Reasons for Business Discontinuation

Introduction

Business discontinuation is a vital component of active economies. A mainstream of entrepreneurship literature has concentrated on efficacious endeavors. Therefore, little is known about why endeavors fail. It is complex, being both a sign of economic vitality and the source of effective individual trauma. This chapter presents a review of the literature to date. The purpose of this review is to provide a complete and serious analysis of business discontinuation research, classify the key reasons of business discontinuation, bond the gap between the numerous perspectives, and grow a consistent understanding of the phenomena upon which future studies can be based.

Start-up business as a high-risk venture may not reach the final line. Each year, many thousands of founders start their new businesses with the hope of achieving great success, but, unfortunately, small business statistics show that more than half of them fail. According to the European Association of Business Angels, about 50 million new projects (137,000 per day) are launched every year, but 90 percent of them fail. The most common reasons that cause the failure of a new project can be divided into three categories: technical, financial, and sales/marketing. In this chapter, we gather and identify the factors that lead to the failure of start-up business to provide an overview of the mistakes that founders may commit at the beginning of their business.

Business discontinuation studies have their heritage in the finance as the formation of commercial banks significantly enlarged the flow and the spread of financial data. Since then, it has been discovered and considered by a variety of researchers using different procedures. A new resurrection of interest in the topic has happened recently with an obvious and satisfying growth in studies associated with business discontinuation developing from entrepreneurship literature. The transformed awareness of business failure inside the entrepreneurship field focuses on individuals’ involvement in failure, thus departing from the moderately separate methods, such as logical exhibiting, that were ordinary when the subject debuted in finance literature. Gathering information on such a delicate topic is hard. Moreover, the leaning of researchers to choose their definition based on access to data rather than logical reasoning is concerning. The purpose of this review is to discover these problems and offer a glimpse of the evolution of business discontinuation studies and key discussions that have bonded the issue along these years within entrepreneurship literature.

Among the early approaches were those of Altman (1968) and Beaver (1966) who proposed to use a firm financial data to predict its probability to fail. The first statistical models developed were based on discriminant analysis (Beaver 1966) and multiple discriminant analysis (Altman 1968), followed by more recent approaches exploiting regression (Kolari, Glennon, Shin, and Caputo 2002; Martin 1977; Zmijewski 1984). Since the 1980s, artificial intelligence methods started to be used as well to predict ventures success/failure. The suggested solutions relied on decision tree algorithms (Frydman, Altman, and Kao 1985), artificial neural networks (Tam 1991), clustering (Ozkan, Türkşen, and Canpolat 2008), and hybrid genetic algorithms (Chiam, Tan, and Mamun 2009). Approaches based on financial data had the advantage of being potentially applied to a high number of companies, as data could be gathered from their annual reports. Nonetheless, company revenues were frequently consequences of other aspects, such as entrepreneur’s ability, company core competencies, market, and so on. In this view, other research works investigated whether such aspects could contribute as well to the success or failure of a venture.

According to statistics published in 2019 by the Small Business Administration (SBA), about 20 percent of business start-ups fail in the first year. About half succumb to business failure within five years. By Year 10, only about 33 percent survive. Those statistics are rather grim. In 2020, small business survival became an even bigger worry because of coronavirusrelated declines in sales. While there are a multitude of conditions that can result in a business failing, most years, the reasons small companies go out of business is because they make one or more common mistakes.

Business discontinuation is defined as exiting business due to failure to sustain the business ongoing, and it is a measure of economy strength. If the rate of business discontinuation decreases, this means that the country economy is strong and vice versa. Research indicates that the failure of SMEs is high, above all within the first year after starting (Franco and Haase 2010). Timmons (1994) show that over 20 percent of new ventures fail within the first year and 66 percent within six years. Other scholars like Paffenholz (1998) and Woywode (1998) state that approximately 50 percent of small start-ups survive for more than five years (Franco and Haase 2010). According to the GEM and Vanags (2018), in 10 economies, discontinuance rates were half or more the level of total early-stage entrepreneurial activity. Six of these were from the Middle East and Africa (Angola, Egypt, Iran, Morocco, Saudi Arabia, and Sudan); three were from Europe (Cyprus, Greece, and Sweden); and one was from Asia (Taiwan). According to Small Business Service (2001), in the UK, 350,000 to 400,000 businesses close every year—in recent years, about 10 percent of the total stock. Among high-income countries, Norway, the United States, Republic of Korea, Iceland, and Ireland have the highest rates of business discontinuation (Arasti 2011). That is why, it is very important to analyze and understand the causes of business discontinuation in order to enhance entrepreneurship and, consequently, enhance the economy.

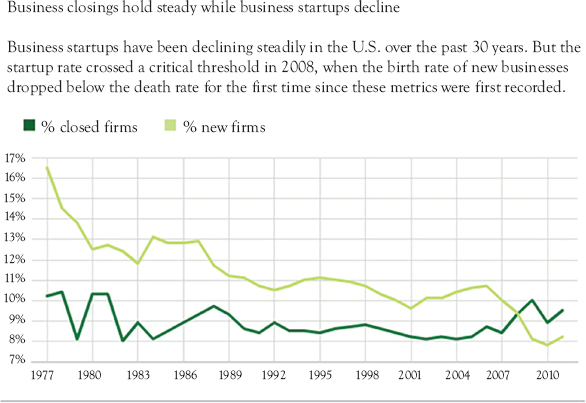

Figure 10.1 Business start-ups decline

Source: U.S. Census Bureau, Business Dynamics Statistics

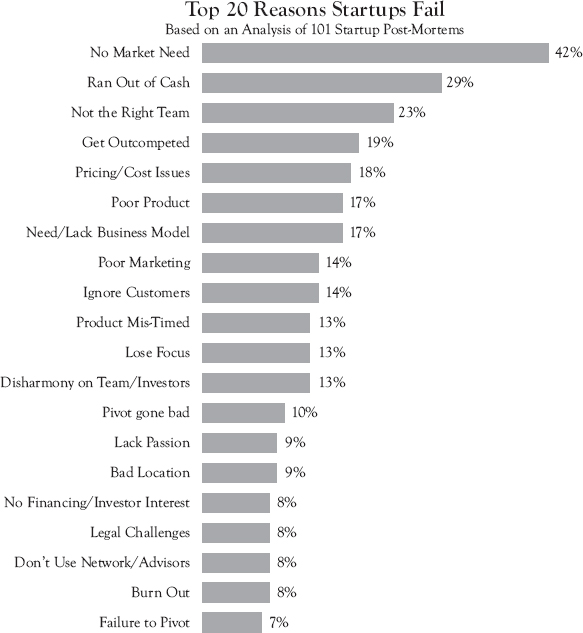

American Portal CB Insights, which collects and analyzes a huge amount of data using algorithms and data visualization, compiled a ranking of the most common factors of start-up failure based on the information gathered. The survey was conducted on 101 start-ups that unfortunately could not resist the pitfalls of the start-up environment.

Figure 10.2 Business startup decline (as cited in Arnaud 2018)

No market need (42 percent): One of the biggest problems is ignoring customer interest in introducing your product or service. As a founder, you should care about the customer need and solve the problems that arise from your competitors. Founders should make a market research based on accurate information before founding the project in addition to analyzing market environment.

Ran out of cash/insufficient funds (29 percent): Finding enough financial resources is very important to the success of any start-up business, especially in the first phase of launching, as there is no generated revenue. Insufficient operating funds can cause a forced closure before having a fair chance to succeed. They also cannot expect a realistic incoming revenue from sales. Spending cash according to a strategic plan is important to avoid running out of cash.

Not the right team (23 percent): Building a wrong team is a direct reason of a start-up failure. A diverse team with different experiences can form a real threat on the success of the start-up. The founders should spread and encourage the spirit of cooperation and participation.

Get outcompeted (19 percent): Start-up founders should maintain their core competencies and keep into competition.

Pricing or cost issues (18 percent): The pricing of the product/service may be one of the main reasons of the project success as it may be a competitive advantage. Product development is complex, expensive, and almost always takes longer than anticipated. Even big tech companies developing new products always struggle to estimate the time and cost required.

Poor product (17 percent): Companies should take the value delivered by their product/service to the customer into consideration.

Lack of a business model (17 percent): It is critical for all businesses to have an accurate business plan based on well-known information. This can ease the track of success and development of any new project.

Poor marketing (14 percent): Segmentation, targeting, and positioning represent the perfect way to market a product. Good marketing based on segmentation, which targets to deliver the right product to the right customer, is one of the most important skills of a successful start-up. It also attracts attention and turns noncustomers into customers.

Ignoring customer needs (13 percent): Empirical results point toward a significant relationship between customer satisfaction and economic performance in general, but less is known about how the satisfaction of company customers translates into security pricing and investment returns, and virtually nothing is known about the associated risks. The tacit link between buyer utility and the allocation of investment capital is a fundamental principle on which the economic system of free market capitalism rests (Anderson 1996; Anderson, Fornell, and Lehmann 1994; Anderson, Fornell, and Mazvancheryl 2004)

Product mistimed (13 percent): Choosing the right time to provide the product/service to the customer, especially in the season.

Lose focus (13 percent): Focusing is very important to keep your business competitive edge.

Disharmony in the team/investors (13 percent): Without a harmonious attitude in the company between both the team and investors, there will be confusion in decisions and their implementation.

Pivot gone bad (10 percent): According to CB Insights collection of 242 start-up postmortems, approximately 10 percent of the failed startup entrepreneurs surveyed attributed their failure at least partially to a pivot gone bad, while 7 percent attributed it partially to a failure to pivot. These start-ups do not give the complete picture. A business that needed to pivot in the first place is a business with other, more complex problems (and motivations for failure).

Lack of passion (9 percent): Most of founders lose their passion after facing some problems and not reaching their expected targets.

Bad location (9 percent): Founders should be very careful in choosing the location that should be close to suppliers, to reduce the transportation cost, and to the customers that they target. According to SBA studies, poor location is among the chief causes of all business failures. In determining a site for a retail operation, you must be willing to pay for a good location. The cost of the location often reflects the volume and/or quality of the business you will generate.

No financing/investor interest (8 percent): One of the important entrepreneur’s tasks is to keep the interest of investors to provide cash to keep the project open.

Legal challenges (8 percent): Sometimes, ignorance of some legal challenges may cause to falling in financial problems that may cause the closure of the project.

Lack of use of the network (8 percent): Every business should have a professional-looking and well-designed website that enables users to easily find out about their business and how to avail themselves of their products and services. In the United States alone, there were 312 million Internet users in 2019, and the U.S. Census Bureau estimates e-commerce sales were $601.7 billion (Clement October 02, 2020).

Cash burnout (8 percent): Taking the right decision to cut your losses and redirect your efforts at the critical point before failure to avoid burnout.

Failure to pivot (8 percent): You should know the perfect time to switch to another product or another strategy.

According to Michael Ames (1983), the major reasons for small business failure are (1) lack of experience, (2) insufficient capital (money), (3) poor location, (4) poor inventory management, (5) overinvestment in fixed assets, (6) poor credit arrangement management, (7) personal use of business funds, (8) unexpected growth. In addition, according to Gustav Berle (1989), there are two more reasons: (9) competition, (10) low sales. Moreover, according to Patricia Schaefer (2020), the top eight reasons for business failure are:

1. You Start Your Business for the Wrong Reasons

The desire to make a lot of money, hope of having more time with one’s family, or being on one’s own—benefits that some successful entrepreneurs achieve after years of hard work—are not reasons to start a business. The right reasons for starting a business and building a successful company include the following:

• You have a passion for what you will be doing.

• You strongly believe—based on educated study and investigation—that your product or service would fulfill a real need in the marketplace.

• You are very determined.

• Failures do not defeat you. You learn from your mistakes and use these lessons as business tips to help you succeed the next time around.

• You thrive on independence and are skilled at taking charge when a creative or intelligent solution is needed.

• You get along with and can deal with all different types of individuals.

2. There Is No Market or Too Small of a Market

Before you start a business, you need to determine if there is a market for what you plan to sell and if that market is big enough to be profitable. Keep in mind that not everyone is a market. To avoid business failure after start-up, business owners should keep an eye on their market and customer changing needs.

3. Poor Management

Poor management is the number one reason for failure. New business owners frequently lack relevant business and management expertise in areas such as finance, purchasing, selling, production as well as hiring and managing employees. If the business owner does not recognize what they do not do well and seek help, the company may fail and go out of business. To fix the problem, small business owners can educate themselves on skills they lack, hire skilled employees, or outsource work to capable professionals.

4. Insufficient Capital

Novel business owners often do not understand cash flow and underestimate how much money they will need to get the business started. As a result, they are forced to close before they have had a fair chance to succeed. They also may have an unrealistic expectation of incoming revenues from sales. It is imperative to determine how much money your business will require. You need to know not only the costs of starting your business but also the costs of staying in business. It is important to realize that many businesses take a year or two to get going. You need enough funds to cover all costs until sales can finally pay for these costs.

5. Wrong Location

Location is critical to the success of most local businesses. A bad location could spell disaster to even the best-managed enterprise. Some factors to consider are:

• Where your customers are

• Traffic, accessibility, parking, and lighting

• Warehousing or equipment storage needs

• Location of competitors

• Condition and safety of the building

• Local incentive programs for business start-ups in specific targeted areas

• History, community flavor and receptiveness to a new business at a prospective site

If you usually do not have customers or clients entering your business establishment, the ideal location for your start-up could be your own home.

6. Lack of Planning

It is critical for all businesses to have a business plan, and it must be realistic and based on accurate, current information and educated projections for the future. Components should include:

• Description of the business, vision, goals and keys to success

• Market analysis

• Workforce needs

• Potential problems and solutions

• Financial considerations: capital equipment and supply list, balance sheet, income statement and cash flow analysis, sales and expense forecast

• Competitive analysis

• Marketing, advertising, and promotional activities

• Budgeting and managing company growth

In addition, most bankers request a business plan if you are seeking funds.

7. Overexpansion

Overexpansion often happens when business owners confuse success with how fast they can expand their business. A focus on slow and steady growth is optimum. Many a bankruptcy has been caused by rapidly expanding companies. At the same time, you do not want to limit growth. Once you have an established solid customer base and a good cash flow, let your success help you set the right measured pace.

8. No Website and No Social Media Presence

You need a website and social media presence. Every business should have a professional-looking and well-designed website that enables users to easily find out about their business and how to benefit themselves of their products and services. If you serve local customers, your website should include your address, phone number, and working hours. It should be listed in Google My Business so that it can show up when customers search for what you sell by location. You get most of your business through networking and referrals. You need a website so that potential customers can research your business before they call you. If you have products that can be sold online, or you can take orders online, that is an added benefit. Nevertheless, at the basic minimum, you need a website that lets customers know what you offer and how they benefit by doing business with you.

According to Zhang et al. (2020), the common reasons of businesses failure are:

9. Starting With Too Much Debt

Sometimes, it is necessary to go into debt to finance the launch or purchase of your business. Few aspiring business owners don’t have the cash to pay out of pocket, so loans are a reasonable choice to help finance a new venture. However, if you do not prioritize repaying your debt and making timely payments, it becomes harder to grow operations. Small business owners through all industries report that lacking of capital or cash flow is their highest challenge. Adding the load of debt makes it more difficult to reach profit. To avoid starting out with so much debt to repay, you may think about alternative funding methods.

A business plan is a crucial element for a small business. Your business plan will help you with almost all aspects of your business, from financing to operations. If you create your business plan early on, you can use it as a guide and a checklist throughout your small business journey. With a good business plan, you will research and understand key areas for success.

11. Mismanaged Cash Flow

Cash flow and profit are two different things. You can be profitable but still not have cash. Profit looks at the current state of your sales— including sales that may have not been processed with your accounts receivable yet. Ignoring your cash flow means ignoring the money you actually have to work with. You need that cash for daily operational needs like paying invoices, bills, and employees. As a business is growing, it is important that accounts receivable be managed to focus on cash flow. When companies fail to make adjustments to cash flow while they are growing, it is more likely they will run out of operating capital. if you are out of capital, it is almost impossible to keep ahead of invoices and paying employees.

12. Ineffective Leadership

Active listening, empathy, encouragement, communication, and compromise are skills that should be considered to step into a leadership role. As a business owner, your employees, vendors, and clients will all look to you as a reflection of the business as a whole.

13. Failure to Adapt

New or adjusted business models have kept many businesses running during times of no or limited in-person occupancy. Change is a constant, so it can be dangerous to grow satisfied. Even if things are going well with your business at the moment, being unprepared or unwilling to adjust can be dangerous. Regularly looking to improve your processes, tweak your business model, and innovate your product or services all help you prepare for future success and protect against future change.

According to Mike Kamo (2020), there are six reasons your small business will fail:

Your business will fail if you show poor management skills. You will struggle as a leader if you do not have enough experience making management decisions, supervising a staff, or the vision to lead your organization.

2. Lacking Uniqueness and Value

You may have a good product or your service has strong demand, but your business is still failing. May be your approach is mediocre, or you do not have a strong value proposition. If there is strong demand, you probably have many competitors, and it is hard to stand out in the crowd.

3. Not in Touch With Customer Needs

Keep in touch with your customers and understand what they need. Keep an eye on the feedback they offer. Your customers may like your product or service, but they might love it if you changed a feature or altered a procedure.

4. Unprofitable Business Model

Similar to leadership failure is building a company on a business model that is not sound, operating without a business plan, or pursuing a business for which there is no proven revenue stream. The business idea may be great, but you may fail in the implementation of the idea.

5. Poor Financial Management

Your business can fail if you lack a contingency funding plan, a reserve of money you can call upon in the event of a financial crisis. Occasionally, people start businesses with a dream of making money, but they do not have skills to manage cash flow, taxes, expenses, and other financial matters. Poor accounting practice pushes a business to failure.

6. Rapid Growth and Overexpansion

Every now and then, a business start-up grows much faster than it can keep up with. You start a website with a trending product and, unexpectedly, you are asked for orders you are not able to fulfill. On the other hand, perhaps the opposite is true. You are convinced that your product is going to succeed that you invest much and order too much inventory, but you cannot move it.

According to Garfield, Moore, and Adams (2019), there are ten reasons why seven out of 10 businesses fail within 10 years:

1. Failure to Deliver Real Value

Value is the heart of any business. The world most successful businesses deliver the highest value. They always overdeliver, no matter what the situation is. If you are looking to get rich quick, you will quickly fail. Instead, focus on the real value proposition, adding more value than your competitors do.

2. Failure to Connect With the Target Audience

If you do not connect with your target audience, your business will fail. You have to be aware of your potential consumers’ wants and needs.

3. Failure to Optimize Conversions

Conversion rate optimization (CRO) is a system for increasing the percentage of visitors to a website that convert into customers, or more generally, take any desired action on a webpage. Without optimizing conversions, no matter what a business does, especially if it raises money and has a high burn rate, it will be useless trying to survive when money runs out. Address the conversions early on to ensure that there is a positive return on investment (ROI). Therefore, you know you have a sustainable business.

4. Failure to Create an Effective Sales Funnel

The sales funnel is each step that someone has to take in order to become your customer. Building an effective sales funnel should be one of the primary goals of any founder. These automated selling machines help to reduce friction in making the sale and help to put many of the functions of running a business on autopilot, allowing founders to grow things like traffic sources or to educate consumers through webinars and so on. Sales funnels also help to build a relationship with the consumer through e-mail warming campaigns.

5. Lack of Authenticity and Transparency

Businesses that lack authenticity and transparency will fail one day soon. Without customers’ needs in sight and a focus on the wrong things, businesses could easily lose consumers’ trust. Rather than risking that, focus on being authentic, transparent, and finding ways that you can give more rather than take.

6. Unable to Compete Against Market Leaders

Staying afloat is exponentially harder when competition is severe, especially true in profitable markets where the stakes are high. If smaller businesses cannot compete against their larger counterparts, they need to find ways to pivot and stay in business. To do that takes a keen business sense and true guts.

7. Inability to Control Expenses

It is easy to spend when funds are available. However, having a critical sense to control company expenses is mandatory. When expenses get out of control, it is impossible for a business to survive.

8. Lack of Strategic and Effective Leadership

Most businesses lack strategic and effective leadership. Without real experience in the business world, most newcomers to the entrepreneurial arena struggle with the irresistible amount of demands placed on them when problems do arise.

9. Failure to Build an Employee “Tribe”

Your employee tribe and culture are crucial for long-term success. Most businesses will fail because they forget about their employees.

10. Failure to Create Proper Business Systems

Customer relationship management (CRM) needs to be implemented and customized. Policies need to take place. Financial audits and tracking procedures need to be created. Without good systems and automation, the amount of work becomes too hard, and the details can easily be missed.

Conclusion

Business discontinuation is an ubiquitous danger for numerous business visionaries. It could be a theme that warrants cautious thought by entrepreneurship analysts. However, both trade history specialists and administration researchers contend to date have basically concentrated on considering victory cases and paid generally small consideration to firm disappointment. Failure may be a result of factors from both outside and inside the organization. Maybe one or two factors occur simultaneously. Business research is the most important step before launching your business to know the market real need. Ignoring receiving product feedback and criticism causes also the failure of founders to continue in the market. It is essential to realize that buyer and user satisfaction are the main targets of business success. In addition, one of the common factors of start-up failure may be incorrect timing. Some start-ups launch products ignoring that the right technology is not yet available. Financial considerations and cash funds are a very important factor in the success and continuity of a business, but it should be based on good planning. Spending cash according to a strategic plan to avoid running out of cash is essential. Without a harmonious attitude in the company between both the team and investors, there will be confusion in decisions and their implementation. Good marketing based on segmentation targeting and positioning is yet another important consideration. You should choose a perfect location that serves the project and your targeted customer. As a founder of a business, you should take all the aforementioned points, and other issues like EGO, theatrical reality, uncontrolled growth, lack of experience, and so on into consideration to avoid failure or discontinuity of your project.