Chapter 16

Supply-Chain Integration: Putting Humpty Dumpty Back Together Again1

Tulane University

University of Texas

Design for Supply-Chain Integration

A KEY FEATURE OF THE economy for the past century has been that the wealth of technological knowledge is increasing at an exponential rate. This has led to the subdivision of technologists into ever-finer specialties creating management problems for large companies that are no longer capable of monitoring and rewarding their technologists effectively (Zenger 1994). This problem is often referred to as a “diseconomies of scale in R and D.” However, two recent trends in the past decade, the rise of information infrastructural capabilities and the breaking down of regional trade barriers, have radically reduced the costs of geographic distance on knowledge collaboration (Fine, Gilboy, and Parker 1995). Thus, we speculate that there is again a return of R and D economies of scale, albeit for groups based on more narrow specializations and greater geographical distribution than before. This leads to what we call the “Humpty Dumpty” problem. Any technical design or development work of the future is likely to incorporate many more firms than five years ago or even today. Each of these firms will have a different set of corporate cultures and beliefs. But once technical development is broken into perhaps a dozen or more pieces, how are all the king’s (or Original Equipment Manufactures) product planners going to put them back together again into a product that satisfies customer requirements? Maintaining product coherence, let alone quality, across the supply chain will become an ever more difficult and important proposition as the number of supply-chain members increases. Hence, in the future, one key to product quality will be how effectively a supply chain integrates individual firms’ development projects into a coherent whole. In this Chapter, we speculate on two themes. First, how does a firm integrate all of the pieces of a Humpty Dumpty project back into a coherent whole? Second, as a key lever to answering the first question, into exactly what sort of sizes and parts should a firm break up the Humpty Dumpty of a product development project? By examining these two questions, we hope to provide a key to successful product development in the future.

BACKGROUND AND MOTIVATION

Product Outsourcing Has Happened

As noted in the heading, outsourcing in the product domain is a well-established practice. Very few firms remain vertically integrated, and those that do are likely to be reconsidering their supply chain design in the near future.

At Japanese automobile firms, outsourcing became common during the 1970s (Clark and Fujimoto 1991; Womack, Jones, and Roos 1990). However, outsourcing did not hit most U.S. firms head-on until the beginning of the 1990s. Now, there is a tidal wave of outsourcing as firms scrutinize their operations and keep in-house only what is core. And—as we shall see in the Hewlett-Packard study—the “new” outsourcing is much more radical than the traditional Japanese keiretsu model in both its extent and continual reconfiguration. As a result, supplier firms are surfacing in all domains and industries. Sturgeon (1997) calls this new model of “brand-name” firm/contractmanufacturer firm partnership a “turnkey production network” and documents its emergence in the electronics industry. For example, it is now possible to purchase a hard drive service in which the supplier firm delivers a certain amount of storage (usually measured in terabytes) and performs maintenance and backups (Parker 1999). This relieves firms of a large asset. The hard drive service has been particularly popular with Web-based start-up firms who want to avoid large capital outlays but require a high level of service. A similar situation has evolved in the shipping industry with the emergence of third-party- and even fourth-party-logistics providers. With annual industry growth rates of 20 percent, these firms are taking control of companies’ docks, inventory control systems, and, in some cases, inventory itself (Alden 1999). A close look at any industry would likely reveal similar breakups of vertically integrated organizations and the formation of firms that provide non-core products and services (non-core to the customer firms). Our goal is to better understand how to work with these new suppliers to ensure successful integration of their activities into a coherent final product or service. We are also concerned with understanding and mitigating transaction costs as non-core activities are performed by suppliers (Williamson 1975). One key source of transaction costs, product integration, is especially important in industries with short product or process life-cycles in which suppliers are often changed, requirements are unclear, and the incentives to achieve coordination have not been specifically addressed.

In answer to these problems, the Japanese keiretsu model is illuminating but insufficient. In the paradigmatic keiretsu, the assembly firm still designs the core components that form a product’s technological center of gravity (Prahalad and Hamel 1990). However, as Parker and Anderson (2000) learned in their study of Hewlett-Packard, some of the new disaggregated firms seem to outsource everything except product integration. Thus, disaggregated firms must “design” products without having any traditional design—that is, component—capabilities to leverage. In contrast, keiretsu assembly firms typically outsource the design of non-core components only to suppliers with whom they have decades-long relationships. These conditions foster an atmosphere of well-understood mutual expectations enabling efficient and precise problem resolution (Fujimoto 1994). However, disaggregated firms do not have the luxury to spend 20 years developing good supplier relationships. One of the challenges firms face as they assemble a virtual organization is how to ensure that products are specified, designed, and built coherently, even though many individual firms may be responsible for pieces of a product, and, as we discuss in the next subsection, the design of a product.

Design Outsourcing Is Coming

We believe that design outsourcing is likely to increase, as firms again examine their corporate structures for areas in which to reduce cost. The design services business is experiencing high rates of growth as firms take advantage of design outsourcing (Wiederhold 2000). In the past, firms have retained design in-house, arguing that this was their core competence, as they outsourced production. However, firms are now asking whether all of design can possibly be a core competence, and if not, what pieces should be subcontracted to a supplier of design services, and what should be retained internally.

Given that much production is outsourced, and that design outsourcing could become a substantial trend, we now discuss some of the possible pitfalls from failing to take integration into account.

OUTSOURCING TRAPS

This section draws substantially from material first developed in Anderson and Parker (2000) and later in Anderson and Anderson (Forthcoming). As we have discussed, since the 1990s there has been a tidal wave of firms outsourcing all or part of their products and services. The two remaining domestic automakers have recently broken off their multibillion-dollar component businesses to focus on their core design and assembly operations. Many personal computer manufacturers, such as Hewlett-Packard, are farming out their notebook computer products to manufacturers in Taiwan. In the software industry, the rise of contract software designers in the “three I’s”—India, Ireland, and Israel—represents a prominent trend. Some firms—such as those who outsource their logistics decisions to fourth-party logistics providers—have even gone so far as to outsource the very decision of whether or not to outsource. Why are so many companies taking this dramatic step? The benefits of this new business model include lower parts or service costs, lower investment, and less financial risk if expected sales volumes do not materialize. But outsourcing has hidden drawbacks that may take several years to emerge. Ultimately, these “outsourcing traps” may actually increase a firm’s cost structure, reduce its products’ competitiveness, or in the worst case, lead to the emergence of new competitors.

As the vertically integrated firm of yesteryear transforms itself into the virtually integrated supply chain of today, it evolves from a firm that produces all of its final products’ subcomponents and services internally into a firm that buys all of its subcomponents and services from a network—or supply chain—of independent supplier companies. But how does it manage this transformation without falling into an outsourcing trap? Research shows that the design of a company’s supply chain is of decisive importance. Fine (1998) argues that supply chain design may be a business’ most important competency and that deciding which components to make and which to buy profoundly influences long-term corporate survival. We suggest in our research that one key to making wise sourcing decisions is to understand the short- and long-term tradeoffs that outsourcing entails.

Although the outsourcing issue has been extensively examined in the academic literature, most of this work has focused on topics such as the economies of scale available through outsourcing. We are aware of few resources that examine the outsourcing issue from a systems perspective, taking into account the intricate relationships, time delays, and feedback processes that relying on an outside vendor sets into motion. But companies that fail to apply this level of analysis to the decision-making process may encounter a series of traps that could seriously undermine their competitive position.

Common Outsourcing Traps

As part of our research, we have developed a system dynamics simulation model that has identified several circumstances in which an organization may experience short-term gains from outsourcing followed by devastating—and unexpected—long-term consequences. We call these outsourcing traps. Three of the more interesting traps are:

1.A firm loses its market dominance when its supplier acquires its propriety technology and diffuses it to its competitors.

2.A firm relies too heavily on a single supplier, which weakens its ability to negotiate favorable purchase agreements.

3.A firm outsources a component to a vendor to reduce costs only to encounter higher expenses or reduced functionality when assembling the final product.

We now examine each of these dynamics in more detail.

Making Life Easy for the Competitor (or Maybe Creating One)

One possible consequence of outsourcing is that a competitor may gain access to critical technology through a common supplier, either directly through purchasing it, or indirectly as the supplier’s engineers move to projects with other companies bringing the knowledge gained from working with the original firm. If the competitor then uses the information to duplicate or improve the original product, it may erode the first company’s market position. The classic example of this dynamic occurred when IBM was developing its new personal computers (PCs) in the early 1980s. The company made what turned out to be a fateful decision to outsource production of the PC’s microprocessor to Intel and development of its operating system to Microsoft. Little did IBM know that by doing so, it was opening the door for direct competitors such as Compaq and Dell to purchase directly the two components of the PC most difficult to duplicate (Carroll 1993). Today, IBM is only the third largest maker in an industry that it helped to create. Furthermore, the majority of profits in IBM’s PC business come not from manufacturing the “box” but rather from servicing it by providing buyers with maintenance and technical support. Hence, its ability to generate profits rests not on its capability to design and manufacture products efficiently, but rather the capability to keep these products up and running for their clients at all times. The logical progression of this trend would be for IBM to give up producing boxes, and instead provide services for those made by other firms.

Enterprise-wide integrated software packages such as SAP provide another example. While they often improve operational performance for many firms, they also remove any chance for a company to obtain a sustainable strategic advantage through advanced information systems. Furthermore, once the information systems group of a corporation is disbanded, a firm may lose its capability to create new technological advantages and become utterly dependent on the supplier for innovation.

Another twist on this situation may occur as the supplier grows more efficient at making the component and learns more about the component’s functionality. Eventually, it may become sufficiently skilled at manufacturing the entire product to become a direct competitor. U.S. consumer electronics firms followed this path in the 1960s and 1970s when they outsourced production of televisions and other electronics to Japanese suppliers (Dertouzos, Solow, and Lester 1989). Ultimately, as domestic suppliers failed to develop their own capabilities, they fell further and further behind their own vendors. The suppliers eventually began to sell products under their own names—including Sony, Panasonic, and Mitsubishi—driving U.S. manufacturers such as Zenith and General Electric out of business. Today’s U.S. electronics and software companies may be repeating the same mistakes, as they increasingly outsource design activities to international suppliers.

Held Hostage by Your Supplier

A common but subtle outsourcing trap occurs when a supplier holds a firm hostage. If a firm—or an industry—becomes too reliant on a particular vendor or set of vendors, power may shift to the supplier, allowing it to reap most of the profits. This dynamic is really just an extension of the problem illustrated earlier in the example of the IBM PC. Little did IBM know that the PC assembly industry would become primarily a commodity business as the functionality that differentiated performance migrated from the assembled circuit board into the purchased semiconductor chips and software. When IBM outsourced the bulk of the PC’s intellectual property to the software and semiconductor houses, they gave up a great deal of power in the supply chain. Intel and Microsoft could sell to any of a number of circuit board manufacturers that could readily duplicate IBM’s design, but IBM could only purchase Intel-compatible processors from Intel and Windows-compatible operating systems from Microsoft. This gave Intel and Microsoft something of a monopolist’s power and enabled them to capture the bulk of the supply chain’s profits (Carroll 1993).

IBM tried to buck this trend by developing OS/2, its own operating system, in the late 1980s. It was arguably a better operating system than Windows, however, customers wouldn’t buy OS/2 because the majority of software applications available at the time functioned only on Windows. Furthermore, because Windows had many more users than OS/2, Windows customers could much more easily trade documents or software with other users than could OS/2 customers. In the end, the OS/2 system didn’t offer enough new features to convince users to overcome these standardization benefits (Carroll 1993). Because of the difficulties in competing with Microsoft or Intel, many PC firms are instead trying to expand beyond the unprofitable PC business today by following IBM’s move into providing services to PC users, which offers more comfortable margins. Others are giving up in another way by outsourcing as much of their production as possible to Asian contract manufacturers with lower personnel costs.

Another possible adverse consequence to outsourcing is that a company may lose the ability to intelligently purchase components—and the suppliers may take advantage of this ignorance and price them at a premium. An executive at a top PC manufacturer recently stated that his firm found completely outsourcing a product to be undesirable (Anderson 2000). He said that, when the company first outsourced its computer manufacturing, it could do so efficiently. However, after three years, the technology had changed sufficiently that internal people no longer knew enough about the product to determine whether a contract bid was sufficiently competitive—especially because they suspected their vendors of engaging in price collusion and price gouging in certain areas. The suppliers had the PC company in a difficult position, because they knew that the firm could no longer make the product themselves and that they had even lost the ability to determine the cost of the products they were buying.

The danger of falling into this trap is especially acute for companies that outsource a component to one supplier for a long period of time. Lack of expertise within the original company to create the component leads to increased in-house manufacturing costs, which makes outsourcing even more attractive. This reinforcing dynamic can prove costly if the firm ever desires to make the part again, because as time passes and the knowledge of how to make the component diminishes, it can become prohibitively expensive to reverse the outsourcing decision. If the firm determines in the future that this component is vital to the performance of the product, it may need to invest to bring the knowledge back in-house. However, this penalty may be necessary to regain some bargaining leverage with suppliers.

Outsourcing’s Impact on Systems Integration

A related problem to having enough information to effectively negotiate with suppliers is the need for a firm to know enough about its components to effectively integrate them into coherent products. As stated earlier, a common reason why a firm outsources is that it can purchase a component from a supplier for much less than the firm can make it itself. In Anderson and Parker (2000), the authors develop a model of sourcing that incorporates learning effects. We draw on this source for Figures 16.1 to 16.3.

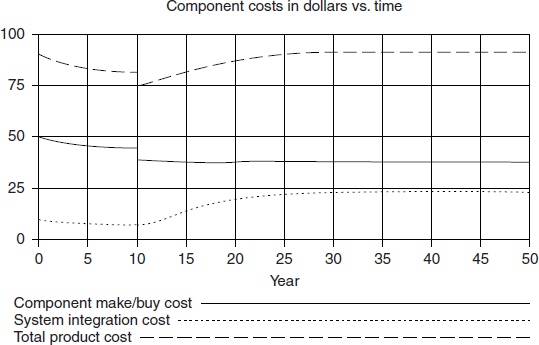

Figure 16.1 illustrates the point about the need to mind integration by showing three cost curves: integration cost, component cost, and total cost. At time t = 10, the firm changes from internal component production to 100 percent component outsourcing in order to take advantage of a supplier’s lower component cost position.

At first, total product costs are lower. In fact, component acquisition costs continue to decline in the short run because the additional manufacturing volume at the supplier will drive its production costs even lower than they were at the time of outsourcing. However, because internal component production has ceased, the OEM is no longer learning about those aspects of the component that are crucial to integrating it effectively into the product. Thus, with time, the integration knowledge stock deteriorates from obsolescence which causes the integration cost to begin to creep upward. After about five years (for these parameter values), the total product cost is equal to the cost before the decision to outsource was made. After this time, increased integration costs exceed the component cost savings, causing the total product cost to climb even more. Thus, while outsourcing provided excellent short-run returns, it proved to have long-run drawbacks. Furthermore, if the OEM decides to “re-insource” it will no longer have the in-house manufacturing experience it had at the time of the outsourcing decision, and will have to climb the learning curve yet again before returning to the lower total product costs. Hence, the OEM has been caught in the outsourcing trap of seductive low initial supplier acquisition costs, and will find a return to its prior cost levels to be quite painful.

FIGURE 16.1OEM switches from 100 percent internal component production to 100 percent purchasing of component at t = 10.

General Motors and Ford may have fallen into this trap when they decided to spin off their component divisions. The two new companies, Delphi and Visteon, are busily expanding their customer base beyond their parent corporations. As they do so, the risk of another automaker gaining access to once-proprietary technology grows. GM and Ford’s knowledge of the components may also become obsolete, leaving them helpless to make innovations in component performance and unable to effectively integrate electronic components with the rest of the system.

We suspect that this was the main reason behind Toyota’s re-insourcing of electronics components. Auto companies may be most vulnerable to potential integration cost penalties in the area of automotive electronics, which has become the decisive factor in advancing car comfort, safety, and performance. Toyota may be acting to avoid this trap by bringing its automotive electronics back in-house after 45 years, even though its supplier, Denso, is the world leader in cost and quality (Hansen Report 1994). It has made this move just as U.S. manufacturers are divesting themselves of this same capability. Without understanding electronics, we believe it will be more difficult to develop a competitive automotive product than in previous years.

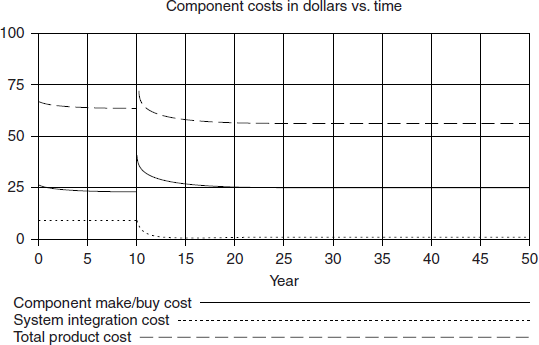

Figure 16.2 illustrates the cost hurdle that a firm must overcome if it wants to insource components after a long period of outsourcing component production.

At time t = 10, a firm that was outsourcing all component production begins to manufacture the component internally. At first, the firm’s costs increase due to higher component costs. However, for products with high integration costs (as in this example), integration costs could fall enough in the long run to offset the higher component cost.

In an example from another industry, the second largest software company in the world, SAP, a German provider of enterprise-wide integrated software packages, experienced serious implementation problems with many of its North American clients. These software packages, often known as enterprise resource planning programs (or ERPs), integrate all the information processing activities in a firm, from purchasing and manufacturing, to order fulfillment and accounting. SAP ultimately traced its difficulties to its outsourcing of implementation to third-party consultants. Because SAP didn’t participate in the implementation process directly, the company didn’t gain knowledge to feed back into product improvements. Many of these problems have lessened since SAP began to join its alliance partners in actual implementation projects.

FIGURE 16.2OEM switches from 100 percent purchasing of components to 100 percent internal component production at t = 10.

Manufacturing a component or performing a service can thus give a firm a decisive edge in knowing how to integrate it effectively into the final product. For example, many of Microsoft’s detractors claim that Microsoft uses its in-depth knowledge of the Windows operating system to give it an edge over its competitors in designing the features of its applications software. If this is true, then splitting Microsoft into an operating systems company and an applications software company may have a hidden cost to the consumer. The new applications company may become less familiar with Windows as the operating systems change with time and their former Microsoft employees turn over, leading it to design products that exploit Windows’ capabilities less effectively. In a related phenomenon, Parker and Van Alstyne (2000) have modeled the potential benefit to consumers when firms are allowed to take advantage of products that exhibit cross-market externalities by setting one price to zero.

Overcoming Outsourcing Traps

How does a firm overcome these outsourcing traps? One way is to avoid outsourcing altogether. This approach may be necessary for firms concerned about the leakage of proprietary knowledge through a supplier. If the company still wants to pursue outsourcing, it may need to have vendors sign binding nondisclosure agreements; however, even the best of these will only slow, not stop, the diffusion of knowledge. Personnel cannot be permanently kept from transferring between projects from different clients. And, even if transfers could be stopped, as long as the supplier is reaping some benefit from selling to more than one customer, there will necessarily be some information leakage between the groups supplying each customer. On the other hand, complete insourcing may not be an option. Making components in-house will avoid the supplier-hostage and systems-integration traps; however, it can also put a firm at a serious competitive disadvantage by raising the cost of acquiring components or services.

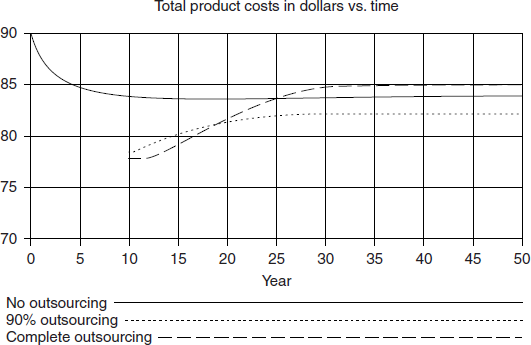

FIGURE 16.3OEM maintains 100 percent internal component production or switches to 90 percent or 100 percent purchasing of component at t = 10.

There is at least one possible way to avoid this dilemma and obtain both the low component cost of outsourcing and the low risks and integration costs of insourcing. In many instances, by making just a small percentage of the component (or one of a number of similar components) in-house, a firm can reduce the average cost to make or buy a component while maintaining adequate knowledge to keep many outsourcing risks and integration penalties under control. A similar strategy can be pursued when outsourcing services. The success of this strategy depends on a number of variables, but clearly of the utmost importance are the fixed costs associated with the component or service. If high fixed costs need to be duplicated at both the firm and its suppliers, then pursuing this partial outsourcing strategy may not be feasible. Figure 16.3 demonstrates the partial outsourcing strategy. In this figure, only total costs are plotted for three different strategies: total component outsourcing, total component insourcing, and 90 percent component outsourcing.

For these parameter values, a firm that pursues total component outsourcing gets into an outsourcing trap, as described above. However, the firm that pursues 90 percent outsourcing gains most of the benefit of lower component costs while keeping integration costs low enough to gain a total cost advantage.

This is essentially the policy we suspect that Toyota has pursued with Denso. It is probable that Toyota can never produce electronics control systems more cheaply than Denso. So it lets Denso produce most of them, thus keeping average parts costs down. However, by designing and manufacturing some electronics in-house, Toyota can gain enough knowledge to utilize the full potential inherent in electronics control systems when designing new automobiles. It also helps prevent a “Denso inside” strategy paralleling Intel’s branding of the personal computer industry. A similar strategy can be pursued when outsourcing services. Franchisors that maintain company-owned stores are classic examples of using partial outsourcing to give “a firm direct knowledge of operations issues and allows it to test and implement marketing strategies franchisees may not be able to do at their stores” (Tikoo 1996). For example, in 1988 Dunkin’ Donuts operated only two percent of its 1500 locations itself. However, it specifically used its company-operated sites to pilot all of its new distribution and marketing programs before asking franchisees to adopt them (Kauffmann 1988). Hence, partial outsourcing is a powerful tool in many economic endeavors to gain outsourcing cost benefits while maintaining insourcing’s innovation and integration benefits.

The success of the partial outsourcing strategy depends on a number of variables including economies of scale, the pace of technological change, and the modularity of components. But most important are the fixed costs associated with the component or service. If high fixed costs need to be duplicated at both the firm and its suppliers, then pursuing this partial outsourcing strategy may not be feasible. For example silicon wafer fabs, which make semiconductor chips, cost several billion dollars and are unsuitable for low-volume production. Unless a semiconductor company has a tremendous number of components, partial outsourcing in this industry is unlikely to be cost-effective. On the other hand, in the software design industry, the majority of fixed costs, such as providing high-end computers and Internet access, are accrued per programmer. Hence, maintaining a small fraction of programming activities in-house is unlikely to duplicate fixed costs at the supplier.

There are other possible solutions to the outsourcing dilemma as well. For example, a firm can lower its integration costs by hiring and training people with certain specific systems-integration skills, such as systems engineering. If employees can carefully design a product so that its component interfaces are well defined and well understood, then many thorny integration problems may be avoided. For example, products that are designed to use “snap-in” components are usually much easier to assemble into a final product than those requiring parts to be screwed into place. Hewlett-Packard has pursued this approach in tandem with increased outsourcing over the past five years. HP’s notebook division has seen a tenfold increase in its revenue and a significant improvement in profitability since it began outsourcing production of its notebook computers in 1997 (Parker and Anderson 2000). In a later section, we discuss the human resource strategy of employing supply-chain integrators whose job is to work to ensure product and service integrity.

Could the IBM PC’s Fate Have Been Avoided?

This section looked at just a few of the difficulties that can result from a decision to outsource. The outsourcing traps highlight how a seemingly simple decision to have a vendor produce a component or service can have devastating effects on a company’s future well-being. By examining the dynamics behind outsourcing, companies can identify potential traps and make better decisions about outsourcing than they might have otherwise.

By building the concept of integration into dynamic models, we can look beyond the short-term benefits achieved by outsourcing and analyze the long-term consequences, including what effects these decisions may have on future economic and market positions. We can be almost certain that IBM’s management did not envision the future that it created when it chose to farm out its microprocessor to Intel and its operating system to Microsoft. Perhaps the fate of IBM in the personal computing market and the structure of the entire industry would have been different if they could have used the tools that system dynamics and systems thinking offer.

In the next section, we consider issues of supplier relationships that affect a supplier’s willingness to invest in the firm-specific technologies necessary to pursue high-performance integrated product design strategies.

SUPPLY-CHAIN DESIGN FOR INTEGRATION-CONTRACTING ISSUES

This section draws substantially from material originally presented in Parker (1998). As firms work to design their supply chains, they must build relationships with providers of goods, technology, and skills, both within and outside company boundaries. In this work, think of a supply chain as a chain of skills or capabilities superimposed on a chain of organizations (Fine 1995, 1998). This section focuses on skill development, taking as given that the types and strengths of capabilities in the chain are key determinants of supply-chain performance.

The question for firms is how to contract for a coherent sequence of projects that satisfies the need to compete successfully in today’s marketplace and builds a set of desired capabilities to enable competition in tomorrow’s marketplace. Supplier capabilities do not remain static over time, but instead constantly evolve as unused capabilities shrink and new capabilities are created (Leonard-Barton 1992). Contracting firms must take into account that suppliers will evaluate business opportunities in part by assessing how projects will improve market opportunities outside the existing relationship. The tension is that buyer firms may prefer projects that add little value to a supplier’s outside opportunities, but create substantial value within the firm/supplier relationship. The work presented in this section attempts to establish some of the building blocks for understanding the strategic implications of projects between customers and suppliers that involve learning.

Key Factors in Building Integration-Enabling Capabilities

The negotiation between firms and suppliers over which projects to undertake and how to distribute rewards takes place in a complex setting that includes but is not limited to the following:

Firm Technology

A major factor that both parties will take into account is the type of technology employed by the firm with which the supplier (firm or individual) must integrate in order to produce the desired output. If the firm employs very specialized technologies, the supplier (if it hasn’t already) will have to acquire the ability to work with this technology. To the extent that the technology is unique, the supplier cannot use the capabilities with other firms, and suppliers will take this into account before agreeing to develop the capability. Suppliers might fear that they will be locked in to a specific technology and that once locked in, they might lose negotiating leverage with the customer firm. Conversely, a firm that pursues specialized designs with high integration requirements might fear supplier hold-up as described in the previous section.

Rate of Technological Change

The rate of technological change is a factor that affects the willingness of suppliers to adopt unique capabilities. For example, suppliers to a coal-fired electric generating plant can be confident that the capabilities they develop will likely be useful over the (thirty-to-forty-year) lifetime of the plant. However, the capabilities of suppliers to a consumer electronics firm may obsolesce in a very short time period of years to months. Planning to make capability investments in a rapidly changing environment requires the parties to make the additional calculation of how long the capability is expected to be relevant. The terminology “slow clockspeed” and “fast clockspeed” is used to describe industries that are innovating slowly versus those which are innovating rapidly (Fine 1998).

Incentives

We assume that supply-chain partners act in their own self-interest. That is, suppliers cannot be compelled to undertake projects that are not in their interest. It is assumed that suppliers always have the option to make (potentially unobserved) capability investments in more general technologies if the customer firm does not offer a sufficiently broad set of project choices. Firms must therefore offer incentives to suppliers if they wish suppliers to risk getting locked in to highly unique technologies.

Supply-Chain Design Matters: IBM Example

As noted in the previous section on outsourcing traps, IBM’s supply-chain design decision for the personal computer product line launched in the early 1980s provides an example of the importance of the supplier decisions that companies make early in product introductions. At the time, no one had a believable prediction for how large the market for personal computers was going to become. “Heavy Iron,” the large mainframe computers upon which IBM was built, remained supreme.

Supply-Chain Decision Allowed Quick Entry

IBM tasked Microsoft with the development of the operating system and assigned microprocessor production to Intel. This division of responsibility allowed IBM to gain quick access to the market. The product design and distribution activities carried out by IBM provided the most value added early in the industry life-cycle. However, as other competitors entered the market over time, product designs became standardized and additional distribution channels were developed. IBM was no longer able to earn substantial profits on the basis of these activities.

Supply-Chain Partners Appropriate the Profit

Fast forward to 2000 and the environment is far different. Both Microsoft and Intel are among the world’s most valuable companies, as measured by market capitalization. As discussed earlier, the design and sale of personal computer boxes became a commodity business, while the majority of industry profit is made further up the supply chain in microprocessors and operating systems; a recent report said that Intel and Microsoft together earn fully half of the total profits earned in the personal computer industry.

Other Firms Learned to Use Intel/Microsoft Output

Early in the personal computer industry life-cycle, there was a very limited market for Intel and Microsoft output, so IBM could appropriate industry profits. However, other firms developed the capability to manufacture PCs using Intel and Microsoft output. In this way, the capabilities developed by Intel and Microsoft became general to the industry instead of specific to IBM.

Could IBM have done anything differently when it was designing the supply system for the personal computer to capture more of the value created by the capabilities developed along the supply chain? Was there a way of thinking about the supply chain and how the locus of relative value could shift, which might have led IBM to make different decisions about control over personal computer components? Should (could) IBM have attempted to bind supply-chain members to technologies controlled by IBM as opposed to opening the architecture for component by component competition? (See Farrell, Monroe, and Saloner 1998). It is unlikely that the industry would have grown nearly so rapidly if IBM had adopted a closed architecture (as Apple did), forcing Intel and Microsoft to remain captive suppliers. So, any answers to the previous questions must take into account the desire to create a large and growing market, while at the same time attempting to earn profits from participating in this market.

Supplier Incentive Designs

Parker (1998) developed models of capability development for suppliers under different sharing regimes. The general problem being considered was how to provide incentives for suppliers to develop highly specific technologies while reducing the holdup problems discussed in Williamson (1975) and many follow-on studies.

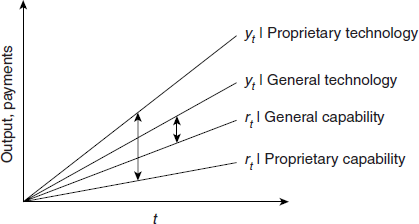

In Figure 16.4, two output (yt) curves, and two reservation payment (rt) curves are shown for two technology and capability emphases, general and proprietary. In this example, the firm’s proprietary technology joined with a supplier that has invested in it creates more output than a general technology. Conversely, when the supplier invests in general capabilities, other firms place a higher valuation on the supplier’s capabilities than if it invests in more firm-specific capabilities. This means that the distance between output and reservation wages in the proprietary case is larger than the distance between output and reservation wages in the general case. If the purchasing firm chooses to share none of this distance, then a rational supplier firm will act to raise its own reservation payments, but not to improve output and would therefore choose to invest only in general capabilities. Such capabilities would be unlikely to lead to successful joint buyer-supplier product development efforts if the design is for a highly integrated product. Parker (1998) models how much a buying firm must employ profit-sharing to induce suppliers to invest in proprietary technologies. In survey results from technical professionals, Parker finds that firms that employ highly sought-after technologies must offer substantially higher sharing contracts than those (such as space flight systems) that employ technologies of relatively little value elsewhere.

FIGURE 16.4Output and payments for two technologies.

This example leads us to consider the issue of how to train and reward people for supply-chain integration roles.

HUMAN RESOURCE ISSUES—SUPPLY-CHAIN INTEGRATORS

This section draws heavily from Parker and Anderson (2000). Our story about the new role of the supply-chain integrator is developed from four sources. (1) We drew upon a substantial set of background interviews through our participation in a research project with Professor Charles Fine and Dr. Daniel Whitney of the Massachusetts Institute of Technology, during which we visited many firms (including the Chrysler Corporation [now DaimlerChrysler], the Ford Motor Company, General Motors, Cincinnati Milacron, Bihler USA, Detroit Center Tool, Progressive Tool, Giddings and Lewis, Leblond-Makino, Nippon-Denso [now Denso], Toyota, Applied Materials, Intel, and others) over the period 1993 to 1996. These visits were part of the supporting research for an investigation of the development of corporate technology supply chains (Whitney 1993; Fine and Whitney 1995; Fine 1998). (2) In 1997 and 1998, we were introduced to the changing role of the supply-chain manager through a series of 19 open-ended interviews at Hewlett-Packard. Between October and December 1999, we followed up with five additional interviews at Hewlett-Packard. We augmented this knowledge base with interviews at BridgePoint (a semiconductor firm), an automotive firm, and an office of the Department of Defense. (3) We made use of articles from the popular business press to delineate a contrast between industry practice in the early 1980s and today, and to add further support to our case study information. (4) Finally, we utilized our own experience as engineers and project managers at General Motors (Anderson 1985–1987), Ford Motor Company (Anderson 1988–1993), and General Electric (Parker 1985–1990). We turned to our former industrial colleagues in these three firms to help clarify issues we observed in our case and archival data.

From these information sources, we have come to believe that there is a job, the supply-chain integrator, that has become critical to the vertically-disaggregated firm’s success and growth. This new job differs radically from those found in traditional supply-management organizations, which have focused primarily on issues of cost, delivery, and inventory control. In the era of large, vertically integrated firms purchasing well-specified components, these issues were of paramount importance. As we have argued above, firms have been disaggregating their operations as they cease to perform non-core activities in-house (Fung and Magretta 1998; Scouras 1996). More and more, firms are purchasing subassemblies for final assembly into complete products to be shipped to customers, leaving detailed engineering and design work to the suppliers. In order to successfully manage this new “virtually-integrated” supply base, some firms have created the position of supply-chain integrator. A number of former midlevel managers, many of whom may have been victims of corporate downsizing only two years ago, have found a new career as individual contributors managing the interaction of supplier firms. Even as firms are reducing head-count and becoming more focused, the people responsible for direct interaction with the suppliers are finding their jobs to be richer and more complex than ever before.

So, how does a disaggregated firm stitch together its suppliers into one virtually-integrated firm? One partial answer to the issue may be to employ supply-chain integrators on both sides of a customer/supplier relationship. By providing the necessary translation, coordination, and negotiation between supply-chain members, these highly-skilled integrators act as the glue to bind together the virtually-integrated firm into a coherent, effective reality. But how does a firm employ them, what skills do these people need, and how does a disaggregated firm find the people possessing them?

Based on case studies presented in Parker and Anderson (2000), we develop a list of desirable supply-chain integrator capabilities. We note that in many cases firms are using veteran employees who learned their skills in large, vertically-integrated manufacturing firms.

We suggest that the supply-chain integrator’s primary purpose is to translate knowledge and mediate requirements across the supply-chain to maintain product integrity. In our case studies, two main themes emerge. From the notebook case described earlier we see one firm emphasizing people-skills and managerial competence:

We needed a whole new group of people. [These new supply-chain managers] need people-management skills, such as objectives setting and planning and exploiting people’s strengths and setting up plans to improve their weaknesses. The supply-chain managers also need negotiation skills. Half of the people . . . were managers [in their former positions].

Third party partners [in Taiwan] are more complicated to manage than HP people. They are 16 hours ahead of us. It’s a lot like having first-shift supervisors managing second shift people. Being really good at setting plans and objectives is more crucial. It’s a better more interesting problem. You need to be a better manager than before. Contingency plans need to be set in place. They’re forced not to micromanage.

They need to know information technology systems and how they fit together. This is needed to stitch together the systems at HP and the suppliers. They need a cursory understanding of what tools are out there and what’s available.

It’s also clearly helpful if they understand logistics, but maybe more emphasis is necessary on the people side. (Parker and Anderson 1999)

In contrast, one domestic automotive firm has stressed a technological solution to the problem of managing the supplier base. This firm is emphasizing systems engineering skills—the ability to make technical trade-offs. A manager at the firm said the following:

Our strategy is to leverage systems engineering capability. We’ve won awards for integration . . . but it’s in pockets. What are our core competencies? What do we need to do to develop people? We’re trying to manage complexity. Systems engineering tools look like the best for the job. We’re not wedded to [them]; if a better methodology comes along, we’ll adopt it. (Anderson and Parker 1999a)

One explanation for the difference in the two approaches is that automobiles are vastly more complex products than notebook computers. Indeed, the instrument panels in some higher-end automobiles incorporate specialized laptop-type computers as subsystems to provide navigation and other information services to drivers and passengers. Despite the emphasis on systems engineering at one automobile firm, we believe that this firm requires at least the same skills in its supply-chain integration function as the notebook computer firm. Combining these approaches, we develop a set of skills for the supply-chain integration role. This set includes:

1.Product development, including system decomposition and interface specification as well as project management. This also includes that portion of marketing science required to translate customer requirements faithfully into a product concept and maintaining its integrity over time. (See Iansiti and Clark 1994 for a fuller description of product integrity.)

2.The “soft” people skills necessary to mediate and resolve conflicts successfully.

3.The ability to evaluate business decisions on a cost and strategic basis.

4.The ability to make trade-offs at the subsystem level to improve system level performance.

5.Operations management, particularly logistics and process analysis.

6.A good working knowledge of information technology capabilities.

Several comments are necessary on the list above. The integrator clearly must understand product development, including system decomposition and the translation of customer needs into product requirements. This is, of course, true for any firm. However, the disaggregated supply chain makes special demands. One is the multiplicity of firm world-views, expectations, and assumptions. In this mixed and ambiguous milieu, a clear articulation of product vision is of the utmost importance in aligning firms to a common purpose. Also crucial is decomposing a product to minimize potential inter-firm design problems because, as we will discuss shortly, resolving problems across firm boundaries is extremely difficult. Thus, a deep understanding of product design is necessary to clearly delineate the virtually-integrated firm’s target, define a path towards it, and removing as many obstacles as possible along the way.

Inevitably such obstacles will arise. Thus, the integrator must also be a skilled practitioner of soft people skills. This requirement may appear unimportant if there is only one integrator purchasing all of a project’s outsourced goods and services. However, as demonstrated in the case of the semiconductor manufacturing chain, the supply-chain integrator may not reside in the same company that purchases the final product. Thus, at that firm, there is automatically a complex relationship cutting across two organizational boundaries (chip supplier → testing, packaging, and integration → customer firm → end-customer). And even if only one integrator is purchasing the services, the buyer’s coercive power is essentially restricted to threatening withdrawal of business from the supplier. While such power can be effective, it is also crude and likely to work only in stable environments with well-known requirements and multiple potential replacements for the affected supplier. Something else must replace the fine-grained coercive power of a product manager in an integrated firm with organizational connections to supplier engineers. What is necessary, then, are the skills of persuasion and mediation. When requirements are not all that clear and product life-cycles short, the integrator’s goal is to tease out the joint solutions with the supplier firms in order to faithfully maintain the original product vision. This suggests that the relationship with suppliers is not a zero-sum game with players negotiating over a fixed-size reward, but instead an effort to create the highest joint reward. An integrator’s ability to engender mutual trust with suppliers is critical to facilitating this type of joint problem solving (Currall and Judge 1995; Zaheer, McEvily and Perrone 1998). It also suggests how necessary it is for the integrator to translate imperfect requirements from the technical and institutional context in one firm to another. For without such inter-firm translation, miscommunications will lead inevitably to either inter-firm conflict or a suboptimal product (Nonaka 1991). Hence, translation as well as mediation and negotiation are the primary tools with which the supply-chain integrator must organize the supply chain.

The complementary abilities to evaluate business cases and system trade-offs are necessary to guide the integrator in solving the inevitable product development and sourcing problems in such a way as to maximize customer value and firm profit. Integrators need not know how to evaluate all the problems themselves; knowing all the possible technological ramifications of every possible problem as well as being expert in project management and soft people skills would require a superhuman. The solution favored by many is to hire specialized technical experts to advise frontline integrators when they must handle especially challenging technical problems. For instance, HP’s notebook division employs several such troubleshooters with deep technical expertise in miniaturization. According to a manager in the notebook division, most of these experts “were small hardware designers at HP for a long time. People who designed calculators in the ‘70s and palmtops” (Parker and Anderson 1999). The Department of Defense employs companies such as Aerospace Corporation to fill a similar role by providing Ph.D. experts in fields such as load dynamics to provide technical evaluation support for their project managers on an as-needed basis (Anderson and Parker 1999b). Thus, while it is imperative that integrators have the general skills of an MBA and systems engineer, they need not know all the technical fields with which they interact in depth.

The integrator must also understand the core concepts of operations management such as process analysis quite well. For the more esoteric aspects of specific areas such as logistics, they can request technical assistance from an operations research group. Without a good understanding of the possibilities inherent in operations management, however, they will not know what questions to ask suppliers or which possible solutions to evaluate. Finally, a basic knowledge of the possibilities inherent in modern information technology is also necessary to the integrator. This may surprise the reader as it did the authors! Increasingly, however, the requirement for a basic knowledge of information technology appears to be true not only for supply-chain integrators, but for operations managers in general. Sturgeon (1997) noted that “electronics firms are using information technology to communicate across the firm boundary. . . .” One of the authors (Anderson) supervised five MBA operations group-internship projects (at four separate firms) in the 1999–2000 academic year. Each project required a significant information technology component; this prevalence was not true even two years ago. Again, the actual information technology applications can be developed by specialists, but a knowledge of what supply-chain strategies information technology can and cannot enable is essential.

The Care and Feeding of Supply Chain Integrators

Having defined the skill set necessary for supply-chain integrators, we must address how to develop and maintain them. Parker and Anderson (2000) discuss some possible options to formally educate supply-chain integrators. However, for the foreseeable future, firms will obtain integrators in one of two ways. The first method described by firms such as Hewlett-Packard that are currently building integration capabilities is to hire older engineers and managers who have held multiple positions in product design and manufacturing over ten to twenty years. While this is a quick and efficient method, it may become less viable as the vertically-integrated firms which created these veterans in the first place disaggregate. The other option available to firms is to create integrators through internal training. This training will necessarily be demanding and lengthy, including in all likelihood both a period of formal training and a following period of on-the-job learning. Once firms obtain a number of experienced integrators, they may be able to reduce this training period by mentoring less-experienced colleagues. However, even with a veteran core of experience integrators, managing these sorts of in-house training programs is quite difficult because of the dynamic trade-offs involved, particularly if there is market growth (Anderson 2000a, b) or cyclicality (Anderson 1999). For example, during upswings in demand, should integrators best spend their time integrating new products or training new integrators? During downswings, should integrators be fired knowing that they will be difficult to replace during the next upswing? Anderson, Fine, and Parker (forthcoming) explore similar issues in skill retention issues in the machine tool industry in the face of industry cyclicality. Further, all of these problems are exacerbated when planning policies for product design staffs must be integrated across a supply chain (Anderson and Morrice 2000). The results of all these papers suggest that such programs and people must be treated as expensive, long-term investment programs. Many firms may be naturally reluctant to bear the costs of such training programs. As discussed earlier, however, the ability to effectively integrate supply chains is becoming increasingly more critical, making the expense of setting up such training programs unavoidable. And given the lead-time required to build up this capability, the earlier that firms begin to develop this capability, the sooner they will be able to exploit their new disaggregated business models most effectively.

CONCLUSION

We have argued that designing supply chains with an eye toward managing learning and integration along the supply chain will provide substantial advantage to firms that can manage these difficult tasks well. As motivation, we note that product outsourcing has led to a number of challenges for managers. As firms have disaggregated their supply chains to take advantage of cost savings offered by supplier organizations, firms become susceptible to the Humpty Dumpty problem. They must somehow ensure that products remain tightly integrated even though their design is broken up into a dozen pieces or more. One response, as described previously, is to design products that have well-defined subsystems (modular architecture) and hence need little integration. Another response is to hire special integrators whose job it is to ensure product integrity over a disaggregated supply chain. The need for such personnel is likely to increase if firms begin to outsource substantial portions of their product design. However, creating such a workforce may be initially quite problematic.

There are other downsides to the vertically-integrated firm. In particular, there are many outsourcing traps that snare firms in low quality, high-cost product solutions. What makes outsourcing traps difficult for firms to avoid is that near-term decisions that offer component cost savings are the very decisions that, in the long run, can increase integration costs, and possibly increase total product cost. Finally, there are substantial contracting issues that firms must confront if they wish to develop proprietary technologies jointly with their suppliers.

We firmly believe that integration will become the key issue for firms as they design their physical and technology supply chains in the future. Because there is little literature examining how learning, integration, and outsourcing mutually interact, we call for a systematic study of their relationship to improve supply-chain design. This study can teach us how to fully exploit the advantages of product and design outsourcing without suffering the possibly devastating consequences of poor outsourcing decisions.

REFERENCES

Alden, E. “One-Stop Shop Is No Cure-All: Supply-Chain Problems Can be Extremely Costly but Passing the Buck to a Third-Party Logistics Company is No Solution in Itself.” London: Financial Times, p. 2.

Anderson E. G. “Managing the Impact of High Market Growth and Learning on Knowledge Worker Productivity and Service Quality.” Under revision for the European Journal of Operational Research. 2000a.

Anderson, E. G. “Partial Insourcing at a Top PC Maker.” Personal comunication, University of Texas at Austin. 2000b.

Anderson, E. G. “The Nonstationary Staff Planning Problem with Business Cycle and Learning Effects.” Under revision for Management Science. 1999.

Anderson, E. G., and M. A. Anderson. “Are Your Purchasing Decisions Today Creating Your Future Competitor: Avoiding the Outsourcing Trap.” Systems Thinker. Forthcoming.

Anderson, E. G., C. H. Fine, and G. G. Parker. “Upstream Volatility in the Supply Chain: The Machine Tool Industry as a Case Study.” Journal of Production and Operations Management. Forthcoming.

Anderson, E. G., and G. G. Parker. “A Dynamic Simulation of the Effect of Learning on the Make/Buy Decision.” Under review at Production and Operations Management. 2000.

Anderson, E. G., and G. G. Parker. “Learning, Product Integration, and the Make/Buy Decision.” Working paper, University of Texas Business School, 2000a.

Anderson, E. G., and D. J. Morrice. “Capacity and Backlog Management in Service-Oriented Supply Chains.” Working paper, McCombs School of Business, University of Texas. 2000b.

Anderson, E. G., and G. G. Parker. Interview with Domestic Automobile Systems Manager. Austin, TX, University of Texas at Austin, 1999a.

Anderson, E. G., and G. G. Parker. Interview with Mr. Alan Sheasley - Former D.O.D. Program Manager, University of Texas at Austin, School of Business, 1999b.

Carroll, P. Big Blues. New York: Crown Publishers, 1993.

Clark, K. B., and T. Fujimoto. Product Development Performance. Boston: Harvard Business School Press, 1991.

Currall, S. C., and T. A. Judge. “Measuring Trust Between Organizational Boundary Role Persons.” Organizational Behavior and Human Decision Processes. 1995, Vol. 64, No. 2, pp. 151–170.

Dertouzos, M. L., R. M. Solow, and R. K. Lester. Made in America. New York: Harper Perennial, 1989.

Farrell, J., H. K. Monroe, and G. Saloner. “The Vertical Organization of Industry: Systems Competition versus Component Competition.” Journal of Economics and Management Strategy. 1998, Vol. 7, No. 2, pp. 143–182.

Fine, C. H. Clockspeed: Winning Industry Control in the Age of Temporary Advantage. Reading, MA: Perseus Books, 1998.

Fine, C., G. Gilboy, and G. Parker. “The Role of Proximity in Automotive Technology Supply-Chain Development: An Introductory Essay,” In Creating and Managing Corporate Technology Supply Chains. Cambridge, MA: M.I.T., 1995.

Fine, C. H., and D. Whitney. Is the Make/Buy Decision a Core Competence? Cambridge, MA: Massachusetts Institute of Technology, 1995.

Fung, V., and J. Magretta. “Fast, Global, and Entrepreneurial: Supply-Chain Management Hong Kong Style: An Interview with Victor Fung.” Harvard Business Review. 1998, Vol. 76, No. 5, pp. 102–114.

Hansen Report. “The Company Profile: Nippondenso.” September 1994.

Kauffmann, P.J. “Dunkin’ Donuts (E): 1988 Distribution Strategies.” Case Study, Harvard Business School, 1988.

Leonard-Barton, D. “Core Capabilities and Core Rigidities: A Paradox in Managing New Product Development.” Strategic Management Journal 1992, Vol. 13, pp. 111–125.

Nevins, J. L., and D. E. Whitney. Concurrent Design of Products and Processes: A Strategy for the Next Generation in Manufacturing. New York: McGraw-Hill, 1989.

Nonaka, I. “The Knowledge Creating Company.” Harvard Business Review. 1991, Vol. 69, No. 6, pp. 96–104.

Parker, G. G. Interview with Storage Networks. Tulane University Freeman School of Business, New Orleans, LA, 1999.

Parker, G. G. “Contracting for Employee and Supplier Capability Development.” Doctoral Dissertation-Management Science. Cambridge, MA: Massachusetts Institute of Technology, 1998.

Parker, G. G., and E. G. Anderson. “From Buyer to Integrator: The Transformation of the Supply-Chain Manager in the Vertically Disintegrating Firm.” Under Review at Production and Operations Management. 2000.

Parker, G. G., and M. W. Van Alstyne. “Information Complements, Substitutes, and Strategic Product Design.” Working paper, William Davidson Institute, University of Michigan, 2000.

Parker, G. G., and E. G. Anderson. Interviews with HP Employees, Tulane University Freeman School of Business, New Orleans, LA, 1999.

Prahalad, C. K., and G. Hamel. 1990. “The Core Competence of the Corporation.” Harvard Business Review. May–June pp. 79–91.

Scouras, I. 1996. “Contract Manufacturing is Changing Industry Map.” Electronic Buyers’ News.

Sturgeon, T. J. “Turnkey Production Networks: A New American Model of Industrial Organization?” Berkeley Roundtable on the International Economy, University of California at Berkeley, 1997.

Tikoo, S. “Assessing the Franchise Option.” Business Horizons, Indiana University Kelley School of Business, May–June 1996, pp. 78–82.

Whitney, D. E. “Nippondenso Co. Ltd: A Case Study of Strategic Product Design.” Research in Engineering Design. 1993, Vol. 5, pp. 1–20.

Wiederhold, R. “Leading Trends in the Design Services Industry.” Web-Driven Development, Boston University Center for Enterprise Leadership, 2000.

Williamson, O. E. Markets and Hierarchies, Analysis and Antitrust Implications: A Study in the Economics of Internal Organization. New York: Free Press, 1975.

Womack, J. P., D. T. Jones, and D. Roos. The Machine that Changed the World. New York: Rawson Associates, 1990.

Zaheer, A., B. McEvily, and V. Perrone. “Does Trust Matter? Exploring the Effects of Inter-Organizational and Inter-Personal Trust on Performance.” Organization Science. 1998, Vol. 9, No. 2, pp. 141–159.

Zenger, T. R. “Explaining Organizational Diseconomies of Scale in R and D: Agency Problems and the Allocation of Engineering Talent, Ideas, and Effort by Firm Size.” Management Science. 1994, Vol. 40, No. 6, pp. 708–729.

1. The authors would like to thank Tonya Boone and Ram Ganeshan for organizing the Batten Conference. We would also like to thank Mary Ann Anderson, who made numerous contributions to the intellectual content of this paper.