Session B

Standard costing

1 Introduction

You know that it is useful to control costs. But how do you know you are controlling the right ones? And by how much should you reduce them, if possible? You can switch lights off and turn down the heating, but your work team are unlikely to work well in the cold and dark.

It helps you to control anything – the output of a machine or a work team, for instance – if there is a standard against which to measure performance.

In cost control, the first step is to decide what the costs should be and then control what happens in such a way that you meet those ‘target’ costs. If actual costs of the operation turn out to be different from the expected figure, then you look at the differences – called variances – and find out why they are different. Then you can decide what action should be taken to bring them back to target.

In this session we will look at different standards and how to use them to control costs.

2 Setting standards

Standard costs are concerned with individual units of production or service. Each item of production or service, for instance, will have a standard cost.

A standard cost is a predetermined cost that is achieved by setting standards related to particular circumstances or conditions of work.

Costs change over time, so standards should be reviewed regularly to ensure that they are still relevant.

A standard cost should indicate not just what a particular cost is expected to be, but also what it ought to be under certain conditions.

You can apply standard costs to all the costs in the workplace. These may include:

![]() direct labour;

direct labour;

![]() direct materials;

direct materials;

![]() overheads (fixed and variable).

overheads (fixed and variable).

A mechanic may, for example, be expected to complete the servicing of a car in an hour and this will involve one hour's direct labour cost plus a direct materials cost for, say, oil filter, lubricants and other replacement parts.

2.1 Standard cost rates

Standard cost rates are estimated by taking all sorts of considerations into account.

Activity 12

a Jot down two things which you would take into account in estimating materials costs for something which will be used extensively in your work-place for the next year.

b Write down two matters you would have to take into account in estimating labour costs for a forthcoming period.

I hope you have thought of taking the following into account in respect of materials costs:

![]() the purchase price;

the purchase price;

![]() any expected change in price (for instance, you might know that the price of oil or floppy disks was going to increase);

any expected change in price (for instance, you might know that the price of oil or floppy disks was going to increase);

![]() any discount you could negotiate.

any discount you could negotiate.

The following factors, among others, would be relevant for labour costs:

![]() the current hourly rate/piece rate;

the current hourly rate/piece rate;

![]() likely agreements on pay rises;

likely agreements on pay rises;

![]() other costs, such as overtime premiums, bonuses, employer's National Insurance contributions, pension contributions.

other costs, such as overtime premiums, bonuses, employer's National Insurance contributions, pension contributions.

Deciding on how much things ought to cost is only one side of the question. The other matter to consider is how many of the things in question should be used for each unit of production or service. In other words, we need to decide how well production will perform.

So now let's look at performance standard rates.

2.2 Standard performance rates

To use a standard costing system, somebody must decide:

![]() the quantities, types and mix of materials to produce any given product;

the quantities, types and mix of materials to produce any given product;

![]() the amount and type of labour to produce any given product or service.

the amount and type of labour to produce any given product or service.

These technical standards are usually set by specialists and involve techniques such as method study and job evaluation.

Two types of standard are commonly used:

![]() ideal standards;

ideal standards;

![]() expected standards.

expected standards.

Ideal standards are based on perfect working conditions. However, conditions are seldom perfect, often for reasons outside our immediate control. Ideal standards can help to highlight major variances, but people tend to find them rather discouraging, because the targets may be too high.

Much better, usually, are expected standards. These could well be called realistic standards, as they build in an allowance for an acceptable level of inefficiency. If the work team is well managed and willing to co-operate, expected standards should be attainable.

Activity 13

This Activity may provide the basis of appropriate evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Identify three causes for breaks in production or delivery of service which are not planned and which your work team has experienced. Suggest changes that you could recommend to your manager to address such situations.

Certain planned breaks are important to allow staff to eat and rest physically and mentally. They are often required by law, say in the case of lorry drivers and users of VDUs. There are, though, breaks that can occur unexpectedly, such as:

![]() when equipment breaks down. A hairdresser may have spare cutting equipment to call upon but if a baker's oven breaks down, replacement may not be possible. A rapid service and repair contract is essential.

when equipment breaks down. A hairdresser may have spare cutting equipment to call upon but if a baker's oven breaks down, replacement may not be possible. A rapid service and repair contract is essential.

![]() where the organization runs out of stock and production ceases. Plans for alternative work so that employees have something to do would avoid unnecessary costs, or alternative stockholding policies could be employed.

where the organization runs out of stock and production ceases. Plans for alternative work so that employees have something to do would avoid unnecessary costs, or alternative stockholding policies could be employed.

![]() when accidents or injuries occur. Good health and safety training and procedures should limit this problem.

when accidents or injuries occur. Good health and safety training and procedures should limit this problem.

2.3 Standard costing and

non-manufacturing organizations

A full standard costing system is less common in organizations that provide a service rather than manufacture something. Many industries, nevertheless, find it useful to set performance standards in order to:

a base costs upon them, and then;

b measure actual performance.

For example, a building contractor might base costs on performance standards for:

![]() cubic metres of earth excavated per hour by a mechanical digger;

cubic metres of earth excavated per hour by a mechanical digger;

![]() lorry loads of earth shifted per day;

lorry loads of earth shifted per day;

![]() bricks laid per hour.

bricks laid per hour.

Activity 14

In an office you may find sales order processing clerks, and administrators sending letters in response to queries at work. Also the manager may spend a lot of time talking to clients in a separate office.

Suggest two possible performance standards which you could set if you were in charge in this situation.

You could set performance standards for:

![]() letters created per hour by an administrator;

letters created per hour by an administrator;

![]() percentage completion of correct invoices by the sales order processing clerks;

percentage completion of correct invoices by the sales order processing clerks;

![]() number of deals by the manager per day.

number of deals by the manager per day.

3 Standard costing in practice

Let's look first at a very simple example.

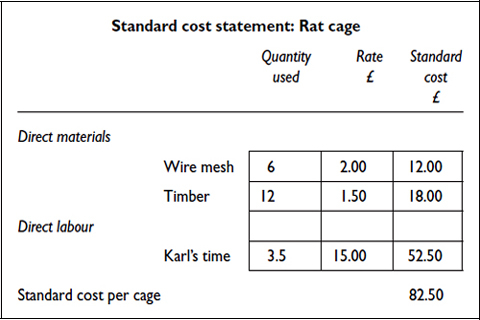

Karl makes large, luxury cages for pet rats. He knows that each cage requires 6 square metres of wire mesh, and 12 metres of timber. It takes him 3.5 hours to make a cage. Wire mesh costs £2 per square metre, and timber costs £1.50 per metre. He pays himself £15 per hour. What is the standard cost for each cage?

We can calculate this by drawing up a standard cost statement. Make sure you can trace every item in the figure below to the information above, and that you can follow through the calculations.

Once you are happy that you understand the way in which this standard cost statement is constructed, you can put standard costing into operation in the following Activity.

Activity 15

Plastiform plc makes a range of plastic furniture. A standard costing system is in operation. The following information is available for one product – plastic tables.

The raw material (plastic) has been costed at £6.10 per metre. The standard usage of material is reckoned to be 5 metres per table.

Two types of labour are required in the production process: moulders and cutters.

![]() The standard rate for moulders is £8.00 per hour.

The standard rate for moulders is £8.00 per hour.

![]() The standard rate for cutters is £10.00 per hour.

The standard rate for cutters is £10.00 per hour.

![]() The expected standard for moulders is 1½ hours per table.

The expected standard for moulders is 1½ hours per table.

![]() The expected standard for cutters is 2½ hours per table.

The expected standard for cutters is 2½ hours per table.

Complete the standard cost statement below to show what the standard cost will be for a table.

Standard cost statement: plastic table

| Direct materials: 5 metres at £6.10 | = £ _________ |

| Direct wages: | |

| Moulder____________hours×£____________ | = £6.00 |

| Cutter ____________hours×£____________ | = ___________ |

| ___________ |

The answer to this Activity can be found on page 124.

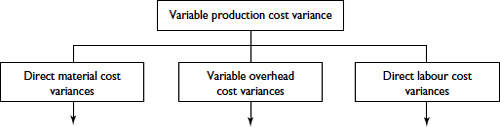

The system an organization uses to analyse and ultimately to control its costs can be as simple or as complicated as the organization wishes. Karl and Plastiform plc produce standard cost statements just for direct materials and labour. What about overheads?

We saw in Session A that an organization can classify its costs in various ways, in particular in relation to:

![]() which costs are treated as direct costs and which as indirect;

which costs are treated as direct costs and which as indirect;

![]() which costs are treated as what type of overhead.

which costs are treated as what type of overhead.

This is important, since a standard costing system can identify a certain amount of overhead to each unit of production or service if the organization sees fit, as well as direct materials and labour.

Activity 16

Karl has also worked out that, for each hour he works on the rat cages, he incurs rent, rates, heating and insurance costs of £3. Remember he works for three and a half hours on each cage. By how much will the standard cost per cage rise if he takes overheads into account?

I hope you calculated that the standard cost will rise by £3.50 × 3 = £10.50 so the total standard cost will be £93.00.

Now let's see how differences between actual costs and standard costs (variances) can be calculated and analysed.

4 Variances from standard

Variances are the differences between what costs actually are and what they should be – the standard.

A variance can be either adverse (when the actual cost is higher than the standard) or favourable (when the cost is actually lower than the standard).

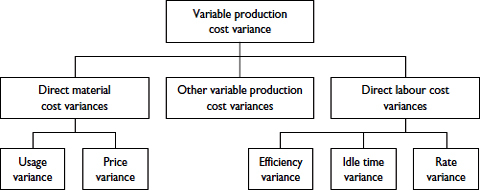

With a basic standard costing system, variances can be highlighted for:

![]() every material used;

every material used;

![]() every type of direct labour;

every type of direct labour;

![]() variable overheads (such as workshop heat and light).

variable overheads (such as workshop heat and light).

Clearly, this detailed information is very important to managers who wish to control work. Notice that we are only looking here at the costs that fluctuate with levels of activity. These are the ones that are most likely to be controllable by first line managers.

The following diagram shows how an analysis of these work variances breaks down.

We shall use an analysis of materials and labour costs to illustrate that standard costing can help pinpoint variances and so improve control.

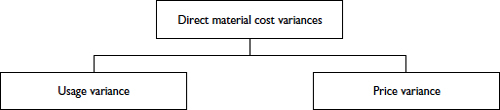

4.1 Direct material cost variances

Direct material cost variances can be divided into two types:

![]() usage variance;

usage variance;

![]() price variance.

price variance.

Don't worry about the terminology too much. We have already seen the usage rate when we said that Karl uses 12 metres of timber. The price rate was £1.50 per metre.

If an adverse usage variance occurs, it means that more material has been used than the standard indicated. This might have come about because inefficient methods meant that more scrap than expected was produced.

Activity 17

A decision to improve a price variance by using cheaper materials can lead to more scrap and a worsening usage variance. The consequence of changes made in response to variances need careful consideration.

Who do you think is ultimately responsible for a usage variance?

Who do you think is directly responsible for excessive scrap being produced?

Ultimately, the production controller, or similarly named person, is responsible for a variance from standard usage. However, the first line manager is likely to have to account directly for scrap being higher than expected.

Now let's look at the direct labour cost variance.

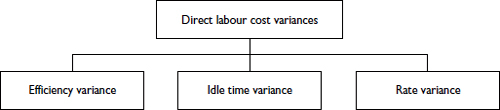

4.2 Direct labour cost variances

Direct labour cost variances break down to:

![]() efficiency variance;

efficiency variance;

![]() idle time variance;

idle time variance;

![]() rate variance.

rate variance.

An adverse efficiency variance means that the work team spent longer making the product than the standard indicated. So, for instance, Karl spent 4 hours making a cage. Once again, we would need to know who was responsible and the reasons for the standard not being achieved.

An idle time variance is caused by the work team not having any work for a longer period than expected.

This could be caused, among other reasons, by:

![]() equipment breakdown;

equipment breakdown;

![]() materials hold-up;

materials hold-up;

![]() a lack of power.

a lack of power.

Activity 18

Suggest who or what you think would be responsible for each of these causes of an adverse idle time variance.

Equipment breakdown _______________________________________

Materials hold-up _______________________________________

Lack of power _______________________________________

EXTENSION 2

Calculating variances can be time-consuming. Computerization is used to provide us with variance information. This extension shows how a spreadsheet can be used to help with costing materials, labour and overheads in Sue Nugus’ book Financial Planning using Spreadsheets.

In practice, things are often more complicated than they seem. There could be a number of contributory factors which different managers would have to account for. It's quite possible that you have suggested:

![]() for equipment breakdown, the maintenance engineer;

for equipment breakdown, the maintenance engineer;

![]() for materials hold-up, the stock control department;

for materials hold-up, the stock control department;

![]() for lack of power, interruption of power supply owing to adverse weather conditions.

for lack of power, interruption of power supply owing to adverse weather conditions.

An adverse rate variance means that the work team costs for the time taken were more than was expected. This is most often because overtime has had to be paid, say because other work overran its time in a factory and so work had to be completed outside normal factory hours. Usually the production controller is responsible for this.

Another common cause of a labour rate variance is the use of more highly paid staff than was anticipated.

4.3 Calculating and presenting variances

Now that we have looked at the nature of variances and at some of their possible causes, we shall briefly calculate some simple variances and try to identify their significance.

Activity 19

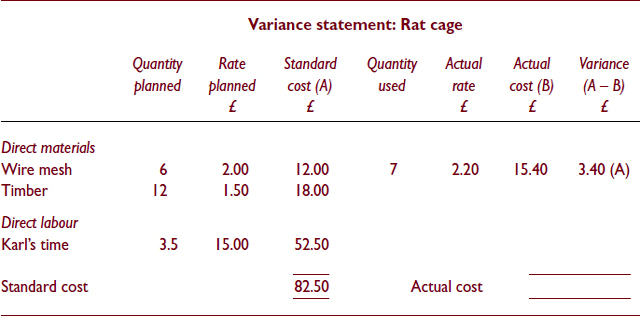

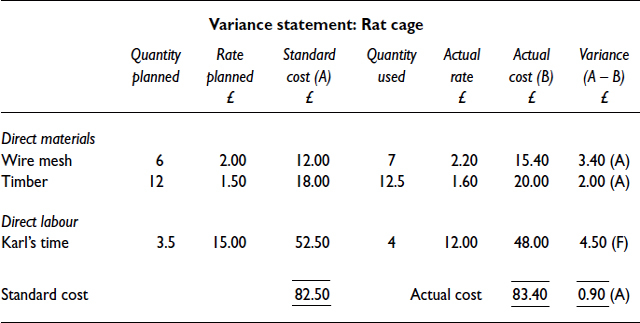

Despite Karl's careful preparation of a standard cost statement for the rat cages, he has now found that it has cost him £83.40 to produce one. He has used 12.5 metres of timber, which cost £20, and 7 square metres of wire mesh, which cost £15.40. He took four hours to make the cage. To try to save money, Karl paid himself only £48.00 for those four hours.

Fill in the variance statement below, in order to identify the causes of the total cost variance (the details have been filled in, and the calculation of the actual rate made, for the wire mesh).

You should have produced a statement like this.

For each type of material, and for labour, we can break the variances down further to see exactly what the causes were (we know that there was no idle time).

| Detailed variance statement: Rat cage | |||

| £ | |||

| Wire mesh price variance | (7 metres × £0.20) | 1.40 (A) | |

| Wire mesh usage variance | (1 × £2.00) | 2.00 (A) | |

| Wire mesh variance (adverse) | £3.40 (A) | ||

| Timber price variance | (12.5 metres × £0.10) | 1.25 (A) | |

| Timber usage variance | (0.5 metres × £1.50) | 0.75 (A) | |

| Timber variance (adverse) | £2.00 (A) | ||

| Labour rate variance | (4 hours × £3.00) | 12.00 (F) | |

| Labour efficiency variance | (0.5 hours × £15.00) | 7.50 (A) | |

| Labour variance (favourable) | £4.50 (F) | ||

| Total cost variance | £0.90 (A) | ||

Don't worry too much about how these detailed variances were calculated. What this statement shows us is what we intuitively knew already: Karl used more materials, and paid more for them per metre, than he expected, and also took longer than he expected to make the cage. By calculating these detailed variances, however, we have pinpointed and quantified the causes, and can then set about ways of reducing those variances that are unacceptable to Karl.

5 The value of standard costing

Standard costing, largely controlled by people, means that a lot of information about performance is gathered.

This leads us to two other advantages of standard costing:

![]() it's possible to achieve real economies through thinking in advance about the best materials to use, the best methods and so on;

it's possible to achieve real economies through thinking in advance about the best materials to use, the best methods and so on;

![]() attention can be concentrated on the variances that exceed predetermined limits, rather than looking at all variances, some of which may be quite minor.

attention can be concentrated on the variances that exceed predetermined limits, rather than looking at all variances, some of which may be quite minor.

So an analysis of variances from standard costs can lead to a very detailed and far-reaching investigation of the problem. Perhaps you've already been involved in such investigations.

Identifying the responsible people is not a witch hunt; we are not looking for somebody to blame. The important step is to account for the variance so that better control can be established in future.

Self-assessment 2

1 Complete the following definition by filling in the missing words.

A standard cost is a ______________ cost that is achieved by setting ______________ related to particular circumstances or conditions of work.

2 Identify two reasons for setting performance standards in any organization.

3 Calculate the standard cost of a vase using the following information:

![]() glass is used which costs £8.00 per metre; a quarter of a metre is used for one vase;

glass is used which costs £8.00 per metre; a quarter of a metre is used for one vase;

![]() a glassworker is paid £7.50 per hour and can make ten vases in an hour.

a glassworker is paid £7.50 per hour and can make ten vases in an hour.

Standard cost statement

| Direct materials: | ___________________________________________ |

| Direct wages: | ___________________________________________ |

| ___________________________________________ |

4 Identify the variance comprising:

![]() direct material cost variances

direct material cost variances

![]() direct labour cost variances

direct labour cost variances

5 State what is indicated by favourable and adverse variances.

Answers to these questions can be found on pages 121–2.

6 Summary

![]() A standard cost is a cost calculated in advance and based on certain approved, specified work practices.

A standard cost is a cost calculated in advance and based on certain approved, specified work practices.

![]() Standard costing allows management to pinpoint variances precisely.

Standard costing allows management to pinpoint variances precisely.

![]() Standard costs have two elements:

Standard costs have two elements:

![]() costs;

costs;

![]() performance level.

performance level.

![]() Standard performance levels should be based on expected standards and contain an allowable level of slack.

Standard performance levels should be based on expected standards and contain an allowable level of slack.

![]() Analysis of cost variances can lead to better cost control.

Analysis of cost variances can lead to better cost control.

![]() The complete diagram of variances we have discussed is as shown below:

The complete diagram of variances we have discussed is as shown below: