3

STEP 3: IMPROVE THE ORGANISATION’s PERFORMANCE THROUGH COACHING

Leading and managing are two separate attitudes. Each delivers different results.

This chapter explores how you must use the skill of coaching to help your organisation establish a high standard of excellence. You will practise your skill of coaching and quickly synthesise critical information as you help your hypothetical friend, Brian, set the tone.

After reading this chapter, you should be able to

take charge of setting the tone at the top of your organisation by addressing key weaknesses.

provide and apply specific tools that will foster balanced risk-taking in your organisation.

persuade other leaders to define and embody accountability so it becomes a cultural norm.

enhance governance inside your organisation without the need to establish new or stronger policies.

The roles outlined in previous chapters may be new ways of thinking about yourself as a CFO, controller or other senior management accountant. Here are some titles that may help you begin to imagine yourself into these roles:

Chief Strategic Officer

Philosopher King of Finance

Manager of Strategic Planning & Institutional Insight

Chief Planning & Strategy Officer

Orchestrator of Financial Management

Accounting Strategy Leader

Leader of Fiscal Discipline, Insight & Foresight

This book will use “CFO” to name this evolving position; you may find it useful or inspiring to employ one or more of the titles just listed.

CFO = INFLUENCER

An important role for the CFO is to influence his or her employer’s culture for the better. This is not a responsibility you can opt out of.

Each employee with whom you come in contact, and many who simply hear about you, observe how you behave, which influences how they behave. Therefore, as a CFO, you should be well-versed in how a leader influences and even transforms an organisation’s culture.

That is what you will learn in the following four best practices.

Exercise: Who Is Driving Your Train?

Instructions

Part 1: Think of five areas in which your firm regularly faces or takes risks or is vulnerable and list them in the table. Next, enter the name of the person who is responsible for managing the area at risk. Last, think about that person’s individual approach to risk-taking using the following spectrum of attitudes.

Part 2: Answer These Questions

What did you notice about the prevailing attitudes towards risk-taking in the people who are “driving the train” in your firm?

Is the attitude of the person managing your risk area appropriate, too much or inadequate? Is there a balanced view towards risk-taking in your organisation?

Exercise: Brian—part 2

Your task is to take the following two actions:

Read the following “Best Practices” information section. Use this information to devise ideas to help Brian arrive at solutions to his leadership challenges.

You have agreed to be Brian’s coach so that he can be successful as a CFO. Read the “About Your Friend Brian” section.

Best Practices

Issue 1: Shape the Culture by Defining It

Main question:

What cultural structure should Brian put into place so that he can focus more on the big picture, yet know that necessary work will get done? What should his overall strategy be?

Specific questions:

What does Brian need to be aware of?

What specific tactics does Brian need to employ over the next year?

What will Brian need to measure to know that he is effective?

Refer to figure 3-1.

Issue 2: Create Balanced Risk-Taking by Establishing a Risk Programme

Main question:

How can Brian use a defined risk management programme to help this enterprise from throwing good money after bad ideas?

Specific questions:

What does Brian need to be aware of?

What specific tactics does Brian need to employ over the next year?

What will Brian need to measure to know that he is effective?

Refer to figures 3-2 through 3-6.

Issue 3: Foster Accountability by Defining It

Main question:

How can he influence Ruwan and Kimberley to pay close attention to their behaviours so that the firm can pull out of its death spiral?

Specific questions:

What does Brian need to be aware of?

What specific tactics does Brian need to employ over the next year?

What will Brian need to measure to know that he is effective?

Refer to figure 3-7.

Issue 4: Establish a Governance Programme That Weeds Out Questionable Practices

Main question:

How can Brian persuade Ruwan and Kimberley to buy into a governance programme for the entire enterprise so that there is less need for redundancies and controls?

Specific questions:

What does Brian need to be aware of?

What specific tactics does Brian need to employ over the next year?

What will Brian need to measure to know that he is effective?

About Your Friend Brian

Brian knows that stepping up as a leader and influencing the managing directors will help solve many of the long-term issues (issues 5 through 8), that R & K Enterprises faces. If Brian is proactive in setting the tone at the top of the organisation, many of these problems will become manageable.

He needs coaching on determining strategic priorities for the next 12 months.

Issue 5: Ruwan and Kimberley Practice Differing Standards

Certain managing directors and core employees are allowed to ignore internal controls because they are not obligated to report their actions to either Ruwan or Kimberley.

Issue 6: Ruwan and Kimberley Show Favouritism

Kimberley plays favourites when it comes to providing funding and setting goals—and whom she excuses for not meeting goals. Each managing director is required to submit an annual operating plan and goals for each year. Each month they meet face-to-face with Kimberley to go over the plan and goals. Brian has noticed that certain managers are regularly let off the hook when they overspend, do not reach their goal or mismanage resources. Most of these managing directors have either worked for R & K for more than 15 years, are members of one of the families or are long-time friends of Ruwan or Kimberley.

Issue 7: Ruwan and Kimberley Use Inappropriate Metrics

In three largest business units—retail, wholesale and manufacturing — Ruwan, Kimberley and the managing directors focus 100% on profits as their main measure of success. The reason for this, Brian surmises, is that these are the cash cows that feed the trust, fund the purchase of new businesses and cover the losses of the smaller units. The smaller units are measured and managed by operational nonfinancial metrics. These smaller units Brian refers to as the “pets.”

Issue 8: Ruwan and Kimberley Do Not Practice Risk Management

Since they define themselves as owners of a “small business,” neither Ruwan nor Kimberley believe in seeing the downside of anything. They are eternally optimistic and ignore any evidence that goes against this optimism. As a result, Brian is certain that the firm’s insurance agency has placed them in very high-risk classifications.

Brian’s Position Description (Important Elements)

Expected Results

Improve cash flows of the entire organisation by 10% the 1st year, 20% the 2nd year and 30% or more the 3rd year

Create an internal management reporting or scorecard system that provides timely information on each business entity and the entire organisation

Improve the internal controls of all entities and establish acceptable loss levels for each business unit Develop a risk management programme for the entire enterprise in order to reduce insurance costs by at least 25%

Improve the quality and speed of the annual planning process

BEST PRACTICE: SHAPE THE CULTURE BY DEFINING IT

Over time, people are conditioned to mimic the leaders they follow.

Tone at the Top

Throughout human history, stories have been shared about great leaders and what made them great. We speak about George Washington’s humility, Oskar Schindler’s compassion, Confucius’ frugality, Stephen Hawking’s vision, Mohandas Gandhi’s courage, and Eva Perón’s passion.

As a leader, you must tell a story to your followers. It is about them, not you.

The Leader as Proactive Shaper of Culture

The story you tell is the culture you shape around your team and organisation. You cannot help but tell this story because a culture is always a reflection of the leader’s attitudes, behaviours and beliefs.

As proof, take the following test.

Exercise: Your Team’s Story

Instructions

Check all those words that your customers would use to describe your team.

|

Customer-focused |

|

Difficult to do business with |

|

Private |

|

Open and transparent |

|

Fun |

|

Serious |

|

Careless |

|

Careful |

|

Trustworthy |

|

Devious |

|

Disorganised |

|

Organised |

|

Precise |

|

Close is good enough |

|

Risk averse |

|

Risk taking |

|

Creative |

|

Old fashioned |

|

Inconsiderate |

|

Respectful |

|

Technology friendly |

|

Technology phobic |

Answer Key

Whatever descriptions you selected, if you are the leader of this group, these traits also describe you.

CFO Tool: Cultural Ideals

The organisation’s culture can be a leader’s best tool for establishing and carrying out a specific intention.

Five Culture Principles

An unmanaged culture never gets better, it only gets worse.

The culture of a team or organisation is a direct reflection of its leader.

Your organisation’s culture determines the effectiveness or ineffectiveness of your team.

When employees do things that are detrimental to your success, it is the symptom of a major problem. These people are being rewarded for their actions.

A leader cannot ask or force people to adopt the organisation’s values. The employees either have similar personal values, or they do not. Only those who have similar values will live up to the organisation’s values.

Culture defined

Culture is instinctive. Any time two or three people join to work together on something, they create a culture. Culture is the mood, attitude and atmosphere of an organisation. It has an effect on almost every result.

Another way to define culture is to understand “How things get done around here.” You will understand your organisation’s culture by discovering answers to the following questions:

How is change handled?

How are employees rewarded and for what?

How is poor or faulty communication handled?

How are new ideas dealt with?

How is dishonesty dealt with?

How are the goals set?

How are goals achieved?

How hard will employees push to achieve their individual goals?

How do the leaders deal with managers who don’t follow the rules?

How are managers who make ethical decisions recognised?

The answers to questions such as these—the truth, not necessarily what you want to hear—will tell you a great deal about your operational dynamics. Operational dynamics refers to how people communicate, cooperate and coordinate. It is a fundamental way of producing the innovation and fresh ideas needed to keep a business strong and healthy. Understanding what works to help or hinder operational dynamics is a key to leading with intention.

Connect the dots

Every decision, behaviour and action has an effect on something in your organisation. You know this; however, most of the time the impact of these actions is undiscovered or ignored.

If you intend to foster a healthy culture, you must connect the dots for others so they understand the mechanisms of cause and effect. It is almost impossible to isolate the individual cultural component or process that contributes to poor decisions or inappropriate behaviour. Still, an understanding of the norms of your culture will give you information about what employees consider important and their attitudes.

Your corporate culture can be either your ally or your downfall in being a great CFO.

The Story You Tell

If your employees are performing activities not related to the organisation’s values or mission, you must determine why.

As a leader you should pay attention to your organisation’s story, which extends beyond the walls of your building. Employees share the story, not only with each other, but also with customers, prospects, vendors, lenders and the general public. Accordingly, you should examine and consider changing your existing story.

If your current story or culture is one of ethical, caring, productive, challenged and contributing employees, not much change will be required. However, if you are like the majority of employers, your story is one of dissension, silos, information hoarding, miscommunication, clueless leaders, unproductive workers, weak accountability and poor decision making.

If any of these descriptors sound familiar, you should activate this leadership responsibility. If the work your employees transact does not further the organisation’s mission or purpose, the reason is embedded in your story.

Ingredients of a Culture

What you may not know about culture—even though you probably have a good intuitive sense of what it is—s that culture is made up of 10 unique pieces. These 10 pieces fit together like a mosaic, and each one affects the other. They all must be in place for the mosaic to exist, and they must create a cohesive picture or image to be useful.

Your Culture Mosaic

Figure 3-1 is an image showing how the 10 unique mosaic pieces fit together. The centrepiece of all culture mosaics is the leader’s attitudes, behaviours and beliefs. This leader can be an individual, team or family, which is why this is the most important element of each mosaic. Your culture can hide or expose poor decisions, fraud, waste, conflicts and silos.

People are often influenced by stories more than by facts and figures. Each story you tell as a leader must be on target.

This brief summary gave you a basic understanding of culture so you can address your cultural norms regarding how employees face up to their responsibilities. The following case study will illustrate how components of the mosaic fit together in this case, creating a negative situation that led to the company’s visible and painful downfall. Here is a recent one.

Exercise: Washington Mutual’s Demise

The Starting Point—The Fatal Decisions

In 2003, Washington Mutual (WAMU) adopted a corporate slogan of “The Power of Yes.” Around the same time the leaders decided to heavily rely on adjustable rate mortgages (ARMs) because of Wall Street’s ravenous appetite for them and because the accounting rules of revenue recognition allowed them to book all the revenue up front without needing to be concerned, in terms of profit, about the risk of bad debts.

Leader’s Attitude, Behaviours and Beliefs (Tone at the Top)

Kerry Killinger, CEO of WAMU, had a vision. He wanted his institution to be the biggest provider of financing for the American public. He envisioned WAMU being among the top five retail banks. He made acquisitions, one after the other, that helped him fulfil that dream. Some were risky, but he felt the risks were worth it because of his charter to do so as stated in the organisation’s vision and mission.

WAMU’s Vision

“Becoming the nation’s leading retailer of financial services for consumers and small businesses.”

WAMU’s Mission

“Building strong, profitable relationships across a broad spectrum of consumers and businesses. We will do this by delivering products and services that offer great value and friendly service, and by adhering to our core values of being fair, caring, human, dynamic, and driven.”

WAMU’s Values (As Extracted From its Entire Statement)

“We are never satisfied with the status quo and know that we must continually reinvent our organisation and ourselves.”

“We continuously drive operational excellence to innovate our products, processes, and services.”

“We are committed to excellence and the achievement of superior long-term returns for our shareholders.”

“We set high, measurable goals and hold ourselves accountable to achieve them.”

Organisational Structure

With each acquisition it became more difficult to both control and maintain the desired culture consistently, despite their worthy values. Experienced management was spread thin due to the challenges that came with WAMU’s meteoric growth as it went from a one-state institution to a national entity with branches or offices in all 50 states. Branches were opening faster than a fast food chain.

With each acquired bank, more of the branch and office managers were permitted to pursue their own directions as long as they met their goals and performance metrics.

Goals and Measurements

The primary measurements that Killinger and his direct reports used to define success were the following:

Share value

Quantity of loans sold to Wall Street

Balance of loans outstanding

Revenue (when the “Power of Yes” became the mantra, WAMU’s revenue went from $707 million in 2002 to $2 billion in 2003)

Growth (from 1996 to 2002, WAMU grew to become the nation’s sixth largest bank)

Notice they were not measuring the quality of those mortgages and credit card balances. This is because the accounting rules allowed WAMU and other institutions to recognise the deferred interest on ARMs as income without booking any bad debt provision, even though they were on the hook for bad loans. ARMs commanded higher fees than conventional mortgages. When Chase took over WAMU’s portfolio, it estimated that 82% of the ARMs were impaired, as were 15% of the credit card balances outstanding.

The week prior to WAMU’s implosion, Kerry Killinger was bragging to an audience in Seattle about how well the bank was doing.

Customs and Norms

At WAMU, the “Power of Yes” gave employees the tacit approval to make a loan regardless of whether the applicant qualified. The pressure to produce loans came from senior management. Everyone’s job became “getting the job done” (that is, bring in and approve loans while steering applicants to ARMs). Employees’ workloads made it impossible to perform quality reviews, check credit scores, verify income and, ultimately, determine if applicants could pay back the loan. WAMU employees had on average, only 35 minutes available per loan file.

As a loan processor, if you said “no,” the loan application was removed from your desk and given to an employee who would say “yes.” Employees who turned down an applicant were either written up or terminated.

Policies and Procedures

To perform a proper valuation of a residential property, competent appraisal firms generally require about 40 hours. This was not satisfactory for WAMU because it slowed down its loan process. In 2005, a policy change allowed employees engage appraisers who could complete the process faster and cheaper. This led to appraisal work being done by unqualified appraisers who never actually visited the property and often relied on websites to evaluate the property’s worth. If a lower-quality home, on the same block, was worth $300K, while a group of higher-quality homes on the same block were worth $600K, the better homes were used as comparables in determining the value of the property being appraised.

To keep the pipeline of resalable mortgages filled, WAMU lowered qualification standards, especially for those who needed ARMs. If the applicant was alive, the loan would be granted. The policy as extolled by supervisors was, “It is not your job to worry if the customer can pay. Your job is to write the loan.”

The policy on loan application files became, “A thin file is a good file.”

Rewards and Recognition

WAMU paid incentives as high as $10,000 in the form of commissions to agents who brought in applicants and to brokers who steered them to mortgages that WAMU could package and sell.

WAMU’s underwriting employees were urged to fund the mortgage, while the top producers were lavished with rewards and incentives. One high-pressure mortgage centre in Southern California produced $1 billion in loans just in 2004. The team’s leader was lavished with bonuses, along with being a perennial member of Kerry’s President’s Club and receiving multiple awards at the Club’s annual meeting. Other mortgage centre managers wanted to receive the same recognition.

The Ending Point—Lack of Accountability via Denial and Blame

Kerry Killinger to this day refuses to accept any culpability for his role in the demise of WAMU and the harm suffered by thousands of homeowners, investors and employees. Despite pocketing $103 million and refusing to pay back a dime of it, and despite telling the U.S. Congress that he took “full responsibility” for the bank’s failure, Killinger also claimed, “I’m certainly very disappointed to think about my customers [borrowers] lying to me. But that’s fraud, and it shouldn’t happen.”

Sources: The Seattle Times, The Seattle Post Intelligencer, Seattle Metropolitan Magazine, Business Week, Wall Street Journal.

In the End

The good leader builds high morale and creates community in their team and organisation.

Knowing your firm’s culture and how it works will enable you and other leaders to become better leaders. You, when setting the tone for the culture, must understand how the culture you formed affects your efforts to produce results and fulfil the mission. Your culture is not formed by policies and words alone. It is a complex and dynamic mosaic that must be shaped by managing through the 10 mosaic pieces as part of your leadership intention.

Exercise: Does Your Organisation Have These Weaknesses?

Instructions

Place a check by each of the following if you have seen examples of it within your organisation.

YES |

I SEE THIS HAPPENING WITHIN THE ORGANISATION: |

_________ |

Conflict regarding important strategies, goals or policies |

_________ |

Adversarial conditions or silos in specific departments, groups or professions |

_________ |

Information stockpiling or dishonesty by certain individuals |

_________ |

Communication errors that go without being addressed or frequent communication errors |

_________ |

Leaders who do not heed advice, listen to their employees or follow the rules |

_________ |

Unproductive workers, especially people who are permitted to do low quality work or waste time |

_________ |

Low level of accountability toward commitments being fulfilled or low level of accountability with the organisation’s customers and other stakeholders |

_________ |

Poor decision making that is not addressed, corrected or improved |

Answer Key

For each item you checked, you have a damaged story. These problem areas will arise occasionally, but when they become the norm, your culture mosaic has weaknesses in various components. These will negatively affect any goals set or improvements a leader contemplates.

CFO Lesson

Culture trumps policy 100% of the time.

BEST PRACTICE: CREATE BALANCED RISK-TAKING WITH A RISK PROGRAMME

Proper risk management is determining the cost you cannot afford before you take the risk.

Exercise: Self-Test

Part 1 : Answer These Questions

Do you take risks?

How do you know that you do or do not take risks?

Is it because other people tell you that you do or do not?

Is your answer because of your definition of risk?

Part 2: Check Those Activities That You Define as Risky

| I CONSIDER THIS TO BE RISKY FOR ME TO DO: | |

| _________ | Driving a race car at more than 200 miles an hour |

| _________ | Flying commercially once a week |

| _________ | Mountaineering |

| _________ | Deep sea fishing |

| _________ | Driving fast on a busy road |

| _________ | Having children |

| _________ | Pursuing a university education |

Risk Is Individual to Each of Us

Each of these activities will be considered risky by some and not risky by others. For example, many people may consider having a child or 2 not to be risky, but may find 5 or 10 children more risk than they can tolerate. And then there are people for whom the thought of having even 1 child is just too risky. Likewise, a university education can carry a high cost in both money and effort, and at the same time choosing the wrong field of study can lead to underemployment or unemployment.

Your daily trips to and from work may carry a greater risk than you driving on a race track at 200 miles per hour. But which of these activities do you consider more risky?

Diverse Spectrum of Attitudes Toward Risk-Taking

Consider risk taking on the individual level as a range across a spectrum going from “black and white” on one end to “flying without a net” on the other. How you value something will determine where you place yourself on the spectrum. You could be black and white about your finances but fly without a net when it comes to your job. You are not at one place on this spectrum for everything you value, nor do you stay in the same place all your life.

Five Risk Management Principles

The negative impact of risk-taking is greatly reduced when you analyse the real cause of the undesirable results.

Because you cannot control all risks, it is much healthier to be prepared for the worst and expect the best.

People do not take risks because of fear.

Risk-taking is a necessity for individual and business success in this changing world.

What we define as risky is all about the specific value we assign to the “thing” that we place in jeopardy.

The Value of What Is At Risk

As the firm’s CFO you must help define the value of both the tangible and intangible things that are put at risk each day. These include

reputation,

brand,

future,

income stream,

sustainability, and

integrity.

Risk Is Everywhere and Never-Ending

The best place for the CFO to add value to his or her employer’s risk management programme is to help the organisation to define its operational risk appetite.

Operational Risk Defined

Operational risk management looks at the business from the operation itself and is defined as the risk of direct or indirect loss resulting from inadequate internal control, processes, people and systems to react to external events. Financial information is not enough to gauge a company’s overall business risk.

The value of managing operational risk is only slowly gaining recognition. One reason is that by the time the financial impact of management’s misjudgement affects the balance sheet or income statement, it typically is too late to do anything about it other than pick up the pieces. By tracking operational indicators and metrics, leaders can identify opportunities and threats before they affect the company’s finances.

One approach to measuring operational risk requires firms to routinely review many nonfinancial factors such as the quality of corporate governance, employee morale, customer satisfaction, implementation of goals and execution of those goals, the company’s application of technology, and its deployment of those practices. Numerous tools that enable you to easily measure operational risk already exist, such as the balanced scorecard, activity-based costing or driver-based forecasting.

Why Defining Risk Is Necessary

CFOs prove their worth when they assist their firm’s leader in defining, measuring and monitoring the risks that could be costly or disastrous.

Answer These Questions:

How does your organisation define risk?

What is a risky activity or decision and what is not?

How do you and others know?

The Meaning of Risk Has Changed

Boards of directors and other stakeholders of corporations are becoming more wary of risk. To ensure their own job security, CEOs must be more aware of the need to develop sophisticated means to measure and manage everyday business risks. Numerous experts agree that there is less tolerance by stakeholders, especially in public organisations, for executives who do not prepare for a disaster of some sort. This leaves boards, shareholders and executives searching for broader and better ways to manage risk in order to achieve their goals and ensure strategy viability. Thus, the entire organisation must focus on the causes of risk instead of the traditional method of only treating the symptoms or focusing on protection through insurance.

Operational risk management is managing the risk of loss resulting from any of the following:

Inadequate processes or systems

Human factors

External events

Operational risk management requires defining authority and accountability for each sort of identified risk.

In your organisation, like all others, the answer to the question of whether an activity is risky often varies. For example, if you are a start-up company in your first years of existence and your funding is shaky, your definition of acceptable risk is going to be very limited. The opposite could also be true. Because you have little to lose, it may be acceptable to throw caution to the wind. Many successful firms started out this way, like Apple Computer and Microsoft.

If your organisation is well established and has survived at least 15 years, the definition of risk will be much broader and wider. Your leaders may decide that growing by 150% in one year is too risky, but growing incrementally at 30% per year is an acceptable risk.

What if your company is a multi-billion dollar international conglomerate? Your leaders’ definition of risk is going to be extremely different than the start-up’s definition.

From 2007 through today, much of the world has faced a major economic downturn and restructuring of the global banking system. In this painful recession, the majority of our companies operated conservatively, cut expenses and strove to weather the storm, yet a large number of organisations used this difficult period as an opportunity to go on merger or acquisition sprees, to spend more on research and development, to invest in new products or new customers, or to create new channels. Risk is always in the eye of the beholder.

Fundamental Sources of All Business Risks

In managing risk, it is of vital importance for the CFO to be aware of the most basic sources of risk. You show yourself to be a great leader when you spend time examining these sources to look for problems and opportunities, because good governance requires the finance team to do this in real-time.

Source No. 1—Your Firm’s Business Model

Strategic planning is managing change and overcoming risks. Strategic planning is a process through which risk can be identified in advance and dealt with proactively. See figure 3-2 for an example of the strategic planning flowchart.

Figure 3-2: Strategic Planning Flowchart

Strategic planning starts with your mission statement because it sets the organisation on a course and instigates change from today’s status quo to where you want to be in the future.

The second element of strategic planning is your actual strategic plan, the measurement of your mission. In this document you identify specific metrics and methods of measuring whether you are accomplishing your mission over the next 18-24 months.

Information from the strategic plan flows into the operating plan, which identifies the technology, facilities and people you need to achieve each specific objective in your strategic plan. The operating plan is where you are headed and what you will commit to accomplishing in the next 12 months.

Out of your operating plan comes your financing plan. In this document you highlight the methods of payment for the technology, facilities and people in your operating plan. For instance, how much capital will come from internal sources and profits? Will some of the funds come from outside investors? Will additional funding be required from banks or other lenders? Your financing plan will address these questions.

Finally, from the financing plan, you develop your budgets: the operating budget, the capital budget and the balance sheet budget. These three documents become your control and feedback systems over the risks and changes that you started with your mission and strategy. An overview of a risk management programme is outlined in figure 3-3.

Figure 3-3: Proper Risk Management Programme

Your global risk management programme consists of your operating plan, inancing plan and the three budgets (see igure 3-3). What goes badly wrong in many organisations today is that the leaders see risk management as a function of insurance. This job is assigned to a senior management accountant or a risk manager, a position that today many irms have outsourced or eliminated. The risk manager is rarely included in the strategic planning process. This means that your executives embark on a global plan, ignoring risks or underestimating their cost, and then turn the risk analysis over to the senior management accountant or risk manager. They drop it on that person’s desk and ask, “Do we have adequate insurance coverage for this particular risk?”

This is a fatal blunder.

As you can see from the strategic planning flowchart, the risk management programme must be a main agenda item of strategic planning done offsite when the leaders decide the next year’s plans. This is also the time they define what risk is. Good and effective risk management, like governance, requires a team approach. An effective programme consists of a cross-functional team of people throughout the organisation who examine risk holistically.

Source No. 2—The Mindset of the Risk-Taking Entrepreneur

Whether it’s a defensive reaction or simple optimism, most business owners refuse to contemplate the possibility of failure. It is as if the word does not exist in their vocabulary. This attitude can be ruinous, wasteful and costly; hurt people; and spoil opportunities for future success. Most entrepreneurs see themselves as the types of people who put their heads down and charge full steam ahead. However, you can badly injure yourself with that mindset. This person does not avoid risk, but ignores it at every opportunity. This person does not recognise that failure is an option. This is why risk can be mismanaged or unacknowledged.

In understanding the possibility of failure in risk-taking, there is a very delicate line to walk. It is better to assume failure can occur than to resign yourself to it. It is acceptable to acknowledge our fear but not let ourselves be overcome by it. Walking that line requires courage.

Source No. 3—the mindset of the Risk-Averse Person

Though many people prize and value those who take risks, there are groups of people who tend to be risk averse. Risk avoidance comes from two human concerns: (1) all people hate to lose money, and (2) all people hate to look incompetent. People in management accounting own the mentality, “I am the guardian of the assets,” and this attitude often leads us to look at risk differently than anyone else.

When you make a critical decision on taking a risk, your decision is composed of the following:

How emotional versus. how rational you are

How confident versus how anxious you are

How impulsive versus how reflective you are

Risk is inherent in almost everything that a business does, including expansion, mergers, research or contraction. Therefore, no matter how much a decision is researched, a typical management accountant must understand the fact that uncertainty will always exist in any strategy and decision.

As CFO, you want to make sure that you do not do anything irresponsible. But that is very different from taking a risk. Your job is to put forth the best alternative, suggest the pros and cons, identify the opportunities that we seek, and then show what the future could look like in both scenarios. While evaluating this risky situation, we must watch for potential gains or upsides as well as potential losses or costs.

Management Accounting Sits in the Middle as a Fulcrum

Management accountants, especially as controllers or CFOs, are a fulcrum of the organisation. They are in the midst of a delicate high-wire act and must make sure that they manage this balance very carefully. They cannot afford to push the organisation too far on one side. If they solely focus on the controls and checks and balances or are perfectionists about people crossing all the T’s and dotting the I’s, they foster a culture in which no one is willing to take any risk. History is littered with businesses that were unable to out-innovate their competitors or keep up with the evolving marketplace.

On the other side of the balancing act, we have employees and leaders who want to be innovative, strive to be creative, and push the envelope on innovation, ideas and processes. Our job is to support them and not let them undermine the success of the organisation.

CFO Solutions to make People Aware that Risk exists

Solution 1—Wisdom Sharing

Share best practices across your organisation. For this sharing to occur, your culture must be one of openness, with managers as interdependent partners within the risk environment. This partnership must include employees from the operational side of the business and employees whose advice is often ignored such as the audit, inance, human resource and risk management teams.

Solution 2—Governance Structure

Implement a governance structure. This is an integral part of the irm’s operational risk programme. Governance promotes cultural transparency and openness together with demanding accountability from each employee, each operating unit and every support function.

Solution 3—measuring What Is Important

Identify, collect and monitor a balanced set of critical performance indicators or metrics that help the leaders to identify control issues and allow for early mitigation. This solution is also important to operational risk management.

CFO Solutions to make People Aware that Risk Can Be Survived

Solution 4—knowing What Is Risky and Why

Unless an employee can quickly identify why something is risky, they will not become aware of alternatives to pursue until it is too late. Provide each employee with this next tool and teach them how to use it before they leap into the unknown.

CFO tool: Risk Identification

This is a two-part tool using questions and a flow chart that will help you, as a leader, look at risk differently. Part one of the tool is six very important questions that need to be asked before a risk is undertaken. Part two is called the critical risk path. Walking this path step-by-step before the organisation takes a major risk will help leaders and others make more intelligent decisions.

Part One—A ddressing Tough Questions

Figure 3-4 outlines six critical questions associated with determining risk.

Figure 3-4: Critical Risk Questions

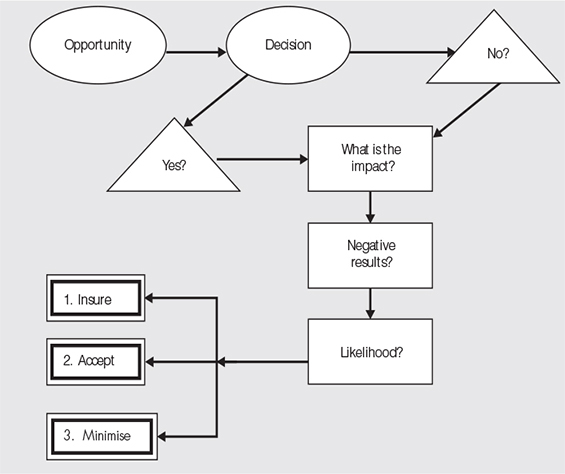

Part Two—Defining the Critical Risk Path

Once you have determined a risk’s likelihood (see critical risk path diagram figure 3-5), you move to the choices you have in addressing the risk. One option is to accept it. Another option is to minimise it. There are plenty of actions to take before undertaking the risk to keep its impact or cost low. A third option is to insure, but that does not mean that insurance is your only option. Sharing the risk, such as partnering with another irm or putting a stop-loss through a limited investment of both time and money, is a way to insure the risk.

Figure 3-5: Critical Risk Path

Best of all, your three options are not mutually exclusive. For example, you could accept part of the risk, insure part of it and closely manage it so that you minimise the potential downsides.

Solution 5 — knowing How to manage a Risk

Once the risk has been identiied and employees understand that they need to address it now, not later, they will need guidance on how to react. Provide all employees with this next tool and train them how to use it so they can become aware of each risk and its impact.

CFO tool: Selecting the Right Strategy

Figure 3-6 helps you to quantify risk based on two variables—likelihood and negative impact.

Figure 3-6: Risk Strategy grid

This risk strategy grid is a matrix that is often used to assist decision makers to foster smarter decisions. It applies to everyday risk management as well.

Not having an exit plan can have negative effects. Some organisations continue to dig themselves into a deeper hole in that the leaders refuse to believe that failure can happen. The belief that “failure is not an option” worked ine for the irst space voyagers, but very few shareholders exist who support executives who throw good money at bad opportunities. There were a lot of dotcom executives whose only business model was to set up a company, and then have an IPO so they could cash out as millionaires. When their business model proved to be worthless, they did not have alternatives lined up.

In the end

Organisations that incorporate proper risk management into their daily operating strategy achieve better returns and help to stabilise their earnings. By employing this best practice and the tight controls built into it, your company avoids the pain of people who colour too far outside the lines or who underestimate the cost of a speciic risk.

To avoid any negative outcome and promote shareholder conidence, the organisation’s leaders must instil transparency regarding the risks that the organisation is undertaking; especially those that will build but also harm shareholder value. Incorporating risk management into your culture will result in leaders being able to trust and empower employees more.

Exercise: Do We Manage Risk Well?

Instructions

Complete this self-test to see if you are adequately managing the everyday risks that your organisation faces. Place a checkmark next to the questions that you answer with a definite “Yes.” Compare the total number of boxes you checked with the answer key at the end.

_________Am I able to sleep at night without worrying about risk in my organisation?

_________Do I have a clear understanding of firm-wide risk, the organisation’s key areas of vulnerability, and our ability to recover quickly?

_________Am I confident that an accountable executive is addressing each risk, large and small?

_________Is there a process or function within my organisation that is responsible for assessing, measuring and monitoring risk?

_________Have we created a realistic balance between innovation and protection?

_________Do our cultural norms help us ensure that all costly risk is identified before we take it?

_________Does my organisation have an operational system or process for evaluating risk?

_________Do I have complete assurance that financial and operational controls are being used as designed?

_________Does a thorough and appropriate reporting mechanism exist that allows for an adequate checks and balances system for sparking fresh ideas, fraud prevention and managing risk?

_________Do I have assurance that financial and other information is reported correctly?

_________Are our processes for risk assessment, management control and governance evaluated and reviewed for both efficiency and effectiveness on an ongoing basis?

_________Is there an emphasis and supporting process within my organisation for aiding productivity and for improving operations?

_________Are my organisation’s stakeholders provided with reliable assurances that their investment is protected by ethical and sustainable means?

_________If I were not part of the organisation, would I be comfortable with the assurances provided to me as an outside stakeholder or investor?

_________Do we have a specific written recovery plan in the event that we suffer as a result of a major risk?

Answer Key

13-15 checked—Congratulations!

You have a high Risk IQ. Keep doing what you are doing and improve those areas you did not check off. 10-12 checked—Good job

You are effectively managing your risk but are still vulnerable in many areas. Get started on removing those weaknesses today.

7-9 checked—Scammers love you

You have many areas of vulnerability. Start addressing them immediately.

0-6 checked—Sharpen your resume or CV

Your company may be out of business soon.

BEST PRACTICE: FOSTER ACCOUNTABILITY BY DEFINING IT

It is impractical, even impossible, to hold an employee to a standard that is never defined for them.

Accountability From a Leader’s Perspective

Fostering accountability is a skill that all leaders and most management accountants need to be better at. You can easily and significantly influence accountability when you understand it at a deeper level.

Exercise: Are You Accountable?

Everyone in your department is talking about a story, usually a rumour, about what the CEO did over the weekend.

What is the proper course of action?

Choose:

_________1. Listen to the rumour and share the story with others.

_________2. Urge your coworkers to stop listening to and spreading the rumour.

_________3. Ignore the rumour.

_________4. Tell the boss about the rumour being spread.

_________5. (Enter your own choice)

In what ways are you accountable in this situation?

In every situation you have a choice. Accountability is enhanced when you make the responsible choice based upon high standards and a commitment to being good. Much of the time, we don’t think about our choices and their impact, and our accountability weakens.

Accountability Is Often Misunderstood

Many people talk about the need for accountability but often cannot define it. Instead, we assume that we and others know what accountability means.

What Is Accountability?

Following are three realities about accountability.

Accountability Reality 1—In order to effect accountability in others, we have to take an honest look at ourselves and understand how others see us.

Accountability Reality 2—Issues of accountability are all around us. It is important that we become aware of them.

Accountability Reality 3—Many people think they are accountable. They are most likely being responsible, but as they define it.

To further understand accountability, review these important principles.

Five Accountability Principles

Everyone is born without an understanding of accountability. We learn it from the people around us. If they have it, we learn it. If they lack it, we do not learn how to be accountable.

When we are accountable, we own all our obligations and duties. We don’t rent them.

The level of accountability in your organisation is an indicator. Lack of accountability indicates that your organisation has weaknesses or does not support accountable behaviours.

Strengthening accountability starts by examining our own actions and attitudes. If we are not changing for the better, we are changing for the worse.

Strengthening accountability starts with you.

Accountability Defined

Accountability is keeping your word, meeting your commitments and taking full ownership for your actions. Accountability is accepting reality without finding fault, placing blame or hiding from the truth.

The most important aspect of accountability is standards. When you clearly set a standard for someone to live up to and he or she meets or exceeds that standard, then that person is accountable. When the person does not meet that standard, despite having the ability to do so, that person is not being accountable. Therefore, when you do not live up to your own standards as defined by your values, then you are not being accountable to yourself.

True leaders hold themselves accountable.

Everyone Is Involved in Instilling Accountability

An entire group of people is necessary to help hold someone accountable. This applies at all levels: family, team, company, community and society. At its very essence, accountability means accounting for one’s own actions. Whenever you say that you want someone to be accountable, in effect you are saying, “I expect you to account to me for the action you took or the decision you made.”

Where Accountability Fits In

To better understand how these individual pieces fit together, review figure 3-7, the accountability target.

Figure 3-7: Accountability Target

Leaders of organisations desire employees who think for themselves and are self-motivated. To achieve this goal, it is important to first look at the centre of the target. At the core, the team member chooses to be or not to be responsible. This person takes responsibility for his or her actions, decisions and behaviours. Like an apple, if the core is rotten, the apple is of no value to anyone. Similarly, if the employee takes no personal responsibility, you will be unable to develop a self-activated employee.

From the centre we go to the next ring, accountability. This is where the leader expects employees to be accountable for their actions and behaviours and support the team and the team’s decisions.

From accountability we go to the next ring, empowerment. This is the level where the leader creates a team or organisation culture that tells the employees they have the freedom and flexibility to take matters into their own hands, with certain limitations. Employees know that they will be held accountable for their actions and decisions but also know that you will support them should they make an error in judgement.

At the outermost ring of the target is a level of self-activation. Employees understand that they have been empowered and use this mantle of authority to look for things that are not currently being done, or intercede when there is a vacuum of leadership. One of the hallmarks of “employer of choice” organisations is that leaders emerge whenever they are needed. Organisations create self-activated employees because they are empowered, accountable, and, most important, take personal responsibility seriously.

If the core is missing, you will never foster accountability, empowerment or self-activation.

The Undefined Standard

You tell your employee: “Fatima, I want you to be more accountable.” Fatima’s automatic response is: “Accountable to what?” Your face-saving answer is: “You know what I mean.”

The sad fact is that Fatima does not know what you mean.

As you saw in the previously discussed principles, learning what accountability means starts in your childhood, and its context is defined by your parents and other adults in your life. Therefore, if you have 200 employees in your organisation and you say globally: “I want you all to be more accountable,” these 200 individuals will default to their own definition unless someone has proactively and clearly defined accountability.

It is a duty and obligation for your organisation’s leaders to establish what accountability means as it fits into your organisation’s cultural ideals.

Enhancement Requires a Common Definition

As you read earlier, enhancing or strengthening accountability within an organisation starts by establishing realistic standards, with great expectations, for employees at every level. High levels of accountable behaviours are a direct result of four ingredients.

The expectation for each person to behave in an accountable manner is embedded as a cultural norm.

A unanimously accepted definition of what accountable behaviour looks like within and without the organisation.

A methodology for holding each person to those standards and weeding out those employees who do not live up to this expectation.

A screening process that determines if a prospective employee can and will buy into this cultural norm.

Before delving into leaders’ and influencers’ role in strengthening accountability, take a look at why it is beneficial to embed accountability into your organisation’s ongoing story.

Why Accountability Works to Make Everyone Successful

While it may seem obvious that accountability helps to build a successful team and company, it may be useful to review a few of accountability’s most important benefits. High levels of accountability

establish individual integrity.

contribute to corporate integrity.

ensure employees follow through on their commitments.

guarantee people can rely on the team and one another.

allow team leaders to spend less time acting as their employees’ supervisor.

build employees who are dependable, yet can act independently.

remind employees to hold themselves and each other accountable.

How Leaders Improve Accountability

Because accountability is something that is affected by what leaders do and say, it is very important for leaders to take the first step and model accountable behaviour. This section provides a few specific suggestions of things that a CFO or controller, as team leader and executive, can do to show that he or she takes accountability seriously. By modelling these behaviours, these leaders communicate the expectation that grants them the permission to hold others accountable.

These three suggestions are explained in the following sections.

1. Monitor Your Own Actions

Meet all your own commitments.

Be consistent in your words and actions.

Catch people doing things right.

Identify and remove barriers to honesty.

Be open to new ideas.

As a leader, you must be very self-aware of each thing that you do and say. Leaders are very visible, and employees take their cue about acceptable behaviours from them. For example, if you refuse to engage in blaming others but instead immediately move to resolution, you show others that this is the accepted norm. If you support every policy, even the ones that affect you negatively, you model that everyone needs to support the organisation’s policies.

2. Use Honesty

Instil and value honesty in others.

Accept differing opinions and views.

Seek solutions instead of blame.

Give timely and honest feedback.

You must always tell the truth. Of course, there will be information that employees do not need to know or must be withheld for legal or strategic purposes. Even in these cases, however, you must always strive to tell the employees the truth. This does not give you permission to be blunt and rude. Leaders use tact when being honest. By being honest and expecting honesty back from others, you set the expectation that you value the truth. O ne thing that almost every human being on this planet despises is a negative surprise. Honesty helps to decrease the likelihood of that occurring.

3. Hold People’s Feet to the Fire

Give employees authority with responsibility.

Require employees to meet their commitments.

Do not accept excuses for less than full efforts.

Set measurable targets with each employee.

Let employees know exactly what you expect from them.

Do not use excuses for your errors and mistakes—own up to them.

10½ Rules of Accountability

Issues of accountability are all around us. The starting point is awareness.

Without a common, understood and accepted definition of accountability, I will never be able to effect any change to it.

Accountability is a nebulous concept until we define what it means for us. It is like quality—“I know it when I see it.” A common definition gives us a basis for understanding and communicating.

In order to encourage accountability in others, I have to take an honest look at myself first and understand how others see me and my actions.

Before I can do anything about my organisation’s accountability, I must open my eyes to the level of accountability my team demonstrates in our daily actions and decisions.

Improving accountability in others begins when I choose to be accountable each day.

Once I decide to question another person’s accountability, I automatically give them permission to question my accountability.

When we find fault with each other, we decrease accountability. Focusing on the problem or issue without placing blame will help us to create solutions more quickly.

If we focus on what is not working and place blame for things that go wrong, we won’t move forward in enhancing accountability.

We become immersed in our culture and soon lose sight of its make-up. It is critical to step back and regularly reexamine our organisation’s cultural ideals to see if they are building or hurting accountable behaviours and decisions.

10½. Strengthening accountability starts with me.

Exercise: self-Test: Are You Accountable?

Instructions

Part 1: Rate yourself on a scale of one to seven for each item to determine if you demonstrate accountability with your actions. Do not guess; be brutally honest and see yourself through the eyes of those you work for and with.

This is how well I show integrity. My family or best friend would say

This is how well I take responsibility for my actions. My family or best friend would say

This is how I take ownership of my results. My family or best friend would say

This is how often I place blame or find fault. My family or best friend would say

This is how I feel about my future. My family or best friend would say

Answer Key:

If most of your responses are 6 or 7 you might be in denial about your commitment to being accountable. At times you will play the victim or feel like blaming others because you are human. Being in denial is the first sign of someone who lacks accountability.

If most of your responses are 1 or 2, you are being too hard on yourself and could benefit from a more objective view.

If your responses were 3, 4 or 5, you understand what accountability looks like and are self-aware about your behaviours.

Part 2: Answer This Question

How accountable are you? How well do you demonstrate to others your commitment to being accountable?

BEST PRACTICE: ESTABLISH A GOVERNANCE PROGRAMME THAT ELIMINATES QUESTIONABLE PRACTICES

Weak governance is self-perpetuating and self-expanding.

Quiz

What is governance?

_________ A book of our policies and code of conduct

_________ Our system of controls

_________ A system of checks and balances

_________ Having a police chief

_________ Something our code of ethics addresses

_________ All of these

_________ None of these

Correct Answer:

All of these and none of these. This is not a trick. By the end of the section you will understand why both of these answers are correct.

Controls or Policies Are Not Governance

Today, the following are expectations placed on the management accounting profession:

The public expects us to prevent fraud.

Our employer expects us to increase the bottom-line.

Oversight agencies expect us to ensure transparency.

Boards of directors expect us to provide better governance.

At the same time, a small group of individuals have tarnished this profession’s reputation because of illegal and unethical acts.

Society demands transparency from the CEO. So the CEO and the board look to their finance group to create the infrastructure of governance.

Governance Defined

Governance is a high level governing philosophy; thus, an organisation’s leadership body has a primary responsibility to guide, direct and shape how its organisation is operated and led. Governance is not a policy manual, list of procedures, code of conduct or system of internal controls. In fact, it is not any specific written document.

Governance is

a philosophy,

a commitment, and

a promise.

The organisation’s leadership body defines for its shareholders, vendors, customers, employees, the public and themselves how it intends to protect the trust placed with it. It promises to follow this definition and back up all promises with a commitment to play “the game” fairly.

The Game of Business

Because the leadership team is the body that establishes the tone, sets the rules and decides how to keep score, it controls the game. Governance is a public communication about how the leadership team will ensure the game is honest and fair. No one wants to be involved in a game that is rigged and the outcome fixed in advance.

Your organisation’s stockholders are placing their bets on your organisation that they have a fair chance to win, that is, they will be rewarded for putting their money on the line and investing it in you. Therefore, anything that your organisation does to harm the stakeholder’s trust communicates: “We don’t honour the trust you placed with us.” Organisations that do not practice good governance tell stakeholders, “We need you but we don’t care about you. We are more important to our success than you are.”

Today’s Organisation Is Complex

An organisation is made up of the following:

Tangible assets

Capital

Technology

Buildings and facilities

Debt

People

Intangible assets such as

ideas,

energy,

brand,

reputation, and

potential

Processes and systems

Communications

Promises

And much more.

Notice that some of these items are measurable and many are not.

Best and Highest Use

This is why governance is a philosophy. When your leadership team establishes governance, it decides how to best use all these resources to accomplish the organisation’s mission.

Makeup of a Governance Programme

Governance is built around the organisation’s mission or purpose. That is always the first component. The next component of governance is corporate values. Values are the selection and publication of the behaviours that make the mission achievable.

Core Value Defined

A core value is a highly prized trait or quality that, in an organisation, defines how its mission will be fulfilled. The mission sets your people on a journey. Your core values explain how you and others on this journey must behave.

Corporate Culture’s Role

The third component of governance is culture, which is also known as “the tone” and is made up of 10 mosaic components.

In proper governance culture is important because

your firm’s culture impacts almost every result from profits to accountability, ethics to risk taking.

your firm’s culture brings forth success or failure with equal efficiency.

Culture is covered in the first best practice in this chapter.

Morale Is Vital in Governance

Recently, a consultant in the human resources field cited several U.S.-based surveys that found more than 80% of employees are unhappy at work because they do not like their jobs or employer, and they are actively looking for something else. Similarly, 82% of executives are currently looking for new jobs.

Answer These Questions:

Assume that one of your executives is searching for a new job.

Is this employee likely to be concerned about the success of your organisation?

Is this employee looking out for your company’s best interest?

Assume that your best employee is unhappy and cannot wait to leave.

Would he or she likely be concerned with controls?

Culture Must Never Be Downplayed

Culture is important because it exposes governance breakdowns rather than hiding them.

The Culture Statement

This is the tool used to define the desired culture. Chapter 4, “Step 4: Improve Your Team’s Effectiveness Through C oaching,” discusses this important governance tool.

Furthering the Makeup of a Governance Programme

After the mission, values and culture statement, the governance programme extends the overriding philosophy to

processes,

policies,

strategies,

plans,

goals, and

relationships.

The final component is your system of controls—operational, financial and external. All components are put into place to ensure that everyone in the organisation behaves themselves and lives up to the philosophy your leaders have established.

Following are graphical and metaphorical explorations of governance.

The Active Atom

Like a useful yet volatile atom, your firm’s governing philosophy must harness and employ the energy of items that manage the enterprise, while preventing the atom from turning into chaos.

The Human Element in Governance

People are the unknown factor of managing and leading as it relates to governance.

Governance Controls this Unknown Factor

People pursue their own self-interest. When their self-interest is in agreement or alignment with their employer’s, they will follow the philosophy. When an employee’s self-interest does not coincide with the employer’s, the governance programme must help the leaders discover this lack of alignment so they can deal with it.

Cost of Governance

By now, you may be thinking that the governance programme is an expensive and time-consuming endeavour and that only large organisations can afford to have one. If you think this, you are incorrect. Remember, governance is a philosophy.

In small and medium-sized organisations, establishing the governance programme is easy, provided it is done properly. You can have a good governance programme without incurring a high cost. The cost is putting all the elements of your active atom containment system in place and then monitoring them ensure that they propagate the leaders’ governing philosophy.

Exercise: Does My organisation Know Governance?

Instructions

Complete this self-test to see if your organisation currently has adequate governance.

Check “Yes” only if you can answer with 95% assurance that this occurs in your organisation.

Check “No” if you are unsure or know that this is not taking place.

QUESTIONS TO ANSWER |

YES |

NO |

Have our executives taken the time to implement a governance programme in our organisation? |

||

Have our executives established clear expectations about the ethical standards of how we do business? |

||

Do we have a proactive board of directors that holds executives accountable to doing what they say they will do? |

||

Are employees who don’t follow policy or break the rules called to task timely and appropriately? |

||

Does our executive body define for everyone the cultural norms it desires and then demonstrate these in its daily actions? Examples include honesty, openness, trust and ownership of results. |

||

Totals |

Answer Key

If you answered “Yes” less than four times, then your organisation does not have a viable governance programme.

Because governance is an area in which the finance function plays a major role, it affects your entire team’s effectiveness as well as your ability to rely on the system of internal controls.