Chapter 22

Personal Financial Statements

22.1 What Are They? And Why Do We Need Them?

(a) What Is a Personal Financial Statement?

(b) Whose Financial Statement Is It?

(d) Cash, Accrual, or Something Else?

(e) Which Asset/Liability Goes First?

(a) Due Diligence in the Accountant–Client Relationship

(b) Understanding of the Engagement to All Parties

(c) Value of Written Representations

(d) Operating Rules Are Otherwise Known as Applicable Professional Standards

22.3 Rules and Guidance in Presenting Asset Values

(a) Start by Using the Estimated Current Value

(c) Stock Market and Other Markets

(d) Limited Partnership Interests Are Limited

(e) Gold, Silver, and Other Precious Metals

(f) Options on Assets Other Than Marketable Securities

(h) A Real Challenge Is Valuing a Closely Held Business

(i) Location, Location, Location

22.4 Rules and Guidance in Presenting Liabilities

(a) Start by Using the Estimated Current Amount of the Debt or Liability

(c) Contingencies, Risks, and Uncertainties

(d) Paying the Devil His Due: Income Taxes

22.5 Provision for Income Taxes

(b) Computing the Provision for Income Taxes

22.6 Statement of Changes in Net Worth

(a) Standard Compilation Report

(b) Reporting When Substantially All Disclosures Are Omitted

(c) Reporting When the Accountant Is Not Independent

(d) Reporting on Prescribed Forms

(e) Reporting When There Is a Departure from Generally Accepted Accounting Principles

22.12 Compiled Statements Only for Client Internal Use

22.13 Sources and Suggested References

22.1 What Are They? And Why Do We Need Them?

(a) What Is a Personal Financial Statement?

A standard definition of a personal financial statement is: a listing of everything owned or owed presented in a uniform way so that the user of the statement can understand it.

A personal financial statement presents the personal assets and liabilities of an individual, a couple or a family. It is not a financial statement on a business owned by the person; however, it does contain important information about such business interests.

The essential purpose of a personal financial statement is to measure wealth at a specified date—to take a snapshot of the person's financial condition. It does this by presenting:

- Estimated current values of assets

- Estimated current amounts of liabilities

- A provision for income taxes based on the taxes that would be owed if all the assets were liquidated and all the liabilities paid on the date of the statement

- Net worth

Although both personal and business financial statements are presented for the purpose of informing a reader about the finances of the entity being presented, the statements have many significant differences (see Exhibit 22.1).

Exhibit 22.1 Personal and Business Financial Statements Compared

| Personal | Business | |

| Objective | Measurement of wealth | Reporting of earnings; evaluation of performance |

| Uses | Facilitation of financial planning; | Procuring of credit; |

| Procuring of credit; | Information for shareholders; | |

| Provision of disclosures to the public or the court | Regulatory requirements | |

| Valuation | Current value | Historical cost |

| Method of accounting | Accrual | Accrual |

| Classification | None: assets presented in order of liquidity, liabilities in order of maturity | Assets and liabilities classified as current or long-term |

| Excess of assets over liabilities | Net worth | Equity earnings |

The basic personal financial statement containing this information is called a statement of financial condition, not a balance sheet. Values and amounts for one or more prior periods may be included for comparison with the current values and amounts, but this is optional. The statement of changes in net worth is also optional (also see Section 22.6). It presents the major sources of increase or decrease in net worth (see Exhibit 22.2).

(b) Whose Financial Statement Is It?

Normally, a personal financial statement is compiled for an individual and his or her spouse or one or the other person individually.

A personal financial statement covering a whole family usually presents the assets and liabilities of the family members in combination, as a single economic unit. However, the members may have different ownership interests in these assets or liabilities. For example, the wife may have a remainder interest in a testamentary trust, whereas the husband may own life insurance with a net cash surrender value. It may be useful, especially when the statement is to be used in a divorce case, to disclose each individual's interests separately. This may be done in separate columns within the statement, in the notes to the statement, or in additional statements for each individual.

Often an individual covered by the statement is one of a group of joint owners of assets, as with community property or property held in joint tenancy. In this case, the statement should include only the individual's interest as a beneficial owner under the laws of the state. If the parties' shares in the assets are not clear, the advice of an attorney may be needed to determine whether the person should regard any interest in the assets as his or her own and, if so, how much. The statement should make full disclosure of the joint ownership of the assets and the grounds for the allocation of shares.

(c) Why Are They Needed?

Many individuals or families use personal financial statements for investment, tax, retirement, gift and estate planning, or for obtaining credit. A personal financial statement may also be required for disclosure to the court in a divorce case or to the public when the individual is a candidate or an incumbent of public office. Another example of the use of a specialized personal financial statement was where the statement was used in litigation to show the solvency of an individual who had been the holder of a business franchise that was terminated due to an “alleged” insolvency.

(d) Cash, Accrual, or Something Else?

American Institute of Certified Public Accountants (AICPA) Statement of Position (SOP) No. 82–1 (Financial Accounting Standards Board [FASB] ASC 274–10; see Section 22.2(d)) establishes the use of estimated current values and amounts and the accrual basis of accounting as generally accepted accounting principles (GAAP) for personal financial statements. The American Institute of Certified Public Accountants (AICPA) Personal Financial Statements Guide (the Guide) allows accountants to prepare, compile, review, or audit personal financial statements on other comprehensive bases of accounting, such as historical cost, tax, or cash. In actual practice, there are many variations on a theme, but the methodologies and approaches should be disclosed and should not be misleading to the user of the statement.

(e) Which Asset/Liability Goes First?

Cash is king (and the most liquid of the assets). So cash is at the top of the list. Assets are presented in order of liquidity and liabilities in order of maturity. No distinction is made between current and long-term assets and liabilities because there is no operating cycle on which to base that distinction in a person's financial affairs.

Assets and liabilities of a closely held business that is conducted as a separate entity are not combined with similar personal items in a personal financial statement. Instead, the estimated current net value of the person's investment in the entity is shown as one amount. But if the person owns a business activity that is not conducted as a separate entity, such as a real estate investment with a related mortgage, the assets and liabilities of the activity are shown as separate amounts.

22.2 Practical Tips

(a) Due Diligence in the Accountant–Client Relationship

As is the case with any potential business relationship, before accepting an engagement involving personal financial statements, the accountant ordinarily would evaluate certain aspects of the potential client relationship.

The accountant may wish to consider facts that might bear on the integrity of the prospective client. Consideration of the character and reputation of the individual helps to minimize the possibility of association with a client who lacks integrity. The extent of the accountant's inquiries before acceptance might depend on his or her previous knowledge of the client and the nature of the client's financial activities. The accountant may want to consult predecessor accountants or auditors, attorneys, bankers, and others having business relationships with the individual regarding facts that might bear on the integrity of the prospective client. This does not suggest that, in accepting an engagement, the accountant vouches for the integrity or reliability of a client. However, prudence suggests that an accountant be selective in determining his or her professional relationships. It is not unknown for a seemingly high-profile potential client, complete with private jet and an entourage of assistants, to be a fraudster, destined for more humble quarters in a prison.

The accountant may also wish to consider circumstances that present unusual business risk, such as considering whether an individual is in serious financial difficulty and if that fact could have a bearing on the integrity of the information presented to the accountant for the preparation of the financial statements.

In addition, the accountant may want to consider up front the effect of any lack of independence on the type of report he may issue in compliance with professional standards. Statements on Standards for Accounting and Review Services (SSARS) No. 19 permits the accountant to issue a compilation report on personal financial statements of an individual with respect to whom the accountant is not independent. However, the accountant must be independent to issue a review report or an audit opinion. For example, if a prospective client requesting a personal financial statement is the co-owner of a business with the spouse of the accountant, the accountant is not independent and can issue a compilation only.

Before accepting an engagement involving personal financial statements, the accountant may want to ask the potential client about the availability of records and consider whether available records provide a basis sufficient for providing the services requested. Incomplete or inadequate accounting records are likely to give rise to problems in compiling, reviewing, or auditing personal financial statements. Because of the informal nature of most personal financial records, the accountant should evaluate the need to perform other accounting services in conjunction with personal financial records. AICPA Interpretation No. 101–3, Performance of Nonattest Services, should be consulted for guidance.

Professional standards require the accountant to attain a certain level of knowledge of the client's financial activities. Before accepting an engagement, the accountant should consider whether he or she can obtain an appropriate understanding of the nature of the prospective client's financial activities and the specialized accounting principles and practices related to any of the client's financial activities.

(b) Understanding of the Engagement to All Parties

Once the accountant has decided to accept an engagement involving personal financial statements, SSARS No. 19, Compilation and Review Engagements, states: “[T]he accountant should establish an understanding with management regarding the services to be performed for compilation engagements and should document the understanding through a written communication with management.”

The individuals requesting personal financial statements may not be familiar with the accountant's service or its limitations and may confuse such engagements with audits. It is important that both parties have an understanding of the engagement, and a written understanding is the best one to prevent misunderstandings. An engagement letter would normally include:

- Type of service being provided (compilation, review, or audit)

- Statements to be produced

- Applicable standards

- Client and accountant/auditor responsibilities

- Differences among compilations, reviews, and audits

- Indication that the engagement cannot be relied on to disclose errors, fraud, or illegal acts

- Fees

(c) Value of Written Representations

Talk is cheap and can be easily misconstrued or, in retrospect, be unclear as to facts and circumstances. During an engagement, the client will ordinarily make many representations to the accountant. Documentation of these representations in written form will indicate their continuing appropriateness and reduce the possibility of misunderstanding. The actual content of the letter will depend on the circumstances of the particular engagement.

Generally accepted auditing standards (GAAS) require that an independent auditor performing an audit in accordance with GAAS obtain written representations from management for all financial statements and periods covered by the auditor's reports. The representation should be addressed to the auditor and should be made as of a date no earlier than the date of the auditor's report.

SAARS No. 19 requires that the accountant obtain a representation letter from the client as part of every review engagement as well. Compilation engagements do not contemplate tests of accounting records and of responses to inquiries by obtaining corroborating evidential matter. However, because of the informal nature of most personal financial records, it is advisable to obtain written representation from the client to confirm the oral representations made in all personal financial statement engagements.

(d) Operating Rules Are Otherwise Known as Applicable Professional Standards

The primary authoritative guidance for accountants on the preparation of personal financial statements is SOP No. 82–1, Accounting and Financial Reporting for Personal Financial Statements, issued by the AICPA (FASB ASC 274–10).

Accountants are often engaged to compile, review, or audit personal financial statements. These different types of engagements are governed by different standards. Standards for compilation of financial statements prescribed by SSARS No. 19 are applicable to the compilation of personal financial statements in the same manner as they apply to the compilation of other financial statements.

However, AICPA release SSARS No. 6, Reporting on Personal Financial Statements Included in Written Personal Financial Plans, provides an exemption from the performance and reporting standards of SSARS No. 19 for personal financial statements included in written personal financial plans as long as both of the next conditions exist:

If an accountant prepares a personal financial statement under this exemption, he or she should issue a written report stating the restricted purpose of the statement and noting that it has not been audited, reviewed, or compiled. (See also Sections 22.8 and 22.9.)

Standards for review of financial statements prescribed by SSARS No. 19 apply to the review of personal financial statements in the same manner as to the review of other financial statements (also see Section 22.8), and GAAS apply to the audit of personal statements in the same manner as to the audit of other financial statements.

Accountants may also be asked to report on specified elements, accounts, or items of a personal financial statement. In those circumstances, the guidance provided by Statement on Auditing Standards (SAS) No. 62, Special Reports, Statements on Standards for Attestation Engagements (SSAE) No. 10, Attestation Standards, as amended, and SSARS No. 19. The authors highly recommend the use of the AICPA Guide. The Guide, which was prepared by the AICPA Personal Statements Task Force, provides excellent guidance about the application of professional standards to personal statement engagements. The Guide was originally published in 1982–1983 but has been updated periodically to include changes resulting from the issuance of authoritative pronouncements since that time.

22.3 Rules and Guidance in Presenting Asset Values

(a) Start by Using the Estimated Current Value

According to SOP No. 82–1 (FASB ASC 274–10), personal financial statements must present assets at their estimated current values.

The definition of estimated current value as shown in SOP No. 82–1 (FASB ASC 274–10) is “the amount at which the item could be exchanged between a buyer and a seller, each of whom is well informed and willing, and neither of whom is compelled to buy or sell.” Sales commissions and other costs of disposal should be considered if they are expected to be material to the value.

SOP No. 82–1 (FASB ASC 274–10) recognizes that determining the estimated current value of some assets may be difficult. Judgment should be exercised if the costs of determining the estimated current value of such assets outweigh the benefits. For example, some unique collections may not have a readily determinable value, as there are few benchmark transactions or no discernible market for these items (as there are for some stamp, coin, and car collections) on which to base a valuation. In such cases, the valuation may be a conservative one, despite the enthusiastic valuation of the assets by their owner.

In general, the best way to determine estimated current value is by reference to recent transactions involving market prices of similar assets in similar circumstances, such as published prices for marketable securities.

If recent market prices are not available, other methods may be used. SOP No. 82–1 (FASB ASC 274–10) recommends:

- Capitalization of past or prospective earnings

- Liquidation value

- Appraisals

- Adjustment of historical cost based on changes in a specific price index

- Discounted amounts of projected cash receipts and payments

Whatever method is used, it should be consistently applied from period to period for the same asset unless there is a change in circumstances. Should there be a change in the method or the circumstances surrounding a particular asset, a disclosure regarding such a change should be made in the notes to the statements.

If the client requests a change in the method used to calculate the value of an asset and it is not supported by a significant change surrounding the circumstances surrounding the asset, this is a departure from GAAP, and the accountant's report should be modified.

(b) What Is Owed from Others?

Debts or obligations that are owed from others are called receivables. When they represent near-term commitments, they often do not carry any provision for interest to be paid, as it would be a nominal amount. The theory, however, is that such notes or promises, when they are far in the future, be presented at the discounted (net of interest) amounts of cash expected to be collected, using the prevailing interest rate at the date of the statement to discount these cash flows.

Even though there is no interest noted in an agreement, the face amount of the note showing the balance owed may not be the amount that should be shown on the statement of condition. Within many families and within certain religious, cultural, or ethnic groups, the concept of interest is not recognized. As a result, the face amount of the amount owed may not appear to specify that there is any interest involved but may, in fact, include an implicit interest amount. Another issue faced in valuation is the determination of the discount when faced with a risk of collectability. For example, a valuation engagement for an estate involved a note receivable from a corporation that was near bankruptcy. After reviewing the statements of the company, the accountant discounted the value of the note by 40 percent, by using a high interest rate to compensate for the risk. In a similar manner, a note from one family member to another may be discounted more heavily based on the poor condition of the debtor.

(c) Stock Market and Other Markets

Marketable securities are stocks, bonds, unfulfilled futures contracts, options on traded securities, certificates of deposit, and money market accounts for which market quotations are publicly available. The estimated current value of a marketable security is its closing price on the date of the statement, less any expected sales commission to be paid. Individual retirement accounts (IRAs) and Keogh accounts should be presented net of the penalty charge for early withdrawal.

- If the security was not traded on that date but published bid and ask prices are available, SOP No. 82–1 (FASB ASC 274–10) states that the estimated current value should be within the range of those prices. Using the principle of conservatism, one school of thought suggests that if there is a wide gap between bid and asked amounts, then the selected price should be toward the lower end of the range.

- If bid and asked prices are not available for the date of the statement, the estimated current value is the closing price on the last day that the security was traded, unless the trade occurred so far in the past as to be meaningless by the date of the statement.

- On over-the-counter securities, unfortunately, the market does not speak with a single voice. Different quotations may be given by the financial press, quotation publications, financial reporting services, and various brokers. In such a case, the mean (average) of the bid prices, of the bid and asked prices, or of the prices quoted by a representative sample of brokers may be used as the estimated current value.

- Movement of large blocks of stock may also pose a problem. If a large block of stock was dumped on the market, the market price may be adversely affected. However, a controlling interest might be worth more, share for share, than a minority interest. Market prices may need to be adjusted for these factors to determine estimated current value. Preparers should consult a qualified stockbroker for an opinion on a particular situation such as this. Discounts for blockage as it relates to accounting and fair value are issues of contemporary accounting discussion for large companies as well as smaller ones.

- Restrictions on the transfer of a stock are yet another factor that might call for an adjustment of market prices to determine estimated current value.

- Options values should be reported at published prices. If prices are not available, value should be determined on the basis of the value of the asset subject to option, considering exercise price and the length of the option period.

Because of the importance of valuations to taxing authorities, some valuations may result in challenges, even though they may conform to accounting practice. For example, when valuing the transfer of stock for gift tax purposes, an accountant discounted the value of the stock by 5 percent for blockage. The facts supported the small discount of 5 percent since, although the stock was regularly traded, it was not traded in large quantities. Unfortunately, the Internal Revenue Service did not agree with the valuation, and, in order to avoid a costly appeals process and possible litigation, a lower, compromise discount was proposed and accepted.

(d) Limited Partnership Interests Are Limited

Since limited partnership interests are limited by the terms of the agreement, they should be discounted to reflect the lack of participation and transferability.

Except for publicly traded limited partnerships, accountants may value the asset by taking the value of the assets less liabilities and discounting the result based on the nature and extent of restrictions contained in the partnership agreement, also giving consideration to the actual operation of the partnership as it relates to distribution of cash flow. In one engagement we found that in a limited partnership that owned and operated a business, the manager/general partner was underpaid for duties and responsibilities. After determining the appropriate compensation and adjusting cash flow downward, we reduced the value of the partnership interests.

If the interests in a limited partnership are actively traded, the estimated current value of such an interest should be based on the prices of recent trades. If interests in the partnership are not actively traded, the value of reasonably comparable securities, or the current value of the partnership's underlying assets may be used to measure the value of the interest (see Section 22.3(h)). When this method is used, the person should consider discounting the value of the interest for lack of marketability and lack of control over the general partner. As with the valuation of private equity securities, discounts should not be based on arbitrary rules of thumb but on the facts and circumstances of the valuation. In practice, discounts they can vary significantly (e.g., 5 to 60 percent) based on the nature and number of the issues.

If it is not feasible to estimate the current value of the partnership's underlying assets (and the interests are not actively traded), and the entity is in an early stage of development, the estimated current value of the interest may be shown as the amount of cash that the person has invested. If the underlying assets of the partnership are considered to be virtually worthless, however, the interest should be valued at zero.

The person's share of the partnership's negative tax basis, if any, should be included in the computation of the provision for income taxes (see Section 22.5).

The statement should disclose the person's share of any recourse debts of the partnership and any commitments for future funding. If the person's interest in the partnership represents a substantial proportion of ownership, it may be useful to disclose summarized financial information about the partnership as an investment in a closely held business (see Section 22.3(h)).

(e) Gold, Silver, and Other Precious Metals

The estimated current value of precious metals, like that of marketable securities, is their closing price on the date of the statement, less the expected sales commission.

(f) Options on Assets Other Than Marketable Securities

Options to buy assets other than marketable securities should first be valued at the difference between the exercise price and the asset's current value. Then this difference should be discounted at the person's borrowing rate over the option period, if this is material. The borrowing rate should reflect the cost of any loan secured by the asset.

Because we are valuing the option, not the asset, we need to find out if the option is in the money. That is, would it make economic sense to exercise the option because the current value is higher than the exercise price? If it is not higher, then the option has no current value.

(g) Life Insurance

The estimated current value of a life insurance policy is its cash surrender value, less any loans against it. This information may be obtained from the insurance company.

Disclosure of the face value of the policy is required by SOP No. 82–1 (FASB ASC 274–10). It may also be useful to disclose the death benefits that would accrue to family members covered by the statement.

(h) A Real Challenge Is Valuing a Closely Held Business

Can a business with liabilities in excess of its assets have value? Answer. It all depends on the facts. One business that had a negative net worth sold for approximately $4 million due to the intangibles of a customer list and its established name. The challenge is finding those assets. Another company was worth more than it would appear due to its trained and in-place workforce.

If the person has a material investment in a closely held business that is conducted as a separate entity, the statement should disclose:

- Name of the company

- Person's percentage of ownership

- Nature of the business

- Summarized financial information on the company's assets, liabilities, and results of operations, based on the company's financial statements for the most recent year

- Basis of presentation of the company's statements, such as GAAP, tax, or cash

- Any significant loss contingencies

Determining the estimated current value of an investment in a closely held business, whether a proprietorship, partnership, joint venture, or corporation, is notoriously difficult. The objective is to approximate the amount at which the investment could be exchanged, on the date of the statement, between a well-informed and willing buyer and seller, neither of whom is compelled to buy or sell. This value is presented as a single item in the statement of financial condition, and a condensed balance sheet of the company should be presented in the notes.

SOP No. 82–1 (FASB ASC 274–10) recognizes several methods, or combinations of methods, for determining the estimated current value of a closely held business:

- Appraisals

- Multiple of earnings

- Liquidation value

- Reproduction value

- Discounted amounts of projected cash receipts

- Adjustments of book value

- Cost of the person's share of the equity of the business

SOP No. 82–1 (FASB ASC 274–10) says that if there is an existing buy-sell agreement specifying the amount that the person will receive when he or she withdraws, retires, or sells out, it should be considered, but it does not necessarily determine estimated current value.

While all of the methods listed are valid valuation methods, the difficulty is determining which method or methods are most appropriate for the particular business being valued. It is also important to keep in mind that estimated current value is based on the accrual basis of accounting. If the business being valued keeps it books on the cash or tax basis of accounting, the amounts utilized in determining the estimated current value should be adjusted to the accrual basis.

A question that SOP No. 82–1 (FASB ASC 274–10) does not address is whether an accountant preparing a personal financial statement should try to value a closely held business at all. Competence in valuing businesses requires a considerable degree of specialized knowledge, and often accountants' litigation liability coverage excludes valuations.

In addition, the Professional Ethics Executive Committee (PEEC) of the AICPA has issued Interpretation 101–3, Performance of Nonattest Services. This interpretation states that independence would be impaired if a member performs an appraisal or valuation service for an attest client where the results of the service, individually or in the aggregate, would be material to the statements, and the appraisal or valuation involves a significant degree of subjectivity. Since valuations and appraisals generally involve a significant degree of subjectivity, independence would often be impaired if the valuation were performed by the accountant issuing a report on the statement. For these reasons, the certified public accountant (CPA) should refrain from valuing the business interest himself or herself. Qualified independent appraisers are often readily accessible to value the business, which will significantly aid in obtaining an objective valuation.

Various business valuation accrediting organizations exist. Some of the best known are the ABA (Accreditation in Business Valuation, by the AICPA), the ASA (Accredited Senior Appraiser of the American Society of Appraisers), and the CBA (Certified Business Appraiser, of the Institute of Business Appraisers). Such organizations generally set standards for objectivity and report preparation and require qualifying examinations and appraisal experience to receive the credential. Additionally, to be an ABA, the candidate must be a CPA.

(i) Real Estate

(i) Location, Location, Location

Estimated current values may be based on:

- Sales of similar properties in similar circumstances

- Discounted amounts of projected cash flows from the property

- Appraisals based on estimates of selling prices and selling costs obtained from independent real estate agents or brokers familiar with similar properties in similar locations

- Appraisals used to obtain financing

- Assessed value for property taxes, considering the basis of the assessment and its relationship to market values in the area

The estimated current value of a property should be presented net of expected sales commissions and closing costs.

Pitfalls sometimes encountered with real estate include environmental problems, zoning restrictions, floodplains, or other hazardous conditions or encumbrances. For example, a property of significant value would be valued at a much lower value because if it was leased by another entity at below-market value on a long-term lease.

(j) Personal Property

Personal property includes but is not limited to cars, jewelry, antiques, and art. These items should be valued at appraisal values derived from a specialist's opinion or at the values given in published guides, such as Kelley's Blue Book for automobiles. If the costs of an appraisal seem to outweigh the benefits and if the valuation is not significant to the overall recorded amount, then, historical costs are often used. Appraisers can be located through the American Society of Appraisers.

From a practical perspective, personal property that has appreciated in value is generally conservatively valued if the purpose of the statement of condition is collateral for lending purposes. Accordingly, it may often be prudent to simply use the cost basis.

(k) Intangible Assets

Patents, copyrights, and other intangible assets should be presented at the net proceeds of a current sale of the asset or the discounted amount of cash flow arising from its future use. If the amounts and timing of receipts from the asset cannot be reasonably estimated, the asset should be presented at its purchased cost, evaluated for impairment.

The real issue is often to identify such assets. Frequently, they are not visible to the accountant or recognized by the person engaging the accountant. Questioning and experience are used to identify potential intangibles that might have a recognizable value. For example, a patent may be owned and used within a business enterprise without a designated, separate cash flow. Sometimes anomalies arise, such as a line of greeting cards being valued at greater than the value of the aggregate business that had created and owned the line of greeting cards. Such situations can arise when some product lines are not profitable.

(l) Future Interests

These future interests should be shown in a personal financial statement:

- Guaranteed minimum portions of pensions

- Vested interests in pension or profit-sharing plans

- Deferred compensation contracts

- Beneficial interests in trusts

- Remainder interests in property subject to life estates

- Fixed amounts of alimony for a definite future period

- Annuities

Any other future interests should also be shown, so long as they are nonforfeitable rights for fixed or determinable amounts; are not contingent on the holder's life expectancy or the occurrence of a particular event, such as disability or death; and do not require future performance of service by the holder.

The presentation of future interests should be at the discounted amount of estimated future receipts, using an appropriate interest (discount) rate as of the date of the statements.

22.4 Rules and Guidance in Presenting Liabilities

(a) Start by Using the Estimated Current Amount of the Debt or Liability

Payables and other liabilities are presented at their estimated current amounts. This is the amount of cash to be paid, discounted by the rate implicit in the transaction in which the debt was incurred. Accounting Principles Board (APB) Opinion No. 21, Interest on Receivables and Payables (FASB ASC 835–30), explains how to determine this rate.

Although certain kinds of liabilities are not discounted in business financial statements, all liabilities should be presented at their discounted amounts in personal financial statements. No distinction is made between current and long-term liabilities.

With some home mortgages and other debts, the person may be able to pay off the debt currently at an amount less than the present value of future payments. If this alternative exists, the debt should be presented at the lower amount, as that is the amount the liability could be satisfied if paid today.

Personal liabilities, such as home mortgages, are shown separately from investment liabilities, such as margin accounts. Obligations related to limited partnership investments should be shown if the person is personally liable for them. Debt that was included in the valuation of an investment in a closely held business, however, should not be shown again in this section of the personal statement.

In addition to discounting because of the terms of the obligation, it may be appropriate to reflect the poor condition of the creditor in the valuation. For example, a 30 percent discount rate was applied to value a $100,000 debt that was payable over 10 years. The discounted value reflected the uncertainty of the later payments, and the reduced valuation was used in creditor negotiations.

(b) Fixed Commitments

Child support, alimony, pledges to charities, and other noncancelable commitments to pay future sums should be presented as liabilities at their discounted amounts if they have all of these characteristics:

- The commitment is for a fixed or determinable amount.

- The commitment is not contingent on someone else's life expectancy or the occurrence of a particular event, such as death or disability.

- The commitment does not require future performance by others, as an operating lease does.

(c) Contingencies, Risks, and Uncertainties

During life we enter into many open transactions, which often may lead to unexpected consequences. While we are waiting for the son's or daughter's business to succeed, the lease we cosigned for their business location may become an unanticipated and unwelcome liability, particularly if it requires reaching for the checkbook. Items like this must be disclosed.

Among the contingent liabilities that should be considered for disclosure are:

- Personal guarantees on others' loans

- Liabilities for limited partnership obligations

- Lawsuits against the person

- Inadequate medical insurance coverage

- Noncoverage for personal liability

Statement of Accounting Standards (SFAS) No. 5, Accounting for Contingencies, as amended (FASB ASC 450–10), provides guidance on whether a contingent liability should be recorded, disclosed in a footnote, or omitted. This pronouncement says, in short, that a liability should be recorded if its related contingent loss or range of loss can be estimated and its occurrence is probable. If the amount of loss cannot be estimated but its occurrence is either probable or possible, the related liability should be disclosed in a footnote. If its occurrence is remote, neither recording nor disclosure is required.

(d) Paying the Devil His Due: Income Taxes

Income taxes currently payable include any unpaid income taxes for past tax years, deferred income taxes arising from timing differences, and the estimated amount of income taxes accrued for the elapsed portion of the current tax year to the date of the statement.

If the statement date coincides with the tax year-end, then there is obviously no difficulty in estimating the amount for the current year. If the dates do not coincide, the estimate should be based on taxable income to date and the tax rate applicable to estimated taxable income for the whole year. The taxes for the current year should be shown net of amounts withheld from pay or paid with estimated tax returns.

Estimated income taxes are shown after the liabilities but before net worth on the statement of condition.

22.5 Provision for Income Taxes

(a) Definition

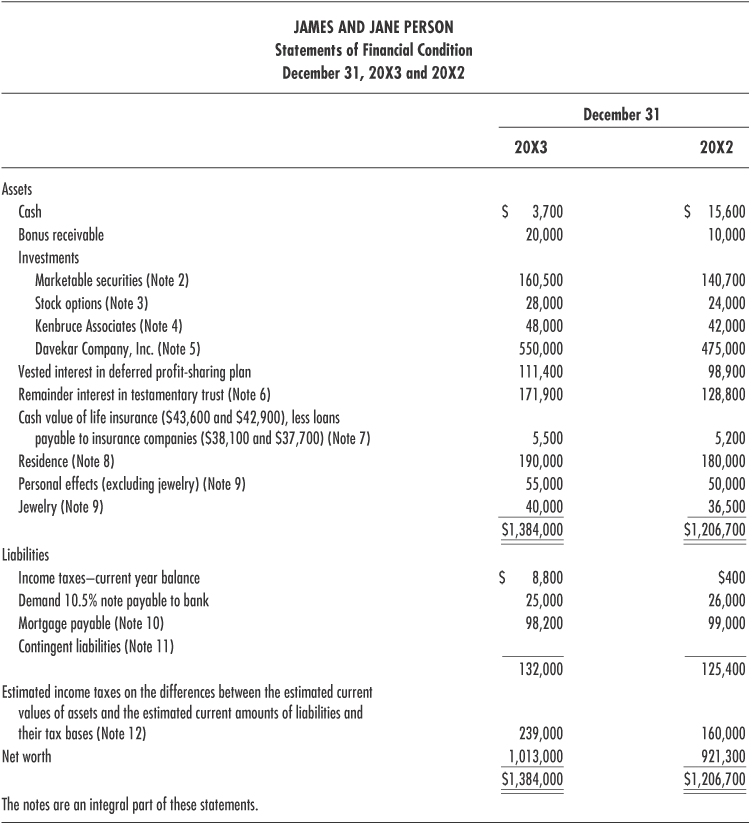

The personal financial statement should show an estimate for the income taxes that would be owed if all of the person's assets were sold, and all of his or her liabilities paid, on the date of the statement. This estimate, known as a provision, should be shown under its full title as given in SOP No. 82–1 (FASB ASC 274–10): “Estimated income taxes on the differences between the estimated current values of assets and the estimated current amounts of liabilities and their tax bases.” It is presented in the statement as one amount and is shown between liabilities and net worth. A note discloses the methods and assumptions used to compute it (refer back to Exhibit 22.2).

(b) Computing the Provision for Income Taxes

Currently applicable income tax laws and regulations—state, local, and federal—should be used in computing the provision for income taxes. Items for consideration include:

- Recapture of depreciation

- Available carryovers of losses, credits, or deductions

- Exclusion for the gain on the sale of a residence

- Deductible state income taxes

- Alternative minimum taxes

Because most of these considerations apply to some assets or liabilities but not to others, the provision for income taxes should be computed separately for each asset and each liability. It is not necessary, however, to disclose all these computations in the note. For example, note 12 in Exhibit 22.2 shows only the excess of estimated current values over the tax bases of major assets.

(c) Tax Basis

It is often difficult to determine the tax basis of an asset or liability acquired long ago or by inheritance or trade. In such a case, the preparer may use a conservative estimate of the tax basis in computing the provision for income taxes, with a note disclosing how the estimate was determined.

(d) Disclaimer

SOP No. 82–1 (FASB ASC 274–10) requires a statement that:

the provision will probably differ from the amounts of income taxes that might eventually be paid because those amounts are determined by the timing and the method of disposal, realization, or liquidation and the tax laws and regulations in effect at the time of disposal, realization, or liquidation.

This statement should be made in the note (see Exhibit 22.2, note 12).

(e) Omission of Disclosure

In addition to omitting the deferred tax liability, some practitioners also do not estimate the income tax liability for the provision for income taxes. This departure from GAAP must be disclosed in the report. In our experience, many personal statements are prepared in connection with bank requirements for loans. We have found that for most of those loans, the banks are not concerned with the amount of estimated taxes on appreciation in value of assets. What they are concerned with are the unpaid income tax obligations for the current and prior years and other short-term liquidity issues. If not provided by the client, one technique to obtain the federal tax liability is to obtain a transcript of the individuals' current and prior tax-year records. The transcripts are available if a power of attorney, Form 2848, has been filed with the Internal Revenue Service.

22.6 Statement of Changes in Net Worth

(a) Definition

A statement of changes in net worth is an optional statement that presents the major sources of change in a person's net worth.

Whereas the statement of financial condition may or may not show amounts for prior periods and thus may not show change in net worth, the statement of changes in net worth should present:

- Increases in net worth produced by income

- Increases in the estimated current values of assets

- Decreases in the estimated current amounts of liabilities

- Decreases in the provision for income taxes

- Decreases in net worth produced by expenses

- Decreases in the estimated current values of assets

- Increases in the estimated current amounts of liabilities

- Increases in the provision for income taxes

The statement of changes in net worth does not attempt to measure net income. It combines income and other changes because the financial affairs of an individual are a mixture of business and personal activities.

The accountant is not precluded from undertaking an engagement to issue a compilation report on a statement of financial condition when a statement of changes in net worth has not been prepared.

(b) Uses

Accountants have often found that lenders do not require a statement of changes in net worth from persons seeking credit and that credit seekers, for their part, are not eager to reveal so much information about their standard of living. But a statement of changes in net worth can be very useful in financial planning by providing information about how much an individual will have to increase earnings or decrease consumption to achieve a desired level of wealth—or how much he or she may decrease earnings or increase consumption and still achieve the same goal.

(c) Format

The sample statement of changes in net worth shown in Exhibit 22.2 distinguishes realized from unrealized sources of increase or decrease in net worth, thus dividing the sources into four categories: realized increases, realized decreases, unrealized increases, and unrealized decreases.

22.7 Disclosures

SOP No. 82–1 (FASB ASC 274–10) states that personal statements should include sufficient disclosures to make the statements adequately informative. These disclosures can be made in the body of the statements or in the notes. The next list, although not exhaustive, indicates the nature and type of information that should ordinarily be disclosed:

- A clear indication of the individuals covered by the statement

- Assets, presented at their estimated current values, and liabilities, presented at their estimated current amounts

- The methods used to determine estimated current values of assets and estimated current amounts of liabilities, and any change in these methods from one period to the next

- Whether any assets shown in the statement are jointly held, and the nature of the joint ownership

- If the person's investment portfolio is material in relation to his or her other assets and is concentrated in one or a few companies or industries, the names of the companies or industries and the estimated current values of the securities

- If the person has a material investment in a closely held business, these points, at a minimum should be disclosed:

- The name of the business, the business form (corporation, partnership, etc.) and the person's percentage of ownership

- The nature of the business

- Summarized information about assets, liabilities, and results of operations for the most recent year based on the statements of the business, including information about the basis of presentation (e.g., GAAP, income tax basis, or cash basis) and any significant loss contingencies

- Descriptions of intangible assets and their useful lives

- The face amount of life insurance owned by the individuals

- Nonforfeitable rights, such as pensions based on life expectancy that do not have the characteristics discussed earlier in the assets section regarding future interests

- This tax information:

- The methods and assumptions used to compute the estimated income taxes on the differences between the estimated current values of assets and the estimated current amounts of liabilities and their tax bases and a statement that the provision will probably differ from the amounts of income taxes that might eventually be paid because those amounts are determined by the timing and the method of disposal, realization, or liquidation

- Unused operating loss and capital loss carryforwards

- Other unused deductions and credits, with their expiration periods, if applicable

- The differences between the estimated current values of major assets and the estimated current amounts of major liabilities or categories of assets and liabilities

- Maturities, interest rates, collateral, and other pertinent details relating to receivables and debt

- Related party transactions, such as notes receivable or notes payable to other family members

- Contingencies such as pending lawsuits and loan guarantees

- Noncancelable commitments, such as operating leases that do not have the characteristics required for inclusion

- Subsequent events, such as a decline in value of an asset after the statement date

It is important to reinforce that the disclosures listed are not all-inclusive. GAAP other than those discussed in SOP No. 82–1 may apply to personal statements. Should a situation arise that is covered by an FASB or other pronouncement, the accountant should look to that source for guidance.

22.8 Compilation

The standards applicable to compilations of financial statements in SSARS No. 19 are applicable to personal financial statements. SSARS No. 19 states that an accountant should establish an understanding with management regarding the services to be performed for compilation engagements and should document the understanding through a written communication with management. Such an understanding reduces the risks that either the accountant or management may misinterpret the needs or expectations of the other party. The AICPA Guide includes sample engagement letters for compilations, reviews, and audits in Appendix A.

The accountant should also have a general understanding of:

- Nature of the individual's financial transactions

- Form of available records

- Qualifications of accounting personnel, if any

- Accounting basis on which the statements are to be presented

- Form and content of the statements

For example, the statements may be on a GAAP, cash, or tax basis.

A compilation requires an understanding of the individual's business and personal records necessary to compile personal financial statements in an appropriate format.

Knowledge required is generally gained through experience with the client's records, such as bank statements, tax returns, broker's statements, property insurance policies, wills, leases, safe deposit box contents, records of closely held business, and through inquiries. The accountant must consider other services that may be necessary to compile an individual's financial statements, such as utilizing a specialist to determine the value of an asset.

Ordinarily an accountant can compile personal statements based on the individual's representation of the estimated current values of assets and the estimated current amounts of liabilities. The accountant should have a clear understanding of the methods used to determine the estimated current values of significant assets and the estimated current amounts of significant liabilities and be satisfied that those methods are appropriate, considering the circumstances of the engagement. The accountant is not an appraiser of assets or an expert in determining present values for items such as pension plans and other assets and liabilities that may appear in personal financial statements. Therefore, it may be appropriate for the accountant to rely on the services of an expert, such as a real estate appraiser or an actuary, in gathering and evaluating client information.

In a compilation, the accountant is not required to make inquiries or perform other procedures to verify, corroborate, or review information supplied by the individual. However, if the accountant has reason to believe that the information supplied by the client is not correct, is incomplete, or is otherwise unsatisfactory to support the compilation of personal financial statements, he or she should attempt to obtain additional or revised information. If the client refuses to provide additional or revised information, or if the accountant cannot otherwise obtain the needed information, he or she should withdraw from the engagement.

Before issuing the report, the accountant should read the compiled personal statements and consider whether they appear to be appropriate in form and free from obvious material errors.

The term errors refers to mistakes (intentional or unintentional) in compiling financial statements, including arithmetical or clerical mistakes, and mistakes in applying accounting standards, which includes inadequate disclosure. Examples of errors that might occur in personal financial statements prepared in conformity with SOP No. 82–1 (FASB ASC 274–10) include:

- Failure to record estimated income taxes on the differences between the estimated current values of assets and the estimated current amounts of liabilities and their tax bases

- Not disclosing the method utilized to estimate current values and amounts

- Presenting asset or liability amounts at an obviously inappropriate value or amount

SSARS No. 19 permits an accountant to compile financial statements that omit substantially all disclosures required by GAAP. Also, since GAAP for personal financial statements involve measurement principles different from those for other reporting entities, the accountant should disclose the use of estimated current values and amounts in the report if the disclosure is not provided in the financial statements.

If the accountant believes that the methods used to determine the estimated current values of assets and the estimated current amounts of liabilities are not in accordance with SOP No. 82–1 (FASB ASC 274–10), or if he or she believes that the methods are not appropriate in light of the nature of each asset and liability, the accountant should modify the report because of a departure from GAAP or should withdraw from the engagement.

If uncertainties are encountered in personal financial statements, the accountant is not required to modify the standard report, provided the financial statements appropriately disclose the matter. However, the accountant may wish to draw attention to such uncertainty in an explanatory paragraph of the compilation report. If so, the accountant should follow the guidance in SSARS No. 19.

The Guide encourages the use of a representation letters in personal statement compilation engagements.

22.9 Review

Standards for reviews of personal financial statements are established in SSARS No. 19. The next items are applicable to reviews:

- reaching an understanding with the client

- gaining an understanding of the individuals' transactions

- understanding the methods used to determine estimated current values of significant assets and the estimated current amounts of significant liabilities

- becoming satisfied that those methods are appropriate

- utilizing the services of an expert when necessary

- reading the statements to ensure they are appropriate in form and free from material error, whether caused unintentionally or due to fraud.

In addition to those items, the accountant must perform inquiry and analytical procedures sufficient to provide a reasonable basis for expressing limited assurance that there are no material modifications that should be made to the client's personal financial statements for them to be in conformity with GAAP or other comprehensive basis of accounting. Analytical procedures include developing an expectation about the relationships between data and comparing recorded amounts to those expectations. The accountant should also consider making inquiries of management concerning their knowledge of fraud in a review engagement. Procedures performed should be documented to support the conclusions reached by the accountant.

Further, before issuing the review report, the accountant should read the reviewed personal statements and consider whether they appear to be appropriate in form and free from obvious material errors, whether unintentional or caused by fraud. The accountant should also consider making inquiries of managers concerning their knowledge of fraud.

A review does not include obtaining an understanding of internal control or assessing control risk, tests of accounting records and of responses to inquiries by obtaining corroborating evidential matter, and certain other procedures ordinarily performed during an audit. Thus, a review does not provide assurance that the accountant will become aware of all significant matters that would be disclosed in an audit. However, if the accountant becomes aware of information that appears incorrect, incomplete, or otherwise unsatisfactory, he or she should perform the additional SSARS No. 19 procedures considered necessary to achieve limited assurance that there are no material modifications that should be made to the financial statements for them to be in conformity with the basis of reporting.

SSARS No. 19 requires a written representation letter in all review engagements. An example representation letter appropriate for a compilation, review, or audit engagement is reproduced in the Guide.

Further, whereas a compilation can be completed without disclosures, a review cannot.

22.10 Audits

GAAS apply to audits of personal financial statements, as they do to other audit engagements. As with any financial statement, the audit objective in personal financial statement engagements is to attest to the fairness of the assertions embodied in the statements. Special attention must be given to the establishment of estimated current values and amounts in accordance with SOP No. 82–1 (FASC ASC 274–10).

GAAS requires a study and evaluation of internal accounting control, tests of accounting records and of responses to inquiries, and other evidential procedures considered necessary in the circumstances of the engagement. Because internal control is not usually a consideration, most of the independent auditors' effort in forming an opinion of personal financial statements consists of gathering evidential matter to support the assertions of existence and valuation of assets and the rights and obligations associated with those assets. SAS No. 101, Auditing Fair Value Measurements and Disclosures, provides important guidance when auditing a personal financial statement, as does a June 2003 Journal of Accountancy article, “The Auditor's Approach to Fair Value.”

Often, as a result of the inadequacy of personal financial records, significant restrictions are imposed on the auditor's efforts to obtain needed evidential matter to support an opinion on personal financial statements. In such a situation, it is not possible to express an unqualified opinion. For this reason, most personal financial statement engagements are compilations, with some reviews.

22.11 Reports

The Guide discusses specific auditor reports relevant to compilation, review, and audit engagements that incorporate the basic reporting standards in the applicable SSARS and SAS.

Because a statement of financial condition is the only personal financial statement required by SOP No. 82–1 (FASB ASC 274–10), often the accountant is engaged to report on that statement only. Occasionally, an individual will need or want the accountant to report on both the statement of financial condition and a statement of changes in net worth. Usually the accountant is asked to report on current-period statements only, although sometimes comparative statements (covering more than one date) are requested.

Reporting standards in the SSARS apply to compilations and reviews of personal financial statements. In a compilation or review engagement, an accountant is required to issue a report whenever the compilation or review is complete; and this requirement is applicable to the personal financial statements of an individual, as specified by SSARS No. 1. However, if an engagement is not completed, a report is unlikely to be issued.

(a) Standard Compilation Report

Personal financial statements compiled by an accountant should be accompanied by a report containing seven areas of information:

Any other procedures the accountant performs in connection with the engagement should not be mentioned in the report.

The compilation report is addressed to the individual whose financial statement(s) are compiled. The date of the report is the date of the completion of the compilation procedures. Also, each page of the statement of financial condition (and the statement of changes in net worth, if presented) should include a reference “See Accountant's Compilation Report.”

An example of a compilation report for a personal financial statement follows.

(INDEPENDENT) ACCOUNTANT'S COMPILATION REPORT

John and Jane Doe

City, State

I (We) have compiled the accompanying statement of financial condition of John and Jane Doe as of December 31, 20XX. I (We) have not audited or reviewed the accompanying financial statement and, accordingly, do not express an opinion or provide any assurance about whether the financial statement is in accordance with accounting principles generally accepted in the United States of America.

The individuals are responsible for the preparation and fair presentation of the financial statement in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statement.

My (Our) responsibility is to conduct the compilation in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. The objective of a compilation is to assist the individuals in presenting financial information in the form of financial statements without undertaking to obtain or provide any assurance that there are no material modifications that should be made to the financial statement.

Firm's Signature

Report Date

(b) Reporting When Substantially All Disclosures Are Omitted

An accountant may be asked to compile personal financial statements that omit substantially all disclosures required by SOP No. 82–1 (FASB ASC 274–10), including disclosures that might appear in the body of the statements. Such reporting is appropriate provided the omission of the disclosures is clearly indicated in the accountant's compilation report and the accountant is not aware that the disclosures are being omitted for the purpose of misleading the intended users of the statements. For example, it would not be appropriate to omit from personal financial statements intended for use in obtaining a home mortgage informative disclosures that would be important to the financial institution in making the loan decision. If disclosures are omitted, and certain selected information is presented in the footnotes—for example, information important in obtaining a mortgage loan—such information should be labeled “Selected Information—Substantially All Disclosures Required by GAAP Are Not Included.”

If substantially all disclosures are omitted from the personal financial statements and the statements do not disclose that the assets are presented at their estimated current values and that the liabilities are presented at their estimated current amounts, the accountant should include this disclosure in the compilation report. If the statements have been presented on a comprehensive basis of accounting other than GAAP, that basis of accounting, if not disclosed in the statements, must be included in the accountant's report.

An example of a compilation report for a personal financial statement with substantially all disclosures omitted follows.

Compilation—Substantially All Disclosures Omitted

(INDEPENDENT) ACCOUNTANT'S COMPILATION REPORT

John and Jane Doe

City, State

I (We) have compiled the accompanying statement of financial condition of John and Jane Doe as of December 31, 20XX. I (We) have not audited or reviewed the accompanying financial statement and, accordingly, do not express an opinion or provide any assurance about whether the financial statement is in accordance with accounting principles generally accepted in the United States of America.

The individuals are responsible for the preparation and fair presentation of the financial statement in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statement.

My (Our) responsibility is to conduct the compilation in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. The objective of a compilation is to assist the individuals in presenting financial information in the form of financial statements without undertaking to obtain or provide any assurance that there are no material modifications that should be made to the financial statement.

John and Jane Doe have elected to omit substantially all of the disclosures required by accounting principles generally accepted in the United States of America. If the omitted disclosures were included in the statement of financial condition, they might influence the user's conclusions about the financial condition of John and Jane Doe. Accordingly, the financial statement is not designed for those who are not informed about such matters.

Firm's Signature

Report Date

(c) Reporting When the Accountant Is Not Independent

An accountant may issue a compilation report on the personal financial statements of an individual even though he or she is not independent with respect to that individual. In such cases, the accountant must modify the compilation report. by adding an additional paragraph to the compilation report stating:

I am [we are] not independent with respect to [name of individual].

The accountant is not precluded from disclosing a description about the reason(s) that his or her independence is impaired. Three examples of descriptions the accountant may use follow.

I am (We are) not independent with respect to [name of individual] as of and for the year ended December 31, 20XX, because I (a member of the engagement team) had a direct financial interest with [name of individual].

I am (We are) not independent with respect to [name of individual] as of and for the year ended December 31, 20XX, because an individual of my immediate family (an immediate family member of one of the members of the engagement team) was employed by [name of individual].

I am (We are) not independent with respect to [name of individual] as of and for the year ended December 31, 20XX, because I (we) performed certain accounting services (the accountant may include a specific description of those services) that impaired my (our) independence.

If the accountant elects to disclose a description about the reasons his or her independence is impaired, the accountant is required to include all reasons for lack of independence in the description.

(d) Reporting on Prescribed Forms

Sometimes an accountant is requested by an individual to assist in assembling data for the completion of a standard preprinted loan form and sign the form or to sign such a form the client has compiled. SSARS No. 3, Compilation Reports on Statements Included in Certain Prescribed Forms (as amended by SSARS Nos. 5, 7, 15, 17 and 19), provides an alternative form of standard compilation report when a prescribed form or related instructions call for a departure from GAAP by specifying a measurement principle not in conformity with GAAP or by failing to request the disclosures required by GAAP.

SSARS No. 3 (as amended by SSARS Nos. 5, 7, 15, 17 and 19) is appropriate for prescribed forms that request information from personal financial statements that have been compiled or reviewed by an accountant.

As stated in SSARS No. 3 (as amended by SSARS Nos. 5, 7, 15, 17 and 19), a prescribed form is any standard preprinted form designed or adopted by the body to which it is to be submitted, for example, forms used by credit agencies. There is a presumption in SSARS No. 3 (as amended by SSARS Nos. 5, 7, 15, 17 and 19) that the information required by a prescribed form is sufficient to meet the needs of the body that designed or adopted the form. Therefore, there is no need for that body to be advised of departures from GAAP SOP No. 82–1 required by the prescribed form or related instructions.

An accountant should not sign a preprinted accountant's report that does not conform to the guidance in SSARS No. 19 regarding the standard compilation report. If the preprinted report form cannot be appropriately revised, the accountant should attach his or her own report following the guidance provided in SSARS No. 3 (as amended by SSARS Nos. 5, 7, 15, 17 and 19) or SSARS No. 19, as appropriate.

(e) Reporting When There Is a Departure from Generally Accepted Accounting Principles

An accountant compiling or reviewing personal statements may become aware of a departure from GAAP involving either measurement principles or disclosure principles, or both. If the accountant determines that explaining the GAAP deficiencies in the personal statements in the report will not adequately communicate the problems to potential statement users, the accountant should withdraw from the engagement and issue no report.

If the accountant believes he or she can appropriately communicate the departure in the compilation or review report, the departure should be described in a separate paragraph of the report. The separate paragraph(s) should explain what GAAP requires, the client's departure, and the effects of the departure on the statements, if such effects have been determined. If the effects have not been determined, this fact should also be disclosed in the separate paragraph(s).

For example, if the client has reported an investment at cost rather than at fair value as required by GAAP for personal financial statements, and the accountant cannot persuade the individual to change the amount, the accountant's report should explain the GAAP departure.

Some departures from GAAP are not as easy to detect. For example, a client going through a divorce may want to change the method utilized from previous financial statements to estimate the fair value of an asset. If the sole purpose of the change is to manipulate the distribution of property in the divorce, the change in method is a departure from GAAP.

(f) Standard Review Report

An example review report for a personal financial statement is shown next.

INDEPENDENT ACCOUNTANT'S REVIEW REPORT

John and Jane Doe

City, State

I (We) have reviewed the accompanying statement of financial condition of John and Jane Doe as of December 31, 20XX. A review includes primarily applying analytical procedures to the individuals' financial data and making inquires of the individuals. A review is substantially less in scope than an audit, the objective of which is the expression of an opinion regarding the financial statement as a whole. Accordingly, I (We) do not express such an opinion.

The individuals are responsible for the preparation and fair presentation of the financial statement in accordance with accounting principles generally accepted in the United States of America and for designing, implementing, and maintaining internal control relevant to the preparation and fair presentation of the financial statement.

My (Our) responsibility is to conduct the review in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants. Those standards require me (us) to perform procedures to obtain limited assurance that there are no material modifications that should be made to the financial statement. I (We) believe that the results of my (our) procedures provide a reasonable basis for our report.

Based on my (our) review, I am (we are) not aware of any material modifications that should be made to the accompanying statement of financial condition in order for it to be in conformity with accounting principles generally accepted in the United States of America.

Firm's Signature

Report Date

Reviews of personal financial statements are not requested as frequently as compilations. Reviews require inquiry and analytical procedures and carry more professional responsibility on the part of the accountant than does a compilation engagement. Further, users of these reports may not understand the concept of limited assurance. As a result, the accountant should take care in determining the type of engagement required and in accepting the engagement. As a matter of simple economics, compilations are the least expensive service. They provide the lowest assurance value to the reader but still may be sufficient for the purpose for which they are prepared.

Audits of personal financial statements are the least common of the three types of engagements primarily because of the general lack of adequate accounting records supporting personal assets and liabilities and the transactions data affecting those balances. Additionally, the required tests and procedures cause this to be a more costly service. Recent requirements regarding the auditor's responsibility to apply procedures relevant to the detection of fraud and other requirements, such as the assessment of the design of the system of internal controls, make little sense in the context of personal statements. Also, the standards requiring presentation of a statement of financial condition with assets at estimated fair values and liabilities at estimated current amounts may create audit difficulties. Fair value estimates involve uncertainty and subjectivity that may not lend themselves to producing evidence that can be efficiently or effectively audited. The auditor may be unable to obtain sufficient competent evidential matter to support an opinion on personal financial statements. Many such engagements that start out as audits end up with a disclaimer of opinion because of scope restrictions on the auditor's ability to obtain necessary evidence.

(g) Standard Audit Report

The auditor's standard report appropriate for personal financial statements is presented next.

INDEPENDENT AUDITOR'S REPORT

I [We] have audited the accompanying statement of financial condition of [James and Jane Person] as of [date], and the related statement of changes in net worth for the [period] then ended. These financial statements are the responsibility of [James and Jane Person]. My [Our] responsibility is to express an opinion on these financial statements based on my [our] audit.

I [We] conducted my [our] audit in accordance with generally accepted auditing standards in the United States of America. Those standards require that I [we] plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by [James and Jane Person], as well as evaluating the overall financial statement presentation. I [We] believe that my [our] audit provides a reasonable basis for my [our] opinion.

In my [our] opinion, the financial statements referred to above present fairly, in all material respects, the financial condition of [James and Jane Person] as of [date], and the changes in their net worth for the [period] then ended in conformity with accounting principles generally accepted in the United States of America.

Paragraphs 9 and 10 of SAS No. 62, Special Reports, paragraphs 9 and 10, provides guidance concerning disclosures in personal financial statements presented on a comprehensive basis of accounting other than GAAP, such as the cash or tax basis of accounting. Similar informative disclosures are appropriate to those required by GAAP for the same or similar issues.

SSARS No. 6 provides an exception for the performance and reporting standards in SSARS No. 19 for personal financial statements included in written personal financial plans. Such statements included in written personal financial plans frequently exclude disclosures required by GAAP and contain other GAAP departures. These exceptions exist because the statements are prepared to facilitate the financial plan and not for credit purposes.

An accountant, according to SSARS No. 6, may submit a written personal financial plan containing unaudited personal financial statements to a client without complying with the compilation and review performance and reporting standards when all these conditions are met:

- An understanding is reached with the client, preferably in writing, that the financial statements will be used solely to assist the client's advisors to develop the client's personal financial goals and objectives.

- The document will not be used to obtain credit or for any purposes other than developing the personal plan.

- Nothing comes to the accountant's attention during the engagement to cause him or her to believe that the statements will be used to obtain credit or for any purposes other than the personal financial plan or its implementation by an insurance agent, broker, attorney, or like agent.

If these objectives are met, the next report, as prescribed in SSARS No. 6, may be used in place of the standard compilation report for personal financial statements included in personal financial plans:

The accompanying statement of financial condition of [James and Jane Person], as of [date], was prepared solely to help you develop your personal financial plan. Accordingly, it may be incomplete or contain other departures from generally accepted accounting principles and should not be used to obtain credit or for any purposes other than developing your financial plan. We have not audited, reviewed, or compiled the statement.

Each of the personal financial statements should include a reference to the accountant's report.

22.12 Compiled Statements Only for Client Internal Use