9

REVIEW YOUR BUSINESS

COMPREHENSIVELY

BEING ANALYTICAL—or more specifically, being successful with analytics—is not a one-time activity. Analytical competitors must constantly review and revise their approaches in light of their business strategies and business models, changing market conditions, competitor initiatives, and the expectations and behaviors of customers. These days the world changes rapidly and analytical models need to reflect the changes. In this chapter, we discuss how to keep track of your analytical processes and models to make it easier to stay in sync with changing business conditions.

The 2007–2009 financial crisis provides an excellent illustration of the importance of continuous review of analytics. Financial institutions repeatedly failed to undertake timely reviews of their financial models and assumptions. When housing prices stopped rising in 2006, customers’ ability to pay off mortgages through refinancing was no longer possible, but banks continued to make subprime loans. The banks simply didn’t monitor and revise their analytical models closely enough.

In an industry like financial services where effective analytics are key to success, firms need to continually review analytical models, assumptions, and management frameworks. These activities are not just good management hygiene; they are a means to survival.

Constant Review to Create New Insights

One important aspect of analytical review is never resting on your laurels. Eternal vigilance is needed to seek out new insights and stay a step (or two or three) ahead of the competition. Progressive Insurance, the third-largest auto insurance firm in the United States, has consistently reviewed its analytical orientation and developed new offerings over time. The company pioneered or adopted early several analytical innovations in the automobile insurance industry, including segmenting high-risk drivers (some had higher risks than others—called “nonstandard” risk), establishing many different price points by risk level, rating drivers based in part on their credit scores and behaviors, and gathering information on actual driver behavior (“pay as you drive”) through its MyRate program. Progressive was rewarded for its innovations by a high rate of growth relative to competitors.

However, in most cases, competitors adopted the same approaches—usually a few years after Progressive did. Allstate, for example, hired an architect of Progressive’s credit scoring approach to implement a similar program, and eventually moved from three different price points to four hundred. 1 A 2001 survey found that 92 percent of property and casualty insurance firms were using credit scores and other measures of financial responsibility for underwriting new policies, and Progressive had only adopted this practice broadly in 1996. 2 It’s relatively easy to copy innovations in the insurance industry, because carriers must file documents with state insurance commissions on how they price and operate. That doesn’t give you everything you need to copy an analytical innovation, but it provides a start.

So Progressive must keep coming up with new ideas. One of the company’s executives suggested that it does so through multiple means: 3

• It has a strong measurement-oriented culture; virtually everything possible is measured.

• It hires and retains people who have an analytical orientation plus a detailed understanding of the business.

• It ensures that any innovations draw heavily on the company’s long data history (Progressive has been in business since 1937).

Most important, analytical innovations at Progressive complement its other strategic advantages. The company has focused on several different strategic capabilities in addition to analytics: a direct-to-consumer competency to augment its industry-leading distribution through independent agents, a strong brand, convenient and efficient claims processing, and the use of the Internet as a channel to customers. When considering new analytical offerings, Progressive also considers how they might interact with other strategic orientations. For example, its initiative to provide consumers with comparative pricing information (Progressive’s price compared to its estimate of competitors’ prices) combined well with the ability to provide prices over the Internet. Sources outside of Progressive suggest that the company probably also maintains an advantage in the extent and complexity of its data and analyses. In pricing, for example, one study found that in one of the markets it serves, Progressive employed over a billion different pricing “cells” (variables times the number of categories per variable). The next closest competitor had one-tenth as many cells. 4

Reviewing Strategy and Business Models

When analytics are used in support of particular strategies and business models, their role needs to be continually reviewed and updated. Analytics make it possible to optimize a strategy, but they are of little value if the strategy itself is no longer viable. Careful monitoring makes organizations more adroit at knowing when it is time to shift strategies. Two organizations that we’ll discuss in this context are Capital One, which has changed its strategy and business model, and American Airlines, which hasn’t yet but probably should.

If you’ve read Competing on Analytics, or if you’ve watched TV or received mail in the United States lately, you’ve heard of Capital One. The company is among the most analytical of firms, and until recently, the most successful. It was founded as a business unit of Signet Bank, and from its spinoff in 1994 up through 2004, it grew earnings per share and return on equity by over 20 percent every year. But by 2005, Capital One’s executives seemed to realize that its primary business—consumer credit cards—was not sufficient to ensure continued success. To avoid being acquired by other banks and to ensure a source of low-cost deposits, it needed to become a full-fledged bank. It therefore bought Hibernia Bank in Louisiana, North Fork Bank in New York, and Chevy Chase Bank in Virginia.

After these acquisitions, Capital One needed to figure out how its “information-based strategy” worked in the new banking business. Its managers immediately set about translating their ethos into the fullservice banking context, which required new data, new models, and new assumptions. As one employee told us, “It’s much easier to do randomized testing with direct-mail envelopes than with branch bankers.” We believe that an innovative firm like Capital One will ultimately figure out how to be an analytical competitor in its current business environment, but it’s not going to happen overnight.

American Airlines was another early analytical competitor, and was earlier at it than almost any other firm. It started its analytical approach to “yield management,” or optimized pricing, in 1985. This approach helped to put some upstart competitors (including People Express) out of business, and according to an operations research society (INFORMS), its yield management systems contributed $1.4 billion in a three-year period at the airline. 5 Today, however, virtually every airline has yield management capabilities, some having learned it from American’s consulting organization, so optimized pricing no longer provides any competitive advantage.

American also uses analytics to optimize its route network and crew schedules. Without analytical tools, managing a complex hub-and-spoke network with over 250 destinations, twelve aircraft types, and 3,400 daily flights would be nearly impossible. Nevertheless, it might be argued that American’s optimized complexity works against it. Neither it nor other major U.S. airlines with similar complexity levels have been very profitable for years.

A much less complex airline model is offered by Southwest Airlines, which has only one aircraft type and no airport hubs. Southwest also uses analytics for seat pricing and operations, but its model is much simpler to optimize. Most important, Southwest has been profitable for thirty-six consecutive years, and at several times over the recent past its market value has been worth more than the combined market value of all other U.S. carriers. This sobering comparison suggests that American and the other more complex carriers need to simplify their own business models.

Reviewing Analytical Targets

We argued in chapter 5 that analytical targets are important, and that they should be driven by your organization’s strategy and business models. If those change—and they should as the world changes—then the analytical targets should change as well. At a global retail finance organization, for example, the need for a “target review” became very apparent when the head of analytics met with some of his internal customers in the U.K. “We are grateful for the mortgage and lending models you have provided for us,” he was told, “However, they are all wrong and need to be made much more conservative.” Further remarks led to the change in targets: “In addition, we would like you to change your focus entirely going forward to concentrate on risk—credit risk, asset management risk, enterprise risk, you name it.”

Now, as the analytics manager noted in a discussion with us, a wholesale shift from credit to risk analytics wouldn’t necessarily be wise. Financial institutions need a balance of focus on risk and opportunity. But you can bet that he and his group are now pursuing risk analytics in a much more aggressive way.

We’ve seen changes in analytical targets in the retail industry that were also motivated by difficult economic times. Several companies in that industry were pursuing analytical strategies based on loyalty programs and customer intelligence. Their primary focus was on how to get currently loyal customers to buy more. Since the economic downturn began in 2008, several retailers have shifted their primary target for analytical work to cost reduction and efficient marketing. One, for example, is focusing on marketing mix optimization topics. A company executive we interviewed admitted, “We’re trying to figure out, at long last, whether our advertising circulars really work, and are comparing them to more targeted offers.” Another retailer that primarily addresses customers through catalogs is pruning its mailing list to those customers who have responded with profitable purchases over the last two years. It is also customizing the content of the catalogs by sending longer, heavier catalogs to better customers. Though these practices may seem like punishing loyal buyers with more and bulkier junk mail, both marketing mix optimization and targeted mailings can save considerable amounts in marketing budgets. Another retailer sought to improve profitability by minimizing returns. Whereas the previous focus had been on identifying the best customers, the company began to identify attributes of “serial returners”—customers who routinely return items—and then took steps to reduce the offers they received. The retailer also retrained the sales force to make certain that customers were happy with their potential purchases before the sale.

Reviewing Competitors

It’s also important to constantly review the analytical activities of competitors to understand how your own activities compare to theirs. You may believe you have a lead, but competitors can catch up—particularly if they have the same sources of data. Meanwhile, your competitors may have adopted analytical approaches that you should be emulating. Of course, if you hope to get any sort of competitive advantage from your analytical activities, just emulating your competitors won’t get you very far.

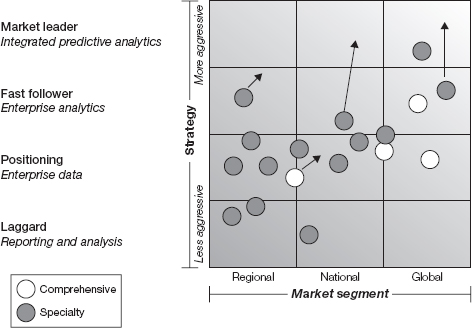

A systematic approach to assessing competitors is likely to yield the greatest benefit. The model in figure 9-1 illustrates the competitive analysis undertaken by a firm in the health care industry.

FIGURE 9-1

Competitive analytics capability model

The bubbles represent each competitor’s current market position and strategy vis-a-vis analytics; the arrow depicts the competitor’s future direction. The shades of gray represent different types of competitors. For each market segment or product line, the framework assesses the key characteristics of analytical investments and the strategic objective of their analytical capabilities. These will vary by industry; the health care firm defined four levels:

• Laggards: Reporting and analysis. The company has limited interest in analytics beyond traditional reporting of data. It is waiting for further proof of adoption for evidence-based medicine before investing in analytics. It may be exploring options for business intelligence products, tools, and programs. (Though if our suspicions are correct, it may not survive long enough to see these initiatives through.)

• Positioning for analytics: Enterprise data. The company recognizes there is a significant risk of diminished market share and adverse selection because of deficiencies in their analytical capabilities. It makes investments in IT and people to support internal analytical needs. It is upgrading information and IT applications to provide a basis for better analytics.

• Fast followers: Enterprise analytics. The company views business intelligence and informatics as part of its “competency portfolio” and acknowledges that analytics could become a force for transformational change in the industry. It makes significant investments in new and upgraded analytical capabilities.

• Market leaders: Integrated predictive analytics. The company views analytics as a growth engine and a high priority for investment. It aggressively acquires information assets and competencies. It makes the development of unique and proprietary data a priority. Management is committed to transforming the company through the use of predictive analytics. The company offers new, analytically based products and services to differentiate from competitors.

We’re not advocating “analytical espionage,” but getting competitive intelligence about analytical projects and capabilities is usually a fairly straightforward task. You can talk with industry consultants or academics, interview or hire analytical people who have worked for competitors, view job opening descriptions, attend conferences, and so forth. And, of course, you will observe competitors’ behavior in the marketplace. Investing in a high-powered telescope is probably a last resort.

One of the best examples of analytics and competition is the transformation of the Oakland A’s described in the book Moneyball by Michael Lewis. 6 When selecting players, the team moved from focusing on players’ intangible attributes to their actual past performance. One metric they employed earlier than other teams was “on-base percentage,” which includes both walks and hits—whereas the primary metric of the past, batting average, includes only hits. Of course, it wasn’t very difficult for other teams to find out what Oakland was up to. If they couldn’t figure it out from their draft choices, they could eventually read about it in a best-selling book. Not surprisingly, our sources in professional baseball say that on-base percentage is now overvalued in the market for talent. As two economists who studied the issue put it (in somewhat academic jargon): “Our tests provided econometric support for Lewis’ claim of mis-pricing in the baseball labor market’s valuation of batting skills. We also found suggestive evidence that the dispersion of statistical knowledge throughout baseball organizations was associated with a sharp attenuation of the mis-pricing.” 7

So what is a smart baseball team to do? There is really only one answer: keep on developing new analytics. That’s why the Boston Red Sox hired a crack baseball statistician like Bill James. He’s come up with dozens of ways to measure player and team performance (and he’s much better at keeping secrets). Similarly, companies have to keep innovating in ways that are consistent with their strategies and business models.

In addition to assessing how well you are competing with analytics against other companies, you should also review the benefits of collaborating with them. Collaboration has been particularly effective in health insurance, where nineteen different Blue Cross and Blue Shield organizations around the United States have banded together to sponsor the Blue Health Intelligence (BHI) initiative at the Blue Cross and Blue Shield Association. The plans have furnished claims data (with no personal identification) on 79 million members. Health care provider and pharmacy data are also being added to the database. The large scale of the database allows not only benchmarking comparisons across state and regional plans, but also analytical projects that can be generalized to a national population. BHI analysts, for example, are studying pediatric diabetes patients and trying to predict the occurrence of hospitalizations. They’re also assessing whether spinal surgeries actually reduce back pain. Only by combining forces could BHI get enough data to perform such analyses.

Reviewing Customers and Partners

Customers and their preferences can change over time, so it’s important to ensure that any models based on customer opportunity, risk, or behavior are reviewed frequently. At Netflix, for example, many of the behavioral models for customers were created when the company was founded around the turn of the twenty-first century. Those customers were relative pioneers in ordering movies online. By the middle of the decade, however, Netflix analysts began to question whether the typical customer was very different from that in 2000. Certainly they were no longer pioneers. So the analysts began to retest their models. Without retesting, the models would probably not fit the data for these new customers.

A major Canadian bank conducts frequent customer reviews to gauge their customers’ willingness to supply information to and be contacted by the bank. This particular bank relies on customer contacts to supply new relationships; it offers preferred pricing not only to good customers, but to their relatives and sometimes even close business associates. The bank also uses “event triggers” (e.g., a major cash deposit) to predict when the customer might value an interaction with the bank. The bank’s customer information managers check several times a year the percentage of customers who request “Do not call” status. Fortunately for the bank, the percentage has remained at about 5 percent for many years—must be that legendary Canadian neighborliness. However, the bank also buys lists of potential customers from external data providers, and on the lists they buy, 50 percent are on the “Do not call” list. As a result of this review, the bank is considering no longer purchasing external lists.

Companies should also review their “analytical ecosystems” to determine whether they have the right partners. In the retail industry, for example, a retailer can create its own analytics. It can also supplement those with analytics from data providers such as Nielsen and Information Resources, from real-time promotions vendors such as Catalina, from consumer products suppliers, from analytical consultants (onshore and offshore), and from vendors of analytical software and hardware. If for some reason the internal analytical resources aren’t up to the task, there are many possible alternatives.

Reviewing Technology, Data, and Information

Firms should also review at least annually the new technologies and information that might affect their businesses in the future. For example, it seems quite likely that retail and distribution businesses will have massive amounts of data available when RFID (radio frequency identification) and electronic product code (EPC) devices become widely available. These were predicted to arrive at reasonable cost several years ago—Wal-Mart required them of suppliers on a pilot basis in 2005, then backed away from the requirement—but their eventual arrival seems inevitable.

Firms that care about competitive advantage from supply chain analytics should be thinking now about how they will factor all the available data into their analytical decisions and how systems and processes will take advantage of the analytics. With products broadcasting their identity, it will be much easier to know what’s on store shelves, and hence much easier to create and update demand forecasts, replenishment models, and logistical optimization models. Not all of the detailed work to accommodate these technologies should be done today, but some planning should begin now.

Similarly, firms in industries where electrical energy is generated, distributed, or consumed in large amounts will soon be blessed with large amounts of data for energy management. In the “smart grids” of the future, devices that use or meter energy will broadcast their energy use for centralized monitoring and management. Devices that distribute energy will be able to provide not only energy consumption information but also details of cost and carbon creation. Analytics will be needed to make intelligent decisions about how to use energy wisely and how to deploy it across organizations. Anyone involved in the energy industry should be thinking now about how to analyze and use this new data.

Other industries already have data-intensive technologies in place, but only in a limited number of their sectors. As the technologies become more pervasive, considerable opportunities for analytical exploitation will arise. In health care, for example, if U.S. providers can ever standardize electronic medical records, very large amounts of data will become available for analysis. With sufficient analytics, providers and payers will develop a greater understanding of which treatments are effective and which patients might benefit from disease management approaches. A few leading institutions are already doing some of this analysis, but every organization in the industry should be planning for it.

In short, with new data sources from the Internet and information providers appearing daily, you should be reviewing the role that analytical decisions might play in your future. The companies that are very capable with analytics didn’t get that way by always reacting to problems and opportunities—they anticipated and prepared for them.

Reviewing and Managing Models

“Model management,” the systematic process of creating, monitoring, and deploying analytical models, helps a company constantly review its use of analytics in its interactions with the outside world. There are plenty of reasons to review and manage your models:

• Knowing what models you have in place—as well as what data they use, what assumptions they make, and how and by whom they were created—makes it much easier to find and change them when necessary.

• Keeping track of all of the competing models allows you to know which ones are winning (in the process of developing models, there are many “challengers” and eventually a single “champion”).

• Keeping track of the multiple versions of your model (which, like any computer code, can have many variations) is important.

• You can check to see how well a particular model is working and alert analysts to “model decay.” If the world changes, for example, if mortgage recipients can no longer pay off their loans, a model decay analysis would suggest a change in credit issuance models, signifying that models and their underlying assumptions need updating.

• Regulatory requirements of certain industries, like banking, mandate some degree of model management (although we admit they didn’t seem to help much in preventing the financial crisis).

Despite these virtues, effective model management should go beyond regulatory requirements and internal control documentation. Effective model management and analytics can be used as a competitive advantage. Coordinating models for assessing accounts, transactions, products, business lines, and risk factors help to optimize business decisions. Going further to align accounting valuation models helps to capture the effectiveness of business performance while reducing the noise and burden of variances. For instance, Capital One went beyond directives from federal regulators and embarked upon a systematic effort to capture and document its analytical models. They realized how coordinating internal models and analytics could be used to better model customer behavior and roll up to overall business line and company performance. Other large banks, including CitiGroup, State Street, and JPMorgan Chase have recognized the value of analytical models involving different asset types and have created centralized model libraries and teams of experts to support business lines and ensure diligence in the application of models. Such teams are typically referred to in terms of “model validation” and are normally found in risk management functions.

As organizations become increasingly reliant on their analytical models, we bet that more and more will realize how important model management is. For an increasing number of firms, their analytical models are their gold mines, their oil reservoirs, their bank deposits. To keep track of them and pay attention to how well they’re working is only common sense.

Analytical leaders—firms and managers that are ahead of the pack in analytical orientation—recognize that the business environment for any firm changes rapidly, and to be successful, their analytical orientation must change with it. In industries where analytics have been broadly adopted—from banking to baseball—review is the only way for an organization to stay on top. It is the antidote to the “resting on their laurels” syndrome that otherwise takes leaders into a period of slow decline.