28

ACCOUNTING FOR LEASES

- Perspective and Issues

- Definitions of Terms

- Concepts, Rules, and Examples

- Classification of Leases—Lessee

- Classification of Leases—Lessor

- Distinction between Sales-Type, Direct Financing, and Leveraged Leases

- Accounting for Leases—Lessee

- Accounting for Leases—Lessor

- Special Situations

- Change in residual value

- Change in the provisions of a lease

- Termination of a lease

- Renewal or extension of an existing lease

- Leases between related parties

- Accounting for leases in a business combination

- Accounting for changes in lease agreements resulting from refunding of tax-exempt debt

- Sale or assignment to third parties; nonrecourse financing

- Transfers of residual value (FASB ASC 860-10)

- Accounting for a sublease

- Sale-Leaseback Transactions

- Leases Involving Real Estate

- Reporting of Current and Noncurrent Lease Receivable (Lessor) and Lease Obligations (Lessee)

- Disclosure Requirements

PERSPECTIVE AND ISSUES

Lease transactions have grown in popularity over the years as many organizations look for new ways to finance their fixed asset additions. Leases have grown increasingly popular for office equipment, including PCs, photocopiers, and telephone systems. For not-for-profit organizations, leases for such items offer a way to finance asset “acquisitions” relatively easily, while spreading the cost of the equipment over the period that it is used; a good technique for tight annual budget requirements. The concepts contained in this chapter for the calculation of the present value of a capital lease are essentially the same as those that would be used by a not-for-profit organization to calculate the present value of a long-term pledge of the use of property. Chapter 9 provides more information on recording contributions. A lease agreement involves at least two parties, a lessor and a lessee, and an asset that is to be leased. The lessor, who owns the asset, agrees to allow the lessee to use it for a specified period of time in return for periodic rent payments. Not-for-profit organizations enter into and account for leases the same way as commercial enterprises. Leases that are sales-type and direct financing leases are less common transactions for not-for-profit organizations, although this chapter will provide the basics of these types of transactions.

FASB ASC 840 is the primary repository for promulgated GAAP for lease accounting.

Lessee Accounting

ASU 2016-02 provides that a lessee should recognize the assets and liabilities that arise from leases. All leases create an asset and a liability for the lessee and recognition of those lease assets and lease liabilities that ASU 2016-02 represents is an improvement over current GAAP, which did not require lease assets and lease liabilities to be recognized for most leases.

Under ASU 2016-02, a lessee should recognize in the statement of financial position a liability to make lease payments (the lease liability) and a right-of-use asset representing its right to use the underlying asset for the lease term. When measuring assets and liabilities arising from a lease, a lessee (and a lessor) should include payments to be made in optional periods only if the lessee is reasonably certain to exercise an option to extend the lease or not to exercise an option to terminate the lease. Similarly, optional payments to purchase the underlying asset should be included in the measurement of lease assets and lease liabilities only if the lessee is reasonably certain to exercise that purchase option. Reasonably certain is a high threshold that is consistent with and intended to be applied in the same way as the reasonably assured threshold in the previous leases guidance. In addition, also consistent with the previous leases guidance, a lessee (and a lessor) should exclude most variable lease payments in measuring lease assets and lease liabilities, other than those that depend on an index or a rate or are in substance fixed payments.

For leases with a term of twelve months or less, a lessee is permitted to make an accounting policy election by class of underlying asset not to recognize lease assets and lease liabilities. If a lessee makes this election, it should recognize lease expense for such leases generally on a straight-line basis over the lease term.

The recognition, measurement, and presentation of expenses and cash flows arising from a lease by a lessee have not significantly changed from current GAAP. There continues to be a differentiation between finance leases and operating leases. However, the principal difference from previous guidance is that the lease assets and lease liabilities arising from operating leases should be recognized in the statement of financial position.

For finance leases, a lessee is required to do the following:

- Recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in the statement of financial position.

- Recognize interest on the lease liability separately from amortization of the right-of-use asset.

- Classify repayments of the principal portion of the lease liability within financing activities and payments of interest on the lease liability and variable lease payments within operating activities in the statement of cash flows.

For operating leases, a lessee is required to do the following:

- Recognize a right-of-use asset and a lease liability, initially measured at the present value of the lease payments, in the statement of financial position.

- Recognize a single lease cost, calculated so that the cost of the lease is allocated over the lease term on a generally straight-line basis.

- Classify all cash payments within operating activities in the statement of cash flows.

Lessor Accounting

ASU 2016-02 notes that the accounting applied by a lessor is largely unchanged from that applied under current GAAP. For example, the vast majority of operating leases should remain classified as operating leases, and lessors should continue to recognize lease income for those leases on a generally straight-line basis over the lease term.

Future editions of this book will include additional details on ASU 2016-02 as its effective date becomes nearer.

Definition of a Lease

ASU 2016-02 provides that at inception of a contract, an entity should determine whether the contract is or contains a lease. A lease is defined as a contract, or part of a contract, that conveys the right to control the use of identified property, plant, or equipment (an identified asset) for a period of time in exchange for consideration. Control over the use of the identified asset means that the customer has both (1) the right to obtain substantially all of the economic benefits from the use of the asset and (2) the right to direct the use of the asset.

Under the lessee accounting model in previous GAAP, the critical determination was whether a lease was a capital lease or an operating lease because lease assets and lease liabilities were recognized only for capital leases. ASU 2016-02 provides that the critical determination is whether a contract is or contains a lease because lessees are required to recognize lease assets and lease liabilities for all leases—finance and operating—other than short-term leases (that is, if the entity elects the short-term lease recognition and measurement exemption). ASU 2016-02 provides detailed guidance and several examples to illustrate the application of the definition of a lease to assist entities in making this critical determination.

Components

ASU 2016-02 requires an entity to separate the lease components from the nonlease components (for example, maintenance services or other activities that transfer a good or service to the customer) in a contract. Although this was a requirement in previous GAAP, ASU 2016-02 provides more guidance on how to identify and separate components than previous GAAP. Only the lease components must be accounted for in accordance with ASU 2016-02's lease accounting standards. The consideration in the contract is allocated to the lease and nonlease components on a relative standalone price basis (for lessees) or in accordance with the allocation guidance as provided in ASU 2016-02 (for lessors). Consideration attributable to nonlease components is not a lease payment and, therefore, is not included in the measurement of lease assets or lease liabilities. Further, ASU 2016-02 provides that activities that do not transfer a good or service to the lessee or amounts paid solely to reimburse costs of the lessor are not components in a contract and are not allocated any of the consideration in the contract.

ASU 2016-02 provides a practical expedient for lessees as it relates to separating lease components from nonlease components. Lessees may make an accounting policy election by class of underlying asset not to separate lease components from nonlease components. If an entity makes that accounting policy election, it is required to account for the nonlease components together with the related lease components as a single lease component.

Effective Date

For a not-for-profit organization that is a conduit debt obligor, ASU 2016-02 will be effective for fiscal years beginning after December 15, 2018. For other not-for-profit entities, ASU 2016-02 will be effective for fiscal years beginning after December 15, 2019. Earlier application is permitted.

ASU 2018-01 is effective at the same time ASU 2016-02 is adopted. If ASU 2016-02 has been early adopted, ASU 2018-01 should be applied upon issuance.

The FASB also issued four additional ASUs during 2018 and early 2019 that made targeted changes to the lease accounting under ASU 2016-02. These were as follows:

- ASU 2018-10 Codification Improvements to Topic 842, Leases;

- ASU 2018-11 Leases (Topic 842): Targeted Improvements;

- ASU 2018-20 Leases (Topic 842): Narrow-Scope Improvements for Lessors;

- ASU 2019-01 Leases (Topic 842): Codification Improvements.

ASU 2018-10 addresses a number of inconsistencies in the FASB Codification, many based on users' comments. The focus of this ASU was correcting these inconsistencies, rather than providing any significant changes to the lease accounting standards.

ASU 2018-11 address two implementation matters:

- An additional transition method is being permitted, which allows entities to initially apply the new lease standard at the adoption date and recognize a cumulative-effect adjustment to the opening balance of net assets in the period of adoption. This method is in addition to the modified transition method that would have required that the lease standard be implemented for the earliest period presented in comparative statements.

- The existing lease standard provided a practical expedient to lessees, by class of underlying asset, to not separate nonlease components from the associated lease component. This ASU provides this practical expedient to lessors. However, the lessor practical expedient is limited to circumstances in which the nonlease components would otherwise be accounted for under the new revenue recognization standards and both

- the timing and pattern of transfer are the same for the nonlease component, and

- the lease component, if accounted for separately, would be classified as an operating lease.

ASU 2018-20 addresses these three specific issues:

- The lease accounting standard required entities to analyze sales and similar taxes on a jurisdiction by jurisdiction basis to determine whether those taxes are the primary obligation of the lessor or lessee on behalf of third parties. This ASU permits lessors to make an accounting policy election to exclude sales and similar taxes from the lease transaction price.

- Requires lessors to exclude from variable payments, and thus lease revenue, lessor costs paid by a lessee directly to a third party. However, costs that are excluded from the consideration in a contract that are paid directly to a third party by the lessor and reimbursed by the lessee are lessor costs to be accounted for as variable payments.

- This ASU also addresses an implementation question regarding recognition of variable payments for contracts with lease and nonlease components. This ASU requires lessors to allocate (rather than recognize, as currently required) certain variable payments to the lease and nonlease components when the changes in facts and circumstances on which the variable payment is based occur. After the allocation, the amount of variable payments allocated to the lease components will be recognized as income in profit or loss, while the amount of variable payments allocated to nonlease components will be recognized in accordance with other standards, such as the revenue recognition standards.

ASU 2019-01 addresses three additional matters related to the lease accounting standards:

- Lessors that are not manufacturers or dealers will use their cost, reflecting any volume or trade discounts that may apply, as the fair value of the underlying asset. However, if significant time lapses between the acquisition of the underlying asset and lease commencement, those lessors will be required to apply the definition of fair value.

- Lessors that are depository and lending institutions should report all principal payments received under leases with investing activities on the statement of cash flows.

- Explicitly provides an exception to interim disclosure standards in transition disclosure requirements.

All four of these ASUs would be applied at the same time that the lease accounting standards are implemented.

DEFINITIONS OF TERMS

The following definitions will be helpful in understanding the accounting for leases.

Bargain purchase option. A provision allowing the lessee the option of purchasing the leased property for an amount, exclusive of lease payments, which is sufficiently lower than the expected fair value of the property at the date the option becomes exercisable. Exercise of the option must appear reasonably assured at the inception of the lease. GAAP does not offer additional guidance defining “sufficiently lower,” in which many factors such as time, value of money, usage, and technological changes influence whether the option fulfills the criteria for a bargain.

Bargain renewal option. A provision allowing the lessee the option to renew the lease agreement for a rental payment sufficiently lower than the expected fair rental of the property at the date the option becomes exercisable. Exercise of the option must appear reasonably assured at the inception of the lease.

Contingent rentals. Rentals that represent the increases or decreases in lease payments that result from changes in the factors on which the lease payments are based occurring subsequent to the inception of the lease. However, changes due to the pass-through of increases in the construction or acquisition cost of the leased property or for increases in some measure of cost during the construction or preconstruction period should be excluded from contingent rentals. Also, provisions that are dependent upon only the passage of time should be excluded from contingent rentals. A lease payment that is based on an existing index or rate, such as the consumer price index or the prime rate, is a contingent payment, and the computation of the minimum lease payments should be based on the index or rate applicable at the inception of the lease.

Estimated economic life of leased property. The estimated remaining time for which the property is expected to be economically usable by one or more users, with normal maintenance and repairs, for its intended purpose at the inception of the lease. The economic life may be determined by such factors as technological changes, normal deterioration, and physical usage. Judgment on these matters may be influenced by knowledge gained through previous experience. This estimated time period should not be limited by the lease term.

Estimated residual value of leased property. The estimated fair value of the leased property at the end of the lease term.

Executory costs. Those costs such as insurance, maintenance, and taxes incurred for leased property, whether paid by the lessor or lessee. Amounts paid by a lessee in consideration for a guarantee from an unrelated third party of the residual value are also executory costs. If executory costs are paid by the lessor, any lessor's profit on those costs is considered the same as executory costs.

Fair value of leased property. The property's selling price in an arm's-length transaction between unrelated parties.

When the lessor is a manufacturer or dealer, the fair value of the property at the inception of the lease will ordinarily be its normal selling price net of volume or trade discounts. In some cases, due to market conditions, fair value may be less than the normal selling price or even the cost of the property.

When the lessor is not a manufacturer or dealer, the fair value of the property at the inception of the lease will ordinarily be its costs net of volume or trade discounts. However, if a significant amount of time has lapsed between the acquisition of the property by the lessor and the inception of the lease, fair value should be determined in light of market conditions prevailing at the inception of the lease. Thus, fair value may be greater or less than the cost or carrying amount of the property.

Implicit interest rate. The discount rate that, when applied to the minimum lease payments, excluding that portion of the payments representing executory costs to be paid by the lessor, together with any profit thereon, and the unguaranteed residual value accruing to the benefit of the lessor, causes the aggregate present value at the beginning of the lease term to be equal to the fair value of the leased property to the lessor at the inception of the lease, minus any investment tax credit retained and expected to be realized by the lessor (and plus initial direct costs in the case of direct financing leases).

Inception of the lease. The date of the written lease agreement or commitment (if earlier) wherein all principal provisions are fixed and no principal provisions remain to be negotiated.

Incremental borrowing rate. The rate that, at the inception of the lease, the lessee would have incurred to borrow over a similar term (i.e., a loan term equal to the lease term) the funds necessary to purchase the leased asset.

Initial direct costs.1 Only those costs incurred by the lessor that are (1) costs to originate a lease incurred in transactions with independent third parties that (a) result directly from and are essential to acquire that lease, and (b) would not have been incurred had that leasing transaction not occurred, and (2) certain costs directly related to specified activities performed by the lessor for that lease. Those activities are evaluating the prospective lessee's financial condition; evaluating and recording guarantees, collateral, and other security arrangements; negotiating lease terms; preparing and processing lease documents; and closing the transaction. The costs directly related to those activities shall include only that portion of the employees' total compensation and payroll-related fringe benefits directly related to time spent performing those activities for that lease and other costs related to those activities that would not have been incurred but for that lease. Initial direct costs shall not include costs related to activities performed by the lessor for advertising, soliciting potential lessees, servicing existing leases, and other ancillary activities related to establishing and monitoring credit policies, supervision, and administration. Initial direct costs shall not include administrative costs, rent, depreciation, any other occupancy and equipment costs and employees' compensation and fringe benefits related to activities described in the previous sentence, unsuccessful origination efforts, and idle time.

Lease. An agreement conveying the right to use property, plant, or equipment (land or depreciable assets or both) usually for a stated period of time.

Lease term. The fixed, noncancelable term of the lease plus the following:

- Periods covered by bargain renewal options;

- Periods for which failure to renew the lease imposes a penalty on the lessee in an amount such that renewal appears, at the inception of the lease, to be reasonably assured;

- Periods covered by ordinary renewal options during which a guarantee by the lessee of the lessor's debt directly or indirectly related to the leased property is expected to be in effect, or a loan from the lessee to the lessor directly or indirectly related to the leased property is expected to be outstanding;

- Periods covered by ordinary renewal options preceding the date that a bargain purchase option is exercisable;

- Periods representing renewals or extensions of the lease at the lessor's option.

However, the lease term shall not extend beyond the date a bargain purchase option becomes exercisable.

Minimum lease payments. For the lessee: The payments that the lessee is or can be required to make in connection with the leased property. Contingent rental guarantees by the lessee of the lessor's debt, and the lessee's obligation to pay executory costs are excluded from minimum lease payments. Additionally, if a portion of the minimum lease payments representing executory costs is not determinable from the provisions of the lease, an estimate of executory costs shall be excluded from the calculation of the minimum lease payments. If the lease contains a bargain purchase option, only the minimum rental payments over the lease term and the payment called for in the bargain purchase option are included in minimum lease payments. Otherwise, minimum lease payments include the following:

- The minimum rental payments called for by the lease over the lease term.

- Any guarantee of residual value at the expiration of the lease term made by the lessee (or any party related to the lessee), whether or not the guarantee payment constitutes a purchase of the leased property. When the lessor has the right to require the lessee to purchase the property at termination of the lease for a certain or determinable amount, that amount shall be considered a lessee guarantee. When the lessee agrees to make up any deficiency below a stated amount in the lessor's realization of the residual value, the guarantee to be included in the MLP is the stated amount rather than an estimate of the deficiency to be made up.

- Any payment that the lessee must or can be required to make upon failure to renew or extend the lease at the expiration of the lease term, whether or not the payment would constitute a purchase of the leased property.

For the lessor: The payments described above plus any guarantee of the residual value or of the rental payments beyond the lease term by a third party unrelated to either the lessee or lessor (provided the third party is financially capable of discharging the guaranteed obligation).

Noncancelable. In this context this is a lease that is cancelable only upon one of the following conditions:

- The occurrence of some remote contingency.

- The permission of the lessor.

- The lessee enters into a new lease with the same lessor.

- The lessee pays a penalty in an amount such that continuation of the lease appears, at inception, reasonably assured.

Nonrecourse financing. Lending or borrowing activities in which the creditor does not have general recourse to the debtor but rather has recourse only to the property used for collateral in the transaction or other specific property.

Penalty. Any requirement that is imposed or can be imposed on the lessee by the lease agreement or by factors outside the lease agreement to pay cash, incur or assume a liability, perform services, surrender or transfer an asset or rights to an asset or otherwise forgo an economic benefit, or suffer an economic detriment.

Related parties. Entities that are in a relationship where one party has the ability to exercise significant influence over the operating and financial policies of the related party. Examples include the following:

- A parent company and its subsidiaries;

- An owner company and its joint ventures and partnerships;

- An investor and its investees.

The ability to exercise significant influence must be present before the parties can be considered related. Significant influence may also be exercised through guarantees of indebtedness, extensions of credit, or through ownership of debt obligations, warrants, or other securities. If two or more entities are subject to the significant influence of a parent, owner, investor, or common officers or directors, then those entities are considered related to each other.

Renewal or extension of a lease. The continuation of a lease agreement beyond the original lease term, including a new lease where the lessee continues to use the same property.

Sale-leaseback accounting. A method of accounting for a sale-leaseback transaction in which the seller-lessee records the sale, removes all property and related liabilities from its balance sheet, recognizes gain or loss from the sale, and classifies the leaseback in accordance with this section.

Unguaranteed residual value. The estimated residual value of the leased property exclusive of any portion guaranteed by the lessee, by any party related to the lessee, or any party unrelated to the lessee. If the guarantor is related to the lessor, the residual value shall be considered as unguaranteed.

Unrelated parties. All parties that are not related parties as defined above.

CONCEPTS, RULES, AND EXAMPLES

Classification of Leases—Lessee

For accounting and reporting purposes the lessee has two alternatives in classifying a lease:

- Operating;

- Capital.

The proper classification of a lease is determined by the circumstances surrounding the transaction. According to SFAS 13 (FASB ASC 840), if substantially all of the benefits and risks of ownership have been transferred to the lessee, the lease should be recorded as a capital lease. Substantially all of the risks or benefits of ownership are deemed to have been transferred if any one of the following criteria has been met:

- The lease transfers ownership to the lessee by the end of the lease term.

- The lease contains a bargain purchase option.

- The lease term is equal to 75% or more of the estimated economic life of the leased property, and the beginning of the lease term does not fall within the last 25% of the total economic life of the leased property.

- The present value (PV) of the minimum lease payments at the beginning of the lease term is 90% or more of the fair market value to the lessor less any investment credit retained by the lessor. This requirement cannot be used if the lease's inception is in the last 25% of the useful economic life of the leased asset. The interest rate, used to compute the PV, should be the incremental borrowing rate of the lessee unless the implicit rate is available and lower.

If a lease agreement meets none of the four criteria set forth above, it is to be classified as an operating lease on the books of a lessee.

Classification of Leases—Lessor

The four options a lessor has in classifying a lease are as follows:

- Operating;

- Sales-type;

- Direct financing;

- Leveraged.

The conditions surrounding the origination of the lease determine its classification on the books of the lessor. If the lease meets any one of the four criteria specified above and both of the qualifications set forth below, the lease is classified as a sales-type lease, direct financing lease, or leveraged lease depending upon the conditions present at the inception of the lease.

Qualifications include:

- Collectibility of the minimum lease payments is reasonably predictable.

- No important uncertainties surround the amount of unreimbursable costs yet to be incurred by the lessor under the lease.

If a lease transaction does not meet the criteria for classification as a sales-type lease, a direct financing lease, or a leveraged lease as specified above, it is to be classified on the books of the lessor as an operating lease. This classification process must take place prior to considering the proper accounting treatment.

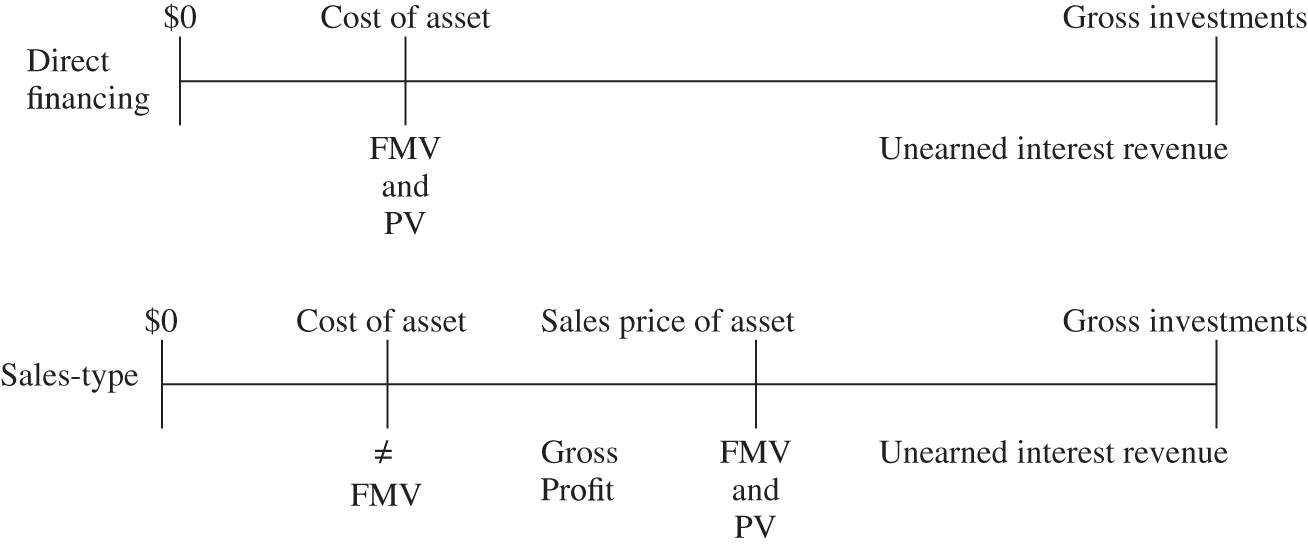

Distinction between Sales-Type, Direct Financing, and Leveraged Leases

A lease is classified as a sales-type lease when the criteria set forth above have been met and the lease transaction is structured in such a way that the lessor (generally a manufacturer or dealer) recognizes a profit or loss on the transaction in addition to interest revenue. (While not-for-profit organizations are generally not parties to sales-type leases, this chapter includes this discussion for the infrequent instances when they may be.) In order for this to occur, the fair value of the property must be different from the cost (carrying value). The essential substance of this transaction is that of a sale, and thus its name.

A direct financing lease differs from a sales-type lease in that the lessor does not realize a profit or loss on the transaction other than interest revenue. In a direct financing lease, the fair value of the property at the inception of the lease is equal to the cost (carrying value). This type of lease transaction most often involves entities engaged in financing operations. The lessor (usually a bank or other financial institution) purchases the asset and then leases the asset to the lessee. This transaction merely replaces the conventional lending transaction where the borrower uses the borrowed funds to purchase the asset. There are many economic reasons why the lease transaction is considered. They are as follows:

- The lessee (borrower) is able to obtain 100% financing.

- The benefits are flexible.

- The lessor receives the equivalent of interest as well as an asset with some remaining value at the end of the lease term.

In summary, it may help to visualize the following chart when considering the classification of a lease:

One form of a direct financing lease is a leveraged lease. This type is mentioned separately both here and in the following section on how to account for leases because it is to receive a different accounting treatment by a lessor. A leveraged lease meets all the defined criteria of a direct financing lease, but differs because it involves at least three parties: a lessee, a long-term creditor, and a lessor (commonly referred to as the equity participant). Other characteristics of a leveraged lease are as follows:

- The financing provided by the long-term creditor must be without recourse as to the general credit of the lessor, although the creditor may hold recourse with respect to the leased property. The amount of the financing must provide the lessor with substantial “leverage” in the transaction.

- The lessor's net investment declines during the early years and rises during the later years of the lease term before its elimination. (FASB ASC 840-10-25-43)

Service concession arrangements are arrangements between a public-sector entity grantor and an operating entity under which the operating entity operates the grantor's infrastructure (for example, airports, roads, and bridges). The operating entity also may provide the construction, upgrading, or maintenance services of the grantor's infrastructure. The scope of ASU 201-05 applies to service concession arrangements entered into with a public sector grantor when the arrangement meets both of these conditions:

- The grantor controls or has the ability to modify or approve the services that the operating entity must provide with the infrastructure, to whom it must provide them, and at what price.

- The grantor controls, through ownership, beneficial entitlement, or otherwise, any residual interest in the infrastructure at the end of the term of the arrangement.

Under ASU 2014-05, arrangements that meet these conditions should not be accounted for by the operator as leases. While public sector entities generally enter into service concession arrangements with for-profit entities, it is possible that they could also do so with not-for-profit organizations.

Accounting for Leases—Lessee

As discussed in the preceding section, there are two classifications that apply to a lease transaction on the books of the lessee. They are as follows:

- Operating;

- Capital.

Operating leases. The accounting treatment accorded an operating lease is relatively simple; the rental payment shall be charged to expense as the payments are made or become payable. This assumes that the lease payments are being made on a straight-line basis (i.e., an equal payment per period over the lease term). If the lease agreement calls for either an alternative payment schedule or a scheduled rent increase over the lease term, the lease expense should still be recognized on a straight-line basis unless another systematic and rational basis is a better representation of the actual physical usage of the leased property. In such an instance it will be necessary to create either a prepaid asset or a liability, depending on the structure of the payment schedule. Additionally, if the lease agreement provides for a scheduled increase(s) in contemplation of the lessee's increased physical use of the leased property, the total amount of rental payments, including the scheduled increase(s) shall be charged to expense over the lease term on a straight-line basis. However, if the scheduled increase(s) is due to additional leased property, recognition should be proportional to the leased property with the increased rents recognized over the years that the lessee has control over the use of the additional leased property.

Notice that in the case of an operating lease there is no balance sheet recognition of the leased asset because the substance of the lease is merely that of a rental. There is no reason to expect that the lessee will derive any future economic benefit from the leased asset beyond the lease term.

Capital leases. The classification of a lease as operating or capital must be determined prior to the consideration of the accounting treatment. Therefore, it is necessary to first examine the lease transaction against the four criteria (transfer of title, bargain purchase option, 75% of useful life, or 90% of net FMV). Assuming that the lease agreement satisfies at least one of these criteria, it must be accounted for as a capital lease.

According to FASB ASC 840-30-30-3, the lessee shall record a capital lease as an asset and an obligation (liability) at an amount equal to the present value of the minimum lease payments at the beginning of the lease term. The asset should be recorded at the lower of the present value of the minimum lease payments or the fair market value of the asset. When the fair value of the leased asset is less than the present value of the minimum lease payments, the interest rate used to amortize the lease obligation will differ from the interest rate used in the 90% test as determined by the lessor. The interest rate used in the amortization will be the same as that used in the 90% test when the fair market value is greater than or equal to the present value of the minimum lease payments.

For purposes of this computation, the minimum lease payments are considered to be the payments that the lessee is obligated to make or can be required to make, excluding executory costs such as insurance, maintenance, and taxes. The minimum lease payments generally include the minimum rental payments, any guarantee of the residual value made by the lessee, and the penalty for failure to renew the lease, if applicable. If the lease includes a bargain purchase option (BPO), the amount required to be paid under the BPO is also included in the minimum lease payments.

The present value shall be computed using the incremental borrowing rate of the lessee unless it is practicable for the lessee to determine the implicit rate computed by the lessor, and the implicit rate is less than the incremental borrowing rate.

The lease term used in this present value computation is the fixed, noncancelable term of the lease plus the following:

- All periods covered by bargain renewal options;

- All periods for which failure to renew imposes a penalty on the lessee;

- All periods covered by ordinary renewal options during which the lessee guarantees the lessor's debt on the leased property;

- All periods covered by ordinary renewals or extension up to the date a BPO is exercisable;

- All periods representing renewals or extensions of the lease at the lessor's option.

If the amount computed as the present value of the minimum lease payments exceeds the fair value of the leased property at the inception of the lease, the amount recorded should be that of the fair value of the leased property.

The amortization of the leased asset will depend on how the lease qualified as a capital lease. If the lease transaction met the criteria as either transferring ownership or containing a bargain purchase option, then the asset arising from the transaction is to be amortized over the estimated useful life of the leased property. If the transaction qualifies as a capital lease because it meets either the 75% of useful life or 90% of FMV criteria, the asset must be amortized over the lease term. The conceptual rationale for this differentiated treatment arises because of the substance of the transaction. Under the first two criteria, the asset actually becomes the property of the lessee at the end of the lease term (or upon exercise of the bargain purchase option). In the latter situation, the title to the property remains with the lessor.

The leased asset is to be amortized (depreciated) over the lease term if title does not transfer to the lessee, while the asset is depreciated in a manner consistent with the lessee's normal depreciation policy if the title is to eventually transfer to the lessee. This latter situation can be interpreted to mean that the asset is depreciated over the useful economic life of the leased asset. The treatment and method used to amortize (depreciate) the leased asset are very similar to those used for any other asset. The amortization entry requires a debit to the lease expense and a credit to an accumulated amortization account. The leased asset shall not be amortized below the estimated residual value.

In some instances when the property is to revert back to the lessor, there may be a guaranteed residual value. This is an amount that the lessee guarantees to the lessor. If the FMV of the asset at the end of the lease term is greater than or equal to the guaranteed residual amount, the lessee incurs no additional obligation. On the other hand, if the FMV of the leased asset is less than the guaranteed residual value, then the lessee must make up the difference, usually with a cash payment. The guaranteed residual value is often used as a tool to reduce the periodic payments by substituting the lump-sum amount at the end of the term that results from the guarantee. In any event, the amortization must still take place based on the estimated residual value. This results in a rational and systematic allocation of the expense through the periods and avoids a large loss (or expense) in the last period as a result of the guarantee.

The annual (periodic) rent payments made during the lease term are to be allocated between a reduction in the obligation and interest expense in a manner such that the interest expense represents a constant periodic rate of interest on the remaining balance of the lease obligation. This is commonly referred to as the effective interest method.

The following examples illustrate the treatment described in the foregoing paragraphs

- The lease is initiated on 1/1/20X1 for equipment with an expected useful life of three years. The equipment reverts back to the lessor upon expiration of the lease agreement.

- The FMV of the equipment is $135,000.

- Three payments are due to the lessor in the amount of $50,000 per year beginning 12/31/20X1. An additional sum of $1,000 is to be paid annually by the lessee for insurance.

- The lessee guarantees a $10,000 residual value on 12/31/20X3 to the lessor.

- Irrespective of the $10,000 residual value guarantee, the leased asset is expected to have only a $1,000 salvage value on 12/31/20X3.

- The lessee's incremental borrowing rate is 10%. (Lessor's implicit rate is unknown.)

- The present value of the lease obligation is as follows:

PV of guaranteed residual value = $10,000 × 0.75131 = $ 7,513 PV of annual payments = $50,000 × 2.48692 = 124,345 $131,858 * The present value of an amount of $1 due in three periods at 10% is .7513.

** The present value of an ordinary annuity of $1 for three periods at 10% is 2.4869.

The first step in accounting for a lease transaction is to classify the lease. In this case, the lease term is for three years, which is equal to 100% of the expected useful life of the asset. Notice that the 90% test is also fulfilled as the PV of the minimum lease payments ($131,858) is greater than 90% of the FMV ($121,500). Thus, the lease is accounted for as a capital lease.

In number 7 (above) the present value of the lease obligation is computed. Note that the executory costs (insurance) are not included in the minimum lease payments and that the incremental borrowing rate of the lessee was used to determine the present value. This rate was used because the implicit rate was not determinable.

The entry necessary to record the lease on 1/1/20X1 is:

| Leased equipment | 131,858 | |

|

131,858 |

Note that the lease is recorded at the present value of the minimum lease payments, which, in this case, is less than the FMV. If the present value of the minimum lease payments had exceeded the FMV, the lease would be recorded at FMV.

The next step is to determine the proper allocation between interest and a reduction in the lease obligation for each lease payment. This is done using the effective interest method as illustrated below.

| Year | Cash payment | Interest expense | Reduction in lease obligation | Balance of lease obligation |

| Inception of lease | $131,858 | |||

| 1 | $50,000 | 13,186 | $36,814 | $95,044 |

| 2 | 50,000 | 9,504 | 40,496 | 54,548 |

| 3 | 50,000 | 5,452 | 44,548 | 10,000 |

The interest is calculated at 10% (the incremental borrowing rate) of the balance of the lease obligation for each period, and the remainder of the $50,000 payment is allocated to a reduction in the lease obligation. The lessee is also required to pay $1,000 for insurance on an annual basis. The entries necessary to record all payments relative to the lease for each of the three years are shown below.

| 12/31/20X3 | 12/31/20X3 | 12/31/20X3 | |

| Insurance expense | $ 1,000 | $ 1,000 | $ 1,000 |

| Interest expense | 13,186 | 9,504 | 5,452 |

| Lease obligation | 36,814 | 40,496 | 44,548 |

| Cash | 51,000 | 51,000 | 51,000 |

The lease equipment recorded as an asset must also be amortized (depreciated). The balance of this account is $131,858; however, as with any other asset, it cannot be depreciated below the estimated residual value of $1,000 (note that it is depreciated down to the actual estimated residual value, not the guaranteed residual value). In this case, the straight-line depreciation method is applied over a period of three years. This three-year period represents the lease term, not the life of the asset, because the asset reverts back to the lessor at the end of the lease term. Therefore, the following entry will be made at the end of each year:

| Depreciation expense | 43,619 |

|

43,619 [($131,858 – 1,000) ÷ 3] |

Finally, on 12/31/20X3, we must recognize the fact that ownership of the property has reverted back to the owner (lessor). The lessee made a guarantee that the residual value would be $10,000 on 12/31/20X3; as a result, the lessee must make up the difference between the guaranteed residual value and the actual residual value with a cash payment to the lessor. The following entry illustrates the removal of the leased asset and obligation from the books of the lessee:

| Lease obligation | 10,000 | |

| Accumulated depreciation | 130,858 | |

|

9,000 | |

|

131,858 |

The foregoing example illustrated a situation where the asset was to be returned to the lessor. Another situation exists (under bargain purchase option or transfer of title) where the asset is expected to remain with the lessee. Remember that leased assets are amortized over their useful life when title transfers or a bargain purchase option exists. At the end of the lease, the balance of the lease obligation should equal the guaranteed residual value, the bargain purchase option price, or a termination penalty.

- A three-year lease is initiated on 1/1/20X1 for equipment with an expected useful life of five years.

- Three annual lease payments of $52,000 are required beginning on 1/1/20X1 (note that the payment at the beginning of the year changes the present value computation). The lessor pays $2,000 per year for insurance on the equipment.

- The lessee can exercise a bargain purchase option on 12/31/20X3 for $10,000. The expected residual value at 12/31/20X4 is $1,000.

- The lessee's incremental borrowing rate is 10% (lessor's implicit rate is unknown).

- The fair market value of the property leased is $140,000.

Once again, the classification of the lease must take place prior to the accounting for it. This lease is classified as a capital lease because it contains a bargain purchase option. In this case, the 90% test is also fulfilled.

The present value of the lease obligation is computed as follows:

| Present value of bargain purchase option | = $10,000 × 0.75133* = $ 7,513 |

| Present value of annual payments | = ($52,000 − $2,000)** × 2.73554 = 136,775 |

| $144,288 |

* 0.7513 is the PV of an amount due in three periods at 10%.

** 2.7355 is the PV of an annuity due for three periods at 10%.

Notice that the present value of the lease obligation is greater than the FMV of the asset. Since the lessor pays $2,000 a year for insurance, this payment is treated as executory costs and excluded from the calculation of the present value of annual payments. Because of this, the lease obligation must be recorded at the FMV of the asset leased.

| 1/1/20X1 Leased equipment | 140,000 | |

|

140,000 |

The allocation between interest and principal is to be such that interest recognized reflects the use of a constant periodic rate of interest applied to the remaining balance of the obligation. If the FMV of the leased asset is greater than or equal to the present value of the lease obligation, the interest rate used would be the same as that used to compute the present value (i.e., the incremental borrowing rate or the implicit rate). In cases such as this when the present value exceeds the FMV of the leased asset, a new rate must be computed through a series of trial and error calculations. In this situation the interest rate used was 13.265%. The amortization of the lease takes place as follows:

| Date | Cash payment | Interest expense | Reduction in lease obligation | Balance of lease obligation |

| Inception of lease | $140,000 | |||

| 1/1/20X1 | $50,000 | $ -- | $50,000 | 90,000 |

| 1/1/20X2 | 50,000 | 11,939 | 38,061 | 51,939 |

| 1/1/20X3 | 50,000 | 6,890 | 43,110 | 8,829 |

| 12/31/20X3 | 10,000 | 1,171 | 8,829 | -- |

The following entries are required in years 20X1 through 20X3 to recognize the payment and amortization.

| 20X1 | 20X2 | 20X3 | |||||

| 1/1 | Operating expense | 2,000 | 2,000 | 2,000 | |||

| Obligation under capital lease | 50,000 | 38,061 | 43,110 | ||||

| Accrued interest payable | 11,939 | 6,890 | |||||

| Cash | 52,000 | 52,000 | 52,000 | ||||

| 12/31 | Interest expense | 11,939 | 6,890 | 1,171 | |||

| Accrued interest payable | 11,939 | 6,890 | |||||

| Obligation under capital lease | 1,171 | ||||||

| 20X1 | 20X2 | 20X3 | |||||

| 12/31 | Depreciation expense | 27,800 | 27,800 | 27,800 | |||

| Accumulated depreciation | 27,800 | 27,800 | 27,800 | ||||

| ($139,000 ÷ five years) | |||||||

| 12/31 | Obligation under capital lease | 10,000 | |||||

| Cash | 10,000 | ||||||

Accounting for Leases—Lessor

As illustrated above, there are four classifications of leases with which a lessor must be concerned. They are as follows:

- Operating;

- Sales-type;

- Direct financing;

- Leveraged.

Operating lease. As in the case of the lessee, the operating lease requires a less complex accounting treatment on the part of the lessor. The payments received by the lessor are to be recorded as rent revenues in the period in which the payment is received or becomes receivable. As with the lessee, if either the rentals vary from a straight-line basis or the lease agreement contains a scheduled rent increase over the lease term, the revenue is to be recorded on a straight-line basis unless an alternative basis of systematic and rational allocation is more representative of the time pattern of physical usage of the leased property. Additionally, if the lease agreement provides for a scheduled increase(s) in contemplation of the lessee's increased physical use of the leased property, the total amount of rental payments including the scheduled increase(s) shall be allocated to revenue over the lease term on a straight-line basis. However, if the scheduled increase(s) is due to additional leased property, recognition should be proportional to the leased property with the increased rents recognized over the years that the lessee has control over the use of the additional leased property.

The lessor shall show the leased property on the statement of position under the caption “Investment in leased property.” This account should be shown with or near the fixed assets of the lessor, and depreciated in the same manner as the rest of the lessor's fixed assets.

Any initial direct leasing costs are to be amortized over the lease term as the revenue is recognized (i.e., on a straight-line basis unless another method is more representative). However, these costs may be charged to expense as they are incurred if the effect is not materially different from what would have occurred if the above method had not been used.

Any incentives made by the lessor to the lessee are to be treated as reductions of rent and recognized on a straight-line basis over the term of the lease.

If, at the inception of the lease, the fair value of the property in an operating lease involving real estate that would have been classified as a sales-type lease, except that it did not transfer title, is less than its carrying amount, then the lessor must recognize a loss equal to that difference at the inception of the lease.

Sales-type lease. In the accounting for a sales-type lease, it is necessary for the lessor to determine the following amounts:

- Gross investment;

- Fair value of the leased asset;

- Cost.

From these amounts, the remainder of the computations necessary to record and account for the lease transaction can be made. The first objective is to determine the numbers necessary to complete the following entry:

| Lease receivable | xx | |

| Cost of goods sold | xx | |

| Sales | xx | |

| Inventory | xx | |

| Unearned interest | xx |

The gross investment (lease receivable) of the lessor is equal to the sum of the minimum lease payments (excluding executory costs) plus the unguaranteed residual value. The difference between the gross investment and the present value of the two components of gross investment (minimum lease payments and unguaranteed residual value) is recorded as the unearned interest revenue. The present value is to be computed using the lease term and implicit interest rate (both of which were discussed earlier). The resulting unearned interest revenue is to be amortized into income using the effective interest method. This will result in a constant periodic rate of return on the net investment (the net investment is the gross investment less the unearned income).

Recall from our earlier discussion that the fair market value (FMV) of the leased property is, by definition, equal to the normal selling price of the asset adjusted by any residual amount retained (this amount retained can be exemplified by an unguaranteed residual value, investment credit, etc.). The adjusted selling price to be used for a sales-type lease is equal to the present value of the minimum lease payments. Thus, we can say that the normal selling price less the residual amount retained is equal to the PV of the minimum lease payments.

The cost of goods sold to be charged against income in the period of the sale is computed as the historic cost or carrying value of the asset (most likely inventory), plus any initial direct costs, less the present value of the unguaranteed residual value. The difference between the adjusted selling price and the amount computed as the cost of goods sold is the gross profit recognized by the lessor on the inception of the lease (sale). Thus, a sales-type lease generates two types of revenue for the lessor:

- The gross profit on the sale;

- The interest earned on the lease receivable.

It should be noted that if the sales-type lease involves real estate, the lessor must account for the transaction under the provisions of FASB ASC 360-20 in the same manner as a seller of the same property.

Direct financing lease. The accounting for a direct financing lease holds many similarities to that for a sales-type lease. Of particular importance is that the terminology used is much the same; however, the treatment accorded these items varies greatly. Again, it is best to preface our discussion by determining our objectives in the accounting for a direct financing lease. Once the lease has been classified, it must be recorded. In order to do this, the following numbers must be obtained:

- Gross investment;

- Cost;

- Residual value.

As mentioned earlier, a direct financing lease generally involves a leasing company or other financial institution and results in only interest revenue being earned by the lessor. This is because the FMV (selling price) and the cost are equal and, therefore, no profit is recognized on the actual lease transaction. Note how this is different from a sales-type lease that involves both a profit on the transaction and interest revenue over the lease term. The reason for this difference is derived from the conceptual nature underlying the purpose of the lease transaction. In a sales-type lease, the manufacturer (distributor, dealer) is seeking an alternative means to finance the sale of its product, whereas a direct financing lease is a result of the consumer's need to finance an equipment purchase. Because the consumer is unable to obtain conventional financing, the consumer turns to a leasing company that will purchase the desired asset and then lease it to the consumer. Here the profit on the transaction remains with the manufacturer while the interest revenue is earned by the leasing company. A not-for-profit organization may acquire assets that it in turn leases to other not-for-profit organizations. This type of transaction may be one that would meet the criteria for accounting as a direct financing lease.

Like a sales-type lease, the first objective is to determine the amounts necessary to complete the following entry:

| Lease receivable | xxx | ||

| Asset | xxx | ||

| Unearned interest | xx |

The gross investment is still defined as the minimum amount of lease payments exclusive of any executory costs plus the unguaranteed residual value. The difference between the gross investment as determined above and the cost (carrying value) of the asset is to be recorded as the unearned interest revenue because there is no manufacturer's/dealer's profit earned on the transaction. The following entry would be made to record initial direct costs:

| Initial direct costs | xx | |

| Cash | xx |

Net investment in the lease is defined as the gross investment less the unearned income plus the unamortized initial direct costs related to the lease. Initial direct costs are defined in the same way that they were for purposes of the sales-type lease; however, the accounting treatment is different. For a direct financing lease, the unearned lease (interest) income and the initial direct costs are to be amortized to income over the lease term so that a constant periodic rate is earned on the net investment. Thus, the effect of the initial direct costs is to reduce the implicit interest rate, or yield, to the lessor over the life of the lease.

An example follows that illustrates the preceding principles.

The Healthcare Research Center needs a new piece of equipment to expand its research and development activities; however, it does not have sufficient funds provided in its budget to purchase the asset at this time. Because of this, the center has employed ABC Leasing to purchase the asset. In turn, the center will lease the asset from ABC. The following information applies to the terms of the lease:

Lease information

- A three-year lease is initiated on 1/1/20X1 for equipment costing $131,858 with an expected useful life of five years. The FMV of the equipment at 1/1/20X1 is $131,858.

- Three annual payments are due to the lessor beginning 12/31/20X1. The property reverts back to ABC Leasing (the lessor) upon termination of the lease.

- The unguaranteed residual value at the end of year 3 is estimated to be $10,000.

- The annual payments are calculated to give the lessor a 10% return (implicit rate).

- The lease payments and unguaranteed residual value have a present value equal to $131,858 (FMV of asset) at the stipulated discount rate.

- The annual payment to the lessor is computed as follows:

Present value of residual value = $10,000 × 0.75135* = $7,513 Present value of lease payments = Selling price – Present value of residual value = $131,858 − 7,513 = $124,345, Annual payment = $124,345 = $124,345 = 50,000 PV3,10% 2.4869 * 0.75135 is the PV of an amount due in three periods at 10%.

- Initial direct costs of $7,500 are incurred by ABC Leasing in the lease transaction.

The center would record the lease as a lessee records a capital lease (described earlier in this chapter). The following describes the calculation and accounting entries that would be made by ABC Leasing.

As with any lease transaction, the first step must be to appropriately classify the lease. In this case, the present value of the lease payments ($124,345) exceeds 90% of the FMV (90% × $131,858). Assume that the lease payments are reasonably assured and that there are no uncertainties surrounding the costs yet to be incurred by the lessor.

Next, determine the unearned interest and the net investment in the lease.

Gross investment in lease [(3 × $50,000) + $10,000] $160,000 Cost of leased property 131,858 Unearned interest $ 28,142 The unamortized initial direct costs are to be added to the gross investment in the lease and the unearned interest income is to be deducted to arrive at the net investment in the lease. The net investment in the lease for this example is determined as follows:

Gross investment in lease $160,000 Add: Unamortized initial direct costs 7,500 $167,500 Less: Unearned interest income 28,142 Net investment in lease $139,358 The net investment in the lease (Gross investment – Unearned revenue) has been increased by the amount of initial direct costs. Therefore, the implicit rate is no longer 10%, and must be recomputed. The implicit rate is really the result of an internal rate of return calculation. We know that the lease payments are to be $50,000 per annum and that a residual value of $10,000 is available at the end of the lease term. In return for these payments (inflows), we are giving up equipment (outflow) and incurring initial direct costs (outflows) with a net investment of $139,358 ($131,858 + $7,500). The only way to obtain the new implicit rate is through a trial and error calculation as set up below.

Where i = implicit rate of interest

In this case, the implicit rate is equal to 7.008%.

Thus, the amortization table would be set up as follows:

(a)

Lease payments(b)

Reduction in unearned interest(c)

PV × implicit rate (7.008%)(d)

Reduction in initial direct costs (b−c)(e)

Reduction in PVI net invest. (a−b + d)(f)

PVI net invest. in lease (f)(n+1) = (f)n – (e)0 $139,358 1 $ 50,000 $13,186 (1) $ 9,766 $3,420 $ 40,234 99,124 2 50,000 9,504 (2) 6,947 2,557 43,053 56,071 3 50,000 5,455 (3) 3,929 1,526 46,071 10,000 $150,000 $28,145* $20,642 $7,503 $129,358 * Rounded

(b.1) $131,858 × 10% = $13,186 (b.2) [$131,858 − ($50,000 − 13,186)] × 10% = $9,504 (b.3) [$ 95,044 − ($50,000 − 9,504)] × 10% = $5,455 Here the interest is computed as 7.008% of the net investment. Note again that the net investment at the end of the lease term is equal to the estimated residual value.

The entry made by ABC Leasing to initially record the lease is as follows:

Lease receivable* [($50,000 × 3) + 10,000] 160,000

- Asset acquired for leasing

131,858

- Unearned lease revenue

28,142 When the payment (or obligation to pay) of the initial direct costs occurs, the following entry must be made:

Initial direct costs 7,500

- Cash

7,500 Using the schedule on the previous page, the following entries would be made during each of the indicated years:

Cash 50,000 50,000 50,000 Lease receivable* 50,000 50,000 50,000 Unearned lease revenue 13,186 9,504 5,455 Initial direct costs 3,420 2,557 1,526 Interest revenue 9,766 6,947 3,929 Finally, when the asset is returned to the lessor at the end of the lease term, it must be recorded on the books. The necessary entry is as follows:

Used asset 10,000 Lease receivable* 10,000 * Also the “gross investment in lease.”

Leveraged lease. Leveraged leases meet all of the definitional requirement criteria of a direct financing lease, but differ because they involve three parties: a lessee, a long-term creditor, and a lessor (or equity participant). Leveraged leases are not discussed in detail in this chapter because they would be so rarely used by not-for-profit organizations.

Special Situations

The following summarizes some special circumstances that may be encountered by a not-for-profit organization in accounting for leases.

Change in residual value. For any of the foregoing types of leases, the lessor is to review the estimated residual value on at least an annual basis. If there is a decline in the estimated residual value, the lessor must make a determination as to whether this decline is temporary or permanent. If temporary, no adjustment is required; however, if the decline is other than temporary, then the estimated residual value must be revised in line with the changed estimate. The loss that arises in the net investment is to be recognized in the period of decline. Under no circumstance is the estimated residual value to be adjusted to reflect an increase in the estimate.

Change in the provisions of a lease. In the case of either a sales-type or direct financing lease where there is a change in the provisions of a lease, the lease shall be accounted for (by the lessor) as discussed below.

The financial statements preparer is basically concerned with changes in the provisions of a lease that affect the amount of the remaining minimum lease payments. When a change such as this occurs, one of the following three things can happen:

- The change does not give rise to a new agreement. A new agreement is defined as a change that, if in effect at the inception of the lease, would have resulted in a different classification.

- The change does give rise to a new agreement that would be classified as a direct financing lease.

- The change gives rise to a new agreement classified as an operating lease.

If either 1. or 2. occurs, the balance of the minimum lease payments receivable and the estimated residual value (if affected) shall be adjusted to reflect the effect of the change. The net adjustment is to be charged (or credited) to the unearned income account, and the accounting for the lease adjusted to reflect the change.

If the new agreement is an operating lease, then the remaining net investment (lease receivable less unearned income) is to be removed from the books and the leased asset shall be recorded at the lower of its cost, present fair value, or carrying value. The net adjustment resulting from these entries shall be charged (or credited) to the income of the period. Thereafter, the new lease shall be accounted for as any other operating lease.

Termination of a lease. The lessor shall remove the remaining net investment from his/her books and record the leased equipment as an asset at the lower of its original cost, present fair value, or current carrying value. The net adjustment shall be reflected in the income of the current period.

The lessee is also affected by the terminated agreement because s/he has been relieved of the obligation. If the lease is a capital lease, then the lessee should remove both the obligation and the asset from his/her accounts and charge any adjustment to the current period income. If accounted for as an operating lease, there is no accounting adjustment required.

Renewal or extension of an existing lease. The renewal or extension of an existing lease agreement affects the accounting of both the lessee and the lessor. FASB ASC 840 specifies two basic situations in this regard: (1) the renewal occurs and makes a residual guarantee or penalty provision inoperative, or (2) the renewal agreement does not do the foregoing and the renewal is to be treated as a new agreement. The accounting treatment prescribed under the latter situation for a lessee is as follows:

- If the renewal or extension is classified as a capital lease, then the (present) current balances of the asset and related obligation should be adjusted by an amount equal to the difference between the present value of the future minimum lease payments under the revised agreement and the (present) current balance of the obligation. The present value of the minimum lease payments under the revised agreement should be computed using the interest rate that was in effect at the inception of the original lease.

- If the renewal or extension is classified as an operating lease, then the current balances in the asset and liability accounts shall be removed from the books and a gain (loss) recognized for the difference. The new lease agreement resulting from a renewal or extension shall be accounted for in the same manner as other operating leases.

Under the same circumstances, FASB ASC 840 prescribes the following treatment to be followed by the lessor:

- If the renewal or extension is classified as a direct financing lease, then the existing balances of the lease receivable and the estimated residual value accounts should be adjusted for the changes resulting from the revised agreement. The net adjustment should be charged or credited to an unearned income account.

- If the renewal or extension is classified as an operating lease, then the remaining net investment under the existing sales-type lease or direct financing lease shall be removed from the books and the leased asset shall be recorded as an asset at the lower of its original cost, present fair value, or current carrying amount. The difference between the net investment and the amount recorded for the leased asset shall be charged to income of the period. The renewal or extension should then be accounted for as any other operating lease.

- If the renewal or extension is classified as a sales-type lease and it occurs at or near the end of the existing lease term, then the renewal or extension should be accounted for as a sales-type lease.

If the renewal or extension causes the guarantee or penalty provision to be inoperative, the lessee shall adjust the current balance of the leased asset and the lease obligation to the present value of the future minimum lease payments by an amount equal to the difference between the PV of future minimum lease payments under the revised agreement and the present balance of the obligation. The PV of the future minimum lease payments shall be computed using the implicit rate used in the original lease agreement.

Given the same circumstances, the lessor shall adjust the existing balance of the lease receivable and estimated residual value accounts to reflect the changes of the revised agreement (remember, no upward adjustments to the residual value). The net adjustment shall be charged (or credited) to unearned income.

Leases between related parties. Leases between related parties shall be classified and accounted for as though the parties are unrelated, except in cases where it is certain that the terms and conditions of the agreement have been influenced significantly by the fact that the lessor and lessee are related. When this is the case, the classification and/or accounting shall be modified to reflect the true economic substance of the transaction rather than the legal form.

If a subsidiary's principal business activity is leasing property to its parent or other affiliated companies, consolidated financial statements shall be presented.

FASB ASC 850 requires that the nature and extent of leasing activities between related parties be disclosed.

Accounting for leases in a business combination. A business combination, in and of itself, has no effect upon the classification of a lease. However, if, in connection with a business combination, the lease agreement is modified to change the original classification of the lease, it should be considered a new agreement and reclassified according to the revised provisions.

In most cases, a business combination that is accounted for by the pooling-of-interests method or by the purchase method will not affect the previous classification of a lease unless the provisions have been modified as indicated in the preceding paragraph.

The acquiring company shall apply the following procedures to account for a leveraged lease in a business combination accounted for by the purchase method:

- The classification of leveraged lease should be kept.

- The net investment in the leveraged lease should be given a fair market value (present value, net of tax) based on the remaining future cash flows. Also, the estimated tax effects of the cash flows should be given recognition.

- The net investment shall then be broken down into three components: net rentals receivable, estimated residual value, and unearned income.

- Thereafter, the leveraged lease should be accounted for as described above in the section on leveraged leases.

Accounting for changes in lease agreements resulting from refunding of tax-exempt debt. If, during the lease term, a change in the lease results from a refunding by the lessor of tax-exempt debt (including an advance refunding) and (1) the lessee receives the economic advantages of the refunding, and (2) the revised agreement can be classified as a capital lease by the lessee and a direct financing lease by the lessor, the change should be accounted for as follows:

- If the change is accounted for as an extinguishment of debt:

- Lessee accounting. The lessee should adjust the lease obligation to the present value of the future minimum lease payments under the revised agreement. The present value of the minimum lease payments should be computed by using the interest rate applicable to the revised agreement. Any gain or loss should be recognized currently as a gain or loss on the extinguishment of debt.

- Lessor accounting. The lessor should adjust the balance of the lease receivable and the estimated residual value, if affected, for the difference in present values between the old and revised agreements. Any resulting gain or loss should be recognized currently.

- If the change is not accounted for as an extinguishment of debt:

- Lessee accounting. The lessee should accrue any costs in connection with the debt refunding that is obligated to be refunded to the lessor. These costs should be amortized by the interest method over the period from the date of refunding to the call date of the debt to be refunded.

- Lessor accounting. The lessor should recognize any reimbursements to be received from the lessee, for costs paid in relation to the debt refunding, as revenue. This revenue should be recognized in a systematic manner over the period from the date of refunding to the call date of the debt to be refunded.

Sale or assignment to third parties; nonrecourse financing. The sale or assignment of a lease or of property subject to a lease that was originally accounted for as a sales-type lease or a direct financing lease will not affect the original accounting treatment of the lease. Any profit or loss on the sale or assignment should be recognized at the time of transaction, except under the following two circumstances:

- When the sale or assignment is between related parties, apply provisions presented above under “related parties.”

- When the sale or assignment is with recourse, it shall be accounted for using the provisions of FASB ASC 860-10.

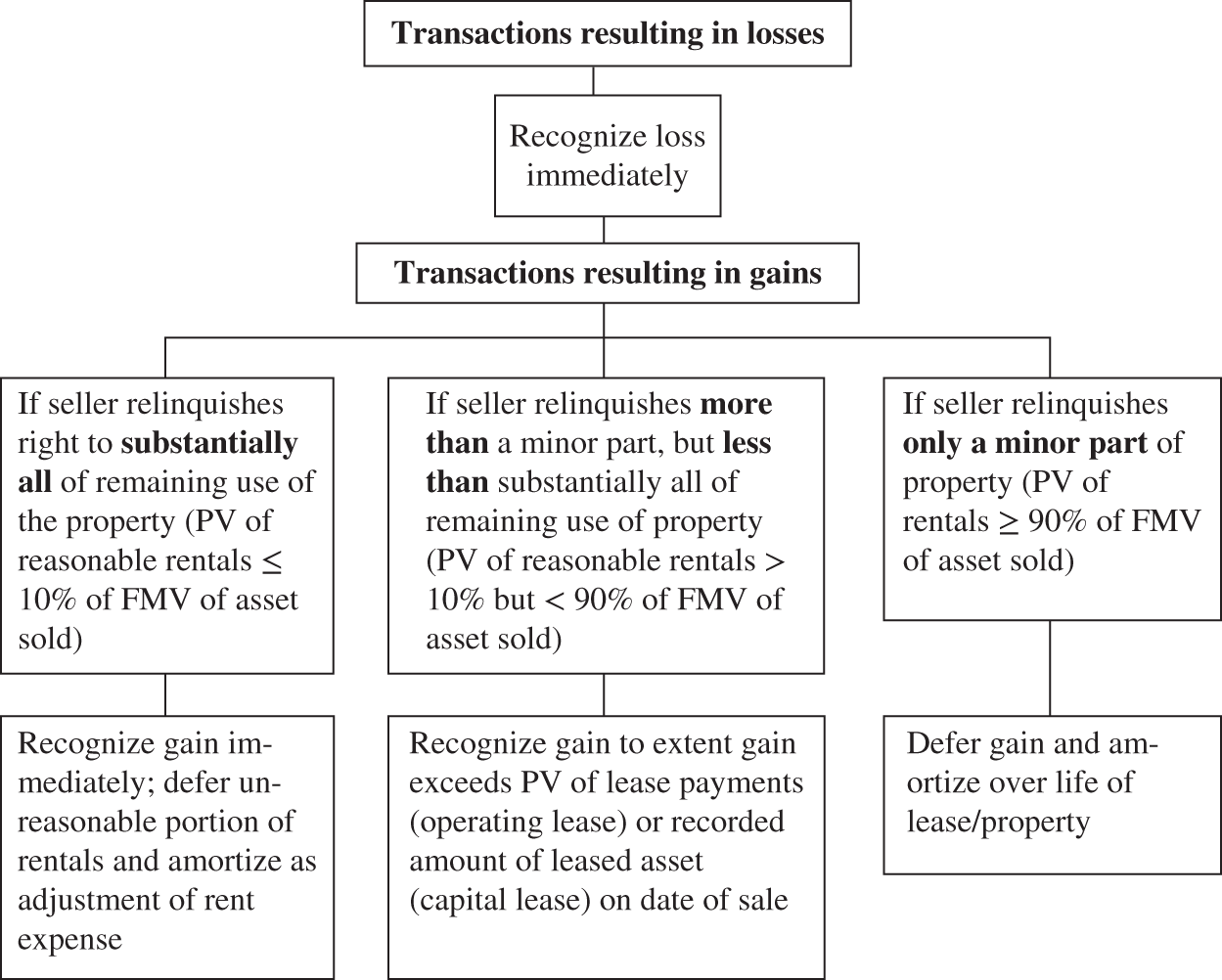

The sale of property subject to an operating lease shall not be treated as a sale if the seller (or any party related to the seller) retains “substantial risks of ownership” in the leased property. A seller may retain “substantial risks of ownership” by various arrangements. For example, if the lessee defaults upon the lease agreement or if the lease terminates, the seller may arrange to do one of the following:

- Acquire the property or the lease.

- Substitute an existing lease.

- Secure a replacement lessee or a buyer for the property under a remarketing agreement.

A seller will not retain substantial risks of ownership by arrangements where one of the following occurs:

- A remarketing agreement includes a reasonable fee to be paid to the seller.

- The seller is not required to give priority to the releasing or disposition of the property owned by the third party over similar property owned by the seller.

When the sale of property subject to an operating lease is not accounted for as a sale because the substantial risk factor is present, it should be accounted for as a borrowing. The proceeds from the sale should be recorded as an obligation on the seller's books. Rental payments made by the lessee under the operating lease should be recorded as revenue by the seller even if the payments are paid to the third-party purchaser. The seller shall account for each rental payment by allocating a portion to interest expense (to be imputed in accordance with the requirements of GAAP), and the remainder will reduce the existing obligation. Other normal accounting procedures for operating leases should be applied, except that the depreciation term for the leased asset is limited to the amortization period of the obligation.

The sale or assignment of lease payments under an operating lease by the lessor should be accounted for as a borrowing as described above.

Nonrecourse financing is a common occurrence in the leasing industry, whereby the stream of lease payments on a lease is discounted on a nonrecourse basis at a financial institution, with the lease payments collateralizing the debt. The proceeds are then used to finance future leasing transactions. Even though the discounting is on a nonrecourse basis, the offsetting of the debt against the related lease receivable is prohibited unless a legal right of offset exists or the lease qualified as a leveraged lease at its inception. The SEC in a recent Staff Accounting Bulletin has also affirmed this position.

Transfers of residual value (FASB ASC 860-10). Recently, there has been an increase in the acquisition of interests in residual values of leased assets by companies whose primary business is other than leasing or financing. This generally occurs through the outright purchase of the right to own the leased asset or the right to receive the proceeds from the sale of a leased asset at the end of its lease term.

In instances such as these, the rights should be recorded by the purchaser at the fair value of the assets surrendered. Recognition of increases in the value of the interest in the residual (i.e., residual value accretion) to the end of the lease term is permitted for guaranteed residual values because they are financial assets. However, recognition of such increases is prohibited for unguaranteed residual values. A nontemporary write-down of a residual value interest (guaranteed/unguaranteed) should be recognized as a loss. This guidance also applies to lessors who sell the related minimum lease payments but retain the interest in the residual value. Guaranteed residual values also have no effect on this guidance.

Accounting for a sublease. A sublease is used to describe the situation where the original lessee re-leases the leased property to a third party (the sublessee), and the original lessee acts as a sublessor. Normally, the nature of a sublease agreement does not affect the original lease agreement, and the original lessee/sublessor retains primary liability.

The original lease remains in effect, and the original lessor continues to account for the lease as before. The original lessee/sublessor shall account for the lease as follows: