Introduction

Many people are honest in their intentions and actions. Some are not. The presence of this “some” necessitates an entity to create rules and to monitor them. The purpose of the rules is to ensure that the participants in the employer-sponsored plans are not being taken advantage of. The American government enacted ERISA (Employee Retirement Income Security Act) in 1974 and the Pension Protection Act in 2006 (PPA) to help with this need to level the playing field and to keep all players honest. There are three primary governmental organizations that influence pension regulation. In this chapter, you will learn about each of them and what they do.

Learning Goals

Explain how ERISA reshaped the world of pension.

Identify the four titles of ERISA.

Understand the major trends in the post-ERISA legislation.

Understand the implications of the PPA of 2006.

Identify the agencies involved in regulating the tax-advantaged retirement plans.

Explain the purpose of an advanced determination letter (ADL).

Introduction to ERISA

Regulation adds a great deal of complexity to any system. The world of employer-sponsored retirement plans is no different. The presence of regulation implies that employees are theoretically safer and consultants, who thoroughly understand the regulation, can benefit from this knowledge.

ERISA is a federal law that protects the employer-sponsored retirement assets of millions of Americans. Its primary purpose is to protect the participants of the employer-sponsored plans by helping them understand and ultimately receive the benefits that have been promised.1

ERISA made some key changes, which will be discussed throughout this textbook. First, it imposes requirements on the vesting schedules and measures of employee participation. Second, it provides options for a company that has not fully funded their promised pension obligations. Third, it establishes a safety net for workers if the company should file for bankruptcy. Fourth, it imposes certain standards, called fiduciary standards, on those who manage the pension assets. Fifth, it removes the monopoly that the employer-sponsored plans had on the retirement savings market pre-ERISA. Before ERISA was enacted, the employer-sponsored plans were the only mechanism for the employees to save for retirement. ERISA also created the Individual Retirement Account (IRA), which enabled the workers to save for retirement outside the purview and limitations of their employer.

It is important to understand that ERISA does not require the employers to establish a pension plan. However, it does require that those who establish plans must meet certain minimum standards.

ERISA is organized under four titles or sections that establish the minimum standards applicable to the employer-sponsored retirement plans. Title I of ERISA establishes the requirement to disclose an employee’s right to collect the promised benefits. Disclosure is the keyword. Title II of ERISA establishes the parameters on the tax deferral of the contributions. Certain requirements and vesting schedules must be in place or the contributions are no longer considered to be tax-deferred. If compliance is not strictly followed, then the plan could be deemed not a “qualified” plan, which would retroactively affect both the employee and employer, who may need to undo several years’ worth of tax deductions if the tax status of the retirement plan were to be reversed. Title III of ERISA creates a regulatory framework for implementing ERISA. The duties are split between the Department of Labor (DOL) and the Internal Revenue Service (IRS). Title IV of ERISA is very important. This title establishes the Pension Benefit Guarantee Corporation (PBGC). We will discuss the PBGC in detail later in this chapter.

Post-ERISA Trends

In the years following the adoption of ERISA, several trends have emerged in the world of employer-sponsored retirement plans. The first trend is a reduction in taxation benefits. At one point, the pension benefits received extremely favorable tax treatment. For example, they were once not subject to estate taxes. This is no longer the case. Each favorable tax treatment has been gradually removed so that today, the pension benefits are taxed as ordinary income (just like earned income). This trend clearly has benefited the federal government more than the pension recipients.

The second trend relates to the use of IRAs. At the time when ERISA was enacted, IRAs permitted very limited contributions. These boundaries have gradually been expanded to encourage more private savings. Now, investors benefit from higher contribution limits and introduction of Roth IRAs.

The third trend is related to the second, and it deals specifically with the contribution limits. Immediately following the passing of ERISA, legislation began to appear that limited the deductible contributions for highly compensated employees. This legislation had the effect of increasing the use of nonqualified-deferred compensation plans, like a 457 plan. In 2001, this trend began to change, and the income limits were gradually made less restrictive. This was done to both encourage savings and incentivize small business owners to open plans. An ongoing trend has been to give all business types equal access to the employer-sponsored retirement savings plans.

A fourth trend has been the limits placed on the tax deferral. The federal government realized that the tax inducement to save in a retirement plan was tremendous and that the government was losing out on a revenue source for a very long period. In 1986, a legislation was passed that required the distributions to begin by the attained age of 70½ to correct this revenue oversight.

A fifth trend relates primarily to small businesses, but it is also applied to other business types. To ensure that small business owners were not giving themselves the retirement benefits to the exclusion of their rank-and-file employees, top-heavy rules were instituted. We will discuss these in detail in a later chapter, but they essentially prevent discrimination. Another rule inspired by small business abuses is the affiliation requirements. Some businesses were forming separate entities to avoid retirement regulations. Now, they must aggregate all related businesses with a common ownership to eliminate this loophole. People can be very creative, and as new loopholes are found, new regulations will likely emerge to plug the leaks.

PPA of 2006

The PPA of 2006 is a legislation that was designed to further protect the employer-sponsored plan participants and to improve the pension system, in general. It mandates an accelerated funding schedule when a defined-benefit (DB) plan does not have enough money to meet its projected obligations. It also mandates accelerated vesting schedules for defined-contribution (DC) plans. Both of these requirements protect the employees (participants) from an employer’s poor judgment.

Another requirement that protects the employees is a requisite to offer more than simply employer stock in a DC plan. Can you imagine a scenario where you work for a large company and have a substantial portion of your 401(k) invested in your employers’ stock only to have your employer go bankrupt? Now, the employee is without a job and their retirement savings have been decimated. This exact nightmare played out in the lives of countless former employees of Enron. Lives were forever altered because the employees failed to diversify their employer from their retirement savings. People invest in what they know ... or what they think they know.

The PPA also made several improvements to the pension system. It made previously temporary higher contribution limits a permanent incentive for additional savings. It also encouraged the autoenrollment feature many plans now incorporate. This feature will automatically enroll new employees in the respective retirement plan of the employer, unless they specifically opt out. There is also now an option for the employees, who are unaware of the basics of asset allocation strategies, to seek investment advice from a representative of the DB plan.

Who Is the Regulator?

Regulation may be wisely designed to protect consumers and encourage proper behavior, but someone must implement and oversee the laws or they will not be applied correctly, if at all. Three agencies are given the regulatory oversight over different corners of the pension law.

The first in the pension regulation triad is the IRS. Before an employer begins to fund a tax-advantaged retirement plan, it is a good idea if they request an ADL from the IRS. This letter is not mandatory, but it is highly recommended. If a company begins to fund a retirement plan in September of a given year, but the IRS audits the company in June of the following year and determines that their retirement plan does not meet the requirements of ERISA, then all contributions into the plan would need to be reversed and both the company and employees have a tax issue on their hands. The employer will need to restate their previous year’s tax return to eliminate the tax deduction that they claimed. They will also need to reissue W-2s for each affected employee, and the employees will all owe taxes potentially with the interest and penalties to the IRS on a personal level. The path of least resistance is to simply apply for an ADL, which will bestow the IRS’s seal of approval on establishing the plan.

The IRS also performs the task of auditing the tax-advantaged plans. Each year, the employers must fill out a special form called a 5,500 form, which helps the IRS determine the ongoing compliance with the pension law.

In addition to these two regulatory responsibilities, the IRS may also issue interpretations of the law to help companies determine compliance with the expanding body of legislation. The IRS may issue a proposed regulation, which is merely an idea that the IRS has had. These cannot be relied upon until they explicitly state that they can. The IRS may also issue regulations that apply to all taxpayers or it may issue revenue rulings that only apply to very unique situations. Occasionally, they may issue a private letter ruling, which is an exclusive interpretation for one company’s unique situation.

The second pension regulator is the DOL. One key area of purview for the DOL is the enforcement of Title I of ERISA (disclosure rules). One thing that they look for is the distribution of the summary plan description (SPD) to all the participants. An SPD discloses all the relevant facts to the employees in a somewhat organized fashion.

The DOL also monitors the use of investment choices within the tax-advantaged retirement plans. There is a list of prohibited transaction types that the DOL monitors. We will discuss this list of prohibited transactions in detail in another chapter. They also monitor adherence to the exclusive benefit rule, which states that all plan assets must be invested for the exclusive benefit of the employees (participants). The purpose of the exclusive benefit rule is to prevent a company from buying shares of another company to attempt to influence their actions in the marketplace, which would be a manipulation of the forces of competition and not a sole benefit for the plan participants.

In addition, the DOL also monitors the actions of the plan’s fiduciaries. A fiduciary is a person or group with the responsibility over the employer-sponsored plan. Every plan has a fiduciary. They are held to a standard known as prudence, which means that they must act as a prudent person would be expected to act. It should go without saying that the fiduciary would act in a prudent way for the exclusive benefit of the plan’s participants, but sadly, the reality has pointed to a different outcome unless the DOL looks over their shoulder. The DOL can sue a plan fiduciary if they breach their duties. We will discuss the fiduciary responsibilities later in this textbook.

One confusing element is that the DOL can potentially issue interpretations of the laws just as the IRS can.

The third regulatory body is the PBGC. The PBGC can issue interpretations of the law in a similar way that both the IRS and DOL can. It would probably be simpler for the field of retirement planning if only one of the three issued interpretations of the law, but for now, all three are able to do so.

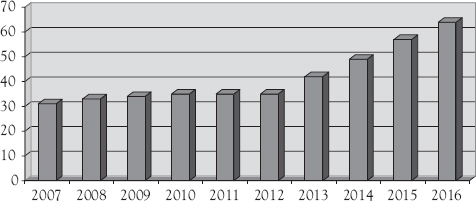

The PBGC is essentially an insurance plan for DB plans. Most employers with DB plans can pay an “insurance fee” of $64 per participant to the PBGC. Figure 2.1 shows the trend of rising insurance premiums with time. With the PBGC in place, the plan participants have a layer of protection, should the employer go bankrupt before all of the participants’ benefits have been paid out to them. This coverage represents a real cost to the employers. It is important to note that the PBGC only guarantees benefits up to $4,500 per month, and this threshold is sufficient for most retirees.

Figure 2.1. PBGC employer premiums

If a DB plan ever desires to terminate, then it must first notify the PBGC. This type of termination is considered a voluntary termination, where the company has a DB plan that is fully funded, but desires to shut it down and switch to a different plan type (perhaps a DC plan) to reduce cost or streamline plan administration (oversight and logistics). It is possible for the PBGC to find that a DB plan is so poorly underfunded that it needs to be forcibly terminated. This is known as an involuntary termination.

Given the regulatory backdrop, it is easy to see why many employer-sponsored retirement plans use a prepackaged (or prototype) plan, which is predesigned to meet all regulatory hurdles. Occasionally, employers will still desire to customize certain features of their plan. These customized plans do provide more flexibility, but they are more costly to administer and more difficult to establish.

Discussion Questions

What were the major reforms instituted by ERISA?

Describe the post-ERISA trends in the world of retirement planning.

What is the role of an ADL in the creation of a new employer-sponsored tax-advantaged retirement plan?

What is the role of the IRS in the retirement market?

What is the role of the DOL in the pension process?