Chapter 4

Tax withholding and estimated tax

What’s New for 2018

Tax law changes for 2018. When you figure how much income tax you want withheld from your pay and when you figure your estimated tax, consider tax law changes effective in 2018. For more information, see Pub. 505, Tax Withholding and Estimated Tax.

Reminders

Estimated tax safe harbor for higher income taxpayers. If your 2017 adjusted gross income was more than $150,000 ($75,000 if you are married filing a separate return), you must pay the smaller of 90% of your expected tax for 2018 or 110% of the tax shown on your 2017 return to avoid an estimated tax penalty.

Introduction

This chapter discusses how to pay your tax as you earn or receive income during the year. In general, the federal income tax is a pay-as-you-go tax. There are two ways to pay as you go.

- Withholding. If you are an employee, your employer probably withholds income tax from your pay. Tax also may be withheld from certain other income, such as pensions, bonuses, commissions, and gambling winnings. The amount withheld is paid to the IRS in your name.

- Estimated tax. If you do not pay your tax through withholding, or do not pay enough tax that way, you may have to pay estimated tax. People who are in business for themselves generally will have to pay their tax this way. Also, you may have to pay estimated tax if you receive income such as dividends, interest, capital gains, rent, and royalties. Estimated tax is used to pay not only income tax, but self-employment tax and alternative minimum tax as well.

This chapter explains these methods. In addition, it also explains the following.

- Credit for withholding and estimated tax. When you file your 2017 income tax return, take credit for all the income tax withheld from your salary, wages, pensions, etc., and for the estimated tax you paid for 2017. Also take credit for any excess social security or railroad retirement tax withheld (discussed in chapter 38).

- Underpayment penalty. If you did not pay enough tax during the year, either through withholding or by making estimated tax payments, you may have to pay a penalty. In most cases, the IRS can figure this penalty for you. See Underpayment Penalty for 2017, at the end of this chapter.

Useful Items

You may want to see:

Publication

505 Tax Withholding and Estimated Tax

505 Tax Withholding and Estimated Tax

Form (and Instructions)

- W-4 Employee’s Withholding Allowance Certificate

- W-4P Withholding Certificate for Pension or Annuity Payments

- W-4S Request for Federal Income Tax Withholding From Sick Pay

- W-4V Voluntary Withholding Request

- 1040-ES Estimated Tax for Individuals

- 2210 Underpayment of Estimated Tax by Individuals, Estates, and Trusts

- 2210-F Underpayment of Estimated Tax by Farmers and Fishermen

Tax Withholding for 2018

This section discusses income tax withholding on:

- Salaries and wages,

- Tips,

- Taxable fringe benefits,

- Sick pay,

- Pensions and annuities,

- Gambling winnings,

- Unemployment compensation, and

- Certain federal payments.

This section explains the rules for withholding tax from each of these types of income.

This section also covers backup withholding on interest, dividends, and other payments.

Salaries and Wages

Income tax is withheld from the pay of most employees. Your pay includes your regular pay, bonuses, commissions, and vacation allowances. It also includes reimbursements and other expense allowances paid under a nonaccountable plan. See Supplemental Wages, later, for more information about reimbursements and allowances paid under a nonaccountable plan. If your income is low enough that you will not have to pay income tax for the year, you may be exempt from withholding. This is explained under Exemption From Withholding, later.

You can ask your employer to withhold income tax from noncash wages and other wages not subject to withholding. If your employer does not agree to withhold tax, or if not enough is withheld, you may have to pay estimated tax, as discussed later under Estimated Tax for 2018.

Military retirees. Military retirement pay is treated in the same manner as regular pay for income tax withholding purposes, even though it is treated as a pension or annuity for other tax purposes.

Household workers. If you are a household worker, you can ask your employer to withhold income tax from your pay. A household worker is an employee who performs household work in a private home, local college club, or local fraternity or sorority chapter. Tax is withheld only if you want it withheld and your employer agrees to withhold it. If you do not have enough income tax withheld, you may have to pay estimated tax, as discussed later under Estimated Tax for 2018.

Farmworkers. Generally, income tax is withheld from your cash wages for work on a farm unless your employer does both of these:

- Pays you cash wages of less than $150 during the year, and

- Has expenditures for agricultural labor totaling less than $2,500 during the year.

Differential wage payments. When employees are on leave from employment for military duty, some employers make up the difference between the military pay and civilian pay. Payments to an employee who is on active duty for a period of more than 30 days will be subject to income tax withholding, but not subject to social security, Medicare, or federal unemployment (FUTA) tax withholding. The wages and withholding will be reported on Form W-2, Wage and Tax Statement.

Determining Amount of Tax Withheld Using Form W-4

The amount of income tax your employer withholds from your regular pay depends on two things.

- The amount you earn in each payroll period.

- The information you give your employer on Form W-4.

Form W-4 includes four types of information that your employer will use to figure your withholding.

- Whether to withhold at the single rate or at the lower married rate.

- How many withholding allowances you claim (each allowance reduces the amount withheld).

- Whether you want an additional amount withheld.

- Whether you are claiming an exemption from withholding in 2018. See Exemption From Withholding, later.

Note. You must specify a filing status and a number of withholding allowances on Form W-4. You cannot specify only a dollar amount of withholding.

New Job

When you start a new job, you must fill out Form W-4 and give it to your employer. Your employer should have copies of the form. If you need to change the information later, you must fill out a new form. If you work only part of the year (for example, you start working after the beginning of the year), too much tax may be withheld. You may be able to avoid over-withholding if your employer agrees to use the part-year method. See Part-Year Method in chapter 1 of Pub. 505 for more information.

Employee also receiving pension income. If you receive pension or annuity income and begin a new job, you will need to file Form W-4 with your new employer. However, you can choose to split your withholding allowances between your pension and job in any manner.

Changing Your Withholding

During the year changes may occur to your marital status, exemptions, adjustments, deductions, or credits you expect to claim on your tax return. When this happens, you may need to give your employer a new Form W-4 to change your withholding status or your number of allowances.

If the changes reduce the number of allowances you are claiming or change your marital status from married to single, you must give your employer a new Form W-4 within 10 days.

Generally, you can submit a new Form W-4 whenever you wish to change the number of your withholding allowances for any other reason.

Changing your withholding for 2019. If events in 2018 will decrease the number of your withholding allowances for 2019, you must give your employer a new Form W-4 by December 1, 2018. If the event occurs in December 2018, submit a new Form W-4 within 10 days.

Checking Your Withholding

After you have given your employer a Form W-4, you can check to see whether the amount of tax withheld from your pay is too little or too much. If too much or too little tax is being withheld, you should give your employer a new Form W-4 to change your withholding. You should try to have your withholding match your actual tax liability. If not enough tax is withheld, you will owe tax at the end of the year and may have to pay interest and a penalty. If too much tax is withheld, you will lose the use of that money until you get your refund. Always check your withholding if there are personal or financial changes in your life or changes in the law that might change your tax liability.

Note. You cannot give your employer a payment to cover withholding on salaries and wages for past pay periods or a payment for estimated tax.

Completing Form W-4 and Worksheets

Form W-4 has worksheets to help you figure how many withholding allowances you can claim. The worksheets are for your own records. Do not give them to your employer.

Multiple jobs. If you have income from more than one job at the same time, complete only one set of Form W-4 worksheets. Then split your allowances between the Forms W-4 for each job. You cannot claim the same allowances with more than one employer at the same time. You can claim all your allowances with one employer and none with the other(s), or divide them any other way.

Married individuals. If both you and your spouse are employed and expect to file a joint return, figure your withholding allowances using your combined income, adjustments, deductions, exemptions, and credits. Use only one set of worksheets. You can divide your total allowances any way, but you cannot claim an allowance that your spouse also claims.

If you and your spouse expect to file separate returns, figure your allowances using separate worksheets based on your own individual income, adjustments, deductions, exemptions, and credits.

Alternative method of figuring withholding allowances. You do not have to use the Form W-4 worksheets if you use a more accurate method of figuring the number of withholding allowances. For more information, see Alternative method of figuring withholding allowances under Completing Form W-4 and Worksheets in Pub. 505, chapter 1.

Personal Allowances Worksheet. Use the Personal Allowances Worksheet on Form W-4 to figure your withholding allowances based on exemptions and any special allowances that apply.

Deduction and Adjustments Worksheet. Use the Deduction and Adjustments Worksheet on Form W-4 if you plan to itemize your deductions, claim certain credits, or claim adjustments to the income on your 2018 tax return and you want to reduce your withholding. Also, complete this worksheet when you have changes to these items to see if you need to change your withholding.

Two-Earners/Multiple Jobs Worksheet. You may need to complete the Two-Earners/Multiple Jobs Worksheet on Form W-4 if you have more than one job, a working spouse, or are also receiving a pension. Also, on this worksheet you can add any additional withholding necessary to cover any amount you expect to owe other than income tax, such as self-employment tax.

Getting the Right Amount of Tax Withheld

In most situations, the tax withheld from your pay will be close to the tax you figure on your return if you follow these two rules.

- You accurately complete all the Form W-4 worksheets that apply to you.

- You give your employer a new Form W-4 when changes occur.

But because the worksheets and withholding methods do not account for all possible situations, you may not be getting the right amount withheld. This is most likely to happen in the following situations.

- You are married and both you and your spouse work.

- You have more than one job at a time.

- You have nonwage income, such as interest, dividends, alimony, unemployment compensation, or self-employment income.

- You will owe additional amounts with your return, such as self-employment tax.

- Your withholding is based on obsolete Form W-4 information for a substantial part of the year.

- Your earnings are more than the amount shown under Check your withholding in the instructions at the top of page 1 of Form W-4.

- You work only part of the year.

- You change the number of your withholding allowances during the year.

Cumulative wage method. If you change the number of your withholding allowances during the year, too much or too little tax may have been withheld for the period before you made the change. You may be able to compensate for this if your employer agrees to use the cumulative wage withholding method for the rest of the year. You must ask your employer in writing to use this method.

To be eligible, you must have been paid for the same kind of payroll period (weekly, biweekly, etc.) since the beginning of the year.

Publication 505

To make sure you are getting the right amount of tax withheld, get Pub. 505. It will help you compare the total tax to be withheld during the year with the tax you can expect to figure on your return. It also will help you determine how much, if any, additional withholding is needed each payday to avoid owing tax when you file your return. If you do not have enough tax withheld, you may have to pay estimated tax, as explained under Estimated Tax for 2018, later.

Rules Your Employer Must Follow

It may be helpful for you to know some of the withholding rules your employer must follow. These rules can affect how to fill out your Form W-4 and how to handle problems that may arise.

New Form W-4. When you start a new job, your employer should have you complete a Form W-4. Beginning with your first payday, your employer will use the information you give on the form to figure your withholding.

If you later fill out a new Form W-4, your employer can put it into effect as soon as possible. The deadline for putting it into effect is the start of the first payroll period ending 30 or more days after you turn it in.

No Form W-4. If you do not give your employer a completed Form W-4, your employer must withhold at the highest rate, as if you were single and claimed no withholding allowances.

Repaying withheld tax. If you find you are having too much tax withheld because you did not claim all the withholding allowances you are entitled to, you should give your employer a new Form W-4. Your employer cannot repay any of the tax previously withheld. Instead, claim the full amount withheld when you file your tax return.

However, if your employer has withheld more than the correct amount of tax for the Form W-4 you have in effect, you do not have to fill out a new Form W-4 to have your withholding lowered to the correct amount. Your employer can repay the amount that was withheld incorrectly. If you are not repaid, your Form W-2 will reflect the full amount actually withheld, which you would claim when you file your tax return.

Exemption From Withholding

If you claim exemption from withholding, your employer will not withhold federal income tax from your wages. The exemption applies only to income tax, not to social security, Medicare, or FUTA tax withholding.

You can claim exemption from withholding for 2018 only if both of the following situations apply.

- For 2017 you had a right to a refund of all federal income tax withheld because you had no tax liability.

- For 2018 you expect a refund of all federal income tax withheld because you expect to have no tax liability.

Students. If you are a student, you are not automatically exempt. See chapter 1 to find out if you must file a return. If you work only part time or only during the summer, you may qualify for exemption from withholding.

Age 65 or older or blind. If you are 65 or older or blind, use Worksheet 1-3 or 1-4 in chapter 1 of Pub. 505, to help you decide if you qualify for exemption from withholding. Do not use either worksheet if you will itemize deductions, claim exemptions for dependents, or claim tax credits on your 2018 return. Instead, see Itemizing deductions or claiming exemptions or credits in chapter 1 of Pub. 505.

Claiming exemption from withholding. To claim exemption, you must give your employer a Form W-4. Do not complete lines 5 and 6. Enter “Exempt” on line 7.

If you claim exemption, but later your situation changes so that you will have to pay income tax after all, you must file a new Form W-4 within 10 days after the change. If you claim exemption in 2018, but you expect to owe income tax for 2019, you must file a new Form W-4 by December 1, 2018.

Your claim of exempt status may be reviewed by the IRS.

An exemption is good for only 1 year. You must give your employer a new Form W-4 by February 15 each year to continue your exemption.

Supplemental Wages

Supplemental wages include bonuses, commissions, overtime pay, vacation allowances, certain sick pay, and expense allowances under certain plans. The payer can figure withholding on supplemental wages using the same method used for your regular wages. However, if these payments are identified separately from your regular wages, your employer or other payer of supplemental wages can withhold income tax from these wages at a flat rate.

Expense allowances. Reimbursements or other expense allowances paid by your employer under a nonaccountable plan are treated as supplemental wages.

Reimbursements or other expense allowances paid under an accountable plan that are more than your proven expenses are treated as paid under a nonaccountable plan if you do not return the excess payments within a reasonable period of time.

For more information about accountable and nonaccountable expense allowance plans, see Reimbursements in chapter 27.

Penalties

You may have to pay a penalty of $500 if both of the following apply.

- You make statements or claim withholding allowances on your Form W-4 that reduce the amount of tax withheld.

- You have no reasonable basis for those statements or allowances at the time you prepare your Form W-4.

There is also a criminal penalty for willfully supplying false or fraudulent information on your Form W-4 or for willfully failing to supply information that would increase the amount withheld. The penalty upon conviction can be either a fine of up to $1,000 or imprisonment for up to 1 year, or both.

These penalties will apply if you deliberately and knowingly falsify your Form W-4 in an attempt to reduce or eliminate the proper withholding of taxes. A simple error or an honest mistake will not result in one of these penalties. For example, a person who has tried to figure the number of withholding allowances correctly, but claims seven when the proper number is six, will not be charged a W-4 penalty.

Tips

The tips you receive while working on your job are considered part of your pay. You must include your tips on your tax return on the same line as your regular pay. However, tax is not withheld directly from tip income, as it is from your regular pay. Nevertheless, your employer will take into account the tips you report when figuring how much to withhold from your regular pay.

See chapter 6 for information on reporting your tips to your employer. For more information on the withholding rules for tip income, see Pub. 531, Reporting Tip Income.

How employer figures amount to withhold. The tips you report to your employer are counted as part of your income for the month you report them. Your employer can figure your withholding in either of two ways.

- By withholding at the regular rate on the sum of your pay plus your reported tips.

- By withholding at the regular rate on your pay plus a percentage of your reported tips.

Not enough pay to cover taxes. If your regular pay is not enough for your employer to withhold all the tax (including income tax and social security and Medicare taxes (or the equivalent railroad retirement tax)) due on your pay plus your tips, you can give your employer money to cover the shortage. See Giving your employer money for taxes in chapter 6.

Allocated tips. Your employer should not withhold income tax, Medicare tax, social security tax, or railroad retirement tax on any allocated tips. Withholding is based only on your pay plus your reported tips. Your employer should refund to you any incorrectly withheld tax. See Allocated Tips in chapter 6 for more information.

Taxable Fringe Benefits

The value of certain noncash fringe benefits you receive from your employer is considered part of your pay. Your employer generally must withhold income tax on these benefits from regular pay.

For information on fringe benefits, see Fringe Benefits under Employee Compensation in chapter 5.

Although the value of your personal use of an employer-provided car, truck, or other highway motor vehicle is taxable, your employer can choose not to withhold income tax on that amount. Your employer must notify you if this choice is made.

For more information on withholding on taxable fringe benefits, see chapter 1 of Pub. 505.

Sick Pay

Sick pay is a payment to you to replace your regular wages while you are temporarily absent from work due to sickness or personal injury. To qualify as sick pay, it must be paid under a plan to which your employer is a party.

If you receive sick pay from your employer or an agent of your employer, income tax must be withheld. An agent who does not pay regular wages to you may choose to withhold income tax at a flat rate.

However, if you receive sick pay from a third party who is not acting as an agent of your employer, income tax will be withheld only if you choose to have it withheld. See Form W-4S, later.

If you receive payments under a plan in which your employer does not participate (such as an accident or health plan where you paid all the premiums), the payments are not sick pay and usually are not taxable.

Union agreements. If you receive sick pay under a collective bargaining agreement between your union and your employer, the agreement may determine the amount of income tax withholding. See your union representative or your employer for more information.

Form W-4S. If you choose to have income tax withheld from sick pay paid by a third party, such as an insurance company, you must fill out Form W-4S. Its instructions contain a worksheet you can use to figure the amount you want withheld. They also explain restrictions that may apply. Give the completed form to the payer of your sick pay. The payer must withhold according to your directions on the form.

Estimated tax. If you do not request withholding on Form W-4S, or if you do not have enough tax withheld, you may have to make estimated tax payments. If you do not pay enough tax, either through estimated tax or withholding, or a combination of both, you may have to pay a penalty. See Underpayment Penalty for 2017, at the end of this chapter.

Pensions and Annuities

Income tax usually will be withheld from your pension or annuity distributions unless you choose not to have it withheld. This rule applies to distributions from:

- A traditional individual retirement arrangement (IRA);

- A life insurance company under an endowment, annuity, or life insurance contract;

- A pension, annuity, or profit-sharing plan;

- A stock bonus plan; and

- Any other plan that defers the time you receive compensation.

The amount withheld depends on whether you receive payments spread out over more than 1 year (periodic payments), within 1 year (nonperiodic payments), or as an eligible rollover distribution (ERD). Income tax withholding from an ERD is mandatory.

More information. For more information on taxation of annuities and distributions (including ERDs) from qualified retirement plans, see chapter 10. For information on IRAs, see chapter 17. For more information on withholding on pensions and annuities, including a discussion of Form W-4P, see Pensions and Annuities in chapter 1 of Pub. 505.

Gambling Winnings

Income tax is withheld at a flat 25% rate from certain kinds of gambling winnings.

Gambling winnings of more than $5,000 from the following sources are subject to income tax withholding.

- Any sweepstakes; wagering pool, including payments made to winners of poker tournaments; or lottery.

- Any other wager, if the proceeds are at least 300 times the amount of the bet.

It does not matter whether your winnings are paid in cash, in property, or as an annuity. Winnings not paid in cash are taken into account at their fair market value.

Exception. Gambling winnings from bingo, keno, and slot machines generally are not subject to income tax withholding. However, you may need to provide the payer with a social security number to avoid withholding. See Backup withholding on gambling winnings in chapter 1 of Pub. 505. If you receive gambling winnings not subject to withholding, you may need to pay estimated tax. See Estimated Tax for 2018, later.

If you do not pay enough tax, either through withholding or estimated tax, or a combination of both, you may have to pay a penalty. See Underpayment Penalty for 2017, at the end of this chapter.

Form W-2G. If a payer withholds income tax from your gambling winnings, you should receive a Form W-2G, Certain Gambling Winnings, showing the amount you won and the amount withheld. Report the tax withheld on line 64 of Form 1040.

Unemployment Compensation

You can choose to have income tax withheld from unemployment compensation. To make this choice, fill out Form W-4V (or a similar form provided by the payer) and give it to the payer.

All unemployment compensation is taxable. If you do not have income tax withheld, you may have to pay estimated tax. See Estimated Tax for 2018, later.

If you do not pay enough tax, either through withholding or estimated tax, or a combination of both, you may have to pay a penalty. For information, see Underpayment Penalty for 2017, at the end of this chapter.

Federal Payments

You can choose to have income tax withheld from certain federal payments you receive. These payments are:

- Social security benefits,

- Tier 1 railroad retirement benefits,

- Commodity credit corporation loans you choose to include in your gross income,

- Payments under the Agricultural Act of 1949 (7 U.S.C. 1421 et. Seq.), as amended, or title II of the Disaster Assistance Act of 1988, that are treated as insurance proceeds and that you receive because:

- Your crops were destroyed or damaged by drought, flood, or any other natural disaster, or

- You were unable to plant crops because of a natural disaster described in (a), and

- Any other payment under federal law as determined by the Secretary.

To make this choice, fill out Form W-4V (or a similar form provided by the payer) and give it to the payer.

If you do not choose to have income tax withheld, you may have to pay estimated tax. See Estimated Tax for 2018, later.

If you do not pay enough tax, either through withholding or estimated tax, or a combination of both, you may have to pay a penalty. For information, see Underpayment Penalty for 2017, at the end of this chapter.

More information. For more information about the tax treatment of social security and railroad retirement benefits, see chapter 11. Get Pub. 225, Farmer’s Tax Guide, for information about the tax treatment of commodity credit corporation loans or crop disaster payments.

Backup Withholding

Banks or other businesses that pay you certain kinds of income must file an information return (Form 1099) with the IRS. The information return shows how much you were paid during the year. It also includes your name and taxpayer identification number (TIN). TINs are explained in chapter 1 under Social Security Number (SSN). These payments generally are not subject to withholding. However, “backup” withholding is required in certain situations. Backup withholding can apply to most kinds of payments that are reported on Form 1099.

The payer must withhold at a flat 28% rate in the following situations.

- You do not give the payer your TIN in the required manner.

- The IRS notifies the payer that the TIN you gave is incorrect.

- You are required, but fail, to certify that you are not subject to backup withholding.

- The IRS notifies the payer to start withholding on interest or dividends because you have underreported interest or dividends on your income tax return. The IRS will do this only after it has mailed you four notices over at least a 210-day period.

See Backup Withholding in chapter 1 of Pub. 505 for more information.

Penalties. There are civil and criminal penalties for giving false information to avoid backup withholding. The civil penalty is $500. The criminal penalty, upon conviction, is a fine of up to $1,000 or imprisonment of up to 1 year, or both.

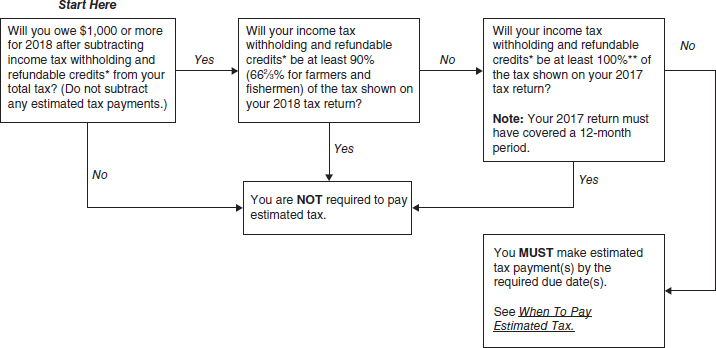

Estimated Tax for 2018

Estimated tax is the method used to pay tax on income that is not subject to withholding. This includes income from self-employment, interest, dividends, alimony, rent, gains from the sale of assets, prizes, and awards. You also may have to pay estimated tax if the amount of income tax being withheld from your salary, pension, or other income is not enough.

Estimated tax is used to pay both income tax and self-employment tax, as well as other taxes and amounts reported on your tax return. If you do not pay enough tax, either through withholding or estimated tax, or a combination of both, you may have to pay a penalty. If you do not pay enough by the due date of each payment period (see When To Pay Estimated Tax, later), you may be charged a penalty even if you are due a refund when you file your tax return. For information on when the penalty applies, see Underpayment Penalty for 2017, at the end of this chapter.

Who Does Not Have To Pay Estimated Tax

If you receive salaries or wages, you can avoid having to pay estimated tax by asking your employer to take more tax out of your earnings. To do this, give a new Form W-4 to your employer. See chapter 1 of Pub. 505.

Estimated tax not required. You do not have to pay estimated tax for 2018 if you meet all three of the following conditions.

- You had no tax liability for 2017.

- You were a U.S. citizen or resident alien for the whole year.

- Your 2017 tax year covered a 12-month period.

You had no tax liability for 2017 if your total tax was zero or you did not have to file an income tax return. For the definition of “total tax” for 2017, see Pub. 505, chapter 2.

Who Must Pay Estimated Tax

If you owe additional tax for 2017, you may have to pay estimated tax for 2018.

You can use the following general rule as a guide during the year to see if you will have enough withholding, or if you should increase your withholding or make estimated tax payments.

General rule. In most cases, you must pay estimated tax for 2018 if both of the following apply.

- You expect to owe at least $1,000 in tax for 2018, after subtracting your withholding and refundable credits.

- You expect your withholding plus your refundable credits to be less than the smaller of:

- 90% of the tax to be shown on your 2018 tax return, or

- 100% of the tax shown on your 2017 tax return (but see Special rules for farmers, fishermen, and higher income taxpayers, later). Your 2017 tax return must cover all 12 months.

Special rules for farmers, fishermen, and higher income taxpayers. If at least two-thirds of your gross income for tax year 2017 or 2018 is from farming or fishing, substitute 66% for 90% in (2a) under the General rule, earlier. If your AGI for 2017 was more than $150,000 ($75,000 if your filing status for 2018 is married filing a separate return), substitute 110% for 100% in (2b) under General rule, earlier. See Figure 4-A and Pub. 505, chapter 2, for more information.

Figure 4-A Do You Have To Pay Estimated Tax?

*Use the refundable credits shown on the 2018 Estimated Tax Worksheet, line 13b.

**110% if less than two-thirds of your gross income for 2017 and 2018 is from farming or fishing and your 2017 adjusted gross income was more than $150,000 ($75,000 if your filing status for 2018 is married filing a separate return).

Aliens. Resident and nonresident aliens also may have to pay estimated tax. Resident aliens should follow the rules in this chapter unless noted otherwise. Nonresident aliens should get Form 1040-ES (NR), U.S. Estimated Tax for Nonresident Alien Individuals.

You are an alien if you are not a citizen or national of the United States. You are a resident alien if you either have a green card or meet the substantial presence test. For more information about the substantial presence test, see Pub. 519, U.S. Tax Guide for Aliens.

Married taxpayers. If you qualify to make joint estimated tax payments, apply the rules discussed here to your joint estimated income.

You and your spouse can make joint estimated tax payments even if you are not living together.

However, you and your spouse cannot make joint estimated tax payments if:

- You are legally separated under a decree of divorce or separate maintenance,

- You and your spouse have different tax years, or

- Either spouse is a nonresident alien (unless that spouse elected to be treated as a resident alien for tax purposes (see chapter 1 of Pub. 519).

If you do not qualify to make joint estimated tax payments, apply these rules to your separate estimated income. Making joint or separate estimated tax payments will not affect your choice of filing a joint tax return or separate returns for 2018.

2017 separate returns and 2018 joint return. If you plan to file a joint return with your spouse for 2018, but you filed separate returns for 2017, your 2017 tax is the total of the tax shown on your separate returns. You filed a separate return if you filed as single, head of household, or married filing separately.

2017 joint return and 2018 separate returns. If you plan to file a separate return for 2018 but you filed a joint return for 2017, your 2017 tax is your share of the tax on the joint return. You file a separate return if you file as single, head of household, or married filing separately.

To figure your share of the tax on the joint return, first figure the tax both you and your spouse would have paid had you filed separate returns for 2017 using the same filing status as for 2018. Then multiply the tax on the joint return by the following fraction.

Example. Joe and Heather filed a joint return for 2017 showing taxable income of $48,500 and a tax of $6,343. Of the $48,500 taxable income, $40,100 was Joe’s and the rest was Heather’s. For 2018, they plan to file married filing separately. Joe figures his share of the tax on the 2017 joint return as follows.

| Tax on $40,100 based on a separate return | $5,764 |

| Tax on $8,400 based on a separate return | 840 |

| Total | $6,604 |

| Joe’s percentage of total ($5,764 ÷ $6,604) | 87.3% |

| Joe’s share of tax on joint return ($6,343 × 87.3%) | $5,537 |

How To Figure Estimated Tax

To figure your estimated tax, you must figure your expected adjusted gross income (AGI), taxable income, taxes, deductions, and credits for the year.

When figuring your 2018 estimated tax, it may be helpful to use your income, deductions, and credits for 2017 as a starting point. Use your 2017 federal tax return as a guide. You can use Form 1040-ES and Pub. 505 to figure your estimated tax. Nonresident aliens use Form 1040-ES (NR) and Pub. 505 to figure estimated tax (see chapter 8 of Pub. 519 for more information).

You must make adjustments both for changes in your own situation and for recent changes in the tax law. For a discussion of these changes, visit IRS.gov.

For more complete information on how to figure your estimated tax for 2018, see chapter 2 of Pub. 505.

When To Pay Estimated Tax

For estimated tax purposes, the tax year is divided into four payment periods. Each period has a specific payment due date. If you do not pay enough tax by the due date of each payment period, you may be charged a penalty even if you are due a refund when you file your income tax return. The payment periods and due dates for estimated tax payments are shown next.

| For the period: | Due date:1 |

| Jan. 1 – March 31 …. | April 15 |

| April 1 – May 31 …. | June 15 |

| June 1 – August 31 …. | Sept. 15 |

| Sept. 1 – Dec. 31 …. | Jan. 15, next year |

1 See Saturday, Sunday, holiday rule, and January payment.

Saturday, Sunday, holiday rule. If the due date for an estimated tax payment falls on a Saturday, Sunday, or legal holiday, the payment will be on time if you make it on the next day that is not a Saturday, Sunday, or legal holiday.

January payment. If you file your 2018 Form 1040 or Form 1040A by January 31, 2019, and pay the rest of the tax you owe, you do not need to make the payment due on January 15.

Fiscal year taxpayers. If your tax year does not start on January 1, see the Form 1040-ES instructions for your payment due dates.

When To Start

You do not have to make estimated tax payments until you have income on which you will owe income tax. If you have income subject to estimated tax during the first payment period, you must make your first payment by the due date for the first payment period. You can pay all your estimated tax at that time, or you can pay it in installments. If you choose to pay in installments, make your first payment by the due date for the first payment period. Make your remaining installment payments by the due dates for the later periods.

No income subject to estimated tax during first period. If you do not have income subject to estimated tax until a later payment period, you must make your first payment by the due date for that period. You can pay your entire estimated tax by the due date for that period or you can pay it in installments by the due date for that period and the due dates for the remaining periods. The following chart shows when to make installment payments.

| If you first have income on which you must pay estimated tax: |

Make a payment by: | Make later installments by: |

| Before April 1 | April 15 |

June 15 Sept. 15 Jan. 15, next year |

| April 1–May 31 | June 15 |

Sept. 15 Jan. 15, next year |

| June 1–Aug. 31 | Sept. 15 | Jan. 15, next year |

| After Aug. 31 | Jan. 15 next year | (None) |

1 See Saturday, Sunday, holiday rule and January payment.

How much to pay to avoid a penalty. To determine how much you should pay by each payment due date, see How To Figure Each Payment, next.

How To Figure Each Payment

You should pay enough estimated tax by the due date of each payment period to avoid a penalty for that period. You can figure your required payment for each period by using either the regular installment method or the annualized income installment method. These methods are described in chapter 2 of Pub. 505. If you do not pay enough during each payment period, you may be charged a penalty even if you are due a refund when you file your tax return.

If the earlier discussion of No income subject to estimated tax during first period or the later discussion of Change in estimated tax applies to you, you may benefit from reading Annualized Income Installment Method in chapter 2 of Pub. 505 for information on how to avoid a penalty.

Underpayment penalty. Under the regular installment method, if your estimated tax payment for any period is less than one-fourth of your estimated tax, you may be charged a penalty for underpayment of estimated tax for that period when you file your tax return. Under the annualized income installment method, your estimated tax payments vary with your income, but the amount required must be paid each period. See chapter 4 of Pub. 505 for more information.

Change in estimated tax. After you make an estimated tax payment, changes in your income, adjustments, deductions, credits, or exemptions may make it necessary for you to refigure your estimated tax. Pay the unpaid balance of your amended estimated tax by the next payment due date after the change or in installments by that date and the due dates for the remaining payment periods.

Estimated Tax Payments Not Required

You do not have to pay estimated tax if your withholding in each payment period is at least as much as:

- One-fourth of your required annual payment, or

- Your required annualized income installment for that period.

You also do not have to pay estimated tax if you will pay enough through withholding to keep the amount you owe with your return under $1,000.

How To Pay Estimated Tax

There are several ways to pay estimated tax.

- Credit an overpayment on your 2017 return to your 2018 estimated tax.

- Pay by direct transfer from your bank account, or pay by debit or credit card using a pay-by-phone system or the Internet.

- Send in your payment (check or money order) with a payment voucher from Form 1040-ES.

Credit an Overpayment

If you show an overpayment of tax after completing your Form 1040 or Form 1040A for 2017, you can apply part or all of it to your estimated tax for 2018. On line 77 of Form 1040, or line 49 of Form 1040A, enter the amount you want credited to your estimated tax rather than refunded. Take the amount you have credited into account when figuring your estimated tax payments. You cannot have any of the amount you credited to your estimated tax refunded to you until you file your tax return for the following year. You also cannot use that overpayment in any other way.

Pay Online

The IRS offers an electronic payment option that is right for you. Paying online is convenient, secure, and helps make sure the IRS gets your payments on time. To pay your taxes online or for more information, go to IRS.gov/payments. You can pay using any of the following methods.

- IRS Direct Pay for online transfers directly from your checking or savings account at no cost to you. Go to IRS.gov/payments.

- Pay by Card to pay by debit or credit card. Go to IRS.gov/payments. A convenience fee is charged by these service providers.

- Electronic Funds Withdrawal (EFW) is an integrated e-file/e-pay option offered when filing your federal taxes electronically using tax preparation software, through a tax professional, or the IRS at IRS.gov/ payments.

- Online Payment Agreement if you can’t pay in full by the due date of your tax return. You can apply for an online monthly installment agreement at IRS.gov/ payments. Once you complete the online process, you will receive immediate notification of whether your agreement has been approved. A convenience fee is charged.

- IRS2GO is the mobile application of the IRS. You can access Direct Pay or Pay By Card by downloading the application.

Pay by Phone

Paying by phone is another safe and secure method of paying electronically. Use one of the following methods. (1) call one of the debit or credit card providers or (2) use the Electronic Federal Tax Payment System (EFTPS).

- Debit or credit card. Call one of the IRS’s service providers. Each charges a fee that varies by provider, card type, and payment amount.

- Link2Gov Corporation 1-888-PAY-1040TM (1-888-729-1040) www.PAY1040.com

- WorldPay US, Inc. 1-844-PAY-TAX-8TM (1-844-729-8298) www.payUSAtax.com

- Official Payments Corporation 1888-UPAY-TAXTM (1-888-872-9829) www.officialpayments.com

- EFTPS. To use EFTPS, you must be enrolled either online or have an enrollment form mailed to you. To make a payment using EFTPS, call 1-800-555-4477 (English) or 1-800-244-4829 (Español). People who are deaf, hard of hearing, or have a speech disability and who have access to TTY/TDD equipment can call 1-800-733-4829. For more information about EFTPS, go to IRS.gov/payments or www.eftps.gov.

For the latest details on how to pay by phone, go to IRS.gov/payments.

Pay by Mobile Device

To pay through your mobile device, download the IRS2Go application.

Pay With Cash

Paying with cash is a new in-person payment option for individuals. This service is provided through retail partners and is limited $1,000 per day per transaction. To make a cash payment, you must first be registered online at www.officialpayments.com, the IRS Official Payment provider.

Pay by Check or Money Order Using the Estimated Tax Payment Voucher

Before submitting a payment through the mail using the estimated tax payment voucher, please consider alternative methods. One of the IRS’s safe, quick, and easy electronic payment options might be right for you.

If you choose to mail in your payment, each payment of estimated tax by check or money order must be accompanied by a payment voucher from Form 1040-ES.

During 2017, if you:

- made at least one estimated tax payment but not by electronic means,

- did not use software or a paid preparer to prepare or file your return,

then you should receive a copy of the 2018 Form 1040-ES/V.

The enclosed payment vouchers will be preprinted with your name, address, and social security number. Using the preprinted vouchers will speed processing, reduce the chance of error, and help save processing costs.

Use the window envelopes that came with your Form 1040-ES package. If you use your own envelopes, make sure you mail your payment vouchers to the address shown in the Form 1040-ES instructions for the place where you live.

Note. These criteria can change without notice. If you do not receive a Form 1040-ES/V package and you are required to make an estimated tax payment, you should go to www.IRS.gov/form1040es and print a copy of Form 1040-ES which includes four blank payment vouchers. Complete one of these and make your payment timely to avoid penalties for paying late.

If you did not pay estimated tax last year you can order Form 1040-ES from the IRS (see inside back cover of this publication) or download it from IRS.gov. Follow the instructions to make sure you use the vouchers correctly.

Joint estimated tax payments. If you file a joint return and are making joint estimated tax payments, enter the names and social security numbers on the payment voucher in the same order as they will appear on the joint return.

Change of address. You must notify the IRS if you are making estimated tax payments and you changed your address during the year. Complete Form 8822, Change of Address, and mail it to the address shown in the instructions for that form.

Credit for Withholding and Estimated Tax for 2017

When you file your 2017 income tax return, take credit for all the income tax and excess social security or railroad retirement tax withheld from your salary, wages, pensions, etc. Also take credit for the estimated tax you paid for 2017. These credits are subtracted from your total tax. Because these credits are refundable, you should file a return and claim these credits, even if you do not owe tax.

Two or more employers. If you had two or more employers in 2017 and were paid wages of more than $118,500, too much social security or tier 1 railroad retirement tax may have been withheld from your pay. You may be able to claim the excess as a credit against your income tax when you file your return. See Credit for Excess Social Security Tax or Railroad Retirement Tax Withheld in chapter 38.

Withholding

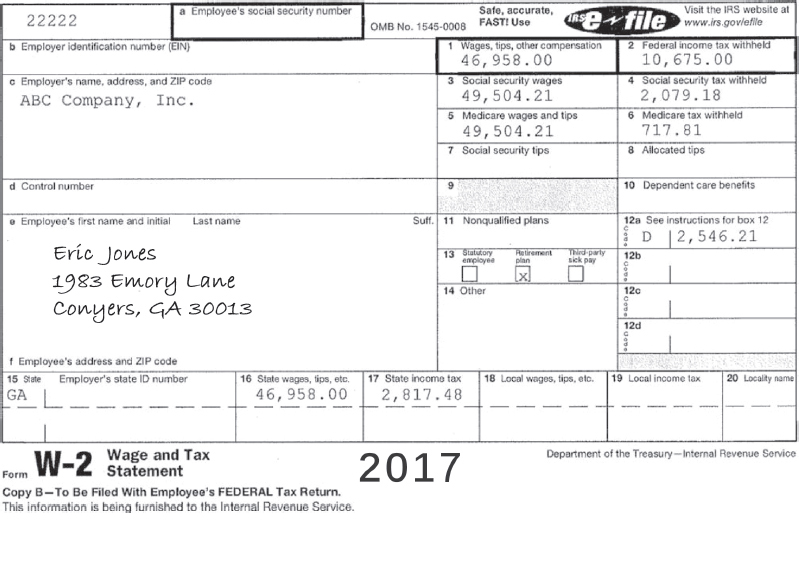

If you had income tax withheld during 2017, you should be sent a statement by January 31, 2018, showing your income and the tax withheld. Depending on the source of your income, you should receive:

- Form W-2, Wage and Tax Statement,

- Form W-2G, Certain Gambling Winnings, or

- A form in the 1099 series.

Forms W-2 and W-2G. If you file a paper return, always file Form W-2 with your income tax return. File Form W-2G with your return only if it shows any federal income tax withheld from your winnings.

You should get at least two copies of each form. If you file a paper return, attach one copy to the front of your federal income tax return. Keep one copy for your records. You also should receive copies to file with your state and local returns.

Form W-2

Your employer is required to provide or send Form W-2 to you no later than January 31, 2018. You should receive a separate Form W-2 from each employer you worked for.

If you stopped working before the end of 2017, your employer could have given you your Form W-2 at any time after you stopped working. However, your employer must provide or send it to you by January 31, 2018.

If you ask for the form, your employer must send it to you within 30 days after receiving your written request or within 30 days after your final wage payment, whichever is later.

If you have not received your Form W-2 by January 31, you should ask your employer for it. If you do not receive it by February 15, call the IRS.

Form W-2 shows your total pay and other compensation and the income tax, social security tax, and Medicare tax that was withheld during the year. Include the federal income tax withheld (as shown in box 2 of Form W-2) on:

- Line 64 if you file Form 1040,

- Line 40 if you file Form 1040A, or

- Line 7 if you file Form 1040EZ.

In addition, Form W-2 is used to report any taxable sick pay you received and any income withheld from your sick pay.

Form W-2G

If you had gambling winnings in 2017, the payer may have withheld income tax. If tax was withheld, the payer will give you a Form W-2G showing the amount you won and the amount of tax withheld.

Report the amounts you won on line 21 of Form 1040. Take credit for the tax withheld on line 64 of Form 1040. If you had gambling winnings, you must use Form 1040; you cannot use Form 1040A or Form 1040EZ.

The 1099 Series

Most forms in the 1099 series are not filed with your return. These forms should be furnished to you by January 31, 2018 (or, for Forms 1099-B, 1099-S, and certain Forms 1099-MISC, by February 15, 2018). Unless instructed to file any of these forms with your return, keep them for your records. There are several different forms in this series, including:

- Form 1099-B, Proceeds From Broker and Barter Exchange Transactions;

- Form 1099-DIV, Dividends and Distributions;

- Form 1099-G, Certain Government Payments;

- Form 1099-INT, Interest Income;

- Form 1099-K, Payment Card and Third Party Network Transactions;

- Form 1099-MISC, Miscellaneous Income;

- Form 1099-OID, Original Issue Discount;

- Form 1099-PATR, Taxable Distributions Received from Cooperatives;

- Form 1099-Q, Payments From Qualified Education Programs;

- Form 1099-R, Distributions From Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc.;

- Form 1099-S, Proceeds From Real Estate Transactions;

- Form RRB-1099, Payments by the Railroad Retirement Board.

If you received the types of income reported on some forms in the 1099 series, you may not be able to use Form 1040A or Form 1040EZ. See the instructions to these forms for details.

Form 1099-R. Attach Form 1099-R to your paper return if box 4 shows federal income tax withheld. Include the amount withheld in the total on line 64 of Form 1040 or line 40 of Form 1040A. You cannot use Form 1040EZ if you received payments reported on Form 1099-R.

Backup withholding. If you were subject to backup withholding on income you received during 2017, include the amount withheld, as shown on your Form 1099, in the total on line 64 of Form 1040, line 40 of Form 1040A, or line 7 of Form 1040EZ.

Form Not Correct

If you receive a form with incorrect information on it, you should ask the payer for a corrected form. Call the telephone number or write to the address given for the payer on the form. The corrected Form W-2G or Form 1099 you receive will have an “X” in the “CORRECTED” box at the top of the form. A special form, Form W-2c, Corrected Wage and Tax Statement, is used to correct a Form W-2.

In certain situations, you will receive two forms in place of the original incorrect form. This will happen when your taxpayer identification number is wrong or missing, your name and address are wrong, or you received the wrong type of form (for example, a Form 1099-DIV instead of a Form 1099-INT). One new form you receive will be the same incorrect form or have the same incorrect information, but all money amounts will be zero. This form will have an “X” in the “CORRECTED” box at the top of the form. The second new form should have all the correct information, prepared as though it is the original (the “CORRECTED” box will not be checked).

Form Received After Filing

If you file your return and you later receive a form for income that you did not include on your return, you should report the income and take credit for any income tax withheld by filing Form 1040X, Amended U.S. Individual Income Tax Return.

Separate Returns

If you are married but file a separate return, you can take credit only for the tax withheld from your own income. Do not include any amount withheld from your spouse’s income. However, different rules may apply if you live in a community property state.

Community property states are listed in chapter 2. For more information on these rules, and some exceptions, see Pub. 555, Community Property.

Fiscal Years

If you file your tax return on the basis of a fiscal year (a 12-month period ending on the last day of any month except December), you must follow special rules to determine your credit for federal income tax withholding. For a discussion of how to take credit for withholding on a fiscal year return, see Fiscal Years (FY) in chapter 3 of Pub. 505.

Estimated Tax

Take credit for all your estimated tax payments for 2017 on line 65 of Form 1040 or line 41 of Form 1040A. Include any overpayment from 2016 that you had credited to your 2017 estimated tax. You must use Form 1040 or Form 1040A if you paid estimated tax. You cannot use Form 1040EZ.

Name changed. If you changed your name, and you made estimated tax payments using your old name, attach a brief statement to the front of your paper tax return indicating:

- When you made the payments,

- The amount of each payment,

- Your name when you made the payments, and

- Your social security number.

The statement should cover payments you made jointly with your spouse as well as any you made separately.

Be sure to report the change to the Social Security Administration. This prevents delays in processing your return and issuing any refunds.

Separate Returns

If you and your spouse made separate estimated tax payments for 2017 and you file separate returns, you can take credit only for your own payments.

If you made joint estimated tax payments, you must decide how to divide the payments between your returns. One of you can claim all of the estimated tax paid and the other none, or you can divide it in any other way you agree on. If you cannot agree, you must divide the payments in proportion to each spouse’s individual tax as shown on your separate returns for 2017.

Divorced Taxpayers

If you made joint estimated tax payments for 2017, and you were divorced during the year, either you or your former spouse can claim all of the joint payments, or you each can claim part of them. If you cannot agree on how to divide the payments, you must divide them in proportion to each spouse’s individual tax as shown on your separate returns for 2017.

If you claim any of the joint payments on your tax return, enter your former spouse’s social security number (SSN) in the space provided on the front of Form 1040 or Form 1040A. If you divorced and remarried in 2017, enter your present spouse’s SSN in that space and write your former spouse’s SSN, followed by “DIV,” to the left of Form 1040, line 65, or Form 1040A, line 41.

Underpayment Penalty for 2017

If you did not pay enough tax, either through withholding or by making timely estimated tax payments, you will have an underpayment of estimated tax and you may have to pay a penalty.

Generally, you will not have to pay a penalty for 2017 if any of the following apply.

- The total of your withholding and estimated tax payments was at least as much as your 2016 tax (or 110% of your 2016 tax if your AGI was more than $150,000, $75,000 if your 2017 filing status is married filing separately) and you paid all required estimated tax payments on time.

- The tax balance due on your 2017 return is no more than 10% of your total 2017 tax, and you paid all required estimated tax payments on time.

- Your total 2017 tax minus your withholding and refundable credits is less than $1,000.

- You did not have a tax liability for 2016 and your 2016 tax year was 12 months, or

- You did not have any withholding taxes and your current year tax less any household employment taxes is less than $1,000.

See Pub. 505, chapter 4, for a definition of “total tax” for 2016 and 2017.

Farmers and fishermen. Special rules apply if you are a farmer or fisherman. See Farmers and Fishermen in chapter 4 of Pub. 505 for more information.

IRS can figure the penalty for you. If you think you owe the penalty but you do not want to figure it yourself when you file your tax return, you may not have to. Generally, the IRS will figure the penalty for you and send you a bill. However, if you think you are able to lower or eliminate your penalty, you must complete Form 2210 or Form 2210-F and attach it to your paper return. See chapter 4 of Pub. 505.