CHAPTER 8

Infrastructure Project Financing

PPP Approaches and Experiences—India and Abroad

After having gone through this chapter, you should be able to

• Understand meaning of PPP

• Appreciate various types of PPP and their features

• Oversee private sector involvement and PPP projects in India

• Appreciate snapshot of infrastructure projects under diverse PPP approaches in various countries and different sectors

• Oversee the comparison of prevalence of PPP in financing infrastructure projects in India and China

Key Terms: Public–Private Partnership (PPP), Private Finance Initiative (PFI), Special Purpose Vehicle, NGO, Service Contract, Management Contract, Lease, Concession, BOOT, BOT, Greenfield Project, Divesture

Having discussed in the previous chapter the meaning of infrastructure, its significance for economic development, massive investment planned during five-year plans, and the need to involve private agency for financing and development of infrastructure, this chapter is devoted to adoption of public–private partnership (PPP) for financing of infrastructure, its meaning, mechanism, various variants and forms, and their comparisons. This chapter presents a snapshot of PPP approach for financing of infrastructure projects in India—sector-wise—for various states and the contract award methods adopted. A snapshot of PPP approach in different regions, countries, and sectors is also presented.

Public–Private Partnership: Meaning

PPP is defined as “any arrangement between a government and the private sector in which partially or traditionally public activities are performed by the private sector.”1 PPP is commonly used in two different ways. In broad terms, it refers to arrangement in which the public and private sectors join together to produce and deliver goods and services. Alternatively, PPP refers to long-term contractual partnership between the public and private sector agencies, specifically targeted toward financing, designing, implementing, and operating infrastructure facilities and services that were traditionally provided by the public sector. Further with the growing urbanization, governments are unable to service the rapidly growing urban population, in particular, when their budgetary resources are constrained and are associating private sector in the delivery of infrastructure and public services. This collaborative arrangement is built around the expertise and capability of project partners. Under the arrangement, the private sector participation is helpful in bringing in technical and managerial expertise, improving operational efficiency, infusing financial resources, and introducing competitiveness. Private sector could take the form as a private company, a consortium, or a nongovernmental organization (NGO); a foreign state-owned enterprise is also considered a private entity. The consortium often forms a “special purpose vehicle” (SPV). As such, the private sector goes beyond their usual role in the marketplace and becomes involved in social services like education, medical care, housing, and urban development.

For example, for the upgradation and modernization of Delhi Airport, Delhi International Airport Limited (DIAL), a joint venture consortium was formed as a private limited company, through a global competitive bidding. Members of the joint venture included GMR and Airport Authority of India (AAI). GMR was a lead member having the experience of developing the Hyderabad International Airport.2

PPP does not reduce responsibility and accountability of the government; the governments remain accountable for service, quality, price certainty, and cost-effectiveness; in fact the role of government gets redefined as one of facilitator, and enabler, while private sector plays the role of financier, builder, and operator of service. Under PPP approach, the skills, expertise, and experience of both public and private sector get combined to deliver higher standard service to the consumers. The public sector contributes assurance in terms of stable governance, citizens’ support, and financing and also assumes social, environmental, and political risks. The private sector brings along operational efficiencies, innovative technologies, managerial effectiveness, and access to additional finances and takes on construction, commercial, and operational risks of the project.

PPP differs from privatization as the former refers to private management of public services through long-term contract between an operator and public authority, while privatization involves outright sale of public service or utility to the private sector.

Since PPP is a long-term contract, it involves complex planning relating to risk management, cost recovery, tariff fixation, construction, financial planning, regulatory policy, and governance issues. PPP approach is not new; it was followed a few centuries ago. In sixteenth and seventeenth centuries in France, roads and bridges were given on concession for tolls in return for maintaining the routes. Canals were built and water was collected and distributed under concessions. By the 1820s, there were six private water companies operating in London. Water works in the United States were with private entities at the beginning of the nineteenth century. Electricity utilities in the nineteenth century in Brazil, Chile, Costa Rica, and Mexico were private utilities. In Argentina, Brazil, and Uruguay, private developers from Britain, France, and the United States built and operated many of the early railways in the nineteenth and twentieth centuries.3

Private Finance Initiative (PFI),4 a form of PPP involving private sector in the provision of public services, was introduced by the Conservative government in the United Kingdom in November 1992. It continued under the Labour government in 1997. From inception in 1992 until 2001, 459 PFI contracts were signed valuing UK pound 20 billion. PFI projects range from small projects, such as a school, to mega construction projects like the London Underground.

A form of PPP, PFI combines public procurement policies and long-term contracting out. Unlike many other PPPs, a PFI project has the private sector contractor arranging finance. PFI has been assessed on the following three criteria:

• Whether it will release resources for additional investment in social infrastructure?

• Whether it will provide value for money?

• Whether the use of PFI will reduce the public sector’s flexibility to pursue its public service objective?

Public–Private Partnership: Features5

PPP is a long-term contract; it involves complex planning relating to risk management, cost recovery, tariff fixation, construction, financial planning, and regulatory policy and governance issues. As such, PPP contracts have the following features:

• Collaboration: It involves sharing of both responsibility and risk in a collaborative framework. It seeks to draw upon the best available skills, knowledge, and resources—whether public or private.

• Focus on Service: The emphasis is on services received by government, not government procurement of economic or social infrastructure, and the government pays for the services.

• Length: It normally entails long-term relationship.

• Trust: The partnership is a high-trust relationship.

• Whole-of-life costing: Under PPP, there is a complete integration under one party of up-front design, construction, delivery, and operating cost.

• Innovation: PPP focuses on output specification and provides for enhanced opportunities and incentives for the bidder.

• Risk allocation: Government retains the risk of owning while operational risk is with the private party.

• Type: PPP arrangement is flexible and can take various forms discussed latter.

Private Sector Involvement in Infrastructure: Mechanism

Involvement of private sector in infrastructure would involve the following process:

• Conceptualization: Preparation of project technical specification laying down the broad outline of the project

• Commercialization: Ascertaining operating cost and service cost per unit which users will have to pay

• Involvement of private agency in development of project: Laying down the timeframe for completion and other conditions relating the project development and operation

• Negotiation of tariff rates/revenues on the principle that the private agency will be able to recover operating costs and investment costs during the period of the operation of the project, say 30 years

• Financing: Arrangement of finances for the project which may be on nonrecourse or recourse basis

• Transfer of project to government after stipulated period, say 30 years

Spectrum of PPP

Various forms of PPP have been adopted in different countries for various infrastructure projects. PPP as per World Bank data may take the following forms6:

Service Contract: Specific services associated with infrastructure are contracted out to a private firm for specific time period in return for a management fee. The public agency, that is, the government retains overall responsibility for the operation and maintenance of the system except for the particular contracted service and it bears all of the commercial risk. The agency finances fixed assets and provides working capital. Compensation to the private firm is generally on bases like time, or lump sum, or fixed fee, or cost plus, or on the basis of a physical parameter (number of water bills sent out, or number of bed roles supplied, etc.). Examples of such services include ticketing, bed roles, cleaning, and food catering for rails; billing and collection for water and electricity.

Management Contract: The private entity performs specific tasks under a management contract for a period and gets payment from the government. The government owns the facility and also retains the ownership and investment decision making. This arrangement is similar to a service contract, but in the former case the private party has overall responsibility for operating and maintaining the system and makes the day-to-day decisions; however, it does not assume any capital risks.

Lease: A private entity is given a long-term lease to develop (with its own funds) and operate an expanded facility. The private entity pays lease rental to the government, is entitled to keep the revenues to recover its investment plus a reasonable return over the term of the lease and assumes the operational risks. Examples are leasing of Delhi airport to GMR and Mumbai airport to GVR.

Concession (BOOT, BOT, etc.): A private entity is awarded a franchise (concession) to finance, build, own, and operate the facility, has a right to collect user fee for a specified period, and also assumes significant investment risk. After the expiry of the contract period, the ownership of the facility is transferred to the government. This is similar to lease and is common form of PPP to build infrastructure. (BOT stands for “build, operate, and transfer” while BOOT refers to “build, own, operate, and transfer”). As discussed latter, under BOOT the concessionaire also gets ownership rights of the land and other assets for the period of the concession agreement, and this is preferred by the concessionaire as it enhances his credit worthiness and he is able to raise funds at relatively low interest).

Greenfield Projects: A private entity or a public–private joint venture builds and operates a new facility for the period specified in the project contract. The facility is to be returned to the government at the end of the concession period. The government usually provides revenue guarantee through long-term take-or-pay contracts for bulk supply facilities or minimum traffic revenue guarantees. It is similar to concession.

Divesture: Government transfers the ownership of existing assets to a private entity through an asset sale, public offering, or mass privatization program and the latter has full responsibility for maintenance of the assets. This involves complete transfer of assets to the private entity and absolves “partnership” and thus cannot be a part of PPP.

PPP Forms Comparison

To understand the characteristics and features of various forms of PPP discussed above, we compare these on the bases like ownership, O&M and capital investment, commercial risk, and period of contracts (see Exhibit 8.1). Comparison is also made for parameters like technical expertise, managing expertise, operating efficiency of private agency, or investment needed; this is presented in Exhibit 8.2. Other factors of comparison include political commitment, cost covering tariff, regulatory framework, or information flows and this is presented in Exhibit 8.3.7

PPP Options Comparison to Private Participation Objectives

|

Objective = => Option |

Technical Expertise |

Managing Expertise |

Operating Efficiency |

Investment Required |

|

Service contract |

Yes |

No |

No |

No |

|

Management contract |

Yes |

Yes |

Some |

No |

|

Lease |

Yes |

Yes |

Some |

No |

|

Concession |

Yes |

Some |

Some |

Yes |

|

Divesture BOO |

Yes |

Yes |

Yes |

Yes |

|

Greenfield |

Yes |

Yes |

Yes |

Yes |

PPP Options Comparison to Factors Priority

|

Requirement => Option |

Political Commitment |

Cost Covering Tariffs |

Regulatory Framework |

Information Flows |

|

Service contract |

Low |

Low |

Low |

Low |

|

Management contract |

Moderate |

Moderate |

Moderate |

Low |

|

Lease |

Moderate |

High |

High |

High |

|

Concession |

Moderate |

High |

High |

High |

|

Divesture BOO |

High |

High |

High |

High |

|

Greenfield |

Moderate |

High |

Moderate |

High |

Source: Public–private partnerships in urban infrastructure by Dr. Sasi Kumar and C. Jayasankar Prasad KERALA CALLING (February 2004).

From the above, following are the principles of PPP:

• Private capital is neither necessary nor sufficient for success of PPP.

• Commercial viability is neither necessary nor sufficient for success of PPP.

• Project development is the name of the game.

• Risk transfer is the aim of the game.

• The last “P,” “Partnership” is the most important “P.” There is a need for institutional, policy, and legal framework for cooperation.

PPP Approaches

Approaches generally followed in developing infrastructure projects are

• Design, Bid, and Build Approach: Under this approach, construction agency is inducted after completion of designs, that is, design process is complete before going in for invitation of bids for project construction.

• Design and Build Approach: Under this approach, the contractor is on board early and both design and construction proceed parallel. It is a fast-track approach. The Delhi Airport project awarded under this approach, was estimated to take about 48 months for master plan, bidding, and actual design and execution, leaving about 37 months for construction, that is, to meet the deadline of 6 months prior to commencement of Commonwealth Games in 2010.8

What Should Be the Bases of Pricing for the Design and Build Approach?

Alternative bases of pricing of the contract under the design and build approach of PPP are broadly categorized as

A) Lump Sum Fixed Price Basis: Since the design information available to bidders under the design and bid approach is minimal, the bidders would normally include disproportionate contingency in the bid price to manage unknown risks. Further, as design is at a conceptual stage and changes are likely to be extensive, in particular, for a complex project, the contractor would have to account for aborted/additional unforeseen additional works in the bid price; Delhi Metro and ATC Tower are examples for the Delhi Airport Project. As such, there are significant project uncertainties due to few numbers of drawings available, limited number of interested bidders, and tight time schedule; and thus the bidders would quote considering a high-risk premium.

Lump sum approach will have the following variants.9

| i. | Negotiated lump sum | |

| ii. | Guaranteed maximum price | |

| iii. | Progressive lump sum |

B) Cost plus Fee Basis: Under this option, the cost is finalized progressively upon completion of designs; as such the risks are managed in a fair manner and both contingencies and additional claims would be minimal. The cost plus basis has been followed in infrastructure projects, including airports, worldwide. Some of the examples are

• Terminal 5 of Heathrow by BAA

• Reliance Petroleum Greenfield Refinery at Jamnagar

• LNG Project in Egypt (5 MTPA) by Conoco Philips

Cost plus fee basis is further refined, as, for example, for Delhi airport modernization, to provide control on costs as follows:

• The contractor-own-work portion (CWP) is to be capped, say, at 40 percent of the value of the total job. The major material included in the CWP like cement, steel, bitumen, and sand is to be procured and all the price negotiations are to be done on competitive bidding basis.

• The subcontract packages are to be awarded on competitive tender basis.

Cost plus fee basis has the following variants10:

| i. | Cost plus percent of cost fee | |

| ii. | Cost plus fixed fee | |

| iii. | Cost plus incentive fee | |

| iv. | Cost plus award fee |

Exhibit 8.4 presents details of cost control under design build approach. Examples following alternative fee basis in cost plus contracts are given in Exhibit 8.5.

Uncapped “cost plus” contracts are the riskiest contracts, as the entire risk of cost overrun is borne by the developer. Such contracts are either prohibited or restricted by the funding agencies such as Asian Development Bank and World Bank.11 Further, under “cost plus” approach, the risks are magnified due to inherent conflict of interest and in the absence of strong monitoring procedures, project cost tends to significantly increase over initial estimates.

KPMG in their audit report have suggested that the DIAL project was awarded on “cost plus” approach and alternate approach to uncapped cost plus approach could have been explored. To quote, “Given the global airport experience of the members of the DIAL, JV and the successful development of the Hyderabad and Istanbul airports by the lead members of DIAL JV, we have reason to believe that the ability of bidders to negotiate an irrationally high risk premium was limited.”12

Another variant of PPP was recommended by the Core Group on Financing of the National Highway Development Programme.13 The order of priority was as under:

a) BOT (Toll)

b) BOT (Annuity)

c) EPC(i.e., engineering-procurement-construction)

d) Item rate construction contract

Cost control with Design Build Approach

|

Sl. No. |

Approach |

Key Features |

Examples |

|

1. |

Negotiated lump sum |

Contractor agrees to a specified price for the services in the contract Contractor receives the agreed price irrespective of the cost incurred |

London Luton Airport Expansion Phase one expansion consisting of new departure building apron and taxiway, lighting, parking, and access roads awarded on a lump sum design build basis. Project cost of USD 140 million in 2 years |

|

2. |

Guaranteed maximum price |

Contractor is compensated for actual costs incurred plus a fixed fee subject to a ceiling price The contractor is responsible for cost over runs in the project |

San Jose International Airport Contractors for Terminal Area Improvement Program were awarded on a guaranteed maximum price negotiated at different levels of design. Project cost of USD 750 million |

|

3. |

Progressive lump sum |

To ensure adequate cost control a review of the design process is conducted at different stages of completion At the completion of review, client and contractor can negotiate to fix the lump sum construction cost. If agreement cannot be reached, the client can opt to shift the project to another approach/contractor |

Chicago O’Hare Terminal 6 Program The contractor as a progressive lump sum negotiation process, which calls for review of the design process at 30%, 60%, and 100% stages. At the 30% stage, contractor submitted the cost for full design services, which the client accepted At the 60% stage, the client and contractor have the option of entering into negotiations to fix the lump sum construction cost. If agreement cannot be reached, the design work continues to 100% and negotiations for final construction costs can be entered into If agreement cannot be reached at this point, the client can shift the process to a more traditional approach. Project cost of USD 1 billion |

Source: KPMG Final Audit Report (Annexure 4) contained in Review of Dial’s Final Cost Project Estimates, October 15, 2010.

Alternative fee basis in cost plus contracts

|

Sl. No. |

Approach |

Key Features |

Examples |

|

1. |

Cost plus fixed fee |

Cost reimbursement contract in which the contractor’s fee is fixed Does not provide incentives to contractor to control costs as the costs are reimbursed However, as compared to cost plus percentage of cost fee, it removes the incentives for the contractor to increase costs for gaining higher profits |

Portland International Airport Involves including a quality-based selection process to choose a contractor, bring the contractor on during design, and negotiate a cost-plus-fixed-fee contract for the work prior to design completion |

|

2. |

Cost plus incentive fee |

Cost reimbursement contract with an initially negotiated fee Fee can be adjusted later by a formula based on the relationship of total allowable costs to total target costs Costs in excess of the target cost is only partially paid according to a client/contractor ratio, thus reducing contractor’s profit Contractor’s profit increases when actual costs are below the target cost defined in the contract incentivizing contractor to control costs |

Heathrow Terminal 5 Construction BAA used cost information from other projects, validated independently, to set cost targets If the costs were lower than the target cost, the savings were shared with the relevant partners |

|

3. |

Cost plus award fee |

Cost reimbursement contract that provides for a fee consisting of a base amount fixed at inception of the contract and an award The contractor may earn the award in whole or in part during performance in areas such as quality, timeliness, technical ingenuity, and cost-effective management |

To tie the contractor to the quality of the end product Development for Orion project awarded on a cost plus award fee basis by NASA |

Source: KPMG Final Audit Report (Annexure 5) contained in Review of Dial’s Final Cost Project Estimates, October 15, 2010.

Broad principles annunciated were

| i. | All highways which are to be tolled should adhere to the BOT (Toll) mode. | |

| ii. | Highway projects which are not amenable to BOT (Toll) mode, including projects which are not to be tolled under government policy, should be undertaken on BOT (Annuity) mode. | |

| iii. | Only those highway projects which are not amenable to BOT (Toll) or BOT(Annuity) approach may be taken up through the EPC mode with competent approvals and after provision of requisite funding. | |

| iv. | The item rate construction contract mode should be discarded for contracts to be awarded after April 1, 2006. Thereafter, EPC mode should be relied upon wherever BOT mode is not feasible. |

BOT (Toll) and BOT (Annuity): Under BOT (Toll) construction, maintenance and tolling form part of the concession, and budgetary support is restricted to an up-front grant to the concessionaire (developer) determined through competitive bidding. As such, toll collections are retained by the concessionaire. (It may be mentioned that another variant of BOT (Toll) is BOOT (Toll), wherein, under BOOT, the concessionaire also gets ownership rights of the land and other assets for the period of the concession agreement, and this is preferred by the concessionaire as it enhances his credit worthiness and he is able to raise funds at relatively low interest. BOOT is normally followed in giant projects involving huge investment and having long life). As against this, under BOT (Annuity) construction and maintenance form part of the concession; the concessionaire relies on annuity payments determined by competitive bidding and made out of budgetary allocations spread over time; and the toll collections are retained by the government.

Under BOT (Toll), traffic or commercial risks are borne by the concessionaire, while the government bears the traffic and revenue risks under BOT (Annuity), as the concessionaire is entitled to receive annuity payments. As such, BOT (Toll) is akin to concession, management, and lease contract. Further, under BOT (Toll) the private developer raises loans at a higher rate of interest than if the government was to raise the same amount, the risk of traffic and revenue fluctuation is borne by the private developer. The Planning Commission has recommended BOT (Toll) model as first preference, followed by engineering-procurement-construction (EPC) basis. The Ministry of Shipping, Road Transport and Highways favor BOT (Annuity) method as the private developers have taken projects on Annuity basis and have met the completion targets, and the disputes and arbitration for EPC contracts are higher than for BOT projects. The per-km cost of annuity projects is reported to be 22 percent higher than EPC projects.14

Private Sector Involvement and PPP Approach

As mentioned in the previous chapter, infrastructure has been accorded a greater importance with an investment of Rs. 9.06 lakh crores and Rs. 24.24 lakh crores during the Tenth and Eleventh Plans, respectively. Still higher thrust has been given to infrastructure during the Twelfth Plan with an investment target of Rs. 65.79 lakh crores. Such high investment in infrastructure requires greater involvement of private sector. As such, the share of private sector in infrastructure financing during the Tenth and Eleventh Plans was 25 and 38.2 percent, respectively; the corresponding figure for the Twelfth Plan is envisaged as 47percent. The private sector investment in infrastructure also involves adoption of PPP approach which is based on a concession agreement with the government. The PPP approach, as discussed earlier, takes various forms as BOT, BOOT, BOLT, BOO, and so on, wherein the private sector performs three roles as contractor or constructor, financier, and operator. Further, such PPP approach may be toll based or an annuity based.

As per the data available, 758 infrastructure projects involving a total investment of Rs. 383,332 crores have been awarded or are under way. Sector-wise break-up of projects under PPP for India is presented in Exhibit 8.6. State-wise projects awarded under PPP approach is given in Exhibit 8.7. Exhibit 8.8 presents sector-wise projects awarded under different contract methods.

The aforesaid presentation of PPP projects in India up to July 2011 indicates that

Sector-Wise Projects Under PPP Approach in India (up to July 30, 2011)

|

Sector |

No. of Projects |

Investment Involved (Rs. Crores) |

|

Airport |

5 |

19,111 |

|

Education |

17 |

1,850 |

|

Energy |

56 |

67,225 |

|

Healthcare |

8 |

1,833 |

|

Ports |

61 |

81,038 |

|

Railways |

4 |

1,570 |

|

Roads |

405 |

176,725 |

|

Tourism |

50 |

4,486 |

|

Urban development |

152 |

29,425 |

|

Total |

758 |

383,332 |

Source: http://www.pppindiadatabase.com/

• Road projects account for 53.4percent of projects in number and 46percent in value.

• Ports account for 8percent of the total number of projects and contribute 21percent in terms of value.

• Only infrastructure projects of Rs. 125,568 crores have been taken up under PPP approach in sectors other than roads and ports and there exists a significant potential for PPP projects across sectors where states and municipalities have primary responsibility.

• Potential use of PPPs in e-governance and health and education sectors remains largely untapped across India as a whole.

• Across states and central agencies, the leading users of PPPs by number of projects have been Karnataka, Andhra Pradesh, and Madhya Pradesh, with 104, 96, and 86 awarded projects, respectively, and the National Highways Authority of India (NHAI), with about 155 projects. In terms of main types of PPP contracts, almost all contracts have been of the BOT/BOOT type (either Toll or Annuity payment models) or close variants.

State-Wise Projects Under PPP Approach in India (up to July 30, 2011)

|

State |

No. of Projects |

Investment Involved (Rs. Crores) |

Of which projects more than Rs. 500 crores |

|

Andhra Pradesh |

96 |

66,918 |

56,173 |

|

Assam |

4 |

391 |

– |

|

Bihar |

6 |

2,094 |

1,247 |

|

Chandigarh |

4 |

875 |

– |

|

Chhattisgarh |

4 |

838 |

– |

|

Delhi |

13 |

11,317 |

1,374 |

|

Goa |

2 |

250 |

– |

|

Gujarat |

63 |

39,637 |

33,181 |

|

Haryana |

10 |

11,163 |

10,588 |

|

Jammu &Kashmir |

3 |

6,320 |

6,320 |

|

Jharkhand |

9 |

1,704 |

625 |

|

Karnataka |

104 |

44,659 |

28,500 |

|

Kerala |

32 |

22,282 |

20,502 |

|

Madhya Pradesh |

86 |

14,983 |

5,678 |

|

Maharashtra |

78 |

45,592 |

39,427 |

|

Meghalaya |

2 |

762 |

536 |

|

Orissa |

27 |

13,350 |

11,430 |

|

Pondicherry |

2 |

3,367 |

2,948 |

|

Punjab |

29 |

3,563 |

705 |

|

Rajasthan |

59 |

15,027 |

12,509 |

|

Sikkim |

24 |

17,111 |

13,708 |

|

Tamil Nadu |

43 |

18,629 |

9,100 |

|

Uttar Pradesh |

14 |

26,596 |

25,137 |

|

Uttarakhand |

2 |

521 |

– |

|

West Bengal |

30 |

6,617 |

3,299 |

|

Inter state |

14 |

9,568 |

6,738 |

|

Total |

758 |

383,332 |

298,726 |

Source: http://www.pppindiadatabase.com/

Sector-Wise Projects Under PPP Approach—Contract Award Method in India (upto July 30, 2011) (Rs. Crores)

Source: http://www.pppindiadatabase.com/

• In terms of approach for the selection of projects, almost all the projects in the sample were competitively bid (either national or international competitive bidding) with the negotiated ones (through MOUs) primarily coming from the railway PPP projects, which is understandable, given the lack of clear policy framework and standard contracts till date.

• In terms of contract award method the international competitive bidding yielded 35 percent of total investment in India followed by domestic competitive bidding of 26 percent.

Snapshot of Infrastructure Projects Under PPP Approaches in Different Countries

The World Bank has the Private Participation in Infrastructure (PPI) Project Database15 for over 5,000 infrastructure projects in 139 low- and middle-income countries covering projects in the energy, telecommunications, transport, and water and sewerage sectors. The data have the following criteria

• Projects are owned or managed by private companies

• Projects that directly or indirectly serve the public

• Projects relate to period 1983–2013 and those have reached financial closure

As per World Bank data, 5,268 projects involving an investment of US $1826,201 million have been awarded in different sectors under PPP approach during 1983 to 2011 (see Exhibits 8.6, 8.9, and 8.10). From these exhibits, the following are observed:

• Telecom sector projects accounted for highest amount of investment through PPP approach (45 percent), followed by energy (34 percent), transport (15 percent), and water sectors (5 percent). In terms of number of projects, the corresponding percentages for the sectors were 16, 44, 26, and 14 percent, respectively.

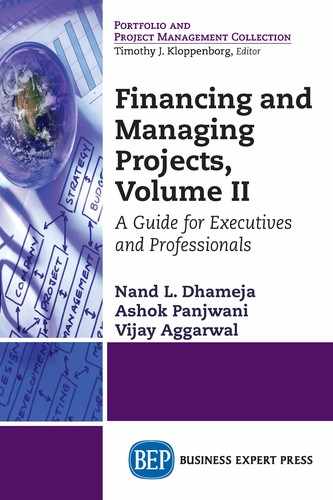

PPP Projects: Across Regions and Sectors

(Investments US $ million and Projects number in parenthesis: for projects reaching financial closure)(1900–2013)

Source: Private Participation in Infrastructure Data Base Mail Stop MCP419,1818,H. St. NW, Washington D C 20433 (World Bank Group).

Snapshot of Infrastructure Projects in 139 low-and middle-income countries; [email protected] (as on August 2014).

• Analysis in terms of regions indicates that Latin American & the Caribbean countries accounted for 1,586 projects (30 percent of total) involving an investment of US $672,494 (37 percent). This is followed by East Asia & Pacific countries accounting for 30 percent of the number of PPP projects involving an investment of 18 percent of the total investment.

• Within the regions, telecom sector projects were very common in terms of investment in Europe & Central Asia, Latin America & the Caribbean, Middle East & North Africa, and sub-Saharan Africa. As against this, energy sector projects were of greater importance in terms of investment in East Asia and South Asia. As such, water projects were last in importance in different sectors.

PPP Projects: Across Regions and Sectors

(Indicators for Sectors, PPI Type having largest share) (1990–2014)

Source: [email protected] (as on August 2014), ibid.

• Greenfields project or new projects form of PPP was most common in terms of number of projects as well as investments involved in all regions.

• Projects cancelled or under distress in percentage in sub-Sahara Africa, Latin America & the Caribbean and East Asia & Pacific were 11, 8.5, and 5.2 percent, respectively. The corresponding percentages in terms of investments involved in such projects were 5, 8, and 19 percent, respectively. In other words, projects cancelled or under distress under PPP were lower in other regions like South Asia, Middle East & North Africa, and Europe & Central Asia.

Snapshot of PPP Projects in India and China

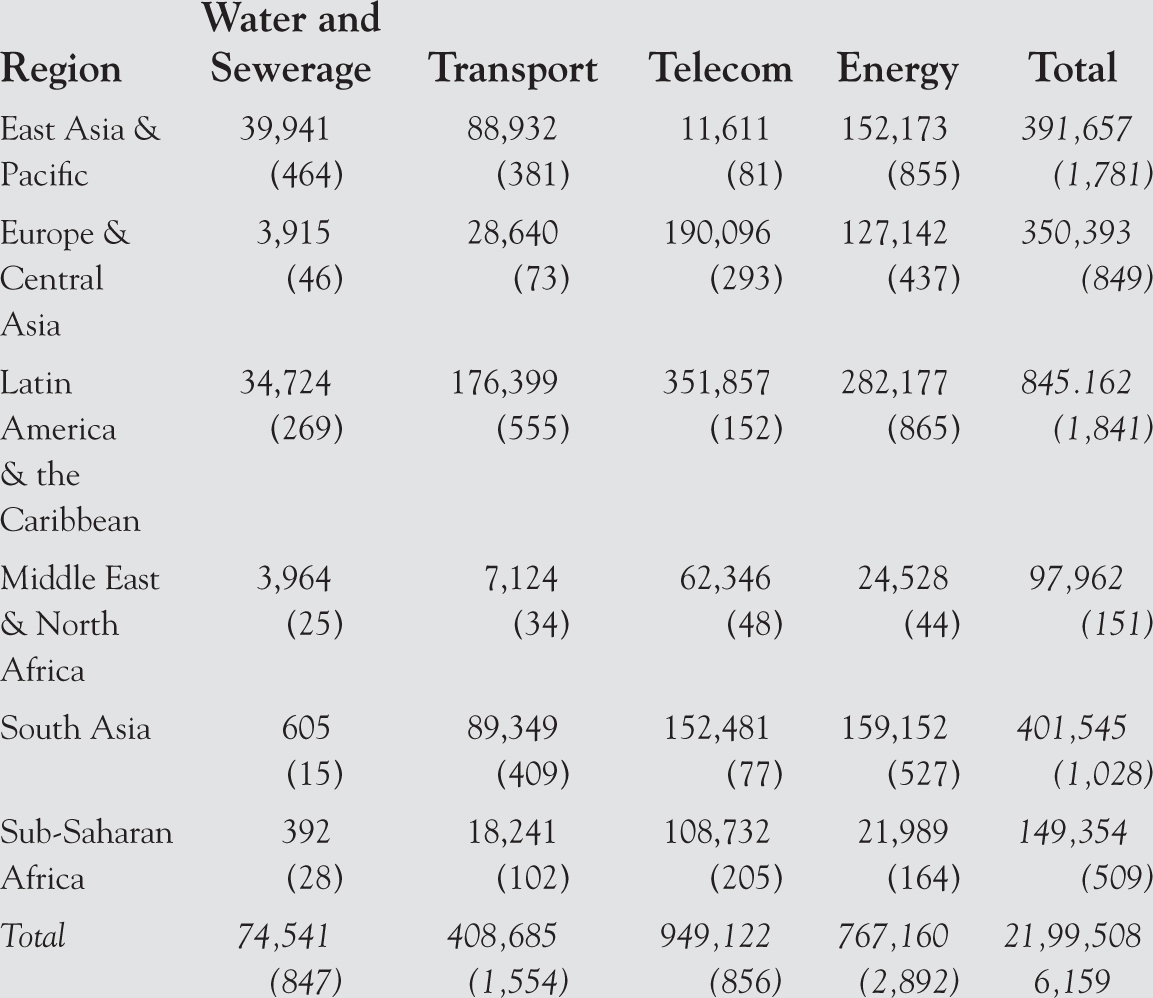

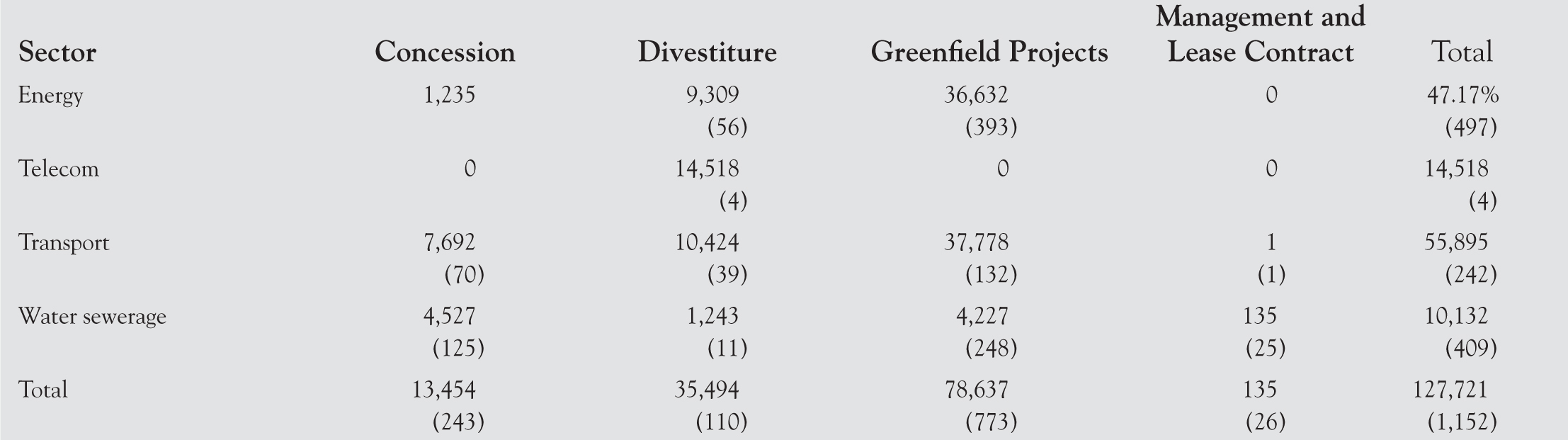

From the World Bank data for the 139 low- and middle-income countries, let us compare the prevalence of PPP in financing infrastructure projects in China and India. Private participation in infrastructure projects in various sectors and subsectors in China is presented in Exhibit 8.11, while Exhibit 8.12 presents the PPP projects under different variants.

Similarly, sector-wise break-up of PPP projects for India is given in Exhibit 8.13 and PPP variants under different sectors for India is presented in Exhibit 8.14. From the above, following are the points of observations:

• In China 1,152 projects on PPP approach involved an investment of US $127,721million; the corresponding figures for India were 776 and US $322,166 million, respectively.

• In China transport sector involved a relatively higher share of investment (42 percent of total); this was followed by energy (37 percent); the shares of investment for telecom and water & sewerage sectors were 13 and 8 percent, respectively.

• As against this, in India energy sector projects accounted for the highest amount of investment (43 percent of total); shares of investment for telecom and transport sectors were 30 and 25 percent, respectively; water sector projects involved only a negligible amount of investment.

China: Total Projects by Primary Sector and Subsector during 1990–2013

|

Sector |

Subsector |

No. of Projects |

Total Investment (US $ million) |

|

Energy |

Electricity Natural gas Total energy |

299 198 497 |

42,613 4,563 47,176 |

|

Telecom |

Telecom |

4 |

14,518 |

|

Transport |

Airport Railroads Seaports Total transport |

17 14 72 139 242 |

2,555 12,908 13,957 26,348 55,768 |

|

Water sewerage |

Treatment plant Utility Total water sewerage |

372 37 409 |

6,190 3,942 10,132 |

|

Total |

1,152 |

127,721 |

Sector with largest investment share: transport

Type of PPI with largest share of investment: Greenfield projects

Projects cancelled or distresses: No. 36 (4 percent of total investment)

Source: [email protected] (August, 2014), ibid.

• In China divestiture form of PPP, wherein there is complete transfer of assets to a private entity, accounted for 28 percent of total investment and these were mainly in telecom and transport sectors followed by the energy sector. As against this, in India, divestiture form accounted for only 4 percent of the total investment under PPP and these were mainly in the energy sector.

• In China Greenfield projects were common form of PPP projects accounting for over 60 percent of the investment, followed by divestiture form (which accounted for 28 percent of total investment). In other words, concession, management, and lease contract forms of PPP, wherein private agency assumes operational and investment risks, are in the nature of BOT (Toll); these accounted for only 5 percent of total investment and were prevalent in transport, water, and sewerage.

China: Infrastructure Projects with Private Participation reaching Financial Closure during 1990–2013

Total Investment in projects by Type and Region (No. of projects in parenthesis)

Source: [email protected] (August, 2014), ibid.

India: Total Projects by Primary Sector and Subsector during 1990–2013

|

Sector |

Subsector |

No. of Projects |

Total Investment (US $ million) |

|

Energy |

Electricity Natural gas Total energy |

328 5 333 |

138,585 831 139,371 |

|

Telecom |

Telecom |

37 |

96,614 |

|

Transport |

Airports Railroads Seaports Roads Total transport |

7 8 36 341 392 |

5,111 7,826 7,642 64,996 85,576 |

|

Water sewerage |

Treatment plant Utility Total water and sewerage |

4 10 14 |

195 411 605 |

|

Total |

776 |

322,166 |

Sector with largest investment share: energy

Type of PPI with largest share of investment: Greenfield projects

Projects cancelled or distresses: No.15 (3 percent of total investment)

Source: [email protected] (August, 2014).

• In India, Greenfield projects were important form of PPP; Greenfield accounted for about 77 percent of total investment; divestiture form of PPP projects’ share in investment was only 4 percent. In other words, concession, management, and lease contract forms of PPP, wherein private agency assumes operational and investment risks, are in the nature of BOT (Toll), and these accounted for only 15 percent of total investment.

India: Infrastructure Projects with Private Participation Reaching Financial Closure during 1990–2013

Total Investment in projects by type and region (no. of projects in parenthesis)

Source: [email protected] (August, 2014).

1Savas E. S, Privatisation—The Key to Better Government, (New Delhi: Tata McGraw Hill Publishing Co Ltd., 1989).

2Dhameja Nand and Dhameja Sarika, Infrastructure Development and Financing including Social Infrastructure Issues and Challenges (New Delhi: Viva Publication, Chapter 13, 2015)

3Dhameja Nand, “Public-Private-Partnership for Infrastructure Development: Cross-Country Scenario” Indian Journal of Public Administration IV, no. 1(2008): 21

4Nand and Sarika, “Infrastructure Development and Financing,” 40

5Grimsey Darrin and Lewis Mervyan K, The Economics of PPP (Cheltenham: Edward Elgar Publishing Co., 2005)

6[email protected] (as on 29/4/2013), Private Participation in Infrastructure Database(Washington DC: World Bank Group)

7Sasi Kumar and C. Jayasankar Prasad, ‘Public-private partnerships in urban infrastructure’ (KERALA CALING, February 2004)

8Dhameja Nand and Dhameja Sarika, “Infrastructure Development and Financing,” Chapter 13

9KPMG Final Audit Report contained in Review of DIAL’s Final Cost Project Cost Estimates Final Report, October15, 2010, Airport Authority of India, Airport Economic Regulatory Authority of India, April, 2011

10Dhameja Nand and Dhameja Sarika, “Infrastructure Development and Financing,” Chapter 13

11Ibid

12Ibid

13Report of the Core Group, Financing of the National Highways Development Programme (The Secretariat for the Committee on Infrastructure, Planning Commission, GOI 2006)

14Economic Times (Delhi Edition, April 2007)

15[email protected] (as on 29/4/2013), “Private Participation in Infrastructure Data Base”