Although the global CAPM (GCAPM) is the simplest risk and return model for internationally integrated financial markets, the GCAPM is not always the best model to use. You will see in this chapter that the GCAPM is a reasonable risk–return model from the US dollar perspective and perhaps from the perspective of a few other currencies as well. For many other currencies, on the other hand, one may want to apply instead the version of the international CAPM (ICAPM) introduced in this chapter.

Introduction to the Two-Factor ICAPM

Whereas the local CAPM and the GCAPM each have only one risk factor, the ICAPM version introduced in the following has two risk factors: (1) the global market index; and (2) a foreign currency index, constructed as described in the box. Because of the two risk factors, an asset has two measures of systematic risk in the ICAPM. An asset has both a “beta,” which measures sensitivity to the global market index, and a “gamma,” which measures sensitivity to the foreign currency index. The “gamma” risk coefficient (g) is called the asset’s FX exposure (to the foreign currency index).1

The ICAPM thus involves two-factor risk premiums from the perspective of home currency H: (1) the global risk premium, GRPH, which is the required rate of return on the global market index in currency H minus the currency-H risk-free rate, ![]() and (2) the foreign currency index risk premium, XRPH, which is the risk premium of the foreign currency index, from the perspective of currency H,

and (2) the foreign currency index risk premium, XRPH, which is the risk premium of the foreign currency index, from the perspective of currency H, ![]() , where

, where ![]() is the required return on the foreign currency index, inclusive of FX changes and foreign currency risk-free rates.

is the required return on the foreign currency index, inclusive of FX changes and foreign currency risk-free rates.

Each of the two ICAPM factor risk premiums is the sum of two components: (1) ![]() ; and (2)

; and (2) ![]() .

.

From the perspective of the home currency H, the foreign currency index contains a position in each of the other currencies. Each position in the foreign currency index is a risk-free, interest-earning deposit in currency C, and has a return equal to the percentage change in currency C versus currency H, xH/C, plus the currency-C risk-free rate. The weights on the index’s currency deposit positions are based on national financial wealth, which is not necessarily the same as an economy’s percentage of global equity market capitalization.

The world wealth percentages for the 21 economies listed in Exhibit 2.1, from the Credit Suisse Research Institute Global Wealth Databook for 2015, represent 94% of world wealth. Exhibit 2.1 shows the wealth weight estimates, wC, which are the 21 world wealth percentages normalized to sum to 100%.

The composition of the foreign currency index is different for each different home currency perspective, because the index contains currencies that are foreign from the perspective of currency H. The position weight for currency C in currency-H’s foreign currency index is wC divided by (1 − wH). For example, the euro’s weight in the US dollar’s foreign currency index is 0.204/(1 − 0.379) = 0.329, or 32.9%. The US dollar’s weight in the euro’s foreign currency index is 0.379/(1 − 0.204) = 0.476, or 47.6%.

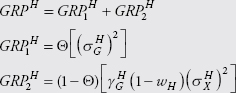

The first GRPH component accounts for the risk in the global market index from the currency-H perspective and the aggregate market’s degree of aversion to that risk: ![]() , where Θ denotes the global market price of risk, and

, where Θ denotes the global market price of risk, and ![]() is the volatility (standard deviation) of the global market index return from the perspective of currency H.

is the volatility (standard deviation) of the global market index return from the perspective of currency H. ![]() is the same as the global risk premium would be if the GCAPM held in currency H, or if there were no correlation between the returns on the global market index and the foreign currency index from the perspective of currency H. The second GRPH component is:

is the same as the global risk premium would be if the GCAPM held in currency H, or if there were no correlation between the returns on the global market index and the foreign currency index from the perspective of currency H. The second GRPH component is: ![]() , where

, where ![]() is the FX exposure of the global market index to the foreign currency index, which accounts for the systematic risk of the global market index versus the foreign currency index; wH is the wealth weight of the currency-H economy; and

is the FX exposure of the global market index to the foreign currency index, which accounts for the systematic risk of the global market index versus the foreign currency index; wH is the wealth weight of the currency-H economy; and ![]() is the volatility of the foreign currency index return.2

is the volatility of the foreign currency index return.2

For example, assume Θ = 2.50 and the following inputs (shown in Exhibit 2.1) for the US dollar perspective: ![]() ;

; ![]() ; and

; and ![]() . The two GRPH components are:

. The two GRPH components are: ![]() = 2.50[(0.1594)2] = 0.0635; and

= 2.50[(0.1594)2] = 0.0635; and ![]() = (1 − 2.50)[1.23(1 −0.379)(0.0616)2] = −0.0043, or −0.43%. Adding the components, we get the global risk premium in US dollars: GRP$ = 0.0635 − 0.0043 = 0.0592, or 5.92%.

= (1 − 2.50)[1.23(1 −0.379)(0.0616)2] = −0.0043, or −0.43%. Adding the components, we get the global risk premium in US dollars: GRP$ = 0.0635 − 0.0043 = 0.0592, or 5.92%.

ICAPM Factor Risk Premiums

Global Risk Premium

Foreign Currency Index Risk Premium

Θ |

= |

Market Price of Risk |

|

= |

Volatility of Global Market Index Return |

|

= |

Volatility of Foreign Currency Index Return |

|

= |

FX Exposure of Global Market Index versus the Foreign Currency Index |

|

= |

Foreign Currency Index’s Global Beta |

wH |

= |

Wealth Weight of the Currency-H Economy |

For the foreign currency index risk premium, XRPH, the first component depends on the volatility of the foreign currency index and the relative wealth weight for currency H: ![]() . The foreign currency index premium would be

. The foreign currency index premium would be ![]() given a zero correlation between the returns of the global market and the foreign currency index from the perspective of currency H. The second XRPH component accounts for any systematic risk of the foreign currency index versus the global market index, through the foreign currency index’s global beta,

given a zero correlation between the returns of the global market and the foreign currency index from the perspective of currency H. The second XRPH component accounts for any systematic risk of the foreign currency index versus the global market index, through the foreign currency index’s global beta, ![]() .

.

For example, assume the foreign currency index has a beta from the US dollar perspective of ![]() (as shown in Exhibit 2.1). If the US dollar is the home currency, the estimates of the two components of the foreign currency index risk premium are:

(as shown in Exhibit 2.1). If the US dollar is the home currency, the estimates of the two components of the foreign currency index risk premium are: ![]() = (1 − 2.50)[(1 − 0.379)(0.0616)2] = −0.0035, or −0.35%; and

= (1 − 2.50)[(1 − 0.379)(0.0616)2] = −0.0035, or −0.35%; and ![]() = 2.50[0.183(0.1594)2] = 0.0116, or 1.16%. Adding the components, the foreign currency index risk premium for the US dollar perspective is: XRP$ = −0.0035 + 0.0116 = 0.0081, or 0.81%.

= 2.50[0.183(0.1594)2] = 0.0116, or 1.16%. Adding the components, the foreign currency index risk premium for the US dollar perspective is: XRP$ = −0.0035 + 0.0116 = 0.0081, or 0.81%.

For 21 currency perspectives, Exhibit 2.1 shows the ICAPM statistical input estimates for the factor risk premium estimates, which are calculated with data for 1999 to 2016. Exhibit 2.2 shows the ICAPM’s two-factor risk premia, GRPC and XRPC, and the two components of each factor risk premium. The estimates assume Θ = 2.50. Note that in the ICAPM, the global market price of risk, Θ, is the same number from any currency perspective, because there is only one market price of risk in a globally integrated market.

Per Exhibit 2.1 for the Australian dollar perspective: wA$ = 0.02; ![]() The global market index’s estimated FX exposure to the foreign currency index

The global market index’s estimated FX exposure to the foreign currency index ![]() is 0.15, and the foreign currency index’s estimated global beta

is 0.15, and the foreign currency index’s estimated global beta ![]() is 0.12. Verify the GRPA$ and XRPA$ estimates in Exhibit 2.2 assuming = 2.50.

is 0.12. Verify the GRPA$ and XRPA$ estimates in Exhibit 2.2 assuming = 2.50.

Answer: ![]() = 2.50[(0.119)2] = 0.0354, and GRP

= 2.50[(0.119)2] = 0.0354, and GRP ![]() = (1 − 2.50) [0.15(1 − 0.02)(0.106)2] = −0.0025. Therefore, GRPA$ = 0.0354 −0.0025 = 0.0329, or 3.29%.

= (1 − 2.50) [0.15(1 − 0.02)(0.106)2] = −0.0025. Therefore, GRPA$ = 0.0354 −0.0025 = 0.0329, or 3.29%. ![]() = (1 − 2.50)[(1 − 0.02)(0.106)2] = −0.0165, and

= (1 − 2.50)[(1 − 0.02)(0.106)2] = −0.0165, and ![]() = 2.50[0.12(0.119)2] = 0.0042. Therefore, XRPA$ = −0.0165 + 0.0042 = −0.0123, or −1.23%.

= 2.50[0.12(0.119)2] = 0.0042. Therefore, XRPA$ = −0.0165 + 0.0042 = −0.0123, or −1.23%.

Exhibit 2.1 ICAPM Statistical Parameter Estimates: Global Market Index and Foreign Currency Index

Global Market Price of Risk = 2.50 |

|||||

Statistical Parameter Estimation Period: 1999–2016 |

|||||

|

wC |

|

|

|

|

United States (dollar) |

0.379 |

0.159 |

0.062 |

1.23 |

0.18 |

Eurozone (euro) |

0.204 |

0.149 |

0.088 |

0.46 |

0.16 |

Japan (yen) |

0.130 |

0.188 |

0.095 |

1.36 |

0.35 |

China (yuan) |

0.070 |

0.158 |

0.042 |

1.67 |

0.12 |

Britain (pound) |

0.066 |

0.150 |

0.069 |

0.58 |

0.13 |

Canada (dollar) |

0.026 |

0.123 |

0.079 |

−0.04 |

−0.02 |

Australia (dollar) |

0.020 |

0.119 |

0.106 |

0.15 |

0.12 |

Taiwan (dollar) |

0.015 |

0.141 |

0.041 |

0.07 |

0.01 |

Switzerland (franc) |

0.015 |

0.167 |

0.080 |

1.01 |

0.23 |

India (rupee) |

0.013 |

0.138 |

0.066 |

0.20 |

0.04 |

Korea (won) |

0.012 |

0.129 |

0.097 |

0.23 |

0.13 |

Brazil (real) |

0.009 |

0.237 |

0.242 |

0.78 |

0.81 |

Mexico (peso) |

0.009 |

0.126 |

0.092 |

0.13 |

0.07 |

Sweden (krona) |

0.008 |

0.133 |

0.085 |

0.22 |

0.09 |

Hong Kong (dollar) |

0.005 |

0.159 |

0.038 |

2.00 |

0.11 |

Norway (krone) |

0.004 |

0.141 |

0.087 |

0.39 |

0.15 |

Denmark (krone) |

0.004 |

0.149 |

0.069 |

0.57 |

0.12 |

New Zealand (dollar) |

0.004 |

0.135 |

0.113 |

0.36 |

0.26 |

Singapore (dollar) |

0.004 |

0.139 |

0.036 |

−0.23 |

−0.02 |

South Africa (rand) |

0.003 |

0.164 |

0.153 |

0.57 |

0.50 |

Thailand (baht) |

0.001 |

0.146 |

0.065 |

0.50 |

0.10 |

Note in the boxed example problem that for the Australian dollar perspective, the global risk premium estimate, 3.29%, is lower than in US dollars, 5.92%, and the foreign currency index risk premium estimate, −1.23%, is also substantially lower than the one for the US dollar perspective, 0.81%. You will better understand these differences as we explore the ICAPM further in this and subsequent chapters. You will also learn why the examples assume a global market price of risk, Θ, of 2.50.

Exhibit 2.2 ICAPM Risk Premium Estimates: Global Market Index and Foreign Currency Index

Global Market Price of Risk = 2.50 |

||||||

Statistical Parameter Estimation Period: 1999–2016 |

||||||

|

|

|

GRPC |

|

|

XRPC |

United States (dollar) |

6.35% |

−0.43% |

5.92% |

−0.35% |

1.16% |

0.81% |

Eurozone (euro) |

5.54% |

−0.46% |

5.12% |

−0.92% |

0.88% |

−0.04% |

Japan (yen) |

8.84% |

−1.60% |

7.24% |

−1.18% |

3.09% |

1.91% |

China (yuan) |

6.23% |

−0.40% |

5.83% |

−0.24% |

0.72% |

0.48% |

Britain (pound) |

5.59% |

−0.39% |

5.20% |

−0.71% |

0.73% |

0.02% |

Canada (dollar) |

3.78% |

0.03% |

3.81% |

−0.92% |

−0.06% |

−0.98% |

Australia (dollar) |

3.54% |

−0.25% |

3.29% |

−1.65% |

0.42% |

−1.23% |

Taiwan (dollar) |

4.94% |

−0.01% |

4.93% |

−0.25% |

0.03% |

−0.22% |

Switzerland (franc) |

6.93% |

−0.96% |

5.97% |

−0.95% |

1.62% |

0.67% |

India (rupee) |

4.74% |

−0.12% |

4.62% |

−0.64% |

0.21% |

−0.43% |

Korea (won) |

4.14% |

−0.33% |

3.81% |

−1.41% |

0.55% |

−0.86% |

Brazil (real) |

14.09% |

−6.81% |

7.28% |

−8.69% |

11.46% |

2.77% |

Mexico (peso) |

3.97% |

−0.17% |

3.80% |

−1.25% |

0.28% |

−0.97% |

Sweden (krona) |

4.42% |

−0.24% |

4.18% |

−1.07% |

0.40% |

−0.67% |

Hong Kong (dollar) |

6.33% |

−0.42% |

5.91% |

−0.21% |

0.71% |

0.50% |

Norway (krone) |

4.99% |

−0.44% |

4.55% |

−1.13% |

0.74% |

−0.39% |

Denmark (krone) |

5.53% |

−0.41% |

5.12% |

−0.72% |

0.69% |

−0.03% |

New Zealand (dollar) |

4.55% |

−0.70% |

3.85% |

−1.92% |

1.16% |

−0.76% |

Singapore (dollar) |

4.83% |

0.04% |

4.87% |

−0.19% |

−0.07% |

−0.26% |

South Africa (rand) |

6.71% |

−1.99% |

4.72% |

−3.51% |

3.32% |

−0.19% |

Thailand (baht) |

5.31% |

−0.31% |

5.00% |

−0.63% |

0.52% |

−0.11% |

ICAPM and Cost of Capital

The traditional expression for asset i’s cost of capital in our ICAPM is the factor risk premium form shown in equation (2.1):

International CAPM (ICAPM)

Traditional Factor Risk Premium Form

![]()

In equation (2.1), ![]() and

and ![]() are asset i’s risk coefficients, where the prime (′) notation indicates that the risk coefficients are the partial coefficients in a multivariate regression of asset i’s return on two independent variables: (1) the global market index return, and (2) the foreign currency index return. (To simplify notation, we do not use a second subscript to denote G or X in the risk factors.) The interpretation of

are asset i’s risk coefficients, where the prime (′) notation indicates that the risk coefficients are the partial coefficients in a multivariate regression of asset i’s return on two independent variables: (1) the global market index return, and (2) the foreign currency index return. (To simplify notation, we do not use a second subscript to denote G or X in the risk factors.) The interpretation of ![]() and

and ![]() is like their standard beta and FX exposure counterparts,

is like their standard beta and FX exposure counterparts, ![]() and

and ![]() , except that

, except that ![]() and

and ![]() include adjustments for the systematic connection between the global market index and the foreign currency index.3

include adjustments for the systematic connection between the global market index and the foreign currency index.3

We now show by example that the ICAPM risk–return expression in equation (2.1) reconciles with a U.S. market index risk premium of 5.65%, using the 1999 to 2016 data and Θ = 2.50. Letting asset i be the U.S. local market index, the partial risk coefficient estimates using Excel regression and 1999 to 2016 data are: ![]() = 1.005 and

= 1.005 and ![]() = −0.353, where the U subscript denotes the U.S. equity index is asset i. Equation (2.1) says that the U.S. market risk premium should be 1.005[0.0592] − 0.353[0.0081] = 0.0565, or 5.65%.

= −0.353, where the U subscript denotes the U.S. equity index is asset i. Equation (2.1) says that the U.S. market risk premium should be 1.005[0.0592] − 0.353[0.0081] = 0.0565, or 5.65%.

The assumption of Θ = 2.50 for the chapter’s examples is for the deliberate purpose of “anchoring” the ICAPM illustrations to the 5.65% U.S. market risk premium estimate justified in the previous chapter.4 Of course, the choice of 5.65% for the U.S. market risk premium is arbitrary, but it is important to see how the various risk premium estimates, in the different currencies, are all linked by a specified global market price of risk.

Let GRPA$ = 3.29% and XRPA$ = −1.23%, per Exhibit 2.2. The Australian equity index’s partial risk coefficient estimates (using Excel regression and 1999 to 2016 data) are: ![]() = 0.689 and

= 0.689 and ![]() = −0.702. Assuming

= −0.702. Assuming ![]() = 3.50%, find the cost of equity and local market risk premium for the Australian equity index in Australian dollars using the traditional ICAPM risk–return expression in equation (2.1).

= 3.50%, find the cost of equity and local market risk premium for the Australian equity index in Australian dollars using the traditional ICAPM risk–return expression in equation (2.1).

Answer: Equation (2.1) says that the Australian equity index’s cost of equity is 0.035 + 0.689[0.0329] − 0.702[−0.0123] = 0.0663, or 6.63%. The Australian local equity market risk premium is 6.63% − 3.50% = 3.13%.

Equation (2.2) shows an alternative ICAPM risk–return relation that is equivalent to the traditional expression in equation (2.1), but uses standard risk coefficients rather than the partial ones:5

Standard Risk Coefficient Form

![]()

As before, ![]() is asset i’s required return in currency H, and

is asset i’s required return in currency H, and ![]() is the currency-H risk-free rate. Instead of the more complex partial risk coeffi-cients, the risk coefficients in equation (2.2) have the standard interpretation:

is the currency-H risk-free rate. Instead of the more complex partial risk coeffi-cients, the risk coefficients in equation (2.2) have the standard interpretation: ![]() is asset i’s (global) beta for the currency-H perspective, and

is asset i’s (global) beta for the currency-H perspective, and ![]() is asset i’s FX exposure to the foreign currency index for the currency-H perspective. The factor risk premiums in equation (2.2) are also not those in equation (2.1), but instead are

is asset i’s FX exposure to the foreign currency index for the currency-H perspective. The factor risk premiums in equation (2.2) are also not those in equation (2.1), but instead are ![]() and

and ![]() , the first components of GRPH and XRPH, respectively.

, the first components of GRPH and XRPH, respectively.

To illustrate the ICAPM risk–return expression in equation (2.2), again let asset i be the U.S. market index, and replace the i subscript with U. The U.S. market index’s global beta estimate, ![]() , is 0.939, and the U.S. market index’s estimated FX exposure to the foreign currency index,

, is 0.939, and the U.S. market index’s estimated FX exposure to the foreign currency index, ![]() , is 0.887 (per Exhibit 2.3). Using the

, is 0.887 (per Exhibit 2.3). Using the ![]() and

and ![]() estimates per Exhibit 2.2, equation (2.2) gives the U.S. market risk premium estimate:

estimates per Exhibit 2.2, equation (2.2) gives the U.S. market risk premium estimate: ![]() = 0.939[0.0635] + 0.887[−0.0035] = 0.0565, or 5.65%, as found using equation (2.1).

= 0.939[0.0635] + 0.887[−0.0035] = 0.0565, or 5.65%, as found using equation (2.1).

Assume that in Australian dollars the Australian equity market index has the standard risk coefficient estimates of ![]() = 0.603 and

= 0.603 and ![]() = −0.595, per Exhibit 2.3. Per Exhibit 2.2, assume

= −0.595, per Exhibit 2.3. Per Exhibit 2.2, assume ![]() = 3.54% and

= 3.54% and ![]() = −1.65%. Assume

= −1.65%. Assume ![]() = 3.50%. Find the cost of equity for the Australian equity market index and the Australian equity market risk premium, in Australian dollars, using the ICAPM risk–return expression in equation (2.2).

= 3.50%. Find the cost of equity for the Australian equity market index and the Australian equity market risk premium, in Australian dollars, using the ICAPM risk–return expression in equation (2.2).

Answers: The cost of equity, ![]() , is equal to 0.035 + 0.603[0.0354]−0.595[−0.0165] = 0.0662, or 6.62%. The Australian equity market risk premium is

, is equal to 0.035 + 0.603[0.0354]−0.595[−0.0165] = 0.0662, or 6.62%. The Australian equity market risk premium is ![]() = 0.0662 − 0.035 = 0.0312, or 3.12%. The answers reconcile with the previous boxed example answers, considering rounding of inputs.

= 0.0662 − 0.035 = 0.0312, or 3.12%. The answers reconcile with the previous boxed example answers, considering rounding of inputs.

The ICAPM traditional factor risk premium form in equation (2.1) is more well-known than the standard risk coefficient form in equation (2.2). However, the benefit of using equation (2.2) is the specification in terms of standard beta and FX exposure inputs, as opposed to the partial beta and FX exposure measures in equation (2.1). This feature makes equation (2.2) advantageous for analyses in subsequent chapters.

ICAPM Versus GCAPM

The ICAPM is a theoretically stronger international risk–return model than the GCAPM, but as you have seen, the ICAPM is more complex than the GCAPM. So, a natural question is how much difference does it make in required return estimates if one uses the simpler GCAPM instead of the more complex, but theoretically superior ICAPM.

Using the “correct” (ICAPM) global risk premium estimate in US dollars (5.92%), and the local U.S. market index’s global beta estimate, 0.939, the GCAPM estimate for the U.S. local market risk premium is 0.939[0.0592] = 0.0556, or 5.56%, which is reasonably close to the “correct” (ICAPM) estimate of 5.65%. For the Australian dollar perspective, on the other hand, if one uses the “correct” (ICAPM) global risk premium estimate in Australian dollars (3.29%), and the Australian local market index’s global beta estimate, 0.603, the GCAPM estimate for the Australian local equity market risk premium is 0.603[0.0329] = 0.0198, or 1.98%, which is 114 basis points below the “correct” (ICAPM) estimate, 3.12%, found in the last boxed example.

For 31 local equity market indexes, including 10 individual Eurozone countries and the Eurozone in aggregate (using the EMU Index), Exhibit 2.3 compares the ICAPM and GCAPM equity market risk premium estimates in local currency for the 1999 to 2016 data. Country Y’s ICAPM market risk premium estimate is based on equation (2.2), using the estimates for the country index’s global beta, ![]() , and FX exposure to the foreign currency index,

, and FX exposure to the foreign currency index, ![]() , as shown in Exhibit 2.3. The other inputs used in equation (2.2) are shown in Exhibit 2.1. Country Y’s GCAPM market risk premium estimate is equal to the country index’s global beta estimate times the local currency’s “correct” (ICAPM) global market risk premium estimate, GRPC, per Exhibit 2.2.

, as shown in Exhibit 2.3. The other inputs used in equation (2.2) are shown in Exhibit 2.1. Country Y’s GCAPM market risk premium estimate is equal to the country index’s global beta estimate times the local currency’s “correct” (ICAPM) global market risk premium estimate, GRPC, per Exhibit 2.2.

Exhibit 2.3 ICAPM vs. GCAPM Local Market Risk Premium Estimates

Global Market Price of Risk = 2.50 |

||||

Statistical Parameter Estimation Period: 1999–2016 |

||||

|

|

|

ICAPM |

GCAPM |

United States (dollar) |

0.939 |

0.887 |

5.65% |

5.56% |

Eurozone (euro) |

1.062 |

−0.156 |

6.03% |

5.44% |

Japan (yen) |

0.723 |

0.888 |

5.34% |

5.23% |

China (yuan) |

1.187 |

2.194 |

6.87% |

6.92% |

Britain (pound) |

0.830 |

0.112 |

4.56% |

4.31% |

Canada (dollar) |

0.848 |

−0.826 |

3.96% |

3.23% |

Australia (dollar) |

0.603 |

−0.595 |

3.12% |

1.98% |

Taiwan (dollar) |

0.924 |

−2.132 |

5.10% |

4.55% |

Switzerland (franc) |

0.668 |

0.398 |

4.25% |

3.99% |

India (rupee) |

0.800 |

−1.529 |

4.77% |

3.70% |

Korea (won) |

0.945 |

−0.889 |

5.16% |

3.60% |

Brazil (real) |

0.255 |

−0.186 |

5.22% |

1.86% |

Mexico (peso) |

0.964 |

−0.612 |

4.59% |

3.66% |

Sweden (krona) |

1.270 |

−0.527 |

6.18% |

5.31% |

Hong Kong (dollar) |

1.047 |

2.261 |

6.15% |

6.19% |

Norway (krone) |

0.960 |

−0.884 |

5.80% |

4.37% |

Denmark (krone) |

0.923 |

0.177 |

4.98% |

4.73% |

New Zealand (dollar) |

0.389 |

−0.346 |

2.43% |

1.50% |

Singapore (dollar) |

1.021 |

−2.111 |

5.34% |

4.98% |

South Africa (rand) |

0.526 |

−0.163 |

4.10% |

2.48% |

Thailand (baht) |

0.789 |

−1.509 |

5.13% |

3.94% |

Germany (euro) |

1.22 |

−0.08 |

6.84% |

6.26% |

France (euro) |

1.02 |

−0.14 |

5.76% |

5.20% |

Italy (euro) |

0.90 |

−0.37 |

5.33% |

4.62% |

Netherlands (euro) |

1.06 |

0.01 |

5.86% |

5.43% |

Belgium (euro) |

0.91 |

−0.18 |

5.22% |

4.67% |

Ireland (euro) |

0.99 |

0.15 |

5.36% |

5.08% |

Spain (euro) |

0.92 |

−0.42 |

5.48% |

4.71% |

Austria (euro) |

0.92 |

−0.66 |

5.70% |

4.71% |

Finland (euro) |

1.44 |

0.15 |

7.84% |

7.37% |

Portugal (euro) |

0.68 |

−0.39 |

4.11% |

3.47% |

Exhibit 2.3 shows that for three countries (in addition to the United States), the GCAPM gives a very close approximation to the “correct” (ICAPM) estimate of the country’s local equity market risk premium: Japan, China, and Hong Kong. Other countries for which the difference is under 30 basis points, and therefore where the GCAPM’s estimates may be a reasonable approximation to the ICAPM’s estimates include Britain, Switzerland, Denmark, and Ireland.

On the other hand, there are many countries where the difference between the GCAPM and “correct” (ICAPM) local market risk premium estimates is more than 60 basis points, and the difference is more than 100 basis points for eight countries: Australia, India, Korea, Brazil, Norway, South Africa, Thailand, and Austria.

Bear in mind that Country Y’s local equity market index represents Country Y’s “average stock.” The difference between the ICAPM and GCAPM cost of equity estimates for individual stocks may be higher than that for the “average stock.”

As a case in point, Exhibit 2.3 indicates the difference between the ICAPM and GCAPM risk premium estimates for the local British equity index is 25 basis points, yet the next boxed example problem shows that the difference between Rio Tinto’s ICAPM and GCAPM cost of equity estimates in British pounds is 80 basis points.

Assume that in British pounds Rio Tinto’s ordinary shares have standard risk coefficient estimates of ![]() = 1.27 and

= 1.27 and ![]() = −0.42. Per Exhibit 2.2, assume that

= −0.42. Per Exhibit 2.2, assume that ![]() = 5.59%,

= 5.59%, ![]() = −0.71%, and GRP£ = 5.20%. Assume

= −0.71%, and GRP£ = 5.20%. Assume ![]() = 3.50%. (a) Find the cost of equity in British pounds for Rio Tinto using the ICAPM risk–return expression in equation (2.2). (b) Compare the answer in (a) to the GCAPM cost of equity estimate.

= 3.50%. (a) Find the cost of equity in British pounds for Rio Tinto using the ICAPM risk–return expression in equation (2.2). (b) Compare the answer in (a) to the GCAPM cost of equity estimate.

Answers: (a) Rio Tinto’s cost of equity estimate with the ICAPM expression in equation (2.2) is ![]() = 0.035 + 1.27[0.0559] − 0.42[−0.0071] = 0.109, or 10.9%. (b) The GCAPM estimate is 0.035 + 1.27[0.0520] = 0.101, or 10.1%, which is 80 basis points lower than the ICAPM estimate.

= 0.035 + 1.27[0.0559] − 0.42[−0.0071] = 0.109, or 10.9%. (b) The GCAPM estimate is 0.035 + 1.27[0.0520] = 0.101, or 10.1%, which is 80 basis points lower than the ICAPM estimate.

An empirical study of ICAPM and GCAPM cost of equity estimates for individual U.S. stocks for the 1985 to 2012 period found an average cost of equity difference of only 32 basis points. This average difference is relatively small, especially considering the sample included many small companies. Thus, the study’s results indicate that the simpler GCAPM may provide an acceptable approximation to the more complex ICAPM for US dollar cost of equity estimates of U.S. companies.6 Although there is no empirical research yet that compares ICAPM and GCAPM cost of equity estimates for individual stocks of other countries and currencies, the results in Exhibit 2.3 suggest that GCAPM cost of equity estimates are not good approximations of ICAPM estimates, on average, for many countries.

An Asset’s Required Return in Different Currencies

Just as an asset’s rate of return is different from the perspective of different currencies, per equation (1.1a), an asset’s required rate of return, or cost of capital, is different from the perspective of different currencies. So, you must be careful to specify which currency you are using to express a cost of capital. Different cost of equity numbers in different currencies are separate ways to express the same cost of equity. This idea is the same as saying that a firm’s equity has only one value, but it is a different number when expressed in different currencies. That is, you can express a firm’s equity value either as $100 or Sf 160 given a spot FX rate of 1.60 Sf/$.

Despite being different numbers, a given asset’s cost of capital estimates in different currencies must be mutually consistent with each other. To better understand what this means, say an angel were to post online the true expected future cash flow per share for BHP Billiton, and the angel provides this information from both the Australian dollar and US dollar perspectives. BHP Billiton’s cost of equity in Australian dollars must be consistent with the cost of equity in US dollars in the following way: If the $/A$ FX rate is correctly valued and expected to be correctly valued in the future, the present (discounted) value of the expected cash flows in the Australian dollar perspective is equivalent at today’s spot FX rate to the present (discounted) value of the expected cash flows in the US dollar perspective.

The theory that underlies the ICAPM implicitly assures us that the estimates of a given asset’s cost of capital in different currencies are consistent with each other. However, the GCAPM does not give consistent cross-currency cost of capital estimates; the reason is technical and beyond the scope here to cover in detail.7

Summary Action Points

• The international CAPM (ICAPM) is theoretically superior to the GCAPM as a risk–return model.

• The GCAPM may provide cost of equity estimates that are reasonable approximations to ICAPM estimates from some currency perspectives, including the US dollar.

• The GCAPM may not provide cost of equity estimates that are reasonable approximations to ICAPM estimates from many non-US dollar perspectives.

Glossary

FX exposure: Sensitivity to changes in FX rates or an index of FX rates, like a beta but with the FX rate(s) replacing the market index.

Partial Risk Coefficients: Risk coefficients (beta and gamma) that are estimated through multiple regression and thus take into consideration the statistical connection of the risk factors.

Standard Risk Coefficients: Risk coefficients (beta and gamma) that are estimated through univariate regression and thus do not take into consideration the statistical connection of the risk factors.

International CAPM (ICAPM): A risk-return model in internationally integrated financial markets in which the global market index replaces the traditional CAPM market index and which has one or more foreign exchange FX risk factors.

Problems

1. Per Exhibit 2.1 for the Swedish krona perspective, ![]()

![]() , the global market index’s estimated FX exposure to the foreign currency index

, the global market index’s estimated FX exposure to the foreign currency index ![]() is 0.22, and the foreign currency index’s estimated global beta

is 0.22, and the foreign currency index’s estimated global beta ![]() is 0.09. Verify (approximately) the GRPSk and XRPSk estimates in Exhibit 2.2 for Θ = 2.50.

is 0.09. Verify (approximately) the GRPSk and XRPSk estimates in Exhibit 2.2 for Θ = 2.50.

2. Assume that in Swedish krona the Sweden equity market index has the standard risk coefficient estimates: ![]() = 1.27 and

= 1.27 and ![]() = −0.527, per Exhibit 2.3. Per Exhibit 2.2, let

= −0.527, per Exhibit 2.3. Per Exhibit 2.2, let ![]() = 4.42% and

= 4.42% and ![]() = −1.07%. Use the ICAPM in equation (2.2). (a) Find the market risk premium for the Sweden equity index in Swedish kronor. (b) Assuming

= −1.07%. Use the ICAPM in equation (2.2). (a) Find the market risk premium for the Sweden equity index in Swedish kronor. (b) Assuming ![]() = 2.50%, find the cost of equity for the Sweden equity index in Swedish kronor.

= 2.50%, find the cost of equity for the Sweden equity index in Swedish kronor.

3. Let GRPSk = 4.18% and XRPSk = −0.67%, per Exhibit 2.2. Using Excel regression and 1999 to 2016 data, the Sweden equity market index’s partial risk coefficient estimates are: ![]() = 1.35 and

= 1.35 and ![]() = −0.82. Use the ICAPM in equation (2.1). (a) Find the market risk premium for the Sweden equity index in Swedish kronor. (b) Assuming

= −0.82. Use the ICAPM in equation (2.1). (a) Find the market risk premium for the Sweden equity index in Swedish kronor. (b) Assuming ![]() = 2.50%, find the cost of equity for the Sweden equity index in Swedish kronor.

= 2.50%, find the cost of equity for the Sweden equity index in Swedish kronor.

4. Verify the GCAPM estimate of the Sweden equity market risk premium of 5.31%, per Exhibit 2.3.

5. Per Exhibit 2.1 for the Japanese yen perspective, w¥ = 0.13, ![]() = 0.188,

= 0.188, ![]() = 0.095, the global market index’s estimated FX exposure to the foreign currency index

= 0.095, the global market index’s estimated FX exposure to the foreign currency index ![]() is 1.36, and the foreign currency index’s estimated global beta

is 1.36, and the foreign currency index’s estimated global beta ![]() is 0.35. Verify (approximately) the GRP¥ and XRP¥ estimates in Exhibit 2.2 for Θ = 2.50.

is 0.35. Verify (approximately) the GRP¥ and XRP¥ estimates in Exhibit 2.2 for Θ = 2.50.

6. Let GRP¥ = 7.24% and XRP¥ = 1.91%, per Exhibit 2.2. Using Excel regression and 1999 to 2016 data, the Japan equity index’s partial risk coefficient estimates are: ![]() = 0.784 and

= 0.784 and ![]() = −0.182. Use the ICAPM in equation (2.1). (a) Find the market risk premium for the Japanese equity index in Japanese yen. (b) Assuming

= −0.182. Use the ICAPM in equation (2.1). (a) Find the market risk premium for the Japanese equity index in Japanese yen. (b) Assuming ![]() = 1%, find the cost of equity for the Japan equity index in Japanese yen.

= 1%, find the cost of equity for the Japan equity index in Japanese yen.

7. Assume that in Japanese yen the Japan equity market index has the standard risk coefficient estimates of ![]() = 0.723 and

= 0.723 and ![]() = 0.888, per Exhibit 2.3. Per Exhibit 2.2, assume

= 0.888, per Exhibit 2.3. Per Exhibit 2.2, assume ![]() = 8.84% and

= 8.84% and ![]() = −1.18%. Use the ICAPM in equation (2.2). (a) Find the market risk premium for the Japanese equity index in Japanese yen. (b) Assuming

= −1.18%. Use the ICAPM in equation (2.2). (a) Find the market risk premium for the Japanese equity index in Japanese yen. (b) Assuming ![]() = 1%, find the cost of equity for the Japan equity index in Japanese yen.

= 1%, find the cost of equity for the Japan equity index in Japanese yen.

8. Verify the GCAPM estimate of the Japan equity market risk premium of 5.23%, per Exhibit 2.3.

Answers to Problems

1. ![]() = 2.50(0.133)2 = 0.0442, and

= 2.50(0.133)2 = 0.0442, and ![]() = (1 − 2.50)(1 − 0.008)(0.22)(0.085)2 = −0.0024. Therefore, GRPsk = 0.0442 − 0.0024 = 0.0418, or 4.18%.

= (1 − 2.50)(1 − 0.008)(0.22)(0.085)2 = −0.0024. Therefore, GRPsk = 0.0442 − 0.0024 = 0.0418, or 4.18%. ![]() = (1 − 2.50)(1 − 0.008)(0.085)2 = −0.0107, and

= (1 − 2.50)(1 − 0.008)(0.085)2 = −0.0107, and ![]() = 2.50(0.09)(0.133)2 = 0.0040. Thus, XRPsk = −0.0107 + 0.0040 = −0.0067, or −0.67%.

= 2.50(0.09)(0.133)2 = 0.0040. Thus, XRPsk = −0.0107 + 0.0040 = −0.0067, or −0.67%.

2. (a) Per equation (2.2), the Sweden equity index’s market risk premium in Swedish kronor is 1.27[0.0442] − 0.527[−0.0107] = 0.0618, or 6.18%. (b) The cost of equity in kronor for the Sweden equity index is 2.50% + 6.18% = 8.68%.

3. (a) Per equation (2.1), the Sweden equity index’s market risk premium in Swedish kronor is 1.35[0.0418] − 0.82[−0.0067] = 0.0619, or 6.19%. (b) The cost of equity in kronor for the Sweden equity index is 2.50% + 6.19% = 8.69%, which is slightly different from the previous answer due to rounding.

4. 1.27[0.0418] = 0.0531, or 5.31%, which is 87 basis points lower than the ICAPM estimate of 6.18%.

5. ![]() = 2.50(0.188)2 = 0.0884, and

= 2.50(0.188)2 = 0.0884, and ![]() = (1 − 2.50)(1 − 0.13)(1.36)(0.095)2 = −0.016. GRP¥ = 0.0884 − 0.016 = 0.0724, or 7.24%.

= (1 − 2.50)(1 − 0.13)(1.36)(0.095)2 = −0.016. GRP¥ = 0.0884 − 0.016 = 0.0724, or 7.24%. ![]() = (1 − 2.50)(1 − 0.13)(0.0.095)2 = −0.0118, and

= (1 − 2.50)(1 − 0.13)(0.0.095)2 = −0.0118, and ![]() = 2.50(0.35)(0.188)2 = 0.0309. Thus, XRP¥ = −0.0118 + 0.0309 = 0.0191, or 1.91%.

= 2.50(0.35)(0.188)2 = 0.0309. Thus, XRP¥ = −0.0118 + 0.0309 = 0.0191, or 1.91%.

6. (a) Per equation (2.1), the Japan equity index’s market risk premium in Japanese yen is 0.785[0.0724] − 0.182[0.0191] = 0.0534, or 5.34%. (b) The cost of equity in yen for the Japan equity index is 1% + 5.34% = 6.34%.

7. (a) Per equation (2.2), the Japan equity index’s market risk premium in Japanese yen is 0.723[0.0884] + 0.888[−0.0118] = 0.0534, or 5.34%, which reconciles with problem 6, using equation (2.1). (b) The cost of equity in yen for the Japan equity index is 1% + 5.34% = 6.34%.

8. 0.723[0.0724] = 0.0523, or 5.23%, which is 11 basis points lower than the ICAPM estimate of 5.34%.

1. Discuss the pros and cons of using the ICAPM as a risk–return model.

2. The GCAPM is an acceptable risk–return model from some currency perspectives but not others. Discuss.