CHAPTER I

Getting Off to a Strong Start

Staging Your Business for Financial Success

It’s not black magic, though sometimes a little magic might help!

IT’S SAFE TO SAY that the great majority of entrepreneurs who start their first business are pretty ignorant about finance. That’s nothing to be ashamed of; we live in times when our education and preparation for the work world are pretty tightly focused. You’re no doubt pretty passionate and proficient in the area on which your business operates. And that matters, a lot.

So if you didn’t have a finance and accounting background, it’s going to be one of your challenges to get educated about the aspects of finance that affect your business (and your industry sector). But the good news is that, for many entrepreneurs, even non-number people, their own numbers become really fascinating. Your business’s finances are part of the score card by which you and others measure your success.

There’s another piece of good news here too. There is a wealth of targeted information out there to help you grasp and manage your business’s finances. As you will soon read, there are professional accountants, bookkeepers, business support groups, government agencies, web sites, social media tribes, associations, clubs and more that you can tap for expertise and advice, not to mention money. Your banker, customers, colleagues, competitors and of course family and friends may be unexpected sources of wisdom. We don’t pretend this book will give you all you need to succeed, but we do believe it will map the world of business finance for you so you will know how to ask good questions and start figuring things out, including what you can do and what you’d best let specialists do for you.

In fact, we are here to help you in the next phase too, after you finish reading this book. If you’d like to drop us a line with a specific question (in English) related to the finance of your established or yet-to-be-launched business, we’ll get back to you with a reply. Having started 17 businesses ourselves, to date, with more in our heads, we have quite a bit of pragmatic knowledge and plenty of experience, both good and bad, to make us confident we can either help directly or point you in the best possible direction. You’ll find our email addresses in the About the Authors section at the end of this book.

We can imagine that you might find the info and advice herein a bit overwhelming if you are just starting out. But trust us, you can build a business step-by-step. And no matter how big or small that business may be, you can bet your successes will flow in part from the care you give to your business’s financial health. So let’s get started.

True Costs and Key Financial Drivers

Knowing the true costs of your products or services is the only way to go.

ONE OF THE MOST IMPORTANT fundamentals to know about your business is the true cost of providing your products or services. It may seem like a basic point, but too many business owners have only a partial grasp of all the costs associated with delivering their products or services. The fully loaded cost to provide your product or service includes much more than just the direct cost of the materials and the labor to produce the offering.

When identifying the costs associated with preparing a product or service for sale, you need to include the proportional expense for every segment of the business that contributes to the creation of the product. This includes sales, marketing, facility overhead, management overhead, and all other expenses associated with operating the business. These are indirect expenses. They don’t go up or down in association with an item’s sale, compared to the direct costs that do.

It’s worth pausing here for a reality check. It’s possible you have been building your dream company with cocktail napkin calculations that look really good. If they don’t include the items you have to pay for whether or not you sell a single thing, you could go broke sooner or later. It can be scary to confront fully loaded costs, but it’s a lot more than scary to go bankrupt, so build your budgets and business plan taking their impact into account.

Allocating indirect costs

The challenge may be in identifying the appropriate portion of indirect expenses associated with a given product or service. The best approach may be to determine the current or potential portion of total sales that it represents in your entire offering. If your intent is to price all items with a similar profit margin, it would be appropriate to assign indirect expenses based on the percentage of total sales revenue an item contributes. So if the product or service you are pricing is expected to provide 20 percent of the sales volume, you would allocate 20 percent of the indirect expenses of your company.

Now compute the indirect expense associated with each individual item in your offering, based on your proportional allocations above. Add your direct material and labor costs to each allocated expense, and you’ll have the fully loaded cost of each of your products or services. Once you have made this calculation of fully loaded cost, you will have a proper basis for understanding the profitability of each product or service you bring to market. It is only after you have a clear understanding of your fully loaded costs will you be able to identify the real profit potential of a product or service.

With a clear picture of all your fully loaded costs, you will be better able to monitor and adjust product development, target sales and marketing initiatives and stage your business to achieve consistent profitability. When a particular product or service falls short of your expectations, you will be able to adjust sales volume, product pricing, or product development with other products to fill the gap and maintain or exceed profit targets for your business. That way, an item that falls short of expected sales volume might be offset by increased sales volume of another better-performing one. Monitoring the performance of all items and knowing their actual impact to company profitability is essential for you to maintain the expected financial performance of your company.

This essential piece, your product performance information, is part of what helps you stage your business for financial success. The other pieces, which we call your key financial drivers, include those items that have the greatest impact to your emerging and long-term financial success. In each business this list may be different, but on it you will see the items that can make or break your best-laid plans. Don’t get distracted by smaller, less relevant numbers if they steal time and effort away from evaluating these key ones. Key financial drivers may include:

• Payroll

• Travel and entertainment

• Advertising

• Marketing

• Consulting (including your legal and financial advice)

• Cost of goods, freight

• Rent and utilities

• Finance charges, bank fees, etc.

Monitoring these numbers on a daily, weekly and monthly basis is key to being able to identify problems and opportunities and make changes that will allow you to optimize your business’s financial success at all times. Identifying fully loaded costs combined with a disciplined method of tracking and responding to your key financial drivers will stage your business for optimum financial success.

Building a Foolproof Budget

In the beginning, keep it simple! The real value of a business budget is being able to see where your money comes in and goes out.

BUSINESS BUDGETS are not always fun to build. Until a budget has saved you and your business from disaster, there’s a good chance you won’t fully appreciate one for what it is. For a very small business, a business budget might not seem necessary. You might think, “No worries, I just won’t spend more than I make.” Sounds like a good plan, at first. However, take it from me, as easy as it seems to manage a small business’s finances without a budget, it is just as easy to find yourself looking at your business’s bank account halfway through the year, asking yourself, “Where did all my money go?” You could even say that a small business needs a budget even more than a larger one, as it’s so vulnerable to the slightest surprise.

Too often, a little more spent here plus a little more spent there can drop a ton of bricks out of the sky and kill a small business. Or it can cause you to have to pay out-of-pocket to get that last shipment in (or out), that last end-of-the-month bill cleared, or that last employee paid. Bottom line: running out of money before you plan to (which should be never) is the last thing you want to deal with.

Even if you’re not faced with the dire situation of running completely out of money, to have less than you planned on is not good either. Remember it this way: Business is a competition. You are always competing with whoever controls other parts of whatever market you’re in. A budget will help ensure you can get one more shipment out, run one more commercial or radio ad, cover payroll, get that company vehicle serviced, or even reward an exceptional employee with an unexpected bonus.

A business budget will help you streamline, stretch, and manage money effectively, and ensure you never run out unexpectedly. So even the smallest, newest business needs a budget, definitely before it starts up. Think about it: Do you really enjoy being clueless about how much money you have or where it’s going?

What is a business budget?

Budgets are not black magic. A business budget is a tool that lets you track and maintain accountability of revenues (or receivables, the money you brought in), costs (payables, or money you spent), and profits (money you have left over after you paid all your bills, including salaries). A budget first of all shows you if your business is able to fund itself. If your trial budget comes out negative, that’s a bummer, but it’s a lot better than discovering that fact at the end of the year. It tells you you’ll need to cut expenses or increase sales, or to tap other funding. So you can be pro-active without fearing that bad news will fall out of the sky.

Once you’ve set up a workable budget, you can monitor reality vs. your estimates. This allows you to watch your money on paper, and ensure you’re not spending more than you’re making. A budget can be managed by an accountant, but if you’re just starting out, there’s a good chance you can manage it yourself. There exist several great software tools that make the process even easier. (See pages 26 and 55).

Sales, costs and profit

The most basic budgets include sales and other revenues. This section will help you keep track of how much money you’re making, and begin to build a history so you will be better able to predict sales trends in the future. Sales forecasts will come in handy if you’re looking to expand your business, and will likely be required by your funder if you’re going to try to take out a business loan or interest someone in investing in your company. The history you accumulate can also point to new opportunities, highlight cyclical highs and lows, and identify trends that can help or harm your success.

Of course, costs are also vital to track in order to ensure they don’t get out of control and pull you into debt, or worse. In the same way your sales forecasts vs. actual sales reveals vital information, comparing your expense forecast with actual costs helps you refine your knowledge of your business’s health. When you can see how much it actually costs to run your business, you can look more intelligently for ways to lower those costs to raise your overall profit!

That final part, profit, is everyone’s favorite. Watching this part of your budget increase is like watching your bank account grow on payday, but it’s much more rewarding. Profits are the fruits of your labor; you created this money! You can do whatever you please with this money: It’s all yours! It might take you a while to actually get anything in this column of your budget, but when you do… Oh Boy! Mike, Marc and I still have the first dollar we ever made as business partners. It represents so much more than just a dollar. It represents something that we created together, and tells us that we are smarter and more capable as businessmen than somebody. Take my word for it, the first time you actually turn a profit as a business owner is like watching a child be born. But don’t expect it to happen overnight.

To put things in perspective, most businesses don’t turn a profit for up to three to five years. Don’t let that scare you: The smaller and simpler your business, the quicker your profits will come. This is why, in our book Starting a Business, we suggest you start as small as possible and build from there. The risks and stress are lower, and you can actually have more fun with it.

In our business, we manage two budgets: monthly and annual. We review them monthly. The monthly budget is much more detailed and includes all of our expenses and every bit of income we receive. The annual budget, naturally more forward-looking and projective, helps us see on paper what we can and can’t do with our money this year. For example, on our monthly budget, we ensure that we can pay our employees using the money we made this month. For the annual budget, we ensure that we don’t hire more new employees than it suggests we will be able to afford at the end of the year. I use our employees as an example because they are the lifeblood of our business and our very top priority. Paid employees are happy employees and happy employees are what keep our business rockin’ and rollin’. So it works out for everyone.

Why is a business budget important?

The great thing about a budget is that it keeps you honest and prevents many unpleasant surprises. It puts you in charge, and saves you from ignorantly responding to circumstances. You can really see what is happening in your business.

When I was a kid, I used to go to the county fair with my parents. My dad would give me some money to spend however I wanted. I could buy candy, ride rides, go to the petting zoo, play games, or do whatever else I wanted. After I spent that money, though, my willy-nilly fun was over, and I had to do whatever my parents wanted to do. So the first year, I spent all my money on the goldfish game, trying over and over and over to win that stupid goldfish (that no one ever wins). I wasn’t able to play any other games, go into the petting zoo, ride any rides, or do any of the other fun things I wanted to do. Eventually, I after I cried for ten minutes, my mom slipped me a little more money and I was able to ride some rides. After that year I got smarter with my “budget” and had a lot more fun.

The same is true for you (and I hope that includes a good fairy who re-lines your pocket if you make the same mistake I made). When you’re starting a business, you can’t spend all your money on the greatest, most popular company cell phone or vehicle out there, because your business’s money is extremely valuable, especially in the beginning. In business, when you’re out of money, you’re out of money and the game is over. A business budget is the best way to ensure you don’t spend yourself into debt, and it helps you stretch your money to the max.

A final thought. Just because you build a monthly and annual budget doesn’t mean you have to stick to it; it just means you can see it. While we don’t often adjust our business’s monthly budget (simply because a month in business goes by in the blink of an eye), we do often adjust our business’s annual budget to accommodate new opportunities that present themselves throughout the year. Just because you create a budget doesn’t mean you can’t buy more cost-effective materials, hire employees at a lower salary if the market changes, or allocate more money to advertising if you get a great deal. Bottom line: Let your budget be your guide. Stay flexible, but within your business’s means.

S.G.

Payment Term Basics

Don’t let your customers treat you like an interest-free lender. Get paid, not played.

GETTING PAID can be tricky if you don’t have the right payment terms in place, especially if you’re new to business and your customer isn’t. If you want to keep your business running smoothly, you should have vigorous payment controls to manage your cash flow and make money management a high priority. In order to avoid potentially lethal debts, from Day 1 put measures in place to help you keep track of, and collect, any money your business is owed.

Bank basics

First, you should open a bank account under your business’s legal name. This is will give customers a means of paying you if they opt for direct deposit payment, and also keep your business’s money away from your personal money. Opening an account will also make your work easy when it comes to making payments and filing taxes. And it will help you avoid transactions using liquid cash (paper money).

Ensure you open an account with a reputable bank that has nationwide or even international access, depending on your needs. Avoid new and up-and-coming banks that you don’t recognize or banks that are run out of the back room of a tattoo parlor or a van down by the river. Activate your account by depositing some money into it. Also, as part of the account opening process, attach some credit to your account—just take care it’s not more than you can reasonably afford to make payments on. A line of credit will come in handy when you need to make purchases or expand your business and you haven’t yet collected everything in your accounts receivables (money customers owe you). Bear in mind that a typical overdraft protection line of credit may have a higher interest rate on the funds you use, compared to the rate on a straight loan, so try not to use that money for long periods of time.

Bookkeeping

You absolutely need to familiarize yourself with basic bookkeeping. That may sound scary, but it’s essentially keeping track of where your money is: where it’s coming from (or should be coming from), and where it’s going. If you need schooling, look into evening classes, start-up support workshops, and read up on areas where you’re weak. You need to have the most basic money management principles clear in your mind, even if you aren’t doing the bookkeeping yourself. And you must understand credit, taxes, and bank statements to run your business intelligently.

Advanced bookkeeping is a challenge that many new entrepreneurs face. If you don’t have master bookkeeping skills, retain or hire a professional accountant to help you maintain your business accounts. You can also invest in software that will help you track your business’s cash flow. Software like QuickBooks will make the tracking of your finances easy and will allow you to create invoices, keep account information, handle payroll, and track your bank accounts. Some entrepreneurs install QuickBooks on their personal computers just to keep track of these key elements, in parallel but apart from what the accountant is doing, so they can come up with instant reports and snapshots of their business any time, day or night. Others set up access to the accountant’s system so they can see actual data in real time.

As we’ve noted elsewhere in this book, if you use software like QuickBooks and you’re not a trained accountant, get professional advice on how to set it up to accurately track your business.

References and quotes

Especially if your business is new, you may feel like anybody who orders from you is a welcome gift from above. But if your product or service is a high-ticket item or it requires a lot of investment before you deliver and invoice, it’s entirely appropriate to ask a prospective customer for bank references. You probably have already filled out credit applications yourself, so consider them if you feel you need added protection against slow payers.

If your business is such that you prepare quotes for your customers, be sure to include the payment terms as part of them. If appropriate, also include such things as kill fees (when the customer stops a project before completion), late fees and partial payment schedules. Once you and your customer have agreed on all the details, ask the customer to sign and fax (or scan and email) you the quote sheet so you have a binding agreement. If you make a policy of not starting work on an order until you have the signed quote back, you won’t risk a loss if the customer changes her mind and cancels the order. By requiring a signed quote (or purchase order) before you start work, you may gain a little leverage in the price negotiation, if the customer needs your product or service by a certain date.

Payment options and terms

For your company’s survival and growth, you also need to be smart about the payment options you get from your own vendors and about terms you offer your own customers. Find out what the industry standard is, e.g., how everybody else in your industry is handling their payment terms. Obviously, the terms you negotiate with your vendors should be as favorable to you as possible.

On the income side, there are a number of payment modes you can allow your customers to use, such as cash, debit and credit cards, certified checks (we recommend staying away from personal checks), PayPal, and direct funds transfer. After you’ve done your homework on all this, sit down and come up with payment terms and debt collection regulations you will apply when you sell your product or service.

State and maintain strict rules regarding late payments from your customers, in line with your business sector. Put your terms on the back of every invoice and reference it on the front. Make sure to state clearly that the goods sold remain your property until the invoice is paid. Without this, in the case of a customer going bankrupt, you will have a hard time retrieving your goods from the customer’s inventory and later on, you may only receive a fraction of their value—paid out over a period of years! Your invoices should also include the date payment is due, the amount, the modes of payment you offer, and your late payment fee schedule. With written terms, you will have something legally binding in case your customers don’t pay on time or refuse to pay a late-payment fee.

Late payment fees

And don’t be afraid to charge a late-payment fee; in fact, if you apply it absolutely rigorously, you’ll save a lot of headaches. Also, don’t let any of your customers give you a guilt trip about this fee. They knew the terms when they went into business with you. It’s not personal; it’s business. If you don’t state any late-payment penalties, you may find that some customers will feel free to hold onto your money for a long period of time. You know what they’re doing? Using you like a bank without paying you banking interest. And why wouldn’t they? Again, it’s not personal; it’s just business! A late payment fee is like an interest rate that discourages customers from using your money too long, so go ahead state one—everybody else does.

Of course, there may be situations where you have a customer who’s “too big to fail.” They are either such big players that they call the shots, or they represent such a huge proportion of your business (something to avoid, generally) that they know they can disregard your late fee schedule. In these cases it’s best to work closely with your accounts payable contact, or the top management, to try to put your case for prompt payment, or work out creative payment terms for an isolated situation. In the end, we feel it’s best to have a late payment fee as a standard operating procedure. You can always vary or waive its terms as the situation dictates.

How do I stay on the offensive?

As we know, the timing of payments you receive for the products and services you offer will strongly influence the growth of your company as you build and grow it. If you don’t get paid, you can’t grow and, if that situation persists, you can go bankrupt. Even on a month-to-month basis, if you collect from your customers before you must pay your vendors, you can opt to use your line of credit for expansion or advertising, rather than for paying vendors. Or… maybe you can opt not to use credit at all, and save all that interest.

In addition to stipulating your late payment terms clearly on your invoices, you should also state the rules that apply in case of accumulated debts. With some customers you may have to establish a credit limit and not deliver goods or services they order when their open invoices exceed that limit.

Collections

When you have strict rules of payment, you naturally will prevent at least some late payments from occurring. Be quick to send late-paying customers a request for payment as soon as the payment is overdue. Automate this task via email if necessary (QuickBooks and similar programs can do this for you). This way, your customers will know that you are serious about collecting on time and will be less likely to fail to pay next time. The reward is critical: If you ensure that all your outstanding invoices are cleared, you have money to run your business. If you become lenient, customers can take advantage of you to pull your business down.

Sadly, there will always be those customers who tell you that they will pay in the future, but frankly, never do. The famous line from these customers is “the check is in the mail.” Decide early how you are going to handle this and stick to your own terms.

Factoring and insuring invoices

Depending on the size of your business and the amount you invoice monthly, you might want to consider factoring to capture cash quickly. Factoring companies effectively buy your accounts receivable for approved customers (your customers whose records show them to be reliable payers) at a discount, paying you perhaps 70 percent to 80 percent of the invoice’s value, less a service charge, in a matter of days. While you lose a big chunk to the factor, it may be better in cash crunch times than applying, waiting for approval, and finally receiving money from a bank in a straight loan. In factoring, the customer, not your company, is evaluated for credit worthiness. (They will want to know you’ve been in business for two years or more, and may have certain minimum monthly billing requirements, however.) If you think factoring might work for your short-term cash needs, educate yourself fully on it and get input from your accounting person before you sign up, and keep your use of factoring to a minimum.

There is also credit insurance. Again, for a fee, a credit insurance company will take over your invoice and pay an agreed portion of it to you, on time. They then attempt to collect from your customer themselves. Since their interest is to protect you, they try to research your customers and report any concerning information they discover to you. Some small businesses favor this service, as the reliability of cash flow can be important in your vulnerable early days. But do your math carefully before signing up, as the fees chew up your profits.

You can also insure your invoices specifically against the bankruptcy of your customers. As you know, if a customer declares bankruptcy, you may never receive payments due you, or get only 10 percent of the open invoice amounts in typical cases. To protect your company’s exposure you can purchase insurance that covers around 75 percent to 80 percent of the invoice value, less a percent or two in service fees. In the event that customer goes belly up, the insurer will compensate you as agreed. You do not need to insure every customer, but it’s worth considering if you are aware a given customer with a large open receivable (one who owes you a lot of money) is in financial trouble. Again, be careful, in your analysis, to see what the actual payment to you would be, vs. your profit margins. Low-margin businesses might erase all profit via the discounts off the invoice value mentioned above. But for many businesses, receiving a good share of an invoice’s value vs. practically nothing in a bankruptcy is at least some help.

Once you have all your payment terms and policies, collections, and other financial protections in place, you can breathe (and rest) a little easier. And hopefully, watch the money that’s due you come rolling in.

Preventing Cash Flow Worries and Woes

Being organized and disciplined are your humble miracle cures. Here are some tips to help keep your business in the black at all times.

AT ONE POINT or another, every business will run into cash flow problems. It’s just the nature of business that you can’t always predict the future, so accept that and move forward. New businesses are more vulnerable than established ones to both internal and external threats, but by far, the most common ones for them are cash flow problems. It pays off to run your business in ways that minimize the chances of negative cash flow so you only have to deal with the rest of the threats!

Cash flow basics

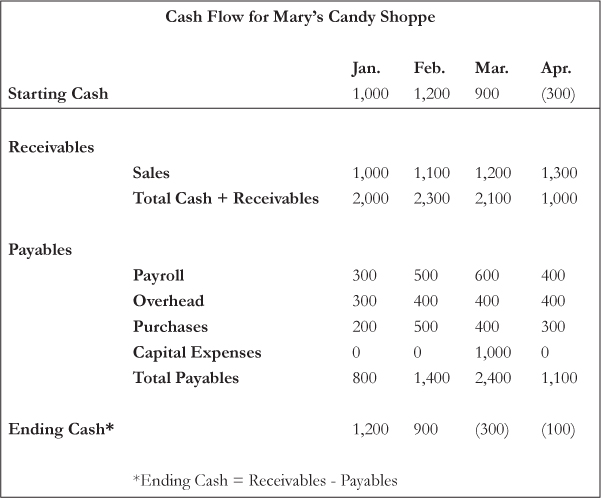

You’ll find mountains of information and advice about cash flow in books, articles and blogs, so we will take the high-altitude view here to get you started. Just as with your household finances, you have income (receivables) and expenses (payables) in your business. While there are some technical uses of the phrase cash flow, for us it means the state of the balance between your income and expenses at any given moment. It’s a snapshot, so it might describe today’s balance, or next month’s or next year’s balance.

Positive cash flow means you have more cash and solidly reliable income—at that moment—than bills that need to be paid at that moment as well. Negative cash flow means you have more expenses to cover than the cash at your disposal.

To create your snapshot, whether of today’s cash flow landscape or at some point in the future, you can use accounting software or even a cocktail napkin, calculator and pen. Let’s say you need it for today, first of all. But you’ll quickly see that this exercise will also start to map your future cash flow landscape as well.

Essentially the process goes like this:

• List all the cash assets your company has on hand today. Credit lines and promises to pay don’t count; just list the cash you can use without going into debt.

• Now list all the payments you must make today: payroll, vendor invoices, taxes, rent, debt interest payments, and so forth. As you make this list you’ll run into all the other bills you’ll be facing in the coming months, so if you want to be efficient, chart them as well, in calendar fashion by date payable. This will start your future-focused cash flow report. The same is true for your receivables—you can chart them now too.

• Tally up today’s bills and subtract that sum from your current cash total. If the result is positive, that number will go to the top of the next cash flow report, to which you’ll add any payments received in the meantime, and that will become part of your cash assets for the next period. If your result is negative, it’s time to get creative.

• Let’s say you’re negative but you have a credit line. You can dip into that, knowing (or hoping) some payments will come in to let you repay that loan quickly so you don’t have a big interest bill to add to the rest of your obligations. Otherwise, you’ll have to decide if any bills can be paid a little late (not recommended, but especially if you notify your debtor that you’ll pay on X date and then do so, it might be okay) or if you need to raise more cash from all the other sources we’ve discussed in other sections.

• Take a look at your receivables due to come in in the future, and judge their certainty of being paid on time. Some payments are like gold: You know your government grant money will come in like clockwork, on the third day of every financial quarter. Others may be highly risky, either by being likely to come in late, or to be only partially paid, or to be heading toward bad debt (a huge reason to keep in touch with your customers!). Say that your current snapshot is negative, but that in the next two weeks you know that your grant money is due to come in, and it will cover today’s shortfall. Taking a deep breath, you could conclude that you’ll be okay for the next two weeks. Then you’ll start the next report period with a zero balance, plus invoices you’ve made in the meantime. And this goes on and on into the future.

Scary but helpful

It’s important to realize that while this process can be scary, it’s far better for your business’s success and survival that you know what today’s and the future’s snapshots look like. As you get experienced with cash flow forecasting, you will find that even a bad situation today might be over, or improved, in a short while.

Making your forecast also dramatically highlights what some of your most urgent priorities ought to be. If you are worried about a customer’s ability to pay a big bill, it’s time to take up contact and learn about her own current and future business outlooks. If necessary, you can discuss a change in payment terms to ease pressure on her cash flow but still get some cash in for your own business’s needs—if your business can support that. Or if her outlook is grim, you may have to speak next with your banker about some form of interim financing to get you through the coming rough time.

It’s not always bad news time when you update your cash flow forecast, however. You may be able to see that in the next six months (if things go as foreseen, of course) you will have paid down your start-up loan. It might be time now to look further ahead and see what that means for your business: time to get a new loan to replace that antique equipment you started with? Time to hire a person to really focus on sales in a new channel? And so forth.

And speaking of bankers, you can understand why they expect you to know how your cash flow is looking. They judge how solid your forecasting skills are, based on your track record. It doesn’t help your credibility if you say vaguely that you think you can repay your loan on time if X, Y and Z all happen with 100 percent certainty—and those things never have happened as hoped before!

If any of this is new to you, it is probably dawning on you that the whole process of cash flow forecasting relies on your having tight control of the data related to your receivables and payables. If you can’t locate a bill or a bank statement, or you can’t tell if your invoicing is up to date, we’re sorry, but you’re really in a mess. We’ll have more to say about this in a moment.

Some internal causes of cash flow problems

As an entrepreneur (unless your business is in the financial sector), you can’t be expected to be a specialist in your company’s main business focus as well as a top-notch accountant. Sure, you need to grasp all the basics of business finance that apply to you, and be able to talk with bankers, investors, accountants, customers and others with a reasonable degree of intelligence. But as we’ve said, it’s important to know what you don’t know, and to seek solid professional support for your internal accounting purposes.

Right from the get-go you should get bookkeeping software and hire someone with accounting experience to keep track of your books. This person doesn’t have to be a fancy financier—just someone with a head for numbers and details and good organizational skills. If you’d rather play it safe, however, hiring an outside bookkeeping service is also an option. Have your bookkeeping person either set up or show you how to set up your internal data systems for accounting purposes. Then it becomes your job to ensure that whoever does your accounting is meticulous in record keeping and reporting. Without accurate, easily accessible data, you are sunk.

You can also run into major cash flow problems due to poor internal communications. It is possible that expenses outweigh income, but the books won’t reflect the imbalance due to sloppy reporting, internal politics, poor performance by key players, mistakes and the like. This problem can paralyze a company, so keep your radar open for any signs of systematic or human problems that need your intervention.

Believe it or not, delayed or disorganized invoicing is another major source of cash flow problems that many businesses face. You would think that with all the precariousness of a start-up business, getting correct invoices out as soon as possible would be a top priority for everybody. Yet there are times when the work is done, or products are shipped, but it isn’t invoiced yet. Every day an invoice is delayed in being sent to your customer risks a later payment than you are due. It will pay off if you periodically sit down with key players in your customer delivery chain to smoke out problems in product or service delivery, invoicing, collecting and so on. It will maintain people’s focus on getting those invoices out and provide opportunities to improve processes based on the workers’ insights into snags and weaknesses.

And the problem extends to collecting past due invoices as well. If you can believe it, some businesspeople say that they are too busy to chase down outstanding invoices. Use your accounting software to generate daily or weekly ageing reports and ensure that all past due accounts receive reminders.

Slow or low-volume sales can also lead to cash flow problems. Obviously, for a company to make large profits, the sales should be made quickly and in huge numbers. In a case where the company is experiencing slow sales, the amount of income will also tend to be low—makes sense. It may be time to review your marketing strategy and sales practices to boost both dimensions of sales in the future.

External causes of cash flow problems

Of course the state of your economy, the trends in your business sector, international or nature-related events and a host of other forces will impact your cash flow. Since you can’t affect most of these factors, the best you can do is try to keep up with news and commentary about them. Cash flow analysis can point to innovative ways you can manage the impact of external forces. For example, if energy costs are rising, would it make sense for you to invest in solar panels for the roof of your office or warehouse? You can chart the outlay to get the panels installed and see how soon energy savings will pay you back.

But not all external forces are huge in scope. You may have a well-oiled invoicing process, but slow-paying customers can still cause serious cash flow problems. Collections can be viewed as an internal matter, but actually making collections is essentially external. It doesn’t really matter where you locate it. The solution lies in maintaining frequent contact with slow-paying customers and exploring flexible terms as needed. If you have some cash reserves, that helps ease pressure on you, but the goal is to get every invoice paid on time.

If your cash flow forecasts are looking mostly negative, that obviously tells you that you need to adjust things so your receivables exceed payables. Review sales performance to see if there’s any way to increase income. Review expenses to see where you can cut them. Look at additional sources of credit, but don’t fool yourself and get too deep into debt if the picture doesn’t convince you that you can make a turnaround.

Don’t be afraid to ask for help, and update reguarly!

Understanding the Credit Industry

In the good old days, many transactions involving money were based on trust or faith. Now, they revolve around credit.

CREDIT GRANTING AND CREDIT USE use have evolved into an entire industry, involving and affecting countless participants from every industry and from every segment of the world’s economy. As an entrepreneur, you will certainly need credit, so it’s vital to understand how this key success factor works.

Today, credit in some form is required for the economic survival of nearly all consumers and businesses. It’s neither intrinsically good or bad—it’s how you use it to your advantage that matters.

Credit is simply a measurement of the risk that a creditor, such as a financial institution or a retail store, agrees to grant to its customer. When the risk factor is determined, credit then lets the credit user borrow funds or pay on some schedule of extended terms for a product or service. As a result, the importance credit plays in the economy is nearly immeasurable, and it has become an industry that circulates unimaginable sums of money every day.

The forces of change

The credit industry is directly affected by the local as well as the global environment. External factors such as unemployment rates, the strength of a government’s currency against other global economies, and import/export ratios all affect the internal factors of the industry. Some of these internal aspects help set the interest rates creditors can offer, the credit limits and amounts of money available to be lent, and even the requirements for extending the credit itself. One thing is certain: the absolute uncertainty of the economy from day to day, and more so from year to year. Forecasters such as economists, financial advisors, and even governmental organizations like the World Bank or the U.S. Federal Reserve Bank constantly strive for innovative ways to improve upon the accuracy of their predictions of the status of the economy. Unfortunately, an incalculable array of influencing factors makes 100 percent accuracy impossible. The supply and use of credit therefore remains in flux.

For the American consumer, for example, the determining factor of each individual’s credit worthiness hinges upon a crucial number. That number is her credit score. This critical number directly establishes the credit worthiness of a consumer, in nearly every instance. Credit scores are determined by the information contained in a consumer’s credit file, which in turn is published in a credit report. The higher the score, the better the terms and conditions creditors will be able to offer. Around the world, the reports themselves are usually generated by organizations known as Credit Reporting Agencies. Even in countries where these don’t (yet) exist, similar evaluations take place less formally. Creditors don’t like to lose money.

In the U.S., Equifax, TransUnion and Experian are the three main players responsible for compiling and storing the data that makes up a consumer credit report. Around the world, other players include Dun & Bradstreet, Experian, Cortera, Credit Information Bureau, Compuscan and CreditInfo. You can Google credit bureau, consumer reporting agency or credit reference agency for your country’s key players.

The data that these companies gather and process includes information received from creditors who supply the monthly results of their customers’ payment history. This sequence, through a proprietary scoring system, creates your credit score. In the U.S., nearly every consumer has a credit file and score stored in each of the three credit reporting agency databases. Currently, the average credit score in America stands at approximately 693, out of a possible perfect score of 850, according to Credit.com (http://www.credit.com/press/statistics/credit-report-and-score-statistics.html/).

Companies likewise can be rated according to their credit worthiness. Standard and Poor’s, Moody’s, Fitch Rating, DBRS and other multinational firms are joined by many country-specific firms in providing this information to lenders and investors. You can find your local players on the Internet.

The impact of an industry

The credit industry links numerous participants in a cyclical structure. The primary suppliers in this industry are the consumers themselves. They fuel the economy through their purchasing power. And when they can’t pay in cash, they turn to credit. The secondary supplier then performs its task, with lenders and creditors extending credit to the consumer, thus allowing consumers to purchase goods and services. Creditors charge a fee for their service in the form of interest, which covers profit plus the risk associated with operating on the basis of faith and trust. This process allows for the distribution of goods and services by the manufacturers, service suppliers and retailers. Producing and selling these goods and services creates the movement of the economy as a whole.

But the impact of credit can be seen in other settings as well. Your credit score can determine the interest rate you receive when financing a home, car, or education. It can also determine your credit worthiness as an entrepreneur when you need to finance a new business (or expand an existing one).

Few may realize their credit score can also become involved to the job interview process, the quotes you receive on various types of insurance, and even in a background check for security clearances, etc. In fact, it could be said that a credit score can be the most important number in a person’s life today. It follows you everywhere and forever.

With the credit industry spreading its sphere of influence like this, consumers and businesspeople are now facing the task of learning how credit works and what to do to positively affect their personal and business credit reports in order to take advantage of the system in place. Knowledge and education are the keys here. And although the credit industry was formed for an entirely different reason, it has now been officially tasked to help in educating people everywhere, due to the public outcry for information regarding the way credit reports and scores are devised and maintained. In 2003, the United States federal government mandated that all Americans receive a free credit report from each of three reporting agencies each year.

What this means for you as an entrepreneur

You may or may not be inclined to take an interest in credit practices, reports and the like. But both as a private person and an entrepreneur, you cannot afford to neglect your credit profile or to ignore the implications of credit-related decisions you make every day. At a minimum, start with these things (we’ll assume here that these apply equally to you privately and in business):

• Order credit reports from the entities that issue them in your location and study them.

• If you spot anything wrong or misleading, contact the issuer and discuss the actions open to you.

• If you find that in fact, you or your business have a poor rating, talk with the issuing agency, your bank, or other reliable sources about how to improve it. It may take a lot longer to improve your rating than it took to get into trouble. But you owe it to yourself or business to raise your score—because you’ll pay for the lower one in higher costs of borrowing until it does rise.

• If you live in a place that doesn’t have such credit rating agencies, use your trusted connections to find out how you or your company are viewed financially. If you hear concerns, get help in addressing them.

• Make a practice of running credit checks on yourself and your business as part of your annual planning cycle.

• Keep an eye on changes in credit conditions and laws that may bear on you. If you have complex credit needs, it may be smart to hire an independent advisor to monitor and report these to you periodically (especially if it’s not your true passion or you don’t have the time).

Change continues

One thing is certain: the credit industry will continue to change as the landscape of every economy across the globe and their dependency on alternatives to cash and bartering fluctuates. New and innovative lending and credit practices will continue to change the face of the credit industry and its impact on us all. That’s why you need to watch out for changes that could affect your ability to borrow money, open or expand businesses, negotiate interest rates, and so forth. Make it your goal to become a minimal credit risk to your financing partners and they will be glad to work with you to help fund the goods, services and capital you need to thrive in your personal and business life.

Your Credit Report and Scores

We’ve accomplished the first step in understanding how the credit industry has evolved and how it currently plays a major role in every economy around the world. What’s next?

DRILLING DOWN FURTHER in the credit landscape, let’s look now at how individual credit reports, and ultimately the corresponding credit scores, are examined by creditors and lending organizations around the world to determine an individual or company’s level of credit worthiness. Simply put, analysis of the score will ultimately determine if a person or business has the qualifications to receive favorable financing they seek to buy the goods or services they need.

Let’s start with the basics. A credit report is a record of your financial behavior and performance over time. It consists of categorized information about your credit-related activities and reveals how responsibly you have used particular credit resources, and subsequently, fulfilled your financial commitments. An individual or business develops a credit history that commences with individual creditors and broadens over time, until it is ultimately collected and evaluated by the credit reporting agencies around the world.

The credit reporting industry is a sophisticated network of lenders, creditors, merchants, and similar sources. They furnish creditors with credit data to on the consumers and businesses that are applying for and using credit. So a credit reporting agency’s main purpose is to supply risk management data to creditors. Equally, lending organizations, such as banks and financing companies, are required to manage risk. Credit reporting agencies also help those organizations do this by providing them with information they can use to assess a particular borrower.

Score big… and win!

After all of this information is compiled, most credit reporting agencies assign corresponding ratings or scores to the history-packed reports. Those scores are calculated using multiple factors. They can be the first thing a creditor views when making decisions on extending credit to the proposed borrower. So, the more you know about how your credit score is calculated, the easier it will be for you to sustain a good one. The key is remembering one thing: The higher your score, the lower the risk you pose to a creditor.

Credit score calculations usually follow roughly the same pattern in every credit reporting agency. These factors can include payment history, amount of debt owed, age of credit, the different mixes of credit, and even recent credit applications (or credit inquiries). In most cases (and certainly in the United States) each of these factors can be weighted. Make sure you are familiar with this process wherever you are seeking credit. For example, in the United States, an individual’s payment history and the amount owed to creditors make up 65 percent of her credit score. Here are a few tips that can help you maintain a high quality credit score.

• Pay your bills on time. Being late on a payment isn’t good for your score. Missing a payment can compound into even more problems. A good rule is to pay early… and pay the bill in full if possible.

• Keep those credit card balances low. It’s not a good idea to have any significant balances for any reason on credit cards. This is how financial responsibility is earned… or lost. The amount of debt you have in comparison to your credit limits is known as credit utilization. If you have a balance on a credit card (or on more than one), keep it low. The higher your credit utilization, the lower your score will be. Keep the utilization of all cards to 30 percent or less.

• Monitor and manage your overall debt. Even if you have a satisfactory payment history on your debt, too much of it can also hurt your score. Keeping a solid debt-to-credit ratio is crucial in maintaining a solid score.

• Keep old credit cards open: Believe it or not, even when you close a credit card it can hurt your credit score. If your credit card issuer stops sending monthly updates to the credit bureaus (even if the account has no balance), your score could be compromised. Your credit history with that creditor will also cease. Additionally, if the credit available is suddenly closed on that account, your overall debt-to-credit ratios will be negatively affected.

• Be careful of making too many credit inquiries: Every time you apply for new credit, your score stands to take a temporary small hit. Also, opening a new credit account can lower your score, because your average credit age is negatively affected. Seek new credit accounts sparingly to avoid a drop in score.

The good old days

The manner in which consumers apply for loans, both business or personal, has changed dramatically in the last several decades. Do you remember your parents or even grandparents ever telling you about how they used to do business with a bank or finance company? I do. The story seemed so simple, mostly because it was simple, back in those days.

When I was much younger (and well before I ever started my first business), my grandfather explained exactly how he did business with the local bank in his community. He described the ease with which he was able to walk into the bank, without an appointment, and to speak directly to the bank manager, who was the sole decision-maker for most financial transactions the bank made locally. His relationship with that bank manager was relaxed and slow paced. The bank manager, of course, lived in the same community.

Because he did all of his banking business there (his personal accounts, loans, etc. as well as business finance), the two of them were able to discuss the new, proposed loan or extension of credit with very little paperwork or red tape. The reason was simple: The bank manager had a personal history with my grandfather. They both knew each other’s character. The banker trusted Grandpa and my grandfather reciprocated. Incredibly, he told other stories about the bank manager actually stopping by his home on occasion to see how things were going. After all, they were both members of the local community.

In fact, a quick look at his previous business dealings with the bank, a short discussion, a review of his the current situation and personal news, and some additional paperwork was about all it took for the deal to go through. And although his transactions may have never been on a major scale, the process of completing the financial transactions were as stress-free as you can imagine. A single one-on-one, realistic discussion was all that was needed to figure out the credit situation and construct the new stage. That was how it used to be done. That was then.

Today, you’re just a number

We would all like to think we have connections. Inside links at the bank or any other financial institution are obviously beneficial. However, your biggest asset will always be what’s hidden in your credit scores. In today’s financial landscape, credit score management has become the most important single factor in getting credit for your small business or yourself. In fact, you could say that credit scores have almost become a form of currency, due to the way they are weighed by the creditors themselves.

Data can be transmitted around the world in seconds now. We can acquire loans and financing in distant cities or countries when the need arises. Our investigations for financing and credit may involve Internet searches and reports from any corner of the globe. We may never even meet the person giving us a loan or step foot into that lending institution for the transaction, either. Reports, scores and other supporting info can be amalgamated in an instant; and credit worthiness can be determined on a computer screen. This is how it’s done today.

So understanding your personal credit reports is where it all begins. Knowing what will affect your corresponding scores is just as vital. This gives you a major advantage in the credit-using world. Empower yourself through education and research and give yourself a huge dose of self-discipline until you can deliver the rock-solid credit reporting and scoring information that your creditors want to see. This way, you can use your understanding of the new landscape and take advantage of it. You can make yourself a perfect candidate for the best interest rates and get quick approvals for the loans, credit and financing you need for your business.

M.P.

Getting Your Financial House in Order

The title above seems simple and straightforward. However, these few words can have immeasurable significance in your life.

REGARDLESS OF WHETHER you are starting a new business, expanding your existing company, or just wanting more financial stability in your personal life, a quick review of how you are structuring and storing relevant financial documentation is a perfect place to start.

Knowing where your information is stored, how it is filed and in what format you keep it is basic prudence. Nevertheless, not all of us are that prudent. Getting—and staying—organized in general is not only a good idea in order to maximize success in your life, it is vital. The most important thing is to be set up so that if you or someone in your household or business needs to find some documentation, it can be located immediately.

Let’s get organized

First, let’s take a look at your private financial data management. Being able to get your hands on essential paperwork such as your mortgage contracts, deeds, insurance policies, vehicle information, health and medical records, credit and loan statements, and similar documentation is crucial. And it’s an ongoing battle, because we all have an incredible amount of data being thrown at us via countless communications each month.

Checking to see if there are changes to your accounts and their policies, validating charges, reconciling your monthly books, and even inspecting every document for inaccuracies is an absolute must, especially in this era of identity theft and Internet scams. Empowering yourself to be in-the-know about everything being reported about you and the records that will be archived for future use is imperative. For these reasons, we recommend that you have your credit report(s) and score(s) pulled once per quarter, to catch and correct possible factual errors.

But what should you do about your business documentation? The same scenario applies here too. In the following paragraphs, we’re going to go over a few basics to apply. Keep in mind that no matter whether your small business is already off the ground or if you are simply interested in getting organized for a future launch, having a structured portfolio of documents that may eventually be needed by a bank or lending institution is central to navigating the waters of financing and credit applications. Depending on the nature of your business type or the length of your current or proposed business history, here is a brief sampling of possible documentation (personal and/or business-related) that may be required to be organized, accurate and up to date.

• Bank statements

• Tax returns

• Legal filings, including contracts, permits, and so forth

• Business plans

• Marketing plans

• Strategic plans

• Profit and loss statements

• Budgets

• Expense sheets

• Lists of assets

• Lists of collateral

• Personal financials

• Letters of reference

• Accounting ledgers

• Insurance documents

• Credit card statements and account numbers

• Medical records and contact information as needed

• Property-related documents

• Up-to-date licensing agreements for future tax purposes, loan applications, and credit extensions from lenders and creditors

One step at a time

Even before your business is off the ground, it is absolutely necessary for you to develop a comprehensive system of organized record-keeping. This practice will enable your business to slowly transition out of that need to supply personal documentation until you can present company-based documentation to any entities requiring it. Of course, your system may not be perfect at first, but a really tight, logical system should be your goal, no matter how small and simple your business is. With time you may need professional accounting services, but at first you may be able to do it all yourself. (Ideally, if you can learn from such professionals how they would organize things before you set them up, you’ll be ahead of the game.)

So organizing your documents and records today will help you be prepared for any future needs for information. It will also be central in protecting your identity, providing security, and keeping you on track for accurate planning overall. Here are a few initial pointers on getting your financial house in order.

• Generate a master list of your necessary documents. Using the information already provided in this section (and in connection with the files and accounts you currently uphold) create a working roster of vital documents to organize and maintain. There is no better place to begin this overall process than making this essential master list.

• Maintain accurate and up-to-date records… always. It’s been mentioned a few times but bears repeating here. You must take charge of ensuring the accuracy on every document. One error on a crucial document could alter your entire loan application standing or even affect future interest rate changes on revolving accounts. Maintain a complete and chronological list of all statements. Make sure to file every statement (monthly or quarterly) too. Lenders will not allow gaps in record-keeping. Finally, be mindful of the expiration date(s) on credit cards, insurances and warranties. Know the renewal dates for everything and be proactive about renewing, if applicable.

• Develop security measures for your protection. Nearly every statement you receive from the companies handling your accounts contains personal and/or financial information that could expose you to fraud or even identity theft. Take measures to secure all documents in a safe place that provides access to only those needing that information (family members, business associates, etc.). Consider making a password-protected master list of passwords, user IDs, and similar sensitive information and do not print it out. Additionally, store duplicate copies of key documents (hard copies or digital ones) offsite to preserve them against fire, flood or other natural disasters. A safety deposit box at the bank branch in which you have accounts is always a good place for back-up copies. A rule of thumb is to back up as often as necessary so you can afford to lose what hasn’t been backed up yet—which means often!

• Preserve tax returns and records. Every country has different requirements here. You should be aware of how many years’ worth of records you need to store for future use. Tax authorities have a right to audit you without notice in most places. Be prepared with your documents and supporting evidence at all times. Some of these records may also be required by lenders for verification purposes regarding a loan you may be seeking for your small business. Keep a master copy of multiple years’ returns and then make a back-up for emergency purposes as well.

• Review, update and stay relevant. Organizing your financials is essential and keeping on top of it is equally so for both your personal and business financials. Once to twice a year, review your business, financial, marketing and strategic plans to make sure they are still relevant. If things have changed (personal situations, market conditions, economy, pricing, budgets, etc.), those items need to be reflected in your various plans. Lenders and funding organizations will need current and accurate information to be able to properly review and underwrite a loan proposal for you. This practice is also essential if you are seeking outside investors or business partners.

• Safely dispose of unnecessary documents. If old, out-of-date or irrelevant documents are no longer needed, take care to dispose of them properly. Shredding is a must for paper documents. If you find those document piles are getting big, there are professional document destruction companies that can assist you in disposing of your paperwork safely and securely. Similarly, you can buy software that can ensure computer files you don’t want to save are eliminated. Do not neglect this responsibility.

• Make this a habit. All the tips and practices above can seem daunting, but you need to take them just as seriously as you take on loan obligations or hire a new person for your business. Your credibility and credit worthiness rest on your command and protection of these essentials to your personal and business life.

Your house is now in order—now what?

Getting your financial house in order may seem like a small step in the overall process of successful starting and running a small business. But it gives you a solid foundation to grow on. And it will also create a huge stepping stone in developing and managing your relationships with future lenders. We’ll have more to say on this in later sections.

Finding and Working with the Right Accountant

The money you spend on getting sound financial services in some ways may be the best investment you’ll make when you start a business.

POOR BUSINESS ACCOUNTING or tax planning can easily derail development of a great business idea or concept. A qualified professional resource is key to optimizing the financial success of your business.

Not a do-it-yourself project

A common mistake entrepreneurs make when starting a business is to save money by setting up their accounting system themselves, using widely available accounting programs like QuickBooks without professional guidance. The basic bookkeeping and daily accounting functions may be easy to execute. It may even be relatively easy to set up the various charts of accounts. Someone with a good background in finance may be comfortable setting up such accounting programs, assigning cost centers and implementing day-to-day business accounting. The challenge is in setting up the most appropriate cost centers, organizing appropriate depreciation schedules, knowing what to treat as one-time expenses or amortized expenses, and other specifics related to tax planning or effective business accounting.

Leading tax accounting professionals we have worked with while reviewing various businesses we have considered buying or investing in have often found errors in the way businesses have set up their charts of accounts. They spot errors in accounting entries, and missed opportunities in tax planning. The first mistake is often related to setting up depreciation schedules (depreciation means taking down the value of something over a scheduled period of time, like three years, or spreading its cost over its expected lifetime). By setting up one depreciation schedule for tax reporting and another one for business accounting, you can optimize the benefits attributable to each. For example, for tax reporting purposes it may be helpful to use a more accelerated depreciation schedule to create more deductible offsets to income tax obligations. This would be a good strategy for a business where principles are interested in maximizing tax deductions earlier. Of course, if your tax planning requires few or no deductions early on, a long-term depreciation schedule could be implemented. The point is that it takes a specialist to grasp the larger implications of choices you make in your bookkeeping and tax preparations. It’s far better to have that specialist make a recommendation and back it up with explanations that to take a shot in the dark all by yourself—and miss.

One accountant or two?

Depreciation schedules are only one example of the need for professional guidance in your financial planning. Tax laws and requirements vary by location and often change more frequently than the average business owner can comfortably track. There are a number of elements a good tax accountant organizes and monitors to optimize the tax planning for a business.

Effective business accounting requires more than just tax planning, however. Business accounting practices need to balance with a solid tax planning strategy to achieve the best possible outcome for the financial success of your business. What many business owners mistake in the selection of their professional accounting resources are the difference in skills and capabilities needed for tax accountants and business accountants. Often a good business accountant is not as effective in tax planning and preparation. In many cases the good tax accountant is not as effective in daily business accounting processes. Finding and working with the right accountant starts with a very important question. Is there one professional resource available to provide the most effective tax and business accounting service, or do you need to look separately for a qualified tax professional and a qualified business accountant?

The selection process

The process of selecting the right accountant or accountants begins with preparing a list of candidates and developing an effective interview strategy.

Where can you find candidates? Start by asking other small business owners who they work with and find out what they think the plusses and minuses of their choices are. Your banker might be willing to recommend some accountants too. If you have worked with a personal tax planner before, you might already have a candidate for at least your business’s tax accounting. There are of course directories, professional associations, and small business development agencies that can broaden your list if you want.

There are four categories to consider when interviewing professional accounting resources for your business.

• Tax planning and preparation

• Business accounting practices

• Fundamental understanding of your business

• Clearly understandable pricing or fee schedule

Prepare number of questions that will help define the quality and fit of the professional resource you are interviewing. Here are some questions that will be effective for the interview process.

1. What are the most important elements related to proper tax planning for my business, short and medium term?

2. What is your process for identifying and setting up the proper chart of accounts for my business accounting?

3. Which accounting software do you recommend for my business?

4. What are the key items I should track daily or weekly in my business?

5. What is the best strategy for depreciation for both business accounting and tax planning?

6. Do you have any clients with a business similar to mine that I may speak with, as one of your references?

7. Do you have a professional fee schedule or hourly rate in writing for me to review?

8. How long has your firm been in business, and how long have you been an associate?

9. How many business clients does your firm represent? How many do you represent?

10. What are your business credentials, degrees, and/or certificates?

11. Do you mostly do business accounting or tax accounting?

Add extra questions to test your candidates’ general knowledge about your specific business and the specific locations in which you operate. For example, if you do international business, probe for experience and training in that regard.

After completing an interview process you will have a much better understanding and expectation about the capabilities of the accountant and his or her potential fit with your business. You may learn that you want to work with one resource for both tax accounting and business accounting or you may determine it works better to select one for business accounting and a separate accountant for tax services.

Ongoing work with your accountant

Finding the right accountant is important, but working with the accountant on an ongoing basis is key to the successful development of your business. Too often a business owner does not coordinate with her accountant to monitor and manage the key drivers of the financial success of the business. Your accountant may be very helpful in identifying the most important measurements to monitor on a daily or weekly basis to keep pace with your business planning and financial goals. To maximize your financial results, work with your accountant to develop a specific list of what will be monitored and how you will respond to variations in expected performance. Following a clear plan, tracking key information, and responding timely to variances will optimize the performance of your business.

Managing Your Relationship with Your Lender

It’s not where you start… but where you finish. Communicate and win!

YOU ARE READY TO SELECT a bank for your new business. Now what?

Obviously, you thought about the bank’s location, hours and array of services. Those were the very basics, based on your own research or even a colleague’s referral. But what about the next level of factors that need to be addressed?

Often, entrepreneurs fail to dig a little deeper to learn about the how a bank interacts with its small business banking and lending customers. They may never even interview a bank officer about lending practices, decision-making on check-clearing processes, or the bank’s track record of success with other small businesses in the area. It is vital to consider these additional aspects before selecting a bank for your small business needs. So if you haven’t made the final choice yet, or even if you have, consider the following advice.

It’s not where you start… but where you finish

Initially, your small business may need nothing more than having the bank handle your deposits, withdrawals and debit cards. Without question, this can be a good foundation for a banking relationship. However, developing a successful banking relationship goes well beyond these narrow parameters. In fact, when developed, and then later managed well, a banking relationship can really help a company thrive and grow over the years.

And thinking of the future, there is often a natural progression in banking relationships. Small businesses that grow into large-scale corporations may at some point decide it’s in their best interest to use more than one bank. This may be for many reasons. You may want to have two or more banks presenting competitive proposals for the financial services you need. Or you have a very long personal history and therefore a stronger trust base with one, yet another is hungry for new customers. One may have a unique service that another lacks. The “feel” of one bank may or may not suit you, despite its competitive terms or good service, etc. The important thing to remember, however, is that if you deal with more than one bank, your business will then need to manage multiple banking relationships. And that will require time and attention.

Once your business becomes even larger, it may be necessary to create additional relationships with investment banks as well. Investment banks support individuals, corporations and even governments with various services such as foreign exchange transactions, mergers and acquisitions, mutual funds, hedge funds and pension funds. Regardless of your needs, the scale of your business or the timeline involved, creating and then managing your relationship with your bank(s) can be as significant as any other aspect of business on your path to success.

Communicate… and win!

Research indicates that a large percentage of business owners feel trepidation regarding their banker(s) and, as a result, experience a disconnect when interacting with them. You should never let this happen. Your bankers, if vetted properly for a perfect fit, will be key players in your financial dealings. And if your communication with them meets their expectations and requirements, they should see you as a partner as well. To say communication is important is a complete understatement.

There are really two keys to banking relationship success: communication and time. Spending quality time and communicating professionally and candidly with your banker, especially in the early stages of developing a relationship, works to establish a better understanding, trust and working knowledge of your organization’s operations, inside and out. Be prepared to educate your banker about the key factors in your business—a good banker is business savvy, but may not have worked with customers in your particular sector before. This fundamental process of sharing will also stabilize and reinforce the view your banker has developed about you, both personally and as a business person.

Meeting with your banker once a year or only when a problem arises just doesn’t cut it. If your company has just won an award or secured a big contract, make sure your banker knows about it. And if you’ve set sales records, added more clients or even been featured in the local paper, include your banker in your public relations announcement list too. This reinforcement helps the banker get a feeling of where you fit in your marketplace, compared with your competition. It can pay off in a future loan or credit line process down the road. This sort of information is difficult to translate onto an application; it’s all the more reason to keep positive lines of communication open.

Make time

We mentioned time as a key relationship factor above. As with any relationship, you need to invest time to foster its growth. Like all entrepreneurs, you wear many hats, and the finance one may not fit your head as well as some of the others on your rack. However, the benefits of a strong relationship with your bank always reward the time you invest in it. You and your banker should review your bank statements, financials and other important documents together a few times a year so both sides understand each other.

Time is important here in another sense. Recognize that you will need adequate time to be thorough and organized in your financial dealings. When it does come time for that application for credit or loan, taking as much time as you need to do it right is an absolute must. This includes providing the bank with every piece of documentation requested, no matter how trivial it may seem to you. Yes, this takes time and effort. But once again, taking great care will make your professionalism shine through, and that will pay off, regardless of the banking goals you may have.