C H A P T E R

4

Step 2: Make Savings and Working Capital Work for You

How to Maintain an Acceptable Real Rate of Return in Different Interest Rate Environments

So far, we've seen how to protect the purchasing power of your emergency fund so that it will have an excellent chance of paying your fixed expenses when you need it. The solution to the problem of inflation works well for funds that need to maintain purchasing power, but it has a drawback if you need to guarantee the dollar value of a certain portion of your cash assets in the near future. The dollar value of metals in your online precious metals account can go up as well as down in the short term, because the price is volatile.

For cash that you are going to need to meet specific obligations in the near term (like college expenses, a vacation you're saving up for, a major purchase like a new vehicle, or the deposit on a new house), you have a different set of requirements. If this is cash that you simply can't afford to take any risk with at all—like next semester's college tuition payment—then there is no alternative but to keep it in cash and accept the negative real rate of return. Remember that risk and reward always go hand in hand, so if you need to take zero risk, then you cannot expect any reward. Any method of capital management that generates a return involves risk (in the form of price volatility) and therefore should not be used for cash that needs to maintain its near-term dollar value.

The method that I describe in the rest of this chapter is for cash that you can afford to take some risk with in order to have a reasonable chance of a decent real rate of return. How to deal with your savings and working capital depends on what the prevailing interest rate environment is for all major currencies.

It would be great if a major currency always paid an annual interest rate a few percentage points above the inflation rate. If your home currency always did this, then you would not have any problems at all. Unfortunately, there are many periods (about 80% of the time, as you'll see before the end of this chapter) where this is not the case. So there is no simple, single-currency solution to this negative real interest rate problem.

Did I say currency? Yes. Holding foreign currency can be an important way to hedge against inflation. And it need not cause undue stress—buying currency is not much different, you'll see, than buying stocks or bonds.

First, I need to define what real rate of return means. The real rate of return on an investment is simply the actual (or nominal) rate of return you have received, minus the current rate of inflation. So if you buy a certificate of deposit (CD) in US dollars that pays 6% per year in interest, and the current CPI-U inflation rate is 2%, then the real rate of return is 6% – 2% = 4%. For the purposes of this chapter, we're going to ignore the caveats of the CPI calculations discussed in Chapter 2, and assume that the CPI-U does represent a “fair” inflation rate with regard to the purchasing power of your cash.

When deciding what to do with savings or working capital, the first thing we need to do is define whether we're in a positive or negative real interest rate environment. For this we need to know two things:

- The current annual interest rate payable in each major currency listed below

- The current annual inflation rate for each home country or geographic area for the currency

The ten major currencies I consider when doing this calculation are

- Australian dollar

- British pound

- Canadian dollar

- Euro

- Hong Kong dollar

- Japanese yen

- New Zealand dollar

- Swedish krona

- Swiss franc

- US dollar

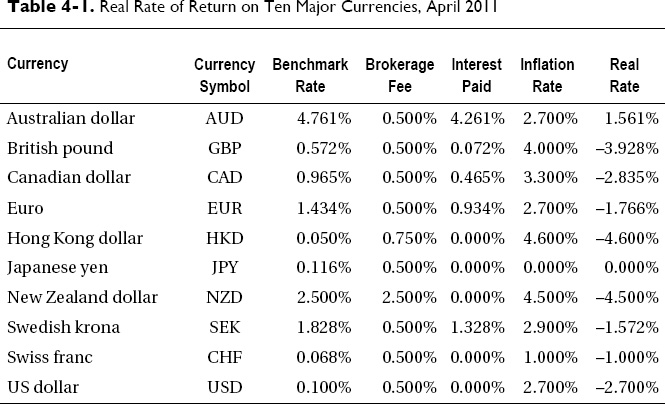

Table 4-1 shows the current interest rates, inflation rates, and real rate of return for each of the ten currencies, as of April 2011.1

__________

1 The resources that were used to determine the data are listed in Appendix A.

As you can see, as of April 2011, only the Australian dollar is paying a positive real rate of interest. This means if you have any cash in any of the other nine major currencies, then the purchasing power of that cash is diminishing every single day. Note that it's important to include any fee or spread that your broker or bank charges, or any other deductions from the actual interest you will receive on each currency balance. If the current benchmark rate is less than the interest fee, then the interest paid will be zero, not negative (i.e., you will not normally be charged for holding positive currency balances in your account).

Once you have constructed this table, then it's easy to determine whether you are in a positive or negative real interest rate environment and act accordingly. If at least eight out of ten of the major currencies are paying a real rate of interest that is at least 2% per annum, then you are in a positive real interest rate environment; otherwise, you're in a zero or negative real interest rate environment.

A Positive Real Interest Rate Environment: What to Do

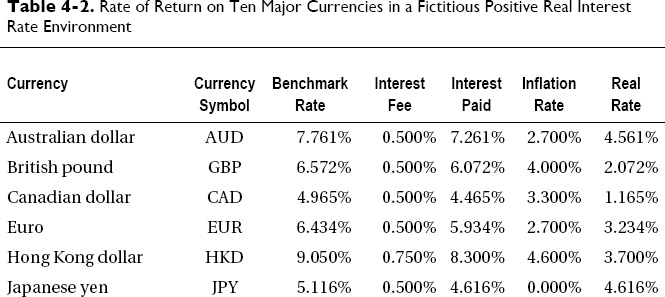

If you're in a positive real interest rate environment, then it's a good idea to keep savings and working capital in major currencies. The best approach is to hold currencies proportional to their real interest rate. The following example should make this clear. Let's assume that prevailing interest rates for at least eight of the ten currencies are at least 2% above inflation, as in Table 4-2.

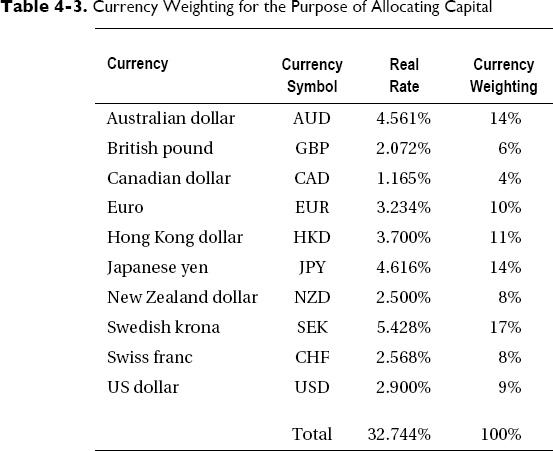

To determine how much of your capital to allocate to each currency, we simply need to construct another table that determines the relative weighting of each currency based on its real interest rate. This is shown in Table 4-3.

How did I come up with these figures? The currency weightings are simply each individual real rate divided by the total of the real rates (32.744% in this example). For example, Australia's 4.561% rate of return divided by 32.744 results in 14% (rounded). Once you have constructed the table, then it's simple to work out how much of each currency you should buy. If you have $100,000, for example, then according to Table 4-3 you should put 6% of it, or $6,000, into British pounds. If the current exchange rate between US dollars and British pounds is 1.6489 (i.e., 1 British pound is worth 1.6489 US dollars), then you would buy 6,000 / 1.6489 = 3,638 GBP.

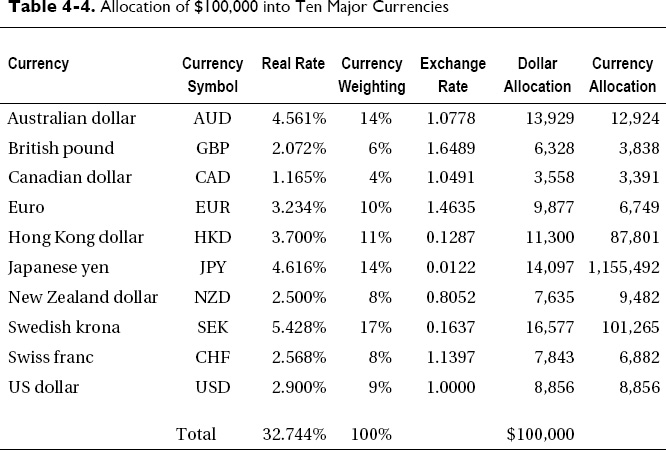

Table 4-4 shows how you would allocate $100,000 US dollars based on the given exchange rates.

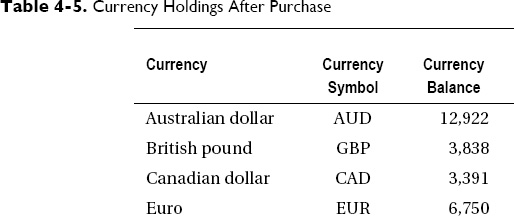

Using the details from Table 4-4, you would take your 100,000 US dollars and buy 1,155,492 Japanese yen with 14% of the US dollars you have. Once you have purchased all the correct amounts of all the currencies with your US dollars, the balances in your account would look like Table 4-5.

So, instead of having 100,000 US dollars, you would only have 8,856 US dollars remaining, and the rest would be held in the other nine currencies.

There are a couple of choices when it comes to which firm to use to implement the cash rebalancing method. These are:

- Everbank

- Interactive Brokers

The simplest way to implement this approach would be to use an Interactive Brokers (IB) account. The advantage of using IB is that the firm offers multicurrency accounts by default. Interest accrues daily in all currency balances, and you can easily switch between all the major currencies in one account with low fees for the transactions. The “base” currency of the account is basically just a reporting currency (which may be switched at any time), and the only practical implication of the base currency for the account is that it is the currency that commissions on foreign exchange (FX) trades are charged in.

Another advantage of using IB is that the universal account is an online brokerage account too, so you can use it for the second part of the cash rebalancing method (described in the next section), and also to manage your investments, as described in Chapter 5.

IB is not a full-service, hand-holding type of brokerage. It is fully electronic with online access, and it expects its customers to know what they are doing. If you find this intimidating, then it's probably best to break up the process into several simple steps:

- Open an individual universal account by going to IB's website, www.interactivebrokers.com, and filling out the application online for an account that allows you to trade equities and FX.

- Send the required identification information that is requested once the account application is completed.

- Once the account is approved, fund it by writing a check or wiring funds with the minimum required amount.

- Log onto the demonstration version of the account and familiarize yourself with how to place currency transactions accurately.

- Build a spreadsheet to allow you to manage the currency balances effectively in the demo account until you are comfortable with the process.

- Manage the currency balances in your real account using the WebTrader application, which is simpler to use than the full Trader Workstation (TWS) application.

- Only when you are completely comfortable with the whole process should you increase the funding of the IB account to include all the savings and working capital you want to apply to this method.

PECULIARITIES OF CURRENCY TRADING

When trading currencies, there are a few things to watch out for. Firstly, it's important to note that there are always two currencies involved in a FX trade. These are called the base currency and the quote currency. For example, in the FX pair GBP/USD (or GBP.USD), GBP is the base and USD is the quote. If the “price” of the FX pair GBP/USD is quoted as 1.6, for example, this means that 1 GBP will buy 1.6 USD.

Traditionally, some pairs are always quoted with US dollars as the base currency. These are

- USD/CAD

- USD/CHF

- USD/HKD

- USD/JPY

- USD/SEK

When you want to do FX trades in these quote currencies, you will have to sell the desired quantity of US dollars in order to buy the quote currencies (just as you would expect).

The other currencies you may want to trade are traditionally listed as the base currency with US dollars being the quote currency. They are as follows:

When you want to do FX trades in these base currencies, you simply have to buy the currency pair, which in turn means you are selling US dollars to purchase the base currency. This means that you will have to calculate the amount of base currency you wish to buy, rather than the quantity of US dollars you wish to sell, as in the first group of currencies where the base currency is US dollars.

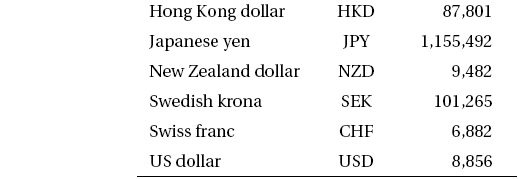

If you're thinking that this all sounds a bit too complicated, or you don't want to open up yet another brokerage account, then there is a simpler alternative to actually doing the FX transactions; you can use currency exchange-traded funds (ETFs) instead.

The following table shows you possible choices for each of the major currencies.

The two firms currently offering currency ETFs are Rydex (CurrencyShares) and Dreyfus (Wisdom Tree). There is not currently a Hong Kong dollar ETF available, so that particular currency would have to be omitted from the method if you chose to implement it using ETFs.

One caveat with the Rydex funds is that they are mainly designed to track the exchange rate rather than both the exchange rate and the interest payable. After the fees charged by the fund and the spread charged by the firm providing the depository account are deducted, there is no guarantee that you will actually receive a reasonable annual rate of interest based on the relevant currency benchmark rate. For this reason I would recommend the Dreyfus WisdomTree ETFs where available (EUR, JPY, and NZD) and the Rydex CurrencyShares ETFs for the remainder. Note that, as with everything in investing, opting for simplicity has a cost, and can have a significant detrimental effect on performance. There is no guarantee that you will be able to achieve results similar to actually using real currency transactions with daily accrued interest in an IB account.

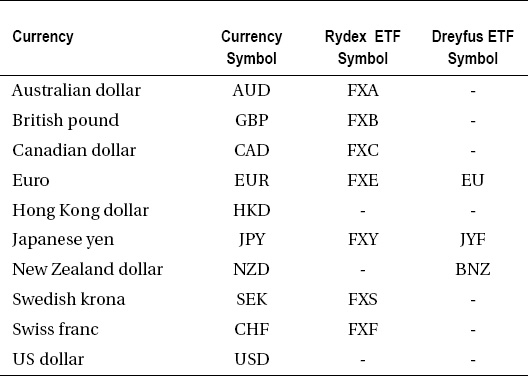

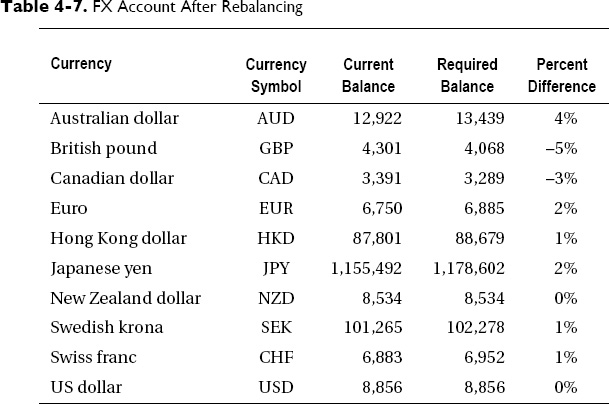

Once you have managed to accurately establish currency balances in proportion to the interest rates with a fully funded account, then quarterly rebalancing should be sufficient unless there is significant change in real interest rates or currency exchange rates. Unless a particular currency is more than 5% out of balance, it's best to leave things unchanged—this minimizes commissions and fees on the account and therefore maximizes your return overall. The easiest way to track this is in a spreadsheet with all the required information in it, as in Table 4-6.

What you need to do is to update the interest rates, CPI numbers, and exchange rates, and then recalculate the currency balances on a quarterly basis and make any modifications necessary to get the balance back (to within 5%) if something changes. For example, in Table 4-6, the British pound and New Zealand dollar balances are now out of balance by more than 5% (positive or negative), so we need to sell some New Zealand dollars and buy British pounds with them to get the balances back in line.

If the current exchange rate between British pounds and New Zealand dollars is 2.047 (i.e., 1 British pound purchases 2.047 New Zealand dollars), then we could sell 9482 – 8534 = 948 NZD and receive 948 / 2.047 = 463 GBP for them. The currency balances would then look like Table 4-7.

Selling the currencies that are overweighted and buying the currencies that are underweighted with them allows us to keep the balances within the 5% tolerance. This should be done on a quarterly basis, with the minimum number of transactions, in order to minimize the fees required to implement the method.

A Low or Negative Real Interest Rate Environment: What to Do

If we're currently in a low or negative real interest rate environment, then keeping savings in major currencies does not make sense—the purchasing power is being diminished every single day. In this kind of environment it's best to allocate equally to metals, ETFs, inflation-protected ETFs, and inverse bond ETFs. (Inverse bond funds are designed to move in the opposite direction of the ETF they are paired with—more on those to come.) The selection I recommend is

- Gold (GLD)

- Silver (SLV)

- Platinum (PPLT)

- Palladium (PALL)

- Inverse Treasury Bonds (TBT)

- Treasury Inflation Protected Securities (TIP)

If your home currency is paying a positive real interest rate, then you can include an allocation to that, as well as the ETFs listed.

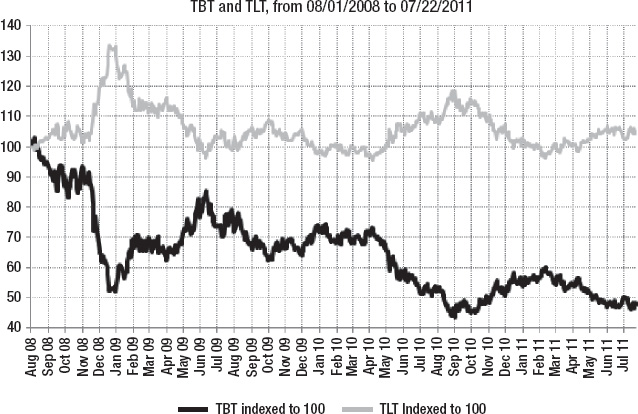

Please note that buying an inverse fund like TBT is not the same as shorting a security. Selling short cannot be done in a retirement account because it requires trading on margin—and retirement accounts can only be cash accounts. Therefore, to ensure this method can be implemented in any brokerage or retirement account, it's better to use inverse funds. In this instance, TBT is a security that is bought, but the fund is designed to move in the opposite direction of another fund—in this case to TLT, which is the iShares Trust Barclays 20+ Year Treasury Bond Fund. Figure 4-1 shows a chart of TBT and TLT over the last three years.

Figure 4-1. TBT and TLT over the last three years

Note that TBT is designed to move twice as much in the opposite direction as any move in TLT, so a 2% move up in TLT should correspond to a 4% move down in TBT. You may be looking at Figure 4-1 and thinking, “Paul, you must be nuts. Why would I want to put cash into something that has lost about 50% of its value in only three years?” The one thing I need to make clear here is that hindsight is always 20:20—interest rates have stayed very low for this whole period and therefore bond prices (which move opposite to interest rates) have stayed high, so TLT has gone up and sideways while TBT has gone down (twice as much) and sideways.

The reason TBT is included in this portfolio is so it does the following:

- Diversifies from simply holding metals ETFs

- Will make a good return for periods in which interest rates are rising but inflation is also rising, such that currencies are not paying a real rate of return yet

The second point here simply has not happened (yet), so the TBT part of the portfolio will be losing money right now. In the testing I performed for this method, going back way before TBT existed, I created a synthetic TBT that moved inversely to yields on US treasuries and included it in the portfolio. It increased CAGR and decreased DD overall, so it's definitely worth including.

The same goes for including TIP, even though we know that the CPI-U understates real inflation. The extra diversification provided by including TIP is worth the caveats and problems. Again, my historical testing shows this to be the case.

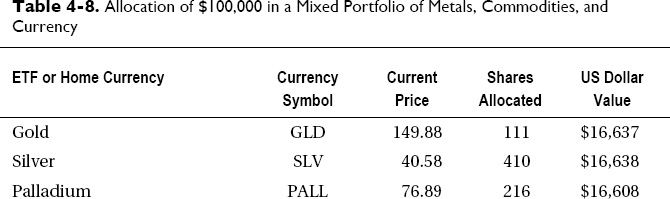

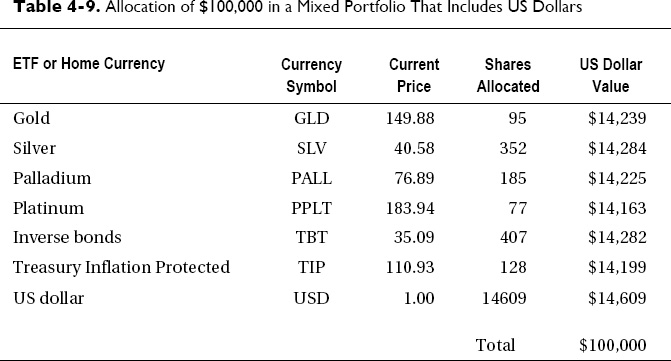

Table 4-8 shows what the allocation would be as of April 2011 for the same $100,000 in cash we dealt with in the previous section (concerning a positive real interest rate environment). Since US dollars are not paying a positive real rate of interest, the $100,000 will be equally allocated to the six ETFs. If US dollars were included, then the allocation would be one-seventh to each ETF and one-seventh to US dollars.

The total is slightly less than $100,000 since we have to round down the number of shares purchased to the nearest whole share. The allocations if US dollars were also included are shown in Table 4-9.

The reason it's a good idea to include an inverse bond fund is that if interest rates are very low, then they only really have one way to go: up. And since bond prices move opposite to interest rates, when rates inevitably go up, then bond prices will go down (and you'll make money being long an inverse bond fund). Also, if inflation does increase significantly, then TIP will go up as well, even if it's not as much as real inflation “in the street.”

If you want further diversification, you could add commodity ETFs such as the following:

If you're thinking that these commodities are all susceptible to speculative bubbles and manipulation by industry participants and professional traders, and you don't want to compete with these people, then simply construct a chart of each commodity priced in ounces of gold rather than US dollars and see where the “speculative bubbles” are then. Remember the chart of oil priced in gold from Chapter 2? Once the effects of currency exchange rate movements and devaluation are removed from the chart, it generally shows a much more stable mean-reverting relationship for each commodity.

However, these ETFs are more likely to be included in your investment account management, which is covered in Chapter 5. This chapter is specifically about savings and working capital, not investment accounts. If you plan to include commodity ETFs in your investment account, then they should not be included in the rebalancing ETFs you use for your savings. You don't want to end up with an overallocation to these particular ETFs.

If you have opened an IB account, then all these ETFs will be automatically available for you to trade in this account, and the switch from currencies to ETFs should be relatively simple.

Historical Results

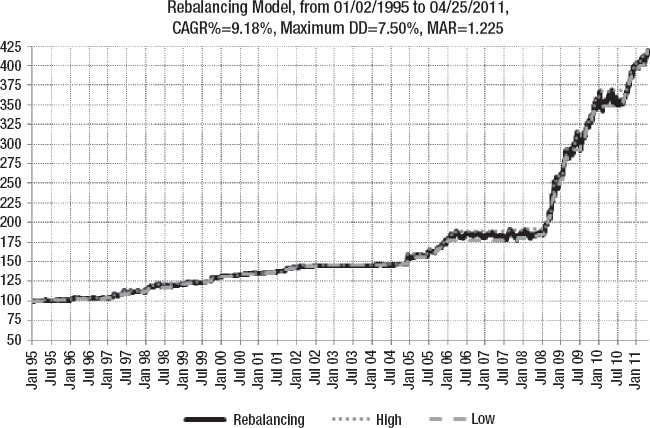

As with everything in trading and investing, it's best to test the implications of any decisions you make about how to manage your investments. I have spent many years researching different investment management techniques, and the method of cash rebalancing described in this chapter is the most effective method I have found. It minimizes volatility, minimizes exposure to a single currency, and generates a positive real rate of return. Test results for the last 16 years are shown in Figure 4-2.

Figure 4-2. Rebalancing model, 1/2/1995 to 4/25/2011, indexed to 100

These results were generated by a product called Trading Blox, which is a sophisticated historical testing environment. Note that these results do not take historical inflation rates into account—only benchmark rates minus the fees charged by IB. Thus, it is not an exact simulation of the method described here.

These results are only meant to be an indication of the kind of return and volatility this type of method generates—not an accurate estimation of future returns using the exact method described in this chapter. Note that as the CAGR has increased over the last three years, so has the maximum DD, but it has still remained under control and produced a reasonable risk-adjusted return without excessive volatility for the period.

Note that some of the ETFs in the test sample did not exist for the whole period, and have been replaced by a similar proxy instrument. For example, SLV has been replaced by silver futures data for periods before it existed as an ETF.

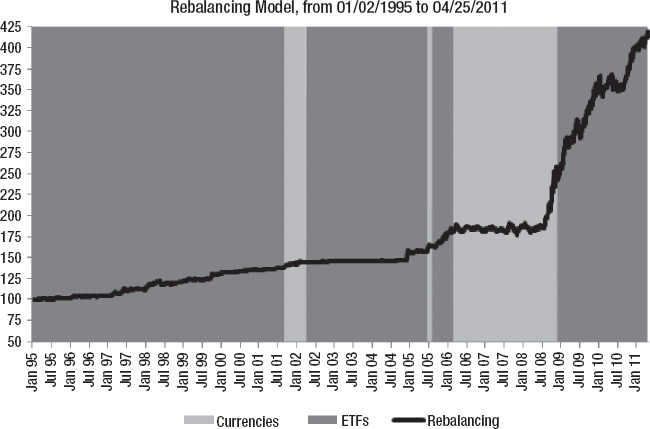

Figure 4-3 shows how the method switched from currency rebalancing to ETF rebalancing over the test period.

Figure 4-3. Rebalancing model showing switching between currencies and ETFs

Over the 16-year test, there were three periods where currency rebalancing was used, and four periods where ETF rebalancing was used. Overall, currency rebalancing was only used about 20% of the time and ETFs 80% of the time.

In Summary

Effectively managing your savings and working capital depends on what the prevailing interest rate environment is. If it's a low or negative real interest rate environment, then keep your capital in metals ETFs and inverse bond funds. If it's a positive real interest rate environment, then keep your savings in major currencies proportional to the real interest rate they are paying.

In this way you will maximize the rate of return on your savings and minimize the volatility of the absolute value of your savings accounts at the same time. This cash rebalancing technique should also be used for any “spare capital” that is not currently being utilized to take risk in your investment accounts. How to actually make a good risk-adjusted return in your investments accounts will be covered in the next chapter.