CHAPTER 3

Project Formulation

After having gone through this chapter, you should be able to

• Oversee contents of feasibility report

• Understand technical aspects of a project

• Appreciate managerial aspects of a project

• Identify the commercial details of a project

![]() Analyze project rationale

Analyze project rationale

![]() Estimate project cost

Estimate project cost

![]() Estimate project operating cost

Estimate project operating cost

![]() Understand project operating revenues

Understand project operating revenues

![]() Estimate project profit, that is, excess of revenues over cost

Estimate project profit, that is, excess of revenues over cost

• Appreciate financial aspects of a project

• View economic aspects of a project

• Appreciate examples of some projects and project management practice

Key Terms: Project cost, operating cost, Project Revenue, Cash inflows, Cash outflows, Financial Ratios, Discount rate

Having identified a project, preparation of the project report is an important task of project management. For example, when we approach a bank for financial assistance, the first thing a banker asks is have you brought the project details? He is referring to the feasibility report of the project for which financial assistance is being sought. Banks and regulatory bodies like Planning Commission normally prescribe the details expected in a feasibility report. The feasibility report is the basis of appraisal by banks or regulatory bodies having stake in the project. In other words, feasibility report is a comprehensive and systematic compilation of data relating to various aspects of a project, namely,

• Technical aspects

• Managerial aspects

• Commercial aspects

• Financial aspects

• Economic aspects

The above aspects are not sequential and at times overlap. These aspects are detailed below.

Technical Aspects

This section lays down details regarding

• Technology to be adopted: Is it indigenous or foreign, has it been used earlier in some other project, and what is the experience of the same?

• Manufacturing process: What process is planned so as to understand its cost and other implications?

• Location of the project: Land availability including for township, so as to see its impact on regional development or entitlement of subsidy, if any.

• Availability of utility services, other services, and manpower.

• Environment: Existing in terms of its effects on population, water, land, air, and flora and fauna.

• Equipment and construction requirements: Size and type required and capacity utilization.

• Transport requirements for bringing in of the raw materials and other inputs and also outward movement of the goods produced.

• Phasing of construction and production as it would have impact on financial requirement and also on the goods produced.

Managerial Aspects

Human resources are the soul of the project, and success of a project to an extent depends upon effectiveness of human resources. For example, of two projects of similar size, one is more successful purely because of its effective or result-oriented human resources. It all depends upon the management, their background, professional qualification, and experience and also arrangements for development for human resource; for example, in an agriculture project, does the management have expertise in agriculture or do they plan to have human resources with that background. Banks also examine the credit worthiness of the entrepreneur. Besides his financial standing or soundness, the bank also analyses whether he has defaulted payment in the past. Banks these days attach greater importance to the managerial aspects and have behavioral workshop with the management. Such details of behavioral aspects are beyond the scope of this book.

Commercial Aspects

It relates to details covering setting of the project, justification in terms of marketing of its products, project cost, cost of operations, operating revenues, and its profitability. Various areas relating to commercial aspects include

Project Rationale: What is the Justification of the Project?

What are the demand and supply estimates for the product/service for future years? Demand forecast is carried out for the future years in terms of existing level of demand as well as demand both for domestic markets and for export markets to be tapped in future due to changing economic scenario. Similarly, supply is estimated in terms of the existing manufacturers and also the new expected establishments, both within the country and abroad. With liberalization and deregulations, in contrast to regulated economy, the aspect of demand–supply estimates has become a complex task as geographical boundaries no longer exist as exports and imports from the foreign markets, many a times, are freely allowed.

As such, such estimates should indicate that the demand outstrip supply and the product produced will have market. Many a time efforts are made to create demand for the product. Such examples are given below:

• Deploying students to go to various stores asking for a particular brand of toothpaste; this was simultaneously advertised on TV, before it was launched in the markets.

• Inserting a matrimonial column in a newspaper, “Wanted a groom having the qualities of a hero of a particular novel,” that pushed the sale of that novel.

Estimate Cost of the Project

Project cost estimate should be realistic considering future needs and it includes

• Fixed assets including costs of land, civil works and buildings, equipment and machinery, engineering services, and in-plant infrastructure

• Outside plant infrastructure, like township

• Start-up costs or trial run cost

• Working capital

• Interest during construction period

The above are normally one-time costs and as such are nonrecurring. However, project construction may spread over a number of years, or the project may be in various phases; in that case, the above costs may be spread over various years. Cost elements of a project are illustrated in Box 1.

Following principles for the project cost are relevant:

i. Cost comprises of all expenses related to the project and incurred to bring it in working condition, that is, the condition it is intended.

For example, cost of an automobile purchased which is intended to be driven would include all cost related to the car and incurred up to the stage of bringing it in a state that it can be driven on the road. Accordingly, road tax, car insurance, and registration charges would be included in the cost of a car as these are required before the car is driven on the road. However, any expense incurred on learning how to drive the car or toward driving license fee would not be included in the cost of the car, as these are not related to the car.

Similarly, cost of computer purchased for the office would include its purchased price, cartage, insurance, and installation expenses as these have to be incurred to bring the computer into operating stage.

Expenses incurred on trial run or preliminary expenses incurred for setting up of the project are included in the project cost. For example, as a part of the setting up of the project, two engineers were invited for the trial run or for pretest which involved a cost of Rs. 300 lakhs. But that pretest yielded some output valued at Rs. 50 lakhs. Accordingly, the net cost of trial run of Rs. 250 lakhs would be included in the project cost.

Project cost includes—as an illustration:

Land and building: Site development; township

• Plant and machinery

• Furniture and fixture

• Office equipment

• Hardware

• Software

• Railway siding

• Livestock

• Intangibles: License, patents

• Preliminary expenses

• Working capital: Margin

• Interest during construction period

• Contingencies

ii. All expenses incurred after the project has been brought into working condition are not included in the project cost.

iii. Financing costs, like interest, related to the project and incurred up to the stage of bringing into working condition are included. However, interest incurred after the project is operationalized or interest paid in general not specifically for the project in question is not included in the project cost.

iv. Administrative and other general expenses related to the project are included in the project cost, if these are specifically attributable to the project.

Ascertain Cost of Production

This cost relates to carrying out manufacturing operations and would depend upon the level of operations and capacity utilization which may vary over the years. As such, this cost is recurring one and is necessary for carrying out the operations. Elements of operating cost are illustrated in Box 2.

Operating Cost Elements: An Illustration

• Materials

• Expenses on components acquired

• Manpower expenses

• Utilities

• Repairs and maintenance

• Travel

• Rent, rates, and taxes

• Publicity

• Security expenses

• Legal expenses

• Depreciation and amortization

• Interest on borrowings

For example, a production unit having a capacity to produce 1,000 units per day is operating at 60 percent in the first 2 years and at 80 percent thereafter; various operating expenses, as illustrated in Box 2, will be estimated at 60 percent level for the first 2 years and at 80 percent level thereafter.

Estimate Project Revenues

This would depend upon the estimated number of units to be sold and the expected selling price for the future years However, for social and community development projects, minimum economic benefits or reduction in operating costs is proxy for the projected revenues.

For example, for highways projects: “avoidable costs,” that is, reduction in vehicles’ operating costs and road maintenance are proxy for revenues estimates.

Similarly, for irrigation projects, expected increase in agriculture production after irrigation is the basis for revenue estimation; and for agriculture projects, market value of estimated increase in output is proxy for revenues.

For public utilities like power or waterworks, administered prices are the basis of revenue estimates. In case, benefits to consumers exceed administered price, the value of economic benefits is the revenue. Similarly, for social and community development projects like education, health, and population planning, opportunity cost for rendering of the services is the basis of revenue estimation.

Surplus (Deficit) from Operations—Year Wise

From the estimates of operating costs and revenues, surplus or deficit is calculated for different years. In other words, surplus is estimated revenues (d) minus estimated operating costs (c) for different years. In commercial terms, surplus (or deficit) is called profit (or loss).

Financial Aspects

Arranging finances for a project and also deciding about mix of various sources are important tasks for the project manager. Traditionally, sources of funds include owners’ fund, popularly known as equity and debt. Promoters’ contribution is supplemented with funds raised from the public. Banks and financial institutions contribution is primarily in the form of debt, but this have different variants each having different implications. In addition, the funds may be for a short period or long period. The following two principles should be the guiding factors for finalizing finances for a project:

• Match funds requirements for a project with the funds availability. Avoid using short-term funds for the project requirements which are normally of long-term nature.

• Have a capital mix so as to minimize financing cost and the restrictive covenants attached.

(Details of finances of a project are discussed in Chapter 6 Vol. 2).

In addition, banks adopt various financial techniques to analyze a project. These include

• Financial ratios:

![]() Profitability

Profitability

![]() Liquidity

Liquidity

![]() Solvency

Solvency

![]() Activity

Activity

• Break-even level calculation: It is the level of operation with no-profit-no-loss or a situation where

• Total revenues = Total costs, that is, no-profit-no-loss

For that purpose, look for a level of capacity utilization, where

![]() Total revenue equals total cost or

Total revenue equals total cost or

![]() The year in which the break-even level is attained, earlier the better

The year in which the break-even level is attained, earlier the better

(These aspects are beyond the purview of the text.)

Further, infrastructure projects have different characteristics and private sector is being involved in developing and managing such projects. Development of Indira Gandhi International Airport in Delhi by involving GMR is a recent example. Private sector is involved through approaches like BOOT/BOT/BOLT. Under these approaches, the private agency has three roles:

• Designer or constructor

• Financer

• Operator

Securitization is another approach of financing projects.

(Details regarding infrastructure projects development and their financing are discussed in Vol. II Chapters 8 and 9.)

Economic Aspects

In this section, we look at the economics of a project, that is, to estimate its cash inflows and cash outflows for future years and to analyze these cash flows. In other words, it has following two aspects:

i. Cash flows estimation: That is, estimate cash outflows and cash inflows over the life of the project. Cash outflows are outflows on account of project cost and are normally at the beginning of the project and may occur in later years also. Cash inflows are annual cash inflows arising from sales after meeting operating cash expenses over the years.

ii. Appraisal techniques: Various techniques are used to analyze the inflows and outflows.

A word of caution while analyzing the cash flows:

• There is no one Best Technique.

• Every technique has some strong points.

In that respect, management judgment is supreme for appraisal and for deciding about the project.

(Appraisal techniques are discussed in the next chapter.)

Cash Flows Estimation

• Cash outflows are project cost as discussed above.

• Cash inflows are estimated on profit after tax (PAT) basis. However, for macro projects or for socio/community development projects where there is no profit element, profit before tax is the basis of cash inflows.

• In other words, cash inflows are PAT + depreciation + interest

where

![]() Depreciation is a part of project cost; it is a noncash expense or is merely a book entry and does not involve cash payment

Depreciation is a part of project cost; it is a noncash expense or is merely a book entry and does not involve cash payment

![]() interest charge being a “Transfer Payment” is not considered as an expense while estimating cash inflows

interest charge being a “Transfer Payment” is not considered as an expense while estimating cash inflows

For cash flows estimation see the following illustrations:

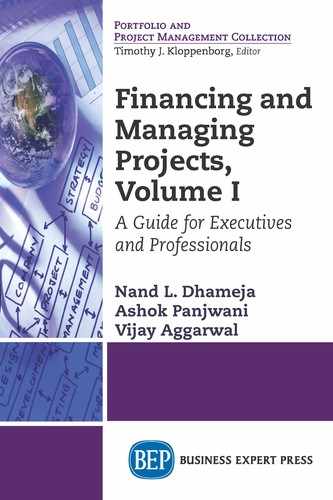

Illustration 3.1

Cash flows calculation (uniform revenues and no tax)

• Project cost: Rs.30,000

• Finances: Equity 10,000; 10% debt 20,000, i.e., project outflows = Rs. 30,000

Operations:

• Sales revenue Rs. 40,000 pa; depreciation Rs. 5,000 pa, and interest expenses Rs.2,000 pa

• Project life 5 years

• No gestation period

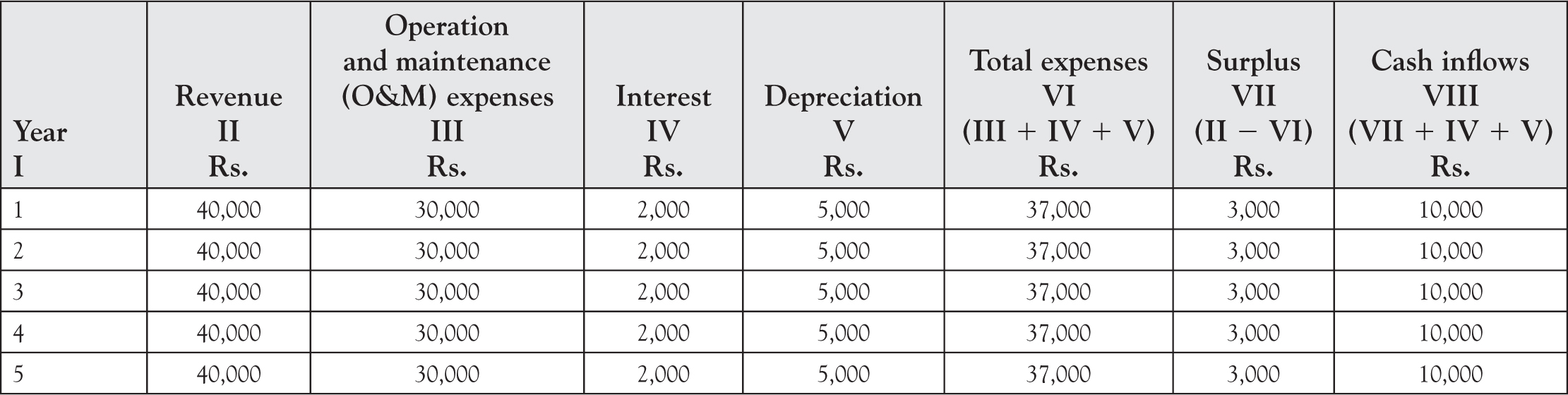

Illustration 3.2

Cash flows calculation (increasing revenues and corporate tax 40%)

• Project cost: Rs. 25,000, i.e., project outflows = Rs. 25,000

• Finances: Equity 10,000 and debt 15,000

Operations:

• Increasing sales revenue

• Uniform depreciation Rs. 4,000 pa

• Interest charges Rs. 1,200 pa

• Life 5 years

• No gestation period

Instances for Discussion

Mahindra Stake in Ssangyong Unit

Mahindra and Mahindra planned to raise its holdings in Ssangyong Motor Co. to 72.85% in a 80 billion Korean won ($73.73 million) investment.

Mahindra, India’s biggest sports utility vehicle manufacturer, would subscribe to preferential shares issued by Ssangyong. This was to facilitate new product development and to strengthen the South Korean company’s financials. The payment was expected in May 2013.

Real Estate Project: Macquarie Infrastructure and Real Assets

Macquarie Infrastructure and Real Assets (MIRA), an arm of Australia’s Macquarie Group Limited, plans to invest in real estate projects in India. The company manages over $100 billion of assets. The company in India, Macquarie Infrastructure and Real Assets (India) Pvt. Ltd, would be managed by R. K. Narayan who was earlier a consultant with real estate investment firm AevitasProperty Partners and also served as the chief operating officer at Infinite India Investment Pvt. Ltd.

MIRA is planning to invest in luxury residential projects jointly with Tata Housing Development Co Ltd, a subsidiary of Tata Sons.

MIRA is a large infrastructure asset manager globally and also has portfolio in real estate agriculture and power across. Its real estate portfolio includes 20 retail, commercial, residential, and industrial properties in China, Mexico, and Australia. (Source: Mint, October 27, 2015).

Brief Case Studies

Tata Sampann: Consumer Products and Food Division

Tata Chemicals Ltd, maker of branded salt and pulses, announced its entry into spices business, and all its consumer products and food segment, such as I-ShaktiBesan (gram flour) and pulses, would come under the Tata Sampann brand except iconic Tata Salt. This was with the objective to treble revenues from the consumer product business to Rs. 5,000 crores in the next 4 years. The move is to focus on quality assurance and play in the mass-market space and better value proposition. The company had been selling pulses since 2010 under the I-Shakti brand and the same network would be used for spices and products that would be launched in the future.

It has planned to launch single-use sachets of spices (five small sachets of 20 gm each in a 100 gm packet). Tata Chemicals had a strong presence in fertilizers, chemicals, crop protection chemicals, specialty fertilizers, and branded food products and food additives.

The overall food market in India is estimated at about Rs. 6 trillion crores; the packaged food market was estimated at Rs. 20 billion in 2014; the spices market in India is estimated at Rs. 40,000 crores, of which just 15 percent is branded.

For sources of pulses, the Tata Chemicals has engaged 150,000 farmers, an initiative led by Rallis India Ltd, a Tata Enterprise. This was to monitor the entire supply chain—from farm to consumer to ensure quality. Tata Chemicals planned to expand its retail footprint to about 2.5 million outlets from the current 1.43 million.

The other fast moving consumer goods (FMCG) providers include ITC Ltd, Hindustan Unilever Ltd; and Swiss packaged food company Nestle India Co. Their retail outlets include 4.3, 6.3, and 4.5 million, respectively.

Sanad Hospital in Riyadh, Saudi Arabia

Aster DM Healthcare, a company owned by Dubai-based Indian billionaire Dr. Azad Moopen, acquired from a Saudi partner, in October 2015, 57 percent stake in Sanad Hospital in Riyadh, Saudi Arabia, for Rs. 1,600 crores, taking its total stake to 97 percent. Earlier 40 percent stake was acquired in December 2011. Thus with the recent acquisition of 57 percent stake, Aster DM Healthcare had become a majority stakeholder.

The deal closed after the necessary clearance from the Saudi Arabia General Investment Authority (SAGIA), the body that takes foreign investment-related decisions in the kingdom. The Kingdom of Saudi Arabia allows 100 percent foreign investment in hospitals provided a player can prove that he would bring in capital and expertise.

With the above acquisition, Rs. 420 crore Aster’s footprint in West Asia extended to all six Gulf Cooperation Council (GCC) countries and Jordan. The healthcare company that operated through a portfolio of hospitals, clinics, and pharmacies had five green field projects underway in GCC, one hospital in Qatar and four in the United Arab Emirates.

Under the company’s two-pronged growth approach, India where the company ran eight hospitals continued to be a focus market for Aster. Further, the company had invested Rs. 550 crores in Aster Medicity in Kochi and was putting in nearly Rs. 230 crores in Aster CMI Hospitals in Bengaluru. As per the policy of the company, “In India we see an opportunity in both mid and long term. Our focus will be to build a position of strength in South and West. And we also see medical tourism as an interesting opportunity.”

The company which started Indian operation in 2001 had three hospitals in Kerala (Calicut, Kottakal, Kochi), two in Maharashtra (Pune, Kolhapur), two in Telangana (Hyderabad), and one in Karnataka (Bengaluru). As per the policy, “In India and abroad we like to follow model that involves taking a majority stake. It allows us accountability and also flexibility to do various things.” As such, Aster had a bed capacity of 2,022 in India compared to 517 in GCC.

Dr. Azad Moopen was awarded Padma Shri and belongs to the set of Maayai entrepreneurs like M. A. Yussuff Ali, Ravi Pillai, Sunny Varkey, and P. N.C. Menon. (Source: Economic Times, October 12, 2015).

Plaza Cables Ltd: Estimation of investment outlay in a machine

Plaza Cables Ltd (PCL) is contemplating to replace its old equipment by a new sophisticated one costing Rs. 10 crores plus 8 percent sales tax. PCL will be getting a discount of 10 percent on the equipment cost from the supplier in Bengaluru. The transportation and insurance will cost Rs 1 lakh each. In addition, the installation will cost another Rs. 5 lakhs. The equipment being sophisticated one, there will be production trials to ensure proper adjustments; the trial runs will cost Rs. 10 lakhs of which 4 lakhs will be realized from the produce of production trials.

The new equipment would necessitate an increase in minimum level of inventory by Rs. 15 lakhs. In addition, the old machine having a book value of Rs. 40 lakhs is estimated to be sold for Rs. 20 lakhs, the company is entitled to save @ 20 percent on capital loss on account of the sale of old equipment.

Bright Motors Company: Estimation of Cash inflows for a Project

Bright Motor Company (BMC) is planning for a project to add a new production unit at Manesar, Haryana. Mr. Mohan Rai, member of the project team is involved with the task of estimation of cash inflows from the project operation. Production operations for the project are estimated as under:

Capacity utilization |

60% |

Sales pa in units in crores |

6.00 |

Sales (crore Rs.) |

180 |

Operation expenses (crore Rs.) |

|

Raw material and components |

100 |

Manpower cost |

20 |

Factory supervision cash cost |

10 |

Administrative and other expenses |

10 |

Marketing and publicity expenses |

5 |

Gross profit (PBDIT) |

35 |

Depreciation |

10 |

Profit before interest and tax (PBIT) |

25 |

Interest on borrowings |

5 |

Profit before tax (PBT) |

20 |

Tax 25% |

5 |

Profit after tax |

15 |

Requirements:

Estimate cash inflows from the project

HIsmelt Plant in Australia Relocated to China and not to Jindal Steel and Power Ltd (JSPL), Orissa

Managements of Jindal Steel and Power Ltd (JSPL), Orissa, and Rio Tinto, Australia, had agreed on August 5, 2011, to relocate the existing HIsmelt plant from Kwinana in Australia to India at JSPL’s existing facility at Angul in Orissa. The relocated plant was to be fully owned by JSPL, and the Indian company and Rio Tinto were to work together to further develop and market the technology.

As against the above arrangement, the HIsmelt technology plant in Australia had been dismantled and sent to China and not to JSPL in Orissa on the understanding that the Chinese company Molong had more urgent need for the technology. Molong’s normal supplies of liquid pig iron were stopped for environmental reasons and was not allowed to build conventional blast furnaces. For environmental reasons, HIsmelt was the only technology capable of producing liquid pig iron at the required capacity and environmental standard. It is viewed that China leapt ahead of Jindal and got HIsmelt plant.

Further, it was argued that bringing the plant to India involved “too many changes” and so it was relocated to a Chinese company as “a pilot plant.”

After the pilot run in China, JSPL would build a plant at its Angul site with the HIsmelt technology with a capacity of 1 or 1.2 mt and this was envisaged for construction in 2015 with the production starting the next year.

HIsmelt—short for high-intensity smelting—is a technology owned by Rio Tinto and is said to be ideal for India. JSPL could directly use iron ore fines and noncoking coal, abundantly available in India, and it is said to be environmentally friendly and more economical than traditional methods.