C H A P T E R

3

Step 1: Set Up an Emergency Fund

Protect the Purchasing Power of Your Emergency Cash

In my experience, elegant solutions tend to be relatively simple once you fully understand the problem and come up with an intelligent method to deal with it. That's why this chapter is relatively short, but still important.

As we saw in Chapter 2, if you do nothing about price inflation, then the emergency fund that is designed to cover your expenses for at least 6 months (preferably 12) if you lose your main source of income will steadily lose purchasing power. This will manifest itself by your monthly expenses steadily increasing but the balance in your checking and savings accounts barely changing.

So what can you do to prevent this from being a problem? There are three main solutions, the first of which isn't very practical and doesn't really solve the problem, but I need to mention it because it's what most people choose to do about it.

Increase Your Emergency Fund by the Same Rate That Your Expenses Go Up

The simplest solution to the problem is obvious—if monthly expenses are going up and you want to keep the fund at, say, 12 months worth of expenses, then simply add to the fund each month to make sure the balance is equal to current monthly expenses times 12 at all times.

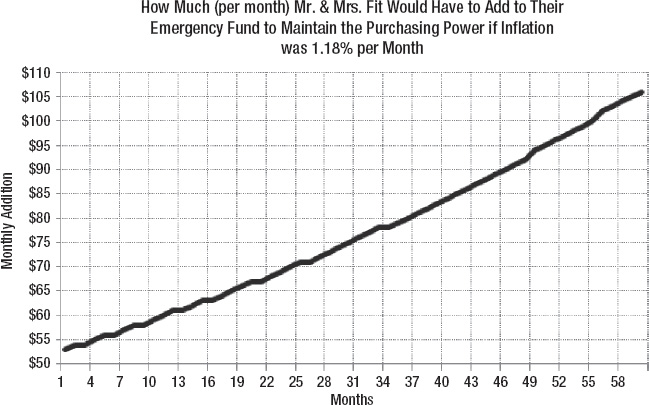

Figure 3-1 shows exactly how much you'd have to add to your emergency fund each month if your monthly expenses were rising by the 1.18% I mentioned in Chapter 2.

Figure 3-1. Maintaining the purchasing power of your emergency fund the hard way

Now this may not seem like a big deal when you initially look at the chart—the monthly addition starts off at a little over $50 and doubles to just over $105 after five years. However, this means that the size of your emergency stash has to double just to buy the same amount of products and services it does today. And that's simply to stand still, so to speak, from a quality-of-life point of view.

This is a very inefficient and costly way to maintain your emergency fund, in my opinion, so I'm not recommending you do this.

The Simple Solution: Precious Metals

If you studied the charts in Chapter 2 closely, you'll probably have a good idea what's at the root of the problem. It has to do with the constant weakening of the purchasing power of fiat currencies, such as the dollar, which translates into price increases for physical commodities.

What if, instead of saving cash for your emergency fund, you decided that you would save nonperishable foods from now on? As a result, you stock your cupboard with the equivalent of 12 months' worth of food. If you did that, what period of time would the food in the cupboard feed you for in 1 year, 10 years, or 50 years? The answer is the same of course: it would feed you for 12 months no matter how far into the future you look (assuming you don't change your daily ration significantly). Why? Because it is a physical commodity that doesn't change in size or caloric value once it's purchased.

I know the size of products in the stores can shrink, but not normally after you've purchased them! Obviously, this solution only works to ensure you will eat during the emergency period. What about other typical monthly expenses like housing, transportation, clothing, entertainment, and other items that can't easily be turned into physical commodities in advance and stored in a cupboard? Yes, I suppose you could purchase all the underwear you'll ever need and put it in a drawer, but what if your taste changes (not to mention your waist size)? Buying all the DVDs you'll ever want to watch in advance is not exactly plausible either unless you only ever want to watch classic movies.

Now you're beginning to see the solution to the emergency fund problem. The fact is that you simply don't want to keep your emergency cash in any fiat currency—you want it in a physical commodity that maintains its purchasing power no matter how long you own it.

You've probably guessed by now. The solution to the problem is to buy precious and industrial metals:

- Gold

- Silver

- Palladium

- Platinum

An Inflation-Proof Emergency Fund That Maintains Purchasing Power

The simplest solution to owning precious metals would be to buy some gold bars and then bury them in the garden (making sure your neighbors don't see you). Take your current monthly expenses, multiply them by 12, divide this number by the current spot price of gold per ounce, and the answer is how many ounces of gold you need to bury in your garden. Then, in ten years, when you lose your job and can't pay your mortgage, simply dig up the bars sell them at the current spot price for dollars, and use the cash to cover your monthly expenses.

If you're looking at the price of gold in US dollars right now and seeing it make new all-time highs, you may be thinking, “Paul, you're nuts. I'm not going to buy into gold right at the high and then watch the value of my emergency cash plummet. The smart money got in months or years ago and is just waiting to cash out at my expense. It's a speculative bubble just waiting to burst.”

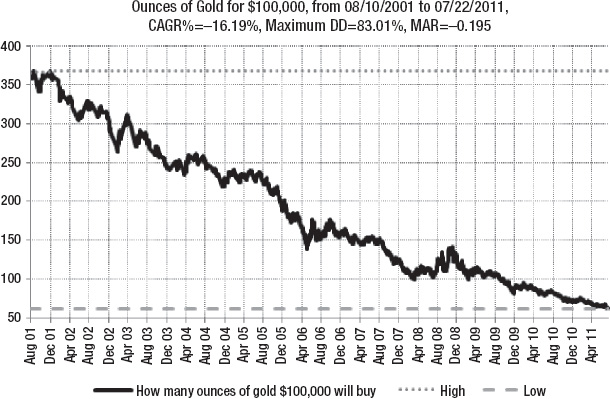

The only thing I would agree with in that previous paragraph is “the smart money got in months or years ago,” but not the part about “waiting to cash out.” Take a look at Figure 3-2, which is a chart that shows how many ounces of gold $100,000 would buy over the last decade.

Figure 3-2. Ounces of gold that $100,000 could purchase over the last decade

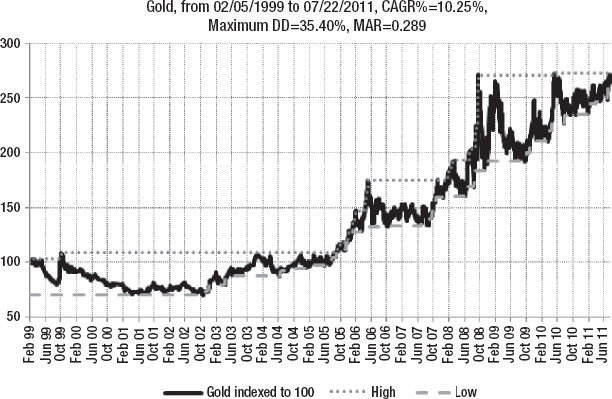

Does that look like a speculative bubble to you? It looks like a secular trend to me. Another way to look at this is shown in Figure 3-3.

Figure 3-3. Gold priced in Australian dollars, February 1999 to July 2011

It's the same chart shown in Chapter 2 (2-10), but instead it uses Australian dollars instead of US dollars for the “price” of gold. Not such a “speculative bubble” visible there, eh? The fact is that it's not really useful to measure the value of a physical commodity using a fiat paper currency—we should be using the physical commodity to measure the value (or lack thereof) of the fiat paper currency.

If you're really concerned about turning your emergency cash into metals just at an “all-time” high, then simply hedge your bets and average in to your metals positions over a period of time—but be warned, in my opinion this is not the time to be gambling the purchasing power of your emergency fund on the strengthening of the US dollar (or any other fiat currency).

Hopefully you'll now agree that metals are the best place for your emergency fund right now. So let's get back to the practical problems of physical ownership. Following is a list of the immediate ones I could think of:

- What if you can't easily sell your load of gold bars for dollars when you want to?

- What if you've moved to another house and forgotten about the gold bars, and you no longer have access to them?

- What if the US government makes it illegal for individuals to own physical gold in the United States (again)?1

- What if you need to make adjustments to the size of the emergency fund because expenses have changed?

- What if you think you can get a job in a couple of months so you don't need to sell a whole gold bar to cover your expenses?

- What if you want to move somewhere else in the world and the US restricts transportation of gold out of the country?

- How practical is this method if you don't want to just own gold, but want platinum or palladium too?

I'm sure there are a few other practical problems you can think of too, and that's why I'm not recommending you own gold bars, gold coins, or gold jewelry. Nor am I recommending you keep gold in your garden, at a security deposit box at a bank, in your own vault at home, or anywhere else actually located inside the United States.

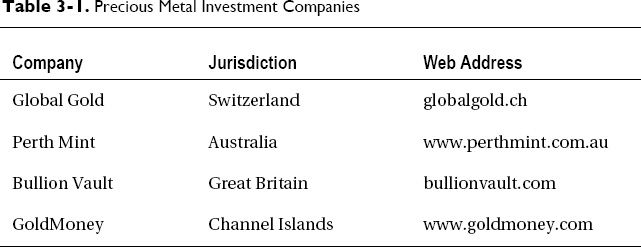

A much better, easier, and more flexible solution to owning metals is using a trustworthy online service. Table 3-1 shows four services that allow you to own precious metals without having to take physical ownership.

The one I personally use and recommend is GoldMoney.2

____________

1This happened previously in the United States when Executive Order 6102 was signed, on April 5, 1933, by US President Franklin D. Roosevelt. It was repealed on December 31, 1974, by Gerald Ford in Public Law 93-373.

2 I have no connection to GoldMoney other than as a satisfied customer.

How GoldMoney Works

GoldMoney allows you to deposit cash (currently US dollars, Canadian dollars, British pounds, Swiss francs, Japanese yen, euros, Australian dollars, Hong Kong dollars, or New Zealand dollars) into your account (called a holding). Once it's there, you can purchase metals (currently gold, silver, platinum, and palladium) in small amounts (1/100th of a gram). The metals that you buy are allocated to you and stored on your behalf—for a reasonable monthly fee that is charged in metal, not currency—in one of the vaults that GoldMoney uses. The vaults are located in London, Zurich, and Hong Kong.

You get online access, along with statements of your account holdings and current values, just like a brokerage account. When you want to convert any of your metal holdings back into fiat currency, you simply enter an online order, specify how much of each metal you want to sell, and say which currency you want to receive.

I'm not a tax advisor, and this book is not intended to deal with the tax implications of different investment choices. However, I can give you an overview of the tax treatment of GoldMoney holdings from a US point of view. In the United States, holdings of precious metals would be considered a collectible, and therefore any capital gains from the sale of your GoldMoney holdings would be subject to capital gains taxes. In addition, the capital gains tax for collectibles is 28% in 2011—not the lower 15% for long-term gains in most securities. This, of course, might change, so check with your accountant.

If you move US dollars into your GoldMoney account, purchase metals with them, and leave them alone, then there are no tax implications to deal with until you sell. However, there is an additional reporting requirement for US residents if the value of the account is greater than $10,000. In this case, you must file form TD F 90-22.1 with the US Department of the Treasury before June 30th of the year following the calendar year that the account first had a value of over $10,000. Uncle Sam always wants to know where your assets are, and it's futile trying to hide them. As long as you intend to pay the capital gains taxes due on your holdings when you do sell them, then reporting the account to the US Treasury shouldn't be a problem.

If you do sell some of your metals holdings, then you need to calculate the net capital gain (minus the fees that have been charged for the storage of your holdings during the period) and report this on your tax return as a capital gain. GoldMoney does not issue 1099 forms to US-resident customers, but your complete transaction history is available as part of the online access to your account, so it should not be a problem for you, or your tax advisor, to calculate the capital gains just like for any other investments you sell.

The following narrative describes how The Fits implement their emergency fund.

Mr. & Mrs. Fit Establish an Emergency Fund

Mr. and Mrs. Fit decide to open a GoldMoney account and use it to manage their emergency fund cash. Mr. Fit goes to GoldMoney.com and downloads the application form. He prints it out, fills it in, and mails it along with the supporting identification documentation. Once he receives notification that the account is open, he moves all their current US dollars into his checking account and writes a check to fund his GoldMoney account for $60,000.

When the check has cleared, his GoldMoney account access shows a balance of $60,000. Mr. Fit then uses this cash to buy equal dollar amounts of gold, silver, palladium, and platinum for their account. He receives the following holdings:

Now that he's done that, Mr. Fit doesn't need to worry about his emergency fund any longer. Even though the dollar value of his account will fluctuate daily, he knows that over the long-term, when he needs to convert his holdings back to currency, he will have the same purchasing power that he has now. He only needs to make an adjustment if his monthly expenses increase significantly (due to adding liabilities, not price inflation). In this case, he will add to his metals holdings by moving more cash into his GoldMoney account and purchasing equal dollar amounts of additional metals.

For example, if he adds a significant monthly expense of $1,000 per month, he would add $12,000 to his GoldMoney account and purchase $3,000 worth of each metal at the current spot price.

Gold vs. the Dollar

At this point you may be saying, “That's all fine, but what if the value of the US dollar significantly strengthens vs. gold? Won't I end up with a shortfall in my emergency fund if I need it?” The simple answer is that this is very unlikely to happen, and if it does, then it's not going to be a problem anyway. If the US dollar is strengthening, inflation is very low, the economy is growing, unemployment is low, the government is doing a great job of managing fiscal policy, then everyone's standard of living will be going up. So you shouldn't be needing your emergency fund any time soon, should you?

If you aren't participating in the financial nirvana for some reason and you need to tap your emergency fund when the value of your precious metals holdings are relatively low (when measured in dollars), remember that you don't have to sell your entire metals holding as soon as you lose your main source of income. If you set up your fund with 12 months' worth of cash, then you can sell 1/12 of your metal positions each month to cover expenses until you replace the income you have lost. This should smooth out any volatility in the value of your emergency fund over a longer period of time. In addition, your emergency fund should not be the only place for you to “park” excess assets – you should have savings that are designed to increase in value if and when fiat currencies are worth holding and use these cash resources if the value of your emergency fund is temporarily depressed.

Chapter 4 explains how to manage your working capital and savings in this kind of utopian environment (and the normal kind too), and Chapter 5 explains how to make a good risk-adjusted return on your investments regardless what's going on with inflation, interest rates, and global currencies. These three steps together help you manage your finances and preserve your wealth regardless of the prevailing economic conditions.

An Alternative Solution, for People with Home Equity to Spare

Earlier in this chapter I mentioned that there were three solutions to the emergency fund problem. We've dealt with two of them (adding to the fund monthly and using precious metals), and now it's time to explain the third one.

Wouldn't it be great if you could have an emergency fund that had the following characteristics?

- It didn't cost you anything until you needed to use it.

- It could be increased and decreased as expenses changed.

- It was cheap to set up.

- It didn't require a large cash deposit at the start.

Fortunately, if you have spare equity in your home (i.e., the current market value of your home is greater than the outstanding balance on your mortgage), then you can use a home equity line of credit (HELOC) as your emergency fund instead of cash in your checking account.

A word of caution here. The old saying that a bank is an institution that lends money only to people who don't need it is true. A HELOC, just like a mortgage, is a loan against future income that is secured on a property so you get a better rate than for an unsecured loan. This means that if you don't have any income, you won't be approved for a HELOC no matter how much equity you have in your home based on its current value. Therefore, this technique should be put in place in advance, before you lose your primary income—not afterward. So if this idea appeals to you, make a call now to your friendly banker.

Inflation will still continue to eat away at the spending power of your HELOC (although this won't cost you anything since it's simply a line of credit you haven't used yet), so it's a good idea to take advantage of any significant local increases in house prices. Get your home revalued, and if it has gone up, then apply for an increase in the HELOC amount too. This way your line of credit can keep up with inflation as long as house prices don't go down the toilet. This is the main reason why using a HELOC should be a secondary method of implementing an emergency fund—it's still a good idea to have some funds in precious metals as well.

Another caution is that if you're the kind of person who will be tempted to use “just a little” of the HELOC for that “emergency” vacation in Hawaii you've always wanted to take, then this technique is probably not for you. Use precious metals instead.

If you currently have cash sitting in a checking account as your emergency fund, but also have a mortgage on your house, then simply use the cash to pay down the mortgage principal and put a line of credit in place that is the same size as the cash you paid off the mortgage. This is usually simpler if you take out the HELOC with the same company that is giving you the primary mortgage on your home. So it's best to wait until next time you want to refinance your primary mortgage and then talk to the bank about the line of credit at the same time. Again, don't wait until after you lose your primary income to do any of this—the bank won't approve any type of loan if you don't have any current income.

If you end up in the situation where you are forced to use your HELOC to pay monthly expenses, it's not all bad. In an inflationary environment where prices are going up, it's better to be a debtor than a creditor—you can pay back borrowed funds with devalued currency units since the balance doesn't grow and the value of the currency units you use to pay the interest on the loan is constantly shrinking. Once you replace your primary income you can simply start to pay down the HELOC until it's down to zero again.

In Summary

This chapter has outlined two practical solutions to implement an emergency fund that should maintain purchasing power over time.

These solutions are:

- Using GoldMoney to own and manage precious metals online

- Utilizing a HELOC if you have (or can create) equity in your home

If you follow one or both of these solutions, you will no longer have to worry about the purchasing power of your emergency fund being significantly diminished when you need it. Although the value as measured by any one currency will be volatile, the purchasing power of the physical metals that you hold should be much more stable and resilient to the ravages of inflation.