5

Recent Trends, Opportunities and Challenges of Sustainable Aviation Fuel

Libing Zhang1, Terri L. Butler2, and Bin Yang*,1

1Bioproducts, Sciences, and Engineering Laboratory, Department of Biological Systems Engineering, Washington State University, Richland, WA 99354, USA

2Buerk Center for Entrepreneurship, University of Washington, Seattle, WA 98195, USA

5.1 Introduction

Climate change is a global challenge to be addressed by governments and industries around the world. It is estimated by the Intergovernmental Panel on Climate Change (IPCC) that by the year 2100 the world will see a temperature change of 2.5–7.8 °C above the average for the years between 1850 and 1900 (Bernstein et al. 2007). The aviation industry contributes approximately 2% of total carbon emissions across all industrial sectors and air transportation growth is increasing rapidly due to globalization of trade and travel. Aviation has no credible near‐term fuel alternative in ethanol or electric power due to the energy density required although aviation fuel can be used in fuel cells to produce electricity locally in dispersed applications. Current jet fuel production processes require huge facilities that are complex to operate while using fossil oil as feedstock. Carbon emission reduction in the aviation industry is essential to combat global warming. The aviation industry has achieved several milestones in emission reduction including improved aircraft fuel efficiency and better air traffic control to promote safe, efficient and sustainable air travel. However, these improvements have led to carbon emission reductions of less than 15% (The global aviation industry 2010). Compared to these non‐fuel approaches, the use of alternative jet fuel can achieve a further 50–80% reduction in carbon emission and is, therefore, considered to be the most efficient way to achieve carbon neutral aviation operation. Thus, addressing the source of fuel for the aviation industry is an important part of the answer to achieving a material reduction in greenhouse gas emissions.

Demands from regulatory agencies for compliance with international carbon emission standards have increased. Domestic interests in biojet fuel powered planes have also been rising. Both of these factors are driving the growth of biojet fuel markets. By 2028, the carbon emission standards for international flights will be regulated, requiring airlines to purchase carbon offsets to compensate for growth in their emissions. This has led to a sense of urgency for airlines and their shareholders, resulting in their encouragement of technologies that are likely to bring new biojet fuel products to market. Although the research, development, and commercialization of biojet fuels are still in the early stages, several activities have been initiated by a number of stakeholders in the past 10 years, including the newly approved by American Society for Testing and Materials (ASTM) biojet standards, biojet fuel development community formation, fuel certification test flights, and off‐take fuel agreements between airline companies and early‐stage biojet fuel suppliers (Radich 2015).

The US jet fuel market represents 20 billion gallons per year. All emerging biojet fuel technologies that meet ASTM standards are included in this number. However, as of this date, no clear winning sustainable jet fuel technology exists, a situation that encourages continued research and development in innovative biojet fuel technologies. For biomass‐based biojet fuels, as in the case of biofuels for ground transportation, one of the most important deciding factors in commercial feasibility is having accessible, low‐cost feedstock. This presents a challenge because, unlike crude oil, biomass contains a high level of oxygen (up to 45%) in its major heteropolymers. Biojet technologies have made progress in dealing with these diverse biomass substrates, but more effort is still needed to improve the biomass conversion efficiencies and to reduce the cost of production.

The aim of this chapter is to provide an overview of current opportunities for the development of biojet fuels and highlight the reasons behind the burgeoning efforts. Information gathered through interviews with parties from the private sector and government agencies indicated a growing interest in purchasing and investment for biojet fuels. This chapter also provides a brief summary of the current biojet fuel technologies, and the status of several specific challenges facing the industry is explained, which help the reader to better understand the overall landscape of biojet fuels.

5.2 Overview of the Jet Fuel Market

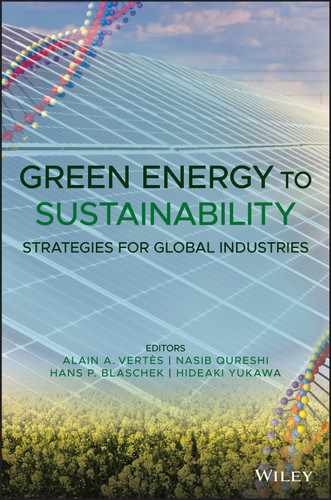

The current US market for jet fuel is dominated by large petroleum‐based refineries that produce a total of approximately 23.6 billion gallons of jet fuel per year (Figure 5.1). Companies such as Exxon Mobil (Irving, TX, USA), Chevron Corporation (San Ramon, CA, USA), BP (London, UK), Valero (San Antonio, TX, USA), and Marathon Petroleum Group (Findlay, Ohio, USA) account for around 50% of that production volume. The global consumption is about four times that much (Indexmundi 2017; US Energy Information Administration 2017a). The domestic jet fuel consumption is expected to increase by more than 40% between 2016 and 2040 as projected by the Energy Information Administration (EIA) (US Energy Information Administration 2017a) because the increased demand for air travel will more than offset projected aircraft efficiencies gained.

Figure 5.1 Global and US Jet fuel consumption (U.S. Energy Information Administration 2017a).

5.2.1 Driving Force of Growing Biojet Fuel Opportunities

Airlines are exploring biojet fuel options to diversify their fuel supplies, lower fuel costs in the long run, reduce price volatility, comply with future emission regulations, and minimize the dependence of the overall aviation industry on fossil fuel. Jet fuel cost represents the highest percentage of total cost in aviation operations. By 2040, the jet fuel price paid by airlines is projected to be 40% higher than that price in 2014 (Radich 2015). The rising jet fuel prices are driving commercial and military aviation operators to look for substitutes or alternative drop‐in fuels. The availability of more drop‐in fuels can provide increased options for the airline industry, reducing dependence on conventional jet fuel made from crude oil and reducing overall costs by reducing fuel price volatility (Radich 2015).

The price fluctuation of jet fuel ranged, according to estimations of the US Gulf Coast Kerosene‐Type Jet Fuel Spot Price provided by the EIA, from between 80 cents to $4.5/gal over the past 10 years (US Energy Information Administration 2017c). Traditionally, fuel hedging, the contractual tool used by the airlines (Morrell and Swan 2006), can reduce the exposure of airline companies to the volatility of jet fuel cost. However, this financial approach is not always as effective as expected. Fuel contracts usually last only 12–18 months (Amanda Peterka 2013). The pricing of jet fuel is not easy to predict, and this uncertainty represents an important operational risk as it causes uncertainties in finance and regular aviation operations. For example, Delta Airlines (Atlanta, GA, USA) reported a loss of $4 billion due to hedging fuel, a contract strategy that airlines applied to reduce exposure to jet fuel volatility (Ed Hirs and Forbes 2016). Biojet fuel is generally expected to reduce pricing volatility (Winchester et al. 2013), although this is somewhat controversial. The arguments refer back to the reasons why the price of jet fuel is volatile. These reasons include: (i) the cost and availability of raw material crude oil, (ii) competitors' pricing, (iii) transportation cost, (iv) international relations, (v) geographic regions, (vi) supply and demand balance, and (vii) the global political climate, etc. (US Energy Information Administration 2017b). Biojet fuels are also influenced by similar factors even though there are arguments from proponents pointing out the more available and sustainable biomass feedstock for producing biojet fuels.

One of the most important driving forces for the biojet fuel market is the increasingly stringent regulatory compliance requirements of international carbon emission standards. In October 2016, the International Civil Aviation Organization (ICAO) stated the new requirements in the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) (ICAO's 39th Assembly 2016) to regulate the industry's carbon emissions. Commercial airlines are facing pressure to pay for renewable credits if they are unable to comply with the regulations. Therefore, the biojet fuel business is not only motivated by the need to reduce the environmental impacts but also has become important to the profit margins of the aviation industry. This is a welcome evolution as such a profitability pressure provides an impetus for the earlier adoption of these fuels and at a large scale.

5.2.2 Biojet Fuel Types and Specifications

Currently there are five main biojet fuel technologies that have been developed and approved by ASTM as meeting the standard specifications ASTM D7566 (ASTM 2014), and so can be blended with Jet A or Jet A‐1 fuel certified to Specification D1655 and 16 certifications in preparation (International Air Transport Association 2009):

- Fischer–Tropsch Synthetic Paraffinic Kerosene (FT‐SPK)

- Fischer–Tropsch Synthetic Kerosene with Aromatics (FT‐SKA)

- Hydrotreated Esters and Fatty Acids (HEFA)

- Synthesized Iso‐Paraffinic (SIP)

- Alcohol (isobutanol) to Jet Synthetic Paraffinic Kerosene (ATJ‐SPK)

Five more biojet fuel technologies are under review as listed in the following:

- High Freeze Point Hydrotreated Esters and Fatty Acids (HFP‐HEFA)

- Virent BioForm Synthesized Aromatic Kerosene (SAK) Jet Fuel (SAK)

- LanzaTech ATJ‐SPK (Ethanol to Jet)

- Applied Research Associates Catalytic Hydrothermolysis Jet (ARA‐CHJ)

- BioForm® Synthesized Kerosene (SK) Jet Fuel (Virent SK)

Data is being collected for three additional technologies including ATJ‐SKA developed by Byogy (Byogy Renewables, Inc., San Jose, USA), Swed Biofuels (Swedish Biofuels AB, Stockholm, Sweden), and the IH2 demonstration scale by Shell (Royal Dutch Shell, UK) which acquired the technology from the Gas Technology Institute (GTI) (Des Plaines, USA) in 2009.

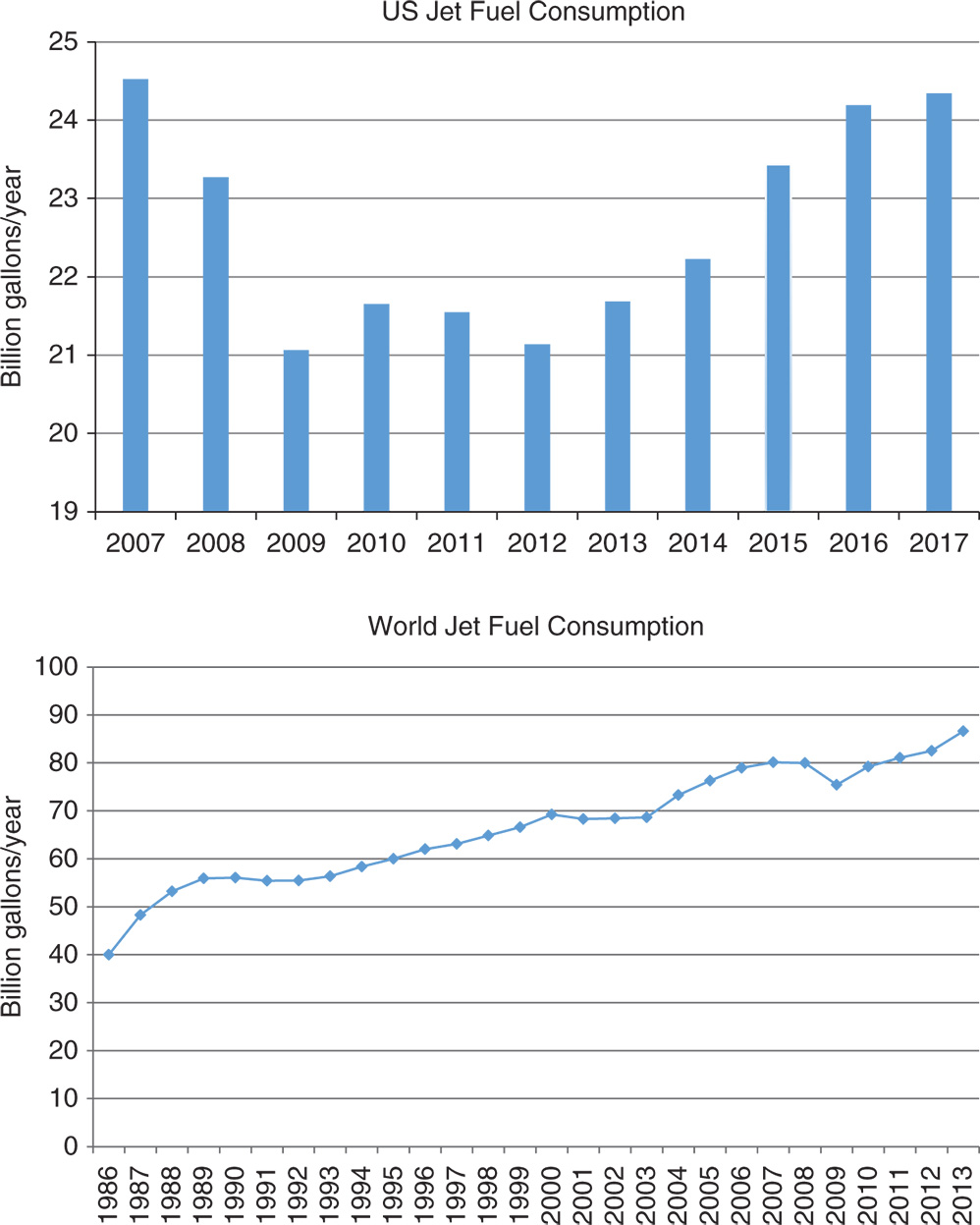

Eight more technologies, listed below, are in exploratory discussions. Figure 5.2 shows some of the technologies that are currently being studied.

- Vertimas. One‐step catalytic conversion of ethanol to jet, petrol, diesel fuel and chemicals which was originally invented at Oak Ridge National Laboratory.

- SBI bioenergy. Continuous catalytic process that converts fat, oil or grease into renewable gasoline, diesel and jet fuel with proprietary Process intensification and Continuous Flow through Processing technologies (PICFTR).

- Joule. CO2‐derived fuels ‘Sunflow‐J’ jet fuel from specially engineered photosynthetic bacteria, waste carbon dioxide, sunlight and water.

- Global bioenergies. Biological production of isobutene and process to jet.

- Eni. hydrogenated vegetable oil (HVO).

- Enerkem. Municipal waste gasification and catalytic conversion to ethanol followed conversions to biofuels and chemicals.

- POET. Agricultural waste derived alcohol to jet fuel.

- Washington State University. Lignin to Jet Fuel (LJ‐D&HDO) through one‐step proprietary catalytic upgrading of lignin waste to jet fuel.

Figure 5.2 Comparison of biojet fuel technologies.

As shown in Figure 5.2, biojet fuel technologies use a broad range of feedstocks such as lignocellulosic biomass, municipal solid wastes, vegetable oils, animal fats, lignin, flue gas, and even seawater. Current biojet fuel technology pathways have been summarized by referring to industry publications, academic research and technology reports (Fahim et al. 2009; Wang and Tao 2016; Wang et al. 2016b; Yang and Laskar 2016). Information has also been gleaned from biofuel development companies and institutions (Biochemtax 2017; LanzaTech 2017; Fellet 2016; US Naval Research Laboratory 2016; Virent 2017; WSU Maegan Murray 2016). Compared to current oil refineries, most of the biojet fuel technologies require more than four functional process units, which is likely to be cost intensive, requiring capital, energy, labor, and water to commercialize (Bridgwater 1975; Gerrard 2000). Among the biojet fuels, the lignin‐based jet fuel technology is one of the most promising, and potentially most sustainable, due to its one‐step process conversion. By 2022, it is projected that 62 million tons of lignin side‐product will be generated annually by cellulosic biomass biorefineries (Ragauskas et al. 2014). The pathways of lignin based jet fuel include depolymerization and hydrodeoxygenation (LJ‐D&HDO) of lignin to a mixture of long‐chain hydrocarbons (C7–C18 cyclic hydrocarbons) that can be made into jet fuel. (Laskar et al. 2014; Laskar and Yang 2012; Laskar et al. 2013; Wang et al. 2015, Wang et al. 2016a; Wang et al. 2017a,b,c; Yang and Laskar 2016) Scaling this process and putting it into production alongside current biorefinery production facilities would significantly improve biomass conversion efficiency and the economics of biofuels and chemicals production.

In discussions of capital cost savings, the co‐processing of biomass by co‐feeding of biomass feedstock with petroleum streams in conventional oil refinery units has received attention (Al‐Sabawi et al. 2012; Huber and Corma 2007; Yanik et al. 2012). Recently, an oil refinery raised great interest by co‐processing biomass and crude oil distillates for instance. Chevron Corporation (San Ramon, CA, USA), Phillips 66 (Houston, USA) and BP (London, UK) are researching the feasibility of co‐processed fuels up to 5 vol% bio‐oils from HEFA and middle crude oil distillates to produce hydrocarbons that could be used in jet fuel (Joseph Sorena and Clark 2015). The compatibility of biojet production united with existing infrastructure motivated the interests in co‐feeding of the biojet feedstock/intermediates with crude oil‐based distillates. Figure 5.2 shows several potential research opportunities in co‐feeding desired by oil refiners.

In 2009, ASTM International Committee on Petroleum Products and Lubricants issued ASTM Standard Specification D7566, titled as Standard Specification for Aviation Turbine Fuel Containing Synthesized Hydrocarbon, to certify drop‐in jet fuel from alternative feedstock. It contains five Annexes that define the specifications of the five biojet fuels blended with conversional jet fuel certified by D1655 ASTM standard. In Table 5.1, the specifications of the five approved biojet fuels are presented. The rest of the specifications of biojet fuel pathways in Figure 5.2, such as syngas fermentation and CH, are still under development. The blending limit of each biojet fuel is different. The FT‐SPK, HEFA, and SIP biojet fuels were approved for higher blending feasibility testing (ASTM Committee 2017).

Table 5.1 Approved biojet fuels specifications (ASTM Committee 2017).

| ASTM D7566‐16b | |||||||

| Jet fuel tests | Jet A/A‐1 | FT‐SPK | FT‐SKA | HEFA | SIP | ATJ‐SPK | |

| Approved blend, % | 100 | 50 | 10 | 50 | 50 | 30 | |

| Composition | |||||||

| Acidity, total (mg KOH/g) | Max | 0.1 | 0.015 | 0.015 | 0.015 | 0.015 | 0.015 |

| Aromatics (vol %) | Max | 8–25 | 0.5 | 20/21.2 | 0.5 | 0.5 | 0.5 |

| Cycloparaffins, mass % | Max | 15 | 15 | 15 | 15 | ||

| Saturated hydrocarbons, mass % | Min | 98 | |||||

| Farnesane, % mass | Min | 97 | |||||

| Carbon and hydrogen, mass % | Min | 99.5 | 99.5 | 99.5 | 99.5 | 99.5 | |

| Nitrogen, mg kg−1 | Max | 2 | 2 | 2 | 2 | 2 | |

| Water, mg kg−1 | Max | 75 | 75 | 75 | 75 | 75 | |

| Sulfur, mg kg−1 | Max | 0.3 | 15 | 15 | 15 | 2 | 15 |

| Metalsa), mg kg−1 | Max | 0.1 per metal | 0.1 per metal | 0.1 per metal | 0.1 per metal | 0.1 per metal | |

| Halogens, mg kg−1 | Max | 1 | 1 | 1 | 1 | 1 | |

| Hexahydrofarnesol | Max | 1.5 | |||||

| Olefins, mgBr2 per 100 g | Max | 300 | |||||

| Contaminants | |||||||

| Existent gum, mg per 100 ml | Max | 7 | 4 | 7 | |||

| FAME, ppm | Max | 5 | |||||

| MSEP | Min | 90 | |||||

| Volatility | |||||||

| Distillation temperature, °C | |||||||

| 10% recovered, temperature (T10) | Max | 205 | 205 | 205 | 205 | 250 | 205 |

| Final boiling point, °C | Max | 300 | 300 | 300 | 300 | 255 | 300 |

| Distillation (D86) T90‐T10, °C | Min | 22 | 22 | 22 | 5 | 21 | |

| Flash point, °C | Min | 38 | 38 | 38 | 38 | 100 | 38 |

| Fluidity | |||||||

| Freezing point, °C | Max | −47 Jet A‐1 −40 Jet A |

−40 | −40 | −40 | −60 | −40 |

| Density @ 15 °C, kg l−1 | 775–840 | 730–770 | 755–800 | 730–770 | 765–780 | 730–770 | |

| Viscosity −20 °C, mm2 s−1 | Max | 8.0 | |||||

| Combustion | |||||||

| Energy density, MJ kg−1 | Min | 42.8 | 44.1 | 43.5 | |||

| Thermal stability | |||||||

| Temperature, °C | 325 | 325 | 328 | 325 | 355 | 325 | |

| Filter pressure drop, mmHg | Max | 25 | 25 | 25 | 25 | 25 | 25 |

| Additives | |||||||

| Antioxidants, mg l−1 | Max | 24 | 17–24 | 17–24 | 17–24 | 17–24 | 17–24 |

a Metal includes Al, Ca, Co, Cr, Cu, Fe, K, Li, Mg, Mn, Mo, Na, Ni, P, Pb, Pd, Pt, Sn, Sr, Ti, V, Zn.

The US civilian jet fuels are mainly categorized into Jet A‐1, Jet A, and Jet B, while the US military sets its own standards, which are JP‐1, JP‐2 to JP‐10, each for specific applications. Jet A‐1 is similar to JP‐8 and Jet B is similar to JP‐4. Biojet fuels imitate Kerosene‐type fuels, which have a carbon number between 8 and 16, for example Jet A, Jet A‐1, JP‐5 and JP‐8. While a lot of interest in biojet fuels has been generated, so far there have been little in the way of commercial products available in the market because research and development in biojet fuels is still in the early stages.

Notably, Jet A/A‐1 and the five approved biojet fuels differ in composition. The energy content per unit weight increases in the following order; aromatic, naphthenic, paraffinic for hydrocarbons with the same carbon number (Hemighaus et al. 2006). As shown in Table 5.1, although biojet fuel possesses more cycloparaffins than paraffins, it remains hard to compare fuel efficiencies between biojet fuel and conventional jet fuel due to variations in hydrocarbon profiling. Whether the composition of biojet fuel, especially the new contaminants that arise in these processes, such as FAMES and Halogens, could cause problems to the propulsion and energy system of an airplane engine needs to be confirmed by engine manufacturers (FAA Aviation Rulemaking Advisory Committee 1998). Biojet fuels with low sulfur content have been achieved, which reduces aviation impact on air pollution (Hileman et al. 2009). Jet A/A‐1 has a minimum requirement of 8% vol of aromatics, so the lack of enough aromatics in biojet poses a theoretical risk of losing proper functions of elastomeric materials in jet engines (Karatzos et al. 2014). However, the performance characteristics of biojet fuels can be adjusted by additives, which is generally required to be compatible with aircraft operations.

Hydrocarbons that can be used in jet fuel can be categorized as: paraffins, olefins, naphthenes, and aromatics (Hemighaus et al. 2006). Hydrocarbons in jet fuel are mixtures of compounds from each of these classes that contain different numbers of carbon atoms. Since biomass and crude oil are both converted to a mixture of hydrocarbon compounds, taking a look at the elemental profiling of various biomass and crude oil compositions is an efficient way to understand the different chemical compositions of jet fuels and conversion efficiency in biomass and crude oil refineries (Table 5.2) (Baedecker et al. 1993; Bilba et al. 2013; Canoira et al. 2008; Valkenburg et al. 2008). For example, the oxygen element in biomass is much more than that of crude oil, which requires more energy input to effectively remove excess oxygen and produce hydrocarbons consisting of only carbon and hydrogen atoms. This is one of the reasons why hydrogen hydrotreating is needed in nearly all biojet fuel conversion pathways, and the cost and availability of these industrial processes are considered a risk in the research and development of biojet fuel (National Academies of Sciences, Engineering, and Medicine 2016). What is more, understanding the different element compositions is extremely useful for estimating the potential abundance of air pollutants that are emitted during fuel combustion.

Table 5.2 Feedstock elemental composition (Baedecker et al. 1993; Bilba et al. 2013; Canoira et al. 2008; Valkenburg et al. 2008).

| Raw materials, % dry weight | Crude oil | Coal | Wood waste | Switchgrass | Sugarcane bagasse | MSW | Animal fat /vegetable oil |

| Carbon | 84–87 | 73.6 | 48.0 | 46.7 | 48.6 | 33.9–84.8 | 76.6 |

| Hydrogen | 11–14 | 4.7 | 5.5 | 5.9 | 6.3 | 1.72–15.16 | 12.0 |

| Oxygen | 0–2 | 5.1 | 39.1 | 39.0 | 45.1 | 15.8–43.7 | 12.4 |

| Nitrogen | 0–1 | 1.3 | 1.4 | 0.54 | 0.48 | 0.12–2.37 | 2.2 |

| Sulfur | 0–3 | 1.6 | 0.1 | 0.13 | 0.21 | 0.06–1.4 | 0.15 |

| Ash mineral | 0.1–0.2 | 13.7 | 5.9 | 7.7 | 3.7 | 4.4–44.2 | 0.1–3.7 |

5.3 Assessment of Environmental Policy and Economic Factors Affecting the Aviation Industry

Aviation should be environmentally sustainable, cause minimal pollution to air and water, and contribute to high quality human life. More and more stringent environmental regulations have been enforced to fight against global warming, affecting the worldwide efforts to reduce carbon footprints. Renewable biojet fuels are significant in such efforts because of the increasing demand for jet fuels.

5.3.1 Momentum Building of International Carbon Emission Regulations

As stated earlier, the aviation industry is responsible for approximately 2% of global CO2 emissions (Lister et al. 1999). The ICAO is a UN agency charged with managing all aspects of international civil aviation such as aviation sustainability, air navigation, and air travel safe (ICAO 1994). The ICAO has set a goal of capping net carbon emissions from 2020 to achieve 50% reduction by 2050 from 2005 emission levels (The global aviation industry 2010). The Carbon Offsetting and Reduction Scheme (CORSIA) is a historic move for the global international aviation industry to meet ICAO's goal of carbon neutrality from 2020 by limiting and offsetting emissions from the aviation sector. A total of 70 countries intend to voluntarily participate in the global market‐based measure (MBM) scheme implemented in May 2017; this indicates that more than 87.7% of international aviation activities are committed to achieving significant emission reductions (ICAO 2016).

In October 2016, the ICAO announced the CORSIA for International Aviation aiming to offset approximately 80% of the emissions above 2020 levels. The ICAO requires airlines to offset emissions by purchasing eligible emission credits (e.g. renewable energy) equivalent to offsetting requirements from the carbon markets. This emission offset is currently voluntary. The first voluntary transition will happen between 2021 and 2027, but it will become mandatory in 2027. This creates an additional opportunity for biojet fuel to become a beneficial fuel alternative for commercial airlines, helping them meet the emission allowance each year. The regulation is legally binding for countries that are signatories to the Kyoto Protocol. In 2016, at the 39th session of the ICAO Assembly, it was decided that CORSIA will become enforceable in 2021, so at that point, the aviation industry will have the obligation to buy carbon offsets to accommodate any growth in their carbon emissions.

CORSIA is taking a route‐based approach where all operators on the same route will have the same offsetting obligations. Before ICAO's CORSIA, the efforts to control greenhouse emissions can be traced back to the1940s, as the International Air Transport Association was founded in 1945 and has since grown to 274 airline members. CORSIA has set up a timeline for execution of the new plan for carbon emission reduction, although ICAO is still working on the implementation plan for quantifying and offsetting regulations. The proposed timeline has three phases, including phase I during years 2021–2023, and phase II during years 2024–2027, as the voluntary participation phases. The carbon offset requirements will become obligatory to airlines from 2028 to 2035 and will be enforced by requiring payment for generating excess carbon emissions above 2020 levels during international flights.

The Paris Agreement consolidates nations aiming to combat climate change within the United Nations Framework Convention on Climate Change (UNFCCC), which was drafted in December 2015, and signed by 195 nations worldwide in 2016, and became effective in 2016. It requires the assessment of carbon emission progress in 2018 and regular reviews every five years. The domestic carbon emission commitments of these countries will be addressed under the Paris Agreement. This is an international agreement that sets out a global action plan to limit global warming, due to be enforced from 2020. As listed in Table 5.3, the commitment to carbon emission reduction receives common consensus internationally. The endorsement of global leaders for reducing carbon emissions and fighting climate change has finally become mainstream.

Table 5.3 Events in carbon emission reduction development.

| Timeline | Organization | Agreements | Ratified nations | Legacy | Notes |

| 1947 | ICAO | 191 | Not enforced | ICAO formation | |

| 1981 | Chicago Convention | Aircraft engine emission | 191 | Not enforced | |

| 1992 | UNFCCC | 154 | Not enforced | UNFCCC formation | |

| 1992 | UNFCCC | Kyoto Protocol | US and Canada not ratified | Legally binding | Commit to reduce emissions of greenhouse gases (Berlin mandates) |

| 2005 | Directive of the European Parliament and the European Council | EU ETS | Linked to Kyoto Protocol members | Legally binding | Phase I (2005–2007) launched |

| 2007 | UNFCCC | Bali Action Plan‐Cop13 | 114 | Legally binding | Set emission measurement; 30 billion fast‐start financing (in 2010–2012) |

| 2008 | Directive of the European Parliament and the European Council | EU ETS | Linked to Kyoto Protocol members | Legally binding | Phase II (2008–2012) |

| 2009 | UNFCCC | Copenhagen Accord | 114 | Not enforced | Set 2 °C limit in global warming |

| 2010 | UNFCCC | Cancun‐Cop 16 | 196 | Not enforced | Establish approaches to achieve carbon reduction |

| 2012 | UNFCCC | Doha Amendment‐Cop 18 | 196 | Legally binding | Regulate 2013–2020 |

| 2013 | Directive of the European Parliament and the European Council | EU ETS | Linked to Kyoto Protocol members | Legally binding | Phase III (2012–2013) |

| 2015 | UNFCCC | Paris Agreement Cop 21 | 196 | Layout | Emission contribution submitted |

| 2015 | UNFCCC | Paris Agreement Cop 22 | 196 | Layout | Method to evaluate contribution |

| 2016 | UNFCCC | Paris Agreement | 196 | Enforced | |

| 2016 | ICAO | CORSIA | 191 | Enforced from 2028 | Carbon offsetting |

Emissions Trading Schemes (ETSs) for greenhouse gas emissions are operational in several countries and regions (Talberg and Swoboda 2013). In the United States, the Regional Greenhouse Gas Initiative (RGGI), implemented in 2009, is known as the first mandatory CO2 cap‐and‐trade program and it involved nine states. Also, the California Air Resources Board (CARB) has established a Californian cap‐and‐trade scheme to reduce greenhouse gas emissions to 1990 levels by 2020 (Reuters 2012).The ICAO has endorsed the potential of MBM such as capping, open trading and charging as a means of quantification and reducing greenhouse gas production for international civil aviation.

The European Union Emissions Trading Scheme (EU ETS) has become a well‐established practice. In 2005, EU ETS launched Phase I (2005–2007) in January and is one of several options that allow the quantification and promote the reduction of carbon emissions. Airlines receive 85% of their proportionally‐allocated allowances based on 2010 emissions for free. The EU suspended full compliance for international flights in and out of the EU until December 31, 2016 for ICAO to set a global scheme. By 2017, EU ETS capped carbon emissions of 1 889 411 334 ton in CO2 emissions (tCO2e), a threshold that is projected to evolve to 1 777 105 173 tCO2e by 2020 (Fund 2013). Whether CORSIA more effectively reduces carbon emissions than does the EU ETS requires more study.

The EU ETS functions using a system of emission allowances, each allowance being equivalent to one ton of CO2. Each airline is required to submit an Annual Emissions Report with a number or certification to depict the free portion of the emission allowance and the renewable credits that should be purchased to compensate the emission difference between the actual and the allowed emission amounts. The trading system allows aviation companies to sell their excess allowance to other parties. The Environmental Protection Agency (EPA) has also determined that aircraft emissions contribute to climate change and, eventually, is expected to move forward on standards that would be at least as stringent as the ICAO's standards (US Environmental Protection Agency 2016). The uncertainties of the regulatory situation for airlines operating in domestic and international markets is a motivator for the development of alternative jet fuels.

5.3.2 Increasing Activities to Address the Carbon Emission Control

Many efforts have focused on emission reduction including lighter aircraft design, better engine efficiency, rigorous air traffic management, and improvement in ground transportation efficiency. The fuel efficiency of aircraft has been improved by 70% over the years, compared with the early days of the airline industry. Boeing (Boeing Company, Chicago, IL, USA) has claimed that fleet efficiency is improving by an estimated 2.9% per year and emphasized that the lifecycle of biofuel can reduce CO2 emissions by 50–80% as compared to fossil fuel (Boeing Company 2015). ICAO reported 1.5% fleet efficiency improvements every year (The global aviation industry 2010). US air travel rose 2.6% in 2016 and 6.7% in global air markets compared to 2015 (International Air Transport Association 2017). The growth rates of air travel were estimated to be 2.8% and 3.7% annually in the US and internationally, respectively (International Air Transport Association 2016). The Federal Aviation Agency (FAA) has a similar estimation in the continuous growth rates to 2037 (Federal Aviation Administration 2017b). Therefore, simply increasing fleet efficiency is not likely to be enough to achieve the carbon emission reduction goals given the rising rate of air travel and increased activity from airport ground transportation.

According to the ICAO environmental report in 2010, several approaches are being implemented to reduce emissions from ground transportation associated with the airlines including: (i) providing public transportation tools for public transport, (ii) regulating emissions from private vehicles, (iii) centralizing shuttles for hotel, rental car or other services, (iv) encouraging the use of alternative fuel or hybrid vehicles, and (v) improving infrastructures to support carbon emission reduction activities (Secretariat 2010). The air traffic management and operational improvements are one of the five pillars in NextGen, a program to ensure sustainable aviation (Federal Aviation Administration 2017a). It was reported that continuous improvement of air traffic and operational management can reduce carbon emissions by 10% (The global aviation industry 2010).

5.3.3 New Technologies and Aviation Operation Improvement

The US accounts for 29% of all greenhouse gas emissions from global commercial aviation as reported by the EPA (US Energy Information Administration 2017b). Three unconventional sources of petroleum including Canadian oil sands, Venezuelan Very Heavy Oils (VHOs), and shale oil can supply jet fuel in addition to fuel produced from conventionally sourced crude oil (Hileman et al. 2009). Life‐cycle studies of these three sources revealed that GHG emissions associated with oil sands and VHOs can be 10–20% higher and oil‐shale can be 50% higher than conventionally produced Jet A (Hileman et al. 2009). The energy return on investment (EROI) is the ratio of the amount of usable energy obtained from a particular resource to the amount of energy needed to obtain that resource. It is a criterion used to evaluate the energy production efficiency. The EROI ratio of a resource should be at least 3:1 to be viable and feasible as a practical energy source. The EROI ratios of several main energy sources have been reported and indicate the exceptional energy‐intensive cost of oil sands compared with the values of coal at 50% and crude oil at 22%, with oil from tar sands at only 3% (Hall et al. 2014).

The prospects for oil shale development remain unclear given the high production cost and environmental risks (Bartis et al. 2005). It was estimated that $20 billion per year of shale oil production is possible with a capacity of 3 million barrels per day, if the production cost proves to be economic (Bartis et al. 2005). The EROI value of oil shale was reported to be <10%, which suggests that the refining of shale oil is an energy‐, capital‐ and water‐intensive process (Hall et al. 2014).

Additionally, efforts have been made to investigate non‐liquid fuel technologies such as electricity, fuel cells, batteries, and hydrogen energy. However, the current energy density of these technologies does not meet jet fuel requirements and non‐liquid fuels are also not compatible with the current liquid fuel distribution infrastructure.

Biodiesel and bioethanol have been widely used as clean energy sources in surface transportation; however, these fuels are not options for jet fuel. Table 5.4 shows a comparison of performance characteristics of jet fuel with ethanol and biodiesel (Renewable Fuels Association 2011; Reynolds et al. 2017). Biodiesel possesses a higher freezing point than what is allowed for jet fuel and its viscosity is too high to meet standards. In addition, it has less energy content per volume compared with regular jet fuel, significantly jeopardizing aircraft range (Appadoo 2009). For example, typical bio‐diesel possesses 38 MJ kg−1, which is much lower than 48 MJ kg−1 of Jet A/Jet A‐1. Assessing the feasibility of ethanol, it has a high volatility and about 40% less energy content than jet fuel, thus posing a real practical problem for aircraft range.

Table 5.4 Comparison of characteristics of ethanol and biodiesel.

| Fuel types | Jet A/A‐1 | Biodiesel (B100) | Ethanol |

| ASTM standards | ASTM D7566‐16b | ASTM D 975 | |

| Viscosity, mm2 s−1 | Max 8.0 at −20 °C | 1.9–6 at 40 °C | 1.2 |

| Flashpoint, °C | Min 38 | Min 130 | 17 |

| Freezing Point, °C | Max −47 Jet A‐1 and −40 Jet A | 0 | −84 |

| Energy Content, MJ kg−1 | Min 42.8 | 38 | 25 |

5.4 Current Activities Around Biojet in the Aviation Industry

Biojet fuels remain the only true alternative for the commercial aviation industry and the military, both facing ambitious near‐term greenhouse gas reduction targets. Thus, the aviation industry is more interested in the biojet fuels as many offtake agreements have been made even though biojet fuels are not commercially available yet. These agreements of taking millions of gallons of biojet fuels by airlines shows a strong commitment towards a green aviation industry. Many test flights have been executed by biojet shareholders in order to enter the jet fuel market.

5.4.1 Alternative Jet Fuel Deployment and Use

The major emission constituents of jet fuel combustion include particulates, SO2, NOX, carbon monoxide, and carbon dioxide. Biojet fuel can greatly reduce air pollution from sulfur and particulates as discussed before. Calculating the levels of carbon emissions of flights is a complex challenge, since it incorporates several factors including aircraft configuration, fuel burning, and flight distance. The Sabre Holdings calculator was reported to be the most accurate compared to others such as the DEFRA, ICAO ( 2008), and ClimateCare calculators (Jardine 2009). The EU ETS scheme has set up aircraft operators and guidelines to assist monitoring and reporting annual emissions and tonne km−1 data for EU emissions trading (Authority 2009).

Over the past 10 years, the interest in biojet fuel has been growing rapidly and the beginnings of a biojet fuel industry has formed. The Commercial Aviation Alternative Fuels Initiative (CAAFI), a coalition of aviation stakeholders interested in bringing commercially viable, sustainable, alternative jet fuels to the marketplace, was established in 2006 to enable and facilitate the near‐term development and commercialization of alternative aviation fuels.

CAAFI is a coalition of airlines, aircraft and engine manufacturers, energy producers, researchers, and federal agencies including FAA, DOT, NASA, DOE's National Renewable Energy Laboratory and Energy Efficiency and Renewable Energy Office and USDA, among others. CAAFI has developed a base technology roadmap and identified milestones along the path to the production, processing, certification, and commercial availability of biofuel for use in commercial aviation. By 2050, the International Air Transportation Association (IATA) aims to reduce the net CO2 production by 50% compared with 2005 levels. The large‐scale production of alternative jet fuels could achieve this goal while improving national energy security, and helping to stabilize fuel costs for the aviation industry. The goal of the Federal Aviation Administration (FAA) is to catalyse the production of 1 billion gallons of ‘drop in fuels’ by 2018.

Private companies have been leading the way in promoting biojet fuel technologies (Mawhood et al. 2016). However, there is only one currently available commercial biojet fuel, that from AltAir (CA, USA). United Airlines (Chicago, IL, USA) recently began using AltAir's fuel in routine flights to and from Los Angeles and regular ground operations at the airport (United Airlines 2016). AltAir (CA, USA) has a production capacity of 2500 bbls per day and has made more than 30 military and commercial flights for certification testing purposes.

Airline customers have been investing in biojet fuel companies to help commercialize the aforementioned alternative fuel technologies to keep their future fuel options open. Since, as of this date, there is no clear market leader in the still‐emerging biojet fuel market, there remains a strong business opportunity for all emerging biojet fuel technology companies. Airlines and oil companies have created multiple offset agreements with biojet fuel companies to support their development in the past five years, even though the products are not yet available. For example, the airliner JetBlue (Long Island, USA) and SG Preston (Philadelphia, PA, USA), a biojet fuel company, have agreed upon JetBlue purchasing 33 million gallons per year of biojet fuel for 10 years starting in 2019. This agreement and other examples in Table 5.5 demonstrate the industry's interest in alternative jet fuels (BP Press Office 2016; FedEx 2015; IATA 2017; SBI bioenergy and Shell Press 2017; United Airlines and Fulcrum BioEnergy Press 2015; Virent and Tesoro Press 2016). The demand is much greater than what biojet fuel technologies can supply right now, this tension in demand realization and biojet fuel manufacturing capacity creates a clear opportunity for additional market entrants.

Table 5.5 Interests in biojet fuel by commercial airlines and oil refinery (BP Press Office 2016; FedEx 2015; IATA 2017; SBI bioenergy and Shell Press 2017; United Airlines and Fulcrum BioEnergy Press 2015; Virent and Tesoro Press 2016).

| Commercial airlines | Biojet company | Contract length in years | Volume (Million gallons per year) | Year to deliver |

| JetBlue | SG Preston | 10 | 33 | 2019 |

| United Airlines | Fulcrum | 10 ($1.58 billion) | 90 | 2017 |

| Cathay Pacific | Amyris | 2 | Toulouse to Hong Kong Flights | 2016 |

| Cathay Pacific | Fulcrum | 10 | 37.5 | 2019 |

| American Airlines | Amyris | N/A | N/A | N/A |

| Lufthansa | Gevo | 5 | 8 | N/A |

| World Fuel (FBO) | Altair | N/A | N/A | N/A |

| Alaska | Hawii Bioenergy | 5 | N/A | 2015 |

| FedEx | RedRock | 8 | 3 | 2017 |

| Southwest | RedRock | N/A | 3 | 2016 |

| South African Airways | Altair | N/A | N/A | N/A |

| United Airlines | Altair | 3 | 17 000 | 2016 |

| KLM | SkyNRG‐Altair | 3 | Undisclosed | 2016 |

| BA (United Kingdom) | Solena | 11 | 16 | 2017 |

| Oil companies | ||||

| BP (investor as well) | Fulcrum | 10 | 500 | 2018 |

| Tesoro | Virent | Company Acquirement | 2016 | |

| Shell | GTI | IH2 Technology Acquiring | 2009 | |

| Shell | SBI Bioenergy | Exclusive Licensees | 2017 | |

| ExxonMobil | Wisconsin Madison University | Continuous 2‐years Funding | 2017 | |

In recent years, more than 20 airlines have flown over 1600 demonstration flights using biojet fuel, especially with conventional fuel blended with biojet fuel (Fellet 2016). Additionally, several test flights were performed using biojet fuel alone, such as the recent flight from Seattle to Washington DC by Alaska Airlines (Seattle, WA, USA) using Gevo's (Englewood, CO, USA) biojet fuel. These examples demonstrate the industry's interest in alternative jet fuel.

5.4.2 Test Flights of Commercial Airlines

As mentioned above, Boeing stated that alternative jet fuel can reduce CO2 emissions by 50 to 80% compared to fossil fuel through an airplane life cycle. As part of an NSF I‐Corps grant received in 2016, the authors' Lignin Biojet team interviewed over 100 jet fuel end users and other stakeholders such as the US Navy, Air Force, Defense Logistics Agency (DLA), Alaska Airlines, JetBlue, United Air, Air Canada (Montreal, Canada), FedEx (Memphis, TN, USA), UPS (Atlanta, GA, USA), Delta Airlines and others. The end users expressed a strong desire to purchase as much cost‐efficient biojet fuel as possible. Chevron, Shell, PBF, BP (London, UK) and other refiners have shown great interest in developing biojet fuel technologies. Boeing and Airbus have partnered with Honeywell, International Aero Engines and JetBlue Airways in the pursuit of developing a sustainable second‐generation biofuel for commercial jet use, with the hope of reducing the aviation industry's environmental footprint.

In biojet fuel development stakeholders include, but are not limited to, oil refineries, various government agencies, biofuel companies, feedstock suppliers, environmental NGOs and aircraft manufacturers. The success of FT‐SPK biojet fuel is mainly attributed to the collaboration of different stakeholders including Boeing, Honeywell/UOP, Air New Zealand (ANZ), Continental Airlines (CAL), Japan Airlines (JAL), General Electric, CFM, Pratt and Whitney, and RollsRoyce (Table 5.6). Table 5.6 shows detail from some test flights (FOCAC 2010; AirportWatch 2012; AirportWatch 2013; Alaska Airlines Press 2011; BBC News 2008; Biofuels International 2015; Boeing Company 2008; ConventryTelegraph 2013; GreenAir Communications 2008, 2009a,b, 2011; LATAM Airlines Group 2013; United Airlines 2016; United Airlines 2011). There has been criticism regarding the emissions of the fuel blends which are, in many cases, the same as emissions from regular jet fuel, given they have similar specifications. Additionally, the land use in the production of biomass feedstock, the necessary hydrogen and conversion inputs for developing biojet fuel, cause carbon emissions, too. The carbon in the fuel goes back to biomass via photosynthesis while the life cycle analysis considers different factors using various methods. In any case, the life cycle analysis of biojet fuel has mostly reported fewer GHG emissions than those of fossil jet fuel (Agusdinata et al. 2011; Budsberg et al. 2016; de Jong et al. 2017).

Table 5.6 Selected flight tests with biojet fuels through different commercial airlines (FOCAC 2010; AirportWatch 2012; AirportWatch 2013; Alaska Airlines Press 2011; BBC News 2008; Biofuels International 2015; Boeing Company 2008; ConventryTelegraph 2013; GreenAir Communications 2008; GreenAir Communications 2011; GreenAir Communications 2009a; GreenAir Communications 2009b; LATAM Airlines Group 2013; United Airlines 2016; United Airlines 2011).

| Year | Airlines | Aircraft manufacturers | Other stakeholders | Technologies | Feedstock | Biofuel % | Destination |

| 2008 | Virgin Atlantic | Boeing and GE | HEFA | Brazilian babassu nuts and coconuts | 20 | Heathrow and Amsterdam | |

| 2008 | United States Air Force | Airbus A380 | Shell International; Rolls Royce | FT | Natural gas | 50 | Filton to Toulouse |

| 2008 | Air New Zealand | Boeing | Boeing Rolls‐Royce; UOP | HEFA | Jatropha | 50 | Auckland |

| 2009 | Continental | Boeing | Boeing; GE Aviation; CFM; Honeywell UOP |

HEFA | 2.5% Algae and 47.5% Jatropha |

50 | Houston |

| 2009 | Japan | Boeing | Pratt and Whitney engines | HEFA | Camelina (84%), jatropha (under 16%) and algae (under 1%) | 50 | Tokyo |

| 2009 | Qatar Airways | Airbus | Shell | FT Synthesis | Natural gas | 50 | London Gatwick to Doha |

| 2010 | South African | Boeing | Sasol | Coal to Liquid | Coal | 100 | Lanseria to Cape Town |

| 2011 | United Airlines | Boeing | Solazyme; Honeywell | HEFA | Algae oil | 40 | Houston to Chicago and Los Angeles to San Francisco |

| 2011 | Alaska Airlines | Boeing | Dynamic Fuels; SkyNRG | HEFA | Algae and waste cooking oil | 20 | Seattle to W ashington, D.C |

| 2011 | KLM Royal Dutch Airlines | Boeing | SkyNRG; Dynamic Fuels | HEFA | Waste cooking oil | 50 | Schiphol bound for Charles de Gaulle |

| 2011 | Thomson Airways | Boeing | N/A | HEFA | Virgin plant oil from the US and babassu nuts from Brazil | 50 | Birmingham to Palma |

| 2011 | Lufthansa | Airbus | Boeing | FT | Jatropha, camelina and animal fats | 50 | Hamburg and Frankfurt |

| 2011 | United Airlines | N/A | AltAir Paramount | HEFA | Algae and waste cooking oil | 15 million over three years 20% | Los Angeles |

| 2012 | Air China | Boeing | Honeywell's UOP; PetroChina | HEFA | Jatropha | 50 | Beijing mainland |

| 2012 | Air Canada | Applied Research Associates, Chevron Lummus Global, and Agrisoma Bioscience Inc. | CH | Carinata | 100 | Ottawa | |

| 2013 | LAN Colombia | Airbus | Gevo | HEFA | Camelina | 30 | Bogota and Cali |

| 2013 | KLM Royal Dutch Airlines | SkyNRG | Schiphol Group, Delta Air Lines, the Port Authority of New York and New Jersey | HEFA | Cooking oil | 25 | New York to Amsterdam |

| 2015 | Hainan | Boeing | Sinopec | HEFA | Waste cooking oil | 50 | Shanghai to Beijing |

5.5 Challenges of Future Biojet Fuel Development

As highlighted above, feedstock is a critically important contributor to the cost of biojet fuel and its availability and price are an indicator of the commercialization feasibility of each of the biojet fuel technologies. It remains a question whether or not the currently available biomass is sufficient to meet the jet fuel demand. The Department of Energy Biomass Billion Ton report used a simulated price of $40–60 per dry ton for some biomass feedstock. The energy crop cost is about $650–890 per acre (Downing et al. 1998). Table 5.7 shows the availabilities and prices of each biomass feedstock that can be converted to biojet fuel through various pathways (Langholtz et al. 2016; Ragauskas et al. 2014). The production yields of each biojet fuel technology varied in different research studies (Wang et al. 2016b). The cost of crude oil is $46.10 per barrel as of June 2017, which is equivalent to $319 per ton, calculated by converting gallons of oil to barrels by dividing the volume by 42 gallons per barrel and the specific gravity of crude oil is assumed to be 915 kg m−3. Compared to the $319 per ton crude oil, animal fat and vegetable oil as well as algae‐derived lipids are much more expensive (Table 5.7). As of June 2017, jet fuel is priced at $1.29 per gallon which is equivalent to $375 per ton. Thus, the final product crude‐derived jet fuel is much cheaper than the starting raw materials of vegetable oil, animal fat and algae‐derived lipids, making the economics of converting these materials into biojet fuel impractical.

Table 5.7 Feedstock availability, pricing, and potential biojet production (Langholtz et al. 2016; Ragauskas et al. 2014).

| Raw Materials | Availability, million dry tons yr−1 | Effective year of availability | Price, $/ton | Conversion yield, gallons per dry ton | Biojet, billion gallons yr−1 | |

| Animal Fat and Vegetable oil | 5 | 2012–2014 | 550–1200 | HEFA | 28–87 | 0.14–0.44 |

| MSW | 51–55 | 2017–2040 | 40–60 | FT | 9–88 | 0.46–4.8 |

| Forestry and wood wastes | 36–56 | 2017–2040 | 40–60 | ATJ | 11–79 | 0.40–4.4 |

| HDCJ | 19 | 0.68–1.1 | ||||

| FT | 9–88 | 0.32–4.9 | ||||

| Energy crops | 78–411 | 2012–2040 | 40–60 | ATJ | 11–79 | 0.89–3.2 |

| HDCJ | 19 | 1.5–7.8 | ||||

| FT | 9–88 | 0.70–36.2 | ||||

| Algae | 47–132 | Present to future | 490–2900 | HEFA | 28–87 | 1.3–11.5 |

| CH | 8–122 | 0.38–16.1 | ||||

| Lignin | 66 | 2016 | 80–250 | LJ‐D&HDO | 30–61 | 2.0–4.0 |

| Total | 4.0–66.5 | |||||

An estimation of the US biojet fuel production capacity from biomass is shown in Table 5.7; it reveals that 4–66.5 billion gallons of biojet fuel per year can be produced according to the biomass availability illustrated in DOE's Biomass Billion Ton report. It indicated that the US has the capacity to produce enough biojet fuel to meet the annual demand of jet fuel if all biomass were used in biojet fuel conversions. However, the biojet fuel production has to compete with ethanol and biodiesel production for biomass feedstock. The ethanol mandate is about 15 billion gallons per year since 2010 while the biodiesel mandate is 1–2 billion gallons per year 2011 to 2017 (US Environmental Protection Agency 2017). For example, the mandates for biodiesel and ethanol in 2016 were 1.90 and 18.11 billion gallons per year, respectively. If the conversion efficiency (gallons per ton) of biomass to ethanol and biodiesel are assumed to be 85 gallons per ton and 267 gallons per ton, 220 million tons biomass would be used in ethanol and biodiesel production. The biojet fuel production would lose about 12 billion gallons per year if 55 gallons per dry ton conversion efficiency is assumed. Thus, the feedstock production and distribution system needs to be well established to ensure an appropriate logistics of biomass feedstock.

The cost of biojet fuels remains a challenge, especially when the cost of crude oil is as low as $46.10 per barrel and the cost of jet fuel is about $1.29 per gallon as of June 2017 (US Energy Information Administration 2017c). It has been reported that the minimum selling price of alternative jet fuels can range from $2–24 (Staples et al. 2014). Biojet fuels can achieve cost‐competitiveness with crude oil‐based jet fuel if crude oil is at least priced at $120 per barrel (National Academies of Sciences, Engineering, and Medicine 2016). The operational cost of biojet fuels is currently high and numerous technical challenges remain. To achieve cost‐competitiveness, biojet fuels will need more research and development effort. Also, it is costly and time consuming to scale up biojet fuel technologies, which is reported to range from US$20 to 50 million over ten to fifteen years (Philippe Novelli 2013). Industrial partnerships are therefore crucial in the scale‐up and demonstration of the viability of drop‐in bio‐based fuels.

In addition, the certification and approval process of biojet fuels takes a long time. One of the reasons may be attributed to the involvement of several functional departments specializing in the certification of biojet fuel. The qualification process starts with Tier 1 which tests fuels for specification properties. Tier 2 focuses on the fit‐for‐purpose properties. Tiers 3 and 4 involve aircraft manufacturers and airlines, including component/rig testing and engine/APU testing. The FAA and ASTM participate heavily in the process (Rumizen 2016). While the first phase of the jet fuel certification is relatively straightforward, which requires 100 gallons of fuel and costs nearly half a million dollars, the requirements for the second phase can vary widely. So far, testing for these phases have required from 30 000 to 200 000 gallons of fuel and have run up costs surpassing $3 million (Rumizen 2017). In addition, there is some level of uncertainty inherent in the certification process.

Private companies are actively involved in biojet fuel commercialization activities (Mawhood et al. 2016). Biojet fuel development is still in the early stages, requiring a lot of effort to overcome challenges. Support from well‐established industrial sectors such as oil refineries and engine or aircraft manufacturers is important for the overall success in biojet fuels. Besides industrial efforts, many federal organizations and agencies have collaborated together in developing alternative jet fuels, including the Department of Agriculture (USDA), Environmental Protection Agency (EPA), Department of Transportation (DOT), Department of Commerce (DOC), Department of Defense (DOD), Department of Energy (DOE) and the National Science Foundation (NSF) with projects such as the Defence Production Act (DPA) and Farm to Fleet (Aeronautics Science and Technology Subcommittee 2016). However, there is still a lack of government incentives for the development of renewable aviation fuel. The only credit biojet fuels can claim is the Renewable Fuel Standards (RFS) (US Environmental Protection Agency 2005), but there is no mandate within RFS that applies to jet fuels (Team‐CAAFI, Reasearch and Development Team 2014). This is an important consideration as it means that the aviation industry is not obligated to use biojet fuels, albeit biojet fuels can generate renewable fuel credits to meet RFS mandates for ground transportation.

5.6 Perspectives

Sustainable aviation fuel is the only option for the airline industry in the future. The mitigation of greenhouse gas emissions in the aviation industry is crucial to combat global climate change. A broad range of renewable alternative jet fuels, also known as biojet fuels (also referred to as biojet), are in development as drop‐in fuels that possess performance characteristics and chemical compositions essentially identical to conventional kerosene jet fuels. Most of the technologies to produce biojet fuels are still in the early stages of research, development, and certification. Notwithstanding this early stage, biojet fuel technologies are the most promising options for alternative energy sources for the airline industry. They present both short‐ and long‐term solutions for replacing crude oil‐derived jet fuels. For example, techno‐economic analyses have shown that a corn stover ethanol plant with an annual capacity of 57.2 million gallons of ethanol would be able to produce an additional 20 million gallons of lignin‐based jet fuel if the catalytic process is applied to upgrade the waste lignin stream (Shen et al. 2019). Results indicated that coproduction of jet fuel from waste lignin can dramatically improve the overall economic viability of an integrated process for corn stover ethanol production. Lignin‐derived jet fuel would offer unique advantages compared to the above‐mentioned six varieties of biojet fuels: (i) uses low cost raw materials without conflicting with food or other biofuel production, (ii) has higher thermal stability, (iii) has higher energy density, (iv) is produced at a lower cost, and (v) reduces greenhouse emissions (Ruan et al. 2019). However, it is also important to realize that the commercialization of new technology presents difficulties even greater than those that have already been overcome in the past for alternative biojet technology development, as well as tremendous dedication, persistence, and financial strength are required to clear this last remaining hurdle. Furthermore, the aviation industry is facing an increasingly stringent regulatory compliance environment, mainly from international carbon emission regulations associated with quantifying emissions and payment of renewable fuel credits. There are both environmental and economic benefits for aviation and biojet fuel groups to be engaged. In about 10 years, commercial airlines will have mandatory and legally‐binding international rules to comply with. It is thus in the interest of all the stakeholders to invest in biojet fuel development now, since biojet fuel technologies will take a long time to be fully developed and be producing at a commercial scale, and to significantly penetrate the conventional jet fuel markets. Many challenges remain, including the availability and price of feedstock, conversion efficiency technical challenges, the tedious and cost‐intensive fuel certifications, and government regulatory factors. These uncertainties and challenges, combined with decreasing oil reserves and volatile fuel pricing, justify strategic alliances for biojet fuel stakeholders to collaborate and contribute to the advancement of viable alternatives to conventional jet fuel.

Acknowledgments

This work was supported by the National Science Foundation I‐Corps #1655505, Sun Grant‐U.S. Department of Transportation (DOT) Award # T0013G‐A‐Task 8, and the Joint Center for Aerospace Technology Innovation with the Bioproducts, Science & Engineering Laboratory and Department of Biological Systems Engineering at Washington State University.

References

- Aeronautics Science and Technology Subcommittee. 2016. Federal alternative jet fuels research and development strategy. National Science and Technology Council.

- Agusdinata, D.B., Zhao, F., Ileleji, K., and DeLaurentis, D. (2011). Life cycle assessment of potential biojet fuel production in the United States. Environmental Science & Technology 45 (21): 9133–9143.

- AirportWatch. 2012. Canada claims world's first 100% biofuel‐powered civil jet flight.

- AirportWatch. 2013. KLM to make one flight per week New York to Amsterdam for 6 months using 25% used cooking oil.

- Alaska Airlines Press. 2011. Alaska Airlines Launching Biofuel‐Powered Commercial Service in the United States

- Al‐Sabawi, M., Chen, J., and Ng, S. (2012). Fluid catalytic cracking of biomass‐derived oils and their blends with petroleum feedstocks: a review. Energy & Fuels 26 (9): 5355–5372.

- Amanda Peterka, E.E.N. 2013. Clean, green options lacking as airlines seek alternatives to petroleum, Vol. 2017.

- Appadoo, R. (2009). Insights into Jet Fuel Specifications. Montreal, Canada: Aviation and Alternative Fuels (ICAO), ICAO.

- ASTM. 2014. Revised ASTM Aviation Fuel Standard Paves the Way for International Use of Synthesized Iso‐Paraffinic Fuel in Airliners.

- ASTM Committee (2017). ASTM Standard, ASTM D7566‐16, Standard Specification for Aviation Turbine Fuel Containing Synthesized Hydrocarbons, ASTM Internation, Est Conshohocken, PA, 2017, www.astm.org.

- Authority, D.E. 2009. Monitoring and Reporting Annual Emissions and Tonne km Data for EU Emissions Trading.

- Baedecker, M.J., CozzARELLI, I.M., Eganhouse, R.P. et al. (1993). Crude oil in a shallow sand and gravel aquifer—III. Biogeochemical reactions and mass balance modeling in anoxic groundwater. Applied Geochemistry 8 (6): 569–586.

- Bartis, J.T., LaTourrette, T., Dixon, L. et al. (2005). Oil Shale Development in the United States: Prospects and Policy Issues. Rand Corporation.

- BBC News. 2008. Airline in first biofuel flight.

- Bernstein, L., Bosch, P., Canziani, O. et al. (2007). Climate change 2007: synthesis report. In: Contribution of Working Groups I, II and III to the Fourth Assessment Report of the Intergovernmental Panel on Climate Change [Core Writing Team, Pachauri, R.K and Reisinger, A. (eds.)], 104. Geneva, Switzerland: IPCC.

- Bilba, K., Savastano Junior, H., and Ghavami, K. (2013). Treatments of non‐wood plant fibres used as reinforcement in composite materials. Materials Research 16 (4): 903–923.

- Biochemtax. 2017. MOGHI project Vol. 2017.

- Biofuels International. 2015. First commercial bio‐jet flight takes off in China.

- Boeing Company (2008). Boeing, Air New Zealand and Rolls‐Royce Announce Biofuel Flight Demo. Boeing Company.

- Boeing Company. 2015. Cut the Carbon: Aviation industry reaffirms pledge to reduce emissions.

- BP Press Office. 2016. BP announces investment of $30 million in biojet producer, Fulcrum.

- Bridgwater, A. (1975). Operating cost analysis and estimation in the chemical process industries. Revista Portuguesa de Quimica 17 (107): 107.

- Budsberg, E., Crawford, J.T., Morgan, H. et al. (2016). Hydrocarbon bio‐jet fuel from bioconversion of poplar biomass: life cycle assessment. Biotechnology for Biofuels 9 (1): 170.

- Canoira, L., Rodríguez‐Gamero, M., Querol, E. et al. (2008). Biodiesel from low‐grade animal fat: production process assessment and biodiesel properties characterization. Industrial & Engineering Chemistry Research 47 (21): 7997–8004.

- ConventryTelegraph. 2013. From coconuts to cooking oil... flight fuel of the future?

- Downing, M., Demeter, C., Braster, M. et al. (1998). Agricultural cooperatives and marketing bioenergy crops: case studies of emerging cooperative development for agriculture and energy. Proceeding of Bioenergy 98: 4–8.

- Hirs, E., Forbes,. 2016. Delta CEO Admits To $4 Billion Lost In Hedging Fuel Costs.

- FAA Aviation Rulemaking Advisory Committee. 1998. Fuel Properties Effect on Aircraft and Infrastructure.

- Fahim, M.A., Al‐Sahhaf, T.A., and Elkilani, A. (2009). Fundamentals of Petroleum Refining. Elsevier.

- Federal Aviation Administration. 2017a. The FAA and its NextGen program aim to balance environmental protection with sustained aviation growth, Vol. 2017.

- Federal Aviation Administration. 2017b. FAA Forecasts Continued Growth in Air Travel.

- FedEx. 2015. Biofuels Take Flight with FedEx.

- Fellet, M. (2016). Now boarding: commercial planes take flight with biobased jet fuel. Chemical & Engineering News 94: 16–18.

- FOCAC. 2010. South Africa launches world first synthetic jet fuel.

- Fund, E.D. 2013. The World's Carbon Markets: A case study guide to emissions trading. Retrieved from IETA website: http://www.ieta.org/worldscarbonmarkets.

- Gerrard, A. 2000. Guide to capital cost estimating. IchemE.

- GreenAir Communications. 2008. Airbus completes first commercial aircraft test flight using alternative fuel.

- GreenAir Communications. 2009a. Japan Airlines demonstration flight concludes current series of alternative biofuel feedstocks testing.

- GreenAir Communications. 2009b. Qatar Airways undertakes first commercial passenger flight powered by a natural gas blended jet fuel.

- GreenAir Communications. 2011. First‐ever transatlantic aviation biofuel flight sets up week of alternative aviation fuel events at Paris Air Show.

- Hall, C.A., Lambert, J.G., and Balogh, S.B. (2014). EROI of different fuels and the implications for society. Energy Policy 64: 141–152.

- Hemighaus, G., Boval, T., Bacha, J. et al. (2006). Aviation Fuels Technical Review. Chevron Products Company.

- Hileman, J.I., Ortiz, D.S., Bartis, J.T. et al. (2009). Near‐Term Feasibility of Alternative Jet Fuels. Santa Monica, CA, USA: RAND Corporation and Massachusetts Institute of Technology.

- Huber, G.W. and Corma, A. (2007). Synergies between bio‐and oil refineries for the production of fuels from biomass. Angewandte Chemie International Edition 46 (38): 7184–7201.

- IATA. 2017. Fact Sheet Alternative Fuels

- ICAO. 1994. About ICAO

- ICAO. 2008. ICAO Carbon Emissions Calculator.

- ICAO. 2016. Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), Vol. 2017.

- ICAO's 39th Assembly. 2016. Historic agreement reached to mitigate international aviation emissions Vol. 2017.

- Indexmundi. 2017. World Jet Fuel Consumption by Year.

- International Air Transport Association. 2009. Fact Sheet: Alternative Fuels.

- International Air Transport Association. 2016. IATA Forecasts Passenger Demand to Double Over 20 Years.

- International Air Transport Association. 2017. Another Strong Year for Air Travel Demand in 2016.

- Jardine, C.N. 2009. Calculating the carbon dioxide emissions of flights. Final report by the Environmental Change Institute.

- de Jong, S., Antonissen, K., Hoefnagels, R. et al. (2017). Life‐cycle analysis of greenhouse gas emissions from renewable jet fuel production. Biotechnology for Biofuels 10 (1): 64.

- Joseph Sorena, E.L. and Clark, A. (2015). Co‐Processing of HEFA Feedstocks with Petroleum Hydrocarbons for Jet Production. Commercial Aviation Alternative Fuels Initiative (CAAFI).

- Karatzos, S., McMillan, J.D., and Saddler, J.N. (2014). The Potential and Challenges of Drop‐in Biofuels, vol. 39. IEA Bioenergy Task Force.

- Langholtz, M., Stokes, B., Eaton, L. 2016. 2016 Billion‐ton report: Advancing domestic resources for a thriving bioeconomy, Volume 1: Economic availability of feedstock.

- LanzaTech. 2017. Technical Overview, Vol. 2017.

- Laskar, D.D., Yang, B. 2012. Aqueous Phase Depolymerization and Hydrodeoxygenation of Lignin to Jet Fuel. Abstract of papers at 34th Symposium on Biotechnology for Fuels and Chemicals (SBFC), April 30 May 3, 2012, at New Orleans, LA.

- Laskar, D.D., Yang, B., Wang, H., and Lee, J. (2013). Pathways for biomass‐derived lignin to hydrocarbon fuels. Biofuels, Bioproducts and Biorefining 7 (5): 602–626.

- Laskar, D.D., Tucker, M.P., Chen, X. et al. (2014). Noble‐metal catalyzed hydrodeoxygenation of biomass‐derived lignin to aromatic hydrocarbons. Green Chemistry 16: 897–910.

- LATAM Airlines Group. 2013. LAN Airlines completes biojet flight in Colombia

- Lister, D., Penner, J.E., Griggs, D.J. et al. (1999). Aviation and the Global Atmosphere‐Summary for Policymakers. Cambridge, UK: Cambridge University Press.

- Mawhood, R., Gazis, E., de Jong, S. et al. (2016). Production pathways for renewable jet fuel: a review of commercialization status and future prospects. Biofuels, Bioproducts and Biorefining 10 (4): 462–484.

- Morrell, P. and Swan, W. (2006). Airline jet fuel hedging: theory and practice. Transport Reviews 26 (6): 713–730.

- National Academies of Sciences, Engineering, and Medicine (2016). Commercial Aircraft Propulsion and Energy Systems Research: Reducing Global Carbon Emissions. Washington, DC: The National Academies Press https://www.nap.edu/catalog/23490/commercial-aircraft-propulsion-and-energy-systemsresearch-reducing-global-carbon.

- Novelli, P. 2013 The Challenges for the Development and Deployment of Sustainable Alternative Fuels in Aviation ‐ Outcomes of ICAO's SUSTAF Experts Group

- Radich, T. (2015). The Flight Paths for Biojet Fuel. U.S. Energy Information Administration, Independent Statistics & Analysis.

- Ragauskas, A.J., Beckham, G.T., Biddy, M.J. et al. (2014). Lignin valorization: improving lignin processing in the biorefinery. Science 344 (6185): 1246843.

- Renewable Fuels Association (2011). Fuel Ethanol Industry Guidelines, Specifications, and Procedures. Renewable Fuels Association (RFA).

- Reuters (2012). Auction to Kick‐Start California Carbon Market. Reuters.

- Reynolds, R.E., Herwick, G., McCormick, R.L. et al. (2017). Changes in Diesel Fuel ‐ the Service Technician's Guide to Compression Ignition Fuel Quality. National Biodiesel Board.

- Ruan, H., Qin, Y. Heyne, J. Gieleciak, R. Feng, M. and Yang, B. (2019), Chemical Compositions and Properties of Lignin‐Based Jet Fuel Range Hydrocarbons, Fuel, 256: 115947.

- Rumizen, M. (2016). Sustainable Alternative Jet Fuel Certification and Qualification. Washington, DC: CAAFI.

- Rumizen, M. 2017. Alternative Jet Fuel Approval Process. 2017 Worldwide Energy Conference, Workshop 18: Alternative/Renewable Fuels Panel Discussion –Technology Development and Certification.

- SBI bioenergy and Shell Press. 2017. Agreement grants Shell exclusive development and licensing rights for SBI Bioenergy patented renewable drop‐in biofuels.

- Secretariat, I. 2010. Aviation's contribution to Climate Change. BAN Ki‐moon.

- Shen, RC., Tao, L. and Yang, B. (2019). Techno‐EconomicAnalysis of Jet Fuel Production from Biorefinery Waste Lignin, BioFPR, 13: 486–501.

- Staples, M.D., Malina, R., Olcay, H. et al. (2014). Lifecycle greenhouse gas footprint and minimum selling price of renewable diesel and jet fuel from fermentation and advanced fermentation production technologies. Energy & Environmental Science 7 (5): 1545–1554.

- Talberg, A., Swoboda, K. 2013. Emissions trading schemes around the world.

- Team‐CAAFI, Reasearch and Development Team. 2014. Policy Research Needs Relevant to Alternative Jet Fuels CAAFI.

- The global aviation industry, I. 2010.The right flightpath to reduce aviation emissions. in: UNFCCC Climiate Talks.

- U.S. Energy Information Administration. 2017a. Annual Energy Outlook 2017.

- U.S. Energy Information Administration. 2017b. Sources of Greenhouse Gas Emissions, Vol. 2017.

- U.S. Energy Information Administration. 2017c. Spot Prices (Crude Oil in Dollars per Barrel), Products in Dollars per Gallon), Vol. 2017.

- U.S. Naval Research Laboratory. 2016. NRL Seawater Carbon Capture Process Receives U.S. Patent, Vol. 2017.

- United Airlines. 2011. United enters the biofuel age.

- United Airlines. 2016. United Airlines begins using biojet fuel in routine LAX flights.

- United Airlines and Fulcrum BioEnergy Press. 2015. United Airlines Purchases Stake in Fulcrum BioEnergy with $30 Million Investment.

- US Energy Information Administration. 2017a. Energy Outlook.

- US Energy Information Administration. 2017b. Factors Affecting Diesel Prices, Vol. 2017.

- US Energy Information Administration. 2017c. U.S. Gulf Coast Kerosene‐Type Jet Fuel Spot Price FOB (Dollars per Gallon), Vol. 2017.

- US Environmental Protection Agency (2005). Renewable Fuel Standard Program. US Environmental Protection Agency.

- US Environmental Protection Agency. 2016. EPA Determines that Aircraft Emissions Contribute to Climate Change Endangering Public Health and the Environment.

- US Environmental Protection Agency. 2017. Final Renewable Fuel Standards for 2014, 2015 and 2016, and the Biomass‐Based Diesel Volume for 2017, Vol. 2017.

- Valkenburg, C., Gerber, M., Walton, C., Jones, S., Thompson, B., Stevens, D.J. 2008. Municipal solid waste (MSW) to liquid fuels synthesis, volume 1: Availability of feedstock and technology. Richland, WA (US): Pacific Northwest National Laboratory, December. http://www.pnl.gov/main/publications/external/technicalBreports/PNNLY18144.pdf. Accessed October, 30, 2009.

- Virent. 2017. Bioreforming Technology, Vol. 2017.

- Virent and Tesoro Press. 2016. Tesoro to Acquire Virent in Support of Commercializing Renewable Fuels and Chemicals.

- Wang, W.‐C. and Tao, L. (2016). Bio‐jet fuel conversion technologies. Renewable and Sustainable Energy Reviews 53: 801–822.

- Wang, H., Ruan, H., Pei, H. et al. (2015). Biomass‐derived lignin to jet fuel range hydrocarbons via aqueous phase hydrodeoxygenation. Green Chemistry 17 (12): 5131–5135.

- Wang, H., Zhang, L., Deng, T. et al. (2016a). ZnCl2 induced catalytic conversion of softwood lignin to aromatics and hydrocarbons. Green Chemistry 18 (9): 2802–2810.

- Wang, W.‐C., Tao, L., Markham, J., Zhang, Y., Tan, E., Batan, L., Warner, E., Biddy, M. 2016b. Review of Biojet Fuel Conversion Technologies. NREL (National Renewable Energy Laboratory (NREL), Golden, CO (United States)).

- Wang, H., Feng, M., and Yang, B. (2017a). Catalytic hydrodeoxygenation of anisole: an insight into the role of metals in transalkylation reactions in bio‐oil upgrading. Green Chemistry: 1668–1673.

- Wang, H., Ruan, H., Feng, M. et al. (2017b). One‐pot process for hydrodeoxygenation of lignin to alkanes using Ru‐based bimetallic and bifunctional catalysts supported on Zeolite Y. ChemSusChem 10 (8): 1846–1856.

- Wang, H., Wang, H., Kuhn, E. et al. (2017c). Production of jet fuel‐range hydrocarbons from hydrodeoxygenation of lignin over super Lewis acid combined with metal catalysts. ChemSusChem: 285–291.

- Winchester, N., McConnachie, D., Wollersheim, C., Waitz, I.A. 2013. Market cost of renewable jet fuel adoption in the United States. MIT Joint Program on the Science and Policy of Global Change.

- WSU Maegan Murray. 2016. WSU Tri‐Cities researchers receive NSF grant to test market potential for jet fuel research.

- Yang, B., Laskar, D.D. 2016. Apparatus and process for preparing reactive lignin with high yield from plant biomass for production of fuels and chemicals, Google Patents.

- Yanik, S., O'connor, P., Bartek, R. 2012. Co‐processing solid biomass in a conventional petroleum refining process unit, Google Patents.