Overview of the Financial Services Industry

This chapter provides a summary of the Financial Services industry. It is not meant to provide an in-depth overview but to provide sufficient context for the rest of the book.

A Simple Definition

The Financial Services industry is a wide and complex area (which this chapter will hopefully demonstrate) which means providing a precise definition can be challenging. Therefore for this book, it will be defined as follows:

The Financial Industry consists of many Financial Services Organizations providing financial services products/services to their customers and consumers.

The Financial Services Organizations that provide these services cover many firms such as banks, credit card providers, investment managers plus others.

The products/services provided cover offerings such as bank accounts, investment products, credit cards, investment advice, capital funding plus others.

These customers and consumers who receive these products/ services will cover everything from individual retail customers to large multinational organizations, local/national governments and pension funds.

Why Is Financial Services Critical?

It is safe to say that the Financial Services industry is critical to the dayto-day operations of the global economy.

The movement of money must happen and if it does not happen then there will be material issues. For example, imagine the situation if invoices, salaries, or pensions were not being paid? There would be uproar, possible rioting, and a general breakdown of society.

Likewise, many activities legally need insurance in place to allow them to happen. For example, a pilot and airline need insurance to fly a plane, people need insurance to drive a car, and people often need to take out insurance before going on holiday.

How Big Is the Financial Services Industry?

Unfortunately, obtaining accurate statistics on the size of the Financial Services industry (or any industry for that matter) is challenging. This is because most assessments are performed using different measurements, using different methodologies, using differing timescales, using different assumptions, and are often performed for different purposes.

However, some high-level statistics can be quoted to demonstrate the size of the global Financial Services industry.

• Forbes in 2019 created a “list of world’s largest public firms in revenue generation” which showed Banking as the third biggest industry by sales globally (at USD 4.424 trillion) and Insurance as the sixth biggest industry by sales globally (at USD 2.611 trillion). The top industry was Oil and Gas (at USD 4.797 trillion) with Technology (also a topic of this book) coming in second at USD 4.726 trillion. Therefore, if Banking and Insurance were combined under the umbrella of Financial Services then it would be the largest industry by sales globally.

• The same study also assessed profitability by industry and Banking was top of the list at USD 773 million with Technology second (at USD 548 billion) and Oil and Gas third (at USD 292 billion). Insurance, in this case, was much further down the list with a profitability of USD 148 billion.

This means it is safe to say that Financial Services (and Technology for that matter) is one of the world’s largest industries in terms of revenue and profitability.

The Structure of the Financial Services Industry

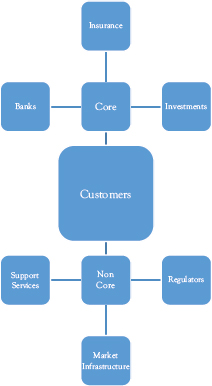

Figure 2.1 provides a high-level summary of the main areas of the industry.

At the center of the industry is (or should always be) the customer because ultimately they are the people which the industry is trying to service. Without customers, the industry would not exist. This area is discussed in more detail further below.

Figure 2.1 High-level summary of the industry

Around the customers, there are a variety of industry players which can be split into “core” players and “non-core” players namely:

• “Core” players are the organizations that provide actual financial products and services to customers. These organizations are Banks, Insurance (and Pension) Companies, and Investors. These are discussed in more detail below.

• “Non-core” players are other key industry members but these provide support services to the industry and do not provide actual services or products to the customers or consumers. These cover organizations such as Technology firms, Legal firms, Infrastructure, and Regulators. These are discussed in more depth below.

Customers

A customer can be any person or organization that can exist globally. For example, these could be individual people, partnerships, charities, organizations, and government bodies. Customers are the group who the industry is supposed to serve but (as this book will demonstrate) this is much more challenging than it sounds. This is because firms are often diverted away from serving their customers due to regulatory challenges, operating model complexities, the challenges of “going green,” the need to make a return for their shareholders plus many others.

Core Players

At the simplest level, there are three types of core players within the Financial Services industry.

Banks

This group is probably the most common and prominent with (a) most people in the developed world having at least one bank account product and (b) most villages, towns, or cities having several different bank branches located within them.

Banking itself can be split into further subgroups, namely:

• Retail, Consumer, or Personal Banking

• Business Banking

• Investment Banking

Each is discussed below.

Retail, Consumer, or Personal Banking

These banks provide services and products to the general public or retail customers which are distributed via branches, websites, and call centers. They offer a range of generic services such as

• Current accounts—An account at a bank where money can be deposited and withdrawn without notice.

• Savings accounts—An account at a bank where a small amount of interest is paid on the amount deposited. Typically, there is no notice for adding or removing monies.

• Mortgages—A legal agreement where a bank will loan money (with interest) to allow an individual to purchase a property. The mortgage loan is guaranteed by the property so if the borrower defaults then the bank can take legal title of the property. However, once the mortgage is fully paid then the bank has no claim over the property.

• Personal loans—A loan from a bank to an individual for a personal need (such as buying a car).

• Debit cards—A debit card is a payment card that deducts money from the customer’s current account when it is used. It can be used to purchase goods or withdraw cash from

an ATM.

• Credit cards—A card that allows a customer (or the cardholder) to borrow money to pay for goods and services. The customer will be charged interest on the borrowed money and sometimes they will also be charged a flat fee as well. The customer will be expected to refund the borrowed money back to the bank regularly.

Also, some countries allow Savings Institutions to exist (such as Building Societies within the UK or Credit Unions in other parts of the world). These will offer similar (if not the same services and products) as Retail Banks. However, the main difference is that Retail Banks are normally owned by shareholders whereas Savings Institutions are owned by their customers. For this reason, they are sometimes called Mutual.

This is similar to Retail Banking but these organizations offer services to corporations and other larger clients. These services are also distributed via Branches, Websites, and Call Centers. Some Banks will offer both Retail and Business Banking through the same Branch (although Business Banking does tend to be performed from larger branches situated in towns and cities). They offer similar services as Retail Banking (see above) but they are tailored more towards corporations. The list of typical services is listed below again for completeness

• Current accounts—An account at a bank where money can be deposited and withdrawn without notice.

• Savings accounts—An account at a bank where a small amount of interest is paid on the amount deposited. Typically, there is no notice for adding or removing monies.

• Mortgages—A legal agreement where a bank will loan money (with interest) to allow an individual to purchase a property. The mortgage loan is guaranteed by the property so if the borrower defaults then the bank can take legal title of the property. However, once the mortgage is fully paid then the bank has no claim over the property.

• Personal loans—A loan from a bank to an individual for a personal need (such as buying a car).

• Debit cards—A debit card is a payment card that deducts money from the customer’s current account when it is used. It can be used to purchase goods or withdraw cash from an ATM.

• Credit cards—A card that allows a customer (or the cardholder) to borrow money to pay for goods and services. The customer will be charged interest on the borrowed money and sometimes they will also be charged a flat fee as well. The customer will be expected to refund the borrowed money back to the bank regularly.

Investment Banking

This area is often misunderstood but effectively it is a bank that performs complex, risky, and large transactions on behalf of large customers such as companies, institutions, and governments. It will offer most of the basic banking services (detailed under Retail and Business Banking above) as well as the following specialist services:

• Raising of Capital—This is trying to raise capital (or money) for its corporate customers. This could involve acting as the “middle man” to match companies who want to issue shares with investors who want to buy them.

• Mergers and Acquisitions—This involves helping customers who want to merge and acquire companies. Specifically, this could cover providing advice, performing research, executing due diligence, negotiating to fund, negotiating contracts, and finding investors.

• Securities sales and trading (across bonds, equities, derivatives, foreign exchange, and other asset classes)—This involves providing books of shares that can be traded with other firms such as other Investment Banks or Asset Managers. These securities are normally trading on behalf of the bank themselves and this is often called propriety trading. This is different to Investment Managers, who trade on behalf of their clients and customers (and this is often called Agent or Agency trading).

• Providing Banking Services for large organizations such as governments and multinational firms. These types of firms will have complex and demanding banking needs (such as large short-term borrowing needs, large transaction amounts, or complex liabilities that need to be managed) which will need support and are far too complex and risky for standard Retail or Business Banks.

Insurance

The concept behind insurance is relatively straightforward. At its simplest level, insurance is a product or service to mitigate against the risk of something nasty happening (often with an associated financial or another type of loss). The party which could be impacted will pay a cash premium to an insurance firm who will then pay a financial amount to re-compensate this party if the event happens. The size of the premium is dependent on the size of the compensation and the likelihood of the event happening. For example, for a large compensation which is likely to happen then the premium will be large whereas for small compensations with a low likelihood then the premium will be smaller.

The types of events that could happen are vast, namely:

• Death—On the death of the insured person then a pre-agreed amount of money will be paid to the policyholders (who are typically family members of the person who has died). In the UK, this is often termed Life Assurance (as opposed to Insurance) to reflect the fact that death will happen as opposed to Insurance which is to mitigate against an event that could happen.

• Critical illness insurance—In this insurance plan, the insurer will pay a lump sum and/or a series of regular payments if the policyholder is diagnosed with one of the specific illnesses detailed in the pre-agreed insurance policy.

• Accident insurance—The policyholder is paid either a lump sum or a set of regular payments if they are injured per the terms of the pre-agreed insurance policy.

• Car (or Vehicle) Insurance—This provides financial insurance against vehicle damage, bodily injuries, and the personal liability that could result from a traffic accident. Some policies may also cover damage to the vehicle caused by events other than traffic accidents such as theft, vandalism, natural disasters, and others. In many countries, it is illegal to drive a vehicle without suitable insurance in place.

• Home or Buildings Insurance—This insurance provides financial support to losses that could happen to a customer’s home such as replacing damaged contents, refunding any extra living expenses, and so on.

• Plus many others such as Agricultural, Flood, Pet, Travel, Income Projection, Cyber, Rent Guarantee, Profession Indemnity, and Personal Indemnity insurance.

However, it cannot stressed be enough how important the Insurance industry is to the day-to-day running of the global economy. This is because many activities cannot take place unless Insurance is in place. For example, individuals need insurance to drive a car, airlines and pilots need insurance to fly their planes, and individuals need professional and personal insurance to perform their work.

Finally, there is a subset of the insurance industry called Reinsurance which is when an insurance firm realizes they have too much exposure to a type of risk then they will look to re-insurance this risk with another insurance firm.

Investments

Investments is an industry where one party (often called the manager) manages investments (such as securities, cash, property, etc.) on behalf of another party (often called the “investor”) against a set of agreed objectives (such as increased value by × percent or track a certain benchmark) as well as an agreed set of constraints (such as do not invest in tobacco or carbon polluting stocks). However, it is important to note that this is an agency arrangement and the managers themselves will not invest their own money.

There are two main types of product groups within the industry, namely:

• Collective investment schemes—The manager will pool all investments into a single portfolio which is unitized and then the units are sold to investors. Collective investment schemes are often referred to as Mutual Funds or just Funds in some cases.

• Standalone or segregated portfolio where an individual portfolio is created for each investor and the Manager will purchase and sell investments, specifically for this client who holds this segregated portfolio. These segregated portfolios can be sub-divided further into execution-only (where the investor will decide what to purchase and the manager will follow that order), advisory (where the investor and manager will work together to determine what investments should be bought and/or sold), and discretionary (where the investors effectively hands over control to the manager who, subject to pre-agreed objectives, will buy, and/or sell investments).

There are four main roles within Investments, namely:

• Investors—The organizations or entities that legally own the assets which are managed. This will cover a wide range of entities from large Sovereign Wealth Funds or Pension Funds down to Retail clients. Retail investors come in many shapes and sizes ranging from an individual who invests a small amount per month into some type of savings plan or collective investment scheme, to day traders and to Retail Clients who are wealthy enough to warrant their segregated portfolio.

• Managers are the entities that manage the assets owned by the Investors via a Collective Investment Scheme or Standalone Segregated Portfolio.

• Distributors are the bodies that are responsible for “distributing” the products that the Manager offers to the Investors. These distributors can cover anything from an individual providing advice on a 1-2-1 basis to complex online platforms which support many products and provide a range of advice and trading services.

• Administrators are responsible for performing all the “day-today” administration and operational tasks involved in managing the funds and the underlying investments.

Overlap Between Banks, Insurance, and Investment Firm

While the above three sections list these players separately, there is a large amount of overlap and interaction between them. For example, it is not uncommon for a single firm to own a Retail Bank, Business Bank, Investment Bank, Insurance firm, and Investment firm. These often trade under the same name which creates confusion.

Likewise, it is also not that uncommon that the Retail Bank part of a firm will distribute (or sell) investment products (such as Collective Investment Schemes) that its Investment Firm subsidiary manages.

Furthermore, an Insurance Firm or large Asset Owner (such as a pension fund) may have their captive Investment Firm to manage their assets.

This interaction and overlap caused contamination issues during the credit crisis when issues with Investment Banks spread into Insurance Firms and Retail Banks and almost brought the entire financial system to its knees. (This is discussed in more detail below.)

“Non-Core” Players

There is a wide range of “non-core” players who provide a support service to the industry.

Regulators

Before the Credit Crisis in 2008, financial regulation tended to be very “light touch” compared to other crucial industries. However, since 2008, there has been a “tsunami” of new regulations which has inundated the Financial Services industry. This regulation sets out to ensure that the stability and integrity of the financial system are maintained as well as ensuring consumers are protected and market confidence is maintained. This wave of new and updated regulation is set to continue for the foreseeable future. This complex set of existing and new global regulations is and will continue to provide many challenges to the industry. For example, increased costs to comply which is squeezing profit margins, an adverse impact on innovation, and increased complexity. These challenges are in turn forcing the industry to change the way they work. Firms now need to constantly review cultures, capital requirements, product development processes, investment strategies, marketing approaches, distribution, their operating model, and associated infrastructures as well developing the ability to complete regulatory returns.

Examples of regulators are the Financial Conduct Authority (FCA) in the UK and the Central Bank of Ireland (CBI) in the Republic of Ireland.

Market Infrastructure

This is an area that is often overlooked.

The key point to note is that the financial services industry is almost entirely reliant on technology (which is a key theme of this book). This covers firms operating within their boundaries (such as maintaining accounting records, performing transactions, and servicing customers) as well as firms interacting with each other regularly (such as trading between firms or transferring money between organizations).

To allow this cross-firm interaction to take place between firms then a shared market infrastructure is required (supported by common standards) which firms can “plug into” as required. For example, SWIFT for messaging, BACS for UK payments, exchanges for trading, and many others.

Support Services

Finally, as part of the industry, there are various support or ancillary players who work in the industry but are not financial services in the strictest sense. This cover the following:

• Technology firms—As mentioned previously, all firms are very reliant on technology and the majority of this is provided by external vendors. This technology can range from applications (such as order management systems), networking infrastructure (such as Internet connectivity), data storage providers (such as data centers or cloud providers) plus many others.

• Legal firms and other legal advisors—Firms are reliant on legal firms to support a wide range of legal areas. Financial services are now governed by a complex set of regulations which means firms are reliant on legal firms to ensure they understand the rules so they can be compliant. Furthermore, firms need external legal firms to help support many other areas such as client contracts, supplier contracts, trading agreements, and so on.

• Consultants—Firms will use consultants for a wide range of purposes. This advice could cover areas such as implementing new technology, advice on launching new products, advice on entering new geographic regions, understanding the impact of political decisions, staff contracts, and so on.

• Academia—Firms will often use academia in various areas. This can cover purchasing and using secondary research to help understand how the industry is developing, how client behaviors are changing, understanding how new technology is impacting the industry plus many other areas. Firms will also employ academics to gather primary research on specific issues that are pertinent to the firm; for example, how will economic conditions impact their client base or product range.

• Training firms—The Financial Services industry is a complex industry covering many specific technical skillsets (banking, investments, technology, etc.) and many general skillsets (leadership, staff management, etc.). Staff need to be trained with these skills and firms will often employ specialist training firms for this.

• Recruitment firms—The Financial Services industry employs a large number of people covering permanent staff, contracting staff, part-time staff, and so on. To ensure their staffing needs are met, the firms will employ specialist recruitment firms.

• Trade Associations—These bodies tend to have two main purposes. The first purpose is to holistically represent the industry to outsiders. For example, during the UK’s exit from the European Union (“Brexit”) between 2016 and 2020, many of the UK Financial Services Trade Association would represent their members and their views to EU and UK governments. It was thought that having a single body (i.e., the Trade Association) with the weight of its member behind it, would carry more gravitas than each firm acting on its own. The second purpose is to allow firms to work together for the general good of the industry. For example, if there is new regulation being implemented then it is not uncommon for Trade Associations to form working groups to allow a large number of firms to work collectively to implement the regulation successfully across the industry.

• There is also a vast number of other support services such as marketing agencies, advertisement agencies, press relations firms, facilities management firms, and others.