7

Accounting for Revenue

CHAPTER OBJECTIVES

This chapter will help the readers to:

- Identify issues involved in revenue recognition from sales of goods, provisions of services and also long-term contracts.

- Apply accrual principle on revenue recognition.

- Analyze the impact of uncertainty on revenue recognition.

- Get familiarity with the key requirement of Ind AS 18 ‘Revenue’, Ind AS 11 ‘Construction Contracts’, and Ind AS 21 ‘The effects of changes in Foreign Exchange Rates’ as applicable to revenue recognition.

7.1 REVENUE

The expression ‘revenue’ means the consideration earned by an enterprise by sale of goods or provision of services in the ordinary course of business. Revenue may also be earned by an enterprise by letting others use resources owned by it. For example, interest is earned on moneys lent by an enterprise. Revenue earned by an entity is known by a variety of different terms including sales, fees, interest, dividends and royalties. Accounting for revenue requires answer to two related questions, firstly, how much revenue to be recognized and secondly, when should it be recognized. Revenue is recognized when it is probable that future economic benefits will flow to the entity and these benefits can be measured reliably.

As per Ind AS 18, ‘Revenue is the gross inflow of economic benefits during the period arising in the course of ordinary activities of an entity when those inflows result in increases in equity, other than increases relating to contributions from equity participants’. Ind AS 18 deals with revenue recognition from:

- Sales of goods.

- Rendering of services.

- The use by others of entity’s assets yielding interest, royalities and dividends.

Revenue recognition from construction contracts is the subject matter of Ind AS 11.

7.2 QUANTUM OF REVENUE

Revenue is measured at the fair value of the consideration received or receivable. Fair value is the amount for which an asset could be exchanged or a liability settled, between knowledgeable and willing parties in an arm’s length transaction. The amount of revenue earned is usually determined with reference to the agreement with the customer. In most cases, the consideration is in the form of cash or cash equivalents and the amount of revenue is in the form of cash or cash equivalents received or receivable.

7.2.1 Discount

An enterprise may offer quantity discount or a trade discount to its customers. The quantity discount is often offered to customers for buying in bulk, whereas a trade discount may be offered to certain categories of customers. In both the cases, the amount of discount is known at the time of sale. In such cases, revenue should be recorded at the net sales value, that is, after deducting trade discount and quantity discount.

In case of credit sale, an enterprise may also offer a cash discount. Cash discount is offered for inducing prompt payment from the customer. For example, an enterprise may sell goods on terms 1/15 net 60. This expression indicate that the customers is being allowed a credit period of 60 days but if he pays within 15 days he will be given a cash discount of 1% of the invoice value. As at the time of sale there is no certainty as to whether the customer will avail the cash discount or not, it is better to record revenue at the gross value without deducting the cash discount. Subsequently, if the customer pays early and earns cash discount, the same will be recognized as an expense.

Trade discount and quantity discount are not shown separately but are taken as reduction of revenue. Cash discount is shown separately as an expense.

This may cause a problem where sales is recorded in one accounting period but the cash discount is availed in the next accounting period. Recording sale in one accounting period and cash discount in the next goes against the matching principle. If the incidence of cash discount is large, an enterprise may make provisions for cash discount and record estimated cash discount as an expense of the period. If cash discount is not availed by the customer, the same will get reversed in the next accounting period.

■ Illustration 7.1

Quick Fox Trading Limited usually sells its goods at the invoice value. In case of bulk orders (exceeding 1,000 units), it offers a quantity discount of 2% on the invoice value. The customers are allowed 45 days credit period however, if the payment is made within 15 days, an additional discount of 1% is given. The company received an order for supply of 1,500 units at an invoice price of ₹2,000 per unit. The customer paid on the 15th day and availed cash discount. How will the transaction be recorded?

The amount expected to be realized at the time of sale is ₹3,000,000 less 2% quantity discount. The sale will be recorded accordingly at ₹2,940,000. The following entry will be passed:

| Customer (Trade Receivables) Account Dr. | ₹2,940,000 |

| To Sales | ₹2,940,000 |

As the customer has availed cash discount of 1% by paying on the 15th day, the net receipt from the customer is ₹2,910,600. At the time of receipt will be:

| Bank Account | Dr. | ₹2,910,600 |

| Cash Discount | Dr. | ₹29,400 |

| To Customer Account | ₹2,940,000 |

If a customer is not satisfied about the quality of goods bought by him, he may be permitted by the enterprise to return the goods. As a consequence of the return, the revenue earlier recorded declines with a corresponding reduction in the receivables from the customer. In the profit and loss statement, the revenue from sales will appear net of sales return. On sales return, the following accounting entry will be passed:

| Sales Return A/c | Dr. |

| To Customer Account |

7.2.2 Agency Relationship

In an agency relationship, the agent collects the economic benefits on behalf of the principal. The agent is merely entitled to receive commission for the services rendered. The amount, collected on behalf of the principal, does not result in increase in equity for the agent. Only the amount of commission will be treated as revenue. Entity engaged in agency business, e.g., real estate agents, insurance brokers, stock brokers, etc., would record amount of commission as revenue and not the entire amount of the transaction.

■ Illustration 7.2

Small Bull Brokers Limited is a stock broking firm. It bought shares on behalf of one of his clients for ₹50 million charging 1% brokerage. It paid ₹50 million to the stock exchange and collected ₹50.5 million (including brokerage) from its client. What amount should be recorded as revenue?

As Small Bull Brokers Limited is acting in the capacity of a broker, only the amount of commission, i.e., ₹0.50 million will be recognized as revenue representing the increase in equity.

7.2.3 Indirect Taxes

Indirect taxes, by nature, are paid to the government by one entity, but it is collected from the consumer as part of the price of a good or service. For example, sales tax, value-added tax, goods and services tax, etc., are levied on an entity but are borne by someone else. Revenue should include only the gross inflows of economic benefits received and receivable by the entity on its own account. As indirect taxes are collected on behalf of government, they are excluded from the definition of revenue. However, if the indirect tax is collected by the enterprise on its own account as a principal and it pays the tax to the government on its own account, the revenue will be taken on gross basis.

Indirect taxes–Excise duty, service tax, sales tax and value added tax are called indirect taxes as the incidence of tax is shifted to the customer.

7.2.4 Deferred Revenue

Revenue is generally recognized as the amount of cash or cash equivalent received or receivable. However, where good are sold or services provided on a deferred credit basis, i.e., revenue is receivable after the lapse of significant time period, the fair value of the consideration may be less than the nominal amount of cash received or receivable. In such a case, the fair value of the consideration is determined by discounting all future receipts using an imputed rate of interest. The difference between the fair value and the nominal amount of the consideration is recognized as interest revenue.

■ Illustration 7.3

HH Engineering Limited sold some machinery to a client on a deferred credit basis. The sale price of ₹20 million is receivable after 2 years. What amount should be recorded as revenue in the following circumstances?

- HHEL sells similar machinery to its clients for ₹16 million if the payment is made immediately; or

- HHEL sells machinery only on deferred credit basis and the prevalent rate of interest is 10%.

As HHEL is permitting its client 2 years to make the payment, the nominal value cannot be taken as the fair value of the goods sold. In case (1) above, the fair value of goods sold would be taken as ₹16 million and ₹4 million would be recognized as interest revenue over 2 years. In case (2), the fair value would be determined by discounting the amount of consideration by 10% per annum.

Revenue from sale of machinery would be recognized at ₹16.53 million and the balance ₹3.47 million would be recognized as interest income spread over the period of 2 years.

7.2.5 Barter Transactions

In case of barter transactions, good or services are exchanged or swapped. Either the entire value of transaction is settled by swap or a part of the consideration is paid in cash. If goods or services being swapped are of similar nature, no revenue would be recognized. For example, two suppliers of commodities like oil or milk agree to exchange inventories in various locations to fulfil demand on a timely basis in a particular location.

On the other hand, exchange of goods or services which are dissimilar in nature is regarded as a transaction which generates revenue. In such a case, revenue is measured at the fair value of the goods or services received. When the fair value of the goods or services received cannot be measured reliably, the revenue is measured at the fair value of the goods or services given up. The revenue recognized would be adjusted with the amount of cash or cash equivalent transferred.

7.2.6 Revenue Earned in Foreign Currency

Revenue earned by an enterprise in foreign currency is converted into the reporting currency by applying the appropriate exchange rate between the foreign currency and the reporting currency on the date of the transaction. An enterprise may instead of using the actual rate decide to use an approximate rate.1 For example, an average rate for a week may be used for all transactions in foreign currency during the week. However, where exchange rate fluctuations are heavy, it is preferable not to use average rate.

Once revenue has been recorded, any subsequent change in foreign exchange rate will not alter the amount of revenue recognized, but will be recorded either as a gain or loss on account of foreign exchange difference.

■ Illustration 7.4

XYZ Limited exported goods invoiced at $700,000. On the date of the sale the prevailing exchange rate was $1 = ₹64. The customer was allowed 30 days to make the payment. The payment was duly received from the customer on due date. The exchange rate on the date of receipt was $1 = ₹63.50. What will be the impact of the above sale in the profit and loss account of the company?

On the date of sale, the invoice value will be converted into Indian rupee by applying the then prevailing exchange rate, i.e., ₹64. Accordingly, sale will be recorded at ₹44,800,000 by passing the following entry:

| Customer (Debtor) Account | Dr. | ₹30,800,000 |

| To Sales Account | ₹30,800,000 |

As the amount realized is at ₹63.50, there is an exchange loss of ₹0.50 per dollar. The following entry will be passed upon receipt of money from the customer:

| Bank Account | Dr. | ₹44,450,000 |

| Exchange Loss Account | Dr. | ₹350,000 |

| To Customer Account | ₹44,800,000 |

In the profit and loss statement revenue from sales will appear at ₹44,800,000. Loss on account of exchange difference will appear along with other expenses.

7.3 TIMING OF REVENUE RECOGNITION

In cash basis of accounting, revenue is recognized only upon receipt of consideration from the customer. No accounting entries are passed at the time of sale of goods or provision of services. In accrual basis of accounting, revenue is recognized when earned and not when cash is received. In the following section, we discuss the revenue recognition from sales of goods, rendering of services and from execution of construction contracts.

7.3.1 Sale of Goods

In case of sales of goods, the revenue normally will be recognized when the seller has performed his part of obligation as per the agreement with the buyer. Goods include goods produced by the entity for the purpose of sale and goods purchased for resale, such as merchandise purchased by a retailer or land and other property held for resale.

Ind AS 18 lays down the following conditions to ascertain that the performance has been achieved:2

- The entity has transferred the significant risks and rewards of ownership of the goods to the buyer.

- The entity retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold.

- The amount of revenue can be measured reliably.

- It is probable that the economic benefits associated with the transaction will flow to the entity.

- The costs incurred or to be incurred in respect of the transaction can be measured reliably.

The transfer of the legal title or passing of possession to the buyer is often taken as an evidence of the transfer of the risks and rewards of ownership. In some cases, however, the transfer of risks and rewards of ownership may occur at a different time from the transfer of legal title or the passing of possession. If significant risk of ownership is retained by the entity, revenue is not recognized. Examples of situations in which the entity may retain the significant risks and rewards of ownership are:

- When the entity retains an obligation for unsatisfactory performance not covered by normal warranty provisions.

- When the receipt of the revenue from a particular sale is contingent on the derivation of revenue by the buyer from its sale of the goods.

- When the goods are shipped subject to installation and the installation is a significant part of the contract which has not yet been completed by the entity.

- When the buyer has the right to rescind the purchase for a reason specified in the sales contract and the entity is uncertain about the probability of return.

If, however, the risk of ownership retained by the entity is insignificant, the transaction is a sale and revenue is recognized. For example, an entity may be offering refund if the customer is not satisfied. The entity would recognize revenue at the time of sale. The seller would estimate future returns based on previous experience and other relevant factors and recognizes a liability for returns.

Revenue is recognized only when it is probable that the economic benefits associated with the transaction will flow to the entity. If there is uncertainty existing at the time of sale regarding receipt of consideration, revenue should not be recognized until the consideration is received or the uncertainty is removed.

In some cases, an uncertainty may arise subsequent to revenue recognition about the collectability of the amount. In such cases, the amount of revenue already booked is not reversed rather suitable provision for probable loss on account of non-recovery would be made.

When the expenses cannot be measured reliably, revenue cannot be recognized. The matching principle requires matching of cost with revenue. Therefore, when it is not possible to measure expenses reliably, any consideration already received for the sale of the goods is recognized as a liability.

Once a sales transaction meets the above conditions, revenue is deemed to have been earned. The timing of receipt has no bearing on revenue recognition. The above describes the general rules for revenue recognition. Some specific situations regarding timing of revenue recognition are discussed below:

- Installation and inspection: Revenue is normally recognized when the buyer accepts delivery, and installation and inspection are complete.

- Consignment sales: Goods are sent by the consignor to the consignee and the later undertakes to sell the goods on behalf of the consignor. Revenue will be recognized only when goods are sold by the consignee to a third party.

- Cash on delivery Sales: Sale is deemed to be completed only upon receipt of cash from the customer. As such revenue will be recognized only when cash is received.

Box 7.1 Accounting Policies Relating to Revenue Recognition from Sale of Goods

Asian Paints Limited

- Revenue is recognized when it is probable that economic benefits associated with a transaction flows to the company in the ordinary course of its activities and the amount of revenue can be measured reliably. Revenue is measured at the fair value of the consideration received or receivable, net of returns, trade discounts and volume rebates allowed by the company.

- Revenue includes only the gross inflows of economic benefits, including excise duty, received and receivable by the company, on its own account. Amounts collected on behalf of third parties, such as sales tax and value added tax are excluded from revenue.

- Revenue from sale of products is recognized when the company transfers all significant risks and rewards of ownership to the buyer, while the company retains neither continuing managerial involvement nor effective control over the products sold.

ITC Limited

- Revenue is measured at the fair value of the consideration received or receivable for goods supplied and services rendered, net of returns and discounts to customers. Revenue from the sale of goods includes excise and other duties which the company pays as a principal but excludes amounts collected on behalf of third parties, such as sales tax and value added tax.

- Revenue from the sale of goods is recognized when significant risks and rewards of ownership have been transferred to the customer, which is mainly upon delivery, the amount of revenue can be measured reliably and recovery of the consideration is probable.

- Sale on approval basis: The seller gives the buyer an option to return the goods within a specified period of time. Sale is considered to be complete when goods are explicitly approved by the buyer or on lapse of the time allowed.

- Installment Sales: In case the sales consideration is payable in installments, revenue is recognized on the date of sale by the normal selling price of the goods. Interest component in installments is recognized separately.

- Delivery delayed at the request of the buyer: If the goods are identified and ready for delivery but delivery is delayed at buyer’s request, revenue is recognized immediately so long there is expectation that delivery will be made.

- Internal sale: Goods sold by one unit of the enterprise to another is not recognized as revenue. As there is no transfer of ownership, no sale can be recorded.

Accounting policies of some companies relating to revenue recognition from sales are given in Box 7.1.

7.3.2 Revenue from Services

Revenue from rendering of services is recognized when the agreed services have been rendered. If the service consists of a single act, revenue can be easily recognized upon performance of that act. However, when service consists of a series of acts, revenue is recognized with reference to the stage of completion of the transaction. Recognizing revenue with reference to the stage of completion is called percentage of completion method. Revenue from service is recognized if it is possible to estimate the outcome of the transaction reliably. The following conditions need to be satisfied for revenue recognition:

- The amount of revenue can be measured reliably.

- It is probable that the economic benefits associated with the transaction will flow to the entity.

- The stage of completion of the transaction at the end of the reporting period can be measured reliably.

- The costs incurred for the transaction and the costs to complete the transaction can be measured reliably.

It is possible to make reliable estimates of revenue to be earned based upon the agreement with the customer. The agreement usually provides for enforceable rights of each party to the transaction, the consideration to be exchanged and the manner and terms of settlement. In addition, internal budgeting and reporting system is helpful in making the estimates.

To ascertain the stage of completion, an entity may use a variety of methods. Some of the methods that could be used for this purpose include surveys of work performed, service performed as a percentage of total services to be performed, cost incurred as a percentage of the total estimated cost. It may be noted that progress payments and advances received from customers may not be indicative of the stage of completion.

In cases where services consist of an indeterminate number of acts over a specified period of time, revenue is recognized on a straight-line basis over the specified period. For example, in case of annual maintenance contract, the revenue may be recognized over the period of the AMC. However, when a specific act is much more significant than any other acts, the recognition of revenue is postponed until the significant act is executed.

When the outcome of the transaction involving the rendering of services cannot be estimated reliably, it would not be correct to recognize any profit. In such a case, revenue is recognized only to the extent of the expenses that are recoverable. Likewise, when the transaction is at early stage of execution, and therefore, it is not possible to estimate the outcome of the transaction reliably, revenue would be recognized only to the extent of cost incurred.

When the outcome of a transaction cannot be estimated reliably and it is not probable that the costs incurred will be recovered, no revenue is recognized and the cost incurred is recorded as an expense.

The accounting policy of Infosys Limited relating to revenue recognition from services is given in Box 7.2.

Box 7.2 Accounting Policy Relating to Revenue Recognition from Services

Revenue Recognition

- The company uses the percentage-of-completion method in accounting for its fixed-price contracts.

- The use of the percentage-of-completion methods require the company to estimate the efforts or costs expensed to date as a proportion of the total efforts or costs to be expended. Efforts or costs expended have been used to measure progress towards completion as there is a direct relationship between input and productivity.

- Provisions for estimated losses, if any, on uncompleted contracts are recorded in the period in which such losses become probable based upon the expected contract estimates at the reporting date.

7.3.3 Income from Construction Contracts2

Revenue recognition in case of construction contracts poses a peculiar problem. A construction contract may take a long time for execution; as a result the construction activity may commence in one accounting period and is completed in another accounting period. Revenue from contracts in such cases will have to be recognized in a systematic manner over the period of time taken for execution. Revenue and expenses associated with the contract are recognized with reference to the stage of completion of the contract activity in a particular accounting period. However, no revenue is recognized unless some reasonable progress has been made in the contract.

Contract revenue shall comprise initial amount of revenue agreed in the contract as well as the variations in contract work, claims and incentive payments. However, the latter is recognized only to the extent that it is probable that they will result in revenue and they are capable of being reliably measured.

A construction contract may be negotiated either on a fixed price basis or on a cost plus basis. In a fixed price contract, the contractor agrees to a fixed contract price, or a fixed rate per unit of output. The price or rate may be subject to cost escalation clauses. In case of a cost plus contract, the contractor is reimbursed for allowable or otherwise defined costs, plus a percentage of these costs or a fixed fee.

In case of a fixed price contract, it is possible to reliably estimate the outcome of a construction contract when the following conditions are satisfied:

- Total contract revenue can be measured reliably.

- It is probable that the economic benefits associated with the contract will flow to the entity.

- Both the contract costs to complete the contract and the stage of contract completion at the end of the reporting period can be measured reliably.

- The contract costs attributable to the contract can be clearly identified and measured reliably so that actual contract costs incurred can be compared with prior estimates.

In the case of a cost plus contract, the following conditions must be satisfied to recognize revenue:

- It is probable that the economic benefits associated with the contract will flow to the entity.

- The contract costs attributable to the contract, whether or not specifically reimbursable, can be clearly identified and measured reliably.

Accounting policies of Punj Lloyd Limited relating to revenue recognition are given in Box 7.3.

Box 7.3 Accounting Policy Relating to Revenue Recognition from Construction Contracts

- Contract revenue associated with long-term construction contracts is recognized as revenue by reference to the stage of completion of the contract at the balance sheet date.

- The stage of completion of project is determined by the proportion that contracts costs incurred for the work performed up to the balance sheet date bear to the estimated total contract costs. However, profit is not recognized unless there is reasonable progress on the contract.

- If total cost of a contract, based on technical and other estimates, is estimated to exceed the total contract revenue, the foreseeable loss is provided for.

- The effect of any adjustment arising from revisions to estimates is included in the statement of profit and loss of the year in which revisions are made.

- Contract revenue earned in excess of billing is classified as ‘unbilled revenue (work-in-progress)’ and billing in excess of contract revenue is classified under ‘other liabilities’ in the financial statements.

- Claims on construction contracts are included based on management’s estimate of the probability that they will result in additional revenue, they are capable of being reliably measured, there is a reasonable basis to support the claim and that such claims would be admitted either wholly or in part.

- The company assesses the carrying value of various claims periodically, and makes adjustments for any unrecoverable amount arising from the legal and arbitration proceedings that they may be involved in from time-to-time. Insurance claims are accounted for on acceptance/settlement with insurers.

In case, the cost already incurred plus the estimated cost to completion is likely to exceed the contract revenue, appropriate provision for the resultant expected loss is made in the accounts.

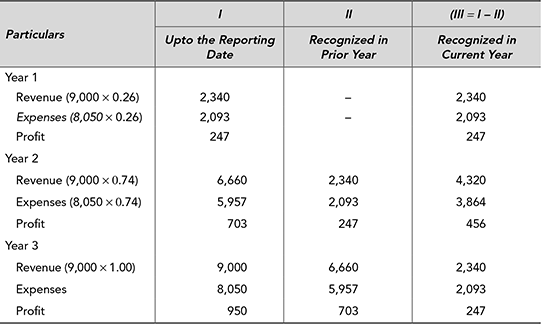

■ Illustration 7.5

A construction contractor has a fixed price contract for ₹9,000 million to build a bridge. The contractor’s initial estimate of contract costs is ₹8,000 million. It will take three years to build the bridge.

By the end of year one, the contractor’s estimate of contract costs has increased to ₹8,050 million.

The contractor determines the stage of completion of the contract by calculating the proportion that contract costs incurred for work performed upto the reporting date bear to the latest estimated total contract costs. A summary of the financial data during the construction period is as follows:

| (₹in Million) | |||

| Year 1 | Year 2 | Year 3 | |

| I) Amount of revenue agreed in contract | 9,000 | 9,000 | 9,000 |

| II) Contract costs incurred upto the reporting date | 2,093 | 5,957 | 8,050 |

| III) Contract costs to complete | 5,957 | 2,093 | —— |

| IV) Total estimated contract costs (II+III) | 8,050 | 8,050 | 8,050 |

| V) Estimated profit (I–IV) | 950 | 950 | 950 |

| VI) Stage of completion (II/IV) | 26% | 74% | 100% |

The amounts of revenue, expenses and profit recognized in the statement of profit and loss in the three years are as follows:

7.3.4 Revenue from Use of Entity’s Assets by Others

In addition to revenue from sales of goods and rendering of services, an enterprise may earn income by letting others use some of its assets. Revenue is recognized when it is probable that the economic benefits associated with the transaction will flow to the entity and the amount of the revenue can be measured reliably.

Interest

Interest accrues on a day-to-day basis on the amount outstanding at the effective rate of interest. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial instrument. To calculate the effective interest rate, future cash flows are estimated considering the contractual terms. Cash flows would consider all fees, transaction costs and premium or discounts. The discount rate that equates the discounted value of inflows and outflows is called effective rate of interest. Interest is accrued using the effective rate of interest so computed.

■ Illustration 7.6

XYZ Limited invested ₹75 million in zero coupon bonds with a maturity period of 3 years. The company paid ₹1 million to the broker. The maturity value of the bond is ₹100 million. Calculate the effective interest rate. How would the interest accrue over next 3 years.

The company has incurred ₹76 million (including brokerage) and would receive ₹100 million after 3 years. The effective interest rate would be calculated as the discount rate that equates the discounted value of ₹100 million (inflow) with ₹76 million (outflow).

Solving for k as the discount rate, k = 9.58%. Interest would accrue using the effective interest rate.

Royalty

Royalties accrue in accordance with the terms of the relevant agreement and are usually recognized on that basis unless, having regard to the substance of the transactions, it is more appropriate to recognize revenue on some other systematic and rational basis.

Dividend

Dividend on shares is recorded, when the right to receive dividend is established. Dividend is recommended by the board of directors of the company and after approval of the shareholders is paid to those shareholders whose name appears in the register of members of the company on the record date. It may be noted that unlike interest, dividend does not accrue on time basis and hence cannot be recognized on time proportionate basis.

Record date is the date fixed by a company to ascertain the eligibility to receive dividend or any other such benefit.

7.4 IMPACT OF UNCERTAINTY

For recognition of revenue the enterprise must be reasonably certain about its ultimate collection. If this condition is not met, revenue recognition may have to be postponed till the uncertainty is resolved. Such an uncertainty may be present at the time of raising a claim for sales of goods or rendering of services or may arise subsequently.

Uncertainty Prevailing at the Time of Raising Claim

In such a case, recognition of revenue is postponed till the uncertainty is removed and the enterprise is reasonably certain that the collection will be made. For example, extra billing to the customer due to escalation clause may be recorded only when confirmed by the customer rather that at the time of raising the invoice. Likewise, if income earned from foreign countries is subject to permission from authorities under foreign exchange regulations which makes remittance uncertain, revenue recognition may be postponed. Thus, the revenue may get recognized in the period when the uncertainty is removed.

Uncertainty Arising Subsequently

In such a case, the revenue recognized earlier is not altered but the impact of uncertainty is accounted for separately by making a provision for doubtful recoveries. As a result, the revenue may get recorded in one accounting period but the loss due to non-recovery may be recognized in a subsequent period.

■ Illustration 7.7

IMI Limited sold goods at an invoice price of ₹50 million on 28th February 2017 giving 90 days credit to the customer. On the due date of payment, i.e., 28th May 2017, the customer was declared insolvent and the amount due had to be written-off. How will this transaction affect the profit and loss statement for the year 2016–17 and 2017–18 assuming the financial year as the accounting period?

2016–17

As there is no uncertainty regarding collection, the revenue of ₹50 million will be recorded on accrual basis on 28th February 2017 by passing the following entry:

| Customer Account | Dr. | ₹50 million |

| To Sales Account | ₹50 million |

The same will reflect in the profit and loss statement for the year 2016–17.

2017–18

Once the customer is declared insolvent, loss due to non-recovery will be recorded by passing the following entry:

| Bad Debts Account (Loss) | Dr. | ₹50 million |

| To Customer Account | ₹50 million |

The loss on account of bad debts will appear in the profit and loss statement for the year 2017–18

7.5 DISCLOSURES

The following disclosures are required to be made in the annual report:

- The accounting policies adopted for the recognition of revenue including the methods adopted to determine the stage of completion of transactions involving the rendering of services.

- The amount of each significant category of revenue recognized during the period, including revenue arising from:

- The sale of goods

- The rendering of services

- Interest

- Royalties

- Dividends

- The amount of revenue arising from exchanges of goods or services included in each significant category of revenue.

7.6 ACCOUNTING FOR RECEIVABLES

Whenever goods are sold or services are provided on credit basis, the income gets recognized based upon the principles discussed earlier. The amount outstanding is debited to the customer’s account by passing the following entry:

| Customer Account | Dr. |

| To Sales/Income from Services Account |

On due date when the payment is received, the following entry is passed:

| Bank Account | Dr. |

| To Customer Account |

Amount Outstanding at the End of the Cccounting Period

The amount outstanding to be received at the year-end is shown in the balance sheet as a current asset under the heading ‘Trade Receivables’.

Provision for Doubtful Debts

At the end of the accounting period an enterprise anticipates that some of the customers may not pay up the amount due from them. In such a case following conservatism principle, it may decide to create a provision for such an anticipated loss by passing the following entry:

| Bad Debt Expenses Account | Dr. |

| To Provision for Doubtful Debts |

At the year end, the bad debt expenses account will be transferred to the statement of profit and loss and accordingly the profit for the period will get reduced. In the balance sheet, the provision for doubtful debts is shown as a deduction from the trade receivables.

■ Illustration 7.8

Strong Plastics Limited usually provides a credit period of 90 days to its customers. During the year 2017–18, the total sales of the company amounted to ₹325 million. Out of this, amounts aggregating to ₹220 million were collected from the customers. Based upon the past experience, the company estimates that about 5% of the amount outstanding will not be recovered and may have to be writtenoff. How will this information appear in the profit and loss statement for the year ending on 31st March 2018 and the balance sheet as on that date?

Statement of Profit and Loss

| ( ₹in Million) | |

| Income | |

| Sales | 325.00 |

| Expenses | |

| Provision for Doubtful Debts | 5.25 (5% of ₹105 million) |

| Balance Sheet | |

| Current Assets | |

| Trade Receivables | 105.00 ( ₹325 million less ₹220 million) |

| Less: Provision for Doubtful Debts | 5.25 |

| Net | 99.75 |

Summary

- Revenue recognition requires answers to two interrelated questions—quantum (how much) and timing (when) to recognize revenue.

- Amount of revenue is usually determined with reference to the agreement with the customer and is net of quantity discount, trade discount, sales return and indirect taxes (sales tax, VAT, etc.).

- Revenue from sales of goods is recorded when the ownership in goods has been transferred to the buyer and there is no significant uncertainty about the amount of consideration or its ultimate collection.

- Revenue from services can be recorded either on completed contract method or proportion completion method. Completed contract method is most suitable when the contract consists of a single act or the final act is so critical that without it the contract cannot be deemed to have been completed.

- Revenue from construction contract is recognized with reference to stage of completion of the contract.

- Interest income is recognized taking into account the amount lent, rate of interest and time period. Interest accrues on day-to-day basis. Income for royalties is recognized based upon the relevant contract with the user. Dividend income is recorded when the right to receive dividend is established.

- If at the time of sales of goods or provision of services there is uncertainty regarding ultimate collection of revenue, revenue recognition is postponed till the uncertainty is resolved. If uncertainty arises subsequently, a separate provision for loss is made.

Assignment Questions

- ‘Revenue is recognized when earned and not necessarily when received’. Explain.

- Discuss the principles of revenue recognition from sales of goods.

- How is the treatment of cash discount different from that of trade discount or quantity discount?

- How are the indirect taxes (excise duty, sales tax, value added tax, service tax) treated while recording revenue?

- Explain method of revenue recognition from services using proportionate completion method.

- What is the impact of uncertainty on revenue recognition?

Problems

- Amount of sales to be recorded: During the year 2017–18, the invoice value of goods sold by Avon Corporation amounted to ₹325 million. The company offered trade discount aggregating to ₹10 million. In addition, Goods and Services Tax (GST) @ 18% of the invoice price was collected by the company and paid to the government. The company normally sells goods on credit of 60 days and offers a cash discount of 1% if payment is made by the customer within 10 days of sales. How will the revenue from sales be shown in the statement of profit and loss for the year 2017–18?

- Revenue earned in foreign exchange: Fair White Limited is a FMCG company largely catering to domestic markets. During the year 2016–17, it received its maiden export order for $ 2 million for supply of fairness cream to USA. The order was duly executed on 1st November 2016. The supplier was allowed a credit period of 90 days for making payment. The rate of exchange on 1st November 2016 was ₹65, whereas by the payments was received on 30th January 2017 at ₹65.30. How will the above transaction appear in the statement of profit and loss for the year 2016–17?

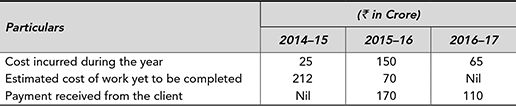

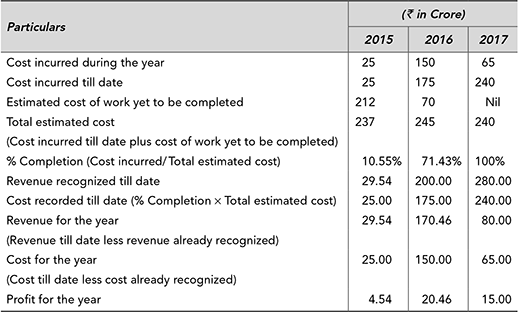

- Revenue from construction contract: Strong Structure Limited was awarded a contract for construction of a fly-over by the Government of Delhi on 1st October 2014. The contact consideration was fixed at ₹280 crore. The fly-over was competed on 31st December 2016 with the following details:

The company uses the percentage of completion method for recording revenue. The stage of completion of project is determined by the proportion that contracts costs incurred for work performed up to the balance sheet date bear to the estimated total contract costs. Show the revenue, cost and profit to be recorded from this contract.

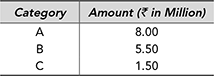

- Provision for doubtful debts: Ram Bharose Limited, a steel trader follows a very liberal credit policy of allowing 120 days to its customer to pay against their purchases. This policy has helped the company in attracting new customers but at the same time results in a high incidence of bad debts. As on 31st March 2017, the company has total debtors of ₹15 million. The company classifies its customers in three categories A, B and C based upon their credit worthiness. The break-up of ₹15 million of sundry debtors is given as follows:

Based upon the past experience, it is estimated that 2% of Category A, 3% of Category B and 5% of Category C may not pay when due and have to be provided for.

What will be the impact of the above in the profit and loss statement for the year and balance sheet as on 31st March 2017.

- Sales on instalment basis: Satyam Machines Limited is a manufacturer of high tech fabrication machines. Each machine is sold on cash down price of ₹3 million. The company also offers the same machine on instalment payment basis. The customers buying on instalment basis can pay the amount in three equated annual instalments of ₹1.3 million each at the end of next three years. The company sold a machine on 1st April 2017.

- When will the revenue from sales be recorded and by how much?

- How will you treat the difference between the cash down price ( ₹3 million) and instalment price ( ₹3.9 million)

- Accounting for accrued interest: RS Finance Limited is a non-banking finance company in the business of providing loans. On 1st October 2016, it gave a loan of ₹1,000,000 to Mr. Ram at 10% per annum to be repaid after three years. Interest is to be paid quarterly. Mr. Ram duly paid interest on 31st December 2016. However, it failed to pay interest due for the next two quarters. On 1st July 2017, the company classified the account as delinquent and decided to create a provision for the same. How will this transaction appear in the profit and loss statement for the year 2016–17 and 2017–18 and balance sheet on 31st March 2017 and 31st March 2018?

Solutions to Problems

- Revenue to be recorded:

(₹in Million) Sales at Invoice Price 325 Less: Trade Discount 10 315 GST collected by the company @18% will not be a part of revenue as this is collected by the company for onward payment to the government. Cash discount if and when availed by the customer by making prompt payment will be shown separately as an expense.

- Profit and loss statement for the year 2016–17

(₹in Million) Sales ($2 million at ₹65) 130.00 Gain on account of foreign exchange difference 0.60 ($2 million × (₹65.30 – ₹65.00) Sales will be recorded using the exchange rate prevailing at the time of sales. Subsequent exchange fluctuation will be recorded as a gain or loss without altering the revenue recorded earlier.

-

- Provision for doubtful debts to be made

2% of ₹8 million + 3% of ₹5.5 million + 5% of ₹1.5 million = ₹0.40 million

The necessary journal entry will be:

Bad Debts Expenses A/c Dr. ₹0.40 million To Provision for Doubtful Debts ₹0.40 million In the profit and loss statement for the year, bad debts expenses account will appear with other expenses at ₹0.40 million. In the balance sheet the trade receivables will appear as follows:

(₹ in Million) Trade Receivables 15.00 Less: Provision for Doubtful Debts 0.40 14.60 - The revenue for Satyam Machines Limited is arising from two different sources—sale of machine and interest earned on instalment sales. The sale of machine will be recorded on 1st April 2017 at the normal cash down price of ₹3 million.

The difference between cash down price ( ₹3 million) and instalment price ( ₹3.9 million) is the interest earned. As the instalments are being paid annually, interest earned ( ₹0.9 million) can be apportioned over three years in the ratio of 3:2:1. Accordingly, interest income will be recognized at ₹0.45 million, ₹0.30 million and ₹0.15 million, respectively in 2017–18, 2018–19 and 2019–20, respectively.

- In profit and loss statement for the year 2016–17, interest income for two quarters will be recorded as income based upon accrual basis of accounting. Accordingly, ₹50,000 will appear as interest income. In the balance sheet the loan amount of ₹1,000,000 plus accrued interest for the quarter ended on 31st March 2017 will appear on the assets side as loans and advances as follows:

(Amount in ₹) Loan amount 1,000,000 Add: Interest accrued but not received 25,000 1,025,000 The interest for quarter ended 30th June 2017 will accrue in the normal course and will be recognized as income. On 1st July 2017 once the company has decided to treat the account as doubtful, further accrual of interest will cease and a provision for doubtful debts will be created in respect of loan amount and the interest accrued till 30th June 2017.

Profit and loss statement for the year 2017–18 (Amount in ₹) Income Interest 25,000 Expense Provision for bad loans 1,050,000 Balance Sheet as on 31st March 2018 Assets Loan to customer 1,050,000 Less: Provision for bad loans 1,050,000 NIL

Try It Yourself

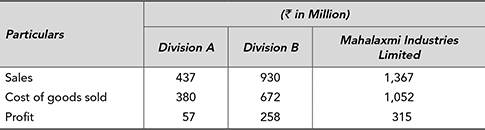

- Internal revenue: Mahalaxmi Industries Limited is engaged in the business of industrial chemicals. It has two divisions. The products of Division A are entirely sold to Division B on a cost plus basis. Division B further processes the goods procured from Division A and sells them in the market. During the year, Division A incurred a total expenditure of ₹380 million and the goods were sold to Division B for ₹437 million. Division B incurred further costs of ₹235 million and sold the goods in the market for ₹930 million. While preparing the profit and loss statement of the company for the year, the accountant aggregated the results of both the divisions as follows:

Accordingly, the company reported sales of ₹1,367 million and profit of ₹315 million. You are requested to comment upon the accounting policy of Mahalaxmi Industries Limited and if necessary redraw the profit and loss statement of the company.

- Quantum of sales: Desire Limited is in the business of manufacturing high fashion accessories. The company sold certain goods with an invoice price of ₹25 million to one of its customer offering him a discount of 2% on the invoice price. The customer is allowed three months credit; however; a discount of 1% is offered if payment is made within 30 days. The customer in this case made the payment within the discount period and availed cash discount. How will the above transaction appear in the profit and loss statement of the company?

- Timing of revenue recognition: In which financial year, will revenue be recognized in each of the following cases:

- Advance received from a customer on 31st December 2016. The goods are manufactured and invoiced on 1st April 2017.

- Goods sent to a commission agent on 15th January 2017. Goods sold by the commission agent on 28th April 2017.

- Loan of ₹ 10 million given to another company at 10% per annum on 1st March 2017 for a period of one year. The interest amount of ₹1 million deducted upfront from the loan amount. The loan is repaid in full on 1st March 2018.

- A Limited sold some of its investments to B Limited for ₹15 Million on 30th November 2016 with an agreement to buy them back on 31st May 2017 at ₹16 million.

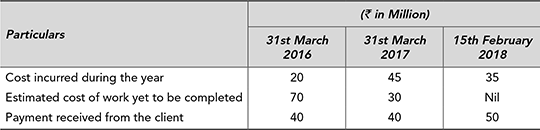

- Revenue from services: Shine Info Limited is engaged in software development business. It received a contract for developing and implementing software for credit risk management for a leading bank on 1st January 2016. The contact consideration was fixed at ₹130 million. The work was completed on 15th February 2018 with the following details:

The company uses the percentage of completion method for recording revenue. The stage of completion of project is determined by the proportion that contracts costs incurred for work performed upto the balance sheet date bear to the estimated total contract costs. Show the revenue, cost and profit to be recorded from this contract in the financial year 2016, 2017 and 2018, respectively.

- Uncertainty in revenue: Reliable Construction Limited is a real estate sub-contractor. It completed some work for a large construction company for a consideration of ₹8 million. In addition to the work scope defined in the beginning, the company also did some extra work at the request of the client. The cost of the extra work came to ₹400,000. The company wants to add a margin of 25% on cost and invoice the client accordingly. However, the consideration for the extra work was never discussed with the client. The company is debating between the following accounting treatments:

- Recognize revenue now at ₹8.5 million (including ₹500,000 towards extra work). If the client does not accept the invoice for the extra work the same can be recorded as bad debts subsequently.

- Recognize revenue now at ₹8 million, that is, the agreed consideration. Revenue of ₹500,000 for extra work will be recognized once the client accepts the claim for the extra work.

- Postpone the entire revenue recognition of ₹8.5 million to a future date till a confirmation from the client is received.

Please advice.

Cases

Case 7.1: Asian Computer Limited—Accounting Policy for Revenue Recognition

Asia Computers Limited is a newly established company in the information technology sector. The company has plans to gradually enter BPO and software development activities. In the initial phases, the company plans to concentrate on the following revenue generating activities:

- Sale of computers: The company buys computers of reputed brands and sells them for personal and office uses. To retail customers, computers are sold on cash basis, whereas commercial customers are given 60 days credit.

- Maintenance services: The company provides maintenance services for computers either on call basis or by entering annual maintenance contracts with its customers. In the former case, the customer pays every time maintenance service is provided. The cost of spares in such cases is also charged to the customer. In case of AMC, fee is charged yearly in advance. The AMC fee covers the service charges as well as the cost of parts that may have to be replaced.

- The surplus funds are kept either in fixed deposits with banks or invested in units of mutual funds.

Please help the company is framing suitable accounting policies for revenue recognition for the above mentioned activities.

Case 7.2: Internet Railway Ticketing Company Limited—Revenue from Sales versus Commission4

Super Fast Internet Railway Ticketing Company Limited provides service of booking railway tickets through the Internet. The company made investment for setting up of infrastructure for providing such services including computers, servers, printers, manpower, etc. The company has been given access to the ‘Passenger Reservation System’ (PRS) of railways for advance reservation. Any customer requiring booking of a railway ticket is required to register himself/herself with the company at its web site and thereafter the customer can send his request for booking of the ticket through the Internet. The company collects cost of the tickets and its service charges from the customer through credit card or direct debit to the customer’s bank account through its payment gateways. Tickets issued to the customers are either hand-delivered from its office or sent by courier at the address given by the customer.

The company maintains an advance deposit with the Railways. Payment to Indian Railways for the tickets booked by the company is made by way of adjustment against the amount being maintained as ‘Advance Deposit’ with the Railways. Statement for the cost of the tickets booked by the company is generated every day and the amount against those tickets is charged by the Railways from the deposit maintained with it.

The company levies service charges on its customers and the same is recovered in addition to the cost of the tickets. No fees or other remuneration is paid by the railways. The quantum of the service charge is exclusively decided by the company. Indian Railways does not interfere in any manner to decide the service charges made by the company from the customers.

In case of default, repudiation of transaction or non-recovery of cost of ticket, etc., the company is responsible for the same and not the Railways. In case of cancellation of tickets also, refund is allowed only by the company. Refund on the cancelled ticket is received by the customer from the company by way of direct credit into his credit card account/bank account. In short, while the company is responsible to Indian Railways for payment of the cost of tickets, it has to recover the cost of the tickets from the customers and also to pay refunds to the customers.

The accounting policy of the company for revenue recognition and expenses is given as follows:

- Income from Internet-ticketing: Income from Internet-ticketing is recognized on the basis of value of the tickets sold through the corporation’s web-enabled payment gateway including service charges.

- Expenditure on Internet-ticketing: The cost of tickets booked through the Passenger Reservation System of Indian Railways is recognized as expenditure on accrual basis.

Questions for Discussion

- Based upon the facts given, suggest appropriate accounting policy for the company for revenue and expenses recognition?

Case 7.3: Asian Paints Limited—Change in Accounting Policy Relating to Captive Consumption

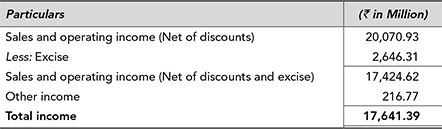

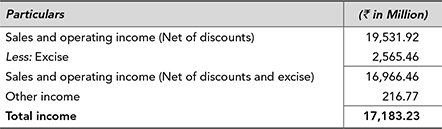

Asian Paints is India’s largest and Asia’s third largest paint company. It manufactures a wide range of paints for decorative and industrial use. For the year 2003–04, the company reported a total income of ₹17,641.39 million and a net profit of ₹1,477.87 million. The breakup of the income as reported in the profit and loss account is given as follows:

The sales and operating income includes a sum of ₹539.01 million as inter-division transfers. The accounting policy of the company states that ‘Inter-division transfers of finished goods for captive consumption are valued at market price. The value of such inter-division transfers is included in the materials consumption of the consuming divisions. The year-end stock of such transferred goods is valued at cost.’

The next year (2004–05) the company decided to change its accounting policy. The revised accounting policy of the company stated that ‘sale of products is recognized when the risks and rewards of ownership are passed on to the customers, which is on dispatch of goods. Sales are stated exclusive of sales tax. Processing income is recognized upon rendition of the services.’

The company further states that ‘Hitherto, the company has been recognizing inter-division transfers of Phthalic Anhydride and Pentaerythritol to paint plants for captive consumption as revenue and the same was disclosed separately in “Sales & Operating Income”. The value of such inter-division transfers was included in material consumption of the consuming divisions. With effect from the financial year ended 31st March 2005, the company has discontinued the method of recognizing interdivision transfers as sales as well as material consumption. The previous year’s figures have been restated accordingly. The above change in the method of revenue recognition has resulted in a reduction in net sales and operating income by ₹600.28 million (previous year ₹458.16 million) with a corresponding reduction in material consumption and has no impact on the profits of the company’.

As a consequence of the change, the company recasted the figures for the year 2003–04 as well. The recasted income details are given as follows:

Though the company reported a lower total income there was no impact on the profit after tax.

Questions for Discussion

- Sales and operating Income are shown net of discounts and excise duty. Why?

- Is inclusion of inter-division transfers in the income consistent with the requirements of AS 18?

- What is the impact of such inclusion on the total income and net profit of the company?

Case 7.4: MMTC Limited: Revenue Recognition for back-to-back Transactions

MMTC Limited was established in the year 1963. It is a leading international trading company in India. It was awarded the status of ‘five star export house’ by the government of India for its contribution to exports.

For the year 2004–05, the auditors of the company issued a qualified report raising questions about the accounting policy regarding purchase and sale. The audit qualification in this regards is stated below:

‘In terms of Accounting Policy No. 1(b) regarding accounting of certain transactions as sales/purchases where letters of credit in the name of the company are assigned in favour of Business Associates and Accounting Policy No. 1(f) where purchases of some commodities are booked based on sales value less service charges, the company has treated sales of ₹27,896,466 thousand and purchases of ₹27,246,587 thousand (to the extent details made available and including canalized items) during the year as its own, as per past practice. On examination of the facts, circumstances and the manner of effecting these transactions, we are of the opinion that the sales and purchases booked by the company are not its own and as such, the above, accounting policy is not in conformity with Accounting Standard 9 “Revenue Recognition” issued by the Institute of Chartered Accountants of India and the guidelines issued by the Department of Public Enterprises. As a result of this policy, sales and purchases have been overstated by ₹27,896,466 thousand and ₹27,246,587 thousand, respectively. However, this policy has no effect on the profit of the company for the year. (Refer Note No.7.1 & 7.2)’.

The accounting policies and notes to account referred to by the auditors as aforesaid are reproduced as follows:

Accounting Policies:

- Purchase and sales

- b) Purchase/Sales include transactions/shipments where L/C (Letter of Credit) in the name of MMTC, are assigned in favour of the business associates.

- f) In respect of some commodities, purchases are booked based on sale value less service charges.

Notes to Accounts

7.1 Purchases and sales include ₹2,924,538 thousand (P.Y. ₹945,000 thousand) and ₹2,932,176 thousand (P.Y. ₹952,730 thousand), respectively, transactions/shipments where LCs in the name of MMTC has been assigned in favour of associates. The above includes canalized sales amounting to ₹1629,115 thousand (P.Y. ₹583,500 thousand and corresponding purchase of ₹622,824 thousand (P.Y. ₹576,300 thousand).

7.2 Sales amounting to ₹24,964,290 thousand (P.Y. ₹13,848,820 thousand) and corresponding purchases of ₹24,322,049 thousand (P.Y. ₹13,463,360 thousand) have been booked on the basis of invoice value reduced by the amount of service charges. The above includes canalized sales amounting to ₹15,894,621 thousand (P.Y. ₹6,203,680 thousand) and corresponding purchase of ₹5,488,915 thousand (P.Y. ₹6,048,070 thousand).

The company reported a total sale of ₹151,237,206 thousand for the year 2004–05 (P.Y. ₹90,991,892 thousand).

Questions for Discussion

- Critically evaluate the accounting policy of MMTC Limited regarding booking of purchases and sales?

- What is the impact of the above accounting policy on the financial performance of the company?

- How will you justify the accounting policy of MMTC Limited to the auditors in view of the qualification made by them?

Endnotes

- ICAI: Ind AS 21, ‘The effects of changes in foreign exchange rates’.

- ICAI: Ind AS 18 ‘Revenue’

- ICAI: Ind AS 11, ‘Construction Contracts’

- Based upon the query 10 in Compendium of Opinions of ICAI, Volume 24