Chapter Objectives

- • Understand the business sustainability concept.

- • Impart basic knowledge about the UN SDGS.

- • Create awareness about the sustainable development challenges in Egypt.

Overview of the Origin

of Sustainable Development Concept

Overpopulation and globalization of markets have added to domestic pressures from overexploitation of resources all over the world. The relevancy of the environmental sustainability concept has increased in many countries as there is more awareness and understanding of the impact of environmental issues on society and economic growth. Research on the natural environment and its relation to business has developed considerably over the years. Many countries in the Asia-Pacific region and the United States are expecting economic, social, and environmental factors to convince the manufacturing companies to consider sustainability more seriously. Nowadays, corporate sustainability is an important topic for both academic research and businesses.

Overview of “sustainable development”: the term “sustainable development” was first made popular by the WCEB, also known as the World Commission on Economic Development. The WCEB defined sustainable development as “development action targeted for meeting the needs of the present without hindering future generations from fulfilling their own needs.” The WCEB stated that in order to realize sustainable development, the adoption of environmental, economic, and equity principles is necessary. Such a statement was, then, highly questioned due to the old prejudice that caring for the environment and establishing social equity go against making money. Over time, corporations began to show commitment to achieving sustainable development. With regard to principles of sustainable development, Elkington (1998) stated that sustainable development can only be achieved by applying three basic principles which are environmental integrity, economic prosperity, and social equity.

Environmental integrity: The environmental integrity principle guarantees that the ecosystem, that is, land, air, and water, is not harmed by any human activities. It is perceived that the ecosystem has a very limited regenerative ability; therefore, human-related events such as population growth and pollution compromise the integrity of the environment. Thus, if the natural environment is, by any means, threatened or compromised then the basic resources necessary for human life, such as food and water, will be threatened as well.

Social equity: The social equity principle guarantees that all members in a society have equal opportunities and equal access to resources. The WCED document released in 1987 stated that sustainability is a universal goal implying that all members of future generations, members of developing and developed countries alike, have the right to equal access to resources.

Economic prosperity: The economic prosperity principle endorses an adequate quality of life through organizations and individual members in society. Economic prosperity calls for the creation and distribution of goods that will most likely elevate the quality of life around the world in addition to the establishment of open and competitive markets that endorse efficiency, wealth creation, and innovation. It was found that economic prosperity is heavily linked to social equity and environmental integrity. For instance, to meet basic needs such as food and shelter, people tend to compromise the long-term health of the natural environment in the process. It is estimated that millions of hectares of forest areas are annihilated annually for the production of fuels, wood, and fertile land for agriculture. Therefore, it is perceived that a society that fails to realize economic prosperity will eventually compromise the health and well-being of its individuals.

Corporate sustainable development: Business is the production of goods or services for the customers in exchange for other services, goods, or money. Particular organizations and the market sector can be referred to as businesses. When many persons are working in one company, they are making business to produce a specific service or good in a good manner in order to raise their company in the market to reach for the lead and to be one of the most important companies in its field.

Sustainable development is a new way for people to use resources before they run out; in other words it is the development that meets the needs of the present without compromising the ability of future generations to meet their own needs. For the business community, sustainable development is extremely important and more than just window-dressing, as the companies can compete by adopting sustainable practices in order to increase both shareholder value and their markets. The company’s value differentiates it from its competitors as the products and services that yield tangible results for the company’s target customers. There are two important parts of a business model, which are production and marketing. The production side combines many factors including activities and mechanisms for providing goods and services. On the other hand, the marketing side combines those mechanisms in order to sell the products, whether they are goods or services. The latter is also known as capturing value but the first is known as creating value. The economic, social, and environmental benefits can be delivered by the business model for sustainable development.

The success of the business models for sustainable development can be determined by disparate factors; trade-offs among different sustainable development goals (economic, social, environmental) need to be recognized and addressed, and the ongoing monitoring and evaluation need to be built into business model. The idea of sustainable development has become a way of creating affirmation, yet it is not the first thought for some business executives. For most, the thought stays hypothetical and theoretical. Guaranteeing an affiliation’s capital base is a recognized business rule. The associations are unable to perceive the likelihood of extension of this idea to the world norm and HR. If sensible progression is to fulfill its potential, it must be fused into the masterminding and estimation systems of business endeavors. For that to happen, the thought must be verbalized in words which are common to business pioneers.

The business response was the idea of eco-effectiveness, uniting ecological and financial execution to make more regard for business itself as well as for the whole gathering, fundamentally, with less impact. Numerous organizations are today close to the cutting edge toward eco-capability, and it has in like manner transformed into a comprehensively recognized methodology supported by the European Commission. Clearly, more businesses need to get eco-capability, not only the multinationals arranged in the industrialized countries, but the small and medium endeavors in all sectors in all countries. Sustainable advancement is based on three factors: financial development, natural parity, and social advancement. These things have dependably been part of the motivation for maintainability; however, the social factor has received less consideration. That is changing; far more noteworthy attention is being set now on social advancement, particularly on what business is doing. This has opened up a number of issues. For a firm to achieve sustainable development it must first fulfill all three basic principles.

Environmental integrity may be achieved through corporate environmental management. Corporate environmental management is an approach made by a firm to reduce its ecological footprint that is the impact of its production processes on the environment, such as waste and carbon emissions. Such management can be achieved by pollution control and product stewardship. Pollution control refers to the proper disposal of wastes by a company, while product stewardship refers to using fewer materials for product design and proper recycling and reuse of products at the end of their life. Companies may seek social equity through corporate social responsibility. Corporate social responsibility encompasses three processes: environmental assessment, stake-holder management, and social issues management. Environmental assessment involves the identification of social, economic, and environmental issues and responding to them accordingly. Stakeholder management involves responding to individuals outside organizations as well as responding to the natural environment (Starik 1995). On the other hand, social management refers to tackling social issues, for instance, the decision not to employ children as labor.

Economic prosperity can be achieved through value creation. A firm can create value via their own products and goods. It can create value through the production of novel and different products desired by consumers, thereby elevating the effectiveness of its products which can be achieved by decreasing input costs or achieving production efficiencies. A firm can capture the value it creates by selling its goods or services at prices that exceed their costs. To conclude, the road to implementing a sustainable development philosophy will be different for smaller businesses, but with ingenuity, perseverance, and cooperation, they can achieve the desired result. In the end it is apparent that corporate prosperity is dependent upon how successful an organization is at achieving sustainable development. In addition to achieving corporate welfare, sustainable development also constitutes an ethical duty that must be exerted by the present generations for the well-being of future generations. There are hundreds of definitions of sustainability. According to Andreas and Cooperman, a well-known definition of the term sustainability related to business or development is the one coined by Gro Harlem, former prime minister of Norway and chairperson of the Brundtland Commission. The concept of sustainability is included as a requirement to “meet the needs of the present without compromising the ability of future generations to meet their needs” (Andreas et al. 2011, p. xii). More recently, researchers have proposed that we should focus more on interdependencies between business and society and take collaborative approaches to create system change (Baas 2008; Porter 2006; Boons and Roome 2005; Svendsen and Laberge 2005; in Loorbach, van Bakel, Whiteman, and Rotmans 2010). This change will cause SMEs to move from being careless of environmental concerns in their business plans and actions, to measuring their environmentally related performance, for example, in terms of waste production or resource use, adoption of ISO 14001, or how regulation influences performance. Moreover, some researchers have labeled as “enviropreneurship” the efforts made by individuals to bring ideas and motivations to increase the ecological sustainability concept of their organization.

For many years, CEOs of both major companies and international organizations such as the United Nations have talked about, or even put on a pedestal, the topic of sustainability as an inevitable challenge to change, as well as an imperative to change.

The UN SDGs (Sustainable Development Goals) as a Broad Universal Context for Sustainability

According to UN Environment Management group, the sustainable development goals (SDGs, also referred to the global goals) are the blueprint to achieve a better and more sustainable future for all. The key element of 2030 Agenda, they address the global challenges we face, including those related to poverty, inequality, climate, environmental degradation, prosperity, and peace and justice. The goals interconnect and, in order to ensure a just transition that leaves no one behind, it is important that we achieve each goal and target by 2030. Each SDG is comprised of a set of subtargets. Additionally, each goal has a set of indicators, jointly known as the global indicator framework, with which to assess progress. The global indicator framework was developed by the Inter-Agency and Expert Group on SDG Indicators (IAEG-SDGs) and agreed to as a practical starting point at the 47th session of the UN Statistical Commission held in March 2016. The report of the commission, which included the global indicator framework, was then taken note of by ECOSOC at its 70th session in June 2016. The links in the list of SDGs in Figure 1.1. will take you to the goals’ unique targets and indicators, as well as recent updates on progress.

Figure 1.1 The sustainable development goals

Source: https://unemg.org/our-work/supporting-the-sdgs/the-un-sustainable-development-goals/

The Sustainable Development Goals

- 1. No poverty—end poverty, in all its forms, everywhere.

- 2. Zero hunger—end hunger, achieve food security and improved nutrition, and improve agriculture.

- 3. Good health and well-being—ensure healthy lives and promote well-being for all, at all ages.

- 4. Quality educations—ensure inclusive and equitable quality education and promote lifelong learning opportunities for all.

- 5. Gender equality—achieve gender equality and empower all women and girls.

- 6. Clean water and sanitation—ensure sustainable management and availability of water and sanitation for all.

- 7. Affordable energy—ensure access to affordable, reliable, sustainable, and modern energy for all.

- 8. Decent work and economic growth—promote sustained, inclusive, and sustainable economic growth, full and productive employment, and decent work for all.

- 9. Industry innovation and infrastructure—build resilient infrastructure, promote inclusive and sustainable industrializations, and foster innovation.

- 10. Reduced inequalities—reduce inequality within and among countries.

- 11. Sustainable cities and communities—make cities and human settlements inclusive, safe, resilient, and sustainable.

- 12. Responsible consumption and production—ensure sustainable consumption and production patterns.

- 13. Climate action—take urgent action to combat climate change and its impacts.

- 14. Life below water—conserve and sustainably use the oceans, seas, and marine resources for sustainable development.

- 15. Life on land—protect, restore, and promote sustainable use of terrestrial ecosystems, sustainably manage forests, combat desertification, halt and reverse land degradation, and halt biodiversity loss.

- 16. Peace, justice, and strong institutions—promote peaceful and inclusive societies for sustainable development, provide access to justice for all, and build effective, accountable institutions at all levels.

- 17. Partnerships for the goals—strengthen the means of implementation and revitalize the global partnership for sustainable development.

Overview of Sustainability

Development Challenge in Egypt

According to the official State Information Service in Egypt (2014), “Egypt currently faces several environmental challenges, which place the prospects of future generations in jeopardy and lead to the depletion of natural resources” (State Information Service, para. 1). Accordingly, the Egyptian Environmental Affairs Agency, in its efforts to achieve sustainable development, attempts to address these challenges by maintaining and managing natural resources within the framework of sustainable development. However, it can be suggested that little progress can be made until organizations in Egypt become interested in these concerns. For the organizations to become interested in environmental challenges there must be some involvement from the leaders.

The problems related to natural environmental resources which play an important role to support the business sector are several. At the top of the list are water shortage, energy shortfalls, the relative nonimplementation of laws to protect the environment, and the declining levels of awareness of environmental issues. For example, the River Nile is the lifeline of Egypt as it services industrial and agricultural demand. Nowadays, Egypt is facing an annual water deficit of around seven billion cubic meters. In fact, the United Nations is already alerting conservationists that Egypt could run out of water by the year 2025. Moreover, Ethiopia started working on building El Nahda dam on the River Nile. The project has raised concerns in Cairo about its potential impact on Egypt’s annual share of water. Another important issue is that Egypt faces chronic gasoline shortages and frequent power cuts, which negatively affect the business sector and which have begun to put some pressure on businesses to be more concerned about the environmental resources, as Mr. Salah Abo Yazid, financial advisor to the Holding Company for Chemical Industries in Egypt, emphasized.

Production rates for nitrogen fertilizers, which rely on natural gas, declined during the year 2014 by up to 40 percent, and this is having a negative impact on the productivity of companies and their subsidiaries. These have been affected significantly by the energy crisis in Egypt during the last period, particularly the National Cement Company which decreased its production capacity by 50 percent, due to lower rates of gas supplied. According to the U.S. Energy Information Administration (2014), Egypt is the largest oil and natural gas consumer in Africa, accounting for more than 20 percent of total oil consumption and more than 40 percent of total dry natural gas consumption in Africa in 2013.

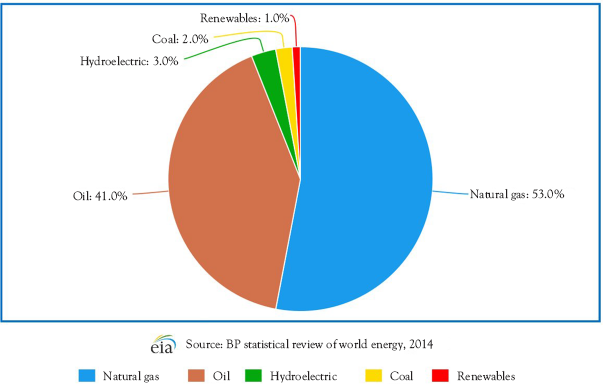

From 2009 to 2013 much of the natural gas consumed in Egypt was used to fuel electric power plants. Since 2013 Egypt has been facing natural gas supply shortages and the natural gas production declined by an average of 3 percent annually; thus there are frequent power cuts. Gas, gasoline, coal, oil, and natural gas are fossil fuel resources and their consumption leads to global warming and climate change. Furthermore, fossil fuels are finite resources and they can irreparably harm the environment (Environmental and Energy Study Institution 2014). Figure 1.2. shows the high consumption of fossil fuels and how renewable energy in Egypt is not used.

Figure 1.2 Energy consumption in Egypt

The above statements highlight two important and noteworthy issues:

- 1. The presence of sustainability practices in different industries and companies in Egypt could have prevented such depletion of valuable resources as well as keeping productivity rates uninterrupted.

- 2. Leaders who apply and are aware of sustainability concepts and practices are crucial for the prevention or reduction of natural resources depletion. The need for such leaders is thus a pressing issue.

The need for such leaders in Egypt becomes even more pressing when we further notice the effect on water and air pollution that the misuse of such resources can have.

Egyptians obtain about 97 percent of their water from the Nile River and the rest from winter rain and nonrenewable groundwater aquifers. Much of this water is polluted through industrial activities. Since the 1950s, many industries have developed in Egypt along the Nile Delta producing industrial waste which is often discarded in the water creating a major chemical threat to agricultural land. Moreover, the industrial companies in Egypt are one of the main reasons for air pollution, due, for example, to the practice of open-air waste burning.

Several of the environmental problems in Egypt stem from the long-term provision of generous fuel subsidies by the government, in order to keep influential people (such as car owners) contented. According to Prime Minster Mahlab (2014), Egypt has some of the lowest energy prices in the world, and the cash-strapped government spends more than a fifth of its budget keeping them down. This is significantly more than both health and education spending combined, which take up 64 billion pounds ($8.9 billion) and 26 billion pounds ($3.6 billion), respectively. The Egyptian government announced that it would spend an additional 70 billion Egyptian pounds ($9.8 billion) on energy subsidies in the fiscal year ending June 30, 2014. All this has, however, changed. One of the plans of the government in the near future is to remove the energy subsidies. To manage all complexities that are required to implement environmental sustainability in an organization and to cope with more limited resources, there is a need for a leader with special competencies (Ghaem 2013).

The statements above suggest that Egypt needs sustainability leaders. Sustainability practices converge around three elements: securing the environment, economic growth, and social development. The Sustainability Leadership Institute (2011) suggests that sustainability leaders are “individuals who are compelled to make a difference by deepening their awareness of themselves in relation to the world around them. In doing so, they adopt new ways of seeing, thinking and interacting that result in innovative, sustainable solution” (The Sustainability Leadership Institute 2011; para. 4).

Another definition of a sustainability leader is that of Visser and Courtice 2011: “someone who inspires and supports action toward a better world” (p. 2).

From the above statements a sustainability leader can be defined as the leader who constantly targets developing the three aspects of sustainability: environmental, social, and economic. In this research the sustainability leader is understood to be the person who focuses on the environmental aspects of sustainability and who can lead his company to achieve its objectives of preserving the environment or taking precautions to avoid damaging the surrounding environment.

The author conducted interviews with several Egyptian leaders of SMEs in order to ask them about their care and interest about the environment and social responsibility, and if a greater concern for the environment would be useful for their business. Mr. A, sales director of N. Company, revealed that

In our company we don’t care about environment or social responsibilities, it’s seen as over cost without profit return. Only sometimes we produce our products for well-known brands with high quality standards, sometimes we use the residuals and wastes from the raw material to produce the same products with low quality and sell them to other clients.

Eng. K, CEO of F. Company, suggested that “Of course it is very important, we already care about that concept and now we recycle all our products.” By contrast, Mr. N, general sales and export manager of M. Company, admitted that “If we don’t see any profit return, we will not care about that. Our main concern is innovation in our products to gain more profit and to compete in the market.” Mr. O, CEO of S. Company, also agreed that “Although we know we have an environmental problem from our production waste, which is the rice straw, until now we haven’t thought of treating this problem.” Taking a different line, Eng. R, CEO of T. Company, explained that “We follow Life Cycle Assessment (LCA) as a tool for sustainability performance evaluation; LCA provides an adequate instrument for environmental decision support” and when asked what he meant by LCA he said “Environmental quality certificates like the ISO 14000.”

Of the five interviewees, only one of the SME leaders had incorporated environmental sustainability practices in his company for the sake of sustainability, while another, who recycled his product line, further asserted that they are doing so only because it has a positive impact on their profits rather than being a sustainability practice. This translates to 20 percent of the total participants being aware of the importance of environmental sustainability in SMEs or its impact on the environment.

The above-mentioned discussions, in addition to the practical work experience of the author as well as findings from the literature review, point to an actual gap represented by a clearly observed negative attitude toward sustainability practices conceived by SMEs leaders as opposed to the actual importance of sustainability to their companies. For example, many SMEs leaders expect that adopting sustainability will increase the cost base for their companies financially, while they cannot expect any profit out of following environmentally sustainable measures. This is despite the widespread belief that consideration for the environment is now much more imperative. So it would seem that lack of appropriate attitudes, competencies, and behaviors on the part of leaders has been stopping the progress of SMEs in adopting policies and strategies that could improve their concern for the environment. There is no doubt among many environmental experts that improvement is needed, but the leaders concerned seem to lack interest and conviction. However, financially,

Environmental costs have increasingly been internalized in the business with such charges as water consumption and waste disposal. As these costs increase, the cost of business increases and in the ever more competitive market place these costs will either reduce the profit or sales or both of SME. (DeLeeuw and Genoff 2000)

Sustainability goals for businesses have been defined as meeting a “triple bottom line comprised of environmental stewardship, standards of human dignity, and financial profit” (p. 3). There is obviously a need for leaders with the ability to take a strategic view of their businesses, as continually internalizing increased costs will eventually drive them out of business.

This book aims to address questions concerned with developing an understanding of a leader’s attributes such as his characteristics, character, personality, competence, and qualities, which affect business sustainability. Drawing from social learning theory, it has been suggested that individuals learn appropriate behavior by observing others’ actions and their consequences. It has been proposed that significant players, namely leaders, may strongly influence followers. Scholars suggest that leaders influence follower behavior by modeling appropriate behavior. According to social learning theory and social cognitive theory, learning that occurs through direct experience may also occur vicariously through observation of others’ behaviors and their consequences (Hind et al. 2009). All the points above suggest that leaders may play a potentially major role in the followers’ behavior toward the business sustainability concept. Culturally, in Egypt, there is a strong tendency for leaders to be dominant in driving subordinate behavior and company strategy. Questioning subordinates and making observations is likely to confirm this, regardless of what the leader says.

There is an increasing agreement that businesses need to embrace environmental sustainability, while recent research on leading sustainable development in the management field still provides only limited guidance on how this should be done. Preliminary research carried out by the author in Egypt suggests that there are few role models to suggest a way forward. We know that many SME leaders in Egypt are doubtful about achieving a PPP balance; we do not know the attributes of those SME leaders who think it might be possible and who are trying to achieve it.

A survey of Australian SMEs showed, during the process of interviewing larger corporations, that the latter became more aware of environmental responsibility than SMEs. Moreover, they showed that SMEs were generally slow to introduce environmental management controls. A small number of Chinese small firms have adopted a formal management system with concern for the environment and attitudes to sustainability management but have not yet incorporated these concerns into their business strategy.

Some researchers argue that organizations require a paradigm shift to adopt more sustainable ways of thinking and behaving (Whittaker et al. 2009; Linnenluecke and Griffiths 2010). Moreover, Millar and Gitsham (2013) state that more research is needed in order to change attitudes and behaviors in the workplace to make companies more interested in environmental sustainability and allow companies to be responsible for their future in terms of resource consumption. A sustainable future is the idea that fits a business system which sustains natural and human resources—again, a form of PPP.

According to Taylor “we can study certain types of leaders in particular contexts” (2011, p. 44). This generates knowledge on:

- • Attributes of individual leaders

- • The nature of group-based leadership processes

- • The contextual factors that help leaders to emerge and be effective

- • Interplay of factors to enhance sustainability attitudes and behaviors of employees (sustainability awareness and citizenship)

In Egypt, the tendency in business (especially in SMEs) is not to have group-based leadership processes. It is seen as a high power-distant culture. Contextual factors helping leaders emerge can be different from those in western countries. Rather than a selection process based on objective factors considered by a board of directors, leaders of SMEs in Egypt might be entrepreneurs or might be chosen due to nepotism.

In Egypt, people tend to depend on advice and instructions from authority figures and are used to a high degree of power distance where power is distributed unequally. This implies that changes would stem from the higher levels of a company, that is, from its leaders. Leaders with a high awareness of PPP would make business and environmental sustainability a priority in the business sector. This would have a positive impact on society and economic growth. There are external factors over which the company has very limited control including, but not limited to, socioeconomic and geopolitical factors. They further assert that top business leaders are held to be in charge of managing the whole sustainability system, where some seem to master this challenge better than others. Perhaps they are just more interested and concerned, as well as being more able. Indeed, this latter point raises the question of whether there are specific leaders’ requirements or competencies that can be identified and further developed for CEOs of SMEs who want to be in the forefront of sustainability efforts. This further suggests the need to discover such competencies and requirements represented by the leader’s attributes as addressed by the research objectives.

According to Andreas et al. (2011) the definition of a sustainable economic system might be “one which fulfills present and future needs while using, and not harming, renewable resources and unique human environmental resources of a site: Air, land, water, energy, mineral resources, and human ecology and/or those of other (off-site) sustainable systems” (p. 3). The SME CEO needs to take this on board mentally and then has to go about implementing changes to make sure this is translated into the management style and system of the organization.

Conclusion

A big gap exists between the laws and regulations enacted by the Egyptian government and their actual adoption and implementation by companies working in Egypt. Even when such laws, regulations, and policies are forced as a requirement for such companies to be able to start working, many companies find ways not to execute and adopt them. The reasons for such large gap are beyond the scope of this research but the fact stands that this is a big reality in Egypt. An extremely relevant example is the case with taxation. Almost all business and their legal accountants found, and still find, ways to circumvent much taxation, which resulted in a loss of billions of Egyptian pounds. For decades this has been the case until, all of a sudden, the government adopted another strategy that depended on deeply understanding people in every business sector, addressing all the range from very small to very large enterprises, focusing on the message that the government clearly understands their concerns and how to unthreateningly approach them. This illustrates the significance of understanding people’s characteristics, personalities, behavioral dimensions, and values to beget optimal results. Based on insights into business leaders and managers this campaign was a great success.

The above-mentioned case as well as the ongoing situation in Egypt encouraged the author to adopt the methodology in this research, to target personal factors rather than contextual factors. In Egypt, sustainability is still a subject that the government is just starting to approach. Moreover in Egypt, unlike in developed countries, public communities and business sectors are not giving enough attention to environmental issues because most are concentrating on profits and survival. For the government to be successful in enacting and implementing sustainability programs, which has long been a global concern, it needs to approach such communities and business sectors in a way similar to the taxation case, based on insightful and in-depth knowledge of leaders and senior managers. Another contribution would be advising the government and the business sector about which leaders’ personalities or attributes would fit such requirements for them to be able to hire such leaders. Leader attributes are suggested to be a rich and relatively immature field of research concerning sustainability and thus still requires further qualitative inspection and insights since it is unlikely that leaders share one and the same set of basic skills or personality traits. Hogan et al. (1994) highlight that some situations call for specific leader attributes in terms of personality and style. In other words, some attributes are particularly needed in specific situations. Sustainability issues might be one of those situational contexts that call for further inspection about leaders’ attributes, and supporting that line of thought is that different studies of qualitative nature came out with different attributes; the studies were conducted in different contexts in terms of industries and cultures. Additionally, SMEs (Perrini and Tencati 2007), the focus of this research, are more reliant on personal relationships between leaders, managers, and their subordinates in achieving their goals and enacting their strategies, emphasizing the role of leader attributes in moving the whole organization to whatever goals are set, highlighting the importance of such leaders being sustainability oriented to enact sustainability programs, which further requires inspection concerning leaders’ attributes (personal characteristics, values, beliefs, convictions) that most fit such endeavors. Large companies, on the contrary, as highlighted by Perrini and Tencati (2007), depend mainly on the organizational system, policies, and models of application in enacting their operations and achieving their objectives and strategic intents. This does not emphasize reliance on leader attributes in larger organizations as is the case with smaller ones, which is again the focus of this research. Additionally, collectivistic cultures, where relations play a critical role, call for more emphasis on inspecting such attributes since such a dimension of the Egyptian culture lends more emphasis to the above argument about SMEs as highlighted by Perrini and Tencati (2007).