13

Fringe Benefits You Will Love, Part 1

The proper avoidance of taxes is the only intellectual pursuit that still carries any reward.

—John Maynard Keynes, economist, Economic Consequences of the Peace (1920)

One of the biggest questions that I get at my seminars is, “How do I get money tax-free out of my corporate business?” The answer is to establish a load of tax-free fringe benefits. In fact, this chapter could be subtitled, “Getting Money Out of a Corporation Tax-Free.”

If starting a successful small business is the engine behind riches, then fringe benefits are the wheels and the frame around this engine.

You’ve probably heard about how many of the big, rich corporations are providing a host of benefits to their employees. The interesting fact is that most of these benefits can be provided by small businesses as well. It’s just that most small business owners never find out about what choices are available to them.

Author’s note: The myth that “my accountant takes care of my taxes” has kept people ignorant about all the amazing fringe benefits that are available.

You will find some fabulous information in this chapter that, in many cases, isn’t available elsewhere. It will give you a good overview of every available fringe benefit that I can suggest for small and mid-sized businesses. Use the various benefits as a checklist for your business.

Although time and space do not permit me to discuss every detail involved in all fringe benefits, and a whole book could be devoted to this subject alone, I give a good overview of what’s required to establish each benefit and to bulletproof the benefit from the Internal Revenue Service (IRS). I also discuss any drawbacks to each benefit that you should be aware of, such as discrimination problems.

I should note that I discuss only benefits that would be available to small-business owners and not necessarily only to publicly traded corporations, although all the benefits mentioned here can and have been used by even the biggest companies.

Pay particular attention to which benefits can be offered to both owners and employees, which benefits can be offered only if you don’t discriminate (which would be most of the benefits), and which benefits have limitations on what can be offered to owner/stockholders. In addition, although all these benefits assume that you’re operating as a corporation, many also apply to other entities, such as limited-liability corporations (LLCs) and sole proprietorships. All in all, using the information in this chapter will result in huge tax savings that will pay for this book many times over.

Author’s note: For a number of benefits, you cannot discriminate in favor of highly compensated individuals, stockholders, or owners of 5 percent or more of stock or profit interest. Highly compensated people for purposes of this book are people who make over $115,000 per year or who own 5 percent or more of the stock or who own 5 percent or more of the business. Thus, throughout Part 3 of this book, this is what I mean when I state that you can’t discriminate in favor of highly compensated people.

Tax-Free Use of Property, Equipment, and Services

You’re going to like this. This is one of the broadest ways to obtain tax-free fringe benefits. This benefit is also known as working-condition fringe benefits. These types of benefits are defined as “any property or services given to an employee by an employer that would have been deductible or depreciable by the employee as a business expense had the employee paid for the property or services.”1 It applies, however, only to employees and not to their dependents—sorry!2 Here are some examples:

• Most business publications

• Business-oriented books

• Use of employer-provided cars to the extent used for business

• Computers used for business

• Cell phones

• Fax machines

• Memberships in business-oriented associations

• Memberships to business-oriented Web sites

• Job-placement assistance if it results in some benefit to the employer, such as raising the morale of remaining workers, and the placement is in the same or similar trade or business

Example: Sam runs his insurance business as a corporation. He wants to receive memberships in the local Chamber of Commerce and life underwriters association. He also wants to receive various publications for insurance agents and various sales publications. His corporation may provide Sam with these memberships and subscriptions as tax-free working-condition fringe benefits because Sam could have deducted the cost of these publications and memberships had he spent the money himself.

Author’s note: You may be wondering why a working-condition fringe benefit is such a good deal because the employee could have deducted the cost of such an item anyway. Good question! The reason is that when an employee takes a deduction for business-related expenses, it’s as an itemized, nonbusiness deduction. These types of deductions have phaseouts and must exceed a threshold amount of 2 percent of your adjusted gross income (net income from a business plus wages, dividends, pensions, rents, etc.). However, if the employer provides these benefits, they are fully deductible by the corporation and tax-free to the employee. There are no phaseouts and no threshold amounts that they must exceed. Thus you get the full benefit of the deduction.

Example: Marjorie operates her network marketing business as an S corporation. She wants to subscribe to various home-based business publications and subscribe to special services for networkers, such as The Greatest Networker Web site maintained by the well-known John Milton Fogg George Madeau. If her corporation pays for these subscriptions, she may receive these benefits tax-free.

Discrimination Is Fully Allowable

This is one benefit in which Congress allows for any type of discrimination, even if the benefit is provided only to the officers or directors or other highly compensated employees of the company. You just can’t discriminate when providing any product testing. Don’t ask me why!3

Example: Sock’em Corporation provides cell phones and computers only to its executive officers. These benefits are fully deductible by Sock’em and tax-free to the employees even though they’re not provided to all employees.

What Is an Employee?

The working-condition fringe benefit applies to employees. Strangely, however, Congress allows many people to be treated as employees that you would never have thought would qualify for this one benefit. For example, for purposes of this rule, employees would include partners and members of the board of directors (although board members can’t be used in any product testing).4 In addition, independent contractors are allowed to be given working-condition fringe benefits on a tax-free basis as long as they don’t involve parking or product testing.5 Self-employed owners are not deemed employees under this rule; however, they can deduct these items anyway as business deductions without any limitation. Thus, in effect, they get the benefits too.

Author’s note: I often wonder what Congress was thinking when it carved out such limited exceptions as product testing and parking for independent contractors. This simply adds needless complexity for some narrow exceptions.

Consumer Testing of Products by Employees

Your corporation can provide employees with products to test and evaluate that are manufactured by you for sale to customers. However, to avoid taxation of the employee on the receipt or use of these products, you must meet the following conditions:6

• It would be a normal expense of the employer (which is usually the case).

• Valid business reasons necessitate that the products be tested off the premises of the employer.

• The products are indeed furnished for testing and evaluation.

• The products are available to the employee for a period that isn’t longer than needed for testing and evaluation.

• At the end of the testing period, the item is returned to the employer.

• The employee must submit detailed reports on his or her evaluation.

• The length of the testing and evaluation period is reasonable for the product.

• The employer imposes strict limits on personal use, such as a prohibition against nonemployees using the product.7

• The employer does not discriminate against highly compensated people in the testing unless it can show a good reason.

No-Additional-Cost Fringe Benefits

A company may provide services to employees on a tax-free basis and IRS bulletproof this benefit if it meets these conditions:

• The services are offered to customers in the ordinary course of business.

• The company doesn’t incur substantial additional cost in providing these benefits.8

You could provide services at no additional cost, for example, when you have excess capacity.

Example: The Shipandstore Corporation provides air transit services and hotel rooms to customers. If there are some free spaces in the plane or some unoccupied hotel rooms, the corporation may provide these tax-free to its employees.

The key to this fringe benefit is that the services offered are in the same line of business as the employer and normally are offered to nonemployee customers.

Example: The Foolproof Bank offers car washes to nonemployees in order to raise funds for charity. This is not the business of the bank, and free car washes provided to employees would not qualify as no-additional-cost fringe benefits.

Author’s note: Even if the employee agrees to reimburse the employer for the increased cost, this would not qualify as a tax-free fringe benefit. The following example illustrates this point.

Example: High-Cost Computer, Inc. (HCC), repairs computers. Jane is an employee with some big computer problems. HCC fixes her computer. The normal retail cost to fix it would have been $500 for labor and materials, but the actual out-of-pocket cost would have been only $100. Even if Jane reimburses HCC for the $100 cost, she would be taxed on the $400 of extra benefit. This is not a no-additional-cost benefit because HCC paid $100 to provide $500 worth of benefits. Jane’s reimbursement does not alter this fact.

Discrimination Toward Owners or Highly Compensated People Not Allowed

Sadly, you can’t discriminate in favor of highly compensated people or owners of the business who hold 5 percent or more of the stock.9

The Bottom Line

For this benefit to be tax-free, the employer must not incur any extra cost, and the benefit provided must be the same services as provided to customers in the employer’s normal course of business.

Tax-Free Day-Care Assistance

You can provide day care tax-free to all employees10 up to a maximum of $5,000 per year ($2,500 if married filing separately).11 The self-employed are considered employees under this rule. Hooray! Even partnerships can offer this benefit to partners who are treated as employees.12 Moreover, you can either pay for the employees’ day care directly or reimburse the employees for the expenses.13 How’s that for flexibility? However, you cannot discriminate in favor of highly compensated people or owners or stockholders who have a 5 percent or more interest in stock or profits of the company, and there are limitations on the benefits that can accrue to the owners as well. This will be discussed below.

Requirements to Bulletproof Tax-Free Day Care from the IRS

In order to receive this benefit tax-free, you must meet all the following requirements:

• The plan must provide employees with dependent care to children who are under age 13 or to any other dependents who are either physically or mentally incapable of caring for themselves.

• You must have a separate, written plan. It doesn’t have to be long and fancy, but you must have a plan in writing that shows who will get the benefits and what these benefits will be. You also have to notify the other employees of the availability of this benefit. You just can’t keep it secret. Nice try!

• A company cannot discriminate in favor of highly compensated employees, more than 5 percent owners, or more than 5 percent stockholders. However, even if a company is found to be discriminating, those employees who are not highly compensated or do not own 5 percent or more of the stock or more than 5 percent of the business will have their benefits tax-free.

• The employee must provide some documentation to the employer, such as the name, address, and Social Security Number or Taxpayer Identification Number of the provider. See your accountant about this.

• Even if you give this benefit to everyone, you can’t have more than 25 percent of the total benefits go to any stockholder or business owner who owns more than 5 percent of the stock or the business.

Author’s note: I personally find this extremely irritating, not to mention idiotic, that Congress would place a limit on the benefits available to owners even if they don’t discriminate. This only complicates the tax law. Why place a limit on benefits to business owners if there’s no discrimination? In addition, placing limits on benefits to owners hurts the small-business owner who may not have lots of employees, and in many cases, these people need the help the most.

I should note that you cannot have your child be the day-care provider if he or she is under age 19 by year’s end or your dependent even if over age 19. Once your child hits age 19 and stops being your dependent, he or she can be a qualified provider for the other children.14

Author’s note: The same rule would apply to any other relative, such as an employee’s parents. If an employee pays one of his or her parents to take care of the employee’s children, these payments would be tax-free if the parent was not a dependent of the employee. This might be a great way to get your parents some money and to take care of your child-care problems at the same time.

Company-Provided Adoption Assistance

There’s a big demand from couples to adopt children. Because of this, Congress created a nice fringe benefit for adoption expenses. A company can set up a qualified plan and pay up to $13,190 in 2014 of adoption expenses per child15 on a tax-free basis.16

Qualifications Needed to Bulletproof This Benefit from the IRS

In order for a company to provide these benefits tax-free, the adoption assistance must meet the following criteria:

• The plan must be in writing, and all eligible employees must be notified.

• The plan must be nondiscriminatory. However, unlike the day-care assistance benefit, there’s no limit on how much goes to the owners or stockholders. The plan just can’t discriminate in favor of highly compensated people, 5 percent or more stockholders, or 5 percent or more owners.

Unfortunately, what Congress gives, it also takes away. The tax credit for the benefits are expected to start phasing out as your adjusted gross income (AGI) exceeds $197,880 in 2014 and completely phases out if your AGI exceeds $238,880 in 2014.17 As a reminder, your AGI generally means any net income from a business plus dividends, interest, rents, penalties, and wages, with a few further modifications. The following examples will illustrate how the phaseout works.

Example: John and Mary have an AGI of $217,880 in 2014. If they receive from Mary’s employer $6,000 of expenses, only one-half, or $3,000, is tax-free. The other $3,000 is taxable. The reason is that they earn $20,000 more than the allowable $197,880, halfway to the $40,000 phaseout. If their AGI were $207,880, one-fourth through the $40,000 phaseout range, one-fourth ($1,500) would be taxable and three-fourths ($4,500) would be tax-free.

Author’s note: Although this is not a tax policy book, think about what Congress has done. This program essentially subsidizes poor to middle-class taxpayers to adopt children and discourages wealthy people, who can best afford children.

Tax-Free Health Insurance

One of the big disadvantages of being solely an employee (among the others mentioned in Chapter 1) is that you can deduct only medical insurance premiums and other medical expenses that exceed a very high threshold, 7.5 percent of your AGI—your net income from a business plus wages, interest, dividends, pensions, and some other modifications.18 Thus, unless you have a huge amount of medical and dental expenses, you likely won’t get any deduction for these expenses.

However, if you have a side business, your business can provide you and your employees and their families with health insurance 100 percent tax-free starting in the year 2003 and thereafter.19 Moreover, you just need to pay for the insurance premiums. No written plan is required, and the benefit is available to all forms of business, whether incorporated, partnerships, or even self-employed.20

In fact, health insurance almost always should be provided owing to the tremendous flexibility of this benefit. For example, long-term care insurance is deemed to be health insurance,21 as are Medicare supplement premiums.22 Companies even can cover domestic partners, although for the payments to be tax-free for an employee, the domestic partner must qualify as a dependent of the employee.23

In addition, a company even can reimburse the employee for the insurance premiums paid under the following conditions:24

• The employer has a plan for health insurance coverage.

• The employer requires the employees to prove what actually was spent on health insurance.

Author’s note: Being able to reimburse employees becomes essential, especially for small-business owners, whenever an employee would not be able to get coverage owing to preexisting conditions.

Finally, and this is my favorite benefit of providing health insurance premiums, the health insurance can be provided on a discriminatory basis. You just can’t discriminate based on health factors,25 and it must seem to cover employees, not just stockholders or owners.26

With the new health reform law, in 2012 and thereafter, medical insurance must be nondiscriminatory but can have the same exceptions as that of the self-insured medical plans.

Example: Harry provides health insurance to all his full-time employees but charges a premium for those with prior health problems. This would be prohibited. However, if Harry provided health insurance to all the officers, regardless of health problems, and a lesser plan to other employees, this would be allowable.

The bottom line is that this is a great, flexible fringe benefit that most firms should provide regardless of size and regardless of entity.

Set Up a Self-Insured Medical Reimbursement Plan

This is a plan that covers all your medical expenses that are not covered by insurance, such as mileage to and from the doctor, deductibles, coinsurance, braces and other dental expenses, hearing aids, chiropractic therapy, over-the-counter medication that alleviates a medical condition, and much more. This is in addition to your health insurance. You’re not dropping your health insurance coverage. However, this is much more limited for 2 percent or more owners of S corporations and partnerships. See the detailed discussion in Chapter 4 on this topic.

Under the new Obamacare rules, if you set up a self-insured medical plan to cover medical expenses not covered by insurance, you will need to also provide the employees medical insurance or you could be penalized with providing a nonqualified plan. However, if you don’t provide the self-insured plan, you won’t be penalized for not providing medical insurance if you have fewer than 50 employees. Here is a good example of “no good deed goes unpunished”.

Provide for Disability Insurance

Disability insurance covers two situations: loss of income owing to being disabled from an accident or illness and payments for the loss of a bodily function, a limb, or an organ.

Loss of a Bodily Function, a Limb, or an Organ

Payments made for the loss of a bodily function or a limb are tax-deductible for your company and tax-free for the employee.27

Example: Juan works in a machine shop and loses an eye. The company provides disability benefits, paying $100,000 for the loss of a bodily function or an organ. The $100,000 that Juan receives is tax-free.

Disability Owing to Accident or Illness

Today, there’s a much better chance of being injured by accident or suffering a long-term illness than dying. Sadly, when a catastrophe of this nature occurs, few would have the ability to continue their income if they could not work. This is the purpose of disability insurance.

Interestingly, companies have two options regarding disability premiums paid to an insurance company. The premiums can be either tax-free to the employee or taxable to the employee.28 There’s a drawback to each option. If they’re tax-free to the employee, then the benefits would be taxable to the employee if he or she gets paid on the policy. However, if the employee gets taxed on the premiums or in fact pays the premiums, then the benefits are not taxable.29

Example: Wise Corp. provides disability insurance on all its employees tax-free. Joan, an employee, becomes seriously injured in a car accident that keeps her out of work for six months. All payments to her will be fully taxable because the premiums were tax-free.

IRS-Approved Tax-Planning Strategy

The IRS has ruled in a private ruling30 that an employee who had paid the total premiums for disability coverage in the policy year in which he suffered a disability and received payments would not be liable for taxes on those payments, even though his employer had paid the premiums in previous years. In other words, all disability payments that the employee received would be allocable to his payments and would not be taxable.

Isn’t this an amazing country?!

What this means to you is simple. Have your company deduct all premiums and treat them as tax-free to all the employees. However, in the year of a disability, have the company treat the premiums as taxable to the disabled employee; thus it will make the benefits tax-free.

Example: Joan is permanently injured in a car accident. If in the year of the injury she were taxed on the premiums paid by her employer, the benefits would seem to be tax-free.

As a final note, self-employed taxpayers or S-corporation shareholders who own more than 2 percent of the stock or partners are not employees.31 Thus a self-employed person cannot deduct disability insurance premiums. However, the benefits then would be tax-free.

The Bottom Line

All companies should provide for disability coverage and should both deduct the premiums and treat them as a tax-free benefit to the employee. If the benefit is for loss of a bodily function, the benefit is always tax-free. If the benefit is for loss of income owing to sickness or accident, treat the last year’s payment as income, and the benefits should become tax-free as well, not withstanding what was done in the prior years.

De Minimis Fringe Benefits and Occasional Supper Money

Your company can provide any employee—even if it discriminates in favor of officers or highly compensated people32—property or services under both the following conditions:33

• The value of the property or services is so small or inconsequential as to not warrant an accounting.

• The property or services are not provided too frequently.

Thus, even if a fringe benefit were small in value but provided daily, it would not be deemed de minimis. It must be both infrequent and inconsequential to be a de minimis fringe benefit.

Example: Financial Destiny is a small corporation that provides income opportunities. If it provides a one-time payment of $1,000 to an employee, this would not be deemed inconsequential and would be fully taxable.

Example: Financial Destiny also provides bus fare for some employees daily. Even though the value of this benefit is inconsequential, it’s provided too frequently, so the total value of the fares would not be considered inconsequential.

Author’s note: Any use of an employer-provided car, constant use of a season tickets, or membership in a country club would not be a de minimis benefit. Such benefits may qualify as working-condition fringe benefits, however.

Examples of De Minimis Benefits

Now that you know what benefits are not de minimis, here are some de minimis benefits that can be provided:

• Occasional typing of a personal letter by a secretary

• Weekly coffee and donuts

• Holiday gifts of low value

• Holiday turkeys if cost is usually less than $25

• Occasional theater and season tickets

• Free soft drinks

• Occasional use of the copy machine, fax machine, or other similar equipment if personal use is less than 15 percent34

Author’s note: The IRS strangely has noted that monthly transit passes that cost no more than $21 would be deemed de minimis if paid to an employee.35 But it doesn’t treat the self-employed as employees. Sorry!

Occasional Supper Money

The IRS allows the payment of occasional supper money under all three of the following conditions:36

• The supper money is provided occasionally and not regularly.

• The supper money allows an extension of the normal workday.

• The supper money enables the employee to work overtime.

Author’s note: This benefit applies only to employees. Thus, if you’re self-employed, you can’t give yourself supper money. You can, however, give it to any employee of yours. In addition, if you incorporate your business, you then become an employee of that business and are eligible to receive supper money.

The key is that supper money can be provided to anyone or everyone if there’s a need for emergency overtime. It can’t be based on hours worked, such as $3 of supper money for each hour of overtime. Thus, if you have a business that requires some overtime owing to a time crunch or emergency, you can provide supper money.

Example: Footer Podiatry, Inc., has a crunch of business once or twice a month. If the employees work two extra hours of overtime, the company can provide tax-free supper money. If this happens every week, this probably would be deemed too frequent and would be taxable.

Author’s note: I’ve spoken with the IRS ruling division about this. Their policy is to allow supper money if it isn’t provided too frequently, such as two or three times a month. Thus, if you have overtime required of employees that does not exceed three days a month, you should be able to provide a reasonable amount of supper money tax-free. Limit the money to what it would cost one person to eat in a medium-priced restaurant. Paying $100 per day for supper money probably would not be reasonable.

The Bottom Line

I don’t consider de minimis fringe benefits the top benefit in this chapter. They have a narrow application and, as the name indicates, can’t be too beneficial. However, when you consider all the items that can be deemed de minimis, such as monthly transit passes under $21, these benefits can add up and not be de minimis to you or your company.

Qualified Employee Discounts

How would you like to be able to provide your employees with tax-free discounts on a wide range of products and services? Well, you can, and it’s easy to implement in any company of any size.

The term qualified employee discounts means giving your employees property or services that you normally provide to the public in your company’s ordinary course of business but you provide them at a discounted price to your employees. If you provide qualified employee discounts, the employees receive the property or services tax-free.37

Example: Safecracking, Inc., runs a nationwide banking consulting service. If the company provides discounts on banking fees to its employees, this would be a qualified employee discount. However, if it purchases and distributes season’s tickets for the Redskins football games, this would not be a qualified employee discount because the company is not in the business of selling season tickets.

A company can provide discounts on any product or service that it offers to the public—with the following exceptions:

• Stocks and bonds

• Commodities

• Real estate

• Money

Author’s note: It’s too bad that Congress passed these exceptions. I would have loved to work for a currency house or a bank and get discounts on money. Wouldn’t you?

Limitations on Qualified Employee Discounts

Besides limiting discounts to qualified property, Congress has placed some limitations on the amount of the discount. As a result of some “tax simplification,” the rules vary depending on whether you’re providing services or property.

If you’re providing a service, such as a flight or legal service, you can allow up to a 20 percent tax-free discount.38

Example: The law firm of Shaft and Shaft provides legal services to all its staff members at a discount. If the normal fees are $300 per hour, it can offer the legal services at a 20 percent discount, charging $240 per hour. If it offers these services for $100 per hour, the $140 “excess” discount would be taxable to the employee.39

If your firm provides discounts on property, the amount of the discount can’t exceed the gross profit percentage.40 You might be wondering what this means! The gross profit percentage is the sale price minus the cost of the property. Thus, in effect, you can offer the property at your company’s cost.

Author’s note: Why Congress couldn’t use the term cost of the property instead of gross profit percentage is beyond me.

Example: IBM offers computers to its employees at a discount. If the normal price of a computer to customers is $2,000 but the profit that IBM makes on each computer is $500, the company can offer its computers to its employees at $1,500. Anything above this discount would be taxable to the employee.

Nondiscrimination Rules

In order to provide qualified employee discounts, you must offer them on a nondiscriminatory basis. You can’t give the discounts just to the officers and other highly paid individuals. However, if you do discriminate, the discounts are still tax-free to employees who are not 5 percent owners of the stock or business or who make less than $115,000 for 2014 and $120,000 for 2015.

There’s a bit of sunshine here. There are some employees who can be deemed ineligible for the discounts:

• Employees who have less than one year of service with the company

• Employees who normally work less than 17.5 hours per week

• Seasonal employees who normally work less than six months per year

• Employees who are under age 21

• Employees who are subject to a collective-bargaining agreement (union contract)

• Employees who normally work less than 1,000 hours per year41

Author’s note: As you can see from some of the fringe benefits, part-time workers need not be offered many benefits. Maybe this is the reason so many companies are hiring employees on a part-time or seasonal basis.

The Bottom Line

Qualified employee discounts can be a real benefit to companies and to their employees. They’re available, however, only for products and services normally provided to the general public. Also, if they are services, the discount is limited to 20 percent. If the discounts are for property, they’re generally limited to the gross profit percentage, which means that the employee can pay the cost of the property.

Deducting Exercise Equipment and a Gym

As we’ve read in many news articles, exercise is being touted as a partial cure for many ailments. Wouldn’t it be great if you could deduct the cost of exercise equipment, tennis courts, and even a gym and provide these items tax-free to your employees and, if incorporated, to yourself? The answer is that you can!

Requirements to Bulletproof Company-Provided Athletic Facilities from the IRS

In order to make this benefit tax-free, you must meet several well-defined tests:42

• The equipment or gym generally must be on the company premises or leased or owned by the employer. (Thus it doesn’t have to be physically in the same building as all the employees.)

• The equipment or gym must be operated by the company.

• The equipment or gym must be used substantially by employees of the company, their spouses, and their dependent children.

There are a couple of implications that can be derived from these rules. First, you can’t pay for a health or country club membership because these clubs would be used by the general public and not substantially by your employees.43 Second, the facilities must be run or operated by the company. This means that you can’t deduct the use of a resort with facilities such as tennis or a swimming pool, which would be part of the association dues.

In addition, the IRS has noted that employees can include partners and employees who are separated from the company (either through retirement or disability).

Example: Your company provides a gym in the office for your employees. The gym is staffed by personnel paid by the company. The gym would be fully deductible and tax-free to the employees. If the company paid for health club memberships, on the other hand, this would not be tax-free to the employees. In addition, the athletic facility must not be offered only to officers or highly paid employees. Most staff members should be allowed to use the facility.

Author’s note: Self-employed individuals ordinarily cannot give themselves this fringe benefit because self-employed individuals are not considered to be employees. However, if you’re self-employed and you hire your spouse and/or other family members, they become your employees. If you place a gym in the location where your family employees work, you may be able to deduct the cost of the gym and the equipment. It’s vital, however, that only employees or their family members use this facility. Thus don’t let your friends use the gym. Keep an exercise log for everyone using the facility.

What Types of Facilities Can Be Operated Under This Fringe Benefit?

Under this benefit, you can deduct and provide on a tax-free basis the following types of items:

• Gyms

• Exercise equipment

• Tennis courts

• Swimming pools

• Golf courses

Author’s note: I really like the idea of being able to provide a golf course to my employees tax-free; however, the cost would be prohibitive to small businesses. However, remember what I stated earlier: “Where there’s a will, there’s a lawyer.” Check out the next exception.

In case you don’t have the hundreds of thousands or, in the case of golf courses, millions necessary to provide this benefit to your employees, there’s a great exception from having your company pay all the costs.44 A company can have an agreement with other employers to operate the gym, golf course, or swimming pool. Thus, you find a company currently providing this benefit to its employees and cut a deal to pay rent or a fee so that your employees can use this facility. I should note that you must cut a deal with another company that provides this benefit solely to its employees. You can’t go to a general health club or a country club and do the same thing.

Author’s note: This is another idiotic rule passed by Congress. I can pay IBM to let my staff use a golf course that it owns and operates, along with employees of other companies that pay IBM for use of this course, but we can’t pay a health club or a country club to do the same thing. Am I missing the point, or is this dumb?

Sandy’s tax tip: Normally, self-employed individuals (otherwise known as sole proprietors) can’t set up a deductible gym for themselves. However, if you were to hire your spouse and provide the gym in the location where your spouse works, such as your home, the gym should be deductible if used by you and your dependent children as well. This option, however, has not been tested yet.

The Bottom Line

This is a terrific and often overlooked benefit. Just have your company either operate the athletic facility or pay rent to another company that’s operating a facility for its own employees.

Retirement Advice

Congress has been concerned recently with the lack of retirement planning of most people. In fact, according to a Harvard University study, only 2 percent of the population can retire by age 65 on the same standard of living that they had before retirement. Thus, starting in 2002, companies now can provide qualified retirement services to their employees and their spouses.45 However, the employer must have some kind of “qualified plan” in place, such as a pension, a profit-sharing plan, a simplified employee pension (SEP), or even a simple individual retirement account (IRA) (most of these plans will be discussed later in this chapter) so that the employees can see where this benefit fits in with all the other retirement planning.

Example: Stop the Clock, Inc., wants to provide retirement planning for its employees. It hires a financial planner to meet with each employee about his or her retirement and to set up individual retirement plans for each employee and his or her spouse. If the company pays a fee for these services, it can deduct the fee, and the benefit would be tax-free to each employee if there were no discrimination.

In addition, anyone, even highly compensated employees and officers, can have this tax-free benefit as long as it doesn’t discriminate.46 Thus provide it to all full-time people.

The Bottom Line

This is both a great benefit and a needed benefit. You’ll have happy and economically healthier employees by providing this benefit. Remember, however, that this benefit must be nondiscriminatory.

Company-Provided Low- or No-Interest Loans to Employees

This has got to be one of the most used and yet misunderstood fringe benefits. Unfortunately, few companies are using this benefit correctly. However, you, my faithful reader, will not have this problem because you will learn exactly what you need to do to make these loans tax-free.

The rules provided by Congress are entitled, “Treatment of Loans with Below-Market Interest Rates.” These are defined as loans made to employees or even independent contractors at rates that are below the minimum rates allowed by the IRS, which are also known as the applicable federal rates. Thus, if you want to make the interest rates on these loans tax-free, there’s a minimum rate that you must charge, or the employee is taxed on the foregone interest that he or she should have paid at the applicable federal rates.47

Example: Alice borrows $50,000 from her corporation for a 10-year period, interest-free. Because she didn’t pay interest equal to the applicable federal rate, she would be taxed on the foregone interest using this rate each year. Yuck!

Applicable Federal Rates

The IRS publishes the applicable federal rates each month. They’re available in your accountant’s office, or you can call the IRS at 800-IRS-1040. (Isn’t that a cute number?) There are three federal rates:

• Short-term rates—for loans of three years or less

• Middle-term rates—for loans over three years but not over nine years

• Long-term rates—for loans over nine years

Author’s note: You would determine how long you want the loan and find out the latest applicable federal rate for the duration of the loan that you want. As long as you charge at least that rate, you can get these below-market loans tax-free. Also, as an estimate for you, the rate for long-term loans (over nine years) approximates the prime rate, whereas the rate for short-term loans is approximately one-half the prime rate. Thus the longer the duration, the more you must charge in interest.

Fabulous Exceptions to the Below-Market Loan Rules

1. $10,000 de minimis exception. The below-market loan rules do not apply to loans of $10,000 or less, which means that you can charge no or little interest.48 However, if the amount is above $10,000, the rules apply even if you pay down the debt below $10,000.49

Example: You borrow $10,000 from your corporation, interest-free. This would be an exception to the rules, and you would not pay any tax on the foregone interest.

Example: You borrow $15,000 from your corporation, interest-free. This would not be an exception even if you pay the loan down below $10,000. You’re taxed on each year’s foregone interest.

2. Employee-relocation mortgage loans made in connection with a new place of work. One fabulous exception would be to provide mortgage loans to employees as part of a transfer to a new location.50 Your new job location has to change, so you would qualify for the moving deduction. Generally, this means that your new job location should be on the other side of the city at least 50 miles away or, even better, in another city or another state. If you qualify, you can charge little or no interest.

The new workplace would have to be at such a distance from the employee’s old residence as to require at least an additional 50 miles of commute. In other words, if the distance between the new site and the old residence is at least 50 miles greater than the distance between the old site and the old residence, the distance requirement is fulfilled.

Author’s note: Hooray! Remember that I told you that we have good tax laws. You just have to know about them.

Requirements to Bulletproof Relocation Loans from the IRS

Nothing comes for free. To qualify, you must meet the following five easy tests:51

• The loan can’t be for the purpose of avoiding taxes. This isn’t usually a problem unless, for example, only the owner of the company gets it, and it isn’t provided to other relocating employees.

• The benefits of this loan aren’t transferable to a new buyer.

• The benefits of this loan are conditioned on continued future performance of substantial services by the employee. Thus the loan agreement could provide that “if the employee ceases working for the company, the applicable federal rate of interest will be charged the employee” or that “the loan will terminate and must be paid off within six months of termination.”

• The employee must give a statement that the employee would itemize deductions on his or her tax return for each outstanding year. In other words, the employee would certify that he or she would be able to take a deduction for the interest on his or her federal tax return.

• The loan agreement provides that the mortgage money can be used only to buy a personal residence and not an investment property.52 In short, you have to use the residence as your home and not rent it out.

Example: Karen works for the I’ve Been Moved Company (IBM). She is relocated from New York to California, and the company provides a no-interest mortgage for 15 years. As long as she uses the mortgage to buy a principal residence, is required to work for the company in order to keep receiving this benefit, and certifies that she will file an itemized return (Schedule A) with her federal tax return, the foregone interest would be tax-free.

Author’s note: Any company of any size can offer this benefit to any employee of the company. Self-employed individuals are not employees, nor are independent contractors. This benefit is also very good for motivating and retaining an employee. What employees would want to leave a job if they were getting a tax-free mortgage that they would have to refinance at the going market interest rate if they quit?

I should note that this benefit is also available to corporate officers and to corporate owners as long as they are employees of the company.

3. Bridge loans. If you don’t want to tie up your company’s money in a mortgage, you can provide a no-interest or low-interest bridge loan to hold an employee until he or she is able to get a permanent mortgage on the real estate. To make this benefit tax-free, you must meet not only all the criteria for mortgage loans but also the following three criteria:53

• The loan agreement with the employee must provide that the employee must pay off the loan in full within 15 days of selling his or her principal residence.

• The total amount of all bridge loans must be less than the equity of the old house sold.

• The old house must be sold and not converted into investment property.

Author’s note: As you can see, making a tax-free temporary loan (bridge loan) is more complicated than simply providing a mortgage. However, you may not want to tie up company funds in a long-term interest-free or low-interest commitment. Bridge loans are ideal in that they are short-term, temporary loans provided until the employee sells the former residence and has the funding to buy a new home. A corporation may provide bridge loans to the owners/stockholders. A sole proprietorship may provide them to employees—but not to the owner!

The Bottom Line

In order to provide tax-free below-market loans, either you must charge what the applicable federal rate would be for your loan’s duration (which can be obtained from the IRS or your accountant) or you must meet one of the exceptions—loans of less than $10,000, relocation mortgage loans, or bridge loans. Make sure that you meet all the criteria noted in this book, and you will bulletproof this nice tax-free fringe benefit from the IRS. It also will provide for much more loyal employees because if they leave, this benefit can terminate.

Employer Educational Assistance and Other Tuition Plans

One big question that I get from most small-business owners is, “Can I provide my employees or my employed children with a tax-free tuition payment each year?”

There’s good news and bad news here. The good news is that there are several possible ways to provide for tax-free tuition money: an educational assistance plan or tax-free use of property, equipment, or services, otherwise known as a working-condition fringe benefit. We’ll discuss each of these in the order presented. The bad news is that for small businesses, most of these plans won’t benefit the owner significantly but will benefit most of the employees of the business.

Generally, any educational expense paid for an employee or for a member of an employee’s family is deductible by the company but taxable to the employee, unless you meet one of the exceptions noted below!

Educational Assistance Programs

You can set up an educational assistance program for your employees and pay up to $5,250 per year for tuition, fees, books, and supplies.54 However, you cannot provide meals, lodging, transportation, or payments for sports, games, or hobbies unless they are part of a degree program.

Example: Jim is studying computers and takes some gym courses to keep in shape. His employer may not reimburse him for the gym courses. However, if Jim were studying exercise physiology and the gym courses were part of the curriculum, his employer could make such payments tax-free.

No discrimination is allowed in favor of business owners or highly compensated employees; however, employees of sole proprietorships can use this benefit. Now, for the bad news: No more than 5 percent of the total benefits can be paid to a stockholder who owns more than 5 percent of the stock or to an individual who owns 5 percent or more of the business even if you don’t discriminate in any way. Yuck!

Author’s note: If you have very few employees using this plan, you won’t meet this requirement because more than 5 percent of the benefits will be benefiting the owner. Thus small-business owners get shafted because they can’t avoid this 5 percent coverage, but larger businesses won’t have a problem. You can, however, provide this assistance to your employees who do not have a 5 percent or more stock or business ownership interest.

Working-Condition Fringe Benefit

Although this was covered earlier, some special rules are applicable here. Even if you don’t qualify for tax-free treatment as an educational assistance program, you may be able to deduct the courses and provide tax-free assistance as a working-condition fringe benefit if you meet certain criteria:55

• The educational expense would have been deductible by the employee if paid by the employee. This means that it doesn’t qualify the employee for a new trade or business. (See author’s note below for further explanation.)

• The courses taken are related to the duties performed by the employee on the job.56

• The employee submits receipts and an expense report for all educational reimbursements.57

Author’s note: There’s only one unclear issue here: When can an employee deduct the educational expenses? The answer is that the course must be to maintain or improve the skills needed by the employee for his or her current duties and cannot be part of a program of study to qualify the employee for a new trade or business. Thus college courses that lead to a basic college undergraduate degree would qualify for a new trade or business, as would law school and medical school courses. However, courses that would not qualify for a new trade or business, such as many postgraduate courses, would qualify as a working-condition fringe benefit. Let’s take some examples to illustrate all this.

Example: Chan works for Hackers, Inc., a computer repair facility. He’s studying computers at the local college. If the company pays for his tuition, without it qualifying as an education assistance program, it would be fully taxable to Chan because he’s seeking an undergraduate degree, which is deemed to qualify most people for a new trade or business.

Example: Let’s assume that Chan already has an undergraduate degree and is seeking a master’s in computers. Now, Hackers, Inc., can pay for any computer courses because these courses would be related to his job duties and would not qualify him for a new trade or business.

Example: Marcia works for an accounting firm by day and goes to law school and takes some tax courses in the evening. If her firm reimbursed her for these courses, none of the reimbursement would qualify as a working-condition fringe benefit because Marcia cannot deduct law school courses that lead to a doctor of law degree. If she already had a law degree, however, and took some graduate law courses in taxation, she could receive reimbursement tax-free.

The Bottom Line

An educational assistance program is great, but you can’t discriminate and can’t have over 5 percent of the benefits go to the business owners or stockholders who own more than 5 percent of the stock. You also have a “fallback” position as a working-condition fringe benefit if the course is related to the employee’s duties and the course doesn’t qualify the employee for a new trade or business. Basic undergraduate courses, basic law courses that lead to the practice of law, and medical school courses that qualify a person to practice medicine would not qualify as a working-condition fringe benefit.

Reimbursed Country Club and Health Club Dues

Before 1987, country club dues were deductible to the extent used for business. Sadly, Congress did some “tax simplification”; thus, you know that you were shafted.

Today, there’s generally no deduction for you or your company for country club or health club dues.58 However, if an employee uses the club for business, any payments made for club dues would be deemed tax-free to the employee to the extent that the club is used for business under the working-condition fringe benefit rule, as discussed earlier.59

Author’s note: Thus, if the club were used in part for business, some of the club dues would be tax-free to the employee using the club. The dues, however, would not be deductible by the company as a result of the “tax simplification” law.

Example: The Getwithit Corporation pays $2,000 a year to a health and golf club for use by its marketing employee. If the employee uses the club 40 percent for business, 40 percent of the $2,000, or $800, would be tax-free to the employee, who would be taxed on the remaining $1,200.60 The employer would get no deduction for the dues.

However, if the company treated the club dues as fully taxable compensation, it could deduct the entire amount as compensation and not club dues, but the employee would be taxed on the full amount.61

Example: If, in the preceding example, Getwithit treated the $2,000 as additional compensation, it could deduct the entire amount as compensation, and the employee would get taxed on the full amount, even the portion that he or she used for business. So much for tax simplification!

Thus the bottom line is that either the employer gets a deduction and the employee gets taxed on all the dues, or the employer gets no deduction for the dues and the employee pays taxes on some of the dues.62

Sandy’s tax tip: The key is to have your company reimburse employees only for the business use of the club. Thus only the business portion would be disallowed as a deduction by the corporation, but the employee gets that portion tax-free. The corporation should treat the portion that’s not used for business as “additional compensation” to the employee in order to take a deduction for this portion.

Author’s note: An employee would establish business use by keeping some form of tax diary or tax organizer showing what business was discussed each day that he or she used the club for business and the name of the person with whom it was discussed. One final point: The disallowance of the club dues deduction by Congress does not apply to other types of expenses. Thus business meals at your club would be deductible.63 The same reasoning would apply to golf caddie fees, green fees, tips, etc.

The bottom line is that health club, golf club, and country club dues are not deductible by a company unless it treats them as additional compensation to the employees who use the club. The company can forego the deduction so that the employee could receive some of the benefits tax-free, but only to the extent that he or she used the club for business.

Company-Provided Trips for Employees and Spouses

Many companies provide their top salespeople with conventions in very desirable places as both a morale booster and, frankly, a reward for good performance.

Author’s note: Unfortunately, as a speaker, I always seem to go to Arizona in the summer and Michigan in the winter. I’m definitely doing something wrong!

We discussed in great depth in Chapter 3 the rules for employees to deduct business trips. Generally, for a trip to be tax-free, the majority of the days must be for business. Training activities must predominate each day, other than weekend days that are sandwiched between business days. In addition, each day would be a business day if the employee attended at least four hours and one second of meetings or it were either a travel day or a sandwiched weekend day. See Chapter 3 for a more detailed analysis of this.

The key question that often arises is what happens if the spouse comes along? Congress actually has thought of this and provides that you can bring your spouse and either get a tax-free reimbursement or deduct the cost if you are not reimbursed—if you meet one of two tests:

• Your spouse is licensed in your business. (If you are an insurance agent, for example, your spouse would have to be licensed in insurance.)

• Your spouse can make money for you or the company at the convention! (You’ve got to like this one!) But what does this mean?

Requirements to Bulletproof Tax-Free Reimbursements for Your Spouse’s Travel from the IRS

The IRS provides that if your spouse is not licensed in your occupation, the company may pay his or her travel and lodging expenses under all the following conditions:

• The spouse is there for a bona fide business reason and not just to keep you company.

• There is proper substantiation for the expenses that the spouse incurs, by keeping some form of expense log, tax diary, or tax organizer.64

• The spouse is an employee of the taxpayer.65

Author’s note: The last requirement is waived if the spouse performs convention duties, such as registering guests and monitoring attendance at the meetings, etc.66

Example: Richard takes his wife to the company convention in Orlando. Her only duties are to accompany Richard and attend some seminars for spouses. The company could either deduct none of her expenses or deduct her expenses and treat them as taxable compensation for Richard.

Example: If, in the preceding example, Richard’s wife also were an employee of the company, she could attend the convention and not be taxed on the reimbursed expenses if she either attends courses related to her duties or performs functions at the convention, such as registering guests.

Author’s note: Self-employed taxpayers have the same rules for deductibility of their spouses’ expenses on business trips.

The Bottom Line

The predominant reason for the trip must be business or training. Each day should consist of at least four hours and one second of training. For a spouse’s expenses to be deductible and tax-free to the spouse or the employee, there must be a valid reason for the spouse to be there, such as convention duties, or the spouse must work for the company and attend meetings related to his or her own job duties.

Corporate Purchase of an Employee’s Home That Has Declined in Value

I’m not sure that this is as much a fringe benefit as a tax loophole. But I should tell you about it.

If an employee sells a home to his or her corporate employer, it would be considered a sale as if the employee sold it to a stranger.67 Thus there’s little benefit to selling your principal residence to your corporation if it has appreciated in value.

However, if the home has declined in value, there’s a possible benefit to the employee. If any employee, even an employee who owns 100 percent of the stock, sells his or her principal residence to the corporation at a loss, none of the loss would be deductible.68

Author’s note: I find it interesting that if you have a gain on your home, you are taxed on the gain, but if you have a loss, the government wants no part of your loss! This is another example of the “golden rule”: “He who has the gold makes the rule.”

Even worse, if there are sales expenses such as commissions, appraisal fees, bank fees, etc., the employee gets no benefit from these fees. It just accentuates the loss! Even worse, if your company reimburses an employee for the loss, the employee gets taxed on the reimbursement.69 Yuck!

Sandy’s tax tip: If an employee would have a loss on his or her residence, have the corporation purchase the house at the appraised fair market value, and then resell the house and pay all the selling expenses, although the employee would not be able to deduct the loss and also would not pay any tax because a loss would have resulted,70 he or she won’t incur additional nondeductible closing costs such as commissions. However, when the corporation incurs these expenses, it can deduct them as part of the resale of the house. Thus, in effect, the corporation is able to deduct the closing costs!

Example: Martha purchased a home for $300,000 several years ago. As a result of a bad real estate market, her home is now worth $250,000. If she sells it for the fair market value of $250,000, she cannot deduct the $50,000 loss (except to the extent that she may have claimed an office in the home). Even worse, if she were to incur $15,000 in real estate commissions and $5,000 in other closing costs, she couldn’t deduct these either.

Example: Assume that Martha’s company purchases the house from her for the fair market value of $250,000 and then resells the house for the same amount and, in addition, incurs the $20,000 of closing costs that Martha would have incurred. The corporation could deduct the $20,000 of costs as a loss. Everyone wins except the IRS.

Author’s note: This will work for any corporation, whether a regular corporation or an S corporation. It also should work if you’re running your business as a partnership or a multiple-owner limited-liability corporation. It will even work for a sole proprietorship, but only for the employees of the proprietorship, not the owner.

The Bottom Line

If you’re incorporated or an employee in any business entity and you own a principal residence that has declined in value, let the corporation purchase the home at the fair market value and resell the home. The company then can deduct the closing costs incurred as a loss.

Reimbursement for Relocating Expenses for a Qualified Move

A company can reimburse tax-free the cost of relocating employees who would have qualified for the moving-expense deduction.71 This means that if an employee makes a qualified move, the corporation can reimburse for the cost of the following:

• Transporting all household goods and furnishings

• Lodging for all family members incurred during the move

• The cost of transporting the family members to the new location

Author’s note: The employee must give the company an itemized record, including receipts for all expenses incurred, or he or she will be taxed on the reimbursement. If this is your corporation, you may use this fringe benefit as if you were an employee.

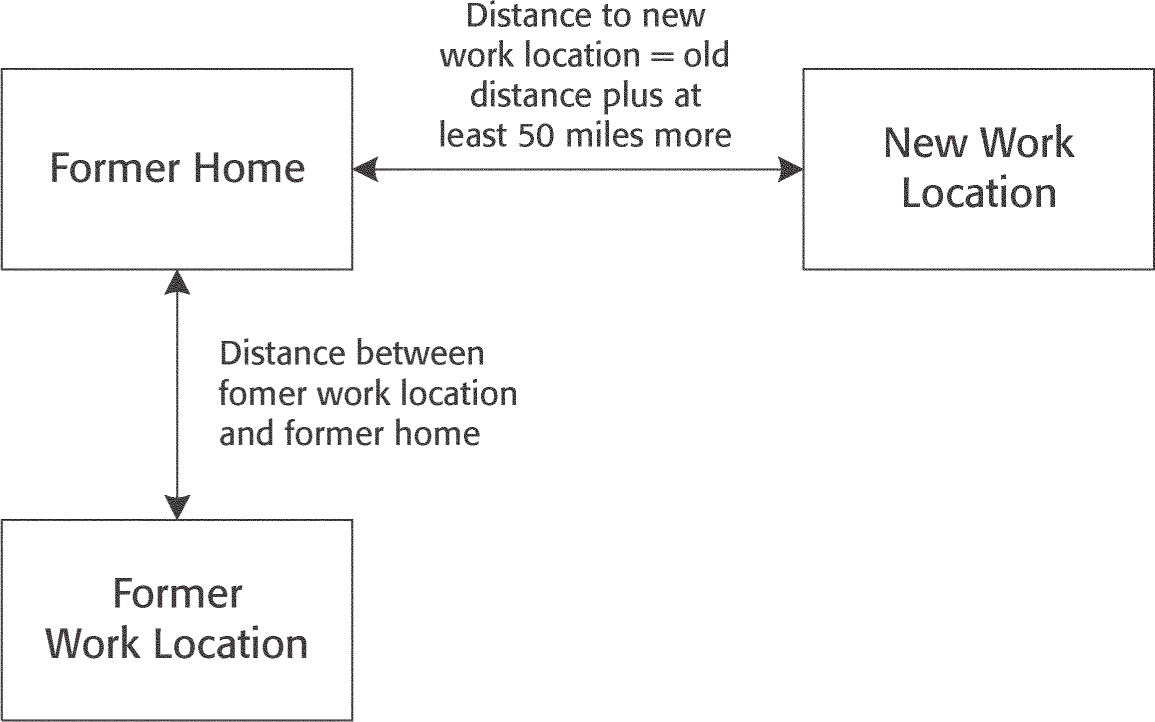

What Is a Qualified Move?

The IRS defines a qualified move this way (Publication 521): “Your move will meet the distance test if your new main job location is at least 50 miles farther from your former home than your old main job location was from your former home.” It adds the following explanation: “The distance between a job location and your home is the shortest of the more commonly traveled routes between them. The distance test considers only the location of your former home. It does not take into account the location of your new home.”

Author’s note: Don’t blame me if this sounds confusing. Blame your members of Congress. It’s hard to believe that someone actually thinks of stuff like this.

In order to help you, I have illustrated this rule in Figure 13-1.

Figure 13-1. Distance test to deduct relocation expenses.

Example: Jan lives 20 miles away from her current office. She’s transferred to a job location that’s 60 miles away. If she moves, she does not qualify to deduct her relocation expenses because the distance between her old home and her new office isn’t at least 50 miles more than her previous commute.

Discrimination Is Okay

As far as I can tell, you can discriminate in determining who gets relocation expenses covered and who doesn’t. If your corporation reimburses you and your family for your moving expenses, this would be acceptable. I would, however, establish a class of people who would qualify, such as only officers or only senior officers. This would make it less likely that the IRS would challenge the reimbursement of relocation expenses as being only for the benefit of stockholders.

The Bottom Line

If you’re incorporated, have your corporation reimburse you and any employees for qualified moving expenses—people, possessions, and lodging. Self-employed people can deduct qualified moving expenses for themselves and their employees as well.

Company-Provided Transportation, Limos, and Chauffeurs

Generally, if your corporation provides you with free transportation to the job by taxi or limo, it’s taxable. However, there’s an exception that applies in some rare instances. This transportation can be provided at a phenomenally low cost to the employee of $1.50 each way,72 regardless of cost, if you meet the following criteria:

• The transportation is provided because of unsafe conditions.

• There’s a written policy that transportation is provided only for commuting and not for personal purposes.

• An unrelated third party provides the transportation. (Thus you shouldn’t use your son or the owner’s brother to drive the employees.)

• The person transported must be a qualified employee. (Here’s the catch.)

Let’s examine what all this means. Unsafe conditions means that “under the facts and circumstances, a reasonable person would consider it unsafe for the employee to walk or use public transportation at the time of the day the employee must commute.”73 Thus the employee would ordinarily have to have either walked to work or taken public transportation. If he or she had driven, this exception presumably wouldn’t apply unless you could show that there was no safe parking near the job location or that walking to or from the parking lot would have been dangerous.

Author’s note: If you’re going to use this exception, you want to think like a prosecuting attorney. You want to show the history of crime in the area surrounding the employee’s workplace or residence at the time of the day of the commute. Perhaps getting a police recommendation to take a cab to and from work because of the unsafe conditions would be very compelling to the IRS. After all, an IRS agent is a sort of police officer, so he or she should respect a police recommendation.

You can provide this benefit only to qualified employees. These are people who are not highly compensated and are not exempt from the Fair Labor Standards Act.74 This simply means that if they put in overtime, they will be paid at least time-and-a-half.

Example: Perry Mason is a staff lawyer who works long hours for his firm. Even if Perry’s commute, which ordinarily would have been by train, could be proven dangerous, he wouldn’t normally be a qualified employee because most lawyers are not paid overtime. If he were paid overtime at overtime rates for work beyond the 40 hours, he would qualify.

Finally, self-employed people cannot qualify for this benefit unless they’re incorporated. Bah, humbug! They can, however, provide this benefit for their employees.

Author’s note: Company-provided taxis and chauffeurs may become fully deductible as a working-condition fringe benefit if these services are provided for deductible stops. For example, if you are meeting various clients, a taxi or chauffeur may be provided to drive you to each business stop.

The Bottom Line

Although this fringe benefit is interesting, it has a very limited use, and corporate owners and officers will not be able to use it unless they’re not highly compensated. Moreover, any employee who wants to use this benefit must be subject to the Fair Labor Standards Act and be paid for overtime. Thus it would be available to traditional employees. The next fringe benefit, in Chapter 14, has some similarities but will be more widely useful.

Notes

1. Section 132(d) of the IRC.

2. Letter Ruling 199929043.

3. Section 1.131-5q of the ITR.

4. Letter Ruling 199929043 and Section 1.132-1(b) of the ITR.

5. Letter Ruling 199929043.

6. Section 1.132-5n of the ITR.

7. Ibid.

8. Section 132(d)(1) of the IRC.

9. Section 132(j)(1) of the IRC.

10. Section 129(a)(1) of the IRC.

11. Sections 129(a)(2) and 129(b)(1) of the IRC.

12. Sections 129 (e)(3) and 129(e)(4) of the IRC.

13. Section 129(a)(2) of the IRC.

14. Section 129(c) of the IRC.

15. Section 137(b)(1) of the IRC. See also American Taxpayer Relief Law.

16. Section 137(a) of the IRC. See also Rev. Proc. 2011-52.

17. Sections 137(b) and 137(c) of the IRC. See also Rev. Proc. 2013-15 IRB 444 and American Taxpayer Relief Law. See also Rev. Proc. 2013-15, IRB 444.

18. Section 212 and 213 of the IRC.

19. Section 106(a) of the IRC. In 2002, the deduction for self-employed businesses and for partnerships was 70 percent of the premium.

20. Section 1.105-5(a) of the ITR.

21. Section 7702B(a)(1) of the IRC.

22. Revenue Ruling 67-360, 1967-2 CB 71.

23. Letter Rulings 9603011 and 9850011.

24. Revenue Ruling 61-146, 1961-2 CB 25.

25. Section 9802 of the IRS.

26. Seidel v. Commissioner, T.C. Memo 1971-238.

27. Sections 105(a) and 105(c) of the IRC.

28. Section 105 of the IRC.

29. Sections 105(a) of the IRC and 1.104-1(a) of the ITR.

30. Letter Rulings 8027088 and 9741035.

31. Sections 105(g), 105(b), and 137(a) of the IRC and Letter Ruling 9320004.

32. Section 1.132-6(f) of the ITR.

33. Section 132(e)(1) of the IRC.

34. Section 1.132-6(e) of the ITR.

35. Section 1.132-6(d)(1) of the ITR.

36. Section 1.132-6(d)(2) of the ITR.

37. Section 132(a)(2) of the IRC.

38. Sections 132(K) and 132(c)(1)(B) of the IRC.

39. Section 1.132-3(e) of the ITR.

40. Sections 132(c)(1) and 132(k) of the IRC.

41. Section 1.132-8T(b)(3) of the ITR.

42. Section 132(j)(4)(B) of the IRC.

43. Section 1.132-1(3) of the ITR.

44. Section 1.132-1(e)(4) of the ITR and Letter Ruling 9029026.

45. Section 132(a)(7) of the IRC.

46. Section 132(m)(2) of the IRC.

47. Section 7872(a)(1) of the IRC.

48. Section 7872(c)(3)(A) of the IRC.

49. Section 7872(f)(10) of the IRC.

50. Sections 1.7872-5T(a) and 1.7872-5T(b) of the ITR.

51. Ibid.

52. Section 1.7872-5T(c)(1)(i) of the ITR.

53. Section 1.7872-5T(c)(1) of the ITR.

54. Sections 127(a)(1) and 127(c) of the IRC.

55. Section 1.132-1(f) of the ITR.

56. Section 1.132-5(d)(2) of the ITR.

57. IRS Publication 508 (2000), p. 6.

58. Section 274(a)(3) of the IRC.

59. Section 1.132-5(s)(1) of the ITR.

60. Sections 1.132-5(s)(1) and 1.132-5(s)(3), ex 1 of the ITR.

61. Ibid.

62. Section 1.132-5(s)(3) of the ITR.

63. Revenue Ruling 63-144, Q&A 48, 1963-2 CB 129.

64. Section 1.132-5(t)(1) of the ITR.

65. Section 274(m)(3) of the IRC.

66. Payments for the spouse’s expenses would be tax-free as a working-condition fringe benefit. See also Section 1.132-5T(1) of the ITR.

67. Harris Bradley v. Commissioner, 324 F. 2d 610 (4th Cir. 1963).

68. Section 1.165-9(a) of the ITR.

69. See footnote 67 and Letter Ruling 9626026.

70. Thomas L. Karston, T.C. Memo 1975-2000.

71. Sections 132(a) and 217 of the IRC.

72. Section 1.61-21(k) of the ITR.

73. Section 1.61-21(k)(5) of the ITR.

74. Section 1.61-21(k)(6) of the ITR.