Health Care Needs Real Competition

by Leemore S. Dafny and Thomas H. Lee

HERE’S THE GOOD NEWS: Thanks to the Affordable Care Act, or Obamacare, more Americans have access to health care than ever before. The bad news? The care itself hasn’t improved much. Despite the hard work of dedicated providers, our health care system remains chaotic, unreliable, inefficient, and crushingly expensive.

There is no shortage of proposed solutions, many of which have appeared in these pages. But central to the best of them is the idea that health care needs more competition. In other sectors of the economy, competition improves quality and efficiency, spurs innovation, and drives down costs. Health care should be no exception.

Industry executives may think they have more than enough competition already. They spend their days fighting to keep patients from being lured away by competitors, new entrants, and alternative sources of care. Their cost of delivering care continues to climb while hard-bargaining insurers hold the line on reimbursements, or even reduce them. Compounding the problem, the services that account for most of providers’ profits, such as radiology and ambulatory surgery, are the ones most vulnerable to poaching. It’s hard to sleep at night when every one of Michael Porter’s five forces is arrayed against you.

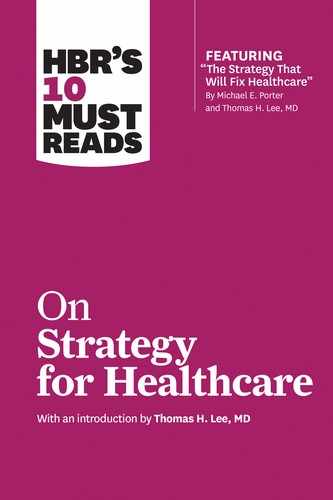

Many health care organizations have sought to stymie competition by consolidating, buying up market share and increasing their bargaining power with insurers and suppliers. From 2005 to 2015, the number of U.S. hospital mergers per year doubled (see the exhibit “Hospital mergers on the rise”).

Leaders of proposed health care mergers usually tout their potential to enhance value. But when asked to name a merger that has improved outcomes or lowered prices, they generally fall silent. That shouldn’t be a surprise. Years of research by one of us (Dafny) and others show that provider consolidation typically raises prices, with no measurable impact on quality. Indeed, merging with a competitor that has the same fundamental problems you do often increases the scale of problems without creating solutions. State and federal antitrust agencies have successfully quashed some mergers that looked like they would reduce competition, but the government can’t possibly challenge every case. It’s an endless game of Whac-A-Mole, and providers continue to bet that they’ll be among the “moles” to win.

Despite its short-term appeal, consolidation for the purpose of increasing negotiating clout will diminish the potential for the health care sector to create value and thrive in the long run. A new competitive marketplace is emerging in health care today, and organizations must decide whether to continue to deflect competition or make competing on value central to their strategy. In this article, we describe the fundamental shifts that are under way and outline the roles that all key stakeholders—regulators, providers, insurers, employers, and patients themselves—must play to transform health care.

Barriers to Competition

To compete on value, providers must meet patients’ needs better or at a lower cost than their competitors do, or both. But this kind of competition has been slow to arrive, because four interrelated barriers have blocked the way.

Limited reimbursement-based incentives

For the most part, providers have not been rewarded financially for delivering value, nor have they been meaningfully penalized for failing to do so. Many hospitals are able to hit their financial targets by competing on the strength of their brand and marketing messages—for example, claiming to have the latest technology, best facilities, or highest magazine rankings. A provider’s brand is often unrelated to its actual performance on outcomes, but it can enhance the provider’s ability to negotiate favorable reimbursement rates with insurers. Because providers’ revenues have not been contingent on the value of the care they deliver, they’ve had little incentive to compete on that basis.

Limited market-share incentives

Even when providers have improved value, they have not been sufficiently rewarded with increased market share. Consumers have been largely insulated from costs and thus have had little need to bargain hunt—and insurers haven’t done it for them—so lowering costs rarely generates an influx of new patients. Nor have providers gained market share by demonstrating improved quality. Most publicly available quality metrics are process measures (such as mammography and cervical cancer screening rates) that vary little among providers. Patients have been only mildly interested in such data—they assume providers are following guidelines—and have been unwilling to switch providers on the basis of them.

Hospital mergers on the rise

Health care providers may seek to blunt competition by consolidating. Over the past decade, the annual number of hospital mergers in the U.S. has doubled.

Source: American Hospital Association and Irving Levin Associates

Inadequate data on value

Good data on outcomes and costs is essential to designing and optimizing value-based care; unfortunately, there’s very little of it available. To the extent that providers have gathered data on outcomes, their collection and analysis methodologies have rarely been standardized, so the data sets are difficult to use for comparison, competition, or learning. Data on costs, at the level of individual patients or procedures, has been rudimentary at best, the result of a business environment with rampant cross-subsidization. Lucrative commercially insured patients, for example, subsidize lower-paying Medicare and Medicaid patients. Profitable services (such as radiology) subsidize unprofitable services (such as mental health care). Many providers find that using revenue from profitable services and contracts to cover losses elsewhere is simpler than doing the brutal work of measuring service- and patient-level costs and identifying ways to reduce them without compromising quality. In the absence of meaningful data on outcomes and costs, value-focused work has generally gone undetected and thus unrewarded.

Inadequate know-how

Finally, health care has suffered from a simple know-how problem. In the absence of financial incentives to pursue value and without good data to guide leadership, the management skills necessary for transforming care delivery have not developed. Health care leaders have not learned how to achieve consensus quickly, overcome cultural resistance to change, or nurture high-performing teams. They have not mastered the principles of lean management or high-reliability cultures. And they have not gained experience in making tough, data-driven strategic choices in the face of powerful resistance, such as when and where to cut services in order to improve efficiency.

Falling Barriers

These intertwined barriers have blocked competition in health care for decades, but we are at a critical turning point. A combination of market trends, advances in information technology, and a turnover in health care leadership is shifting the environment.

Increasing reimbursement-based incentives

In January 2015, Sylvia Mathews Burwell, the secretary of the U.S. Department of Health and Human Services, announced plans to shift 30% of Medicare fee-for-service payments—$362 billion in 2014—to alternative models that explicitly reward value. That change is slated to take effect by the end of 2016; the figure will rise to 50% by the end of 2018. Under the new contracts, providers that perform well on both quality and cost will see their reimbursements increase; underperformers will see them fall. Soon after Burwell’s announcement, Cigna declared that it was committing to the same goals, and other payers are following suit.

Even if insurers fall short of these targets, the message is clear: They’ve become ever more hostile to fee-for-service payment increases. We spoke with the leaders of a major hospital system about a recent contract negotiation with a commercial insurer. The system sought an 8% increase and were stunned by the insurer’s counteroffer: a 20% decrease. After public threats from both sides, the parties agreed on a contract that gave the provider no increase in the first year and small decreases in the next two years.

That provider’s leaders and most others we’ve spoken with agree: Providers can no longer negotiate and cross-subsidize their way out of their financial challenges. As personnel, equipment, and drug costs rise faster than revenues and as the path to higher revenues increasingly depends on better performance, the need for new value-oriented business models has become pressing.

Growing market-share incentives

Until recently, consumers had little reason to seek out value in health care. But as their cost burden rises, their behavior is changing. They’re increasingly signing up for lower-cost narrowed networks that limit access to more-expensive providers and choosing high-deductible or tiered insurance products that require them to pay more out of pocket for higher-cost care.

In addition, faster flows of information are allowing insurers to steer patients to similar—but cheaper—options more often and more effectively. For example, a patient who is scheduled for an elective operation might get a phone call from her insurer informing her that she’ll pay a lot less out of pocket if she has the same operation by the same surgeon in an ambulatory facility rather than the hospital where it has been scheduled. Presented with options like this, patients tend to call the surgeon—who may be indifferent to where the operation is performed—and the site gets switched.

Thus even if providers manage to renew their contracts with insurers at the same payment levels, they can still lose market share because their customer base is defecting to lower-cost alternatives. Conversations at patients’ kitchen tables are becoming as important to providers as their own contract discussions at negotiating tables—perhaps more so.

Meanwhile, increasing numbers of large employers and some insurers are implementing bundled payment programs that provide incentives to patients to get cancer care or major operations at medical centers with outstanding reputations for value. These employers and insurers are figuring out which kinds of patients will travel and how far and tailoring their programs accordingly. The pain from loss of market share is still minimal at most organizations, but the fear of patient defection is real and growing.

Improving data

Two developments are dismantling the data barrier: (1) the emergence of consistent standards and incentives for measuring outcomes and (2) the widespread adoption of technologies that enable data sharing. The National Quality Forum provides a gold standard for quality measures, and the International Consortium for Health Outcomes Measurement is defining minimum sets of outcomes measures for use in evaluating care for common conditions. In addition, Medicare bundled-payment programs increasingly include monetary incentives for publicly reporting outcomes. Given Medicare’s prior pattern with patient-experience data (reporting was voluntary at first, then mandatory), we expect a similar trajectory with disclosure of outcomes data.

Outcomes data is also becoming easier to collect and compare, in part because electronic medical records (EMRs) now sit on nearly every clinician’s desk. Clinicians have legitimate gripes about EMRs, but their continually improving interoperability across delivery systems has major implications for competition. When clinicians can readily see notes and lab results for patients receiving care in other organizations, they can make informed determinations about which ones provide the greatest value—and favor those providers by referring patients there.

Consider Atrius Health, an organization in the Boston area with nearly 750 physicians and 16 hospital affiliates. Atrius has functional access to EMRs for all those clinicians and providers, so its doctors can coordinate care effectively with them. All those hospitals can—and do—compete for Atrius’s business.

Expanding know-how

As the old guard that has long dominated medicine’s leadership exits the stage, the know-how barrier is falling. In the past, leaders of health care organizations were physicians who prized autonomy above all else. Today’s leaders are younger physicians who value teamwork over autonomy, recognize that managerial skills are essential, and actively seek out opportunities to acquire them.

These emerging leaders are pursuing degrees in management and strategy at business schools and participating in training programs for health care executives. The venerable two-year fellowship at the National Institutes of Health that used to launch physicians into leadership roles has been replaced with stints at consulting firms or management positions in other parts of health care or business. Look at the top ranks of health care organizations, and you’ll see 70-year-old physicians being replaced by MD/MBAs in their 40s.

Leaders today are not being picked for their skill in defending the status quo and pushing back at external foes. They are selected for their ability to lead performance improvement—giving organizations the ability to compete and win.

Catalyzing Competition

As barriers to competition crumble, the health care industry must take action to create positive change. There are five ways to accelerate progress.

Put patients first

A central tenet of most businesses is that customers come first. For many providers, though, keeping peace with internal stakeholders (particularly physicians) often takes precedence. But it’s only when organizations prioritize patient welfare that they can improve and compete on value.

Consider the initiative launched by the Cleveland Clinic in 2011 to offer same-day appointments to patients. At the time it was common for patients who needed specialty care to wait weeks or even months for appointments, often enduring anxiety during the delays and occasionally suffering complications that might have been averted with more timely care. Providers had little incentive to solve the problem; indeed, at academic medical centers, some physicians famously took pride in the length of their waiting lists. When the Cleveland Clinic began asking patients who called for appointments whether they’d like to be seen that day, other care centers rapidly followed suit. Although waits are still all too common, a web search for “same-day appointments” at academic medical centers now delivers thousands of hits. This simple development underscores the power of a patient-first approach to catalyze competition.

To be sure, reorganizing care delivery to meet patients’ needs is not easy. Unlike same-day appointments, which are fairly straightforward to implement, other changes can be highly disruptive. For example, the first step in any customer-centric strategy is segmentation. But segmenting patients into groups with similar needs, and assembling multidisciplinary teams to care for those groups, challenges the entrenched organizational structure of medicine and the flow of money within it. Thus it’s often met with resistance, particularly from the old guard.

But even the old guard knows that teams are better than individuals at providing coordinated, integrated, efficient care. And in a value-driven marketplace, teams are not just nice to have—they’re essential to competitiveness.

Create choice

For change to take hold in health care, decision makers at every level need real choices: consumers when picking health insurance products, patients when choosing clinicians, and clinicians when selecting the facilities where their patients receive care. When choices exist, clear winners and losers emerge, creating relentless pressure on all providers to improve. Rousing speeches by executives and policymakers can generate some enthusiasm for change, but fear of losing market share to a competitor is uniquely effective in mobilizing organizations. Organizations that are hungry or afraid—be they new entrants or established players—are often the most innovative, generating new choices and stimulating competition.

Take Advocate Health Care, a Chicago-based provider system formed in 1995 in a market dominated by famous academic medical centers like the University of Chicago and Northwestern. Advocate believed that the sustainable strategy in the long run was to offer patients a new choice—a clinically integrated health system focused on increasing quality of care while holding the line on total costs. After the Affordable Care Act was passed, Advocate committed to reorganizing and optimizing patient care in order to succeed under “shared savings” arrangements, which reward providers for beating cost benchmarks while meeting quality goals, and global capitation contracts, which pay providers a fixed amount of revenue per member, per month.

It was a bold move: To succeed, Advocate had to reduce the total cost of care while improving quality and service. But fee-for-service contracts, which dominated the reimbursement landscape at the time, actually punish providers for reducing spending—and fail to compensate them for activities that improve efficiency.

Advocate’s gamble paid off. It is thriving under global capitation, which accounts for nearly 40% of its revenues today (up from 11% in 2011), and generates another 30% to 35% of revenues from shared savings arrangements. Advocate has reduced spending growth to below local averages and has partnered with insurers to pass the savings along to consumers through more-affordable, narrow network products. Today Advocate is the largest health system in Illinois and has the state’s largest physician network. Growth via acquisitions and affiliations has played a supporting role in Advocate’s strategy, but its success derives not from its size but from its commitment to offering patients innovative new choices.

To seriously challenge market leaders, health care needs the kind of hunger demonstrated by Advocate—and by a senior executive we spoke to at the number two provider in another region. “We see [the market leader] as our competition, but they don’t think of us as theirs,” she told us. “It’s perfect. We are eating their lunch, and they are just waking up to it.” That provider has launched a wide range of patient-centric initiatives and organizational improvements, some of which have earned the most sincere form of flattery from its rival—imitation.

Stop rewarding volume

Value-based payments may be ramping up, but the vast majority of money in health care still moves through the fee-for-service system, which encourages inefficiency and overutilization. Simply layering modest incentives to offer services that might reduce costs—care coordination, for example—atop a fee-for-service chassis only results in more volume, even if it is better coordinated. Indeed, there’s no evidence that overall health care costs go down when the main intervention is adding services, however well intended. So don’t hold your breath waiting for savings to accrue from compensating physicians for developing end-of-life care plans with patients, for example. What leads to cost savings is reorganizing care around the delivery of health rather than health care.

One step in the right direction is to pay providers one lump sum to treat a patient’s condition over the entire episode of care or a defined period of time. Bundled payments are a prime example. As Michael Porter and Robert Kaplan detail in their July–August 2016 HBR article, “How to Pay for Health Care,” bundles are not a new idea, and their ability to drive value improvement in focused areas like transplantation is well established. But for bundles and other non-fee-for-service models to move from theory to practice on a broad scale, the incentives must be compelling and inescapable.

Standardize methods to pay for value

Both public and private payers must do more than push financial risk onto providers. They need to agree on the rules of the game. That means identifying segments of patients with similar needs—typically groups with the same condition (such as heart failure or prostate cancer)—and agreeing on the outcomes measures that will be used to assess the quality of care for the conditions. Payers should propose common methods for collecting and analyzing data, using input from providers, government agencies, and health care IT experts. And they should agree on a common payment structure for episodes of care so that providers can focus on improving care delivery rather than navigating the reimbursement maze. Insurers, meanwhile, can use the standardized data to identify and reward the highest-value providers.

Catalysts for competition

Five interrelated actions can spur value-based competition in health care.

While patients can’t be perfectly divided into all-inclusive, mutually exclusive categories, some movement in this direction is surely better than none. Working with providers, payers can change the game in health care by defining some rules.

Make outcomes transparent

Even when health care providers collect data on outcomes, and even when the data is standardized, providers often resist sharing results publicly. But real competition will emerge only if outcomes data is made available to decision makers, be they patients, payers, or other providers. Data transparency has already driven improvement in clinical outcomes in transplantation, cardiac surgery, in vitro fertilization, and patient experience. Consumers may initially pay the data little heed, but providers will still vie to earn the highest marks, and payers and referring physicians will ultimately shift volume toward those that do.

Such transparency unnerves many providers, who worry that factors beyond their control will negatively impact their results and that reported data will be misinterpreted. For example, “safety net” institutions that serve poorer populations and teaching hospitals that attract the sickest patients can look worse than those with healthier patient populations. Although risk adjustment methodologies can mitigate the effects of differences among patient populations, transparency will sometimes lead to rankings of providers that are not fair. Nevertheless, transparency can be more effective than financial incentives in driving quality improvement—and it’s often cheaper.

Stakeholder Roles

As the competitive marketplace emerges, no one wants to be the last to embrace the rapid changes under way. Here are some of the ways key stakeholders—governments, providers, payers, employers, and consumers—could be (and in many cases are) responding to the new landscape.

Government as regulator

Governments and their myriad agencies perform important regulatory functions, ranging from establishing and enforcing insurer-solvency requirements to specifying which health care facilities need backup electricity generators. But government also has a vital role to play in protecting and promoting competition. In particular, the Federal Trade Commission, the antitrust division of the Department of Justice, and state attorneys general all have a mandate to enforce competition law. However, the volume of health care mergers and the pace of change in business practices exceed the resources available to investigate them.

Increasing funding for these agencies is a wise long-term investment in the productivity of the health care sector. Entrenched anticompetitive practices—such as Blue Cross Blue Shield’s “exclusive territory” agreements, which preclude affiliates from competing against one another in most geographies—are difficult to challenge and undo. Dissolving mergers that prove anticompetitive is costly and exceedingly difficult as well. It is much more effective to get ahead of the gamesmanship.

Governmental agencies can also promote competition by monitoring and reporting on changes—particularly prospective mergers—in local health care markets. This will require new resources, but the business adage about spending money to make money (or in this case, to save it) applies.

One agency playing this role is the Massachusetts Health Policy Commission (HPC), established and funded by state legislation enacted in 2012. The HPC requires all providers to disclose merger and acquisition plans and conducts analyses of sizeable transactions. Merging entities may be asked to describe how their deals will benefit consumers and, after the fact, to report publicly on their progress toward goals. The HPC also set a target of 3.6% for the annual growth rate of total health care spending over the period 2013 through 2017—a figure that matched the projected growth in state GDP from 2013 to 2015. Providers complained that this target was arbitrary, but it had the intended effect: In contract negotiations with insurers, providers shifted their demands for reimbursement increases downward to reflect the goal.

Finally, regulators should seek to lower barriers for new entrants into payer and provider marketplaces. State legislatures can repeal (or not enact) laws that protect incumbents rather than consumers. Such laws are common: Texas, for example, requires that patients see a physician face-to-face in order to pursue a telehealth consultation, even when there are no legitimate health or safety justifications for such a requirement. Some states have created similar obstacles for retail health clinics that otherwise could safely and effectively serve patients. These barriers to competition reflect the tendency of state medical societies to resist challenges to traditional health-care-delivery models and demonstrate the need for government to ramp up efforts to promote delivery innovations, particularly in regions where competition among traditional providers is weak.

Government as payer

Medicare and Medicaid have emerged as potent leaders of change—developing innovative payment mechanisms, setting ambitious targets, and using their sheer scale to move the marketplace. Consider Medicare’s Comprehensive Care for Joint Replacement (CJR) program under which hospitals in 67 regions receive a lump sum for the entire episode of care involving total hip and knee replacements, rather than individual payments for discrete services (radiology, anesthesia, surgery, and so on). The key difference between the CJR and Medicare’s earlier bundled payment initiatives is that prior programs were voluntary; the CJR is mandatory.

Instead of meeting to discuss whether to participate in the CJR, hospital leaders now meet to discuss how to do so. Hospitals that organize to improve quality and efficiency can expect to share in the savings; those that do not should be prepared to lose money. In July, the Centers for Medicare & Medicaid Services announced plans to implement the approach for acute myocardial infarction, coronary artery bypass graft surgery, and femur fracture surgery. Those programs are slated to launch in July 2017.

Medicaid is becoming a change agent on a state-by-state basis as well. In Arkansas, Tennessee, and Ohio, Medicaid programs have recently implemented mandatory bundled payment programs that cover more than a dozen conditions, including asthma, pregnancy, attention deficit disorder, and congestive heart failure. Regulations in Arizona, Pennsylvania, and South Carolina require that commercial insurers covering Medicaid enrollees generate 20% to 30% of their revenues from value-based payment methods over the next three years. New York State has declared that 80% to 90% of Medicaid payments must be delivered through value-based models by 2020.

The incentive for providers to comply with these mandates is compelling. In many states, the Medicaid-covered share of the population is now pushing 25%. If those patients go elsewhere, many providers won’t have the critical mass they need to stay afloat. A decade ago, the idea of providers actively pursuing Medicaid patients would have defied credulity; the fact that they are now competing fiercely to hold onto that market share is a sign of the magnitude of the change under way.

Providers

Health care providers must be the protagonists in this unfolding story. Boards of directors have to ask questions at the heart of strategy: “What is our goal? How are we going to differentiate ourselves?”

Providers instinctively avoid new payment models, but they need to recognize the writing on the wall and embrace models that reward value, despite their risks and imperfections. They should work with other providers as well as insurers to develop new care-delivery schemes such as bundles and to engage in the open-ended work of making them better. Where a provider’s rivals are paralyzed, there is a competitive opportunity both to redesign care delivery so that it improves value and to reshape the payment models that reward it.

The emergence of the Health Care Transformation Task Force, a consortium of patients, payers, providers, and purchasers committed to improving health care, is compelling evidence that the landscape is changing. The task force includes 26 provider organizations that have committed to generating more than 75% of their revenues via payment arrangements that hold them accountable for cost and quality by 2020. The providers have also declared their support for voluntary reporting on outcomes for patients undergoing surgery as part of Medicare’s CJR bundle program.

These are not small providers under the spell of charismatic leaders. They include enormous delivery systems, such as Trinity Health, Advocate Health Care, Ascension, Dignity Health, Partners HealthCare, and Providence Health & Services. Nor are they merely paying lip service to the need for change: Task force providers and payers reported that 41% of their business was in new value-based payment models at the end of 2015—an increase from 30% at the end of 2014.

One path providers should not pursue is consolidation that does not directly lead to improved value for patients. Some providers argue that the Affordable Care Act encourages mergers as a means to create larger organizations that are more resilient in the face of financial risk. However, the real goal of health care reform is to encourage alliances that are better, not just bigger. There has been a good deal of horizontal consolidation (among competing hospitals, for example), but these deals often change little about the way care is delivered. In contrast, vertical integration (for example, between hospitals and nonacute facilities) may have greater potential to improve quality and efficiency—and in many cases can be achieved via joint ventures rather than mergers.

Too often, providers seek to grow by searching for targets with similar values and complementary geographic footprints. Instead, providers seeking growth should first consider how they can serve patients better, and only then ask if an acquisition is the way to do it. If managers can’t explain how an acquisition will improve the value of care, boards should question whether to pursue it.

Commercial insurers

Private insurers historically have battled with providers to secure the lowest reimbursement for each service. A better way for insurers to keep prices low is to foster and reward competition among providers on value.

First, commercial insurers should align themselves with the Centers for Medicare & Medicaid Services in making value-based payment the norm and adopt a similar structure for bundled payments. Early experience with bundles suggests that providers are more likely to be successful when they reorganize care delivery for all patients, not just those of a single payer, and when they implement bundles for multiple conditions, not just one. For this reason, commercial insurers should work together to create common definitions and outcomes measures for bundles and other value-based payment models.

At the same time, insurers should compete vigorously with one another for market share on the basis of creative new product offerings. Like providers, they should engage in more market segmentation (for example, creating insurance plans designed for families with young children). Simply getting bigger is not a strategy. The insurance industry is already highly consolidated; meanwhile, the pace of new-product design and levels of customer satisfaction are disappointing, to say the least.

Commercial insurers should continue to resist fee-for-service payment increases. This will keep a lid on costs and compel providers to focus on value rather than volume. Insurers should also combat provider consolidation by creating programs that effectively expand the market, such as offering patients incentives to travel to other regions to get quality care at a lower cost and negotiating prices on the basis of regional or national benchmarks.

Patients and employers

Consumers can energize the marketplace by creating real consequences for the winners and losers. If patients choose to receive care from high-value providers, which may mean traveling farther, then providers will focus their energy on improving care delivery. Patients should no longer settle for care that is not coordinated, compassionate, safe, and technically excellent. When it falls short, they should be vocal—or leave. Consumers should also demand a broader set of insurance choices from their employers—perhaps via private insurance exchanges—so that they can vote with their feet and switch to products that best suit their needs. Only then will payers find it profitable to introduce easy-to-navigate plans that reward low-cost, high-quality providers.

Employers also wield considerable influence. Major corporations such as Walmart are already collaborating with providers and insurers to create programs that encourage employees to seek out high-value care. Other entities that work on behalf of employees are proving similarly catalytic. The California Public Employees’ Retirement System (CalPERS), which provides health insurance coverage for 1.3 million people, is a case in point. CalPERS was seeing wide variation in prices for many procedures its members received, depending on where they got their care. For example, it was paying anywhere from $12,000 to $75,000 for joint replacement surgery, although there was no clear difference in the quality of the services. To address the problem, CalPERS introduced a “reference price” of $30,000—the maximum it would pay—and assembled a list of high-quality providers willing to accept it. Patients who chose to go to more expensive providers had to pay the difference out of pocket.

Patients responded by shifting their business to lower-cost providers. Faced with the threat of losing market share, most providers cut their prices. From 2011 to 2015, the number of California hospitals charging less than $30,000 for joint replacement increased nearly 60%, from 46 to 72. That kind of change could never have been achieved at the negotiating table; it took the fear of losing business to focus providers’ attention. Once it was clear that some well-regarded hospitals in California could meet CalPERS’s price, it did not take long for others to follow.

We don’t underestimate the turmoil that the health care sector faces in the years ahead. We know that every scenario for transforming the sector will yield unpleasant or unintended consequences for some stakeholders. But the consequences of failing to compete on value will be worse: chaotic, costly care of uneven quality, with a growing toll on individuals and the economy. Real competition must be the path forward. Health care organizations that try to deflect competition are on the wrong side of history and the wrong side of strategy.

Originally published in December 2016. Reprint R1612F