUT COSTING

- Average unit cost: Average cost per unit is computed by dividing the total costs by the number of units produced in a specified period.

- Single product: In this method of costing, only a single product or a number of grades of the product are involved.

- Applicability: This method of costing is applied to industries where the manufacturing process is not continuous.

7.3 ANALYSIS OF COST

The collection of costs incurred on material labour and direct expenses is to be carried out in a manner discussed earlier in respective chapters. The total cost is analysed in terms of prime cost, factory cost or works cost, office cost or cost of production.

The prime cost consists of cost of (1) raw materials, (2) direct labour and (3) direct expenses. But as per CIMA terminology, “direct expenses” have been excluded from prime cost.

The works cost consists of prime cost PLUS works (factory) overheads.

The cost of production consists of works cost PLUS office and administration overheads.

The total cost (or) cost of sales consists of cost of production PLUS selling and distribution overheads.

Overheads are included in respective accounts based on estimates.

This kind of analysis is to be presented through a cost sheet or a production account.

7.4 COST SHEET

The terminology of CIMA defines cost sheet “as a document which provides for the assembly of the estimated detailed cost in respect of a cost centre or a cost unit”. Cost sheet is a periodical statement of cost depicted to show in detail the various elements of cost, namely, prime cost, works cost, cost of production, cost of sales.

Cost sheet can be prepared either based on actual data or on estimated data. Depending on preparation it can be classified into (1) historical cost sheet and (2) estimated cost sheet.

7.4.1 Historical Cost Sheet

Historical cost sheet is to be prepared after the costs have been incurred. It is prepared based on the costs that have been incurred actually. It is prepared periodically. If it is prepared at shorter intervals, comparisons can be made and effective decision-making can be made for cost control.

7.4.2 Estimated Cost Sheet

Actually, it is prepared before the commencement of production. It is prepared based on the estimated data. It is prepared at regular intervals. The estimated costs are compared with actual costs and effective cost control and decision-making is arrived at.

Specimen of a cost sheet is shown below:

Number of units produced

| Particulars | Total Cost Rs. | Cost per Unit Rs. |

|---|---|---|

Direct materials |

|

|

Direct labour |

|

|

Direct expenses |

|

|

PRIME COST |

|

|

Works overheads |

|

|

WORKS COST |

|

|

Office and administration overheads |

|

|

COST OF PRODUCTION |

|

|

Selling and distribution overheads |

|

|

TOTAL COST |

|

|

or |

|

|

COST OF SALES |

|

|

Additional columns may be provided with cost data pertaining to previous periods, for easy comparison.

7.4.3 Uses of Cost Sheet

- It provides information on total cost and cost per unit of a product for a specified period.

- It facilitates the process of cost control.

- It helps the management in decision-making process.

- It helps in fixing the selling price of products.

- It facilitates comparative study of actual costs with the cost of relative corresponding periods.

7.4.4 Exclusion of Certain Items from Cost Sheet

Some items, which are of financial nature, are not to be included in a cost sheet. They are:

- Donations

- Cash discount

- Interest paid

- Income tax paid

- Dividend paid

- Preliminary expenses written off

- Goodwill written off

- Profit or loss on sale of assets

- Transfer to reserves

- Provision—for taxes, bad debts etc.

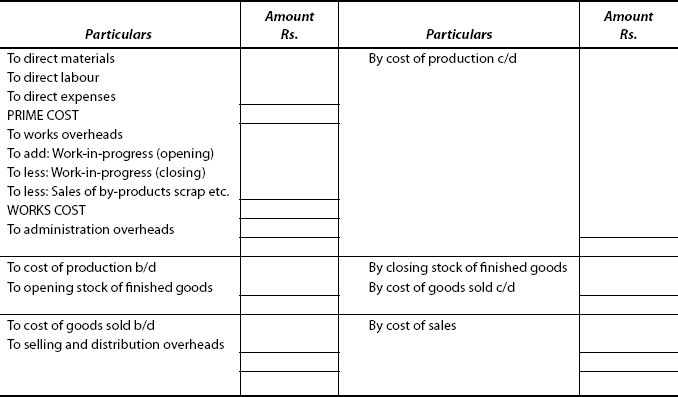

7.5 PRODUCTION ACCOUNT

- In this document, or account, in addition to the details shown in the cost sheet, the following items are to be included:

- Finished goods inventories

- Sales and

- Profit or loss

- These items are shown in the form of ledger account.

- It is an account depicting cost of production, sales and profit/loss during a specified period.

- It is prepared in three parts:

Part 1 → consists of the cost of production

Part 2 → consists of the cost of goods sold

Part 3 → consists of the cost of sales

A specimen of production account is shown below:

7.6 DIFFERENCE BETWEEN COST SHEET AND PRODUCTION ACCOUNT

The following are the differences between cost sheet and production account:

| Basis of Disinction | Cost Sheet | Production Account |

|---|---|---|

1. Format |

It is shown as a statement. |

It is shown as ledger account. |

2. Classification of expenses |

Expenses are classified to compute prime cost, works cost, total cost. |

Expenses are not classified. |

3. Accounting system |

Cost sheet is not based on double-entry system. |

It is based on double-entry system. |

4. Comparison |

Comparison is possible as previous period data are provided. |

Comparison is not possible, as there are no previous period data. |

5. Basis |

It is based on actual and estimated figures of expenses. |

It is based on actual figures only. |

6. Coverage |

It is prepared for each job. |

It is prepared for each production department. |

7. Usefulness |

It is useful for preparing tenders or quotations. |

It may not be useful for preparing tenders or quotations. |

7.7 PREPARATION OF A COST SHEET

We have to discuss certain items that require special treatment in the preparation of cost sheet.

7.7.1 Stock

Stock may be of

- Raw materials

- Work-in-progress and

- Finished goods

7.7.1.1 Stock of Raw Materials

Raw materials consumed during the period can be calculated as:

|

Rs. |

Opening stock of raw materials |

….. |

Add: Purchase of raw materials |

….. |

|

XXX |

Less: Closing stock of raw materials |

……. |

Value of raw materials consumed |

XXX |

Example:

Calculate the value of raw materials consumed, from the following data:

|

Rs. |

Raw materials purchased |

70,000 |

Opening stock of raw materials |

15,000 |

Closing stock of raw materials |

35,000 |

Solution

|

Rs. |

Opening stock of raw materials |

15,000 |

Add: Purchase of raw materials |

70,000 |

85,000 |

|

Less: Closing stock of raw materials |

35,000 |

Value of raw materials consumed |

50,000 |

7.7.1.2 Stock of Work-in-Progress

Work-in-progress means units (products) which are not yet completed but manufacturing process has been initiated, that is, semi-finished goods. Work-in-progress is valued either as prime cost basis or works cost basis. In practice, mostly it is valued at works cost. Opening and closing stock will have to be adjusted as follows:

|

Rs. |

Prime Cost |

.…. |

Add: Factory overheads |

.…. |

Add: Work-in-progress (beginning) |

.…. |

|

xxx |

Less: Work-in-progress (closing) |

.…. |

Works cost |

xxx |

Example:

Compute the works cost from the following:

|

Rs. |

Materials |

40,000 |

Labour |

30,000 |

Direct expenses |

15,000 |

Factory overheads |

35,000 |

Work-in-progress: |

|

Opening stock |

17,000 |

Closing stock |

7,000 |

Solution

To determine prime cost add materials, labour, and direct expenses. The aggregate value of these items will be the prime cost.

Based on the prime cost, adjustments have to be made as follows:

|

Rs. |

Materials |

40,000 |

Labour |

30,000 |

Direct expenses |

15,000 |

PRIME COST |

85,000 |

Factory overheads |

35,000 |

GROSS WORKS COST |

1,20,000 |

Add: Opening stock of work-in-progress |

17,000 |

|

1,37,000 |

7,000 |

|

WORKS COST (or) FACTORY COST |

1,30,000 |

7.7.1.3 Stock of Finished Goods

Opening stock and closing stock of finished goods have to be adjusted before computing the cost of goods sold, as follows:

|

Rs. |

Cost of production |

.…. |

Add: Opening stock of finished goods |

.…. |

|

xxx |

Less: Closing stock of finished goods |

.…… |

Cost of goods sold |

xxx |

Example:

Calculate the cost of goods sold, from the following:

|

Rs. |

Cost of production |

85,000 |

Opening stock (finished goods) |

15,000 |

Closing stock |

25,000 |

Solution

|

Rs. |

Cost of production |

85,000 |

Add: Opening stock |

15,000 |

|

1,00,000 |

Less: Closing stock |

25,000 |

Cost of goods sold |

75,000 |

7.7.2 Computation of Profit

This is another item to be treated carefully while preparing a cost sheet. Profit has to be ascertained as a percentage of cost or as a percentage of selling price. To avoid confusion, students have to remember always the basic equation:

Cost price + Profit = Selling price

CASE 1: Given: Cost price and profit as a percentage of cost

Required: Profit on cost

Example:

Cost price = Rs. 7,000

Profit = 20% of cost

Calculate the profit on cost.

In this case, profit can be calculated straightaway by applying the percentage as follows:

Profit on cost |

= Cost price × Percentage of cost |

|

= Rs. 7,000 × 20% |

= Rs. 7,000 × 20/100 |

|

|

= Rs. 1,400. |

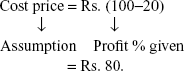

CASE 2: Given: Cost price and profit as percentage on selling price

Required: Profit on cost

Example:

Cost price = Rs. 7,000

Profit is 20% on selling price.

Calculate the profit on cost price.

We have to remember the equation and then the following procedure is adopted.

Let selling price be Rs. 100 (assumption)

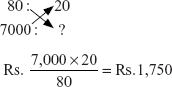

Equation: Cost price = Selling price – Profit

On a cost price of 80, the profit is Rs. 20.

On a cost price of Rs. 7,000, the profit?

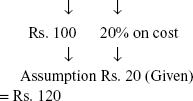

CASE 3: Given: Selling price and profit as percentage on cost

Required: Profit on selling price

Example:

Selling price is Rs. 7,000

Profit = 20% on cost

Compute profit on selling price.

Remember the equation:

Selling price = Cost + Profit

Cost price is not given.

So let the cost price be Rs. 100 (Assumption).

Then selling price will be (cost + profit)

On a selling price of Rs. 120, profit is Rs. 20.

On a selling price of Rs. 7,000, profit is ?

Profit on selling price of Rs. 7000 = Rs. 1166.67

Remember the above three cases whenever any question arises in the computation of profit while preparing a cost sheet.

Illustration 7.1

Model: Preparation of cost sheet

X Ltd manufactures a consumable product. From the following data relating to a year, you are required to prepare the cost sheet.

|

Rs. |

Materials (opening) |

30,000 |

Materials (closing) |

25,000 |

Work-in-progress (opening) |

50,000 |

Work-in-progress (closing) |

55,000 |

Finished goods (opening) |

60,000 |

Finished goods (closing) |

80,000 |

Materials purchased during the year |

1,20,000 |

Direct labour |

90,000 |

Manufacturing overhead |

80,000 |

Selling expenses |

40,000 |

General expenses |

32,000 |

Sales |

3,92,000 |

Solution

| Rs. | ||

|---|---|---|

Step 1: Materials used (consumed) |

Rs. |

|

Raw materials: |

|

|

(a) Purchases |

1,20,000 |

|

(b) Add: Opening stock |

30,000 |

|

|

1,50,000 |

|

(c) Less: Closing stock |

25,000 |

1,25,000 |

Step 2: Labour |

|

90,000 |

PRIME COST |

|

2,15,000 |

Step 3: Manufacturing overheads |

|

80,000 |

GROSS WORKS COST |

|

2,95,000 |

Step 4: (a) Add: Opening work-in-progress |

|

50,000 |

|

|

3,45,000 |

(b) Less: Closing work-in-progress |

|

55,000 |

WORKS COST (or) FACTORY COST |

|

2,90,000 |

Step 5: General expenses |

|

32,000 |

COST OF PRODUCTION |

|

3,22,000 |

Step 6: (a) Add: Opening stock of finished goods |

|

60,000 |

|

|

3,82,000 |

(b) Less: Closing stock of finished goods |

|

80,000 |

COST OF GOODS SOLD |

|

3,02,000 |

Step 7: Add: Selling expenses |

|

40,000 |

Step 8: (COST OF SALES) or TOTAL COST |

|

3,42,000 |

Step 9: *PROFIT (Step 10 - Step 8) |

|

50,000 |

Step 10: SALES |

|

3,92,000 |

(* Profit = Sales – Total cost)

Illustration 7.2

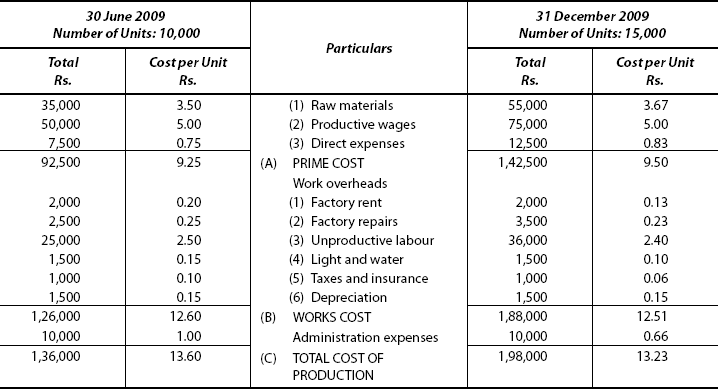

Model: Comparative (cost sheet) form

From the following figures, you are required to prepare a cost sheet showing the comparative cost per unit of the product for both the periods:

| Six Months Ended | ||

|---|---|---|

| 30 June 2009 Rs. | 31 December 2009 Rs. | |

Productive wages |

50,000 |

75,000 |

Raw materials |

35,000 |

55,000 |

Administrative expenses |

10,000 |

10,000 |

Taxes and insurance (factory) |

1,000 |

1,000 |

Direct expenses |

7,500 |

12,500 |

Light and water |

1,500 |

1,500 |

Depreciation |

1,500 |

1,500 |

Factory rent |

2,000 |

2,000 |

Unproductive labour |

25,000 |

36,000 |

Repairs – factory |

2,500 |

3,500 |

|

1,36,000 |

1,98,000 |

Total number of units produced for the two periods are 10,000 units and 15,000 units, respectively.

Solution

Illustration 7.3

Model: Computation of selling price

From the following information, you are required to prepare a cost sheet for the year.

|

Rs. |

Consumable materials: |

|

Opening stock |

15,000 |

Purchases |

1,15,000 |

Closing stock |

20,000 |

Direct wages |

30,000 |

Other direct expenses |

15,000 |

Factory overheads |

100% of direct wages |

Office overheads |

10% of works cost |

Selling and distribution expenses |

Rs. 3 per unit sold |

Units of finished products |

|

In hand at the beginning of the period: (Value: Rs. 26,500) |

2,000 |

Produced during the period |

20,000 |

In hand at the end of the period |

3,000 |

Also find the selling price per unit assuming that profit margin is uniformly made to yield a profit of 20% on selling price. (Assume that there is no work-in-progress in the beginning as well as at the end of the year.)

Solution

This question has to be solved in two parts.

Part 1 → Total cost is to be ascertained by preparing cost sheet.

Part 2 → Selling price is to be computed.

Part 1

Output: 20,000 units

| Particulars | Amount Rs. | |

|---|---|---|

Step 1: Raw materials consumed: |

Rs. |

|

Opening stock |

15,000 |

|

Add: Purchases |

1,15,000 |

|

|

1,30,000 |

|

Less: Closing stock |

20,000 |

1,10,000 |

Step 2: Direct wages |

|

30,000 |

Step 3: Direct expenses |

|

15,000 |

Step 4: PRIME COST (Step 1 + Step 2 + Step 3) |

|

1,55,000 |

Step 5: Factory overheads (100% on direct wages) |

|

30,000 |

Step 6: WORKS COST (or) FACTORY COST |

|

1,85,000 |

|

|

18,500 |

Step 8: TOTAL COST |

|

2,03,500 |

Part 2

Sales: 19,000 Units

Illustration 7.4

Model: Computation of cost of production (manufacturing expenses at prime cost)

VRS Ltd is manufacturing DVD players and the following details are provided by it for the year ended 31 March 2010.

|

Rs. |

Rs. |

Work-in-progress, 1 April 2009 |

|

|

At prime cost |

60,000 |

|

Manufacturing expenses |

15,000 |

75,000 |

Work-in-progress, 31 March 2010 |

|

|

At prime cost |

50,000 |

|

Manufacturing expenses |

10,000 |

60,000 |

Stock of raw materials, 1 April 2009 |

|

3,00,000 |

Purchase of raw materials |

|

7,00,000 |

Direct labour |

|

1,40,000 |

Manufacturing expenses |

|

90,000 |

Stock of raw materials, 31 March 2010 |

|

3,20,000 |

Based on above data, prepare a statement showing cost of production. You are required to show separately the amount of manufacturing expenses which enter into the cost of production.

Solution

NOTE:

- In this problem, work-in-progress is to be adjusted as prime cost (not works cost), as desired in the question, that is, prime cost is arrived at after adjusting work-in-progress.

- Manufacturing expenses relating to work-in-progress are adjusted after computing prime cost as desired by the problem.

Preparation of statement showing cost of production by showing separately manufacturing expenses which enter into the cost of production is done as follows:

Statement Showing Cost of Production of DVD Players for the Year Ended 31 March 2010

| Particulars | Amount (Rs.) | Amount (Rs.) |

|---|---|---|

Stepl: Raw materials consumed: |

|

|

Stock as of 1 April 2009 |

3,00,000 |

|

Add: Purchases |

7,00,000 |

|

|

10,00,000 |

|

Less: Stock on 31 March 2010 |

3,20,000 |

6,80,000 |

Step 2: Direct labour |

|

1,40,000 |

|

|

8,20,000 |

Step 3: Add: Work-in-progress, |

|

60,000 |

1 April 2009 (at prime cost) |

|

|

|

|

8,80,000 |

Step 4: Less: Work-in-progress, |

|

50,000 |

31 March 2010 (at prime cost) |

|

|

Step 5: PRIME COST |

|

8,30,000 |

Manufacturing Expenses: |

|

|

Step 6: Relating to work-in- |

15,000 |

|

progress, 1 April 2009 |

|

|

Step 7: Add: Expenses incurred |

90,000 |

|

in the year |

|

|

|

1,05,000 |

|

Step 8: Less: Relating to work-in- |

10,000 |

95,000 |

progress, 31March 2010 |

|

|

Step 9: COST OF PRODUCTION |

|

9,25,000 |

Illustration 7.5

Model: Cost sheet (value of stock to be computed)

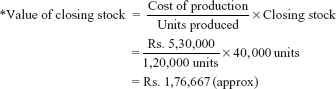

Vasant Ltd manufactures a product. A summary of its activities for the year 2009–2010 is given below:

Units |

Rs. |

|

Sales |

1,00,000 |

10,00,000 |

Material, 1 April 2009 |

|

50,000 |

Material, 31 March 2010 |

|

35,000 |

Work-in-progress, 1 April 09 |

|

45,000 |

Work-in-progress, 31 March 10 |

|

60,000 |

Finished goods, 1 April 2009 |

20,000 |

1,00,000 |

Finished goods, 31 March 2010 |

40,000 |

|

Materials purchased |

|

2,00,000 |

Direct labour |

|

1,60,000 |

Manufacturing overhead |

|

1,20,000 |

Selling expenses |

|

1,10,000 |

General expenses |

|

50,000 |

Prepare a cost sheet. |

|

|

[B.Com (Hons), Delhi. Modified]

Solution

Number of Units Produced: 1,20,000 (1,00,000 + 40,000 – 20,000)

| Rs. | Rs. | |

|---|---|---|

Step 1: Materials consumed: |

|

|

Opening stock |

50,000 |

|

Add: Purchases |

2,00,000 |

|

|

2,50,000 |

|

Less: Closing stock |

35,000 |

|

|

|

2,15,000 |

Step 2: Direct labour |

|

1,60,000 |

Step 3: PRIME COST |

|

3,75,000 |

Step 4: Manufacturing overheads |

|

1,20,000 |

Step 5: Add: Opening work-in-progress |

|

45,000 |

|

|

5,40,000 |

Step 6: Less: Closing work-in-progress |

|

60,000 |

Step 7: FACTORY COST or WORK COST |

|

4,80,000 |

Step 8: General expenses |

|

50,000 |

Step 9: COST OF PRODUCTION |

|

5,30,000 |

Step 10: Add: Opening stock of finished goods |

|

1,00,000 |

|

|

6,30,000 |

*Step 11: Less: Closing stock of finished goods |

|

1,76,667 |

Step 12: COST OF GOODS SOLD |

|

4,53,333 |

Step 13: Selling expenses |

|

1,10,000 |

Step 14: TOTAL COST |

|

5,63,333 |

Step 15: PROFIT (Step 16 – Step 14) |

|

4,36,667 |

Step 16: SALES (Given) |

|

10,00,000 |

Illustration 7.6

Model: Cost sheet with the following columns: Total cost, % to Total cost, Cost/unit

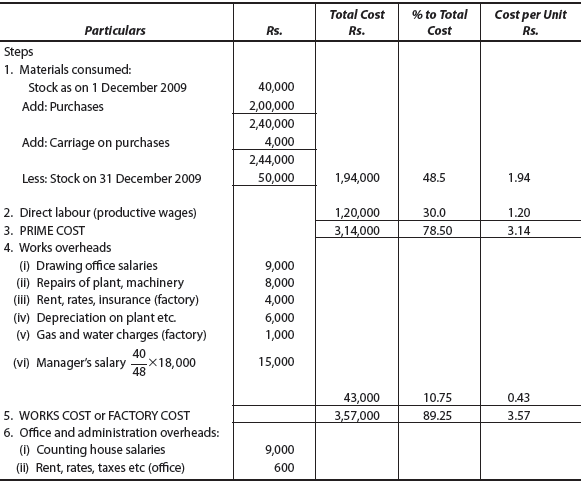

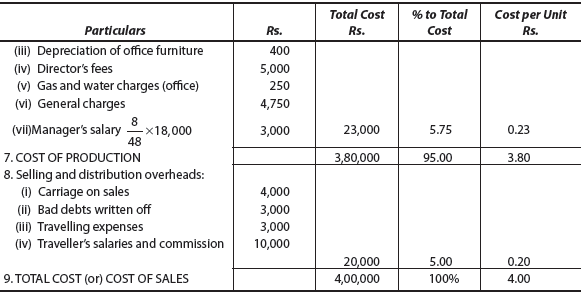

The following particulars have been extracted from the books of a manufacturing company for the month of December 2009:

Rs. |

|

Stock of materials as on 1 December 2009 |

40,000 |

Stock of materials as on 31 December 2009 |

50,000 |

Materials purchased during the month |

2,00,000 |

Drawing office salaries |

9,000 |

Counting house salaries |

9,000 |

Carriage on purchases |

7,000 |

Carriage on sales |

4,000 |

Cash discount allowed |

2,750 |

Bad debts written off |

3,000 |

Repairs of plant, machinery and tools |

8,000 |

Rent, rates, taxes and insurance (factory) |

4,000 |

Rent, rates, taxes and insurance (office) |

600 |

Travelling expenses |

3,000 |

Traveller’s salaries and commission |

10,000 |

Productive wages |

1,20,000 |

Depreciation written off on plant, machinery, tools |

6,000 |

400 |

|

Director’s fees |

5,000 |

Gas and water charges (factory) |

1,000 |

Gas and water charges (office) |

250 |

General charges |

4,750 |

Manager’s salary |

18,000 |

Out of 48 working hours in a week, the time devoted by the manager to the factory and office was on an average 40 hours and 8 hours respectively. 1,00,000 units were produced and sold. There was no opening and closing stock of it.

You are required to prepare a cost sheet showing:

- Cost of materials consumed

- Prime cost

- Works overhead

- Works cost

- Office and administration overhead

- Cost of production

- Selling and distribution overhead

- Cost of sales

Each with percentage to total cost and cost per unit.

Important Note

Cash discount allowed is of financial nature. Hence it is excluded from costs.

7.8 TREATMENT OF SCRAP

- Scrap is residue arising in a manufacturing process.

- Its quantity is small and value is low.

- It is mostly recoverable without further processing.

- Any realization by sale of scrap is deducted from gross works cost or works overheads.

- Materials found to be defective before undergoing process should be sold and deducted from the cost of such materials.

- Loss on sale of such materials is to be charged to costing profit and loss account.

7.8.1 Treatment of Spoilage and Defective Work

- Spoilage means goods that are damaged and that cannot be rectified.

- Defective means goods damaged but can be rectified

- Normal spoilage: Loss due to normal spoilage is to be spread over good units. The same is the case with normal defectives.

- Abnormal spoilage and abnormal defectives: Loss on account of these should be charged to costing profit and loss account.

Illustration 7.7

Input 500 units @ Rs. 10 per unit.

Direct labour Rs. 3,000.

Factory overheads 100% of direct labour.

10% of the units introduced is considered as normal spoilage which realizes Rs. 6 per unit.

Another 10% of the input is considered to be normal defectives.

Actual spoilage amounts to 75 units; while actual defectives are 100 units. The cost of rectification of defective goods is Rs. 5 per unit.

You are required to prepare the cost sheet and compute the amount to be charged to costing profit and loss account.

Solution

| Particulars | Units | Rs. |

|---|---|---|

Step 1 Direct material (input) |

500 |

5,000 |

Step 2 Direct labour |

|

3,000 |

Step 3 PRIME COST (Step 1 + Step 2) |

|

8,000 |

Step 4 Factory overheads (100% of direct labour) |

|

3,000 |

GROSS FACTORY COST |

500 |

11,000 |

Step 5 Less: Normal spoilage (10% of 500 units) 50 x Rs. 6 |

50 |

300 |

|

450 |

10,700 |

Step 6 Less: Cost of abnormal spoilage |

|

|

|

25 |

594 * |

|

425 |

10,106 |

Step 7 Add: Cost of rectification of normal defective units: 50 x 5 |

– |

250 |

FACTORY COST |

425 |

10,356 |

| Rs. | Rs. | |

|---|---|---|

* Cost of abnormal spoilage |

594 |

|

Less: Amount realized on sale of spoiled goods (25 × Rs. 6) (75 – 50) |

150 |

|

|

|

444 |

Cost of rectification of abnormal defective goods: 50 units × Rs. 5 (100 – 50) |

|

250 |

Total loss |

|

694 |

Illustration 7.8

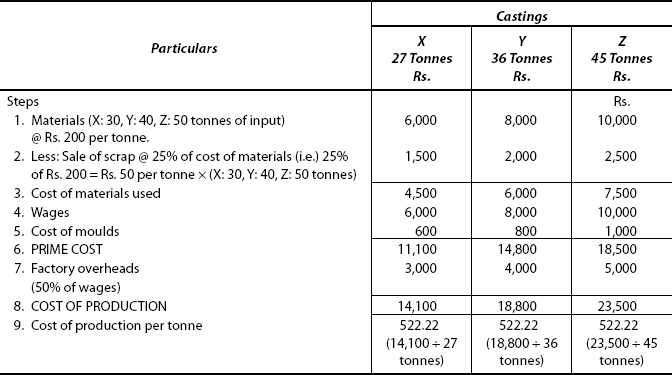

Model: Scrap – Raw materials

A factory has received an order of three different types of casting X, Y and Z, weighing respectively 27, 36 and 45 tonnes. 10% of raw materials used are wasted in manufacturing process and are sold as scrap for 25% of the cost price of raw materials.

The cost of raw materials is Rs. 200 per tonne. The wages for the three types of castings are Rs. 6,000, Rs. 8,000 and Rs. 10,000 respectively. The costs of moulds for the three different types of costings are Rs. 600, Rs. 800 and Rs. 1,000 respectively.

If the factory overhead charges are 50% of the wages in each case, find the cost of production per tonne for each type of casting.

[I.C.W.A. (Inter). Modified]

Solution

10% of raw material used is wasted.

Then finished output will be 100% – 10% = 90%.

For finished output of 90 tonnes, raw materials required = 100 tonnes.

- For finished output of 27 tonnes, raw materials required

- For finished output of 36 tonnes, raw materials required

- For finished output of 45 tonnes, raw materials required

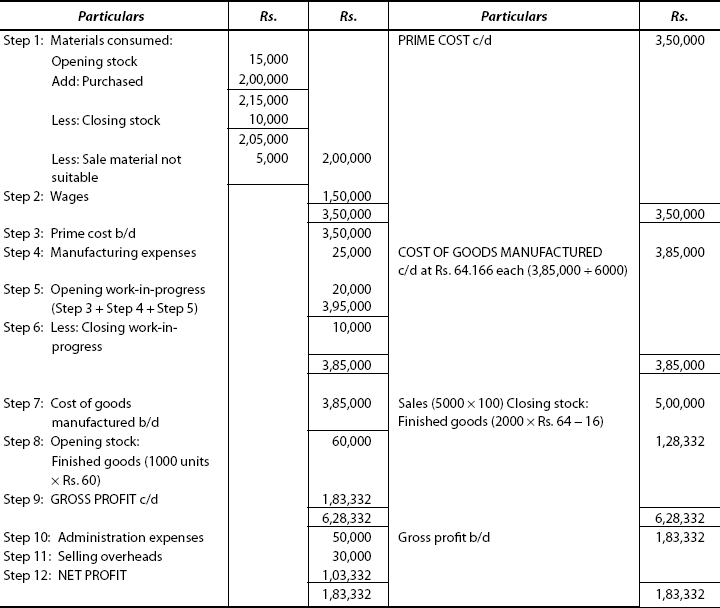

7.9 PREPARATION OF PRODUCTION ACCOUNT

Illustration 7.9

Prepare a production account for March 2010 from the following particulars showing the final cost per unit produced.

|

Rs. |

Materials purchased |

2,00,000 |

Wages |

1,50,000 |

Manufacturing expenses |

25,000 |

Sale of materials (not suitable) |

5,000 |

Inventories: |

|

Materials: Opening |

15,000 |

Closing |

10,000 |

Work-in-progress: |

|

Opening |

20,000 |

Closing |

10,000 |

Finished goods: |

|

Opening: 1000 units at Rs. 60 each |

|

Closing: 2000 units at current cost |

|

Administration expenses |

50,000 |

Selling overheads |

30,000 |

Output during the month was 6,000 units |

|

Sales for the month 5,000 units at Rs. 100 each. |

|

Solution

Remember, production account is to be prepared in the traditional ledger account method.

Important stages

This is shown in the following production account:

Important Note

“To” and “By” are omitted in the ledger account. These prefix words are, of late, not used in ledger accounts, being the latest trend in accounting procedure.

7.10 FOR PROFESSIONAL COURSES

Illustration 7.10

Model: Cost of production of goods manufactured – statement of cost of sales and profit earned

The following data have been extracted from the records of XYZ Co. Ltd for the month of December 2009.

|

Rs. |

Cost of raw materials on 1 December 2009 |

25,000 |

Raw materials purchased during the month |

4,20,000 |

Wages paid |

2,00,000 |

Factory overheads |

70,000 |

Cost of work-in-progress on 1 December 2009 |

10,000 |

Cost of raw materials on 31 December 2009 |

15,000 |

12,000 |

|

Cost of stock of finished goods on 1 December 2009 |

40,000 |

Cost of stock of finished goods on 31, December 2009 |

37,000 |

Administration overheads |

25,000 |

Selling and distribution overheads |

20,000 |

Sales |

8,00,000 |

You are required to prepare:

- Cost sheet showing the cost of production of goods manufactured

- Statement showing the cost of sales and the profit earned.

[C.S. (Inter). Modified]

Solution

Important Notes

- For work-in-progress: Cost of opening and closing stock of work-in-progress should be adjusted after the factory overhead is added to the prime cost and before the works cost is arrived at. The reason is that factory overheads are incurred on work-in-progress also.

- For selling and distribution expenses: Selling and distribution expenses would have incurred only on the goods sold and not on the goods in stock.

for the Month of December 2009

| Rs. | Rs. | |

|---|---|---|

Step 1: Raw materials consumed |

25,000 |

|

Cost of raw materials on 1 December 2009 |

|

|

Add: Purchases during |

4,20,000 |

|

December 2009 |

4,45,000 |

|

Less: Cost of raw materials on 31 December 2009 |

15,000 |

|

|

|

4,30,000 |

Step 2: Direct wages |

|

2,00,000 |

Step 3: PRIME COST |

|

6,30,000 |

Step 4: Factory overheads |

|

70,000 |

|

|

7,00,000 |

Step 5: Add: Cost of work-in-progress on 1 December 2009 |

10,000 |

|

|

|

7,10,000 |

Step 6: Less: Cost of work-in-progress on 31 December 2009 |

|

12,000 |

Step 7: FACTORY COST (or) WORKS COST |

|

6,98,000 |

Step 8: Administration overheads |

|

25,000 |

Step 9: COST OF PRODUCTION OF GOODS MANUFACTURED |

|

7,23,000 |

| Rs. | |

|---|---|

Step 1: Cost of stock of finished goods on 1 December 2009 |

40,000 |

Step 2: Add: Cost of goods manufactured during December (Transfer from Step 9 of cost sheet) |

7,23,000 |

Step 3: Cost of total goods available for sale |

7,63,000 |

Step 4: Less: Cost of stock of finished goods on 31 December 09 |

37,000 |

Step 5: COST OF GOODS SOLD |

7,26,000 |

Step 6: Add: Selling and distribution overhead |

20,000 |

Step 7: TOTAL COST (or) COST OF SALES |

7,46,000 |

Step 8: PROFIT (Step 9 – Step 7) |

54,000 |

Step 9: |

8,00,000 |

Illustration 7.11

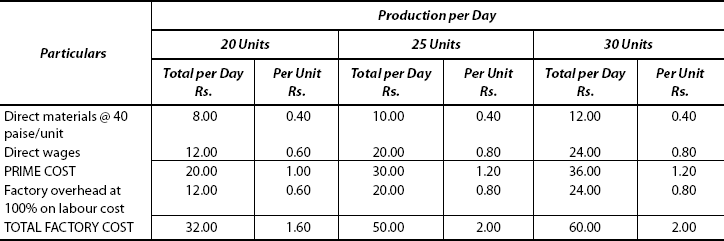

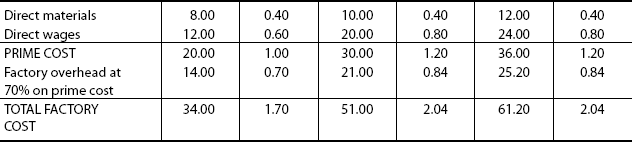

Model: Factory cost per unit – computation

The standard production for a particular work order is 25 units per day, and the price rate wage is 80 paise per unit if the production is 25 units or more. The rate is 60 paise if production is less than 25 units. Cost of material is 40 paise per unit. It is proposed to charge factory overheads under one of the following methods:

- 100% of labour cost

- 70% of prime cost

You are required to tabulate the above data in the form of a suitable statement and indicate the factory cost per unit under each of the above methods if the daily production is (i) 20 units (ii) 25 units and (iii) 30 units.

[I.C.W.A. (Inter). Modified]

Solution

Method (1): 100% on labour cost

Statement showing factory cost per unit

Method (2): Factory overheads at 70% of prime cost

Illustration 7.12

Model: Quotation of selling price

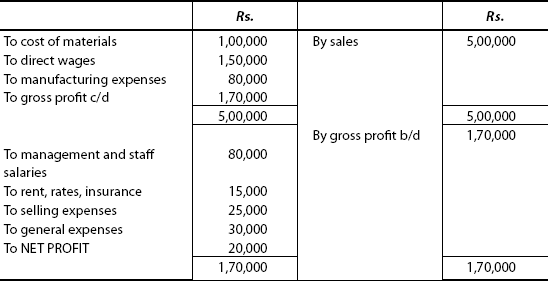

Alpha Co. Ltd manufactured and sold 1,000 iron boxes in the year ending 31 March 2010. The summarized trading and profit and loss account is shown as follows:

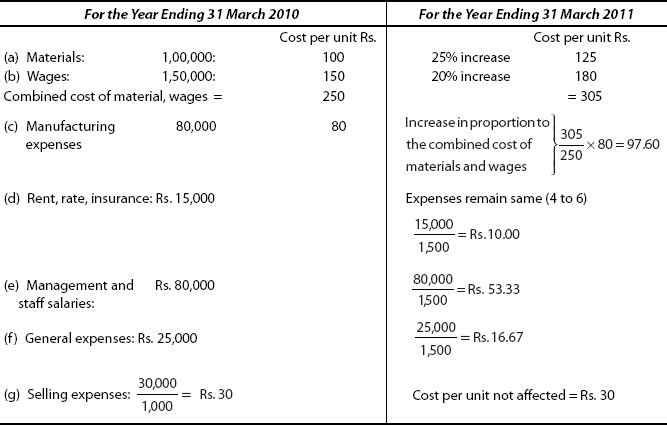

For the year ending 31 March 2011 it is estimated that

- Output and sales will be 1,500 iron boxes.

- Prices of raw materials will rise by 25% on the previous year’s level.

- Wages will rise by 20%.

- Manufacturing cost will rise in proportion to the combined cost of materials and wages.

- Selling cost per unit will remain unaffected.

- Other expenses will remain unaffected by the rise in output.

You are required to submit a statement to the board of directors showing the price at which the iron box should be marketed so as to show a profit of 20% on selling price.

Solution

Basic calculations

For the year ending on 31 March 2010, cost per unit for the following items has to be computed, and based on the figures, estimation for next year has to be made:

Statement showing the price at which iron boxes should be marketed in 2010–2011.

| Rs. | |

|---|---|

Step 1: Materials |

125.00 |

Step 2: Direct wages |

180.00 |

Step 3: PRIME COST (Step 1 + Step 2) |

305.00 |

Step 4: Manufacturing cost (Ref: (c) above) |

97.60 |

Step 5: WORKS COST Add: |

402.60 |

Step 6: (i) Rent, rate, insurance (Ref: (d) above) |

10.00 |

(ii) Management and staff salaries (Ref: (e) above) |

53.33 |

(iii) General expenses (Ref: (f) above) |

16.67 |

Step 7: COST OF PRODUCTION |

482.60 |

Step 8: Selling expenses |

30.00 |

Step 9: TOTAL COST (or) COST OF SALES |

512.60 |

*Step 10: PROFIT (20% on selling price) |

128.15 |

Step 11: SELLING PRICE |

640.75 |

* Profit @ 20% on selling price ![]()

Illustration 7.13

(Miscellaneous)

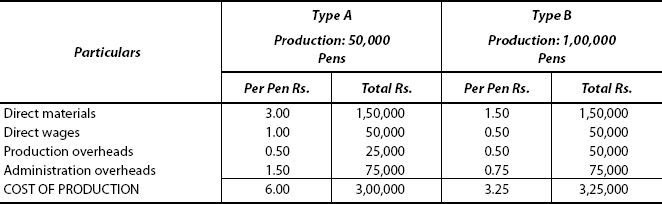

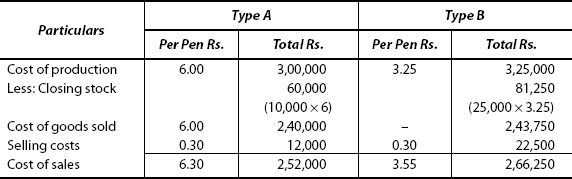

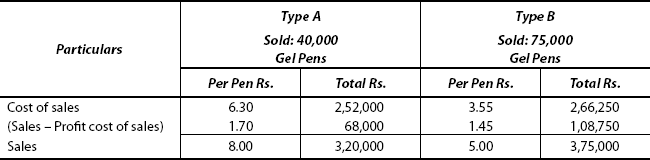

The Super Fine Pen Co. manufactures two types of gel pens A and B. The manufacturing costs for the year ended 31 December 2009 were:

Rs. |

|

Direct material |

3,00,000 |

Direct wages |

1,50,000 |

Production overheads |

50,000 |

|

5,00,000 |

It is ascertained that:

- Direct materials in ‘A’ costs twice as much as direct material in type “B”

- Direct wages for type ‘B’ were 50% if those for type ‘A’.

- Production Overhead was 50 Paise the same per pen of type A & B.

- Administration Overhead for each type was 150% of direct wages

- Selling cost was 30 Paise per pen for each type of Gel Pen

- Production and sales during the period was:

Type A – 50,000 gel pens of which 40,000 were sold

Type B – 1,00,000 gel pens of which 75,000 were sold

- Selling prices were Rs. 8 for type A and Rs. 5 per gel pen of type B.

You are required to prepare a statement showing the total cost per pen for each type of gel pen and the profit made on each type of pen.

[I.C.W.A. (Inter). Modified]

Solution

Statement of Cost of Production for the Year Ended 31 December 2009

Illustration 7.14

The cost structure of an LCD T V, the selling price of which is Rs. 90,000, is as follows:

Direct materials = 50% |

|

Direct labour = 20% |

|

Overheads = 30% |

|

An increase of 15% in the cost of materials and 25% in the cost of labour is anticipated. These increased costs in relation to the present selling price would cause a 25% decrease in the amount of present profit per T V. You are required to (1) prepare the statement of profit per TV at present and (2) the revised selling price to produce the same percentage of profit to sales as before.

[C.A. (Inter); I.C.W.A. (Inter). Modified]

Solution

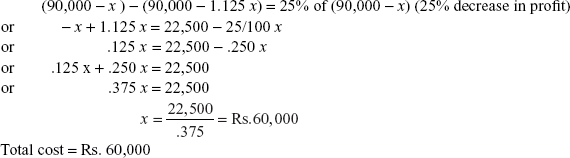

Selling price = Rs. 90,000 (Given)

Total cost is not given. So it is assumed as x.

Present position |

Anticipated level |

|

Direct material |

|

.575 x |

|

|

(increase of 15%) |

Direct labour |

20% or .2x |

.250 x |

|

|

(increase of 25%) |

Overheads |

30% or .3x |

. 300 x |

|

|

(no change) |

Total |

1.0 x |

1.125 x |

∴ Profit (selling price – total cost): (90,000 – x) (90 – 1.125 x)

From this, the following equation is obtained:

(1) Present statement of profit per TV

| Rs. | |

|---|---|

Direct material: .5 × 60,000 | 30,000 |

Direct labour: .2 × 60,000 | 12,000 |

Overheads: .3 × 60,000 | 18,000 |

Total cost | 60,000 |

Profit (selling price – total cost) | 30,000 |

Selling price | 90,000 |

Percentage of profit to cost ![]()

(or)

Percentage of profit to selling price ![]()

(2) Statement of revised selling price

| Rs. | |

|---|---|

Direct material 60,000 × .575 |

34,500 |

Direct labour 60,000 × .250 |

15,000 |

Overheads 60,000 × .300 |

18,000 |

Total anticipated cost |

67,500 |

Profit 50% on cost |

33,750 |

Selling price |

1,01,250 |

Summary

Unit Costing, a method of costing, under which cost per unit is determined by dividing the total costs by number of units. Features of output costing are: (i) Average Unit Cost, (ii) Single Product and (iii) Applicable if Manufacturing Process is not continuous.

Cost sheet is a document which provides for the assembly of the estimated detailed cost in respect of a cost centre.

Uses of cost sheet: (i) Provides data on total cost and cost per unit of a Product; (ii) facilitates cost control (iii) assists the decision making process (iv) facilitates fixing of selling price and (v) facilitates comparative study of costs.

The following items are excluded from cost sheet: (i) donation (ii) cash discount, (iii) interest paid; (iv) income tax paid; (v) dividend paid (vi) preliminary expenses written off; (vi) goodwill written off; (vii) profit or loss on sale of fixed assets; (ix) transfer to reserves and (x) provisions.

Production Account is prepared in three parts viz. (i) cost of production; (ii) cost of goods sold and (iii) cost of sales.

Accounting Treatment of Raw Materials, W.I.P and finished goods refer section 7.1.1 to 7.1.3 in the text.

Preparation of cost sheet: Ref. illustrations from 7.1 to 7.5. For accounting treatment of scrap, spoilage and defective work refer section 8 & 8.1 and illustrations 7.7 & 7.8. Preparation of Production Account is discussed in illustration 7.9.

Key Terms

Unit Costing (Single or Output Costing): A method of costing applied to firms that are engaged in the production of a single product or two or more grades of one product.

Cost Sheet: A document which provides for the assembly of the estimated detailed cost in respect of a cost centre or a cost unit.

Production Account: An account that provides details of cost of production, cost of sales and profit. Statement of cost and profit presented in ‘T’ form.

Scrap: Incidental residue from certain types of manufacturing processes of small amount and low value.

QUESTION BANK

Objective Type Questions

I: State whether the following statements are true or false

- Unit costing is a method of costing.

- Unit costing is suitable for industries producing a variety of products in large numbers.

- In unit costing work-in-progress is ignored.

- Cost sheet which includes income and profit is termed as production account.

- Output costing is suitable for assembly-type production such as computer, automobile.

- Scrap has no recoverable value.

- Cost sheet and production account are both one and the same.

- For the purpose of tender or quotation, unit costing method is useful.

- Sale value of scrap is charged to profit and loss account.

- Sale value of factory scrap is deducted from factory overhead.

Answers:

1. True |

2. False |

3. True |

4. True |

5. True |

6. False |

7. False |

8. True |

9. False |

10. True |

|

|

II. Fill in the blanks with suitable word(s)

- Unit or output costing is termed as one _____ costing.

- When units of output are _____, unit costing may be adopted.

- The cost per unit is determined by dividing the total cost during a given period by _____ produced during the same period.

- Scrap may be of two kinds: (1) material scrap and (2) _____.

- Production account is based on _____ system.

- Production account is prepared as a _____——account.

- Sale value of _____—is deducted from the cost of raw materials consumed.

- Ratio of administration overhead to _____ cost is used to charge office overhead in quotations.

- Ratio of _____ to works cost is used to charge selling and distribution overhead in tenders.

- In sugar industries, the unit of cost is _____.

Answers:

- operation

- identical

- number of units

- factory scrap

- double entry

- ledger

- raw material scrap

- works

- selling and distribution

- quintal

III: Multiple choice questions

- Unit costing is a

- technique

- method

- quotation

- tender

- Unit costing is also known as

- single operation costing

- contract costing

- job costing

- marginal costing

- Which one is a feature of unit costing

- It is based on specific order.

- It is for a specific contract work.

- Output is identical and uniform.

- It involves a number of processes in production.

- Unit costing is suitable for

- chemical manufacturing

- specific contract activities

- oil refineries

- sugar industry

- Tenders or quotations are usually based on

- cost statement alone

- profit alone

- future estimates

- previous period’s costs adjusted for future forecasts

Answers:

1. (b) |

2. (a) |

3. (c) |

4. (d) |

5. (d) |

|

|

|

Short Answer Questions

- Define unit or single or output or single operation costing.

- Name the industries where unit costing method may be applied.

- How unit cost can be ascertained?

- Define scrap. Mention the kinds of scrap.

- What is a tender?

- What is a production account?

- How would you treat raw material scrap?

- How would you treat factory scrap?

- What is the basis for the preparation of tender or quotation?

- In what ways a production account differs from a cost sheet?

Essay Type Questions

- Draw a pro forma of a cost sheet and production account. Use imaginary figures to explain the difference between the two.

- How costs are accumulated and ascertained in unit costing method. Use your own figures.

Exercises

[Model: Simple cost sheet]

1. A factory produces a standard product. The following information is given to you, from which you are required to prepare a cost sheet for January 2010:

|

Rs. |

Raw materials consumed |

1,82,000 |

Direct wages |

58,000 |

Other direct expenses |

22,000 |

Factory overheads: 80% of direct wages

Office overheads: 10% of works cost

Selling and distribution expenses: Rs. 4 per unit sold.

Units produced and sold during the month: 10,000

Also find the selling price per unit so that profit mark-up is uniformly made to yield a profit of 20% of the selling price. There was no stock or work-in-progress either at the beginning or at the end of the period.

[Ans: Prime cost: Rs. 2,62,000; Works cost: Rs. 3,08,400; Cost of production: 3,39,240; Cost of sales: 3,79,240; Profit: Rs. 94,810; Sales: 4,74,050; Selling price per unit: Rs. 47.40]

2. The following data relate to the manufacture of a standard product during the month of March 2010:

|

Rs. |

Raw materials: |

|

Opening stock |

30,000 |

Purchases |

70,000 |

Closing stock |

20,000 |

Wages |

1,20,000 |

Works on cost, 50% of wages; office on cost, 20% on works cost; selling on cost, 10% of works cost; profit, 20% on sales; and number of units produced, 10,000. Prepare a statement showing the total cost and profit.

[Ans: Prime cost: Rs. 2,20,000; Works cost: Rs. 2,78,000; Cost of production: Rs. 3,16,800; Cost of sales: Rs. 3,12,120; Profit: Rs. 62,880; Cost per unit: Rs.105.60]

3. The following particulars have been extracted from the books of a manufacturing company:

|

Rs. |

Stock of materials on 1 January 2009 |

94,000 |

Stock of materials on 31 December 2009 |

1,00,000 |

Materials purchased |

4,16,000 |

Office salaries (drawing) |

19,200 |

Counting house salaries |

28,000 |

Carriage inwards |

16,400 |

Carriage outwards |

10,200 |

Cash discount allowed |

6,800 |

Bad debts written off |

9,400 |

Repairs to plant and machinery |

21,200 |

Rent, rates etc.: |

|

Factory |

6,000 |

Office |

3,200 |

Travelling expenses |

6,200 |

Travelling commission |

16,800 |

Productive wages |

2,80,000 |

Depreciation: |

|

Plant and machinery |

14,200 |

Office furniture |

1,200 |

Director’s fees |

12,000 |

Gas and water charges: |

|

Factory |

3,000 |

Office |

600 |

General charges |

10,000 |

Manager’s salary |

24,000 |

Out of 48 hours in a week, the time devoted by the manager to the factory and office was on an average 40 hours and 8 hours respectively throughout the accounting year.

Prepare a statement giving the following information: (a) prime cost, (b) factory on cost as a percentage of production wages, (c) factory cost, (d) general on cost as a percentage of factory cost and (e) total cost.

[Ans: (a) Rs. 7,06,400; (b) 29.86%; (c) Rs. 7,90,000; (d) 12.86%; (e) Rs. 8,91,600]

4. Draw a statement of cost from the following particulars.

|

Rs. |

Opening stock: |

|

Materials |

1,00,000 |

Work-in-progress |

30,000 |

Finished goods |

2,500 |

Closing Stock: |

|

Materials |

90,000 |

Work-in-progress |

25,000 |

Finished goods |

7,500 |

Materials purchased |

2,50,000 |

Direct wages |

75,000 |

Manufacturing expenses |

50,000 |

Sales |

4,00,000 |

Selling and distribution expenses |

10,000 |

[Ans: Materials consumed: Rs. 2,60,000; Prime cost: Rs. 3,35,000; Works cost: Rs. 3,90,000; Cost of production of goods sold: Rs. 3,85,000; Cost of sales: Rs. 3,95,000; Profit: Rs. 5,000]

5. The following information has been obtained from the records of Harpreet Corporation for the period from 1 January to 31 January 2010:

|

1 January |

31 January |

Cost of raw materials |

15,000 |

12,500 |

Cost of work-in-progress |

6,000 |

7,500 |

Cost of stock of finished goods |

30,000 |

27,500 |

Transactions during the month: |

|

Rs. |

Purchase of raw materials |

|

2,25,000 |

Wages paid |

|

1,15,000 |

Factory overheads |

|

46,000 |

Administrative overheads |

|

15,000 |

Selling and distribution overheads |

|

10,000 |

Sales |

|

4,50,000 |

Prepare a cost sheet and the income statement showing the gross profit and net profit.

[Ans: Prime cost: Rs. 3,42,500; Works cost: Rs. 3,87,000; Cost of production: Rs. 4,02,000; Cost of sales: 4,14,500; Gross profit: Rs. 60,500; Net profit: Rs. 35,500]

6. From the following particulars, prepare a cost statement:

|

Rs. |

Stock (1 January 2009) |

|

Raw materials |

91,500 |

Finished goods |

61,200 |

Stock (31 December 2009) |

|

Raw materials |

1,45,500 |

Finished goods |

30,000 |

Purchase of raw materials |

75,000 |

Work-in-progress |

|

On 1 January 2009 |

24,000 |

On 31 December 2009 |

27,000 |

Sales |

2,85,000 |

Direct wages |

61,200 |

Factory expenses |

31,500 |

Office expenses |

16,200 |

Selling expenses |

11,400 |

Distribution expenses |

7,500 |

Also calculate the percentage of works expenses to direct wages and the percentage of office expenses to works cost.

[Ans: Prime cost: Rs. 82,200; Works cost: Rs. 1,10,700; Cost of production: Rs. 1,26,900; Cost of sales: 1,77,000; Profit: Rs. 1,08,000; Percentage of works expenses to direct wages: 51.47%; Percentage of office expenses to works cost: 14.63%]

7. From the following particulars of a manufacturing company, prepare a statement showing (a) cost of materials used; (b) prime cost; (c) works cost; (d) percentage of works overheads to productive wages; (e) cost of production; (f) percentage of general overheads to works cost; and (g) net profit.

|

Rs. |

Stock of materials on 01 March 2010 |

10,000 |

Purchase of materials in March |

2,75,000 |

Stock of finished goods on 1 March 2010 |

12,500 |

Productive wages |

1,25,000 |

Finished goods sold |

6,00,000 |

Works overheads |

37,500 |

Office and general overheads |

25,000 |

Stock of materials on 31 March 2010 |

35,000 |

Stock of finished goods on 31 March 2010 |

15,000 |

[Ans: (a) Rs. 25,000; (b) Rs. 3,75,000; (c) Rs. 4,12,500; (d) 30%; (e) Rs. 4,37,500; (f) 6.06% and (g) Rs. 1,65,000]

8. The following data are related to the manufacture of a standard product during the month of January 2010:

|

Rs. |

Raw materials |

4,00,000 |

Direct wages |

2,40,000 |

Machine hours worked |

8,000 hours |

Machine hour rate |

Rs. 20 |

Administration overheads |

10% of works cost |

Selling overheads |

Rs. 7.50 per unit |

Units produced |

4,000 |

Units sold |

3,600 @ Rs. 250 each |

You are required to prepare a cost sheet in respect of the above showing (a) cost per unit and (b) profit for the month.

[Ans: (a) Rs. 220; (b) Rs. 81,000; Value of closing stock of finished goods: Rs. 88,000]

9. The following particulars are obtained from the records of a factory:

|

Rs. |

Materials issued |

1,28,000 |

Wages paid |

1,12,000 |

Factory overheads |

60% of wages |

Materials returned to stores: |

1,600 |

Materials transferred to other jobs: |

800 |

10% of the production has been scrapped as bad and a further 20% has been brought up to the specification by increasing the factory overheads to 80% of wages. If the scrapped production fetches only Rs. 940, find the production cost per unit if the finished product of the total production (including the quantity scrapped) is 100 units.

[Ans: |

Prime cost: Rs. 2,37,600; Factory overheads: |

|

Rs. 71,680 (sale of scrap is adjusted here); |

|

Works cost: Rs. 3,08,340] |

10. A steel company has received an order for the supply of three different types of castings A, B and C, weighing 36, 90 and 54 tonnes respectively. 10% of raw materials used is wasted in manufacturing and sold as scrap for 25% of its cost. The cost of raw materials is Rs. 1,000 per tonne. The wages for the three types of casting amount to Rs. 24,000, Rs. 63,000 and Rs. 33,000 respectively. The costs of the moulds for the three types of castings are Rs. 2,400, Rs. 2,000 and Rs. 1,800 respectively. Factory overheads are to be charged at 30% of wages and selling, and distribution and administration overheads at 20% of works cost. It is desired to earn a profit of 25% on selling price. Ascertain the price to be charged of these different types of castings on the basis of the above information.

[Ans:

11. A re-roller company produced 400 tonnes of MS bars, spending Rs. 1,80,000 towards materials and Rs. 60,000 towards rolling charges. 10% of the output was found defective, which had to be sold at 10% less than the price of good ones. If the sales realization should give the company an overall profit of 12½% on cost, find the selling price per tonne of both the categories of bars. The scrap arisings fetched a realization of Rs. 3,000.

[Madras University]

[Ans: |

Selling price per good unit: Rs. 673.30 |

|

Selling price per defective unit: Rs. 605.97 |

|

Total cost less scrap: Rs. 2,37,000 |

|

Profit on cost: Rs. 29,625 |

|

Required sales: Rs. 2,66,625] |

12. The following inventories data relate to Bright Ltd.

|

Inventories |

|

|

Beginning |

Ending |

Finished goods |

55,000 |

47,500 |

Work-in-progress |

35,000 |

40,000 |

Raw materials |

45,000 |

47,500 |

Additional information |

|

Rs. |

Cost of goods available for sale |

|

3,42,000 |

Total goods processed during the period |

|

3,27,000 |

Factory overheads |

|

83,500 |

Direct materials used |

|

96,500 |

Requirements:

- Determine raw material purchases.

- Determine the direct labour cost incurred.

- Determine the cost of goods sold.

[B.Com (Hons). Modified]

[Ans: (1) Rs. 99,000; (2) Rs. 1,12,000; (3) 2,94,500]

13. On 30 June 2009, a flash flood damaged the warehouse and factory of ABC corporation, completely destroying the work-in-progress inventory. There was no damage to either the raw materials or finished goods inventories. A physical verification taken after the flood revealed the following valuations:

|

Rs. |

Raw materials |

1,24,000 |

Work-in-progress |

? |

Finished goods |

2,38,000 |

The inventory on 1 January 2009 consisted of the following:

|

Rs. |

Raw materials |

60,000 |

Work-in-progress |

2,00,000 |

Finished goods |

2,80,000 |

|

5,40,000 |

A review of the books and records disclosed that the gross profit margin historically approximated 25% of sales. The sales for the first six months were Rs. 6,80,000. Raw material purchases were Rs. 2,30,000. Direct labour costs for this period were Rs. 1,60,000 and manufacturing overhead has historically been 50% of direct labour.

Compute the cost of work-in-progress inventory lost on 30 June 2009 by preparing a statement of cost and profit.

[B.Com (Hons), Delhi. Modified]

[Ans: Closing work-in-progress (which was lost on 30 June 2009): Rs. 1,38,000; Profit: Rs. 1,70,000]

14. A factory’s normal capacity is 1,20,000 units per annum. The estimated costs of production are as follows: direct materials, Rs. 6 per unit; direct labour, Rs. 4 per unit (subject to a minimum of Rs. 24,000 p.m.); overheads (fixed), Rs. 3,20,000 p.a.; variable, Rs. 4 per unit; semi-variable, Rs. 1,20,000 p.a.; up to 50% capacity and an additional Rs. 40,000 for every 20% increase in capacity or part thereof.

In 2009 the factory worked at 50% capacity for the first three months, but it was expected that it would work @ 80% capacity for the remaining 9 months.

During the first three months, the selling price per unit was Rs. 24. What should be the price in the remaining 9 months to produce a total profit of Rs. 4,36,000?

[C.S. (Inter). Modified]

[Ans: Rs. 25 per unit]

15. An air-conditioning company produces and sells ‘Triple x’ model of air-conditioner for Rs. 20,000 during the year 2008. The direct material, the direct labour and overhead costs are 60%, 20% and 20% respectively of the cost of sales.

In the year 2009, the direct material cost has increased by 15% and direct labour cost by 17%. Due to these increase in costs, there would be a 50% decrease in the amount of profit if the same selling price is to be maintained.

Compute the new selling price to enable the company to maintain the same percentage of profit as that earned during the year 2008.

[B.Com (Hons), Delhi. Modified]

[Ans: New selling price: Rs. 22,500]

16. Mr. Diraj has a small furniture factory. He specializes in the manufacture of small computer tables which he can make 15,000 a year. The cost per table worked out as follows for the year 2008–09, when he made and sold 10,000 tables.

|

Rs. |

Materials |

300 |

Labour |

100 |

Overheads (fixed) recovered @ 50% of material cost |

150 |

|

550 |

Price is fixed by adding a standard margin of 10% to the total cost arrived as above.

In 2009–2010, due to recession, there is a fall in the cost of materials, total cost being worked out as follows:

|

Rs. |

Materials |

200 |

Labour |

100 |

Overhead (fixed) recovered @ 50% of material cost |

100 |

|

400 |

Mr. Diraj maintained his standard margin of 10% on the cost of sales. Sales were at the same level as in 2008–09.You are asked to

- Determine profit or loss for the year 2009–2010

- Compute the price which should have been charged in 2009–2010 to yield the same profit or loss as in 2008–2009.

[I.C.W.A. Modified]

[Ans: (1) Profit for 2009–2010: Rs. 5,50,000 (2) Selling price: Rs. 505 per table]

17. A company makes two different types of pen drives XZ and YZ. The total expenses during the period as shown by the books – 600 of XZ and 800 of YZ – are as follows:

|

Rs. |

Material |

99,000 |

Direct wages |

6,000 |

Stoves overheads |

9,900 |

Running expenses of machine |

2,200 |

Depreciation |

1,100 |

Labour amenities |

750 |

Works general |

15,000 |

Administration and selling |

13,400 |

XZ : YZ |

|

Materials cost ratio per unit |

1 : 2 |

Direct labour ratio per unit |

2 : 3 |

Machine utilization ratio per unit |

1 : 2 |

Calculate the cost of each pen drive per unit giving reasons for the basis of apportionment by you.

[I.C.W.A. (Inter). Modified]

[Ans: Cost per unit: XZ, Rs. 277.60 YZ, Rs. 528.56 ]

18. Delta Engineering Ltd produces a uniform type of product and has a manufacturing capacity of 3,000 units per week of 48 hours. From the cost records of the company, the following data are available relating to output and cost of three consecutive weeks.

Assuming that the company charges a profit of 20% on the selling price, find out the selling price per unit when the weekly output is 2,000 units

[I.C.W.A. (Inter)]

[Ans: Rs. 35 per unit]

19. A Limited company has capacity to produce 1,00,000 units of a product every month. Its works cost at varying levels of production is as under:

Its fixed administration expenses amount to Rs. 1,50,000 and fixed marketing expenses amount to Rs. 2,50,000 per month. The variable distribution cost amounts to Rs. 30 per unit. It can market 100% of its output at Rs. 500 per unit provided it incurs the following further expenditure:

- It gives gift items costing Rs. 30 per unit of sale.

- It has lucky draws every month giving the first prize of Rs. 50,000, second prize of Rs. 25,000, third prize of Rs. 10,000 and three consolation prizes of Rs. 5000 each to customers buying the product.

- It spends Rs. 1,00,000 on refreshments served every month to its customers.

- It sponsors a television programme every week at a cost of Rs. 20,00,000 per month.

It can market 30% of its output at Rs. 550 per unit without incurring any of the expenses referred to in (1) to (4) above.

Advise the company on its course of action. Show the supporting cost sheets.

[C.A. (Inter)]

[Ans: The profit will increase by Rs. 81 lakhs if the company produces 1,00,000 units and incurs the special costs for the marketing of its 100% output. Hence the company is advised to produce 1,00,000 units and incur the special costs for the marketing of its 100% output.]

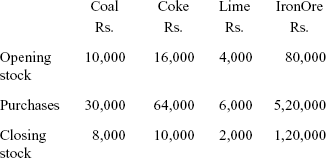

20. The Iron and Steel Company Ltd provides you the following information and requests you to prepare:

- Statement showing material consumed

- Pig iron production account.

Pig iron produced during the year: |

2,000 tonnes |

Works expenses for the year: |

Rs. 10,000 |

Wages for the year: |

Rs. 4,80,000 |

Scrap realized from iron one bits: |

Rs. 20,000 |

Details of materials for the year: |

|

[Ans: |

(a) Coal: Rs. 32,000 |

|

Coke: Rs. 70,000 |

|

Lime: Rs. 4,000 |

|

Iron ore: Rs. 4,60,000 |

|

(b) Prime cost: Rs. 10,50,000 |

|

Works cost: Rs. 11,50,000 |

|

Cost per tonne: Rs. 575] |