Future-Proof Your Climate Strategy

by Joseph E. Aldy and Gianfranco Gianfrate

AS GLOBAL WEATHER BECOMES MORE EXTREME, the threat that climate change poses for companies is no longer theoretical. Businesses are working to protect their assets and supply chains from increasingly severe hurricanes, heat waves, fires, and droughts. More and more companies are figuring such “climate risk” into their calculations, and investors are paying close attention. But there is a related threat that many haven’t fully taken in: carbon risk—the impact of climate-change policies on a company’s strategy and returns. As global warming worsens, companies can expect tougher government measures that will extract a growing price for their carbon emissions. These mechanisms could sideline the unprepared. In this article we describe the approach used by more and more companies to brace for the future and even flourish in it: internal carbon pricing. (See the exhibit “The rise of internal carbon pricing.”) At its core, this involves setting a monetary value on the company’s own emissions that reflects carbon prices outside the firm. In 2017 nearly 1,400 companies were actively using internal carbon pricing or planning to do so. As we’ll show, by putting their own price on carbon, companies can better evaluate investments, manage risk, and forge strategy.

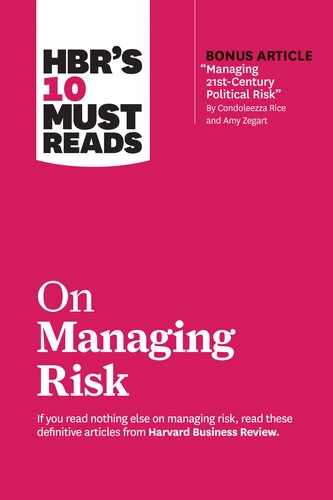

The rise of internal carbon pricing

The number of global companies that have adopted an ICP is growing rapidly.

Source: CDP, Putting a Price on Carbon (2017).

Before we get into the details, let’s consider the context. U.S. companies may think the pressure’s off, given the Trump administration’s efforts to dismantle existing climate and energy policies. But the rest of the world, and many U.S. states, are plowing ahead to strengthen their efforts to fight climate change. More than 60 regional, national, and subnational governments—representing about half of the global economy—have implemented policies that price carbon emissions, and 184 nations have ratified the Paris Agreement to reduce them. The governments of Mexico, Sweden, British Columbia, and other jurisdictions are currently levying taxes. And China, the European Union, and California are among those rolling out cap-and-trade programs that put a ceiling on total emissions to create incentives for reducing them. (See the sidebar “How Governments Price Carbon.”)

Thus even with the policy retreat under way in Washington, DC, American corporations must actively manage the potential increased cost of their emissions if carbon prices rise—for several reasons. First, state-level cap-and-trade programs have already led to carbon pricing for about one-quarter of the electricity consumed in the United States. Second, federal and state policies—such as regulations pertaining to fuel economy, the energy efficiency of appliances, biofuels, and renewable power—can impose an implicit carbon price on the firms that must comply with those rules. Third, the likelihood of expanded carbon pricing under a future administration and Congress must be considered when making investments in long-lived equipment, factories, and power plants. Finally, many American corporations operate in or sell products to countries that have already implemented cap-and-trade programs or carbon taxes.

It’s no wonder that companies are finding it hard to quantify the risk posed by this myriad of policies or to see potential opportunities. And consider how heterogeneous and volatile the policies are. Cap-and-trade emission allowances in the EU Emissions Trading System, for example, were trading at €5 per ton of carbon dioxide in 2017 but jumped to more than €20 per ton in 2018. Those prices apply to some sources of carbon dioxide in Sweden, but others there face a separate carbon tax greater than €90 per ton. And California’s emission allowances have traded at prices three times those in the Regional Greenhouse Gas Initiative, a power-sector cap-and-trade program in the Northeast and mid-Atlantic states.

Carbon policies may be all over the map, but one thing is virtually certain: In time, every jurisdiction will have some pricing scheme in place. By setting an internal carbon price (ICP), companies can prepare for uncertain external pricing in the future, and investors can get a clearer picture of a firm’s ability to compete in a low-carbon world.

Getting Started

Internal carbon pricing allows companies to place a monetary value on emitting a ton of carbon, even when few or none of their operations are currently subject to external carbon-pricing policies and related regulations. Companies use internal pricing in three key ways: to inform decisions about capital investments (especially when projects directly affect emissions, energy efficiency, or changes in the portfolio of energy sources); to measure, model, and manage the financial and regulatory risks associated with existing and potential government pricing regimes; and to help identify risks and opportunities and adjust strategy accordingly.

Although an ICP may be levied as an actual fee on business units within a company (as we discuss later), it is more typically a theoretical price used in economic and strategic analyses. For some companies, the price adopted internally is just a reflection of the existing carbon tax or price imposed where they do business. Some firms may not have operations in jurisdictions with explicit carbon-pricing policies, but they may still face carbon risk if their supply chains extend into those areas, especially if they are large consumers of electricity, fuels, and energy-intensive manufactured goods.

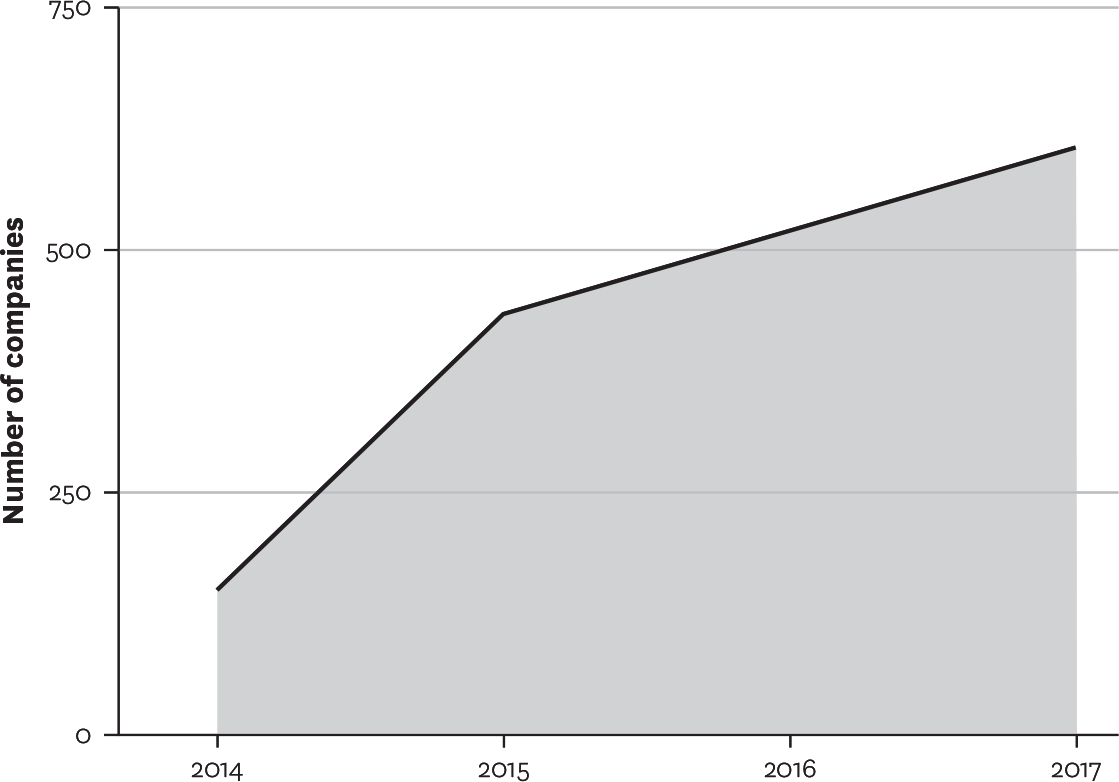

The prices adopted by companies globally vary widely, with some companies pricing carbon as low as one cent per ton while others assess it at well above $100 per ton. To put those numbers in context, $10 per ton of CO2 translates into about 10 cents per gallon of gasoline, one cent per kilowatt-hour of electricity from a coal-fired power plant, and 0.5 cents per kilowatt-hour from a natural gas–fired power plant. The carbon price selected depends on the industry, the country, and the company’s objectives. (See the exhibit “The range of internal carbon prices.”)

The range of internal carbon prices

Some companies price carbon as low as one cent per ton, while others assess it at well above $100 per ton. The price depends on the industry, the country, and the company’s objectives. Here’s a look at the distribution of 185 firms by price range in 2017.

Source: Authors’ calculations based on CDP data.

Before we illustrate the various ways in which firms use internal carbon pricing, it’s important to understand how they determine a carbon price.

Measuring Carbon Footprints

At the outset, companies must get a clear picture of their emissions. Since different countries (and different states in the same country) are adopting different environmental regulations and carbon prices, companies should determine the quantity and geographic location of both their direct and their indirect CO2 emissions. Energy firms and energy-intensive manufacturers in the United States already report their direct emissions to the U.S. Environmental Protection Agency (EPA) under two separate requirements, but most other companies are further behind in quantifying how much carbon dioxide they’re generating.

Direct emissions (often referred to as scope 1 emissions) come from sources owned or controlled by the company—for example, emissions from combustion in a company’s boilers or from its vehicle fleet. Indirect scope 2 emissions result from a company’s consumption of purchased electricity, heat, steam, and cooling. Other indirect emissions (scope 3) occur up and down a company’s supply chain—for example, in the production and transport of purchased materials and in waste disposal. The distinction between direct and indirect emissions shows that even companies that aren’t in carbon-intensive industries may actually be responsible for significant emissions. The global reinsurer Swiss Re, for instance, has very low direct CO2 emissions, but in 2017 its indirect emissions from business travel were 15 times as high as its direct emissions per employee. To raise awareness and decrease unnecessary flights, the company applies an internal carbon fee to its business units, charging each for the emissions associated with its employees’ trips.

A framework for mapping emissions is beyond the scope of this article, but many resources are publicly available. For example, Greenhouse Gas Protocol has created a standardized approach for measuring and managing corporate emissions, and it provides accounting and reporting standards, guidance by sector, and calculation tools.

Forecasting Future Carbon Prices

After mapping their emissions, companies should examine their exposure to current and estimated future carbon prices, beginning with an assessment of existing climate policies in the countries where they operate or plan to expand. In jurisdictions with cap-and-trade policies, the price placed on a ton of carbon is made explicit in the marketplace for emissions allowances—for example, on the European Energy Exchange platform. In other jurisdictions, carbon tax rates can be easily determined by looking at national tax laws. Additionally, several international organizations have compiled explicit and implicit carbon prices under existing government policies. The World Bank provides updated data from each national regulatory system in its annual State and Trends of Carbon Pricing. The OECD has recently published “effective carbon rates” that account for explicit carbon prices (such as EU Emissions Trading System allowance prices) and implicit carbon prices (such as gasoline taxes and regulatory mandates).

Current carbon prices are useful data points, but to build a long-term strategy, companies also need to make predictions about future carbon prices. This is a daunting exercise, given the lack of clear and consistent signals from governments and the uncertainty about technological and economic developments that could affect carbon pricing policies. But a collaborative approach can help.

In 2017 CDP (formerly the Carbon Disclosure Project) and the We Mean Business coalition created the Carbon Pricing Corridors initiative, which engages large companies in identifying industry-specific carbon price levels necessary to achieve the Paris Agreement goals. For example, in the chemical industry (according to executives from companies representing about $200 billion in market capitalization), carbon prices for 2020 should range from $30 to $50 per ton, increasing to $50 to $100 per ton by 2035. These numbers reveal three important insights about the implications of public policy for business. First, companies need to think beyond current regulations; the 2020 range is much higher than the price of carbon currently imposed by climate policies in most countries. Second, the average price is expected to increase over time as more-aggressive climate policies are enacted. Third, the range of prices will widen; the longer the time horizon, the greater the uncertainty about the possible impact of policy and technology innovations.

Predicting carbon prices requires navigating and critically reviewing data and analyses from climate experts, research institutions, peer companies, and environmental agencies. Forecasts produced by academics and government analysts are based on assumptions that are difficult for nonexperts to fully gauge. And relying solely on the estimates disclosed by peer companies may lead to groupthink effects and biased forecasts. Companies need to develop in-house expertise or rely on external professionals to identify the likely evolution of public policies and associated carbon prices. Ideally, they should project not only the level of prices but also the timeline of their changes, the extreme values that could be reached, and the probabilities attached to each possible scenario. (See the sidebar “Carbon Price Scenarios and Simulations.”)

Setting Internal Carbon Prices

With a sense of the likely trajectory of external carbon prices, companies can set their ICPs. This requires a deep understanding of both carbon economics and company operations and strategy.

One consideration is the time period that an internal carbon price is expected to cover. It is not uncommon for a company to adopt different prices for decisions with different time horizons. For example, when bidding on contracts, Acciona, a Spanish infrastructure developer, varies its internal price as follows: €36 per ton for near-term projects, €45 per ton for projects that extend through 2030, and €72 per ton for those that will continue through 2050.

In making short- to medium-term decisions, it’s probably adequate to set ICPs in line with current carbon prices. That’s what Alphabet did in 2016, when it reported to the CDP an internal carbon price of $14 per ton of CO2—a price aligned with the market value of the allowances traded that year in California’s cap-and-trade system. When making business decisions with a long-term impact, such as those that affect a firm’s business model, applying an internal price that reflects future scenarios makes more sense. ExxonMobil is highly exposed to enduring carbon risk domestically and internationally; it therefore uses a high ICP of $80 per ton—more than five times Alphabet’s and closer to the long-term social cost of carbon used by the EPA, the U.S. Department of Energy, and the U.S. Department of Transportation in many of their regulatory impact analyses over the past decade.

Some companies have established specific emissions or carbon-intensity targets. Carefully considered ICPs can help them meet those targets. In most cases these ICPs are framed as “shadow prices,” meaning that the carbon price is included in the evaluation of investment options, just as other costs are. This price, rather than representing actual outlays today, may reflect the costs the firm expects to be imposed on carbon emissions as public policy and regulations evolve over the lifetime of the investment. Suppose a firm is choosing among energy sources for a new power plant. Fossil-based energy may be the cheapest option given current regulations, but when a carbon price reflecting likely future climate policies is taken into account, a renewable power source may be more financially attractive. Similarly, shadow pricing may reveal hidden costs related to an investment. ConocoPhillips reported that after factoring in shadow pricing, it abandoned an investment project that otherwise looked financially worthwhile.

Sometimes internal carbon prices are not just hypothetical costs; as we saw with Swiss Re, they can be used to set and then levy an actual fee on business units for their emissions. The goal is to encourage a shift to low-carbon investments and behaviors, so the ICP must be set high enough to drive the desired change. Companies using this model charge each business unit an amount proportional to the emissions associated with its energy consumption. The fees generated can then be used either to reward the units with the best emissions-reduction performance or to make further investments to green the company. In 2012 Microsoft implemented an internal carbon-pricing system that holds business units accountable for their scope 1, 2, and 3 emissions. The collected fees—ranging from $5 to $10 per ton—are pooled in a central company fund that invests in internal efficiency projects, green energy, and carbon offset programs. Overall, Microsoft has reported more than $10 million in energy cost savings each year and emissions reductions of nearly 10 million tons since 2012.

A final consideration in setting internal carbon prices is an organization’s incentives for executives to deliver on carbon-reduction initiatives. If the company has ambitious targets and compensates its managers accordingly against those targets, higher ICPs can be instrumental in achieving objectives.

Applying the Price

Let’s look more closely at how companies factor internal carbon prices into their decisions about new investments, risk management, and long-term strategy.

New investments

When evaluating investments, a firm can assess the carbon footprint of each option and use its internal carbon price to estimate the potential carbon costs. For example, when deciding how to source energy for a new plant, an ICP can be applied to estimate the carbon costs of fossil-based electricity versus renewable sources. The product of the internal carbon price and the expected carbon footprint becomes a financial cost included in the net present valuation of the project.

The use of an internal carbon price enhances the quality of the financial valuation by allowing a more informed decision about production costs such as energy, machines, and materials, assigning them an implicit price that is more likely to increase than decrease over time. Beginning in 2016, Michelin set an internal carbon price of €50 per ton. Multiplying this price by a project’s expected carbon footprint over its lifetime allows the company to estimate the project’s carbon cost and return on investment. In this way, Michelin’s executives consider the implied cost of carbon—even for markets where there is currently no regulated carbon price—as they make decisions about production capacity increases, boiler upgrades, and logistics. Michelin intentionally set an ICP higher than the carbon price imposed in Europe and China, with the objective of getting its operations climate-ready both in countries with no climate regulations and in those where existing rules are likely to become more stringent.

Risk management

Climate policies are changing fast, and the regulated prices of carbon can move abruptly. Internal carbon prices are useful for gauging the impact of regulatory changes and assessing exposure to carbon risk throughout the supply chain, beyond the operations directly controlled by the company. Managing carbon risk is similar to managing other financial risks (such as currency and interest rate fluctuations) and compliance risks.

In jurisdictions that have cap-and-trade systems, power plants and factories must pay for allowances that grant them the right to emit carbon. Higher carbon prices make it more expensive for utilities to burn fossil fuels, thus encouraging a shift to cleaner sources of power. Utilities are hedging their exposure to rising carbon prices through energy investment decisions and carbon-allowance transactions, including the purchase and banking of allowances for use in the future, when allowance prices are expected to be higher. Internal carbon prices provide guidance for the hedging strategies of many utilities.

ICPs are also instrumental in managing regulatory compliance. Teck Resources, a Canadian metals and mining company, systematically conducts analyses to better understand firm exposure and risks under various carbon-pricing and regulatory scenarios. For example, in evaluating the exposure of its operations in British Columbia, it uses a variety of scenarios that assume ICPs ranging from $30 per ton (matching the provincial government’s current tax) to $50 per ton (the planned tax for 2021). Such scenarios have allowed the company to estimate potential carbon costs in 2022 that will range from $45 million to $80 million—valuable information that informs Teck Resources’ financial planning. Importantly, carbon risk management should not be limited to firms’ operations; internal carbon pricing can allow firms to reduce carbon risk up and down their supply chains by helping them benchmark suppliers and design carbon-reducing collaborations with them.

Strategy

Internal carbon pricing can inform long-term strategy that accelerates emissions reduction and helps companies find new markets and revenue opportunities. The Swedish packaging and processing company Tetra Pak, for example, has used its ICP in new-product development. Tetra Pak sets its ICP dynamically using the EU Emissions Trading System price as a reference point, with a floor price of €10 per ton. Such pricing helped the company gauge the potential financial impact of incorporating recycled and renewable materials into caps, cartons, and other packaging products, and it supported the introduction of more renewables into the company’s supply chain. It has also helped Tetra Pak launch innovative new packaging that uses less aluminum, which is energy-intensive to produce. Goldman Sachs has adopted an internal carbon price to help it achieve carbon neutrality in its operations. More broadly, its sophisticated understanding of carbon economics and scenario planning has allowed it to become the major financier for clean-energy companies globally and a leading underwriter for new products such as green bonds.

Assessing Results and Engaging Stakeholders

The integration of carbon prices into operations and strategic decisions should be regularly reassessed and the results fed back into the process to set updated prices. For example, if the ICP isn’t driving enough emissions reduction by the business units, or if the firm operates in a jurisdiction where the carbon price is higher than the firm’s ICP, it might make sense to raise the internal price.

Getting the business carbon-ready requires real commitment and a cultural transformation that should start with the board and top management. Leadership must communicate the firm’s emissions targets and strategies to all employees and consider monetary incentives for delivering on the targets. Companies should share the objectives of their ICP programs with partners along the supply chain and work with suppliers and customers to reduce their carbon risk. This will help optimize the ICP and enhance collaboration with all stakeholders—including customers, supply chain partners, local communities where green funds are directed, and, crucially, investors.

Investors have become increasingly eager to understand how firms manage the risks and opportunities under climate-change policies. For example, BlackRock, the world’s largest asset manager, recently announced plans to press companies to disclose how climate change could affect their business. And in 2017, more than 60% of ExxonMobil’s shareholders approved a resolution calling for greater disclosure of the financial risks posed by long-term climate-change policy.

Scenario-planning techniques, coupled with rigorous analysis of climate-policy risks, can provide executives with a broad view of how their business might evolve under various carbon-pricing regimes. Developing these sophisticated capabilities can help managers engage more effectively with regulators and policy makers.

Getting on Board

Many companies don’t yet price carbon. Some may be fairly carbon-lean and thus don’t expect emerging carbon policies to have a significant impact on their cash flows. This is often a false assumption. Companies with negligible scope 1 emissions may still be high polluters when scope 2 and 3 emissions are considered. Other firms aren’t pricing carbon because they lack the capabilities needed to anticipate and evaluate potential regulations and policies, and they don’t fully realize how exposed they are to carbon risk.

However, the rapid adoption of internal carbon pricing shows that companies increasingly recognize its importance to competitive operations and strategy. Only firms that understand and proactively manage carbon risk will sustain long-term advantage as more and more countries move to decarbonize their economies.

Originally published May–June 2019. Reprint R1903E