Make Your Credit Cards Work for You Instead of You for Them

Gregory Karp

Credit Cards: Play the Game Right

Credit card companies are masters at separating you from your money. But you have power too. For example, did you know credit card companies will take a little less money from you—and all you have to do is ask? You just have to know how to play the game.

A secret of the credit card industry is this: If you’ve been a long-time customer and have paid on time, a card issuer will bend over backward to keep you—even if it makes less money. That’s because it’s cheaper for card issuers to cut you a break than lose your business and have to find a new customer, which involves marketing and other expenses.

Periodically, you want to call your card company and ask for three things: a lower interest rate, a higher limit, and waived fees. You can save literally thousands of dollars.

So you don’t get tripped up in trying to land a great deal, use the following script when calling your credit card company—and do it today. The script is adapted from a variety of sources, including a free e-book Credit Card Insider Tips by Cindy Morus.

Call the phone number on the back of the credit card and prepare yourself to be polite but aggressive during the conversation. Remember, you won’t be hurting anybody’s feelings by making these requests. And each time you call back, you’re likely to get a different operator who might give you a better deal.

Here are the three requests you should make:

• Lower my interest rate. The less interest you pay, the more you can put toward eliminating the debt completely. A script might go like this:

You: “Hi, can you tell me what my current interest rate is?”

Operator: “Your current interest rate is X percent.”

You: “Hmmm. I would like you to lower my interest rate now, please.” Don’t say another word. The ball is in their court, and they’ll fill the silence with an offer.

Operator: “Okay, I can lower it to X percent.”

You: “That’s not enough, but I will take that for now. Thank you for your help. I’d like to tell your supervisor how helpful you’ve been. Could you pass me over?”

Supervisor: “How can I help you?”

You: “First, I wanted to let you know how helpful the operator was. She/he did an excellent job of helping me. Now, can you tell me what my interest rate is?”

Repeat the script above. Call back in a month or two and do it all again. Don’t worry about nagging them. It won’t hurt your relationship with a giant card company, and you might luck into a new deal it is offering. The point of asking for a supervisor is that he or she may be authorized to do more for you than the operator is.

• Raise my credit limit. This one is a little trickier and seems counterintuitive. You might wonder why you’d want more credit available if you’re trying to get out of debt. The reason is your credit score, which is partly calculated on how much debt you have compared with your available credit. So, even if your credit card balance is always $1,000, it’s better to have a limit of $5,000 than $2,000 because you’re using less of your total available credit. That can help your credit score, which can, in turn, help you qualify for lower interest rates on a mortgage or car loan, and even lower insurance rates.

• Cancel my card fees. With competition among cards so fierce, there’s often no reason to pay an annual fee. Ask the operator to waive the fee. When you get that, ask the operator to waive the current year’s fee that you already paid. If just one card company eliminates its $50 fee for the current year and next year, that’s $100 you made in about two minutes.

Of course, these scripts won’t work all the time, and conversations are likely to deviate from the scripts. Just roll with it.

Credit Cards II: Advanced Tactics

Credit cards are clearly a vice for many Americans. They’re an easy way to overspend and buy stuff you can’t afford. Even people who don’t carry a balance are likely to spend more using a credit card than cash, studies show.

But for all their ills, credit cards can have advantages for some consumers, namely people who can control their spending. Realizing there are many ways credit cards can hurt your finances, here are some of the ways they could help:

• Built-in benefits. The first benefit of using a credit card and paying off the balance is improving your credit score, or FICO score, which allows you to spend less on interest for other borrowing, such as house and car loans, and even insurance. Other benefits of using a credit card are lesser known. They might include a host of insurances, including car rental insurance, travel cancellation insurance, travel accident insurance, airline luggage insurance, and hotel burglary insurance. You’re likely to get favorable foreign exchange rates for using a credit card overseas. For purchases, some cards will replace or repair merchandise you buy with the card if the item is defective, stolen, or destroyed. Others will automatically extend the manufacturer’s warranty. Other cards offer such perks as concierge services, upgraded hotel rooms, peak-demand restaurant reservations, or free valet parking. And you are not liable if the card is stolen and fraudulently used.

But to use the benefits of your card, you’ll have to take the time to learn about them. Go online to the credit card Web site or call the number on the card to inquire about the card’s benefits.

• Rewards. Getting something for nothing is the ultimate in smart spending. And that more or less describes rewards credit cards. You can reap a host of freebies, from cash and merchandise to gasoline and airline miles. A rewards card credits you with points for every dollar you spend on your credit card. Then you redeem your points for cash or free stuff. The danger comes if you use the rewards card to spend more money than you would otherwise. And for those who carry credit card balances, rewards could be dwarfed by the extra interest you would pay with a high-rate rewards card. In choosing a rewards card, find out how quickly you can accumulate points and ask yourself whether you really want the stuff you get with points. In general, give preference to cash rewards cards, which are simpler and often more lucrative than earning points to spend on merchandise or airline tickets.

• Risky tactics. With all the competition among cards, some people are tempted to play the system using dangerous tactics. One is “surfing” balances from one 0-percent introductory offer to another. Continually transferring your debt can reduce the amount of interest you pay, but it takes diligence. The danger of surfing arises when you make a late payment or let the introductory period expire without surfing to another card. In both cases, the card company will raise the interest rate, maybe to more than 20 percent. The same is true if you exceed the credit limit on the card. And many transfers involve a balance transfer fee that eats into your savings. If lack of discipline is the reason you’re in credit card debt in the first place, you’ll probably fail at card surfing.

Debt Reduction: Finish Paying for Your Purchases

One of the smartest ways to spend your money is to get out of debt. Whether you carry a balance on credit cards, borrowed money against your house, or financed your car, you probably have debt.

Carrying a reasonable home mortgage is acceptable, but most other debt is probably standing between you and wealth. Americans have $2.16 trillion in nonmortgage debt, according to the Federal Reserve Bank. That averages $7,250 for every person in the country, children included.

Here are ideas on getting out of debt and spending your paying-off-debt dollars wisely:

• Don’t shuffle debt. Lots of advice about debt strategies involves simply moving your debt. Examples are using debt consolidation services, wrapping debts into a refinancing of your home, or surfing your credit card balances to a lower interest-rate card. The objective is not to get the lowest interest rate on your debt. It’s to get rid of it—fast.

• Address the problem. The only reason for debt is that you bought something you didn’t pay for. Debt is only the symptom. Try to fix the root problem, whether spending or income. A temporary fix, such as consolidating credit card debt into a house refinancing, will clear your card balances. But unless you fixed the root problem, those balances will build again.

• Use windfalls. It’s easy to see how spending money on eliminating debt is smart. Say you have a typical federal tax refund of $2,700. You have a choice of paying credit card debt, saving the money, or buying a fancy television. Which would you choose? The result after one year is that $2,700 turns into $3,186 by paying off an 18 percent credit card because you’d avoid paying $486 in interest. You’d earn $81 in a 3-percent savings account. Or that $2,700 turns into about $1,350 if you bought a TV because a year later it’s worth about half what you paid. So your tax refund can earn you $486 or $81, or lose you $1,350. The choice is clear. Pay the debt.

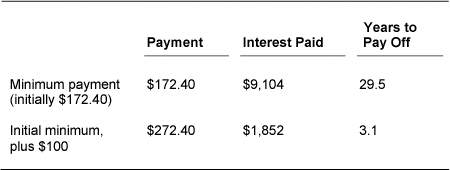

• Pay more than the minimum. Try cutting spending and putting that toward debt. Just an extra $100 a month can make a shocking difference. An $8,000 balance on a 14-percent credit card with a minimum payment of $172 would take almost 30 years to pay off, and you’ll pay $9,104 in interest, according to a calculator at Bankrate.com. If you added $100 a month to the initial minimum payment and used that amount each month, you’d pay it off in three years and pay about $1,850 in interest. See Table 1 for details. Thirty years or three years. Which would you choose?

TABLE 1 Pay the Minimum on $8,000 Credit Card at 14% Interest

• Focus efforts. Pay minimums on all your debts except the one you’ve decided to attack. So, for example, put an extra $100 per month toward your targeted debt, rather than pay an extra $20 on five different debts.

• Snowball the payments. When you complete one debt, add that entire monthly payment to the payment on your next debt and so on. Each time, you’re putting more money toward debts as you proceed through them. Debt reduction grows and accelerates like a snowball rolling downhill.

• Choose a pay-down strategy. Which nonmortgage debt should you pay off first? After paying for basic necessities and the minimums on all your consumer debts, extra money can go toward debt in three ways:

Pay the loans with the highest interest rates first. Simple math tells you this is a wise choice, and it’s the most commonly advocated method. That’s because you’ll end up paying less interest by attacking loans that cost you the most money. For example, paying off a $3,000 balance on a 14-percent credit card saves you $420 a year, while paying $3,000 toward a student loan at 4 percent saves $120.

Pay the smallest debt first. This method disregards math and goes straight to human behavior. If you pay your smallest debts first, you’ll eliminate several of them quickly and get a sense of accomplishment. It’s like losing a few pounds the first week you’re on a diet. It’s an encouragement to keep going.

Use a hybrid method. You could combine the preceding two strategies by knocking out the smallest debts first—say, all those less than $1,000—and then paying the big ones in order of interest rate, highest to lowest.

Getting out of debt is a lot like dieting. It’s difficult and takes self-discipline. By paying off small debts first, you can wipe out a number of them and feel like you’re gaining traction and succeeding. It’s the atta-boy or atta-girl to help you keep going and pay off more debt. It’s similar to losing a few pounds during the first days of a diet. It gives you encouragement to continue.