CHAPTER 6

The Gift of Security

LIFE INSURANCE

You don’t even want to read this chapter, do you? I say life insurance, and you immediately get a picture of someone in a plaid short-sleeved shirt accented with a squared-end tie and maybe even a brown corduroy jacket with the elbow pads and a serious comb-over. You picture someone sitting across the kitchen table launching a guilt blitzkrieg with a hefty price tag in your direction. You picture someone who has as much conflict of interest as the hungry lion circling the wounded wildebeest on a National Geographic show.

You may be partly right, but that doesn’t mean you can ignore the duty of properly managing the financial risk associated with death. There are certainly times when properly managing risk warrants or even mandates the transfer of that risk with—you guessed it—life insurance. If you are already financially independent, you have self-insured the financial risk that you might die prematurely. However, if you are a young parent with a good income but not enough saved to keep paying the bills indefinitely if you leave this earth, you need to purchase some life insurance. We will give you the guidelines required to begin making this decision.

Ultimate Advice

As Red Stevens learned in “The Gift of a Day” in The Ultimate Gift, discussions of financial protection from death need not be a morbid topic, but can instead lead us to life-giving discussions and decisions.

It is not easy to talk about life insurance because it’s not easy to talk about death. It is especially difficult to pin a numerical value on a person, but that is precisely what we do with life insurance. It is important now to recall the lesson we learned in the first chapter: Money is not powerful, but your relationships are. The point of life insurance is not to “buy off” someone’s pain and suffering after the loss of a loved one; it’s to provide financial stability so that the survivors don’t have to worry about money and can instead properly mourn their loss. I encourage you to have deep and meaningful thoughts and discussions surrounding the topics of life and death, but when you are doing life insurance planning, an objective approach is wisest.

Timeless Truth

Life insurance is not a way to get rich, nor does it really insure your life or eliminate the risk of your death. Fear is often used to sell life insurance, and please remember that if someone mailed, e-mailed, or phoned you regarding insurance, he or she is an insurance salesperson. There’s nothing wrong with being a salesperson. It is an honorable, highly paid vocation; but it is important to realize that salespeople sell products. They don’t necessarily assess needs, manage risks, or conduct financial planning. To a man with a hammer, everything indeed looks like a nail, and to an insurance salesman, every human being with a pulse looks like a potential customer.

I hate to be the one to tell you, but you and I and everyone we have ever met are going to die. The act of dying, in and of itself, does not create a need for insurance, but the result of your death may. Life insurance could more aptly be named income and expense insurance as these are the risks it covers. Life insurance exists to provide money that you or your family do not have. If you already have the money that will be needed, having insurance is like carrying two umbrellas on a sunny day. Never insure a risk you don’t have.

Jim Stovall

What is life insurance and how did it come to be? As mentioned in the previous chapter, insurance is a form of highly sophisticated gambling. You’ll remember that an insurance company throws you into a pool with many others like you. In this case, the stakes are clear. The insurance company makes a bet on the probability that you are going to live—or die. They calculate how much premium they need to receive from their pool so that they have enough money to pay a benefit to the probable number of families who are likely to lose a loved one in a particular time frame, and collect a handsome profit on top of that. The sale of life insurance in the United States dates back to pre-Revolutionary times, when Christian organizations created risk pools for the underprivileged in their communities.

First, let’s view life insurance through the eyes of a risk manager.

- Risk avoidance: Regarding the financial impact of death, risk avoidance is extremely difficult. Unless you intend to go out like Elijah in a chariot of fire, I must deliver the sobering news that you will eventually die. This reality renders the risk avoidance method of life insurance quite impotent. There is a place, however, for . . .

- Risk reduction: You reduce the risk of the negative financial impact of an unexpected death by being proactive about your pursuit of good health. In addition to lessening the risk of a heart attack at a young age, for example, you will also be significantly reducing the premiums that you do pay on any life insurance you own. In the eyes of the actuaries, smokers have effectively submitted themselves to a virtual guarantee of an early death, and their insurance premiums can as much as double to reflect that increased risk.

- Risk assumption: It is not only possible, but probable, for any individual or family who reaches a level of financial independence to assume some or all of the financial risk of death. Although the insurance industry has tried to convince each generation that we’ll always have a reason to own life insurance, their postulation is self-serving and dead wrong (pun intended). If the empty-nest retired couple is debt free and completely self-sufficient with their sources of fixed income and their investment assets, they don’t need any life insurance, though they might want some (more on that later).

- Risk transfer: Life insurance, the featured topic in this chapter, is the optimal way to transfer the financial risk of death once you have exhausted the previous risk management measures.

Like all of financial planning, there is both a science and an art to life insurance planning. While there is enough subjectivity in the thought processes surrounding life insurance to create an exception for nearly every rule, we will begin by separating the various reasons to purchase life insurance into concrete needs and wants. Life insurance needs are that which would allow the surviving family members to continue on, unencumbered by the financial loss of the deceased. If no one else is reliant on your financial wherewithal, you have no life insurance needs. Life insurance wants, then, are anything else that would further improve your situation beyond what it is today. Let’s look at the primary examples.

Life insurance needs:

- Final expenses

- Payment of debts and mortgages

- Education for children

- Needed income replacement

Life insurance wants:

- Pre-insurance

- Build cash value

- Estate creation

- Wealth replacement

- Charitable bequests

Until you have addressed your life insurance needs and all other financial planning priorities, you need not be concerned with life insurance wants. The other financial planning priorities discussed throughout this book are 1) mastery of the three Personal Financial Statements and their perpetual implementation; 2) adequate emergency reserves specific to your situation; 3) ensuring that all of your insurance needs are met; 4) contributing the maximum to your 401k(s); 5) contributing the maximum to Roth IRA(s) or an equivalent liquid savings account if you’re beyond the Roth income limitations; 6) contributing enough to 529 plans or an equivalent for education savings; and 7) contributing to a “freedom” liquid investment savings account. I estimate the annual cost of these priorities at over $70,000!1 Therefore, until you have an annual household income of more than $250,000, or you have otherwise been blessed to amass an estate in the millions, you may rid yourself of the concerns associated with life insurance wants and the bells-and-whistles insurance policies accompanying them.

![]() Economic Bias Alert!

Economic Bias Alert!

When I went through sales training to be a financial advisor with one of the best insurance companies in the world, I was told in no uncertain terms, “If anyone ever asks you the question, ‘Do I need insurance?’, no matter who they are or how old they are, the answer is always a resounding yes!” When your income is derived solely and directly from commissions made on the sale of insurance, it only makes sense that these types of tactics exist.

Let’s examine how you can determine how much life insurance it will take to cover the basic needs:

- Final expenses are the costs incurred to make viewing, funeral, and burial arrangements. This cost can be estimated between $15,000 and $25,000. We’ll compromise at $20,000. Some families will be able to self-insure this expense, but many will need to account for it in their life insurance planning.

- Payment of debts and mortgages sets the surviving spouse or other heirs free from their largest and most demanding bills. The amount of life insurance for debts and mortgages should correspond directly with their balances. While it may be appropriate for some spouses to take these funds and pay off the mortgage, it may be optimal for others to keep the cash, invest it, and use the income and gains to help make the mortgage payments. This is an individual decision and should not be made until after the first year has passed since the loss of the loved one. During that time, the life insurance proceeds should be kept in a liquid account with U.S. government protection. Certificates of deposit (CDs) are a logical choice, but be aware that Federal Deposit Insurance Corporation (FDIC) protection has its limits. FDIC limits are currently set at $250,000 per bank per account type per bank.

- Education for the children is for expected costs of private elementary or high school education and especially college. Throughout our life insurance planning, we’re going to assume a “safe” rate of return of 5 percent for the invested life insurance benefit. The cost of education is also thought to rise at a rate of approximately 5 percent, so we’ll want to have enough life insurance to cover the cost of every year of expected education in today’s dollars. Therefore, if you have two children, ages nine and 11, who are attending public elementary and high school and then going on to an in-state, state university currently costing $15,000 per year, you will want $120,000 of life insurance to cover the future costs of education. If you send the same two children to an expensive private school (say, $25,000 per child per year) and expect them to go to your alma mater, Harvard (more than $50,000 per child per year), then you’ll need at least $800,000 of life insurance simply to cover future education costs. We address saving, planning, and paying for education in Chapter 12.

- Needed income replacement is going to be less than 100 percent of the spouse’s income since our calculations have already prepaid debts, mortgages, and education. With those major expenses covered, most people will only need to replace approximately 50 percent of the deceased spouse’s income. (This multiple will vary depending on the income of the decedent and the lifestyle of the family.) So, if the primary wage earner in the single-income household had an income of $100,000, you should use life insurance to recreate a $50,000 income going forward. We’ll again use the 5 percent rate of return assumption, and seek to create a $50,000 income stream from the amount of cash that—earning 5 percent—would satisfy the income need. In order to determine what lump sum earning 5 percent would generate $50,000 of annual income, divide $50,000 by 5 percent (.05), and the answer is $1,000,000. Properly invested, this amount will hopefully take care of the income need into the future.

Timely Application #1

Life Insurance Audit

The first step in your personal insurance analysis is to figure out what you own (or have) currently by conducting a Life Insurance Audit. Yes, it’s possible to have some even if you didn’t buy any as most companies give you a relatively small group life insurance policy at no charge.

Collect all of your existing life insurance policies and the most recent annual statement corresponding with each. These documents are filled with legalese and jargon, but they also contain almost everything you need to know about your policies. Create a chart using the template provided on our web site with the pertinent information from your policies, including the following: inception date, type of insurance (term, whole life, universal life, or variable life), length of term, death benefit, cash value, and surrender value.

There are two additional documents associated with permanent life insurance policies (whole life, universal life, and variable life) for which you’ll need to contact the insurance company. These are an In-Force Illustration and a Cost Basis Report. I recommend calling the company’s customer service number instead of calling your agent directly, because most agents know the request for these two documents is often the indication someone is investigating the viability of the policies they sold. (They’re right.) At the least, their judgment is being called into question. At most, they may also be losing residual commissions.

The information you collect will be combined with your Timely Application at the end of this chapter to help you conclude which policies you should keep, what additional policies you may need to apply for, and which policies you should surrender. (NOTE: You should never surrender any existing life insurance policies until you have determined your needs and applied for any additional insurance needed.)

Visit www.ultimatefinancialplan.com to find a template to use for your Life Insurance Audit.

Tim Maurer

Next we’ll examine the most common family paradigms and provide a framework to use in making your life insurance decisions for both your needs and wants.

Life insurance should be simple, but it’s typically not. Made complex by companies and agents with a powerful economic bias, it’s very difficult to separate wheat from chaff and determine the difference between your life insurance needs and wants. Following is an analysis of the prospective needs of the four primary demographic households:

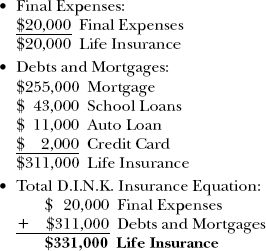

D.I.N.K. (Dual Income/No Kids):

DINK households have “the life”—financially speaking, anyway. They have two incomes coming in and fewer variable expenses. Much beloved by retailers, they can afford all the iPhones, Playstations, flat-screen TVs, and vacations that come their way. Their insurance needs are slim, and the primary objective of life insurance is to pay off the debts and mortgages for the surviving spouse. Their insurance needs break down the following way:

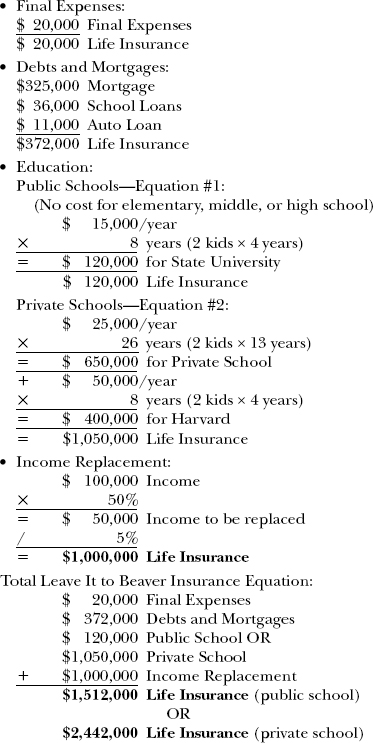

Leave It to Beaver:

This is the single-income, two-parent household with two children. With a growing number of men becoming stay-at-home dads, Ward may be the one with the apron and June may bring home the bacon, but in either case, the insurance logic is the same. To plan for the unexpected death of the primary or sole breadwinner and assume the spouse working in the home is able to continue that course indefinitely, this scenario often results in a large amount of insurance on the income-earning spouse. Here is how we plan for their life insurance needs:

A common and excellent question regarding life insurance planning for the single-income household is, “What about the stay-at-home spouse? Does he or she have a life insurance need?” This traces back to our discussion of what life insurance is and isn’t. It isn’t an attempt to put a value on someone’s life, but instead a hedge against the financial risk of the loss of someone’s life. So, what about the stay-at-home mom who doesn’t earn any income? The amount of work mom does on the home front might not earn her income, but it certainly is worth something! Without Mom, Dad is going to either work less (and earn less money) to spend more time at home trying to make up for Mom’s absence, or he’s going to need to hire a significant amount of help with child care and the myriad other duties on the home front that Mom managed. Although it’s not one-size-fits-all, a $250,000 life insurance policy on the life of the stay-at-home mom or dad should provide the surviving spouse with about $35,000 of additional annual liquidity for seven to 10 years. A larger or younger family may consider up to $500,000 of coverage.

Another great question for a single-income household is, “Do we really need all that life insurance to perpetuate the lifestyle, when in actuality the surviving spouse who was staying at home would go back to work?” The answer here is no. If the surviving spouse intends to go back to work, at least after the children are in school, you may assume a lesser amount of insurance need. This is when it becomes important to recognize the purpose of your insurance planning at the onset. If the objective is to allow the current lifestyle to go on unimpeded, you should err on the higher side of the calculation. If you’d prefer to calculate down to the month and year that a surviving spouse will go back to work, you can specifically tailor your insurance calculation to reflect that as well.

Another great question is, “What about the money we’ve already saved? How is that taken into account?” The liquid assets—unpledged cash, investments, and retirement accounts—may be subtracted from the total amount of insurance needed. In this example, if Mom and Dad have liquid cash and investments of $3 million, they have the ability to assume or self-insure this life insurance need. Similarly, if they have $200,000, they may consider subtracting this number from the insurance need, but their decision to do so should be weighed in light of their general appetite for financial risk.

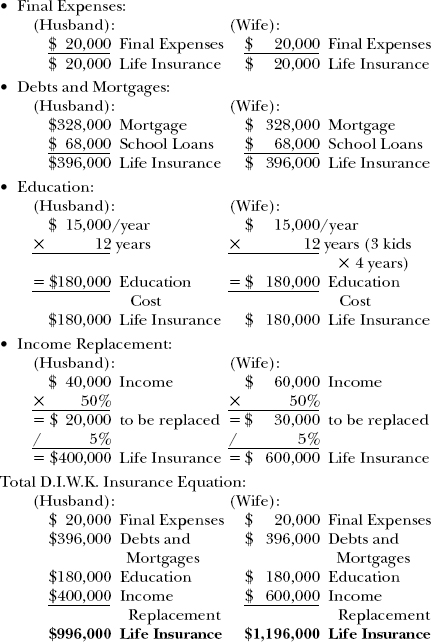

D.I.W.K. (Dual Income/With Kids):

For the many families with sources of income from both parents, the calculation for life insurance is very similar to the single-income household. In this case, you simply have to run the calculation twice assuming that the household is reliant on both sources of income. In this example, let’s assume that the husband earns $60,000 and the wife earns $40,000.

Empty Nest:

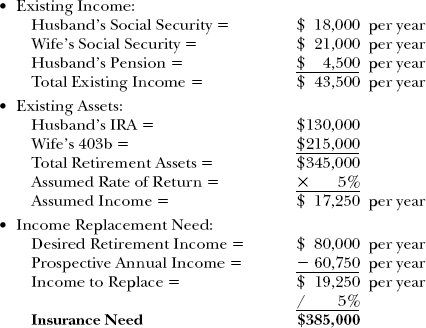

As mentioned earlier, if someone has enough retirement income and assets to sustain his or her lifestyle indefinitely (regardless of whether or not he or she is working), there is no additional need for life insurance. But what about the many individuals and couples in this scenario who have made it past the child-rearing and college years but still aren’t financially independent yet? They need a life insurance bridge to financial independence. The easiest way to calculate this is to determine what their prospective retirement income would be today, then calculate the assets that would need to be added to their holdings to get them to the point of financial independence. Let’s assume in this scenario that the husband and wife both are old enough to be receiving Social Security.

Consideration should also be made for any income that would be lost per spouse if an empty nester leaves behind his or her spouse, and the above calculation should be tweaked to reflect this. One spouse may have a pension stream of income that will die with him or her, or be materially reduced. In this case, it may be necessary to include additional funds in this insurance bridge to replace that lost income. In the above calculation, the husband had a small pension of $4,500 per year. If you divide that number by .05 (5%), you’ll find that $90,000 would be the lump sum expected to recreate that $4,500 annual income stream. Social Security income will also inevitably be impacted by a spouse’s passing. The rule is that the surviving spouse will receive the higher of the two spouses’ Social Security retirement benefits.

Therefore, in the previous calculation, regardless of who passed away, it would be the husband’s lower income benefit of $18,000 that would need to be replaced. Again, divide $18,000 by 5 percent, and you’ll find that $360,000 will be required to replace the surviving spouse’s lost Social Security income. Remember, however, that life for one person will be less costly than for two. Since we’re planning for life insurance needs, lost pension or Social Security income that would not be required after the passing of a spouse need not be replaced with life insurance.

Now that you have a better understanding of how to calculate your insurance needs, let’s explore the most common life insurance wants to help you determine if any of them are appropriate for you:

- Pre-insurance is when you don’t need life insurance today, but you feel you may need it at some point in the future. The rationale with this line of thought is that, “You’re likely to need it at some point in the future, so why not buy it while you’re young and healthy?” This is a want, not a need.

- Building cash value is also a life insurance want. Cash value is a feature of whole life, universal life, and variable life insurance policies. The intricacies of these products will be discussed momentarily, but cash value is one of the bells and whistles that come with life insurance policies. As in every case, those bells and whistles come with a price tag. An agent intent on making a nice life insurance sale may say, “Term is like renting. Whole life is owning your life insurance.” That’s a sales pitch if I’ve ever heard one! Owning a house is typically one-and-one-half to two times the price of renting a comparable residence; whole life insurance can cost more than 20 times the price of comparable term! There are wise uses for permanent life insurance with cash value. For business owners and folks blessed with the problem of having an estate large enough to be diminished by federal estate tax when they pass on, term insurance will likely not be sufficient to handle their desires. But those are still wants, not needs.

Economic Bias Alert!

Economic Bias Alert!Because the premiums are so much higher for cash value life insurance policies, and the commissions for life insurance agents are based on the premiums (not the death benefit amount), agents are actually incentivized to make poor recommendations to clients. I was conducting a comprehensive analysis for two different married couples with very young children. In both cases, the husband was almost solely responsible for the household income. I was astonished that in both cases, these couples were sold policies that would pay only $250,000 if the husband passed away, although it was quite clear that in order to cover the mortgage, education for the kids, and income replacement, he needed at least $1,000,000 of life insurance. The $250,000 policies were cash value insurance policies with premiums up to the maximum that either of these young families could afford. They actually saved money by purchasing the $1,000,000 term policies they needed and dumping the cash value policies that their agents wanted. You would think the insurance agents making the recommendations to clients would have a legal obligation to act in the clients’ best interest, but they don’t. Insurance is regulated by each state, and in most states, the legal burden placed on a life insurance agent is caveat emptor—buyer beware. As long as the policy is approved in that state, the burden is on the consumer to make the right choice.

- Estate creation is the life insurance want for the individual with a strong desire to leave a financial legacy behind but doesn’t yet have the estate in place. Picture the single mom or dad with adult children. The adult children don’t rely on the parent financially and are living an independent life, but the parent daydreams about leaving behind a financial lump sum. This, by its very definition, is not a need but a want.

- Charitable bequests and the accompanying charitable inclination are honorable and virtuous, but to make a charity or charities the beneficiary of a life insurance policy is certainly a life insurance want.

- Wealth replacement is the final life insurance want we’ll discuss, and it will be discussed in greater detail in our estate planning chapter. Many families have been blessed financially to the point that they have estates large enough the federal government sees fit to tax their money a third time. They do this through a federal estate tax, or, as it’s known by its detractors, the Death Tax. As it stands, in 2011 and 2012, federal estate tax is levied on individual estates in excess of $5 million. In the case of a married couple, proper planning will provide a $10 million exemption. Everything in excess of five or 10 million, respectively, will be taxed at a rate up to 35 percent. What makes planning for wealth replacement so difficult right now, however, is that in 2013, the law sunsets to the 2001 law, in which the individual limit is $1 million and estates larger than that exemption level may be taxed at a rate up to 55 percent. In that instance, picture the farmer with an estate valued at $5 million—most of it in land—and his heirs may have to sell the farm in order to pay the federal estate tax of two million big ones! To add insult to injury, many of our united states also charge a state estate tax and/or inheritance tax on top of the federal tax. Having a well-conceived life insurance strategy for estate taxes does not decrease the amount of tax due, but replaces the wealth lost by one’s heirs. Now you see why and how someone might wisely use this life insurance strategy, but in the nebulous tax environment of 2011 and 2012 it is a challenge to know what tax law to expect.

Ultimate Advice

We’re not told in The Ultimate Gift whether or not the billionaire, Red Stevens, owned any life insurance. He surely didn’t need any, but he may have wanted some to keep certain business or philanthropic initiatives alive. I doubt he employed the wealth replacement concept because he didn’t seem to think his heirs would spend their inheritance wisely, and that should certainly be a consideration of yours as well. The best insurance and estate planning carefully considers how to protect assets for heirs, but also from them.

Different Types of Life Insurance

Life insurance can be split into two basic categories: term life insurance and permanent life insurance—term and perm. As is evidenced in their names, term life insurance is intended to exist for a stated term or time frame and permanent life insurance has features allowing it to continue into perpetuity. One of the sales ploys I’ve heard used to sell permanent insurance products when term is more appropriate is, “Only two percent of term life insurance policies pay out!” That statistic is true, and for that I say thank God! Much like we never hope to receive the benefit of our auto, home, liability, and disability insurance coverage, I very much hope that your term life insurance policies never pay out! Good risk managers are willing to temporarily transfer risk that they cannot bear until which time they have enough assets to self-insure.

Term life insurance is pure insurance. It is a calculation on the part of the brilliant number crunchers called actuaries to determine the probability of your passing away in an established period of time. There is no cash value to the policy. It only pays out when you die in the vast majority of cases. (There is a relatively new term product now available called Return of Premium. It solves only an emotional need, not an economic one. You are likely better off buying standard term for less and putting the difference into your Roth IRA.) The most common term is a 20-year period. Twenty-year term guarantees that as long as you make the level premium payments for the next 20 years, the insurance company will pay out to the beneficiaries if you (ahem) croak. For the family that can reasonably assume they would reach financial independence in the next 20 years, this is a very appropriate product. Term is also sold in many variations with lengths as short as one year, but also in nearly every increment of five up through 30-year term. Virtually all of the life insurance needs can be adequately insured with term.

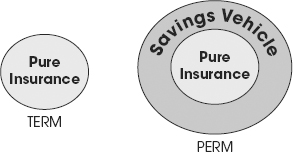

Permanent life insurance can be viewed as having a core of the pure insurance with an additional layer around the core of a cash savings vehicle. (See Figure 6.1.) This additional savings receives certain tax privileges and allows policy owners to take loans against or distributions from that cash value. The investment components also come in various forms. Whole life, the most costly of the varieties of permanent insurance, has a fixed-income savings mechanism inside. It should function similarly to a conservative fixed-income investment, like a CD. Variable life has investment components that are more like mutual funds. They have a range of investment options, known as subaccounts, which are various types of mutual fund–style stock, bond, and cash investment vehicles. Another form of permanent insurance is universal life. Universal life was designed to offer a less costly form of permanent life insurance. It is a hybrid between whole life and term life insurance. Several of the life insurance wants require the purchase of some form of permanent life insurance, but remember, if you earn less than $250,000 per year and/or have an estate in the millions, there is little chance that one of these products is appropriate for you.

Figure 6.1 Types of Life Insurance

Although the benefits of permanent life insurance exist, the costs must also be weighed. I recently replaced one of my term life insurance policies with a new policy bearing a $1 million death benefit and an annual premium of $465 per year, so in preparation for this chapter I reached out to several life insurance agents to see what the cost would have been for permanent life insurance policies with the same death benefit. The answers? A comparable whole life policy was 20 times more costly—$10,380 per year! The universal or variable life policies would cost around 10 times the amount that I am paying for my term policy. I’d rather control the fate of that extra money than trust a life insurance company to manage it.

Another factor that must be weighed when considering the appropriateness of a permanent insurance policy is the surrender charge. The investment portion of the premiums paid in most permanent policies is not fully available to you for years—often nine but even up to 20 years. The insurance company takes the bulk of its profit out of your policy in the formative years much as a bank takes more interest at the front end of a loan amortization. Your policy will have a contract value and a surrender value; the latter is the amount you’d actually receive if you cancelled your policy. The difference between the contract value and the surrender value is called the surrender charge—the penalty assessed by the insurance company if you cancel a policy in the early years.

Ultimate Advice

When you’re paying someone else to cover your risk, it is more expensive than doing it yourself.

When you go out to eat dinner, the owner of the restaurant buys the food for far less than you or I can buy the same food. They prepare and serve it to you and then charge you far more than you would pay to cook the same meal at your home. This certainly does not mean we all shouldn’t enjoy a nice dinner out. We should simply remember that we are paying for the privilege. In the same way, if an insurance company covers your risk, you are paying a premium—literally and figuratively—for that safety net.

Conversely, if you are using insurance as an investment vehicle, you have invited a very expensive middleman into your world. Rarely, if ever, will you find a case where the investment portion of an insurance policy performs better than buying term insurance and investing the rest on your own. It’s just like cooking a meal in your own kitchen. It will always save you money. While there are other benefits to eating out versus eating at home, when you’re considering insurance to cover your risk or investments versus covering them yourself, there are no benefits to consider other than the dollars.

Jim Stovall

One additional type of insurance that we must mention is group life insurance. Group coverage is provided by your employer. In many instances, your company may provide a life insurance benefit based on a multiple of your salary or compensation. For example, your company might give you a death benefit of your salary multiplied by one or two ($60,000 salary × 2 = $120,000 benefit). These policies often offer additional coverage to be purchased by the employee that will increase in multiples of your salary. Advantages of this type of insurance are that it may be free and it requires little to no underwriting, the process undertaken by the insurance company to determine if you represent a risk they are willing to take. By all means, take the free insurance, but carefully weigh the benefits of purchasing additional coverage through your employer for the following two reasons:

1. Unless subsidized by your employer (and these subsidies have become rarer in recent years), the cost for group life insurance is typically higher than insurance you could purchase privately, especially if you are in reasonably good health and would garner a favorable report from a life insurance underwriter. The coverage is more expensive because it often is available with no underwriting. They assume something close to a standard (average) underwriting level because they recognize that in that group there are likely to be many who would meet higher underwriting guidelines and others who will meet lower guidelines. The insurance company reduces their risk by giving everyone standard pricing. This could result in a cost that is 50 to 100 percent higher for someone who would otherwise qualify for “preferred” or “preferred best” underwriting. However, for an employee with a health condition precluding him or her from being approved for a privately written life insurance policy, group life insurance presents a great opportunity to get coverage he or she otherwise couldn’t get.

2. Most group life insurance is not portable—you cannot keep it after you leave the company through which you received the coverage—and, therefore, is significantly diminished in value. Most of us will change companies seven to 10 times in our careers, by choice or not, and if you are too reliant on your group life insurance to be there for you indefinitely, you may be in for a rude awakening if you change companies and find the new company does not offer the same level of group life insurance.

There are several ways to purchase life insurance. Numerous online calculators are available, and while this is a good place to start your research, I don’t suggest completing your process with an 800 number. Your rates will likely not be any lower if you apply online than if you go through a life insurance agent or broker. A life insurance agent represents a company to the consuming public while a life insurance broker represents you to a plethora of different insurance companies. When searching for term life insurance to cover your needs, an insurance broker is typically going to be the best bet; however, if you are shopping permanent insurance, you will need to include some insurance agents in your search. Some of the best insurance companies in the U.S. are captive agencies, which means they do not make their products available to brokers. Only their company’s agents can sell their products.

While there are many reputable, respectful, knowledgeable, helpful insurance specialists out there, most of whom, by the way, are very good dressers, there are also many who have helped solidify the stereotype. But please don’t allow that stereotype—or even a bad experience—lead you to the mistaken assumption that you can write off the strategy of managing the financial risk of a death in the household. Instead of going directly to an insurance salesperson to buy life insurance, talk to a fee-only financial planner who has given up the ability to take commissions. Allow him or her to give you an unbiased, third-party recommendation on how much life insurance you should have and then go to an insurance salesperson with your “prescription” and place your order. Many fee-only planners will even help manage this process.

Timely Application #2

Life Insurance Needs Analysis

Using the demographic templates in this chapter and the calculator for Insurance Needs Analysis on our web site, determine what your needs are for final expenses, debts and mortgages, education, and income replacement. Contrast what you found in your Life Insurance Audit and your Life Insurance Needs Analysis in order to get an idea for your next steps.

If you conclude that you have policies you don’t need or want, and you’ve confirmed your research with an independent planner who does not accept commissions on the sale of life insurance, then you have several options for terminating your policies. But don’t make those decisions hastily. Even if you shouldn’t have purchased the whole life insurance policy you bought 15 years ago and don’t need or want it now, in some instances it will make sense to keep it. Requesting an “In-force Life Insurance Illustration” and a “Policy Cost Basis Report” from your agent (or the insurance company’s home office) will help you and your independent planner determine whether the policy should be kept or surrendered based on the investment value, future prospects for growth, stability of the insurer, and tax consequences of liquidating.

Especially in these economic times, it is important to ensure that every dollar of yours is working hard for you, and that includes the dollars channeled toward life insurance.

Visit www.ultimatefinancialplan.com to find a template to use for your Life Insurance Needs Analysis.

Tim Maurer

Now that you have an idea how much life insurance you need, you can expect to have insurance companies falling over themselves to get you to take one of their policies, right? Yes and no. Sure, they want to sell you a policy, but they really don’t want to lose money on you either, so once you’ve decided what kind and how much insurance you need or want, the prospective insurance company will turn you over to the underwriters. When I was going through life insurance training, underwriters were referred to jokingly as the company’s “Business Prevention Unit.” You will fill out an application asking you a string of personal and financial questions deep and wide enough to make anyone blush. They will ask about a number of your personal habits and even delve into the health and welfare of your parents, grandparents, and siblings. Beyond the application itself, you’ll also have to have a nurse visit you to take blood and urine samples and ask you a bunch of the health questions again to ensure that you don’t tell a different story than you did in the application. (Sounds like fun, eh?) It is vitally important to remember these two underwriting tips when applying for life insurance:

1. Tell the truth. Beyond being a generally good character trait, honesty will allow you to keep your story straight. If an insurance company catches you in a lie, they can decline you completely, leaving a mark on your record for future business with other insurance companies. And while it is difficult for them to catch a host of little white lies, if they catch one in the unfortunate instance that you die shortly after the policy was initiated, any fraud on your part, if exposed, could mean that your family is left with nothing.

2. Don’t answer questions that aren’t asked! I want you to be honest, but I also want your answers to be as concise as possible. If they ask if you are a mountain climber, and you’re not but you enjoy doing hiking and bouldering with your kids on weekends, the concise answer to their questions is no. If they ask if you have plans to visit a host of nations that they deem politically or medically unstable and you don’t have airline tickets and accommodations for an upcoming visit, don’t go into a diatribe about how you’ve yearned to go on a hunting expedition to Africa to hunt wild boar!

Ultimate Advice

All the money in the world won’t buy you one more day of life.

Red Stevens in The Ultimate Gift

Isn’t it amazing how complicated a simple financial product intended to care for one’s family in the case of an untimely passing can be? At this point, if you are not thoroughly frustrated and confused, you should consider a career as an economist or insurance actuary. We are all baffled by the abundance of information thrust upon us regarding life insurance. Unfortunately, we are using technical, mathematical, and legal jargon to try to make decisions about the most emotional eventualities that a family can face.

Our natural reaction may be to throw our hands up in frustration and do nothing, or turn the matter over to an insurance salesperson and hope for the best. Either choice would be wrong. You must get the help you need to get the information you require to provide the protection that your family deserves. Insurance presents some of the hardest decisions you will ever have to make, and unfortunately, you’ve got to get it right the first time. There are no spell checks, mulligans, or do-overs when dealing with life insurance after the fact. By the time your family figures out they don’t have adequate insurance, it is too late to do anything about it.

In the next chapter, we’ll continue to simplify insurance decisions involving products with even more moving pieces than life insurance.

| Emergency Savings | $12,000/year ($1,000 per month) |

| 401ks for Husband and Wife | $33,000/year ($16,500 annual limit per person) |

| Roth IRAs for Husband and Wife | $10,000/year ($5,000 annual limit per person) |

| Education Savings | $4,800/year ($200 per child per month, two children) |

| + Liquid Investment Savings | $12,000/year ($1,000 per month) |

| Optimal Household Savings | $71,800/year ($5,983 per month) |