Chapter 3

Basic Accounting

INTRODUCTION

As I work on the new edition of this book, I’m constantly reminded of how much the industry has changed since the previous edition was released. When it comes to Accounting, what comes to mind immediately is how the size of the accounting department has exponentially grown by leaps and bounds. I know this dates me, but I remember that on the small to moderately budgeted features and television shows I used to work on, we always had a two-person accounting department — maybe three if it was a bigger show — the third person being a payroll accountant. On the last feature I worked on, there were 12 people in the accounting department (which included two payroll accountants and a construction accountant). It’s also fairly common now to send an advance person/accountant to each distant or foreign location to set up the department before the rest of the accounting team arrives. And I’ve heard that on big international studio films, it’s not unheard of to employ an accounting department of 25 to 30 people.

I asked some of my accountant friends why they think this is, and they point out that they’re under more scrutiny, that there are more reporting procedures than ever before — especially now that all the major studios and networks are owned by major corporations. More red tape and the fact that Enron and other high-profile corporate scandals have left us with an array of new anticrime and antifraud laws. Just look at how thick the start paperwork packets have become and at some of the items they contain — like Conflict of Interest and Standards of Business Conduct guidelines. Everything employees are given to read and sign dictates that they must perform their jobs by the book — and the book just keeps growing thicker and heavier all the time.

The accountant’s proverbial plate is overflowing these days with multiple rebates to apply for, cast and crews from multiple states and/or countries with corresponding reporting requirements, more shows shooting on multiple locations and sometimes more than one studio or financing entity to answer to. Not only have reporting procedures become more rigorous, but newer and more complex accounting systems are being used. And although long gone are the days when budgets were being done by hand, having the latest technology in budgeting software doesn’t necessarily make the process less time-consuming, because studios and producers now routinely request various scenarios on each budget. Accountants can be kept busy for weeks on end coming up with multiple versions based on different locations or combinations of locations. All in all, it appears that the more they can do, the more they’re required to do.

In a post-9/11 world, some studios have installed a system that allows them to check each new vendor against a terrorist watch list, and I recently heard that one studio is now doing criminal background and credit checks on all of the accountants they hire.

Another answer I received to my question as to why accounting departments have grown reflected a belief that when it comes to features was that many directors aren’t as prepared as they should be, and they change their minds often (I also know some producers who change their minds on a fairly regular basis as well); plus, they’re allowed to. So it’s not uncommon (especially on the larger studio pictures where schedules and budgets aren’t carved in granite) for schedules to increase, locations to change, scenes to be added, stunts and effects to become more elaborate, one unit to become two, two to become three or another high-paid producer to be brought onto the picture halfway through principal photography. And without a doubt, multiple changes of any kind ultimately add time and expense to a picture and increase the load of the accounting department.

Low-budget and ultra-low-budget shows still have rather small accounting departments, and one-hour episodic shows generally employ a four-to six-person accounting team, but the rather large staffs on the bigger features still amaze me.

This chapter won’t teach you how to become a qualified production accountant or how to budget your film. What is intended is for you to gain an understanding and appreciation of what a production accountant does, how an accounting department functions, how a budget is created and how costs are tracked. Defining the following responsibilities and procedures will help to explain how significantly large sums of money are handled, dispersed, accounted for and effectively managed to facilitate the needs of an entire production.

THE PRODUCTION ACCOUNTANT

On studio films, network shows and indies produced by established production companies, the accountant will work closely with both an in-house finance and production executive — the finance executive being the individual who often hires (or at least approves the producer’s request for the) accountant. On other shows, the accountant may deal directly with a representative of the completion bond company and/or the financing company. On a day-to-day basis, he or she works closely with the show’s producer. Having to essentially work for and answer to both the studio/bond company/financiers and the producer is one of the most challenging aspects of any accountant’s job — especially when the needs and interests of both parties aren’t always the same.

The accountant is responsible for contributing to the preparation of the budget, monitoring all costs incurred and is essentially the guardian of the production’s purse strings. They’re instrumental in opening the production’s bank account(s); are one of the signators on the bank account; are responsible for creating cash flow charts, daily hot costs and weekly cost reports; managing and supervising the accounting department; working with department heads in overseeing and managing their individual budgets and keeping the studio, producers, bond company (if applicable) and production manager constantly apprised of where the show is financially. The accountant is frequently asked to estimate how potential changes to the schedule, cast, sets or locations will in turn affect the budget (something that occasionally must be determined after the fact). Estimating how any given production-related decision or change will affect the budget requires a knowledge of pro-duction-related expenses, union rates and regulations, in addition to the ability to predict costs. (This often comes intuitively after a certain amount of experience in this position.) Offsetting overages created by overtime days and meal penalties, the accountant will often pull funds not being fully utilized from one account and transfer them to an account that’s over budget. If no amount of shifting money from one account to another can help the fact that the production is over budget, then the accountant will generally meet with the finance and/or production executive, producers and/or production manager to decide how to best remedy the situation. If there’s no choice but to remain on budget, such decisions may include cutting out a location, scheduling shorter days or even shaving a day off of the schedule if necessary.

Nowadays, accountants need to be conversant in incentive-speak and become thoroughly familiar with the incentive programs being offered in the states or countries where they’re working, so they can set up a system that properly tags and isolates expenses that qualify for all appropriate rebates and/or tax credits. And for those studios/ productions that track a show’s carbon footprint, they’ll likewise tag all fuel and utility expenses as well as receipts for harmful materials (such as those used to create explosions, for example). The same system of tagging and isolating expenses is required for costs relating to insurance claims.

Working on foreign locations and/or with international crews, the accountant may need to open and monitor various bank accounts in multiple currencies. If the accountant doesn’t purchase the foreign currency, then it’s generally done by someone within the studio, network or production company’s finance department who must monitor the exchange rate and anticipate when to buy and how much to buy at any one time. Once foreign currency is deposited into a bank account, the accountant is responsible for keeping track of how much is being spent in each currency and for submitting a request when additional funds are needed. The trick is to have little foreign currency left at the end of the shoot, because what’s not used must then be sold off.

In many cases, at least one additional accountant or assistant accountant from the country you’re working in should be hired to assist in paying local crew and vendors and in meeting local government and union obligations. They’ll also help you with cash flow projections in the currency of their country. When working on distant locations, it’s always a good idea to have at least one local on the accounting team who knows that state’s payroll regulations and local union guidelines. And while you’re at it, you may want to make it at least two locals, as it really does makes sense to hire a local accounting clerk rather than to bring one with — thus saving on airfare, housing and per diem. But no matter how many locals are hired, accountants almost always bring their first accountant along, because this is the person who knows the accounting system, how the studio, network or production company operates and what they expect.

For those interested in becoming a production accountant, it’s a position that doesn’t necessarily require a financial background. Having been a bookkeeper or being a CPA would be helpful, but isn’t mandatory. What is essential is having a fair amount of common sense. One can work their way up the accounting department ladder starting as a clerk, moving up to a second assistant or a payroll assistant, first assistant and then accountant. It’s a position that carries with it a great deal of responsibility and innumerable challenges. And it’s job that remains the same whether it’s on a $1 million show or a $250 million show. The only thing that changes is the volume and the size of your staff.

THE ACCOUNTING DEPARTMENT

As already stated, accounting departments have grown considerably over the past several years. But the basic structure of the department is comprised of the accountant, a first assistant accountant (there are sometimes more than one first assistant, especially on shows shooting in multiple countries), any number of second assistant accountants, a payroll accountant (or two), a construction accountant and at least one accounting clerk.

This department, headed by the production accountant, is responsible for opening vendor accounts; processing check requests and purchase orders; paying the production’s bills (accounts payable); processing payroll; dispersing petty cash; making sure studio or production company accounting procedures are being adhered to and that all state, federal, union and contractual obligations are being met as they come due. They also play a major role in preparing insurance claims.

When it comes to the dispersing of money on a production, it seems as if everyone’s in a hurry and everything is urgent. Some requests for cash or checks are indeed time-sensitive and needed immediately, but rush requests that aren’t crucial may stem from overzealous crew members. Part of the accounting department’s job is to prioritize the needs of the production and to make sure that payments are made in a timely manner. Responsible accounting, however, dictates that prior to any funds being dispersed, certain steps (safeguards) must be taken. The first is the auditing of the check request or invoice to make sure the charges are correct and fit within the perimeters of the budget. There must be substantiating backup as well, such as an original contract, invoice, purchase order or check request (the amounts of which must match the amounts on the contract, bid, request or invoice), and approvals must be obtained from the department head and production manager, production supervisor or producer. As a last measure, the check is generally signed by two different people (who first have to be located), making it impossible for any one person to issue funds without the other’s knowledge or approval. So should you find yourself in the position of the person asking, you’ll now (hopefully) have an appreciation for what the accounting department must go through before you can receive your emergency check.

HANDLING PAYROLL

Most productions rely on the services of a payroll company to handle the payroll for their staff, cast and crew, and these companies are set up to pay both union and nonunion employees. The payroll company becomes the employer of record, and being such, show employees are covered by their workers’ compensation policy. A payroll company’s fees will vary depending on the payroll company, your budget and your relationship with the payroll company. Charges have traditionally been negotiated at $10 per check for all above-the-line payments and a one-half percent fee based on the below-the-line payroll (although some companies are now using new payment models). The production company or studio will select the payroll company to be used, and the accountant will designate an individual to oversee all payroll matters. On larger shows, it would be a payroll accountant who would deal exclusively with payroll. On smaller shows, it might be a first assistant who would handle payroll along with other responsibilities. Whomever this individual is, she or he is responsible for the following: making sure that start paperwork for each employee is properly and promptly submitted; getting accurate in and out times for each member of the cast and crew — information that should be listed on the daily production report; making sure that hours listed on the production reports match employees’ time cards; knowing all local guild and union contracts, along with state and federal payroll guidelines; calculating time cards (cast, crew and staff); verifying that any sixth and seventh days worked had been preapproved; flagging any irregular or suspicious time cards and bringing them to the attention of the accountant and/or production manager; submitting production manager— approved weekly time cards to the payroll company in a timely manner and approving the payroll company’s audit on Wednesday (or the third day of the shoot week) before checks are cut and issued on Thursday (or the fourth day of the shoot week) or Friday (or the fifth day) when on distant location due to the time that may be needed to ship the checks to location. This individual also tracks the payment of all box rentals, per diems, mileage reimbursement and car allowances; deals with actors’ agents on cast payroll issues and answers all payroll-related questions from crew members. Working closely with the payroll company, it’s necessary to make sure the payroll checks are ready on time, that they’re prepared correctly, that errors are quickly remedied and that all appropriate union and guild hours and fringes are reported and submitted as required.

PAYROLL COMPANIES

Few productions still handle their own payroll, because using a payroll company makes so much sense. Above and beyond cutting payroll checks, payroll companies pay all appropriate payroll taxes and union benefits, report union hours, provide workers’ compensation insurance, pay residuals, issue W-2s, provide the accounting system for their clients’ shows and handle trust accounts for child actors. They’re signatory to all the unions and guilds, have a labor relations department that’s made available to their clients, and advise on all matters relating to incentive programs.

Each of the major payroll companies (such as Entertainment Partners and Cast & Crew) license accounting system software (on a show-by-show basis) to the studios and production companies they do business with. This system interfaces with your show’s payroll and allows the accounting staff to input accounts payable, purchase orders, petty cash expenditures, etc. It generates reports such as general ledgers, trial balances, check registers, cost reports and a “bible” (a history of all the accounting transactions on your production). It wouldn’t be practical to use one payroll company to handle a show’s payroll and to license the software package from another, as it makes sense to be able to download the production’s payroll records onto the software program being used.

ACCOUNTING GUIDELINES

Start Paperwork Packets

On their first day on a new show, crew members are given a packet of paperwork. This packet (which keeps growing in size) may include some or all of the following:

• A blank deal memo form (to be approved by the UPM after it’s completed)

• An additional DGA deal memo form for DGA members

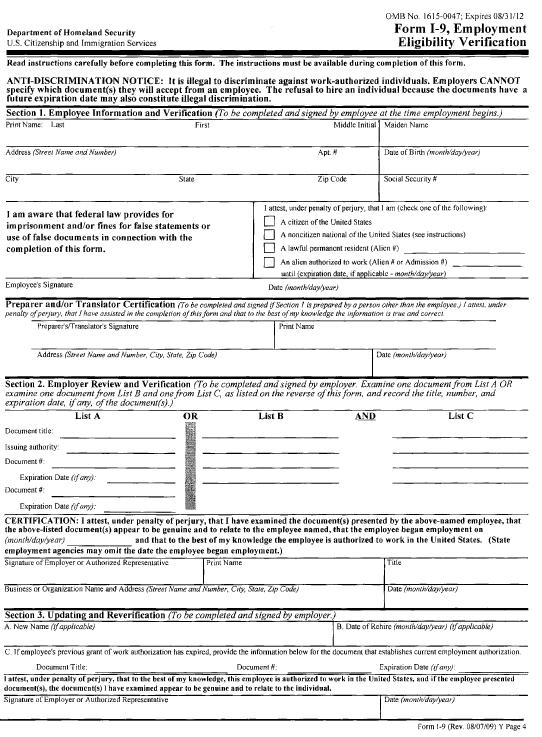

• Payroll company’s Start/Close form (regular or loan-out); regular Start/Close forms contain a U.S. Immigration I-9 Form at the back

• If the employee is a loanout: an Inducement Form & W-9

• A blank time card l Filmmaker’s Code of Conduct

• Request for insurance beneficiary designation/emer gency contact/doctor information

• Crew Info Sheet (to be completed and kept on file in the production office)

• Injury and Illness Prevention Program (IIPP), which includes a set of safety procedures

• Acknowledgement of Safety Guidelines l Travel Policy Acknowledgement/Travel Accident Form

• Environmental Guidelines

• Standards of Business Conduct see Chapter 9 for more information on this)

• Standards of Business Conduct Acknowledgement

• An Accounting Procedures Memo (this will generally cover procedures pertaining to payroll, box rentals, vendor accounts, competitive bids, purchase orders, check requests, petty cash, assets, automobile allowances, mileage reimbursement, invoicing and additional taxable income)

• Box Rental Inventory form

• Blank Box Rental Invoice form

• Car Allowance form

• Discrimination and Sexual Harassment Policy

• EEOC (Equal Employment Opportunity Commission) Form (acknowledgement of federal employment discrimination laws)

• Personal Vehicle Release

Payroll

Certain studios, networks and production companies have specific salary ceilings for crew and staff that can’t be exceeded, except by executive approval. This is information the line producer, UPM, production supervisor and accountant will receive before hiring begins. Unless dictated by union or guild guidelines, few production companies will guarantee an employee a set period of employment. Some will negotiate a guaranteed number of daily hours, but for a nonexempt employee, approval is generally required for anything more than an eight-hour day. Although most of the crew is paid by the week, weekly rates are prorated on a daily basis for partial weeks worked.

A nonexempt employee is hired on an hourly basis, whereas someone paid on a weekly flat rate is considered “exempt” from overtime. Exempt employees are also considered on-call — employees hired on a weekly basis with no minimum or maximum guaranteed hours of employment — guaranteed only a number of hours submitted for purposes of pension and health contributions.

For union shows originating from the West Coast, certain categories of union/crew members must be cleared through the Industry Experience Roster (IER) prior to their employment. The IER encompasses more than 125 job classifications, which span the jurisdiction of 19 unions within the motion picture and television industry. Those on the list have acquired a certain level of work experience within their specific craft and are members in good standing of their respective locals.

A member of the accounting department is usually responsible for going to the Contract Services Administration Trust Fund website (www.csatf.org) to verify that the names of new hires are on the IER. If a union crew is being hired in other parts of the country, be sure to check out the local requirements for verifying the union status of each new hire.

All individuals are subject to withholding of applicable federal, state and local taxes — except those with loanout corporations. Under these circumstances, the corporation “loans out” the employee’s services to the production company, the employee’s compensation is paid directly to the corporation, and the corporation is responsible for all applicable payroll taxes. Most studios dictate which positions can be paid as a loanout through their corporations, and they generally include the actors, writer(s), director, producer(s), casting director, director of photography, production designer, costume designer, editor, stunt coordinator, sound mixer and music composer. Those who qualify are asked to complete a Loanout Agreement and Inducement form and provide the accounting department with a stamped copy of their articles of incorporation. The corporation must also be qualified to do business in the state in which the production company operates, or state income taxes are assessed.

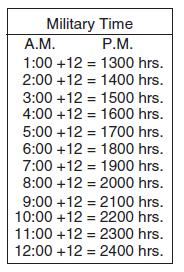

All employees (those subject to withholding as well as loanouts) must complete a U.S. Immigration I-9 Form (substantiated with a valid driver’s license and social security card, birth certificate, U.S. passport or alien registration card). Time cards are due at the end of the last working day of the week. They must include the employee’s name, project name and social security number or tax ID number — clearly printed. While indicating actual hours worked and the time taken for meals, the use of military time is preferred. On union shows, the hours worked are calculated by tenths, where each six-minute period is one-tenth of an hour. The following figures will help you reference military time and tenths.

FIGURE 3.1

FIGURE 3.2

Time cards must be approved by a department head prior to being turned in. Those not turned in on time may result in late paychecks.

Paychecks are issued on the fourth work day of the following week — usually Thursday (or Friday if Monday was a legal holiday or if the company is shooting on a distant location). If there’s an error on a paycheck, it should be politely discussed with the production accountant or payroll accountant on any day except time card day (the first day of the work week), as this is the deadline to get time cards to the payroll company if Accounting is to get the paychecks back in time. If there’s a valid error on a check, the payroll company will be contacted and the adjustment made. If a cast or crew member approaches the accountant or another member of the accounting department as if they’re trying to cheat them out of their hard-earned money, they’ll be anything but cooperative in helping to rectify the problem. Most payroll errors are inadvertent mistakes (often made by the payroll company) and are easily corrected. If the perceived error concerns a differing interpretation of a deal, rate, hours or union-related issues, it should be cleared up by discussing it with the person who approved the original deal (the line producer, production manager or production supervisor).

Note the illustration up ahead that will show you how to correctly fill out a time card.

Box Rentals

Those who have an approved deal that includes a box rental must complete an itemized inventory of the box/ kit contents. They should check with Accounting regarding whether this payment can be included on their weekly time card or if they need to invoice for it. (See Box/Equipment Rental Inventory Form.)

With regard to box rentals for computers, the standard industry payment has been $50–$100 a week, but now the standard includes a standard cap of $1,000 per show. Furthermore, some studios and production companies allow a computer rental fee only for certain individuals, like the assistant directors, production coordinator and assistant coordinator, art department coordinator, location manager, script supervisor and assistant editor.

Vendor Accounts

At the start of a new show, some studios and production companies will supply their production personnel with a list of preferred vendors they’re expected to use — vendors who have negotiated set (usually discounted) rates for all shows being done by that studio or production company. Other studios and production company executives understand that the production personnel on their shows may have solid, long-standing relationships with certain vendors, which they’re fine with — as long as they use established and known vendors whose prices are competitive. But even when the production isn’t required to use certain vendors, the UPM, production supervisor and/or coordinator should check with the production or financial executive to find out:

• Which vendors the production company already has established accounts with

• Which vendors the company might have discounted

• Whether the production company has any vendor rental credits that could be transferred to your show

Even if the studio or production company has accounts with vendors the crew would like to use (and the production is still entitled to whatever discounts the company may have prenegotiated), Accounting may still be required to open new accounts for your particular show — especially if the show is being produced under a separate entity.

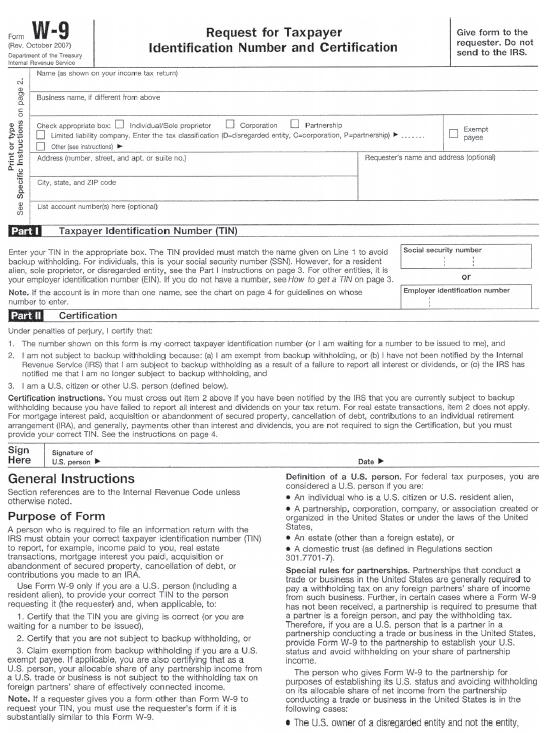

Once Production or individual department heads have a list of vendors they’d like to open new accounts with, that list should be given to Accounting and should include the vendors’ names, contact names, phone and fax numbers and e-mail address if possible and should indicate who in each department is authorized to make purchases/rentals on each account. No one should set up an account on their own, and vendors should be asked to fax or e-mail their credit applications to Accounting along with a completed W-9 (Request for Taxpayer Identification Number and Certification) form. Also inform all vendors that once accounts are opened, orders should not be accepted without a purchase order (PO).

All equipment packages should come with a rental agreement and/or contract that describes in detail the terms of payment, payment schedule, the cost of addons, insurance requirements, loss and damage settlements and the cost/terms of keeping equipment longer than anticipated due to schedule overages.

Competitive Bids

Most studios and production companies will require two or three competitive bids on all major purchases and rentals. This is almost always mandatory when it applies to the rental of equipment owned by department heads and other members of the crew, as it’s a conflict of interest for employees to have a financial interest in companies the production will be doing business with. So any rentals (or purchases) made from a crew member must be fully disclosed. The employee must have a valid company and provide the production with a formal rental agreement.

Each company will have their own guidelines as to which rentals or purchases require multiple bids. These typically include (but aren’t limited to): Camera, Grip, Electric and Sound Packages, Catering and Visual Effects. You’ll find a competitive bid form at the back of the chapter and will notice that it includes a section for explanation, if, for whatever reason, the lowest bid isn’t the one selected. Once the form is completed, copies of the three proposed bids should be attached to the back. The production executive, UPM and accountant should all sign off on the form, and the form (along with the attached bids) should be kept with the show’s financial files.

Purchase Orders

Use of purchase orders is Accounting’s most valuable method of tracking and forecasting costs. Most production companies so seriously and stringently enforce this policy that many refuse to pay invoices that don’t have purchase orders. If your accounting department doesn’t send out letters informing vendors of this policy, then it’s everyone’s responsibility to inform the vendors they’re working with that all invoices must reference a PO number. Also, never hold a purchase order until the corresponding invoice arrives. Department heads should sign off on all POS before submitting them for approval and should submit them as soon as possible so that the cost can be approved and accounted for.

Purchase orders must be used whenever possible for purchases, rentals and/or services with vendors the company has, or will have, an account with. If cash isn’t being used for a particular purchase or rental, and Accounting hasn’t already issued a check for it, it needs a PO. Purchase orders are obtained from the accounting department or production coordinator and must be completely filled out and approved before an order or purchase can be made. It must also be determined that the cost of this purchase, rental or service is covered within the confines of the budget. If the purchase order is for $500 or less, it’s generally approved by the production manager or production supervisor. If the purchase order is for more than $500, it may require the approval of a producer or studio executive.

When a purchase order number is received, it should be for the exact items and amount indicated on the PO. If additional items are added to an order at a later time, a new PO is needed, as the existing one can’t be altered once it’s been approved and submitted to Accounting. If it’s necessary to extend the date of a rental, some accountants will require a new purchase order, some will ask for a PO extension form and still others will prefer that the extended dates be written on a copy of the original PO and resubmitted.

Purchase orders must (legibly) indicate the name, address and phone number of the vendor, the vendor’s federal ID number (if the business entity is a corporation) or Social Security number (required by federal law), a detailed description of the work, materials ordered or items to be rented. If it’s for a rental, it must indicate when the rental begins and when it’ll end. Purchase orders should also include a set number if applicable. Once received by Accounting, each PO is coded based on the budget’s chart of accounts (see farther ahead for information on chart of accounts), so that each cost is attributed to the proper account.

An open-ended PO is rarely issued and will be allowed only under special circumstances and with prior approval. If the exact dollar amount of the purchase, rental or work is not known at the time the purchase order is issued, it should reflect an estimated amount that will not be exceeded. Any charge exceeding this amount must have prior written approval, and unapproved overages could be rejected.

If the PO is being issued by the production department, a copy should be made for the production files before submitting it to the accounting department. Accounting will obtain approval signatures (if not already signed) and distribute fully executed copies to the department head and vendor.

Accounting keeps its own log of purchase orders, and the production coordinator (or assistant coordinator) generally keeps a running log of the POS issued by the production office. This log should indicate the date, vendor, item(s) being purchased or rented, amount of purchase or rental, date of rental return and the department to which each PO is assigned. Also noted on the PO log are purchases that at the end of the show become part of the company’s asset inventory. As these costs are entered into the system, assets generally valued between $50–$100 are automatically scheduled on an ongoing asset list monitored by Accounting.

Check Requests

When a purchase order can’t be used and a check is needed right away, the process of obtaining that check begins by obtaining a Check Request form from the production or accounting department. After it’s filled out completely, the UPM or production supervisor must approve it before payment can be made and an original invoice, contract or other form of substantiation must be submitted to back up the request. If an original invoice hasn’t yet been received, ask the vendor to fax or e-mail you a copy; and attach that to the check request (noting that the original will be submitted as soon as it arrives). As with purchase orders, don’t hold up the check request process waiting for an original invoice.

Each check request should contain the following: vendor name, address, phone number, tax ID number or Social Security number, department/individual requesting the check, a set number (if applicable) and a description that includes as many of the following details as possible:

• Is this for a purchase, rental, service, location fee, petty cash advance or deposit?

• If it’s for a deposit, is it refundable or to be applied to the final bill?

• Is this a partial payment or the first of many?

• What are the terms of the purchase, rental or service?

• Is the check to be mailed or held for pickup?

• What’s the total amount to be?

• Specify date and time check is needed

If a check is needed immediately and the UPM or production supervisor isn’t present to approve the request, an effort should be made to locate him or her and to obtain verbal approval over the phone or via walkie-talkie. If the UPM or supervisor can’t be found, approval should be obtained from the producer or studio executive. Keep in mind, however, that as much as everyone hustles to get an emergency check out as soon as possible, Accounting still needs time to process the request and to obtain the necessary approvals and signatures. The process is rarely instantaneous.

Items purchased by check requests (with substantiating backup) for the purchase of tools, props, wardrobe, etc. (anything that can be considered a company asset) also becomes part of Accounting’s asset inventory log. Major assets should also be noted as such on your purchase order inventory log.

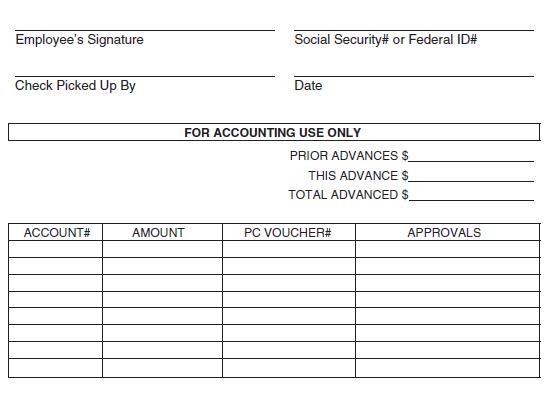

Petty Cash

Petty cash should be used for small purchases that aren’t covered by a purchase order or check request, generally for items such as fuel for company vehicles, parking fees, expendable supplies, small props and miscellaneous office supplies. Although most studios prefer petty cash to be used for items costing less than $100, most place a $200–$400 cap on receipts that can be paid in cash. Petty cash is requested via a Check Request form or a specific Request for Petty Cash Advance form that’s approved by the UPM. Those receiving petty cash will receive a check in their name (or actual cash, to be determined by the production accountant) and a petty cash envelope to keep track of all petty cash expenditures.

Anyone receiving a cash advance from another person in the company will need to sign a Received of Petty Cash slip acknowledging receipt of the cash. The person advancing the funds will also sign the slip. When petty cash receipts are turned in, it’s the responsibility of the individuals who had been given the cash to retrieve and discard the Received of Petty Cash slip, so they will no longer be responsible for the money.

Petty cash receipts (originals only) should be numbered and neatly taped to 8½ × 11 sheets of paper, in sequence, each clearly labeled as to exactly what it’s for. Use one side of the paper only, and don’t overlap receipts. Date and list the corresponding numbers on the front of the envelope, along with a description of each item. Use ink, and add your name and department in the appropriate spaces. If applicable, provide the set numbers that correspond to the purchases listed, and have department heads approve all envelopes being submitted from their respective departments.

All petty cash receipts are subject to approval, so the crew should be made aware of the regulations pertaining to petty cash expenditures imposed by the studio or production company – standard guidelines such as:

• If one individual advances any of his petty cash to other individuals, he is still responsible for all the receipts and for the collection of any outstanding sums.

• Services of individuals or casual labor must be paid through the payroll company and not through petty cash. In case of emergencies, however, or last-minute site rental fees, have the individual you’re paying write out a receipt that includes his or her name, address, telephone number, tax ID number or Social Security number and a signature for receipt of the cash. Examples of when this might be appropriate would be if Props or Set Dressing were to buy an item from an individual at a flea market or garage sale or a location manager would have to make a “courtesy” payment to a disgruntled resident in a neighborhood where the production is shooting.

• Some companies require receipts for gasoline charges to be identified by date, driver’s name, vehicle license plate, quantity purchased, price per gallon and gas station.

• Meals purchased with petty cash often require pre-approval from the UPM.

• It’s an IRS requirement that restaurant charges over $25 be submitted on credit card receipts, but the charge receipt alone isn’t sufficient. Also submit the detailed restaurant receipt that lists the food and drinks ordered.

• On the restaurant receipt — alongside each menu item, note the name of the individual who ordered that item.

• Restaurant receipts in the form of check stubs are no longer acceptable (at any company). If the restaurant eaten at or ordered form only takes cash and only offers receipt stubs, they should be asked to write out an itemized receipt and to staple one of their business cards to it.

• Receipts for cigarettes, cigars or alcoholic beverages for non-prop use will not be accepted. l Only original receipts are acceptable — no photocopies.

• All petty cash envelopes must be done in ink — not pencil.

• All receipts must have the vendor’s name, address telephone number imprinted or stamped on them (if not, once again, staple one of their business to it).

• Note any petty cash purchases that will become company assets (usually anything over $50).

• When cash or change is used for things there are no receipts for, such as parking meters or gratuities, a receipt should be made up noting what the expense was for and the date(s) incurred.

• If a receipt doesn’t clearly indicate what was purchased, a brief description should be written on the paper next to the receipt. Unclear, incomplete or illegible receipts will not be accepted.

• On each receipt, circle the date, vendor’s name and the amount of the purchase. Don’t use a highlighter for this, as the highlighter causes the printing to fade on certain paper receipts.

• Submit petty cash envelopes once a week or, ideally, when you’ve spent half of your money. Date, list and total all expenditures. Don’t seal the envelope. Once approved, the accounting department will either reimburse the total in cash or issue a check for the amount of the expenditures, keeping the initial draw (“float”) at the same balance. At the completion of principal photography or wrap, the balance of receipts and remaining cash must be accounted for before the person responsible for the petty cash leaves the show.

• Petty cash expenditures not accounted for by the end of one’s employment on a film will generally be deducted from that person’s final paycheck.

Tales from The Trenches

From my friend, Tom Udell

I had a large sum of money in a certain compartment of my briefcase. But I had a cough, and in Australia, where I was working at the time, they happen to have cough syrup with codeine in it, available over the counter. So on my way into work, I took a swig of cough syrup with codeine and then stuffed the bottle of cough syrup into my briefcase — as luck would have it, into the same compartment where I had the cash. Of course, the bottle leaked all over the cash, and I had to spend most of that night laundering money.

Lesson? I suppose the lesson is that if you get involved with drugs, you’d better be prepared to launder your money.

Online Purchases

The rules got a bit blurred when certain department heads started making online purchases for items needed right away and/or for things that couldn’t be found elsewhere and neither petty cash nor submitting a check request were practical. Depending on the studio or production company, these situations are all handled a bit differently. Some productions will issue debit cards (and some debit cards are supplied by the payroll company) and some studios will issue American Express cards, but they’re only given to a couple of departments, like Costume and Set Dressing. The accountant is also given a debit or credit card for emergencies. For those who have and use company debit or credit cards, they submit their expenses and receipts in a petty cash envelope (just like petty cash), but at the top of the envelope they write DEBIT CARD or CREDIT CARD. Anyone else (not approved to have a company-issued debit/credit card) who makes online purchases must use her own credit or debit card and then submit a check request for reimbursement.

Studios will selectively issue a certain number of debit or credit cards, but on independent films, this is generally done through the payroll company. These companies put the money up in advance (made payable to the payroll company), and the cards are issued with fixed limits.

Cell Phone Reimbursement

This industry utilizes different methods of reimbursement when it comes to personal cell phone use. Each production should establish its own policy, and make sure it’s known to all those who plan to use their own phones for business purposes. No one should be reimbursed for personal cell phone charges without preapproval. Some companies reimburse only up to a certain dollar amount (I’ve seen it anywhere from $75–$200). Other productions will ask individuals to determine what percentage of their bill is work-related and then pay that percentage.

When requesting reimbursement for work-related calls, either from a personal cell phone or home (land) line, original phone bills should be submitted (not photocopies), and all work-related calls should be highlighted or circled and totaled. The bills should then be attached to a completed check request form and submitted to Accounting. Petty cash can’t be used to reimburse crew members for cell phone charges.

Auto Allowances

Some negotiated crew deals (primarily those of department heads) include a weekly auto allowance (amounts vary depending on the show, budget of the show and anticipated use of the individual’s vehicle). IRS regulations require car allowances to be paid through Payroll and are subject to income tax withholding.

Mileage Reimbursement

Production assistants are the most common recipients of mileage reimbursement, because part of their job requires them to use their own vehicles to make production-related “runs.” The most common form of reimbursement is made by paying a predetermined rate per mile. Some companies choose to refund gas receipts instead.

To qualify for a per mile reimbursement, one should fill out a Mileage Log, indicating a beginning mileage, destination, purpose and ending mileage for each run. Estimated mileage isn’t acceptable. Mileage to and from home isn’t reimbursable. And employees who receive mileage reimbursement aren’t reimbursed for gas receipts.

In order to be reimbursed for mileage expenses, a completed Mileage Log should be submitted to the UPM, production supervisor or production coordinator for approval. Once approved, the production office will pass it on to Accounting for payment. Some companies include mileage reimbursement in weekly payroll checks. Others require approved mileage logs to be submitted with a check request, and payment is made through Accounts Payable. Requests for mileage reimbursement should be submitted on a weekly basis. If your company reimburses gas receipts, this is generally done through petty cash.

Drive-To

Drive-to is another form of mileage reimbursement paid to cast, crew and background talent for reporting to a local location. The mileage is determined by calculating the distance from the studio or production office to the location and back and multiplying that distance by an amount determined by individual union/guild contracts. Daily mileage to and from a location (or “report-to”) site is recorded on the daily production reports. At one time, individuals would sign for their drive-to money and receive cash on the set on a daily basis, but IRS regulations now require a week’s accumulated drive-to to be added to each person’s time card and paid through Payroll. If the amount per mile is more than what the IRS allows, that amount is subject to income tax withholding.

Per Diem and Living Allowance

Per diem is an amount of money paid to cast and crew members to cover their food/meal expenses while on location. SAG rules specify a minimum amount to be paid to their members (check your SAG agreement for the current rate), the DGA requires that its members be paid per diem plus an additional amount (it’s presently $17) for incidentals (like laundry) and the IRS imposes minimum allowable amounts per city. Producers generally choose rates of per diem based on the average cost of meals (breakfast, lunch and dinner) at a particular location (never less than the minimum requirements). Also taken into consideration are contractual obligations, negotiations with individual agents representing key department heads, and of course the show’s budget. But it’s not unheard of for crews to be paid $50 a day when working on a show in Baton Rouge and $100 a day when working in Manhattan.

The production is technically not responsible for paying per diem for meals served on-set (usually lunch), but many producers choose to pay per diem that covers three meals a day anyway.

While on distant location, per diem is usually paid in cash at the end of the week for the following week. (Sometimes, on long location shoots, crew members will open temporary accounts at a local bank, and their per diem is transferred directly into their accounts.) Scouting trips to distant and foreign locations are different, though, and in these situations, the production will generally reimburse for all customary travel-, food-and lodging-related expenses as well as reasonable gratuities.

A living or housing allowance is given to those who choose not to live at the production-chosen/based hotel on location, and the amount given to someone on the cast or crew is equivalent of what the production would pay for that individual’s room per night at the hotel. Living allowances are sometimes paid in advance a week or more at a time, but some companies will include it (a week at a time) in with the weekly paychecks. And as with the paychecks, payment is received the Thursday after the week its being received for. For those who choose to make their own housing arrangements, the production is not responsible for deposits, leases or damages to their rental unit.

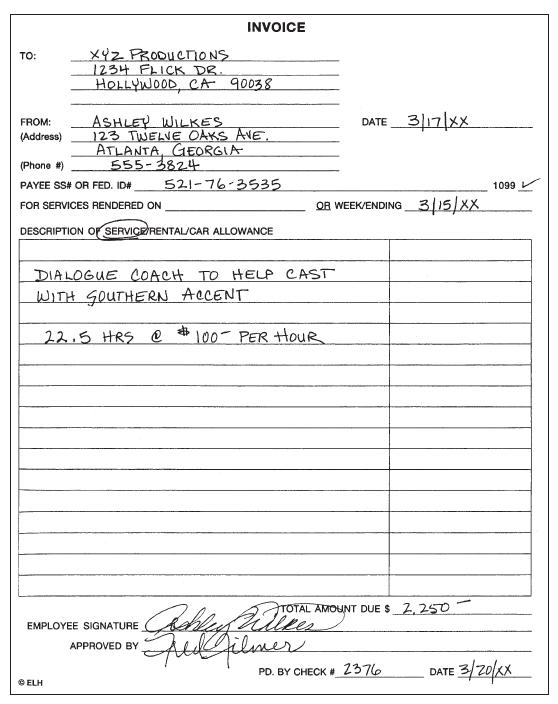

Invoicing

Crew members should submit their invoices for services, equipment/ box rental, vehicle rental, car allowance or mileage reimbursement at the end of each week for payment the following week. Each invoice must include the employee’s name, his corporation name, address and Social Security number (or tax ID number). A complete description of what the invoice is for (i.e., services rendered or equipment rental) and a week-ending date must also be indicated on the invoice. All invoices are approved by the UPM or production supervisor before payment can be made.

Additional Taxable Income

The federal government has set an allowable limit for mileage reimbursement, drive-to and per diems. Any amount over such limit (see your accountant for limit guidelines) is considered taxable income and will be taxed along with the weekly payroll checks. Box rental fees are also considered taxable income but are generally not taxed on a weekly basis when a detailed inventory list is provided and an invoice is submitted weekly. Those receiving box rentals will receive a 1099 at the end of the year and will be responsible for the taxes on this additional income.

THE BUDGET

Each budget starts with a top sheet, which is a summary of the budget categories. The accounts are broken down into above-the-line or below-the-line categories. Abovethe-line includes: the story rights, script, writer(s), producer(s), director, cast (including casting, bits and stunts) and above-the-line expenses. Below-the-line refers to all production and post production expenses (or sometimes shooting period, completion period and miscellaneous other expenses). The top sheet indicates each account, on what page in the budget the detail can be found and the budgeted amount for that account. Lastly, above-the-line and below-the-line costs are added together to form a grand total for the entire budget.

FIGURE 3.3

Each account has an account number, which is listed along the left-hand column of each page. After the two-page top sheet, the budget is broken down and detailed by subaccounts. For example, if Production Staff is Account #20-00, then the Unit Production Manager might be #20-01, the First Assistant Director, #20-02, and so on, although the subnumbers don’t always follow consecutively. A Chart of Accounts is a list of all account and subaccount numbers and is used for the purpose of coding all production-related expenses on purchase orders, check requests, invoices, petty cash purchases, payroll entries, etc. Although the budget format is generally the same, master account numbers vary depending on the studio or production company. Each uses its own budgeting format.

So much goes into the preparation, modification and monitoring of the budget, that the goal is be able to keep a firm grasp on exactly where the show is financially on any given week (if not day). The size of a budget doesn’t matter. It should be apparent however if, when, where and how the project is going over budget, and if necessary, when it’s time to bring it back under control.

Here’s what a portion of a chart of accounts might look like:

FIGURE 3.4

Preliminary Budgets are often done prior to a project ever being sold or picked up and are usually based on a first or early version of a script. They reflect how much a particular script will cost to produce and can be a major contributing factor to selling (or not selling) the project.

The first budget is prepared in conjunction with a script breakdown, production board and schedule, and the process begins as this data is translated into: man hours, pay scales, cast salaries, location fees, anticipated rentals, etc. Although some individuals create budgets straight from the script, the budgeting is considerably more accurate when based on a shooting schedule. Also, the more variables that are provided up front, the more precise the budget will be. These variables would include knowing such things as whether this is a union or nonunion film, which format it’s to be shot in, which actors are being considered for specific roles, where the film’s to be shot, etc.

A budget is an estimate based largely on the experience of the person preparing the budget. Anyone can look up costs, but a somewhat seasoned production manager, accountant or estimator will intuitively know where to factor in costs not always found in books or on pay scale charts. As capable as the preparer is, however, there are always unexpected circumstances that will arise to alter the budget. That’s why, whenever possible, budgets include “pads” (certain line items in the budget where you can inconspicuously forecast slightly higher costs and rates for items/ crew you know will cost less) and/or “contingencies” (generally, an additional 10 percent of the total budget) to accommodate for those unforeseen overages.

If a completed budget is determined insufficient to make the film as envisioned, then compromises have to be made. From a budgetary standpoint, this is where pads and contingencies (or portions thereof) are removed. Changes can be made to the script to reflect smaller sets, fewer locations, fewer cast members, etc. Other compromises might include using a less expensive cast, shooting in less expensive locations, using a smaller crew or making this a nonunion instead of a union film. Not until the budget reasonably reflects the agreed-upon scope of the production is the project going to receive a green light.

Most budgets go through several incarnations during development and pre-production as locations are changed, one actor is replaced with another and the writer adds, deletes or changes scenes. Budgets are also refined during this period as department heads research and anticipate their specific needs. If something is going to cost more than originally anticipated, and it’s agreed that incurring this additional cost will benefit the film, then either permission is required from the investor(s), studio, network, company or agency to increase the budget or other costs must be reduced to accommodate the overage.

Before the budget is finalized, department heads should feel confident that (barring any unforeseen circumstances) they can operate within the boundaries of their departmental budgets; and the line producer and UPM should feel confident that they’ll endeavor to do so.

During pre-production, the accountant prepares a Cash Flow Chart for the investor(s), studio or production company. This schedule divides the total amount of the budget by how much cash will be needed to operate the production during any given week from the beginning of pre-production through post production and delivery. Each week, the figure varies depending on the size of the cast and crew that week; whether it’s a prep, shoot or wrap week; whether the company is filming on location and so on. As in the budget, a Cash Flow Chart is an estimate. It’s the accountant’s best guess as what will keep the company operating on a week-to-week basis. Some companies will use this as a schedule for depositing funds into the production’s bank account(s).

The final budget is the one everyone agrees to adhere to, and the studio executive, producer, production manager and accountant are asked to sign off on. This means no more changes or additions are allowed that will add to the budget, unless they’re studio-approved. It happens occasionally that a production manager or accountant feels that it’ll cost more to do a picture than what the studio is allowing, and the studio isn’t willing to make the necessary changes to accommodate the difference. In these situations, someone will occasionally choose not to sign off on the budget.

Nonapproved overages from then on are deficit financed by the studio or production company or taken from other (underutilized) areas of the budget. If neither of those options is feasible, then production-and/or post production — related cuts are made to make up for the overage. If a completion bond company is involved, and the picture has gone over budget, the bond company may have the right to take over the management of the film.

TRACKING COSTS

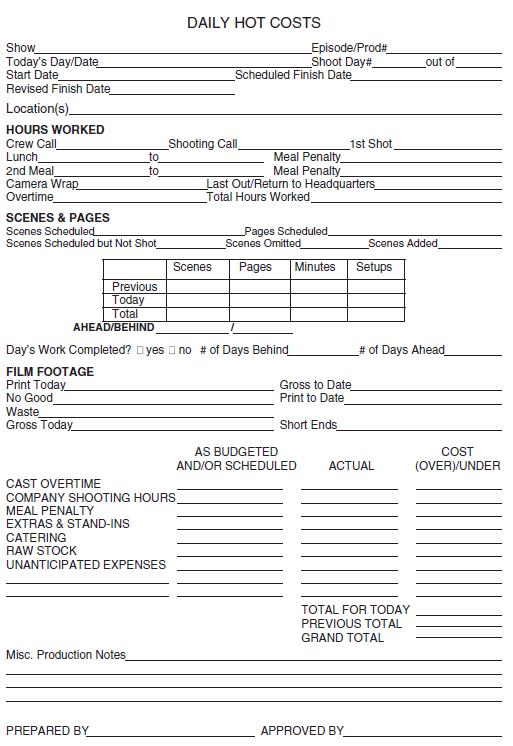

Daily Hot Costs represent an analysis of how much was spent versus what was budgeted and/or scheduled for. Most accountants do a hot cost analysis based on each day of principal photography. It may also be called a Daily Cost Overview. This report indicates what was budgeted and/or scheduled for that day: the number of scenes, the number of pages, cast overtime, company shooting hours, meal penalty, catering and use of raw stock. There’s a second column to indicate actual figures and then a third to indicate the variance. These figures are fed into the accounting system by account, keeping the status of the budget as current as possible. Conscientious departments heads often keep track of their own daily hot costs.

All expenses entered into the accounting system are used to produce Weekly Cost Reports (or Estimated Final Cost Reports). A cost report details each account listing: total cost to date, cost to complete, estimated final cost, what was budgeted and the variance. These reports continually provide you with the latest financial status of your film. The following is what the above-the-line portion of a cost report top sheet might look like, and as noted earlier — the account numbers will vary depending on the studio or production company.

In a perfect world, if an accounting department is set up and run properly, there should be no excuse for not knowing the financial status of a show on a weekly basis. Unfortunately, sometimes a lack of information from a producer or UPM (either on purpose or inadvertent) and pressures from a producer for one reason or another to inflate or deflate costs will make this difficult. When everyone’s on the same page, though, the figures are there.

As a working (or potential) production professional, or someone who wants to become a production accountant, knowing how to accurately budget a film and how to use a good budgeting software program, (such as Entertainment Partner’s Movie Magic) is an incredibly valuable asset. There are several good books on the subject and classes available that do just that. One such book I highly recommend is: The Budget Book for Film and Television by Robert J. Koster (Focal Press).

FIGURE 3.5

THE AUDIT

Internal audits of shows are performed by a team — generally two or three professional accountants, who work for the studio or production company’s parent company. Just like IRS audits, not all shows are targeted, and of those that are, their accounting staff is generally given notice to be ready for an audit within 30 days. Audits generally occur during principal photography, and once the auditors arrive, the process itself generally takes five to ten working days. Upon completion of the audit, the studio and production receive a graded report based on the auditors’ findings.

The auditors’ job is to evaluate the procedures and effectiveness of the accountingdepartmentbyinterviewingkey personnel, reviewing files and specific documents, following transaction flows and reviewing certain departmental processes. They’ll randomly select documents (POS, contracts, check requests, petty cash envelopes, etc.) to see whether they contain proper: supporting documentation, authorizations, coding, flagging of assets, signatures, reimbursements, completions, etc. (Note that accounting staffs are now routinely scanning all documents, so that originals can be left for audit purposes in the country or state of origin, yet still allowing the studio to have access to all documentation.)

Auditors generally assess areas such as above-the-line contract approval and administration; budget preparation, approval and monitoring; cost report preparation and approval; bank reconciliation and petty cash administration; trial balance closing and reconciliation; payroll processing and per diem administration; procurement and accounts payable; asset/inventory management; union reporting compliance and employee box rentals. They also look at costs to date compared to the final budget.

The auditor’s reach affects production as well with regard to procedures that relate to product placement, competitive bidding, call sheets and production reports, film stock totals, talent contracts, box rental inventories, travel guidelines, proper completion and submission of union and guild report forms, matching time card and production report hours and more.

Audits also now include compliance with incentive programs (the various rebates and tax credits being offered by states and countries) as well as adherence to the U.S. Foreign Corrupt Practices Act (see more about this federal statue in Chapter 20).

Their reports generally consist of an overall assessment and as well as specific observations and suggested plans of action to correct whatever deficiency or problems they find. Suggestions may include a more detailed explanation of certain guidelines in the company’s production or finance manual, adding to or changing policies stated in the employees’ start paperwork packets or on crew deal memos, instituting new guidelines or requiring additional authorizations.

My sincere thanks to Jim Turner and Tom Udell for helping me revise and improve this chapter — and to Terry Edinger and Cindy Quan for answering all the questions I kept throwing at them.

FORMS IN THIS CHAPTER

• Box/Equipment Rental Form

• Box/Equipment Rental Invoice

• Car Allowance Rider — to be completed by those individuals given a flat weekly car allowance as part of their deal

• Cash or Sales Receipt — generic form that would most commonly be used at the end of a show when assets (left-over raw stock short ends, props and set dressing, office supplies, etc.) are being sold

• Check Request

• Competitive Bid Form

• Crew Data Sheet — this is not a standard form, and this information can be found on Accounting’s software system, but as a production coordinator/supervisor, I find it helpful in keeping track of crew members’ start and wrap dates and in making sure everyone’s paper work is turned in to Accounting

• Daily Hot Costs — used by the production accountant and others to assist them in staying on top of costs and managing the budget

• -9 Form (issued by the U.S. Department of Justice) — to be completed by all employees (this form can be downloaded from the Internet)

• Individual Petty Cash Account

• Inducement — to be completed by a loanout (along with a Loanout Conversion Agreement) and accompany a W-9 form

• Invoice — generic form that can be used for any invoicing purpose

• Loanout Conversion Agreement — for employees who work as loanouts, this is to be submitted along with the individual/artist’s agreement and an Inducement form and W-9

• Mileage Log — mainly used by production assistants, but can be used by anyone who gets reimbursed for mileage when driving his or her own vehicle for production-related purposes

• Personal Vehicle Release — to be filled out by anyone who will be using their own vehicle for business purposes and will be reimbursed for mileage or gas receipts

• Petty Cash Accounting — you can attach this form to the front of an envelope, or buy petty cash envelopes with this (or one of a few other standard formats) printed right on the envelope

• Purchase Order — usually on NCR paper with four or five (different-colored) pages, printed with sequential numbers in the upper-right-hand corner of the page and the name of the production, production company, insurance agency, so they have more complete infor address and phone number in the upper-left-hand corner of the page and the name of the production, production company, address and phone number in the upper-left-hand corner of the page

• Purchase Order Extension

• Purchase Order Log

• Received of Petty Cash — these usually come in pads and can be purchased at any stationery or office supply store

• Request for Petty Cash Advance

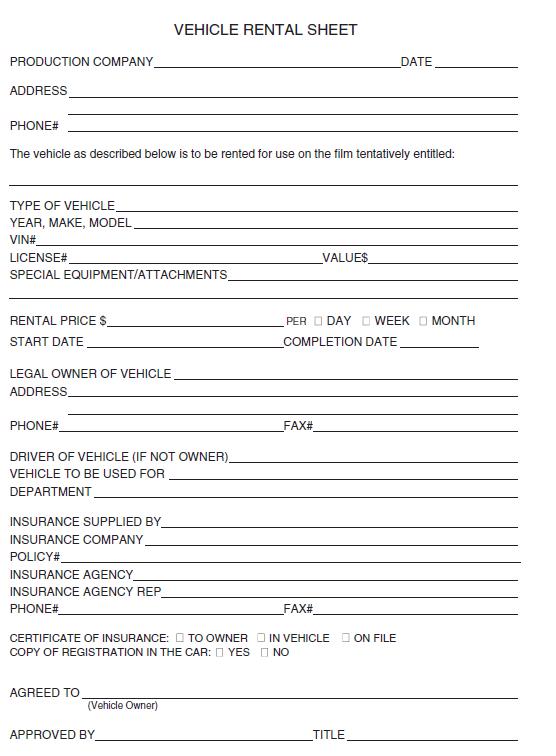

• Vehicle Rental Sheet — not a standard form, but it should be. Keep one on file for every vehicle being rented for your show and attach copies to respective certificates of insurance being forwarded to your insurance agency, so they have more complete information when scheduling the vehicles for coverage.

• Vendor Credit Request — to be filled out by department heads who wish to have accounts opened with various vendors

• W-8BEN Form (IRS) Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding — to be filled out by non-U.S. citizens subject to U.S. tax on income they receive from working for a U.S. company (this form can also be downloaded from the Internet)

• W-9 Form (IRS) Request for Taxpayer Identification Number and Certification — to be completed by all vendors (this form can also be downloaded from the Internet)

Please note:

1. Box rental rates are paid for actual workdays only.

2. The production is not responsible for any claims of loss or damage to box/equipment.

3. Box rental fees are not to be listed on weekly time cards. An invoice must be submitted to Accounting on a weekly basis, and payment will be remitted weekly.

4. Box rentals are subject to 1099 reporting.

5. The production must be provided with an inventory of box rental items, which can be listed below or attached to this form. Please indicate all make, model and serial numbers.

Inventoried Items:

BOX/EQUIPMENT RENTAL INVOICE

CAR ALLOWANCE RIDER

Car allowance shall only be paid for days actually worked and will be pro-rated on a weekly basis.

Employee must carry his or her own automobile insurance coverage (liability and physical damage), and neither the production’s insurance nor that of its parent companies shall apply to any claims, loss or damage related to the use of Employee’s car. At the request of the production, Employee must provide proof of adequate insurance coverage.

Employee understands that he or she is prohibited from using his/her cell phone or texting while driving. Should it be necessary to use a cell phone while driving, employee agrees to use a hands-free device and dial by voice command or while the vehicle is safely stopped.

While receiving a car allowance, gas receipts and/or mileage will not be reimbursed.

Car allowance is taxable income, and car allowance fees should be indicated on Employee’s weekly time cards.

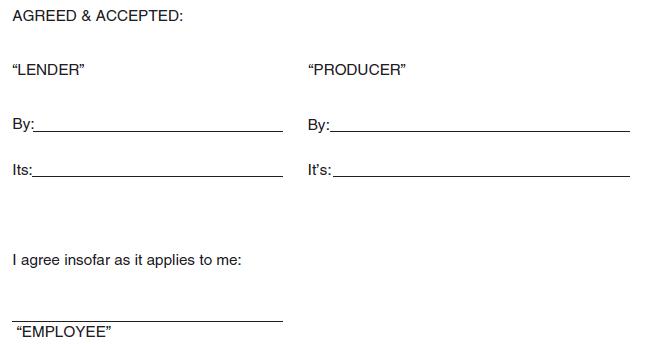

INDUCEMENT

Reference is hereby made to that certain agreement (“Agreement”) dated as of [DATE], is made between [NAME OF PRODUCTION ENTITY] (“Company”) and [NAME OF LOANOUT ENTITY]. (“Lender”) f/s/o [NAME OF INDIVIDUAL] (“Artist”) for Artist’s services as [POSITION OR ROLE] in connection with the motion picture entitled “[NAME OF PROJECT]” (the “Picture”).

A. I am familiar with all of the terms, covenants and conditions of the Agreement and I hereby consent to the execution thereof. I shall perform and comply with all of the material terms, covenants, conditions and obligations of the Agreement, even if the employment agreement between me and Lender should hereafter expire, terminate or be suspended. I hereby confirm all grants, representations, warranties and agreements made by Lender under the Agreement.

B. Unless I am deemed substituted for Lender as a direct party to the Agreement pursuant to paragraph D below, I shall look solely to Lender and not to Company for the payment of compensation for my services and for the discharge of all other obligations of my employer with respect to my services under the Agreement.

C. In the event of a material breach or threatened material breach of the Agreement by Lender or by me, Company may join me in any action against Lender without being first required to resort to or exhaust any rights or remedies against Lender.

D. I represent that Lender is a duly qualified and existing corporation under the laws of its state of incorporation. If Lender or its successors in interest should be dissolved or should otherwise cease to exist, or for any reason should fail, refuse or neglect to perform, observe or comply with the terms, covenants and conditions of the Agreement, I shall, at Company’s election, be deemed to be employed directly by Company for the balance of the term of the Agreement upon the terms, covenants and conditions set forth therein.

E. I will indemnify Company for and hold it harmless from and against any and all taxes which Company may have to pay and any and all liabilities (including judgments, penalties, fines, interest, damages, costs and expenses, including reasonable outside attorneys’ fees) which may be obtained against, imposed upon or suffered by Company or which Company may incur by reason of its failure to deduct and withhold from the compensation payable under the Agreement, any amounts required or permitted to be deducted and withheld from the compensation of any employee under the provisions of the federal and applicable state income tax laws, the Federal Social Security Act, the applicable state unemployment insurance tax laws, and/or any amendments thereof and/or any other applicable statutes heretofore or hereafter enacted requiring the withholding of any amount from the compensation of an employee.

F. If Company shall serve Lender with any notices, demands or instruments relating to the Agreement, or to the rendition of my services thereunder, service upon Lender shall also constitute service upon me.

G. For purposes of any and all Workers’ Compensation statutes, laws, or regulations (“Workers’ Compensation”), I acknowledge that an employment relationship exists between Company and me, Company being my special employer under the Agreement. Accordingly, I acknowledge that in the event of my injury, illness, disability or death falling within the purview of Workers’ Compensation, my rights and remedies (and those of my heirs, executors, administrators, successors, and assigns) against Company or Company’s affiliated companies and their respective officers, agents and employees (including, without limitation, any other special employee and any corporation or other entity furnishing to Company or an affiliate Company the services of any such other special employee) shall be governed by and limited to those provided by Workers’ Compensation.

H. I acknowledge and agree that the results and proceeds of my services hereunder (“Results”) shall be “works made for hire” (for the purpose of U.S. copyright law and all other copyright laws throughout the universe) with all rights (copyrights, rights under copyright and otherwise, whether now or hereafter known) and all renewals and extensions of such rights as may now or hereafter exist, to be vested initially in Lender and assigned to Company. If or to the extent for any reason in any country, such Results are not recognized to be a “work made for hire” then I hereby irrevocably and absolutely assign to Lender (and Company as Lender’s assignee) all of my respective rights (copyrights, rights under copyright and otherwise, whether now or hereafter known) and all renewals and extensions thereof as may now or hereafter exist, in and to such Results throughout the universe and in perpetuity. I hereby assign absolutely and irrevocably to Lender (and Company as Lender’s assignee) in perpetuity, on my own behalf and on behalf of my respective successors-in-interest, heirs, executors, administrators, and assigns, all of my respective “economic/neighboring” rights in and to such Results and in the Picture and any derivative works based on such Results and/or the Picture which are, at any time, granted by domestic, foreign, or multi-national legislation, including, but not limited to EC or other legislation or directives concerning remuneration pursuant to any blank audio/visual tape levy, rental, lending, public performance rights, so-called “performer property rights” and/or rights in respect of satellite and cable retransmission broadcasts in EC member states or otherwise. I acknowledge that the compensation paid to Lender under the Agreement includes full, equitable and adequate consideration for this assignment and that such consideration is an adequate part of the revenues derived or to be derived by Lender (and Company as Lender’s assignee) from such rights. I hereby irrevocably and unconditionally waive the “moral rights” and analogous rights of authors (and rights of enforcement thereof), as said term is commonly understood throughout the world.

I.I hereby grant to Company the right, in perpetuity and throughout the universe to use my name, photograph, likeness, biographical data, and recordings of my voice and other sound effects in connection with any of the following: the production, advertisement, distribution, or exploitation of the Picture or any television Picture or motion picture containing any of the results and proceeds of my services hereunder, including without limitation, the filming and exploitation of featurettes, promotional films, “behind-the-scenes” or “making of” films, programming, interviews and/or documentaries, however exploited or distributed (and/or writing and exploiting a book); Company’s institutional advertising; publications of other material based on the Picture; and all subsidiary and ancillary rights therein, in any and all media, including, but not limited to, recordings (in any configuration) containing any material derived from the Picture, including, without limitation, all or any part of the soundtrack of the Picture, publications, merchandising and commercial tie-ups; provided, however, that in no event shall I be depicted as using any product, commodity or services without my prior consent. Notwithstanding the foregoing, it is understood and agreed that Company’s uses of my name in a billing block on any item of merchandise or other material shall constitute an acceptable use of my name which shall not require such consent.

J. I warrant and represent that: (i) I have the right to execute this document; (ii) I have not entered into and will not enter into any commitment or agreement which will or might in any way conflict with the material obligations under the Agreement; (iii) the Results are or shall be wholly original with me (or, in minor part, in the public domain throughout the universe; provided, that I so advise Company upon submission of my work to Company and identify the material I used which I believe to be in the public domain) and not copied in whole or in part from, or based upon, any other work or source (except for assigned material submitted to me by Company as a basis for the Results); (iv) the Results do not and shall not infringe upon the copyright of any person or entity; (v) the Results are not and shall not be based in whole or in part on the life of any real person, except as approved in advance in writing by Company; (vi) the Results do not and shall not, to the best of my knowledge in the exercise of reasonable prudence, violate the right of privacy or publicity of, or constitute a libel or slander against, or otherwise violate any other rights of any kind or nature whatsoever of, any person or entity; and (vii) the Results are not and shall not be the subject of any litigation or claim pending or, to the best of my knowledge in the exercise of reasonable prudence, threatened that might give rise to litigation.

K.I agree to defend, indemnify and hold harmless Company, its successors, licensees and assigns, and the respective shareholders, officers, parents, affiliates, directors, employees, agents and representatives of each of the foregoing, and any person(s) or entity(s), in whole or in part, owning, financing, producing or otherwise exploiting the Results and/or any work based thereon, and each of them, from and against any and all claims, liabilities, losses, judgments, damages, costs and expenses (including, without limitation, reasonable outside attorneys’ and accountants’ fees and costs and court costs, whether or not in connection with litigation) arising out of the breach or alleged breach of any representation, warranty or agreement made by me herein.

L. No breach by Lender or any other person or entity of any obligation to me shall allow me to terminate or rescind the rights granted herein or in any way otherwise affect such rights or enjoin the exhibition of the Picture, any other television Picture, motion picture or other production based upon the Picture or part thereof or rights therein, or to obtain any other form of equitable or injunctive relief, any right to which I irrevocably waive.

M. Company shall be free to assign the Agreement and its rights thereunder, and to delegate its duties under the Agreement at any time and from time to time, in whole or in part, to any person or entity. I may not assign the Agreement or my rights thereunder, or delegate my duties under the Agreement, in whole or in part.

N. I agree to execute and deliver any and all documents and take any and all actions reasonably necessary or advisable to effectuate, document, perfect or implement the terms set forth herein, including, without limitation, the assignment of rights contemplated herein. In the event that I fail to so execute and deliver such documents or I fail to take such actions within five days of Company’s written request, I hereby appoint Company as my attorney-in-fact to execute such document and/or take such actions, which appointment is coupled with an interest and, therefore, is irrevocable.

_____________________

[ARTIST’S OR EMPLOYEE’S SIGNATURE]

LOANOUT CONVERSION AGREEMENT

As of [DATE] (“Effective Date”)

[EMPLOYEE’S COMPANY NAME] (“Lender”) [ADDRESS]

Attention:

Re: [TITLE OF PICTURE] (the “Picture”)

To Whom It May Concern:

Reference is made to that certain agreement between [NAME OF PRODUCTION ENTITY] (“Producer”) and Employee regarding the Picture (the “Initial Agreement”). As of the Effective Date, the parties have agreed as follows:

1. Employee assigns to Lender the Initial Agreement which is incorporated by this reference. As of the date of such assignment, Employee will cease to be a direct employee of Producer and Producer will have no obligation directly to Employee for the payment of services thereafter performed under the Initial Agreement. Lender will furnish the services of Employee to Producer and Employee will perform such services to the same extent as though Employee had remained directly employed by Producer.

2. Lender hereby grants and assigns to Producer all of the rights to Employee’s services which are granted to Producer under the Initial Agreement and Producer will become the owner of the results and proceeds of Employee’s services as provided in the Initial Agreement to the same extent as though Employee had been employed directly by Producer and Producer were the employer for hire of Employee.

3. For the performance of all of Lender’s obligations hereunder and for all rights granted by Lender, Producer will pay Lender an amount equal to the compensation that would have been paid to Employee pursuant to all of the terms and conditions of the Initial Agreement had Employee remained a direct employee of Producer and had not assigned the Initial Agreement to Lender.