The Store Is Dead — Long Live the Store

Legacy offline stores and next-generation online retailers are each finding their way to a new kind of shopping experience: the showroom.

Offline demise and offline renaissance is the paradox of new retail writ large. Swiss multinational financial services company Credit Suisse projects that by the time the numbers are in, more than 8,500 stores in the United States will have closed in 2017.1 Consensus estimates predict that 25% of all shopping malls will shrink or close in the near future. At the same time, online-first brands from suitcase retailer Away to eyewear maker Warby Parker are successfully opening pop-ups, showrooms, and full-blown stores.2 Not to be outdone, Amazon.com, the granddaddy of online-first, has opened bookstores and is rumored to be planning to open 2,000 AmazonFresh grocery stores over the next 10 years.3

The net result: Offline is dead and dying, yet it is also alive and thriving.

To understand why, consider the arc of Bonobos, founded in New York City in 2007 as Bonobos.com and sold in 2017, as Bonobos, to Walmart Stores Inc. for $310 million.4 CEO Andy Dunn founded the company with Brian Spaly while both were MBA students at Stanford’s Graduate School of Business.5 Their vision was simple: Sell men a better-fitting pair of pants, and do it without the “burden” of physical stores. Looking back to 2007, Dunn readily admits, “I really thought stores were going away at that time.”6 Ironically, nearly 10 years later, The Economist praised Bonobos for pioneering a new form of physical retail. The “zero-inventory store” is a small-footprint store where customers get a high-service, tactile experience, purchase via tablet, and order the product shipped to a location of their choosing.7

The trends exemplified by Bonobos reveal retail’s future: It will be small footprint and high experience, regardless of whether the retailer is online-first with offline additions or offline-first (legacy) plus e-commerce.

In this article, we pursue two interconnected themes: the expansion of online-first retailers into offline stores that serve the purpose of “supercharging” customer value, and the transformation of the stores of offline-first retailers from fulfillment-dominant centers into experience-dominant centers, which simultaneously reduce store size and inventory while improving the customer experience. In doing so, we explain how offline-first retailers can benefit from mimicking the showroom concepts started by online-first retailers, and why online-first retailers can benefit from opening more traditional stores. (See “About the Research.”)

About the Research

We developed initial insights into “The Store Is Dead — Long Live the Store” while working in partnership with management at Bonobos, the retail originator of the zero-inventory store and what it calls the Guide Shop. We utilized an extensive customer database of almost 10 years of data (from the inception of the company in October 2007) to measure the effects of customer place of birth (online or offline) on subsequent trajectories for demand and product returns. We developed additional insights and validation from a second database from the online-first eyewear company Warby Parker (again, from the inception of the company in February 2010).

Management of both organizations, in exchange for our research, provided us with the following data fields: unique customer ID (disguised for confidentiality), transaction date, transaction items, transaction value, returns, and customer (shipping) ZIP code. We were privy to information on the location and timing of showroom and Guide Shop openings, and when or whether customers visited them.

As sales through online channels vary considerably by geographic location due to the kinds of customers, and their preferences and offline option,i we further augmented data with readily available geodemographic data from the U.S. Census Bureau and Esri, a geographic information systems company based in Redlands, California. This allowed us to properly characterize the offline retailing environment when estimating online demand. Given all the data, we tabulated summary statistics and estimated state-of-the-art econometric models to derive our insights on supercharging. In particular, we analyzed so-called natural experiments: real management interventions in actual markets, and the effects on customer buying and return behavior.

To track how physical stores have evolved for offline-first retailers, we used data available from Wharton Research Data Services. This data includes square footage and inventory for a panel of offline retailers.

Finally, we created simulations to demonstrate the benefits for offline-first retailers from adopting a zero-inventory strategy for their stores; we conducted sensitivity analyses to show how the benefits obtained from the strategy vary by different assumptions and circumstances.

Supercharging Customers of Online Brands With Offline Showrooms

We coined the concept, “supercharging” after first hearing the principle explained in a lecture by Lawrence Lenihan, CEO of Resonance Companies, and subsequently investigating it with data obtained through our extensive work with digitally native vertical brands (DNVBs). Supercharging occurs when customers are nurtured in a small-footprint location that typically holds no inventory — and fulfilled, initially (and subsequently, for repeat purchases), from an operationally efficient distribution center.

The intuition for supercharging is the following: A customer who is exposed to the brand offline, rather than online, is not only more likely to peruse and sample a wider selection of product categories, but also is more immersed in the brand experience. This immersion and affinity serve to increase the rate and volume of subsequent purchases, whether online or offline, by an individual shopper. The experience also generates operational efficiencies by reducing returns. This is a critical virtue, as returns are a major headache for online sellers, often approaching 30%, and as high as 40% for apparel sellers.8

Resonance’s Lenihan, who identified and articulated the concept of supercharging,9 suggests it is replicated in the world of human relationships. When two people have an email-only relationship, it typically lacks the depth and intimacy of a relationship that begins with a face-to-face encounter. In the latter case, future online interactions have the support and context of the initial offline connection. By analogy, shoppers who have experienced a brand offline develop a greater sense of context and emotional connection to the brand, and this comes into play when they purchase online in the future.

There are less immediately apparent benefits to the retailer as well. Just as customers learn more about the retailer and the retailer’s products when immersed in an offline experience, retailers have the opportunity to observe, study, and learn about customers who enter their physical locations. Specifically, the retailer is able to observe nondigital customer attributes, including their emotional and sensory response to products, salespeople, and in-store stimuli, and compile and collate a history of in-store interactions, product sampling, shopping paths, and so on. Deployment of relevant technology amplifies this reciprocal learning.10 One of the key innovations initiated by DNVBs like Bonobos and Warby Parker was the “head office showroom,” which nicely encapsulates both types of benefits. (See “The Head Office Showroom.”)

The Head Office Showroom

From their early days of operations, both Bonobos and Warby Parker deployed their head offices as showrooms. Initially, it was a matter of necessity: The companies had limited capital and they knew that some customers might want to touch and feel the products before purchasing — hence, it made sense to double up the physical space they had for an office and use it as a showroom too. (One might argue that the very first Warby Parker showroom was Neil and Rachel Blumenthal’s Philadelphia apartment when Neil was an MBA student at the Wharton School.) Pretty soon, both companies realized the symbiotic nature of this relationship. It was not simply that customers could touch and feel products, or even that customers could also get a “feel” for the brand, including the employees who work there. It was the realization that product design teams and others could have direct access to customers. In short, the offline showroom at both companies’ headquarters created a constant inflow of flesh-and-blood customers, reminding employees of who they are ultimately working for, and allowing employees across all business functions to learn more about the nondigital attributes and footprint of their customers.

Showroom experiences create better customers: Customers are exposed to the brand in a more meaningful and immersive way, and they are better able to resolve any uncertainty about the nondigital attributes of the retailer’s products. Likewise, showrooms create better retailers: When customers are physically present in the retail environment, observation of their behaviors can lead to meaningful insights.11 Salespeople can anticipate and respond to customer needs, provide exceptional service, recommend additional items, look for signs of customer discomfort, and so on.

The Quantifiable Benefits of Supercharging

At Bonobos, we find that customers who are “born offline,” meaning that they complete their first transaction at a physical location (one of the Bonobos Guide Shops),12 account for a larger than proportional share of sales than the customers who are “born online.” If we normalize the percentage of customers who are born offline to 20% (for ease of exposition and to maintain confidentiality), these customers account for 24% of the total sales, about 19% more volume than would be expected on a proportional basis.

This apparent superiority of the customers coming from Guide Shops does not account for what a business academic might call a “selection effect” — specifically, that more “enthusiastic” (and higher-value) customers might be motivated to initially visit the Guide Shop or similar offline showrooms. We analyze this further below, but the bottom line is that customers who visit the Guide Shop generate outsized sales.

Data from Warby Parker customers show similar findings. When showrooms are opened in locations where they did not previously exist, the number of first-time customers within the trading area of the showroom increases by more than 7%.13 Showrooms also garner a higher percentage of first-time buyers: 83%, compared with only 75% for the online channel. More telling in terms of attribution is that when a showroom is opened, the fraction of new buyers acquired online falls from 75% to 67%.

Clearly, showrooms are useful for attracting new customers. In fact, customers with a showroom experience are significantly more attached to the brand than are customers who never visit and are online-only, and they are more attached than they had been before their offline experience. The purchase histories and trajectories of two actual “matched” Bonobos customers nicely illustrate the point.

“Tom” and “Bob” (names changed) are real Bonobos customers who live in New York City and made their first transactions with Bonobos in early 2015. In their first transactions, both Tom and Bob bought a pair of pants online. Later that year, Tom visited a Guide Shop in New York and placed a new order ($106). Bob also placed a second order ($182), but he did not visit the Guide Shop. In fact, Bob remains an online-only customer and has not been supercharged to this day. By his sixth transaction, Bob had spent a total of $762 and bought items from four product categories. In the same period, Tom made two more visits to the Guide Shop. By his sixth transaction, Tom had spent a total of $2,082 across seven product categories. (For a more detailed analysis of the data, see “Demand Benefits From Supercharging.”)

Demand Benefits From Supercharging

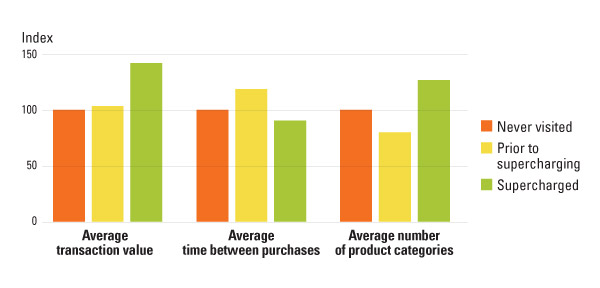

Demand benefits from supercharging customers offline at a Bonobos Guide Shop are reflected in three metrics: average transaction value, order velocity, and breadth of purchasing across the product line.

Analyses below focus on customers who made the same total number of transactions, which facilitates an apples-to-apples comparison. (See “Effect of Showroom Visits on Shopping Patterns.”) The left-most orange bar represents the average transaction value of customers who never visit a Guide Shop and are therefore never subject to a supercharging experience. We index their average spend as the baseline at 100 points (we do so for ease of exposition and to preserve confidentiality of the actual dollar value). The yellow bar represents customers who will be supercharged eventually (via a visit to the Guide Shop), but it reflects the average value of their transactions prior to supercharging. At 103 points, the yellow bar average spend index is statistically indistinguishable from the orange bar. The lift induced by the Guide Shop (green bar) is substantial. The average value of transactions made by customers after they have visited a Guide Shop is 141 points, a supercharge effect of more than 40%. Note that after a Guide Shop visit, transactions could be made either online or offline.

A similar dynamic is at work for frequency and breadth of purchases across the product line. Again, the orange bar (see “average time between purchases” grouping) indexes the visit frequency of the online-only customers at 100. Prior to visiting a showroom, customers who eventually do so are less frequent Bonobos shoppers than their online-only counterparts. This likely reflects a lower level of comfort with an online-only experience. Post-showroom experience, however, supercharged customers (green bar) increase their purchase frequency relative to online-only customers (orange bar) and their pre-Guide Shop selves (yellow bar) as the inter-purchase time index drops considerably, to 90.

Bonobos is a multicategory apparel retailer, selling pants, shirts, jackets, suits, and other items. Customers who never enter a showroom and are online-only (orange) buy products in 15.5% of the total categories sold by Bonobos, on average. We again define this as the baseline, indexed at 100. Prior to their supercharging experience, customers who eventually visit the Guide Shop (yellow) show less breadth of brand engagement than their online-only counterparts and are indexed at 80. This is a continuation of what we saw in the “average time between purchases” grouping. Similarly, the breadth index for the average transaction by supercharged customers (green bar) increases to a whopping 126 after the showroom experience. These customers go from buying in about 12.4% of the total assortment to more than 19.5%.

Effect of Showroom Visits on Shopping Patterns

Customers who experience the brand offline and are thereby “supercharged” spend more per transaction, shop more frequently, and buy in more categories.

Supercharging also has a positive impact on returns. Returns are a perennial problem in apparel retailing, especially in e-commerce. A report by The Retail Equation, “Consumer Returns in the Retail Industry 2015,”14 puts average offline returns, across all apparel categories, at about 8% (10% during the holiday season), substantially lower than the 30% to 40% often seen with online purchases.

As before, we do not report the actual return rate but index it at 100 for customers who are online-only and never visit a showroom. (See the orange bar in “Effect of Showroom Visits on Returns.”) Customers who eventually visit a showroom index at 117 for returns on their online preshowroom purchases (yellow bar), meaning they are more likely to return items relative to online-only shoppers. Again, relative to online-only (orange) customers, they are more tentative and show less ability to assess fit through the online channel alone. Subsequent to a showroom visit, however, when supercharged, these customers index substantially lower product returns than their preshowroom selves, at 95 (green), and lower than online-only customers as well (orange).

Effect of Showroom Visits on Returns

Customers who experience the brand offline and are thereby “supercharged” are less likely to return the items they purchase.

Warby Parker data provides complementary evidence on how the retailer gains from seeing customers in person. When customers buy offline, customer-retailer interaction reduces return rates by about 1% in absolute terms, a statistically and economically meaningful reduction.15 Customers with more complex eyewear needs, such as people who need to wear glasses throughout the day, are more likely to visit showrooms. Strikingly, the reduction in returns for these customers is nearly four times greater, at 3.6%. Complex-need customers are better able to assess product suitability offline, and Warby Parker is better able to service and understand this group offline as well.

Offline Retailers: From Inventory to Experience

Offline-first retailers can learn from the innovations of the DNVBs. First, they can transform stores into experience centers where customers can engage meaningfully with the retailer, making the store not only a place to fulfill orders (and sometimes not even that) but also a destination.

This transformation is already happening. South Korean multinational Samsung Group recently opened its flagship store, Samsung 837, in New York City. Rather than selling and fulfilling orders, Samsung 837 is a 55,000-square-foot space where customers can try out Samsung products and have a good time. In addition to the newest Samsung products offered to the consumer market, the store features installations that change every season, including interactive virtual reality rides, disc jockeys, a 75-seat theater, and a selfie station that encourages customers to share their pictures on social media.16 This parallels innovations that DNVBs had introduced, such as Warby Parker’s store photo booths, where customers can take pictures with different frames and share them with friends. Bucketfeet, a Chicago-based retailer of artist-designed footwear, has studios where artists exhibit their work and customers can design their own shoes.

Legacy retailers can also redesign merchandise presentations to provide a richer and more pleasant store experience. Minneapolis, Minnesota-based discount retailer Target Corp., for example, has introduced new layouts, called “vignettes,” for its home-décor category. By showcasing products in showroom-like areas, customers gain decorating ideas as they imagine how the products would look in their homes. And Nordstrom Inc., a luxury department store chain based in Seattle, Washington, is starting to roll out small-format stores without merchandise, where customers can try products (which are not stocked at the store), interact with personal stylists, or even get a manicure or a drink at an in-store bar.17

Here again, online-first retailers offer interesting models that offline retailers can learn from. Bonobos and Trunk Club, a personalized clothing service based in Chicago, for example, allow customers to make one-on-one appointments with salespeople. In a similar vein, online-first retailers have explored how to integrate and improve the customer experience by combining data from the different channels. Amazon Books provides a curated assortment by displaying in the stores only those books that are rated four stars and above on its website.18

Other retailers have implemented advanced technologies that increase the utility that customers attribute to stores. San Francisco-based software company Oak Labs Inc., for example, developed in-store intelligent fitting rooms, where customers can see how the clothes would fit under different circumstances.19 These enhanced experiences not only attract customers to stores but also provide the retailer with opportunities to learn about shopper behavior.

Retailers can generate store visits by implementing omnichannel initiatives, such as in-store pickup of online orders. Spanish retailer Desigual, for example, has built unattended ship-to-store lockers in its stores where customers pick up their online orders for free.20 Again, this encourages customers to visit the store and refresh their connection with the retailer. Brickwork Software, a New York City startup that provides a location-based service that allows customers of its retail clients to book appointments and reserve “try-ons” at nearby stores of their choosing.21

Through these initiatives, savvy retailers nudge customers to visit offline locations when they are shopping, or searching, online. This strategy is also useful for transactions that have a higher risk of being returned: Retailers can encourage customers to return products at the store, rather than shipping them to a sorting center.

The Store Shrinks Into a Showroom

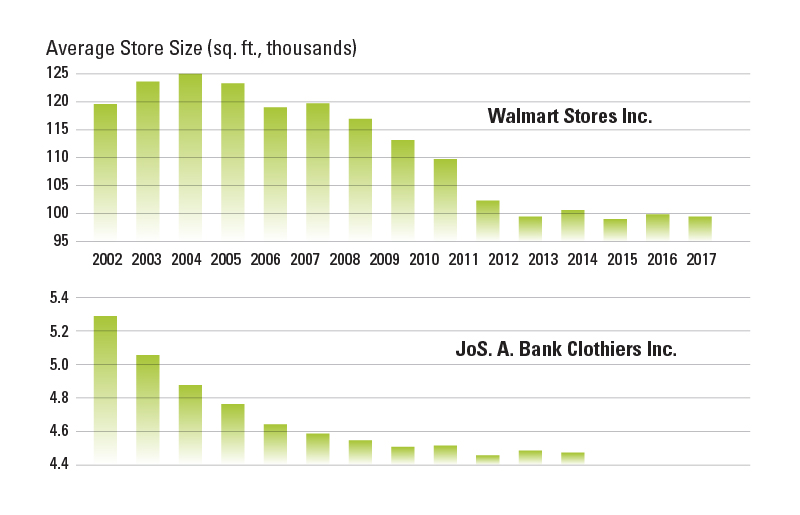

The transformation of the role of stores in offline-first retailers is seen in the evolution of several hard metrics for leading apparel retailers. Consider the trajectory of average (normalized) store size for a general retailer, Walmart, and for a specialty apparel retailer, JoS. A. Bank Clothiers Inc., based in Hampstead, Maryland. (See “Average Offline Store Size Over Time.”) While we’ve shown only two stores for ease of exposition, the pattern is similar for many representative retailers, including Bed Bath & Beyond Inc., Neiman Marcus Group LLC, and numerous others.22

Average Offline Store Size Over Time

Research shows that traditional stores are shrinking.

Clearly, the average store size is decreasing over time, consistent with the idea that offline-first retailers are providing a more intimate environment and moving away from stores with a predominantly fulfillment-oriented role. Dollars of inventory per square foot also shows a declining trend. Because many legacy retailers now have a substantial online presence and omnichannel capabilities, they are able to greatly reduce the fraction of stock keeping units (SKUs) they routinely carry in their stores.23

If offline-first retailers continue to transition their stores from a fulfillment-dominant role and add more experiential components, what benefits and costs could they experience if they take this transition to its ultimate conclusion: the zero-inventory store, as pioneered by Bonobos? We have conducted a series of simulations to explore the benefits and costs of such radical transformation, and we provide the key insights below.

Our simulations consider a fashion-apparel chain with 200 physical stores. As would be the case in real life, each store has a different footprint and different average demand.24 We choose a conservative average retail markup of 125%. We then compare the performance of conventional stores with what could be achieved via showrooms in combination with centralized fulfillment. We do this by manipulating two key retail variables: the chance that customers can find items for sale — that is, the in-stock rate — and the amount of inventory that a retailer has to hold in order to meet a specific in-stock rate objective.

In our simulated world, we imagine two separate scenarios. In the first, the store and the showroom are both required to maintain the same probability that items carried are actually in stock — that is, the same in-stock rate. Note, however, that the amount of inventory needed to ensure this might be different for the store and the showroom. In the second scenario, we reverse the problem and force the store and showroom to hold the same quantity of inventory (for the showroom, no inventory is held on-site; rather, it is held in a centralized fulfillment center). When the inventory positions are held constant, the probability that customers can find items in stock might differ between the store and showroom.

In the first scenario, let’s imagine that the retailer’s goal is to offer its customers a 95% in-stock rate,25 both in traditional offline stores and in showrooms. (Inventory requirements to achieve this in-stock rate depend on the level of demand uncertainty.) The first insight is that demand pooling from converting traditional stores into showrooms brings a substantial reduction in the amount of inventory that is needed. Even at a modest level of uncertainty (say 20%) about what sales will be, there is a 25% reduction in the amount of inventory that needs to be carried in order to maintain the 95% in-stock rate for the showroom.

The second insight is that this leads to gross margins going up by about 40% (again using the 20% demand uncertainty value).

Next, we simply “reverse” the analysis and hold total inventory constant in the two systems. If we fix the inventory level to that needed for a retailer to achieve a 95% in-stock rate when using showrooms, we find that the same level of inventory would provide only a 59% in-stock rate when using traditional stores.

Naturally, the in-stock rate has a big effect on revenue and gross margin. In a world with 20% demand uncertainty, and when stores and showrooms use the same amount of inventory, the showroom retailer generates 7% more revenue and 14% higher gross margins.

So far, we have simply described the effect of the direct cost reduction that comes from the pooling of inventory in a centralized location. Showroom benefits, however, do not stop there. Relative to stores, showrooms require a smaller footprint, which translates into lower fixed costs. Furthermore, they do not need to be replenished multiple times a week, reducing logistic costs. Showroom employees need not tend to big boxes coming from the distribution center, nor arrange products on the shelves. Finally, stores that are converted into showrooms can be redesigned to create a more welcoming and engaging environment.

We do recognize that there is cost attributable to potential lost sales, as customers who seek instant gratification — or have an immediate need — cannot take product from showrooms. This effect, unfortunately, is hard to estimate in general, but it can be assessed to some degree on a case-by-case basis by retail professionals. (A customer might have a more urgent need for a Bonobos suit, for example, than for Away luggage.) Regardless, it remains a source of potentially significant risk.

Nevertheless, our simulation can be used to illustrate how “bad” things need to be, in terms of sales, to make the showroom a losing proposition. For a retailer wanting a 95% in-stock rate, it’s possible to lose up to 15% of sales and yet obtain the same gross margin as that provided by using stores. In short, the showroom model appears a viable strategy — even when lost sales from customers wanting immediate gratification are significant.

We began this article with an apparent paradox: Offline is dead and dying, yet it is also alive and thriving. The bottom line is that stores are very much alive, but with a subtle yet profound shift in focus — from fulfillment to experience-oriented environments. Smaller footprint, tech-enabled, high-touch, and creative spaces are becoming the norm — and they are proving effective for retailers built originally with bricks and bytes alike.

David R. Bell (@davidbnz) is the Xinmei Zhang and Yongge Dai Professor of Marketing, Wharton School, University of Pennsylvania, and president of Idea Farm Ventures, a New York City-based venture studio. (He is also an investor in Bonobos and Warby Parker.) Santiago Gallino is associate professor of business administration, Tuck School of Business, Dartmouth College. Antonio Moreno is the Sicupira Family Associate Professor of Business Administration, Harvard Business School, Harvard University.

References

1. J. Wattles, “Stores Are Closing at an Epic Pace,” April 22, 2017, http://money.cnn.com.

2. J. Smith IV, “Long Live Retail: Fashion Startups Finally Learned Why Physical Stores Still Matter,” Observer, Jan. 8, 2015.

3. See, for example, M. Addady, “Amazon Wants to Open 2,000 Grocery Stores Across the U.S.,” Fortune, Oct. 27, 2016.

4. M. de la Merced, “Walmart to Buy Bonobos, Men’s Wear Company, for $310 Million,” The New York Times, June 16, 2017.

5. Spaly went on to found Trunk Club, which sold to Nordstrom for $350 million. This “curated commerce in a box” has found favor with Stitch Fix, an online subscription and personal shopping service, as well.

6. L. Zumbach, “Bonobos CEO Says ‘Guideshop’ Model Is Working,” Chicago Tribune, April 25, 2016.

7. “Shops to Showrooms: Why Some Firms Are Opening Stores With No Stock,” The Economist, March 10, 2016.

8. C. Reagan, “A $260 Billion ‘Ticking Time Bomb’: The Costly Business of Retail Returns,” Dec. 16, 2016, www.cnbc.com.

9. Lenihan delivered this insight while giving a guest lecture to MBA and undergraduate students at the Wharton School.

10. L. Dishman, “Inside LA’s New, Futuristic Store — Magic Mirrors Included,” Oct. 8, 2015, http://fortune.com.

11. This concept has a long and important history in retailing. In his best-selling book, “Why We Buy: The Science of Shopping,” Paco Underhill introduced and validated the idea of an anthropological view of shoppers. His researchers literally followed shoppers through the store environment in order to glean nuggets of insight into their behavior.

12. As of January 2018, Bonobos had 48 Guide Shops throughout the United States. https://bonobos.com/guideshop.

13. D.R. Bell, S. Gallino, and A. Moreno, “Offline Showrooms in Omnichannel Retail: Demand and Operational Benefits,” Management Science, published online March 23, 2017.

14. The Retail Equation, “2015 Consumer Returns in the Retail Industry,” (December 2015), PDF.

15. Once frames are fitted with customer-specific prescription lenses, the salvage value is close to marginal cost.

16. M. Matousek, “Samsung’s Vision for the Future of Retail Is a Store That Doesn’t Try to Sell You Anything — Take a Look Inside,” Jan. 1, 2018, www.businessinsider.com.

17. S. Kapner, “Nordstrom Tries on a New Look: Stores Without Merchandise,” The Wall Street Journal, Sept. 10, 2017.

18. N. Walters, “7 Cool Things You Can Buy at the New Amazon Books Store in New York,” Aug. 29, 2017, www.thestreet.com.

19. K. Opam, “Oak Labs’ Interactive Fitting Room Feels Like the Future,” Nov. 18, 2015, www.theverge.com.

20. S. Miles, “5 Buy Online, Pick Up In-Store Platforms for Retailers,” Aug. 9, 2016, http://streetfightmag.com.

21. A customer walking in New York City enters “Nike stores” in the search bar on his or her mobile phone. Brickwork surfaces store locations and appointment options.

22. Additional examples are available from the authors, upon request. All the reported differences are statistically significant with p<.01.

23. K. Stock, “Staples Is Shrinking; Radio Shack Is Sinking,” March 6, 2014, www.bloomberg.com.

24. For the technically inclined, the simulated demand for each store comes from a log-normal distribution (to ensure that the sales number generated for each store and from each draw from the simulation is positive).

25. “95% in-stock rate” means that there is a 95% chance that a customer will find his or her preferred item in stock.

i. See D.R. Bell, J. Choi, and L. Lodish, “What Matters Most in Internet Retailing,” MIT Sloan Management Review 54, no. 1 (fall 2012): 27-33.

Reprint 59302.

For ordering information, visit our FAQ page. Copyright © Massachusetts Institute of Technology, 2018. All rights reserved.