"Four basic premises of writing: clarity, brevity, simplicity, and humanity." | ||

| --William Zinsser (American author and editor) | ||

In this chapter, we're going to dig into a subject almost every startup gets wrong the first time around. Some recover, many don't. The subject is how well you present your startup's software to first-time visitors to your site. The goal is to make that case in the right order, with the right parts, so that those prospective customers become actual customers.

Describing clearly why someone should give you money for your software is a skill that doesn't come naturally to most developers and startups. It makes us somewhat uncomfortable to do so, probably because we're too close to see the benefits of what we've created, apart from the flaws. But if you're going to succeed, you need to be able to step back, look with the eyes of your prospective customers at what you're going to be selling, and then know how to present your case.

Before we get to two case studies illustrating how to make a case for your software, let's examine a couple of assumptions and a design pattern I and others call the Unique Selling Proposition.

First off, I'm assuming you've got no desire to inflate, overplay, or exaggerate what your software does and no interest in bamboozling, conniving, or manipulating though yard-long web pages of screaming headlines, coercive text, pop-ups demanding your visitors' e-mail address, gushing testimonials, multiple bonuses, and hidden prices. In other words, you're not interested in the Internet Marketing approach to marketing your software: Make! Money! Now! (see Figure 7-1). If you are, then return this book. You probably wanted MindControlMarketing.com[87] (Steel Icarus, 2003) by Mark Joyner or some lesser practitioner of the Dark Arts. Internet Marketing is the evil mutant digital offspring of the first kind of spam—direct mail advertising. And though I'd like to tell you that approach doesn't work, someone is nonetheless making money from it and those late-night television ads.

You see, I'm assuming you have an application with some real benefits to the right people and that those people would probably be extremely interested in your web or desktop app if they were properly introduced. The point of this chapter is to help you understand and structure honestly the prospective customer's initial experience with your software—your home page—and communicate clearly your value to them.

With that out of the way, let's take a quick look at something I've written about elsewhere[88] at much greater length: the Unique Selling Proposition pattern.

Let me put what I'm talking about here into programmer-speak. The Unique Selling Proposition (USP) is a robust and powerful marketing design pattern that can effectively save you from designing spaghetti-like marketing that's hard to understand, let alone maintain. It's a pattern for connecting what you are selling to the right people in the right way so that they are eager to purchase.

What's more, it's an extremely efficient, effective, and elegant pattern that can be used and reused in a wide variety of circumstances. It's a pattern that has been employed successfully on literally thousands of projects worldwide. Marketing is just another programming language. And the USP pattern is one of its most useful and flexible design patterns.

Another way to describe the USP is that it's the set of expectations most people have about what is—and is not—good software from a trustworthy vendor worth their attention.

All right, enough chatter. Let's walk through the components of a USP, the timeline of how a typical prospective customer sees—or doesn't see—these components, and what the USP means for your startup web site's home page.

When people go to a web site for the first time, there's logically going to be one thing they perceive and comprehend first. They are going to glance at the site and make—literally—a split-second decision to stay or go based on the first thing they see. Your job as a founder of a startup that wants to succeed is to control as much as possible the first thing prospective customers see on your web site and to make sure that what they see or read connects with them so that they keep reading. It's a big Internet out there, and that new arrival to your wonderful web site cares not one bit about it, about you, or about your startup—yet.

The job of the hook is to give potential customers a reason to care (a little), to read on (a little), and to think that there might be some value at your site that's worth a few seconds more of their valuable time.

Now, before you mentally complain that your startup is different, that your app is so interesting that, of course, prospective customers are going to analyze your 23 bullet points and decipher your 193 industry-specific terms, ask yourself what you did the last time you went looking for something on the Web. You probably did a Google search, opened a bunch of pages, quickly scanned through the lot, with your fingers poised to press Ctrl-W, and without a second's hesitation chopped any page that didn't look right, didn't tell you that you were on the right page for what you wanted, didn't make unequivocally clear what it was offering. Why would your prospective customers act any differently?

Let's take a closer look at what your prospective customers are looking for in the first couple of seconds.

They want to know that they haven't navigated to some weird, spammy, amateur, possibly dangerous site.

They want to know that the site is relevant, that it relates to what they want.

They want to know what you intend to offer them.

Here, then, are the three key elements of the hook: credibility, relevant value, and a clear offer. These are also the main components of a compelling Unique Selling Proposition.

The hook needs to be the first words to which the prospective customer's eye is drawn. That's usually accomplished by making its text three times larger than any other headline on the page, with plenty of white space around it to set it off. But the right text size isn't enough. Let's look at each of these elements in turn.

Whatever you say in that one- or two-sentence hook should be honest, not hyperbole, believable, not bull. Claims such as "Best," "Revolutionary," "Industry Leader," "Unique," and "Easy to Use" immediately trigger most people's MFR—marketing filter response.[89] Now, maybe your web app is revolutionary, unique, easy to use, and more. Fine. But first you have to establish some trust between you and would-be buyers, and then you must introduce and back up your claims. Remember, they've just opened a bunch of web sites via Google, and they're itching for a reason to close your page. Don't give them one.

Instead, here are three good ways to establish your credibility via your hook.

Show that you speak their language, that you understand the need that brought them to your page, their mindset, their vocabulary for describing things in this part of their world.

Don't use terms at the beginning of the sales conversation that blow your credibility.

Don't try the patience of your prospective customer. Get to the point.

I know, I know, you want to mention in your hook all your software's really cool features, because, well, they're cool. Don't! Your prospective customers need to grasp easily why you matter to them, what in the news business is called the "So what?" test.

Let's move on to the second component of the hook and, for that matter, of you're entire site: relevant value. Value depends on relevance. Relevance can be as simple as "I'm a happy Windows user. What do I care about Mac apps?" [90] It's all about what's at the top of the pain/I Want list of your customers-to-be when they arrive at your web site.

Some of my clients initially want to try to be as relevant as possible to anyone and everyone having any need, however tangential, for what they're selling. Doesn't work—and it costs credibility points. Let's put it this way: What's the one thing about your web or desktop app that matters most to the one or two kinds of people who constitute your collection of market segments? That's the relevant value you want to put upfront and center in your hook.

Are you trying to sell a web app, a Windows or Mac app, an Apple iPhone or Google Android or Windows Smartphone app? Do you want people to buy it, subscribe to it, get consulting on it, or consume it for free? Given the number of ways software is being delivered today, people visiting this site need to know what platform your startup's software is for and how you intend to charge them for it.

So you should tell them they can choose a free 30-day trial or a free account, right? Nope. Those are things in your marketing toolbox, just as glossy brochures and info packets were during the last century. Worse, including the F-word (free) in the hook, only to have potential customers find out that you're talking about a limited account or a trial version, is like sticking a hard drive in a microwave: the results are not pretty.

When you walk into a store, you know you're going to grab things off the shelves, walk to the front of the store, and pay for them. If you go to Amazon, you're going to click a button to put the item into your Amazon cart or, if you're logged in, you're going to click one of the three orange Buy Now buttons to do your business. Your customers need the same kind of guidance from you when they are comprehending your hook; they need to know you are selling them something and what form that something is going to take.

OK, enough about the hook. Let's look at the other parts of the Unique Selling Proposition pattern, starting with an expanded view of this whole "Should I trust you?" thing: credibility markers. There are two aspects to this part of the USP: (1) what you say and how you say it and (2) whether you've competently included the standard things most online buyers look for in order to pass judgment on a site. Let's deal with the latter first. Here's the short list.

Do you identify your company by providing its logo, physical/mailing address, phone number, and general e-mail? If not, why would you expect people to give an anonymous page their credit card info? Now, I realize that startups in some parts of the world—eastern Europe and Russia come to mind—think their customers in the United States will penalize them. Some will, although not as many as you think and not if you do the right things.[91] But the cost of not having this information on your site is far higher.

Did you include a copyright notice and, if you mention other companies' products on the page, a trademark disclaimer? You're running a business; these are the signposts of a business.

Is the price of what you are selling shown either on the home page or where you expect people to sign up?

Is it clear and unmistakable what people have to do to buy your app or service and, for that matter, to try it?

When a person goes to buy your app or web service, do you make clear what your refund policy is and, if you are using a third-party payment processor (see Chapter 5), who that processor is?

Does the site look professional and businesslike, whatever that means in your particular online industry?

Do you have testimonials praising your product or web app from other people who visitors may already trust or with whom they can at least associate themselves? Is at least one of those testimonials on the home page?

The people looking at your web site expect and understand that they are involved in a specific social situation called a sale. This sale situation has its own etiquette, its own rhythm, its own do's and don'ts—ignore them at your financial peril.

Testimonials and (positive) reviews are a big part of establishing the overall credibility of your offering. The comfort factor goes way up when prospective customers see the name of a media organization or a prominent blog or logo on your home page. We covered this in some depth in Chapter 6, but in this context the thing to know is that no matter how many steps it takes, you want those media/blogger reviews—they really matter.

The word famous has a television definition like everything else, but don't forget that famous could mean the head of surgery at a major hospital if you are selling surgery-related software or, for that matter, the head tree surgeon at a well-known landscaping company if you're selling software to landscaping companies.

It's all about relevance—and since many of your customers may not take what "authorities" say seriously, positive quotes from real people who use your software and are willing to say, they use and like your software can be just as important. Notice that I didn't say "purchased your software" in that last sentence. The catch-22 of not getting sales because you have zero testimonials and having zero testimonials because you have no sales is best fixed when you do either your initial or your major release public beta.

Of course, if you establish your credibility but don't communicate your relevant value, your job's at best half done.

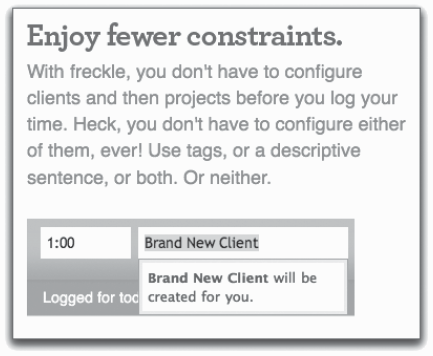

Once a visitor is past the hook, relevant value is all about bullet points. No, I'm not talking about bullet points that escaped a corporate PowerPoint presentation. I'm talking about a modern startup benefit and customer-centric bullet points.

Let's look at a good example from the startup freckle time tracking. First off, a good modern bullet point isn't just text, it's a headline to preview the message and give it a mental peg to hang on to. And it's small visual image to associate with the feature. And it's ultra-easy to read and comprehend block of text that is about you the prospective customer, not me the amazing startup (see Figure 7-2).

The word you appears four times in this one bullet point. Amy Hoy, Thomas Fuchs, and the two other founders use the word you or the like 31 times on freckle's home page.[92] It's all about the customer, not about your product and certainly not about your startup.

Something else you should notice about this benefit bullet point: it's simple—no jargon, no long sentences. The goal is customer comprehension, not data packing.

You'll have to visit freckle time tracking (http://letsfreckle.com) to realize how each of its four bullet points—that's right, only four—backs up and buttresses the site's hook ("freckle time tracking helps you do more of what you love, and less of what you don't."). If you haven't nailed the customer after that many shots, something is wrong with your ammunition.

Before we get to the Case Studies there's the last component of the process: asking for the sale. You are selling, they're (maybe) buying, and it's your job to ask nicely for their money.

Should you do this by having an unmissable Buy Now button, or should you go for the sale via the indirect route of the free 30-day trial? Do both, because you're dealing with the entire bell curve here, from the earliest adopters who will buy anything they consider shiny to the middle-of-the-road folks who've been burned and want to taste your wine before they buy a case.[93]

And what if your startup doesn't actually sell something, like our first case study, Mint.com? You don't actually have to have to sell, do you? Yes, you do. If you don't ask for the sale, whatever that means for your startup, then you leave visitors hanging, wondering what they are supposed to do next. So even if you've found a cool way to get someone other than your customers to pay for your startup, get comfortable asking them to take the next step leading where you want them to go; it's the only way they'll get there.

URL: http://mint.com

Area: Personal financial management.

Platform(s): Web, Apple iPhone, and SMS text.

Summary: At the time of this writing (mid-January 2009), Mint.com had gone from zero users to over 800,000, with a whopping 23,000 people signing up the day before my interview with 28-year-old CEO Aaron Patzer. The free consumer personal financial manager makes its revenue when its patent-pending search algorithm finds a way to save money for a customer and that customer chooses to accept that offer. Since starting in November 2006, Mint.com has raised a total of $17.45 million in three rounds of equity funding.[94] Those are impressive numbers.

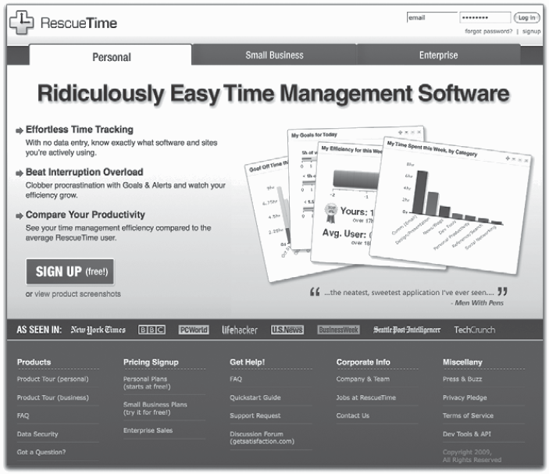

For purposes of this chapter, let's have a look at the home page of Mint.com (see Figure 7-3).

Any chance you'll miss the hook of Mint.com? Nope. And while it's a pretty big claim, notice how it's buttressed by great major media quotes right under it? That deactivates most people's marketing filter response.

The PC Editor's Choice award certainly helps, as does the customer testimonial that leads to an entire page of both test and video customer testimonials.[95]

The VeriSign, TRUSTe, and McAfee badges at the bottom help further establish the credibility of Mint.com.

Aaron would agree with you that establishing Mint.com's credibility was the hardest hurdle to jump (see the upcoming interview). If you click down to their Privacy and Security page, you won't get privacy boilerplate. Instead, you get a video of Aaron talking about security and, page after page, covering exactly why you can trust Mint.com with your financial data and bank passwords.

Bank passwords? Danger! Danger! We've all been trained by authorities and spammers never, ever, ever to give out that information. Yet people are doing just that—in droves. Partly because Mint.com spells out exactly what happens to that information, how it is a read-only app (you can't move money around), how while your financial data is in the cloud, your identity is never asked for.

Here's what Aaron had to say about the trust issue, what it took to get his initial funding, and why he decided to build Mint.com.

Bob: Let's start with how you decided that Mint.com was something you wanted to do.

Aaron: Yes, I had started a couple of businesses back in high school, building web sites and doing online marketing. When the Internet was quite new, I guess, it was back in sort of the 1996–97 era. And that's how I put myself through college, went to Duke and then to Princeton.

So I was combining doing my personal and business finances and I was using Quicken and Microsoft Money to sort of separate out my personal and my business finances. I was really religious about getting in there and entering all my transactions and balancing all my accounts, categorizing everything.

I did that probably every Sunday afternoon, for an hour every Sunday, every week for about eight years. Then I got really busy with another job. I was working as a software architect for another startup, and I didn't log into Quicken for, like, five months. When I got in there it downloaded about 500 transactions from my banks that said, hey, your bank balance just doesn't match your Quicken balance. Will you please reconcile these 500 transactions.

I thought, man, that's going to take me all weekend to get back to square one. And it just dawned on me that I been putting all this work and all this effort into a system that really wasn't giving me anything back in return. Why did I have to balance my checkbook anyway? The electronic version of my checkbook can't just figure it out for me?

I was incredibly frustrated and I realized it was a huge waste of time and I didn't want to do it anymore, and it turned out I wasn't alone in my frustration. Turned out there were a lot of people who really didn't like Quicken and Microsoft Money anymore, half of the people didn't even get through the installation process, because it was so cumbersome to set up.

So the core idea started out in my frustration, and the core idea was to make personal finance effortless and simple. You know, get in and out in five minutes a week or less and get set up in five to ten minutes to get all of your accounts in there.

Bob: OK, well, I've used Quicken and I actually used Microsoft Money and I don't do it on Sundays; I do it on Fridays. But I know exactly the frustration you're talking about. How does Mint.com solve the problem?

Aaron: Yes, it's a free online application and links to 7,500 banks, credit cards, loans, and brokerages. So instead of the setup process you go through with, say, Microsoft Money, where you buy the software in the store, you install it on your computer that takes 20 minutes, and you go through 30 different setup screens, search for your bank, enter your credentials, what you want to rename and call these bank accounts, how you want to rename transactions.

Mint.com basically makes intelligent decisions for you. All you have to do is search for your bank and enter your username and password; after that point it will update your balances, your transactions, your bill-due dates. It will pull it in every single night, whether you logged in or not, sends you bill reminders, low-balance alerts, credit alerts. Things that the desktop program can't do because a desktop program is only running when that application is open. So it's always up to date and it's always watching your back, 24/7, making sure you don't have any late fees, making sure the bank doesn't charge you any fee, and it categorizes everything for you.

So I spent about three or four months alone in a room working on a patent pending categorization program so that it knows that when you go to Rose's Café, that's a coffee shop, or that the "Superior Court" entry, despite its name, is actually a racquetball court and not a traffic ticket or something. So there is a tremendous amount of technology behind it. We get five patents in what were doing.

Bob: Whoa! Let me ask you about something, from sort of the marketing point of view here. Financial tracking desktop software has been around for, well, at least 15 years that I know of.

Aaron: Yup.

Bob: But nobody seemed to have the right mix of message and features to convince people to put their financial information on a web site, somewhere that we don't even know where they exist. How do you deal with this issue of credibility?

Aaron: Yeah. I mean, every venture capitalist I talked to in the early days said that Mint.com would definitely fail because people would never trust a startup with their financial information, and certainly they were never going to enter their bank username and password. But we need your bank username and bank password if were going to sort of essentially get your information out.

The banks need to know it's you that's authorized it. So there are a number of things we did with our messaging. Every reporter asks about security, so we spent a lot of time talking about what to do with security from an engineering standpoint and then how to brand that.

Mint.com has bank-level security. We have all the same encryption and backend protections that a bank would. We have outside security auditing, by hacker-safe outfits, and we verify signing outside, late-night hackers, they're called, who try to break into the system, who haven't so far.

We are a read-only system, so you can't actually move money around. So even if somebody breaks in, that person can't drain your accounts. And we're anonymous, so we made a conscious decision not to request name, age, address, phone number, social security number, anything like that; we only ask for e-mail and a zip code.

So even if somebody broke in, got into our database, he wouldn't know who you are; he just knows happygirl17@yahoo drinks a lot of Starbucks coffee or something.

Bob: So like cutting off the head of the information, who you are actually are . . .

Aaron: Exactly, but no personal identifying information. And then the other thing is Mint.com helps actually protect you. So we've turned the security issue 180° into a strength because Mint.com is going out and monitoring your four or five different credit cards that you have in your wallet, every single night.

And so 90% of all fraud occurs offline, not online. You're much more likely to get your credit card stolen at a restaurant or a gas station or if somebody is actually physically handling your card. The alternative is you can log into four or five different web sites every day and check for fraud, or you link them into Mint.com and Mint.com will just tell you if there's suspicious activity on your card.

Bob: Hence the alerts about these 25-cent charges that started popping up on various people's accounts.

Aaron: Yes, and on our database; and we let those users know that their accounts may have been compromised, certainly not at Mint.com, but somewhere else. Well, I guess they lost 25 cents in it, but they should probably have those credit cards reissued by their provider.

Bob: OK, let's talk more about money. Specifically you're saying that when you talked to VCs, they were of the attitude that this is never going to fly because nobody is going to give you any personal financial information.

Aaron: Yes.

Bob: When you got your first round of capital, which according to CrunchBase was $325,000, how did you sell that?

Aaron: I found one guy who believed in the vision or was willing to take a bet on me and the team that I put together. Here's the catch of venture funding. It was in spring of 2006. I went to see Sequoia. And I came in and gave them a pitch, and they said, good idea, but no one will trust it and, by the way, you have no team and no product, so there's no way we can ever give you money. The catch-22 is they only want to invest in something they know will work or is starting to work.

Bob: Right.

Aaron: But you need money in order to get it to that point. We won't invest in the company unless they've built a product, but you need money to build the product. I built Mint.com off my own savings and sat alone in a room for seven months and worked 14 hours a day, seven days a week, until I basically got a prototype of the system—front end, graphics, functionality, everything.

Then I was able to do a demo in front an investor, Josh Kopelman (First Round Capital), who's the founder of half.com. He said, yes, I think this might work, but, to help with the trust aspect, don't use the domain mymint.com, which is from before; mint.com is much more valuable. We spent three months negotiating for mint.com because that's a much better name and a more trustworthy name.

Bob: Was Josh the person you were referring to that was your first VC believer?

Aaron: Yes, he was.

Bob: And just to clarify here, what then was the $325,000 that CrunchBase is referring to? Is that the money and time you put into it?

Aaron: That's how much that First Round Capital themselves put in.

Bob: OK.

Aaron: The $750,000 was $325,000 from First Round Capital and $425,000 from other investors.

Bob: Hence don't always believe what you read on the Web. Let me ask you: How about when you went to talk to the banks and the credit cards and Visa International and you're saying, hey, look, we want to put all this information online, how about it? How did you convince what is basically a whole bunch of conservative people that this was in their interest?

Aaron: Yes, there's a way around that, in that someone else had already solved that problem. In the late 1990s Microsoft and Intuit developed the OFX standard, which was the Open Financial Exchange. That lets you sync up with bank servers and, if you have credentials, download transactions and balances and things like that.

Some banks use that. And the banks that didn't support that, we partnered with a company called Yodlee [http://www.yodlee.com], and they do what's known as screen scrapping, which is essentially logging in as the user; they pull down the web pages and pull out the columns of data representing your transactions and your balances.

They already had those relationships set up, and they were already partnered with Bank of America and some of the large institutions.

Bob: So, bottom line, it wasn't a problem. It was basically outsourced to Yodlee for those people who don't use the sort of standard industry format.

Aaron: That's right.

Bob: There's not that many people in their mid-20s who already have 800,000 users. To what do you attribute your success?

Aaron: Well, first and foremost, solving a real need and a real pain point that people have. I mean, every adult in the Free World needs to manage his money, and existing tools just made it way too difficult. Then bank web sites, well, they only show you your balance for a particular credit card or a particular account.

The average American has 11 different accounts where they need some way to track all of it. All their loans, all their investments, their 401Ks, their IRAs, their credit cards, their checking and savings accounts. We just made it really easy to do that, really easy navigation. We hired a designer, a user action designer, who built apple.com, so we took our inspiration from Apple and then we focused a lot on the product and the usability and the user interface.

We brought actual people in to help with software, like right off the street. A woman brought her kid with a stroller in and tested mint.com out while the kid was screaming. We brought people who were in their 40s and 50s and people who were in their 20s, men and women. Got a diverse set of people in and saw where they were using the software well and the places where things weren't going well. Just took a really user-centric approach.

Once we launched, I will basically do any and every interview from any blogger or any press.

Bob: [laughs] OK, that helps.

Aaron: Yes.

Bob: One more question on that. Did going multiplatform . . . In other words, you start as a web app and now you've added an iPhone interface. How much did that help?

Aaron: Well, it's been four weeks, but it's helped tremendously. We are the number 1 finance application in the finance category in the apps store, which means we've beaten Bank of America, Wells Fargo, PayPal, the AT&T mobile banking system. At one point we were ranked as high as number 30 on the top 100 free applications overall, and we're the only finance app ever to have done that. We were almost as high as Pandora and Facebook at one point.

Bob: Was this part of your strategy way back when, that you wanted to diversify across platforms, or was it, Hey, wow, this iPhone is incredibly cool. Lots of people are buying them. Let's go for it.

Aaron: Well, we didn't launch right when the iPhone launched. What we did was we did some user research and found out that 40% of our users had iPhones. And of the 60% who didn't have them, half of them were planning to buy one within the next year.

The overlap between Mint.com's user base and iPhone usage was insane, it was phenomenal. It was a highly requested feature, so we put some engineers on it and got it out in very short order and launched it. I always knew that I wanted Mint.com to be mobile, but originally I thought that was going to be text message based.

You can actually—and you've been able to do this for four months now—you can get text message alerts and little reminders and you can query for your balances. You just text shortcode mymint.

Bob: OK.

Aaron: And type the word balance or bal. It'll send you your balances back when you're at a restaurant and you want to figure if you have enough money to pick up the tab. Or if you're in a store and you want to make a purchase and you want to see how much you've got on your credit card bill, it will tell you your balances right then.

Bob: OK. If you're sitting down with yourself right now and you're going to do another type of startup, another whole new venture, what lessons have you learned that you'd want to pass on to avoid some pain?

Aaron: Well, managing, raising capital, and figuring out what value the company should be at and when you should raise and when you shouldn't is definitely a big lesson that I didn't entirely understand until after raising a couple of rounds of financing.

The other lesson would be: hiring people is the very most important thing that you do at a company, a greater focus on the interview process, and training everyone to interview people well and deliberately. A lot of times people interview and they get into a room and they're, like, Well, I thought that guy sounded like he knew what he was talking about.

You need well-defined criteria for how you evaluate: who asks what questions. Make sure you cover all areas of technical and management skills. Ask the same sort of technical questions between two engineering candidates so that you can compare them head to head accurately, efficiently. All those things matter, but they're actually not done all that well in most companies.

Bob: Well, there is one more question that I really should ask: Here we are in 2009; the offline economy is looking like a train wreck.

Aaron: Yes.

Bob: Do you think it's a good, or a bad, or a great, or a horrible time to create a startup?

Aaron: I think if you're solving a real problem, it's always a good time to start a company, because if you don't do it, someone else will.

URL: http://www.rescuetime.com/

Disclosure: I did some strategy/positioning consulting with Tony Wright in 2008.

Area: Time management—individual, small business, and enterprise.

Platform(s): Web, with GUI-less Windows and Mac clients.

Summary: RescueTime puts a new spin on time management: target people who live at their keyboards and require zip effort on their part to track how much time they're spending on which apps and web sites.

Now, it may seem that CEO and founder Tony Wright has built a YARTTA—yet another Rails time tracking app. Well, the investors who've put up $900,000 after the initial Y Combinator seed round of funding beg to differ.

Chris Sacca, one of RescueTime's investors, had this to say about the Seattle-based startup to the BBC's Business Daily podcast.[96]

I have a little company called RescueTime. It's free for individuals and $4 to $8 a month. It watches and helps you understand where you spend your time online. So you're able to set time goals and targets for yourself so you realize, "Wow. I'm spending a lot of time on Twitter; maybe I need to focus back on my [business] Gmail account."

So that actually make employees 9% more efficient in the first month they use it. So companies are really excited to pay for it. They pay such a small fee for it, so the company does really well, despite being such a small company, and all the users are very happy to use it.

RescueTime's challenge, and why they're a case study for this chapter, is how you communicate clearly your startup's value to three different audiences, all of which have seen so many time management apps they've lost count (see Figure 7-4).

Start with a simple, brief hook, essentially the same for all three market segments.

Next, talk about what matters to each market segment. Effortless Time Tracking for individuals and small businesses; Business Intelligence You've Never Had Before for enterprise.

The AS SEEN IN bar has some very heavy media hitters: check out the following interview with Tony for how he got these positive mentions.

Make your web site's layout back up your message. Here, Tony is selling effortlessness, and the site could not be easier to understand or navigate.

Time management has been around for over a century. But what Tony and RescueTime are doing here is addressing the relatively new problem of reduced productivity, due primarily to oversurfing the Web, while steering well clear of evil software that involuntarily tracks employees' every keystroke, glance, and moment.

Here's what Tony had to say about how he got into Y Combinator, what that did for him, how he raised $900,000 after that, and what's left on his to-do list.

Bob: Let me ask you about RescueTime. First off, where did you get the idea?

Tony: It was born out of our personal inability to understand how we spend our time. Every day we had a scrum agile meeting. We're a bunch of software geeks. Everyone's job would say what they'd accomplished in the last 24 hours and what they were going to do in the next 24. We found that people's ability to articulate what they'd done, literally, just in the last workday, was terrible. People would say, well, I felt busy but I can't really articulate what I did.

We wanted to understand that, but we recognize that despite all these time management books that say keep a log of how you spend your time, that's incredibly impractical for a technology worker who's shifting between applications and websites, sometimes in 10-, 20-second blocks.

We wanted something that was totally passive that would answer those questions for us and for our business without actually requiring data entry, which is no fun.

Bob: So the biggest point was making it, as you say in your first bullet here, effortless.

Tony: Well, yeah. From a business perspective, whether you're a freelancer or a business, the idea is that time is precious. It's really hard to do a good job. If you screw up and don't do a good job for a couple of days, that data is irrecoverable. The effort was the thing that we thought prevented all knowledge workers from having this data at their fingertips—it's just too much of a pain in the butt.

Bob: Time management has actually been around for over a century now in one form or another. How did you break through people's resistance to, oh, it's just another time tracking application?

Tony: I'm not entirely sure we're done breaking through, but we're still trying. I think we've done a good job on a couple of fronts. I think one of the biggest things for us is that it does have a twist. I don't know if you've read the book called Made to Stick,[97] but it's about sticky ideas. One of the things that makes an idea sticky is that it's surprising. What we've done is put a surprising twist of—everyone's done time entry at one point or another in his or her life, or a lot of people have. Everyone's familiar with the concept. We've basically said this is just going to happen.

We also have some surprising stuff, in the sense of people who use it tend to be shocked by what they see. People have a picture in their head of what they think they do with their time. What they actually do with their time has only a bare relationship to that sometimes.

We get a lot of credibility and a lot of breakthrough, in that people talk about this. So they use RescueTime, they may go on Twitter, or they go on their blog, or they sit down at a bar somewhere and say, "Dear Lord, look what I found out. I had no idea." And that creates questions in other people's minds.

I think that part of the breakthrough comes from the kind of word-of-mouth engine; if you hear about something from someone else whom you trust, that's huge. That's basically them saying, "Yes, I understand that time management is something that everyone's tried and looked at and paid attention to and gotten frustrated with. But look what I did. It worked. I learned some things. I'm now smarter about myself."

The way we talked about is important, but I think the way we created something that made other people talk about it was arguably more important.

Bob: OK. Well, part of the credibility that really comes across when I look at this web site . . . By the way, I am disclosing we've done a little business together here. I look and I see New York Times, the BBC, PC World, Lifehacker, U.S. News, BusinessWeek, TechCrunch. How do you get all these major media brands to talk about you? Is there a strategy there, or did it happen by chance?

Tony: I would love to pat myself on the back for that or pat someone on our team on the back for that. I think, what we did, again, was, if I could give one bit of marketing advice for people, I would say get the book Made to Stick. It is absolutely awesome. I think we kind of stumbled into that. But that's how I map it—we really, again, created surprising data and we have some surprising data in aggregate. This is kind of a web-based service. This is in the cloud and has all the advantages web-based e-mail has over Outlook, for example.

And what we get as a result of that is the ability to say that the average person spends X hours in e-mail. Or the average person shifts to an instant message window 77 times per day. So, if you use IM, you're shifting to an instant message window 77 times per day on average.

Now there's obviously a mean. That kind of data, I think, really . . .

Bob: . . . creates headlines.

Tony: If you mention that to a reporter or a blogger and they say, "I can build an article around that," whether it's an article on how people could sort of manage instant message more effectively or just a sort of shock piece of, gosh, look how knowledge workers aren't getting stuff done.

Bob: Are these media brands calling you, or are you calling them? Do you send out press releases? Walk me through here.

Tony: Yeah, so we're not doing anything. We don't have anyone who's dedicated PR. I'm probably the closest thing to that as CEO. There are a couple overt things that we did. For example, we took this data that we thought was pretty shocking, the aggregate data of the entire user base, and made a little spreadsheet of: here are the top 100 applications and web sites that people are spending time on. We kind of made a list of that and what percentage they work. You could see, like, how much percentage time people spent on communication stuff or productivity stuff or word processing or what have you, or Google.

Then whatever we found, a surprising bit like that with that particular list, we sent that to TechCrunch. TechCrunch said, "Oh, we can build an article around that." I believe it was called "Early Adopters Still Sticking with Microsoft" or desktop products, or some such.

Showing the idea that, hey, while there is all this wonderful stuff in the cloud where you can word process and do spreadsheets and stuff, people are still really using the old-style desktop software for this stuff. Outlook is more dominant than Gmail. And, you know, we have pretty early-adopter audience yet.

So we would do stuff like that. I've done a speaking engagement as a result of the Y Combinator thing, because we were kind of in the productivity space. I think we got tapped for that. Someone asked Paul Graham if he knew a good startup to be on a panel at the Churchill Club, so I did a speaking engagement at the Churchill Club.

Bob: It sounds to me like one of your core strategies was to be remarkable.

Tony: Yeah, and, really, the subset of remarkable of the sort of surprising kind. Obviously, we could be incredibly beautiful. I mean, we try to focus a little bit on graphic design, but I don't think we're anywhere in the top 5% of most stunning web sites out there. But there's lots of remarkable things. We've really focused on the sort of surprising, and I think that's the sort of asset we have.

Bob: OK.

Tony: Really, I think that's one of the lessons that I really learned is that you need to have that twist, that hook that makes someone do a double take, and whether they say, "Wait a minute. There's no data entry" or "Wait a minute. People spend that much time doing that?" Something that basically makes someone give that second look, because of just the noise level out there, you need to have something like that.

Bob: You mentioned Y Combinator. Tell me what your experience was like.

Tony: It was kind of a forcing function for us. Y Combinator's basically a software incubator in the Valley that basically takes you into the Valley. You have to be down there for three months. So we relocated from Seattle to do this.

Bob: Now, who is "we"—you, or you and your partner?

Tony: Yeah. I had two cofounders. We were getting some traction and some exciting interest in our product. We had done a permission-marketing kind of campaign. At the very beginning of this, we weren't sure that anybody wanted it. So we put up a little, three-page splash site that said, "Hey, here's some screenshots that are fake of what we're building, and if you'd like to have this, give us your e-mail address and we'll let you know when we launch."

Bob: And how many people responded?

Tony: Well, on the basis of literally that three-page HTML site with no code behind it, we got on TechCrunch. And the way we got on TechCrunch was, again, very organic. We didn't pitch them. We posted on a couple of forums in various places: "Hey, here's a site." And all we really wanted to do was measure, for every 100 people who we can get to come to the site, what percentage of them will give us their e-mail address? What is their sort of take rate for this value proposition and these screenshots that we're pitching?

And we found that about a third of the users who came to the site would give us their e-mail address, which was very encouraging. TechCrunch will give you 12,000 to 14,000 uniques over a weeklong period. I mean, we got about 4,000 from TechCrunch, and then a lot of splash coverage from that.

Bob: So you started by saying to the world, "This is what we're going to do. Do you want us to do it?"

Tony: Yeah. [laughs]

Bob: And no code, other than whatever form you had.

Tony: Yep.

Bob: And from there you got press, because TechCrunch picked it up, because they decided to pick it up. Did you apply to Y Combinator? Did they come to you? How did that happen?

Tony: Y Combinator has an application process. And the Y Combinator thing was kind of my idea to my cofounders to say, "Hey, I want us all to jump into this full time." And we all had full-time jobs. We were fairly well compensated for what we did. So Y Combinator was sort of a, "Hey, if Y Combinator accepts our application, that will be sort of the thing that pushes us out of the nest, so to speak." [laughs] So we did apply. It's a one-and-a-half-page application, very small. It takes probably a couple hours to fill out well. And so the process, they won't publish how many people apply, but it's in the sort of thousands of people apply for about 20-ish company slots.

Bob: OK.

Tony: And they will basically call you if they like your application and fly out—I think, for us, it was about 50 or 60 people—to go through a 10-minute interview process. We managed to get 17 minutes, so we were fairly encouraged by that. But that is the amount of time that they give to you. And that interview process is just riotous in its chaos. It's pretty amazing. So you go in, and you think you have this agenda and this demo that you're going to pitch. And they very strongly emphasize that if you're going to go to Y Combinator for this interview that you'd darn well better have a demo.

So we had this demo and this flow that we were going to show them through the demo. We got about two minutes into the demo, and then we start getting peppered with questions. And it goes off on tangents. It's really just total stream of consciousness from Paul Graham and the other interviewers, just peppering us with questions.

So the agenda that we had sort of set up and the practice that we did was not—I mean, it was valuable, I think, but it had very little resemblance to reality.

So if you're going to practice for that particular interview, I would practice—find someone who will pretend to interview you and constantly pepper you with questions.

Bob: You mean, like, grill you unmercifully?

Tony: Yeah. [laughs] I would say that's pretty safe. And they ask very good questions. When you get the gist of a demo, it doesn't make sense to get into the sort of details of what the software does, because the software's going to change dramatically.

Bob: OK.

Tony: So the sort of central tenets of Y Combinator are "Build something people want," which is seemingly obvious, but so many people build things that are neat that no one actually wants, that are technologically impressive that no one has an itch for. So "Build something that people want" is really the sort of core thing that they're after. And beyond that, [laughs] they don't have a lot of criteria.

Bob: And what were the top three things or one thing or five things that you got out of Y Combinator?

Tony: It's a pretty long list. Toward the top, a real quick one is obviously just the credibility. This is a pretty exclusive club that Y Combinator has kind of built. So if you've made it through there, that immediately gets you access to reporters and investors and bloggers and things that you wouldn't otherwise have easy access to. It's a bit of a leg up, there. There's obviously the huge mentorship that Paul Graham, Trevor Blackwell, and Jessica Livingston all provide. They are very generous on that front.

These guys, obviously . . . You think about what most mentors have. They have maybe one startup under their belt or maybe two. I think with that, oftentimes you don't necessarily have great pattern recognition. You might have seen one way that things succeeded. But you've only really seen one kind of success.

Paul Graham, having mentored, literally—I think he's into about 150 of these companies. I think Paul Graham and all of these guys have a really unique perspective. They can see patterns in startups that other people can't see because they don't have the depth of the variety of startup vision that Paul had.

Bob: Right. OK.

Tony: I think that's really powerful. I think one of the hugest lessons was: Build something that a small number of people want a lot rather than a lot of people want a little. Find a small audience that would literally chew off their own leg to have what you are building.

Bob: [laughs] OK.

Tony: The idea there is that once you find a heart of people who are madly in love with what you are doing, then to get bigger and more successful as a startup, all you need to do is find more people like that or move laterally to serve a slightly different type of audience. An example is, you might say, "Gosh, we serve a small audience. You're making a small product." Craigslist launched serving San Francisco. They are a little bit bigger than that now. Amazon launched selling books. Gosh, they are doing a little bit more than books now.

If you do it the other way, and you make something that everyone kind of thinks is neat, then what is the action item for you to get more successful? What do you do? You basically have to make them want it more. What is the formula for making them want it more? It's a hard formula to know. You don't know what's missing from your product to make them love it, because right now they only just like it.

Bob: I see where you're going with this.

Tony: That was really kind of a neat thing to hear. We focused on our core users, the users who are really enjoying it and yelling at us to build certain things and add certain things to the product. Yeah, and Paul, the other thing that he really focuses on is to listen to your users. If you aren't building something that you yourself are madly in love with . . . Paul built Viaweb, which was an e-commerce platform.

Bob: I remember it.

Tony: He wasn't necessarily a shop owner. He was a software developer who saw a need. So when you aren't building something that you yourself are a passionate user for, listen to your users. Be constantly engaged with them, and make sure you understand what they need. It's not always what they say they need. That's an art form in and of itself.

Bob: How much did that $20,000 help?

Tony: Part of the Y Combinator thing is that they do you give you money. You notice that I didn't list that on the valuable assets that we got from Y Combinator. For us, Y Combinator attracts a bunch of different types of people, ranging from 20 years old to I think the oldest is 40. You don't want to talk about it too much, but some of those guys are going to the Y Combinator meetings driving Mercedes SLKs. Especially as Y Combinator gets more and more credibility, you get higher- and higher-end people applying.

I don't think the financial motivation is that it's nice for someone, some wunderkind, applying out of college and wanting to live in an apartment and eat Ramen. We live pretty cheaply, but obviously the money doesn't get you far. It gets you three months' worth of server bills, rent, and Ramen. [laughs] That's how I always put it.

Bob: Were you building RescueTime while you were in the Y Combinator program, or did that come later? In other words, how long before you launched 1.0?

Tony: That's the other thing that Paul emphasizes. I keep saying Paul and that's wrong. It should be Y Combinator.

Bob: OK. We'll take that as the entire Y Combinator team.

Tony: He is the squeakiest wheel there. One of the other things that he emphasizes is to release early. Get something out the door. Because before you get it out the door, you are operating on theories. Just like no battle plan survives contact with the enemy, no product plan survives contact with the users. Yeah. Basically, the idea with Y Combinator is almost everybody . . . He'll push really hard and at the end of three months, you'd better have launched your product. Some people take a little bit longer.

Certain products are more ambitious, obviously, than others. But really, finding that barest iota of value that you can create and trimming your feature set down so that you can launch it. Start getting that user feedback and that market understanding that you are just guessing at now.

Bob: Were you able to launch?

Tony: Yeah, we sure were. We weren't unique; this is happening more and more with Y Combinator. We had a moderately flushed-out alpha release even before we interviewed. We had a richer demo than a lot of people did. Some people apply literally with just an idea, and then have two weeks between their application and their interview to build some sort of demo.

That is the other kind of pattern recognition that Y Combinator tries to do: trying to understand what the recipe for a successful entrepreneur is.

I think initially they had a stronger bias toward education than they do. They used to think, "Oh, Ivy League is a good thing." I think, at this point they think it is a nonsignificant thing. It's not a bad thing, but it's not a serious determiner of success.

One of the things that they really focus on now is people who can't stop building stuff. If you can build a demo of something even moderately interesting in two weeks, that's encouraging. If you've actually got something out in the world, that's encouraging. That is a lot of what Y Combinator is a test of. Can you build something that people want in two weeks or three months?

Bob: OK.

Tony: Just about everybody did. I think there is one team that hasn't launched and a couple of teams that launched a little bit afterward.

Bob: Let me ask you a couple of more questions, and I think that will wrap it up.

Tony: Sure.

Bob: If you and your partners had not gone down to Silicon Valley and made this commitment to jump in to doing this app pretty much full time, do you think you would have succeeded?

Tony: I don't think so. I still think success is not a foregone conclusion. But I don't think we would have had the shot that we do. One of the things—and this is another Paul Graham-ism that I constantly parrot—the biggest motivator for most people isn't financial. It isn't building cool stuff. For a lot of people it is fear of public shame.

Bob: [laughs]

Tony: The way you hack this is . . . This is a life hack, right? People do this for weight loss and other things—they make a public declaration of intent. It means that if your startup fails, you are a failure. And if we hadn't jumped in full time, it would have been a side project. There have been times with RescueTime where things looked tough, right? We had a hard time.

Bob: Right.

Tony: It wasn't fun anymore. You push through those walls. But if it's just a side project, you don't have a ton of incentive to push through those walls. Because, gosh, you have this other idea that sounds like a lot of fun—your day job.

Bob: There is always another technology to chase.

Tony: Yeah. There is always something else fun to do. Now, if I publicly say, "RescueTime and Tony Wright are the exact same thing. When RescueTime fails, Tony Wright fails. This is now my livelihood." It is no longer the side project that didn't work out. It's the livelihood or core thing that is failing in Tony's life. That is a huge motivator, I think. Could we have done that without Y Combinator? Certainly. I think the cash didn't hurt. One of the things that I probably didn't list on the Y Combinator advantages that I could is that, after Y Combinator, about six months after Y Combinator ended, we raised a small Series A—very small and small on purpose. But nonetheless, it gave us the ability to have actual paychecks for the foreseeable future.

Bob: According to CrunchBase, your Series A was $900,000.

Tony: Yeah.

Bob: Let me ask it this way. Did Y Combinator up open doors you wouldn't have known about otherwise?

Tony: Absolutely.

Tony: Yeah, for the fundraising stuff, absolutely. Fundraising is hard. If anyone says, "Tell me the bullet points about fundraising that I should care about." For early-stage fundraising, the only bullet point you should care about is that there are two things that can allow you to raise early-stage funding. One is traction: people who are either paying for or using—whether you are a consumer or a business—either paying for or actively using your application and a growth curve that keeps growing. Or a rock star team, basically. You have Bill Gates coming out of retirement to help you with your product, or what have you.

Bob: How did you get Tim Ferriss, who I assume is the same Tim Ferriss we all know and love from "The 4-Hour Workweek"?

Tony: Yeah, that is. [laughs] Tim was interesting. He was introduced through another angel. This is really awesome. It's a great story. Tim actually was evangelizing RescueTime before we ever said a word to him. We saw in a US News and World Report interview with him that he was recommending Rescue Time. I was, like, "Oh my God, Ferriss is recommending us. How awesome is that?" I tried to e-mail him a thank you and never got anything back. The guy obviously gets as much e-mail as anybody.

Bob: Yeah.

Tony: When we were actually fundraising, one of the guys who did express interest in being an angel said, "Do you know who you should talk to is Tim Ferriss, and let me make an introduction." That is another lesson in fundraising: introductions win big. If you have an introduction from someone they trust, that is 90% of the battle.

On Y Combinator demo day, which is the big coming-out party at the end of Y Combinator, where you present to 100 to 150 investors. From that we maybe landed, ultimately, one or two investors. Every one of the other investors that we landed was an introduction chain from those initial investors.

So (a) introductions win and (b) you have to ask for them. If you have someone onboard who is willing to fund you, you say, "Can you give me five names of people who you think might be a good fit as an investor, and can you make that introduction? That is your first job as an investor." [laughs]

Bob: I think the key thing, to roll this all the way back, is you wouldn't have gotten those introductions—you probably wouldn't have gotten into Y Combinator—if you hadn't started with something that was remarkable and made people double take, based on what you could show them there.

Tony: Right. Absolutely. I think that making something remarkable and not underestimating the challenges of an early-stage startup are critical. If you are going to be funded, I think Y Combinator, TechStars, or anything of that sort is so incredibly valuable.

In this chapter we've discussed just how you go about marketing your startup's product with clarity and results. I've suggested that the right way forward is to understand and craft what I call a Unique Selling Proposition, and to make sure your web site delivers the components of that offer in the right way, in the right order.

We've talked to two startups who have made the leap from "I want" to "I am," and seen the outlines of how they got there while we've examined their web sites and how they communicate their USPs.

In the next chapter, we'll talk to a different kind of startup and arguably one of the foremost leaders in personal productivity, David Allen. And, standing on the shoulders of giants, I'll offer some suggestions on how you can and how you must improve your online, developer, and startup founder productivity.

[87] http://www.markjoyner.name//logs/mj_books.php

[88] MicroISVs Sites That Sell!, and I apologize for the exclamation mark. http://www.47hats.com/?page_id=534.

[89] Did you think it was an accident that all those weird television ads with impossible claims and promises are on late-night television?

[90] Of course, there are no happy Windows users, just some who have a higher pain threshold and can endure almost anything before they beg for mercy (joke!).

[91] Such as having a very detailed About page showing who you are and where; making sure your site's text is written in grammatically perfect English; using a blog and other social media so that people can get to know you; and having a product that's loaded with real value.

[92] As of May 1, 2009.

[93] This raises an interesting point I'll leave up to you to think about: What's the bell curve of your primary market segment? Are you going for the early adopters, the online mainstream where the money is, or those just now joining the show. It's a good thing to know in terms of how you construct your USP.

[94] http://www.crunchbase.com/company/mint is wrong: First Round Capital's investment was part of the angel round, not separate. So says Aaron, and he should know.

[95] I love those MintFanatic videos. If your market is comfortable with videos of themselves online, these are powerful. Check out 12seconds and, of course, YouTube.

[96] January 6, 2009. If you're not listening to this podcast and the BBC's Peter Day's World of Business, you should be.

[97] "Made to Stick: Why Some Ideas Survive and Others Die" by Chip and Dan Heath (Random House, 2007), http://www.madetostick.com