This chapter discusses rental income and expenses. It also covers the following topics.

Personal use of dwelling unit (including vacation home).

Depreciation.

Limits on rental losses.

How to report your rental income and expenses.

If you sell or otherwise dispose of your rental property, see Pub. 544, Sales and Other Dispositions of Assets.

If you have a loss from damage to, or theft of, rental property, see Pub. 547, Casualties, Disasters, and Thefts.

If you rent a condominium or a cooperative apartment, some special rules apply to you even though you receive the same tax treatment as other owners of rental property. See Pub. 527, Residential Rental Property, for more information.

Useful Items

You may want to see:

Publication

527Residential Rental Property

534Depreciating Property Placed in Service Before 1987

535Business Expenses

925Passive Activity and At-Risk Rules

946How To Depreciate Property

Form (and Instructions)

4562Depreciation and Amortization

6251Alternative Minimum Tax—Individuals

8582Passive Activity Loss Limitations

Schedule E (Form 1040) Supplemental Income and Loss

Rental Income

In most cases, you must include in your gross income all amounts you receive as rent. Rental income is any payment you receive for the use or occupation of property. In addition to amounts you receive as normal rent payments, there are other amounts that may be rental income.

When to report. If you are a cash-basis taxpayer, you report rental income on your return for the year you actually or constructively receive it. You are a cash-basis taxpayer if you report income in the year you receive it, regardless of when it was earned. You constructively receive income when it is made available to you, for example, by being credited to your bank account.

For more information about when you constructively receive income, see Accounting Methods in chapter 1.

Advance rent. Advance rent is any amount you receive before the period that it covers. Include advance rent in your rental income in the year you receive it regardless of the period covered or the method of accounting you use.

Example. You sign a 10-year lease to rent your property. In the first year, you receive $5,000 for the first year’s rent and $5,000 as rent for the last year of the lease. You must include $10,000 in your income in the first year.

Canceling a lease. If your tenant pays you to cancel a lease, the amount you receive is rent. Include the payment in your income in the year you receive it regardless of your method of accounting.

Expenses paid by tenant. If your tenant pays any of your expenses, the payments are rental income. Because you must include this amount in income, you can deduct the expenses if they are deductible rental expenses. See Rental Expenses, later, for more information.

Your tenant pays the water and sewage bill for your rental property and deducts the amount from the normal rent payment. Under the terms of the lease, your tenant does not have to pay this bill. Include the utility bill paid by the tenant and any amount received as a rent payment in your rental income. You can deduct the utility payment made by your tenant as a rental expense.

While you are out of town, the furnace in your rental property stops working. Your tenant pays for the necessary repairs and deducts the repair bill from the rent payment. Include the repair bill paid by the tenant and any amount received as a rent payment in your rental income. You can deduct the repair payment made by your tenant as a rental expense.

Property or services. If you receive property or services, instead of money, as rent, include the fair market value of the property or services in your rental income.

If the services are provided at an agreed upon or specified price, that price is the fair market value unless there is evidence to the contrary.

Security deposits. Do not include a security deposit in your income when you receive it if you plan to return it to your tenant at the end of the lease. But if you keep part or all of the security deposit during any year because your tenant does not live up to the terms of the lease, include the amount you keep in your income in that year.

If an amount called a security deposit is to be used as a final payment of rent, it is advance rent. Include it in your income when you receive it.

If you keep part or all of the security deposit because the tenant breaks the lease by vacating the property early, include the amount you keep in your income that year. If you keep part or all of the security deposit because the tenant damaged the property and you must make repairs, include the amount you keep in that year if your practice is to deduct the cost of repairs as expenses. To the extent the security deposit reimburses those expenses, do not include the amount in income if your practice is not to deduct the cost of repairs as expenses. If a security deposit amount is to be used as the tenant’s final month’s rent, it is advance rent that you include as income when you receive it, rather than when you apply it to the last month’s rent.

Part interest. If you own a part interest in rental property, you must report your part of the rental income from the property.

Rental of property also used as your home. If you rent property that you also use as your home and you rent it less than 15 days during the tax year, do not include the rent you receive in your income and do not deduct rental expenses. However, you can deduct on Schedule A (Form 1040) the interest, taxes, and casualty and theft losses that are allowed for nonrental property. See Personal Use of Dwelling Unit (Including Vacation Home), later.

Rental Expenses

This part discusses expenses of renting property that you ordinarily can deduct from your rental income. It includes information on the expenses you can deduct if you rent part of your property, or if you change your property to rental use. Depreciation, which you can also deduct from your rental income, is discussed later.

Personal use of rental property. If you sometimes use your rental property for personal purposes, you must divide your expenses between rental and personal use. Also, your rental expense deductions may be limited. See Personal Use of Dwelling Unit (Including Vacation Home), later.

Part interest. If you own a part interest in rental property, you can deduct expenses that you paid according to your percentage of ownership.

Roger owns a one-half undivided interest in a rental house. Last year he paid $968 for necessary repairs on the property. Roger can deduct $484 (50% × $968) as a rental expense. He is entitled to reimbursement for the remaining half from the co-owner.

When to deduct. If you are a cash-basis taxpayer, you generally deduct your rental expenses in the year you pay them. If you use the accrual method, see Pub. 538 for more information.

Depreciation.Depreciation is a capital expense. It is the mechanism for recovering your cost in an income producing property and must be taken over the expected life of the property. You can begin to depreciate rental property when it is ready and available for rent. See Placed-in-Service under When Does Depreciation Begin and End in chapter 2 of Pub. 527.

Pre-rental expenses. You can deduct your ordinary and necessary expenses for managing, conserving, or maintaining rental property from the time you make it available for rent.

Uncollected rent. If you are a cash-basis taxpayer, do not deduct uncollected rent. Because you have not included it in your income, it is not deductible.

Vacant rental property. If you hold property for rental purposes, you may be able to deduct your ordinary and necessary expenses (including depreciation) for managing, conserving, or maintaining the property while the property is vacant. However, you cannot deduct any loss of rental income for the period the property is vacant.

Vacant while listed for sale. If you sell property you held for rental purposes, you can deduct the ordinary and necessary expenses for managing, conserving, or maintaining the property until it is sold. If the property is not held out and available for rent while listed for sale, the expenses are not deductible rental expenses.

Repairs and Improvements

Generally, an expense for repairing or maintaining your rental property may be deducted if you are not required to capitalize the expense.

Improvements. You must capitalize any expense you pay to improve your rental property. An expense is for an improvement if it results in a betterment to your property, restores your property, or adapts your property to a new or different use.

Betterments. Expenses that may result in a betterment to your property include expenses for fixing a pre-existing defect or condition, enlarging or expanding your property, or increasing the capacity, strength, or quality of your property.

Restoration. Expenses that may be for restoration include expenses for replacing a substantial structural part of your property, repairing damage to your property after you properly adjusted the basis of your property as a result of a casualty loss, or rebuilding your property to a like-new condition.

Adaptation. Expenses that may be for adaptation include expenses for altering your property to a use that is not consistent with the intended ordinary use of your property when you began renting the property.

The expenses you capitalize for improving your property can generally be depreciated as if the improvement were separate property.

Other Expenses

Other expenses you can deduct from your rental income include advertising, cleaning and maintenance, utilities, fire and liability insurance, taxes, interest, commissions for the collection of rent, ordinary and necessary travel and transportation, and other expenses, discussed next.

Insurance premiums paid in advance. If you pay an insurance premium for more than one year in advance, you cannot deduct the total premium in the year you pay it. For each year of coverage, you deduct only the part of the premium payment that applies to that year.

Legal and other professional fees. You can deduct, as a rental expense, legal and other professional expenses, such as tax return preparation fees you paid to prepare Schedule E (Form 1040), Part I. For example, on your 2017 Schedule E, you can deduct fees paid in 2017 to prepare your 2015 Schedule E, Part I. You can also deduct, as a rental expense, any expense (other than federal taxes and penalties) you paid to resolve a tax underpayment related to your rental activities.

Local benefit. In most cases, you cannot deduct charges for local benefits that increase the value of your property, such as charges for putting in streets, sidewalks, or water and sewer systems. These charges are nondepreciable capital expenditures, and must be added to the basis of your property. However, you can deduct local benefit taxes that are for maintaining, repairing, or paying interest charges for the benefits.

Local transportation expenses. You may be able to deduct your ordinary and necessary local transportation expenses if you incur them to collect rental income or to manage, conserve, or maintain your rental property. However, transportation expenses incurred to travel between your home and a rental property generally constitute nondeductible commuting costs unless you use your home as your principal place of business. See Pub. 587, Business Use of Your Home, for information on determining if your home office qualifies as a principal place of business.

Generally, if you use your personal car, pickup truck, or light van for rental activities, you can deduct the expenses using one of two methods: actual expenses or the standard mileage rate. For 2017, the standard mileage rate for business use is 53.5 cents per mile. For more information, see chapter 27.

Rental of equipment. You can deduct the rent you pay for equipment that you use for rental purposes. However, in some cases, lease contracts are actually purchase contracts. If so, you cannot deduct these payments. You can recover the cost of purchased equipment through depreciation.

Rental of property. You can deduct the rent you pay for property that you use for rental purposes. If you buy a leasehold for rental purposes, you can deduct an equal part of the cost each year over the term of the lease.

Travel expenses. You can deduct the ordinary and necessary expenses of traveling away from home if the primary purpose of the trip is to collect rental income or to manage, conserve, or maintain your rental property. You must properly allocate your expenses between rental and nonrental activities. You cannot deduct the cost of traveling away from home if the primary purpose of the trip was to improve your property. You recover the cost of improvements by taking depreciation. For information on travel expenses, see chapter 27.

See Rental Expenses in Pub. 527 for more information.

Property Changed To Rental Use

If you change your home or other property (or a part of it) to rental use at any time other than the beginning of your tax year, you must divide yearly expenses, such as taxes and insurance, between rental use and personal use.

You can deduct as rental expenses only the part of the expense that is for the part of the year the property was used or held for rental purposes.

You cannot deduct depreciation or insurance for the part of the year the property was held for personal use. However, you can include the home mortgage interest, qualified mortgage insurance premiums, and real estate tax expenses for the part of the year the property was held for personal use as an itemized deduction on Schedule A (Form 1040).

Example

Your tax year is the calendar year. You moved from your home in May and started renting it out on June 1. You can deduct as rental expenses seven-twelfths of your yearly expenses, such as taxes and insurance.

Starting with June, you can deduct as rental expenses the amounts you pay for items generally billed monthly, such as utilities.

Renting Part of Property

If you rent part of your property, you must divide certain expenses between the part of the property used for rental purposes and the part of the property used for personal purposes, as though you actually had two separate pieces of property.

You can deduct the expenses related to the part of the property used for rental purposes, such as home mortgage interest, qualified mortgage insurance premiums, and real estate taxes, as rental expenses on Schedule E (Form 1040). You can also deduct as rental expenses a portion of other expenses that normally are nondeductible personal expenses, such as expenses for electricity or painting the outside of your house.

There is no change in the types of expenses deductible for the personal-use part of your property. Generally, these expenses may be deducted only if you itemize your deductions on Schedule A (Form 1040).

You cannot deduct any part of the cost of the first phone line even if your tenants have unlimited use of it.

You do not have to divide the expenses that belong only to the rental part of your property. For example, if you paint a room that you rent, or if you pay premiums for liability insurance in connection with renting a room in your home, your entire cost is a rental expense. If you install a second phone line strictly for your tenants’ use, all of the cost of the second line is deductible as a rental expense. You can deduct depreciation, discussed later, on the part of the house used for rental purposes as well as on the furniture and equipment you use for rental purposes.

How to divide expenses. If an expense is for both rental use and personal use, such as mortgage interest or heat for the entire house, you must divide the expense between the rental use and the personal use. You can use any reasonable method for dividing the expense. It may be reasonable to divide the cost of some items (for example, water) based on the number of people using them. The two most common methods for dividing an expense are based on (1) the number of rooms in your home, and (2) the square footage of your home.

Not Rented for Profit

If you do not rent your property to make a profit, you can deduct your rental expenses only up to the amount of your rental income. You cannot deduct a loss or carry forward to the next year any rental expenses that are more than your rental income for the year. For more information about the rules for an activity not engaged in for profit, see Not-for-Profit Activities in chapter 1 of Pub. 535.

Where to report. Report your not-for-profit rental income on Form 1040, line 21. For example, you can include your mortgage interest and any qualified mortgage insurance premiums (if you use the property as your main home or second home), real estate taxes, and casualty losses on the appropriate lines of Schedule A (Form 1040) if you itemize your deductions.

If you itemize your deductions, claim your other rental expenses, subject to the rules explained in chapter 1 of Pub. 535, as miscellaneous itemized deductions on Schedule A (Form 1040). You can deduct these expenses only if they, together with certain other miscellaneous itemized deductions, total more than 2% of your adjusted gross income.

Personal Use of Dwelling Unit (Including Vacation Home)

If you have any personal use of a dwelling unit (including a vacation home) that you rent, you must divide your expenses between rental use and personal use. In general, your rental expenses will be no more than your total expenses multiplied by a fraction, the denominator of which is the total number of days the dwelling unit is used and the numerator of which is the total number of days actually rented at a fair rental price. Only your rental expenses may be deducted on Schedule E (Form 1040). Some of your personal expenses may be deductible if you itemize your deductions on Schedule A (Form 1040).

You must also determine if the dwelling unit is considered a home. The amount of rental expenses that you can deduct may be limited if the dwelling unit is considered a home. Whether a dwelling unit is considered a home depends on how many days during the year are considered to be days of personal use. There is a special rule if you used the dwelling unit as a home and you rented it for less than 15 days during the year.

Dwelling unit. A dwelling unit includes a house, apartment, condominium, mobile home, boat, vacation home, or similar property. It also includes all structures or other property belonging to the dwelling unit. A dwelling unit has basic living accommodations, such as sleeping space, a toilet, and cooking facilities.

A dwelling unit does not include property used solely as a hotel, motel, inn, or similar establishment. Property is used solely as a hotel, motel, inn, or similar establishment if it is regularly available for occupancy by paying customers and is not used by an owner as a home during the year.

Example. You rent a room in your home that is always available for short-term occupancy by paying customers. You do not use the room yourself, and you allow only paying customers to use the room. The room is used solely as a hotel, motel, inn, or similar establishment and is not a dwelling unit.

Dividing Expenses

If you use a dwelling unit for both rental and personal purposes, divide your expenses between the rental use and the personal use based on the number of days used for each purpose.

When dividing your expenses, follow these rules.

Any day that the unit is rented at a fair rental price is a day of rental use even if you used the unit for personal purposes that day. This rule does not apply when determining whether you used the unit as a home.

Any day that the unit is available for rent but not actually rented is not a day of rental use.

Example. Your beach cottage was available for rent from June 1 through August 31 (92 days). During that time, except for the first week in August (7 days) when you were unable to find a renter, you rented the cottage at a fair rental price. The person who rented the cottage for July allowed you to use it over the weekend (2 days) without any reduction in or refund of rent. Your family also used the cottage during the last 2 weeks of May (14 days). The cottage was not used at all before May 17 or after August 31.

You figure the part of the cottage expenses to treat as rental expenses as follows.

The cottage was used for rental a total of 85 days (92 – 7). The days it was available for rent but not rented (7 days) are not days of rental use. The July weekend (2 days) you used it is rental use because you received a fair rental price for the weekend.

You used the cottage for personal purposes for 14 days (the last 2 weeks in May).

The total use of the cottage was 99 days (14 days personal use + 85 days rental use).

Your rental expenses are 85/99 (86%) of the cottage expenses.

Note. When determining whether you used the cottage as a home, the July weekend (2 days) you used it is considered personal use even though you received a fair rental price for the weekend. Therefore, you had 16 days of personal use and 83 days of rental use for this purpose. Because you used the cottage for personal purposes more than 14 days and more than 10% of the days of rental use (8 days), you used it as a home. If you have a net loss, you may not be able to deduct all of the rental expenses. See Dwelling Unit Used as a Home, next.

Dwelling Unit Used as a Home

If you use a dwelling unit for both rental and personal purposes, the tax treatment of the rental expenses you figured earlier under Dividing Expenses and rental income depends on whether you are considered to be using the dwelling unit as a home.

You use a dwelling unit as a home during the tax year if you use it for personal purposes more than the greater of:

14 days, or

10% of the total days it is rented to others at a fair rental price.

Fair rental price. A fair rental price for your property generally is the amount of rent that a person who is not related to you would be willing to pay. The rent you charge is not a fair rental price if it is substantially less than the rents charged for other properties that are similar to your property in your area.

If a dwelling unit is used for personal purposes on a day it is rented at a fair rental price, do not count that day as a day of rental use in applying (2) just described. Instead, count it as a day of personal use in applying both (1) and (2) just described.

What is a day of personal use? A day of personal use of a dwelling unit is any day that the unit is used by any of the following persons.

You or any other person who has an interest in the unit, unless you rent it to another owner as his or her main home under a shared equity financing agreement (defined later). However, see Days used as a main home before or after renting, later.

A member of your family or a member of the family of any other person who owns an interest in the unit, unless the family member uses the dwelling unit as his or her main home and pays a fair rental price. Family includes only your spouse, brothers and sisters, half-brothers and half-sisters, ancestors (parents, grandparents, etc.), and lineal descendants (children, grandchildren, etc.).

Anyone under an arrangement that lets you use some other dwelling unit.

Anyone at less than a fair rental price.

Main home. If the other person or member of the family in (1) or (2) just described has more than one home, his or her main home is ordinarily the one he or she lived in most of the time.

Shared equity financing agreement. This is an agreement under which two or more persons acquire undivided interests for more than 50 years in an entire dwelling unit, including the land, and one or more of the co-owners is entitled to occupy the unit as his or her main home upon payment of rent to the other co-owner or owners.

Donation of use of property. You use a dwelling unit for personal purposes if:

You donate the use of the unit to a charitable organization,

The organization sells the use of the unit at a fund-raising event, and

The “purchaser” uses the unit.

Examples. The following examples show how to determine days of personal use.

Example 1. You and your neighbor are co-owners of a condominium at the beach. Last year, you rented the unit to vacationers whenever possible. The unit was not used as a main home by anyone. Your neighbor used the unit for 2 weeks last year; you did not use it at all.

Because your neighbor has an interest in the unit, both of you are considered to have used the unit for personal purposes during those 2 weeks.

Example 2. You and your neighbors are co-owners of a house under a shared equity financing agreement. Your neighbors live in the house and pay you a fair rental price.

Even though your neighbors have an interest in the house, the days your neighbors live there are not counted as days of personal use by you. This is because your neighbors rent the house as their main home under a shared equity financing agreement.

Example 3. You own a rental property that you rent to your son. Your son does not own any interest in this property. He uses it as his main home and pays you a fair rental price.

Your son’s use of the property is not personal use by you because your son is using it as his main home, he owns no interest in the property, and he is paying you a fair rental price.

Example 4. You rent your beach house to Joshua. Joshua rents his cabin in the mountains to you. You each pay a fair rental price.

You are using your house for personal purposes on the days that Joshua uses it because your house is used by Joshua under an arrangement that allows you to use his house.

Example 5.You rent an apartment to your mother at less than a fair rental price. You are using the apartment for personal purposes on the days that your mother rents it because you rent it for less than a fair rental price.

Days used for repairs and maintenance. Any day that you spend working substantially full-time repairing and maintaining (not improving) your property is not counted as a day of personal use. Do not count such a day as a day of personal use even if family members use the property for recreational purposes on the same day.

Days used as a main home before or after renting. For purposes of determining whether a dwelling unit was used as a home, you may not have to count days you used the property as your main home before or after renting it or offering it for rent as days of personal use. Do not count them as days of personal use if:

You rented or tried to rent the property for 12 or more consecutive months.

You rented or tried to rent the property for a period of less than 12 consecutive months and the period ended because you sold or exchanged the property.

However, this special rule does not apply when dividing expenses between rental and personal use.

Examples. The following examples show how to determine whether you used your rental property as a home.

Example 1. You converted the basement of your home into an apartment with a bedroom, a bathroom, and a small kitchen. You rented the basement apartment at a fair rental price to college students during the regular school year. You rented to them on a 9-month lease (273 days). You figured 10% of the total days rented to others at a fair rental price is 27 days.

During June (30 days), your brothers stayed with you and lived in the basement apartment rent free.

Your basement apartment was used as a home because you used it for personal purposes for 30 days. Rent-free use by your brothers is considered personal use. Your personal use (30 days) is more than the greater of 14 days or 10% of the total days it was rented (27 days).

Example 2. You rented the guest bedroom in your home at a fair rental price during the local college’s homecoming, commencement, and football weekends (a total of 27 days). Your sister-in-law stayed in the room, rent free, for the last 3 weeks (21 days) in July. You figured 10% of the total days rented to others at a fair rental price is 3 days.

The room was used as a home because you used it for personal purposes for 21 days. That is more than the greater of 14 days or 10% of the 27 days it was rented (3 days).

Example 3. You own a condominium apartment in a resort area. You rented it at a fair rental price for a total of 170 days during the year. For 12 of those days, the tenant was not able to use the apartment and allowed you to use it even though you did not refund any of the rent. Your family actually used the apartment for 10 of those days. Therefore, the apartment is treated as having been rented for 160 (170 − 10) days. You figured 10% of the total days rented to others at a fair rental price is 16 days. Your family also used the apartment for 7 other days during the year.

You used the apartment as a home because you used it for personal purposes for 17 days. That is more than the greater of 14 days or 10% of the 160 days it was rented (16 days).

Minimal rental use. If you use the dwelling unit as a home and you rent it less than 15 days during the year, that period is not treated as rental activity. See Used as a home but rented less than 15 days, later, for more information.

Limit on deductions. Renting a dwelling unit that is considered a home is not a passive activity. Instead, if your rental expenses are more than your rental income, some or all of the excess expenses cannot be used to offset income from other sources. The excess expenses that cannot be used to offset income from other sources are carried forward to the next year and treated as rental expenses for the same property. Any expenses carried forward to the next year will be subject to any limits that apply for that year. This limitation will apply to expenses carried forward to another year even if you do not use the property as your home for that subsequent year.

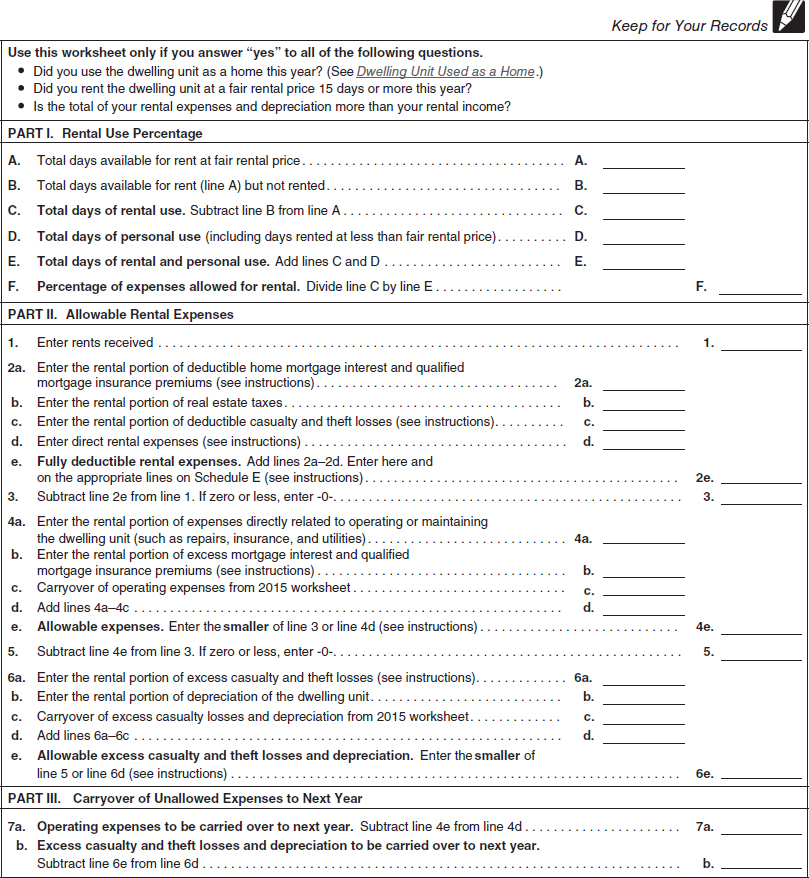

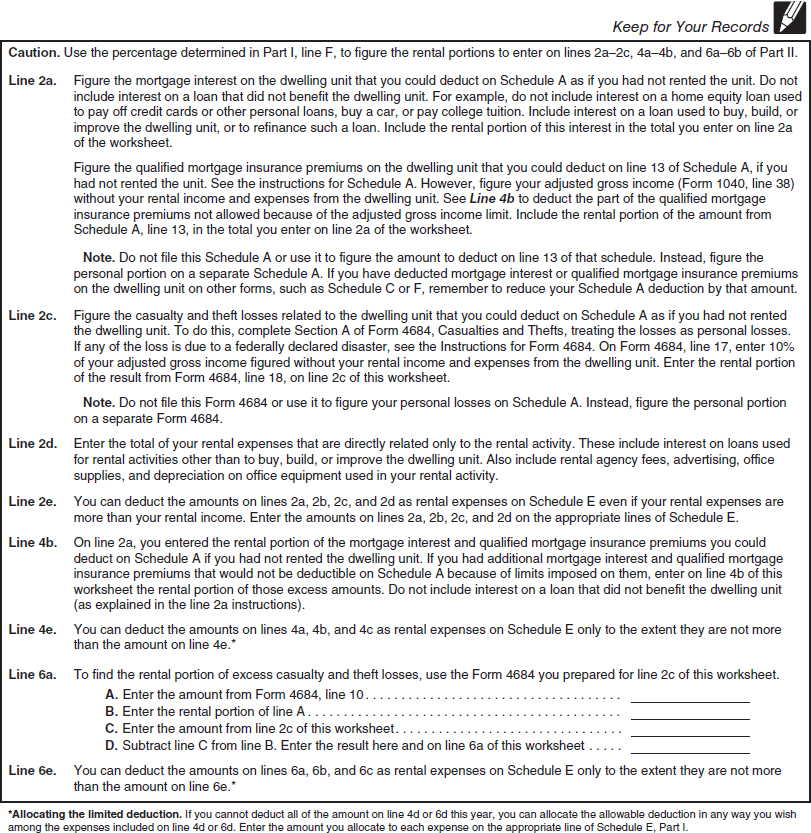

To figure your deductible rental expenses for this year and any carryover to next year, use Worksheet 9-1.

Worksheet 9-1. Worksheet for Figuring Rental Deductions for a Dwelling Unit Used as a Home

Reporting Income and Deductions

Property not used for personal purposes. If you do not use a dwelling unit for personal purposes, see How To Report Rental Income and Expenses, later, for how to report your rental income and expenses.

Property used for personal purposes. If you do use a dwelling unit for personal purposes, then how you report your rental income and expenses depends on whether you used the dwelling unit as a home.

Not used as a home. If you use a dwelling unit for personal purposes, but not as a home, report all the rental income in your income. Since you used the dwelling unit for personal purposes, you must divide your expenses between the rental use and the personal use as described earlier in Dividing Expenses. The expenses for personal use are not deductible as rental expenses.

Your deductible rental expenses can be more than your gross rental income; however, see Limits on Rental Losses, later.

Used as a home but rented less than 15 days. If you use a dwelling unit as a home and you rent it less than 15 days during the year, its primary function is not considered to be rental and it should not be reported on Schedule E (Form 1040). You are not required to report the rental income and rental expenses from this activity. The expenses, including qualified mortgage interest, property taxes, and any qualified casualty loss will be reported as normally allowed on Schedule A (Form 1040). See the Instructions for Schedule A (Form 1040) for more information on deducting these expenses.

Used as a home and rented 15 days or more. If you use a dwelling unit as a home and rent it 15 days or more during the year, include all your rental income in your income. Since you used the dwelling unit for personal purposes, you must divide your expenses between the rental use and the personal use as described earlier in Dividing Expenses. The expenses for personal use are not deductible as rental expenses.

If you had a net profit from renting the dwelling unit for the year (that is, if your rental income is more than the total of your rental expenses, including depreciation), deduct all of your rental expenses. You do not need to use Worksheet 9-1.

However, if you had a net loss from renting the dwelling unit for the year, your deduction for certain rental expenses is limited. To figure your deductible rental expenses and any carryover to next year, use Worksheet 9-1.

Tangible Property Regulations

Depreciation

You recover the cost of income-producing property through yearly tax deductions. You do this by depreciating the property; that is, by deducting some of the cost each year on your tax return.

Three factors determine how much depreciation you can deduct each year: (1) your basis in the property, (2) the recovery period for the property, and (3) the depreciation method used. You cannot simply deduct your mortgage or principal payments, or the cost of furniture, fixtures, and equipment, as an expense.

You can deduct depreciation only on the part of your property used for rental purposes. Depreciation reduces your basis for figuring gain or loss on a later sale or exchange.

Alternative minimum tax (AMT). If you use accelerated depreciation, you may be subject to the AMT. Accelerated depreciation allows you to deduct more depreciation earlier in the recovery period than you could deduct using a straight-line method (same deduction each year).

Claiming the correct amount of depreciation. You should claim the correct amount of depreciation each tax year. If you did not claim all the depreciation you were entitled to deduct, you must still reduce your basis in the property by the full amount of depreciation that you could have deducted.

If you deducted an incorrect amount of depreciation for property in any year, you may be able to make a correction by filing Form 1040X, Amended U.S. Individual Income Tax Return. If you are not allowed to make the correction on an amended return, you can change your accounting method to claim the correct amount of depreciation. See Claiming the correct amount of depreciation in chapter 2 of Pub. 527 for more information.

Changing your accounting method to deduct unclaimed depreciation. To change your accounting method, you generally must file Form 3115, Application for Change in Accounting Method, to get the consent of the IRS. In some instances, that consent is automatic. For more information, see chapter 1 of Pub. 946.

Land. You cannot depreciate the cost of land because land generally does not wear out, become obsolete, or get used up. The costs of clearing, grading, planting, and landscaping are usually all part of the cost of land and cannot be depreciated.

More information. See Pub. 527 for more information about depreciating rental property and see Pub. 946 for more information about depreciation.

Limits on Rental Losses

If you have a loss from your rental real estate activity, two sets of rules may limit the amount of loss you can deduct. You must consider these rules in the order shown below.

At-risk rules. These rules are applied first if there is investment in your rental real estate activity for which you are not at risk. This applies only if the real property was placed in service after 1986.

Passive activity limits. Generally, rental real estate activities are considered passive activities and losses are not deductible unless you have income from other passive activities to offset them. However, there are exceptions.

At-Risk Rules

You may be subject to the at-risk rules if you have:

A loss from an activity carried on as a trade or business or for the production of income, and

Amounts invested in the activity for which you are not fully at risk.

Losses from holding real property (other than mineral property) placed in service before 1987 are not subject to the at-risk rules.

In most cases, any loss from an activity subject to the at-risk rules is allowed only to the extent of the total amount you have at risk in the activity at the end of the tax year. You are considered at risk in an activity to the extent of cash and the adjusted basis of other property you contributed to the activity and certain amounts borrowed for use in the activity. See Pub. 925 for more information.

Passive Activity Limits

In most cases, all rental real estate activities (except those of certain real estate professionals, discussed later) are passive activities. For this purpose, a rental activity is an activity from which you receive income mainly for the use of tangible property, rather than for services.

Limits on passive activity deductions and credits. Deductions or losses from passive activities are limited. You generally cannot offset income, other than passive income, with losses from passive activities. Nor can you offset taxes on income, other than passive income, with credits resulting from passive activities. Any excess loss or credit is carried forward to the next tax year.

For a detailed discussion of these rules, see Pub. 925.

You may have to complete Form 8582 to figure the amount of any passive activity loss for the current tax year for all activities and the amount of the passive activity loss allowed on your tax return.

Real estate professionals. Rental activities in which you materially participated during the year are not passive activities if, for that year, you were a real estate professional. For a detailed discussion of the requirements, see Pub. 527. For a detailed discussion of material participation, see Pub. 925.

Exception for Personal Use of Dwelling Unit

If you used the rental property as a home during the year, any income, deductions, gain, or loss allocable to such use shall not be taken into account for purposes of the passive activity loss limitation. Instead, follow the rules explained in Personal Use of Dwelling Unit (Including Vacation Home), earlier.

Exception for Rental Real Estate Activities With Active Participation

If you or your spouse actively participated in a passive rental real estate activity, you may be able to deduct up to $25,000 of loss from the activity from your nonpassive income. This special allowance is an exception to the general rule disallowing losses in excess of income from passive activities. Similarly, you may be able to offset credits from the activity against the tax on up to $25,000 of nonpassive income after taking into account any losses allowed under this exception.

Active participation. You actively participated in a rental real estate activity if you (and your spouse) owned at least 10% of the rental property and you made management decisions or arranged for others to provide services (such as repairs) in a significant and bona fide sense. Management decisions that may count as active participation include approving new tenants, deciding on rental terms, approving expenditures, and similar decisions.

Maximum special allowance. The maximum special allowance is:

$25,000 for single individuals and married individuals filing a joint return for the tax year,

$12,500 for married individuals who file separate returns for the tax year and lived apart from their spouses at all times during the tax year, and

$25,000 for a qualifying estate reduced by the special allowance for which the surviving spouse qualified.

If your modified adjusted gross income (MAGI) is $100,000 or less ($50,000 or less if married filing separately), you can deduct your loss up to the amount specified above. If your MAGI is more than $100,000 (more than $50,000 if married filing separately), your special allowance is limited to 50% of the difference between $150,000 ($75,000 if married filing separately) and your MAGI.

Generally, if your MAGI is $150,000 or more ($75,000 or more if you are married filing separately), there is no special allowance.

More information. See Pub. 925 for more information on the passive loss limits, including information on the treatment of unused disallowed passive losses and credits and the treatment of gains and losses realized on the disposition of a passive activity.

How To Report Rental Income and Expenses

The basic form for reporting residential rental income and expenses is Schedule E (Form 1040). However, do not use that schedule to report a not-for-profit activity. See Not Rented for Profit, earlier.

Providing substantial services. If you provide substantial services that are primarily for your tenant’s convenience, such as regular cleaning, changing linen, or maid service, report your rental income and expenses on Schedule C (Form 1040), Profit or Loss From Business, or Schedule C-EZ (Form 1040), Net Profit From Business (Sole Proprietorship). Substantial services do not include the furnishing of heat and light, cleaning of public areas, trash collection, etc. For information, see Pub. 334, Tax Guide for Small Business. You also may have to pay self-employment tax on your rental income using Schedule SE (Form 1040), Self-Employment Tax.

Use Form 1065, U.S. Return of Partnership Income, if your rental activity is a partnership (including a partnership with your spouse unless it is a qualified joint venture).

Qualified joint venture. If you and your spouse each materially participate as the only members of a jointly owned and operated real estate business, and you file a joint return for the tax year, you can make a joint election to be treated as a qualified joint venture instead of a partnership. This election, in most cases, will not increase the total tax owed on the joint return, but it does give each of you credit for social security earnings on which retirement benefits are based and for Medicare coverage if your rental income is subject to self-employment tax. For more information, see Pub. 527.

Form 1098, Mortgage Interest Statement. If you paid $600 or more of mortgage interest on your rental property to any one person, you should receive a Form 1098, or similar statement showing the interest you paid for the year. If you and at least one other person (other than your spouse if you file a joint return) were liable for, and paid interest, on the mortgage, and the other person received the Form 1098, report your share of the interest on Schedule E (Form 1040), line 13. Attach a statement to your return showing the name and address of the other person. See the instructions for Schedule E (Form 1040) for more information.

Interest expense. You can deduct mortgage interest you pay on your rental property. When you refinance a rental property for more than the previous outstanding balance, the portion of the interest allocable to loan proceeds not related to rental use generally cannot be deducted as a rental expense. Chapter 4 of Pub. 535 explains mortgage interest in detail.

Expenses paid to obtain a mortgage. Certain expenses you pay to obtain a mortgage on your rental property cannot be deducted as interest. These expenses, which include mortgage commissions, abstract fees, and recording fees, are capital expenses that are part of your basis in the property.

Schedule E (Form 1040)

If you rent buildings, rooms, or apartments, and provide basic services such as heat and light, trash collection, etc., you normally report your rental income and expenses on Schedule E, Part I.

Page 2 of Schedule E is used to report income or loss from partnerships, S corporations, estates, trusts, and real estate mortgage investment conduits. If you need to use page 2 of Schedule E, be sure to use page 2 of the same Schedule E you used to enter your rental activity on page 1. See the instructions for Schedule E (Form 1040).

527 Residential Rental Property

527 Residential Rental Property