APPENDIX 1

Winning Entries from the Financial Services Forum Marketing Effectiveness Awards

In our chapter on marketing measurement (Chapter 19), we draw extensively on the experience of managing and judging the Financial Services Forum Marketing Effectiveness Awards, which over the past 16 years have established an important role as the only awards scheme of their kind.

We suggest in the chapter that the structure which entries are required to follow can act as a template to ensure good marketing planning and measurement in firms' day-to-day activities. The sequence of seven headings – listed and explained on page 235 – call for clear and focused thinking on the issue to be addressed, the strategy to address it and the measures put in place to assess the results.

In this appendix, we expand on this thinking by including three papers that won awards in the past couple of years. Each has been slightly edited to remove commercially sensitive information, but even so – within the 1,000-word limit imposed by the scheme – they all stand as good examples of well-planned, well-implemented and well-measured marketing activities – and, of course, even more importantly, activities that achieved excellent results against their objectives.

SANTANDER

Simple | Personal | Fair: How Santander Redefined Customer Experience

Entry Category: Customer Experience

Question 1: What was the issue or challenge facing the business?

- In 2013 Britain was limping out of the worst economic crash in a generation. Banks were perceived as being completely out of touch with society.

- If times were tough for the established banks, the challenges were greater for a Spanish newcomer.

Santander faced two unique challenges:

- We needed to evolve our brand identity.

Formed through a merger of three former building societies – with three different cultures – we needed to establish what Santander stood for, for staff, customers and consumers.

- Customer loyalty and satisfaction needed improving.

Despite having a great product in the 1|2|3 Current Account, we had a low number of loyal customers and ranked amongst the worst high street banks for customer service.

- This is the story of a radical new approach, which completely redefined customer experience at Santander.

Question 2: What was the insight that underpinned your strategy and tactics?

- Too often, banking insights start with products. To redefine the customer experience, we needed to understand exactly what consumers wanted from their bank.

- We commissioned six research groups with existing customers and our competitors' customers, and they told us about their strains with banks, what they liked and what they wanted.

- They spoke about their frustration when things went wrong and took too long to resolve. About feeling overwhelmed by the range of products on offer. About being ripped off.

- Listening to their pain points, we realised there was deep-seated anxiety at the core of the relationship between bank and customer. Customers didn't trust banks, and wanted to feel confident in managing their money.

- Our task became clear, and it would be mammoth, requiring a wholesale change in how we did business.

Question 3: What was your proposed strategy to address the issue or challenge?

- Our strategy for redefining this relationship came from looking at the elements we were already getting right.

- Our customers defined their positive experiences in the same terms. The best encounters with us were simple, personal or fair.

- New account openings and the mobile app were praised for being simple.

- Friendly interactions with staff and rewards linked to spending were championed for being personal.

- Genuinely beneficial products and reciprocal rewards were heroed for being fair.

- Therefore if customers' best encounters with us were either simple, personal or fair, imagine if we could make every experience hit all three.

- We hypothesised that this could build a genuine sense of trust, successfully changing the customer experience.

Question 4: How did you execute the strategy?

- We embedded Simple | Personal | Fair within Santander, instilling a new culture among our 20,000 UK colleagues.

- We needed our people to have ownership of defining what it meant for them, so we welcomed our staff's feedback and input.

- Ana Botin, Santander UK CEO, conducted workshops countrywide to find out what being Simple | Personal | Fair meant to our UK staff.

- The roadshows led to the launch of an online forum called ‘Better Together’, that allowed any colleague – from branch to boardroom – to suggest ideas to make us more Simple | Personal | Fair. Nearly 2,000 colleagues participated, suggesting 542 ideas and casting 23,000 votes.

- This work led to ‘The Santander Way’; we empowered every member of staff to speak up and say ‘Stop. This isn't right; we need to do things differently.’

- We continued to transform the whole business:

- Made incentive schemes more customer focused.

- Moved contact centres back to the UK.

- Simplified products and their range (e.g. reducing 11 adult bank accounts to 2).

- Redesigned our website.

- Launched the SmartBank app, to help with money management.

- After establishing Simple | Personal | Fair internally, a consumer-facing campaign followed in March 2014.

- We wanted to communicate each value's individual merits whilst giving Simple | Personal | Fair meaning as a collective entity.

- We used a construct that dramatised how anything can be described in three words.

Question 5: What metrics did you put in place to track the effectiveness of your solution?

- Uplift in key brand and perception measures

- Awareness and impact of Simple | Personal | Fair

- Double the number of loyal customers

- Satisfaction in line with the top performing banks

- Top 25 employer in The Sunday Times

- Make inroads into the current account market

Question 6: How can you prove that your campaign strategy met its objectives?

- Our first success was transforming our culture internally. As early as December 2013, the Financial Conduct Authority found that Santander ‘employees … enthusiastically articulated the new Simple Personal Fair culture with examples of how they were applying it in their interactions with customers’.

- Improved staff engagement continued, now one of the Sunday Times Top 25 companies to work for (2015).

- Also saw a far-reaching perception change externally. Just one year on, we saw spectacular results:

- Simple | Personal | Fair was spontaneously linked to Santander three times more than any other bank.

- 75% agreed Santander is striving to be Simple | Personal | Fair and 78% agreed we reward customers.

- YouGov's Buzz rankings put Santander in the number one spot for most improved positive sentiment, with a 28-fold improvement over the previous year.

- In a study of 179 Personal Financial Journalists (April 2014), Santander ranked in the number-one spot as the company that impressed them most in the past year and as the company that is changing for the better.

- The impact of communications on interest in finding out about the bank' rose from 21% to 31%.

- Trust improved by 12%, and in 2015 Santander won Most Trusted Mainstream Bank at Moneywise Awards.

- Advocacy rank moved from seventh (May 2013) to fourth (May 2014) and second place (April 2015).

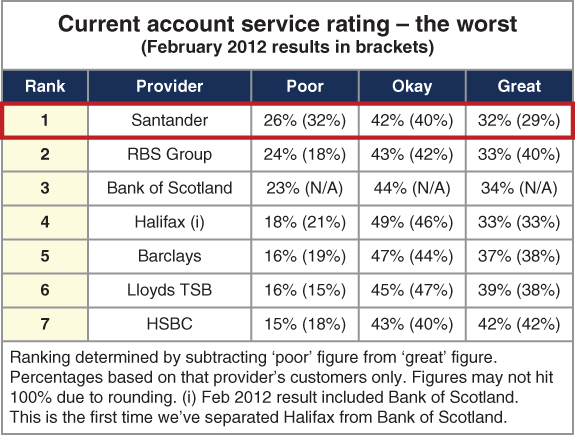

- Martin Lewis's – one of the most influential financial commentators – current account service rating from last place 2012, to second place 2014 (after First Direct) or the first high street bank.

- Loyal customers up 119%.

Question 7: What value was added to your business as a result of your strategy?

- Crucially, we also saw an increase in consideration and sales.

- Our lead over our competitors for Current Account consideration increased from 6% (February 2014) to 13% (June 2014).1

- 31% increase in sales of our 1|2|3 Current Account since 2013, and now the most switched to current account on the market.

- Profit before tax up 26% 2013 to 2014. Growth in operating income over eight consecutive quarters, and an unprecedented increase in banking liability.

- We have and continue to transform the bank with Simple | Personal | Fair.

DIRECT LINE GROUP

Alfie Deyes' Direct Line Driving Challenge

Entry Category: Social Media

Question 1: What was the issue or challenge facing the business?

- How can a leading car insurer emulate prior brand marketing success when reaching out to a younger, more modern demographic? This was the challenge facing Direct Line's latest social media campaign.

- In 2014, Direct Line transformed its fortunes with a new marketing message. Switching our iconic little red telephone on wheels for ‘the fixer’ Winston Wolf and the strapline ‘Can your insurance do that?’, we positioned ourselves as the ‘go-to’ firm for fixing things when they go wrong. However, despite revenue-raising success, we still failed to engage with a younger driver demographic, with a cost per action totalling a whopping £335.80 per sale between April and July 20152 for drivers within the 17- to 25-year-old age bracket.

Objectives

- Clearly more cost-effective measures had to be taken to attract and retain a demographic that is pivotal to the long-term sustainability of the brand.

- Placing DrivePlus – our telematics plug-in that analyses driver behaviour to offer discounted premiums – at our campaign's heart, we set three objectives that would be targeted at 17- to 25-year-olds:

- Grow return on marketing investment (ROMI) for DrivePlus, by selling more gross written premiums (GWPs) in 2016 from a 37% lower marketing spend over 2015.

- Raise brand awareness, measured by DrivePlus installation and the amount of generated quotes.

- Use DrivePlus to convince 17- to 25-year-olds that Direct Line is the champion when it comes to being there for young drivers.

Question 2: What was the insight that underpinned your strategy and tactics?

- We were under no illusions: engaging with a 17- to 25-year-old, millennial audience would be difficult. Notoriously hard to reach, given the speed at which they switch off and skip material, conventional advertising methods are often expensively ineffective.

- Such insight, coupled with the implied ‘boring’ nature of insurance, meant that bold thinking would be needed to engage and explain the key DrivePlus benefits, which included:

- Discounts – An automatic entitlement of a 25% reduction on under-21 premiums and a discount of at least 15% for 21- to 25-year-olds.

- Simplicity – While telematics products usually need to be fitted by an engineer, DrivePlus's ‘black box’ can be installed easily and directly by the customer.

- Our strategic insight, therefore, was to produce a campaign that would not only engage but also effectively inform our young demographic of the product and the advantages it can directly offer them.

Question 3: What was your proposed strategy to address the issue or challenge?

- Direct Line would need to speak to a millennial market on its own terms in regard to content, platform and message. Conscious of the target audience's fleeting attentions, we chose to adopt a branded content strategy.

The power of vlogging and Alfie Deyes

- This decision pointed us to the popularity of vlogging and the high-profile vlogger Alfie Deyes. With 4.5 million followers at the time, including a large young female demographic which is a key audience for Direct Line, 23-year-old Alfie was also famed for his inability to drive.

- Alfie's lack of prowess behind the wheel suggested an engaging backstory that had already spawned the #alfiecantdrive hashtag – a running joke among his subscribers.

- This ready-made 17- to 25-year-old audience, coupled with the ability to safely film Alfie's own demonstrations of DrivePlus in context, made the vlogging medium seem an ideal choice.

Question 4: How did you execute the strategy?

- The campaign began with Alfie being contracted and ready to accept Direct Line's challenge. Crucially, could the vlogger learn to drive and do it safely using telematics?

- Following an initial video unboxing of the DrivePlus plug-in device, app instructions and his one-year insurance policy, Alfie would complete a seven-day intensive driving course. Mentioning the challenge in his vlog and snapchat output, Alfie's efforts included:

- Five videos – Appearing on both Direct Line's and his own PointlessBlogVlogs channel, multiple YouTube vlogs detailed his driving experiences after passing his driving test (a four-month period).

- Traction – Going above and beyond his contract requirements, Alfie involved other popular celebrity vloggers (including girlfriend Zoella) in his videos to yield almost three times the average views of the other videos (384k).

- Competitions – Alfie invited young drivers to enter and win driving lessons, producing 12,033 impressions and an overall engagement rate of 63% (versus 2% average for the Direct Line account as a whole).

- The detailing of what DrivePlus is and how it is used remained central to all content.

Question 5: What metrics did you put in place to track the effectiveness of your solution?

- From the outset, campaign effectiveness would be measured by:

- Awareness and brand perception of Direct Line and DrivePlus

- Video views, viewing times, likes and comments (YouTube, Instagram)

- Impressions and engagement rates (Twitter)

- Website click-through rates (CTRs)

- High-level metrics measured included:

- Total number of DrivePlus quotes

- Total number of DrivePlus gross written premiums (GWPs)

- These metrics gauged the success of a socially driven, online content strategy, while also measuring our overriding campaign and business objectives.

Question 6: How can you prove that your campaign strategy met its objectives?

Achieving growth via organic engagement

- In terms of tangible online results, the campaign:

- Generated over 1 million organic video views with an average viewing time of over six minutes, producing over 52k likes.

- Achieved over 258k Twitter impressions, 11.9k Twitter engagements and an average engagement rate of 11.4%.

- Coincided with an improved click-through rate (CTR) to the DrivePlus section of directline.com, with CTR rising 169% during the campaign.

- This level of engagement not only outperformed Direct Line's brand average, it proved to be both the most successful organic content on our channel and the second most successful overall.

Greater brand awareness and product perception

- Such a positive reception of the campaign content was always dependent on Direct Line's effective reach for 17- to 25-year-old drivers. Deeper analysis of viewer feedback on Alfie's videos showed not just greater awareness of the DrivePlus product and the incentives for safer driving, but that 36% of viewers agreed Direct Line is ‘there for young drivers.’

- Alfie's vlogs also helped to boost brand perceptions, with consumers among the campaign target market revealing greater appreciation of:

- Direct Line's promotion of better, safer driving.

- Telematics products and a desire to learn more about them.

- The DrivePlus app, with 17% of viewers perceiving the product more positively post-exposure and 40% more likely to download.

40% of viewers claimed that they would be likely to download the app. This is an important metric for brand consideration since anyone can download the app as part of Direct Line's ‘try before you buy’ approach.

Question 7: What value was added to your business as a result of your strategy?

- In terms of the business value, our campaign successfully managed to:

- Drive a 29.1% year-on-year increase in the total number of quotes for DrivePlus in 2016.

- Deliver 22.9k DrivePlus GWPs during the campaign period (Apr–Jul 2016).

- Increase DrivePlus GWPs by 30% against the same period in 2015, despite a 37% reduction in budget.

- Dramatically reduce cost per action (5.9 times) and per quote (8.3 times) figures within the 17- to 25-year-old target market.

- Ultimately, the rise in Apr–Jul 2016 GWP revenues over the equivalent 2015 period, with lower costs, yielded a healthier bottom line for Direct Line. Acting as a pivotal driver behind the consistent increase in DrivePlus policy uptake, the Alfie Deyes campaign serves as a brand marketing success story within a notoriously challenging demographic.

The launch of the Alfie Deyes campaign brought about a consistent increase in DrivePlus policies and thus revenue. There were consistently more DrivePlus policies compared to the same period the previous year over the campaign period.

POLICE MUTUAL

Intelligent Marketing to Deliver Sustainable Growth

Entry Category: Direct Marketing

Question 1: What was the issue or challenge facing the business?

- The Regular Savings Plan (RSP) is Police Mutual's flagship product and accounts for 35% of all sales and income and 25% of new member acquisition. The sales performance had been in decline for eight years until this was arrested in 2013 and since then performance has increased by 3% on average per year until 2016.

- As part of its growth ambitions, Police Mutual has set a target of increasing RSP sales by 10% year on year alongside an increase of 10% new savers. This must be delivered cost efficiently, with marketing investment in the product being reduced by 15% over the same period. This effectively results in a ROMI investment target increase of 15%.

- As a provider who serves the needs of a specific audience, we are still heavily reliant on our direct marketing channels, specifically direct mail, e-mail and outbound phone calls.

- With blended conversion falling 1% between 2015 and 2016 across these channels, it was clear that a new direct marketing strategy was required to deliver the required growth.

Question 2: What was the insight that underpinned your strategy and tactics?

- We adopted a Discover, Define, Deliver and Deploy framework to help build and implement the new strategy.

- As part of our discovery phase, we immersed ourselves in our target audience's environment (primarily in police stations/headquarters), conducting face-to-face interviews and running quantitative research with our database. This allowed us to understand what was driving non-savers to purchase or not purchase.

- It was clear that we were very effective at generating repeat business from existing savers, with 57% of this audience opening a new plan year on year.

- However, it also became clear that our ability to convert prospects through direct marketing was weak, accounting for just 8% of all new non-saver sales.

- Feedback from member-facing teams, prospects and current savers highlighted that there was a large degree of apathy towards saving regularly and a more persuasive approach was required, facilitated by the application of social psychology and consideration of the impact of system 1 / system 2 thinking.

- This led to us defining a hypothesis that the social mind was more important than we had considered previously and that loss aversion was a key barrier for prospects purchasing a new RSP.

- Our hypothesis was: ‘People do not see the positive value of saving. They only see the negative value – costing £30 per month’.

- To validate this and build a plan of how we could overcome resistance, we worked closely with the Social Psychology Department, Aston Business School.

Question 3: What was your proposed strategy to address the issue or challenge?

- Our strategy was to transform our direct marketing by applying the EAST Model developed by the Behavioural Insights Team, The Cabinet Office.

- There were four aspects to our strategy:

- Replace current marketing activity with scalable marketing programmes developed through a programme of test and learn.

- Build marketing activities that are timely, relevant and personalised through the use of appropriate triggers.

- Automate these triggers through our CRM technology to improve efficiency and contribute to a reduction in CPA and increase in ROI.

- Apply relevant behavioural psychology techniques such as social norming, social scripting and perceptual fluency to help nudge prospects to purchase.

The examples in question 4 demonstrate how we have applied the EAST model to the marketing material.

Question 4: How did you execute the strategy?

Pay rise campaign letters

- Personalisation (A)

- Segmentation (A, S)

- Social norms (S)

- Loss aversion (S)

- Perceptual fluency (A)

- Scripting (E, A)

- Identification (A)

- Timely

Triggered by the month the pay rise is due email follow-up

- Scripting (A)

- Personalisation (A)

- Consistency (S)

- Social norms (A, S)

- Ownership (E)

- Defaults (A)

- Scripting (A)

- Timely

Triggered by anniversary of last plan taken

- Application form premium test

Example of thinking beyond marketing collateral to operational elements of the journey

- Choice framing

- Segmentation

AB testing proved that the average amount saved per year increased by 2.45% when offering £7 as a minimum premium. The conversion rate was not affected.

Question 5: What metrics did you put in place to track the effectiveness of your solution?

- The objective of each activity was to outperform current BAU marketing activity (our control and benchmark). An ‘effective campaign’ was defined as an activity that generated 100% ROMI and outperformed the relevant BAU activity.

- Key metrics measured over a period of 56 days were:

Business outcomes:

- Annual Premium Equivalent (APE)

- Sales volumes

- Income

- CPA

- ROMI

Behavioural measures:

- Unique open rate

- Unique click-through rate

- Conversion rate

- Telephone calls

To date we have measured success at a macro level and are now identifying which specific elements of the new approach drove the increase in performance.

Question 6: How can you prove that your campaign strategy met its objectives?

- At a macro level we generated the best sales performance for RSP in 2016 since 2010 and have increased sales performance by 12% in 2017 (against a target of 10% uplift) whilst reducing our costs by 18% (against a target of 15% reduction).

- This increased ROMI by 22% in 2017 against our target of 15%.

- The performances of specific direct marketing activities have all increased, with positive results versus benchmark marketing activities.

- This quantitative data shows the strategy being employed is driving increased performance amongst our non-saver audience.

- This is supported by MI showing the volume of new saver RSP business has increased by 19% in 2017 against a target of 10%.

Sales ROMI Income/APE CPA Direct Mail +89% +67% +92% –53% E-mail +35% +24% +35% –16% Unique Open Rate Unique CTR Conversion Rate Direct Mail – – +120% E-mail +29% +99% +50% Metrics based on relevant campaigns. No metric = not relevant for that channel.

Question 7: What value was added to your business as a result of your strategy?

This programme has and is delivering these long-term benefits:

- Increased Lifetime Value

RSP customers have a higher average product holding and lifetime value compared to the average member (£420 versus £238).

This represents 36% of total lifetime value for police business and is set to grow to 45% by 2020. RSP customers therefore represent a significant and growing proportion of total member long-term value.

- Validation of B2B Proposition

The Police Service is at the heart of what we do and much of our activity is dependent on gaining access to the police at the local level. Our B2B proposition is dependent on us demonstrating continued relevance to our members and the Service.

RSP is critical to this and we must continue to demonstrate products like this can and do contribute to the financial wellbeing of police officers. We estimate this access can save us around 90% of our total marketing expenditure, equivalent to a 30% increase in RSP sales.

Over the past 12 months we have helped 5,000 police officers acquire the savings habit and have paid out the equivalent of a 15% pay rise from maturing plans, for a typical police officer, helping validate the value of our proposition to the Police Service and building and maintaining access to it.

- Knowledge transfer

Having proven the value of this approach – development and application of social psychology and the overall approach of hypothesis development – test and learn and rapid upscaling is being more widely adopted across other marketing programmes.

These are showing early promise and we are confident that the ongoing application of this approach will result in considerable improvements in the effectiveness of our marketing investment.