Chapter Sixteen

Selecting the Arm’s Length Price in Japan

In Japan, the taxpayer’s selection of the arm’s length price is an important facet of its transfer pricing regime. The arm’s length price selection in Japan is particularly onerous because the transfer pricing provisions contain two specific factors:

BACKGROUND

The National Tax Agency (NTA) of Japan issued its Transfer Pricing Administrative Guidelines in 2001 and amended these Administrative Guidelines to reflect 2007 litigation. The NTA, to supplement these Administrative Transfer Pricing Guidelines, issued its Reference Case Studies on the Application of Transfer Pricing Taxation (hereafter Reference Case Studies). These “cases,” or, more technically “examples,” provide an analysis of many transfer pricing issues a multinational taxpayer might face, 26 examples in all:

DEMONSTRATING THE SELECTION OF ARM’S LENGTH PRICE

The Reference Case Studies specifically examine nine method selection examples within Section 1:

- Case 1: Comparable uncontrolled price method

- Case 2: Resale price method

- Case 3: Cost plus method

- Case 4: Methods consistent with the comparable uncontrolled price method

- Case 5: Methods equivalent to methods that are consistent with the cost plus method

- Case 6: Use of the transactional net margin method

- Case 7: Use of the contribution profit split method

- Case 8: Use of the residual profit split method

- Case 9: Adjustments for differences

SELECTION OF THE METHOD OF CALCULATION OF ARM’S LENGTH PRICE

The Reference Case Studies first examine selection of the method of calculation of arm’s length price:

CASE 1: USE OF THE COMPARABLE UNCONTROLLED PRICE METHOD

The schematic of the business relations is:

- Japanese corporation P is a distributor of Products A and B.

- Corporation P established Corporation S in Country X ten years before to distribute Product A.

- Corporation P purchases Product A and purchases Product B to different intermediaries.

- Corporation P sells Product A to S, a foreign-related person.

- S sells Product A to 200 third-party retailers.

- Corporation P sells Product B to T, a third party.

- T sells Product B to third-party wholesalers.

Functions and Activities

Company P classifies Product A differently from Product B in terms of model numbers, but both products are similar in terms of properties, construction, functions, and so forth.

The functions performed by:

- Company P in the sale of Product A to Company S

- Company P in the sale of Product B to Company T

are:

- The purchase of the inventory of Product A

- The purchase of the inventory of Product B

and:

- The sale of the Product A inventory to Company S

- The sale of the Product B inventory to Company T

Note that the phraseology in the Reference Case Studies is misleading. The Reference Case Studies refer to “the sale of these inventories to Company S and Company T,” thus erroneously suggesting that Company P is selling both Product A and Product B to Company S and Company T.

Company P engages in no unique activities. Further, there are no differences in function between the sale of the product A inventory to Company S and the sale of the product B inventory to Company T. Neither the sale of the Product A inventory to Company S nor the sale of the Product B inventory to Company T makes use of trademarks or other functions.

Note the lack of contract differences between the sale of the Product A inventory to Company S and the sale of the Product B inventory to Company T:

- Both transactions have the same market level (e.g., wholesale or retail).

- Both transactions have substantially the same volume.

- The terms of the contracts for both transactions are the same as to delivery terms, payment terms, product warranties, and conditions for returns.

- The transaction price differs between Product A and Product B.

Treatment of Case 1 Facts for Transfer Pricing Taxation Purposes

Japan’s Act on Special Measures Concerning Taxation (ASMT) provides that traditional transaction pricing methods have preference in selecting an arm’s length price.1 The examination of Case 1 facts produces these findings:

- Product A and Product B are of the same type of product in terms of properties, construction, functions, and so forth despite the fact the Company P classified the products into different product categories.

- Both Company S and Company T are wholesale traders, selling products to retailers in Country X. There are no differences in market level between these two transactions.

- The two transactions have the same volume and have the same contract terms. There are no differences in the volume of the goods or transactional contract terms.

- Company P has the same business strategies toward Product A and toward Product B.

- There were no differences in Company P’s role and functions as to these transactions. The parties made no use of intangible properties.

- Both Company S and Company T are located in Country X. As such, the market conditions are the same. There are no government regulations on Product A or Product B.

Selection of the Method for Determining the Arm’s Length Price

The NTA would have the taxpayer first determine traditional transaction methods to determine the arm’s length price. The NTA would apply the comparable uncontrolled price method2 to the sales of inventories of Product A that Company P sells to Company S and the sales of Product B that Company P sells to Company T, treating these transactions as being comparable transactions.

Explanation of the Comparable Uncontrolled Price Method

Part 1. As a general matter, the NTA requires the taxpayer to select a “reasonable method” that is in “keeping with the particular facts” and in compliance with the requirements that law lays down. Such a taxpayer, when selecting the method of calculation of the arm’s length price, must first consider the applicability of the traditional transaction methods. Such traditional transaction methods include methods equivalent to the traditional transaction methods. The taxpayer is to explain the difference in the “explanation” section.

The judgment as to the applicability of the traditional transaction methods must conform to the specific facts. The taxpayer can rely on an internal comparable transaction or on an external comparable transaction based on:

Public information includes the last three of the preceding four categories.

Six ASMT Directives become relevant:

The third ASMT, ASMT Directive 66-4(2)-3, Factors to Consider when Selecting Comparable Transactions, is most specifically relevant as to the comparable uncontrolled price method, especially through examining the factors contained on that list.

Foreign-related transaction might involve intangible properties. In the event that the foreign-related transaction does involve intangible properties, the taxpayer should consider comparability based particularly on ASMT Directive 66-4(2)-3-(8), Intangible Properties Used by the Seller or Buyer. Administrative Guideline 3-2 specifies that in such intangible property cases, the taxpayer is to consider the similarity of the intangible property in terms of type, scope, mode of use, and so forth when selecting comparable transactions.

Part 2. The taxpayer is to consider the application of the traditional transaction methods. When the taxpayer does consider the application of the traditional transaction methods, the Reference Case Studies suggest that it is “often comparatively simple” to determine whether internal comparable transactions engaged in by a corporation or by a foreign-related person qualify as comparable transactions, as described in Part 1 above, because the corporation or the foreign-related person will have the information on these transactions.

In contrast, the Reference Case Studies suggest that cases can exist where the taxpayer does not have sufficient information to make a comparability judgment. Such a taxpayer may need to rely on publicly available information pertaining to external comparable transactions engaged in by a corporation and third parties other than foreign-related parties.

In some cases, the resale price method or the cost plus method uses the profit margin calculated from gross sales of comparable transactions. In situations in which the taxpayer determines the gross profitability of those transactions, it is often not possible to obtain sufficient information concerning transactions deemed comparable with the foreign-related transactions. This failure is due to differences in the systems for the disclosure of corporate financial data in different countries in these cases:

- When applying the resale price method when the foreign-related person is the buyer of the inventories involved in a foreign-related transaction

- When applying the cost plus method when the foreign-related person is the seller of inventories in foreign-related transactions

The Reference Case Studies caution that the taxpayer might not have the access to the data required to examine comparability from financial data at the individual enterprise level on the basis of publicly available data. These data might not be available in cases where an enterprise does business in a number of segments unless the taxpayer can extract financial data as to a specified segment from the overall data.

The Reference Case Studies thus recognize that it might not be possible for the taxpayer to apply the traditional transaction methods, especially where the taxpayer cannot obtain the information it requires to determine whether transactions qualify as comparable transactions in applying the traditional transaction methods. The Reference Case Studies state that the taxpayer should undertake the following procedure:

- The method of application might be consistent with traditional transaction methods, ASMT Article 66-4(2), Item 1(d).

- Other methods prescribed in the ASMT Cabinet Order, or methods equivalent to such methods under Item 2(b), above.

- See Part 3 and Part 4, below, regarding methods consistent with the traditional transaction methods.

- See the following cases prescribed in the ASMT Cabinet Order:

- Case 6—transactional net margin method

- Case 7—contribution profit split method

- Case 8—residual profit split method

The Reference Case Studies recommends that the taxpayer verify the validity of the results of its calculations using these transactions as necessary, doing so to identify transactions having a certain degree of comparability. The Reference Case Studies would apply these verification rules even where the taxpayer cannot select comparable transactions for the application of the traditional transaction methods and when the taxpayer determines the arm’s length price by a method other than the traditional transaction methods.

Part 3. The Reference Case Studies recognize that the taxpayer might apply the traditional transaction methods. The Reference Case Studies recognize legal provisions that are consistent with each of the traditional transaction methods. These methods are considered to leave the way open to employing reasonable methods suited to the content of the transactions. This rule contains a proviso that these methods do not diverge from the concept behind the traditional transaction methods.

The Reference Case Studies recognize that there may be cases in which the taxpayer cannot easily find comparable foreign-related transactions when applying the traditional transaction methods as prescribed by law. The Reference Case Studies do recognize, though, that there are instances in which it is possible to select comparable transactions by using “reasonable similar methods of calculation.” These reasonable similar methods of calculation can focus on the various forms of these transactions, or the taxpayer can determine the arm’s length price by adopting “reasonable transactions” as comparable transactions.

The Reference Case Studies recognize that the above-mentioned transfer pricing methods allow a wider choice of comparable transactions than do the traditional transaction methods. As a result, the taxpayer must consider comparability, bearing in mind the possibility of applying these transfer pricing methods in a manner consistent with the traditional transaction methods.

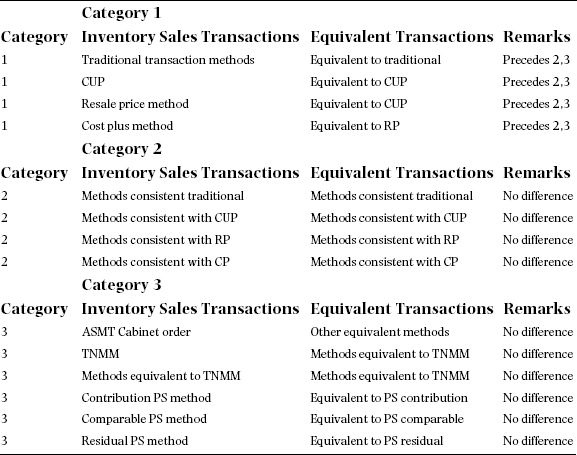

The Reference Case Studies provide five examples of transfer pricing methods that are “consistent with” the traditional transaction methods:

Administrative Guideline 3-3 permits the taxpayer to use the average price or profit margin or similar amount of these transactions when calculating the arm’s length price in the case of multiple comparable transactions deemed to be equivalently similar. The next table illustrates inventory sales transactions and equivalent transactions.

Priority of Methods for Calculating the Arm’s Length Price

Part 4. Japan does not permit a relaxation of the comparability requirements for comparable transactions when applying the traditional transaction methods as to ascertaining methods that are consistent with the traditional transaction methods. The ASMT Directive 66-4(2)-3 as to the similarity of factors does not negate the comparability requirements. The taxpayer cannot use transactions that do not meet these comparability requirements as being comparable transactions when applying methods that are consistent with the transaction methods.

Part 5. The Reference Case Studies find it necessary to draw taxpayers’ attention to these points: The underlying purpose is the acquiring of information concerning the grounds for determining the transaction prices and other ordinary transaction prices. The taxpayer must consider this information together with information on other matters, including the functions performed by the counterpart foreign-related parties as to these transactions.

The tax authorities need this information to ensure the “smooth and proper administration of transfer pricing taxation.” The tax authorities are concerned with the validity of the transfer price, as various factors determine that price. These points apply:

- The taxpayer, upon the request from the tax authority, must promptly present or submit the books of account or other documents that the tax authority requires to calculate the arm’s length price that the taxpayer selected when calculating the arm’s length price. If the taxpayer fails to meet the preceding compliance requirement, the tax authority has the power to estimate the taxpayer’s taxation, undertaking this action pursuant to ASMT Article 66-4(7) and ASMT Article 66-4(9).

- Taxpayers are obligated to acquire the books of account and other documents kept by foreign-related persons, as the tax authority requires, to calculate the arm’s length price in transfer pricing examinations. Taxpayers are to promptly present or submit the materials that the tax authority requests, in order to calculate the arm’s length price. Such taxpayers will be considered having met the conditions for applying the estimated tax amount requirements.

The tax authorities can inspect documents and other materials, as set forth in Administrative Guidelines 2-4, that form the basis of the taxpayers’ final tax returns. The tax authorities can request the submission of the necessary materials if the results that the taxpayer produces are not found by the tax authorities to be the arm’s length price. The tax authorities are to take care to fully explain to the taxpayer the reasons why the results found by the tax authorities are not the arm’s length price. The tax authorities are to explain the details of the adjustments rather than presenting the taxpayer with examination findings with a view toward achieving the taxpayer’s understanding.

Part 6. Taxpayers should make efforts to ascertain whether comparable transactions do exist in applying the traditional transaction methods, and should extend the effort to acquire “regular information” to the extent that this information is “normally available,” and should take this information into consideration.

Taxpayers are to undertake the process of selecting comparable transactions in applying the traditional transaction methods. Certain constraints can apply in compiling the necessary information. Such constraints include the lack of publicly available information, and the location of the information being overseas.

The Reference Case Studies provide an analysis of the “typical steps” in the process of selecting comparable transactions. Nevertheless, despite determining these steps as being “typical,” the Reference Case Studies treat this process as being mandatory.

Comparable Transaction Process

The Japanese tax authorities enumerate data the multinational enterprise or the tax administration will need in undertaking the comparable transaction process:

- Transactions deemed comparable with foreign-related transactions:

- Internal information—materials of the corporation or on the foreign-related person on these transactions

- External information—corporate databases

- External information—industry information for business associations, and so forth

- External information—other information

- Information the tax authorities obtain from questioning and inspection of other companies in the same line of business, ASMT Article 66-4, Paragraph 9

- Uncontrolled transactions—Are the transactions between unrelated parties?

- Availability of data—Are price data or are the data for calculating the profit margin available for each transaction?

Typical factors the taxpayer is to consider:

- Type of inventory, the content of the services, and so forth. Are the physical characteristics of the inventories and the nature of the services involved in the same or similar foreign-related party transactions?

- Market level. Are we concerned about a retailer or wholesaler, or a primary or secondary wholesaler?

- Volume and time of transactions. Do the transactions differ in volume or differ in timing?

- Contract terms. Are there any differences in terms of trade, payment terms, conditions for returns, or conditions regarding contract renewal?

- Functions performed and risks assumed by the buyer or by the seller. Are there any differences in the functions of the seller or of the buyer? These differences could include research and development (R&D), marketing, after-sales service, and so forth.

- Intangible properties the seller or the buyer uses. Are intangible properties used by the seller or by the buyer in these transactions?

- Business strategy and the timing of the market entry of the seller or of the buyer. Are there any differences in terms of business strategy? “Business strategy” means the policy toward market development and penetration. Are there any differences in terms of the timing of market entry?

- Status of government regulation and markets. Are there any differences in governmental regulation (i.e., price regulation), market size, competition, and so forth affecting prices and profit margins?

- Special circumstances. Are there any special circumstances that dictate that transactions might not be regarded as comparable, such as a bankruptcy situation?

The final result is to achieve comparable transactions.

CASE 2: USE OF THE RESALE PRICE METHOD

Consider the next fact pattern that leads to the conclusion that the resale price method is the applicable transfer pricing method.

Transaction Itself

Here are basic facts:

- Foreign-related person P purchases raw materials and so forth in Country X.

- Foreign-related person P manufactures product A in Country X.

- Foreign-related person P sells product A to Japanese corporation S as being the sole import agent.

- Japanese Corporation S sells product A to about a dozen third-party companies as agents.

Comparable Transaction

Here is the information as to the comparable transaction:

- Independent third parties purchase raw materials and so forth in Country X.

- Independent third parties manufacture Product B in Country X. The schematic prepared by the Reference Case Studies erroneously refers to Product A rather than to Product B at this phase of the schematic.

- Independent third parties sell Product B to Japanese Corporation T as being the sole import agent.

- Japanese Corporation T sells Product B to third parties as agents.

Additional Facets of the Transactions

Here are the additional facets as to the transactions:

- Japanese Corporation S is a distributor of Product A in Japan.

- Corporation P, located in Country X, is Company S’s parent company.

- Corporation P manufactures and distributes Product A in Country X.

- Company S imports product A as Company P’s sole import agent.

- Company S sells Product A to some ten third-party agents in Japan.

- Company S does not engage in unique or original advertising or sales promotion activities.

- Company S does not make use of its own trademarks or of such other properties in its distribution activities.

State of the Japanese Market

Approximately a dozen manufacturers make products that compete with Product A, and these manufacturers have entered the Japanese market. Five of these manufacturers are sole import agents and file financial statements that are openly accessible. These sole import agents provide additional information, including information from the companies’ Web sites, and market researchers publish analysis as well.

The taxpayer reviews the preceding materials and determines that Company T is a reseller of products imported from a third-party foreign manufacturer to third-party agents in Japan. Company T does not engage in any other business. Company T sells Product B, which is a product similar to Product A in terms of its properties, construction, and function. The taxpayer found that Company T is similar to Company S in terms of sales, market level, and sales functions, such as advertising, sales promotion, after-sales service, packing, and delivery. The taxpayer found that Company T does not use its own trademarks or other such properties in its distribution activities.

Applicability of the Traditional Transaction Methods

The Japanese tax authorities give preference to the traditional transaction methods when selecting the method of calculation of the arm’s length price pursuant to ASMT Article 66-4(2), Item 1. An examination of comparable transactions, made in accordance with ASMT Directive 66-4(2)-1, ASMT Directive 66-4(2)-3, and other relevant provisions, produced these findings:

- The resale price method might potentially be viable, among the traditional transaction methods, because Company S resells Product A that Company S purchases from third parties. Company S has access to the financial data to apply the resale price method from publicly available information pertaining to Company T.

- Product B, imported from a third party from Company T and sold by Company T to agents in Japan, is strongly similar to Product A. Company T is generally similar to Company S in terms of its functions as a reseller, the scale of the transactions, market conditions, and so forth.

Section of the Method of Calculating the Arm’s Length Price

The taxpayer found that it can use similar Product B, imported from a foreign third party, as a comparable transaction to Product A that Company S buys from Company P. Based on this situation, the taxpayer found that, among the traditional transaction methods, it is appropriate to apply the resale price method to Company S pursuant to ASMT Article 66-4(2), Item 1(b) to calculate the arm’s length price. Here S was the buyer of inventories involved in the foreign-related transaction. See the explanation to Case 1 regarding notes to consider when applying the applicability of the traditional transaction methods, including methods equivalent to the transaction methods, and in judging whether transactions correspond to comparable transactions.

CASE 3: USE OF THE COST PLUS METHOD

In this case, the taxpayer found, after considering the applicability of the traditional transaction methods, that the cost plus method was appropriate.

- Japanese Corporation P purchases Product A and Product B.

- Japanese Corporation P then separately sells Product A and Product B.

- Japanese Corporation P’s sales of Product A are to foreign-related person S, located in Country X.

- Japanese Corporation P’s sales of Product B are to third-party T, an agent, in Country X.

- Foreign-related party S, having purchased Product A from Japanese Corporation P, then sells Product A to approximately 200 third-party retailers.

- Third-party T, having purchased Product B from Japanese Corporation P, then sells Product B as agent to third-party retailers.

Explanation of the Activities

These are business activities that the companies undertake:

- Japanese Corporation P is a distributor of Product A and Product B.

- Japanese Corporation P established Corporation S in Country X as a subsidiary ten years ago to distribute Product A.

- Company P sells Product A to Company S.

- Company S then sells Product A to approximately 200 third-party retailers located in Country X.

- In the same time frame, Company P sells Product B to agent T, a third-party company located in Country X.

- Company T sells Product B to retailers located in Country X.

- Product B has a somewhat different specification from Product A, but the two products are similar in terms of properties, construction, function, and so forth.

- The volume of Product A that Japanese Corporation P sells to foreign-related person S is about the same as the volume of Product B that Japanese Corporation P sells to third-party T as agent.

- Japanese Corporation P performs the same functions for Product B as for Product A: purchasing Product A, selling Product A to foreign-related party S, purchasing Product B, selling Product B to third-party T as agent.

- Japanese Corporation P is not engaged in unique activities.

- Japanese Corporation P does not use trademarks or other such properties.

- Japanese Corporation P performs the same functions for the sales transaction with Company S as with the sales transaction with Company T.

- The terms and conditions are identical except as to price:

- P’s sales of Product A to Company S

- P’s sales of Product B to Company T

- The terms and conditions of the preceding sales contracts are identical as to delivery terms, payment terms, product warranties, and return conditions.

Treatment of the Cost Plus Method

The Japanese transfer pricing provisions give preference to the traditional transfer pricing methods when selecting an arm’s length price pursuant to ASMT Article 66-4(2), Item 1, or an examination of comparable transactions in accordance with ASMT Directive 66-4(2)-1 and Directive 66-4(2)-3 and other relevant provisions.

- Product A and Product B have similar properties, constructions, functions, and so forth, and are deemed to be similar inventories.

- Company S and Company T are both wholesale traders, selling products to retailers in Country X. There are deemed to be no differences in the market level concerning P’s sales to Company S and P’s sales to Company T.

- The two transactions are substantially the same in volume and in contract terms.

- There are no differences in Company P’s business strategies toward Product A and Product B.

- There are no differences in P’s role and functions as to these transactions.

- The parties make no use of intangible properties.

- The market conditions are the same as both Company S and Company T are located in Country X.

- There are no governmental regulations on Product A or Product B.

The taxpayer determined that Company P’s sale of Product B to Company T could be used as the comparable transaction for the sale of Company P’s sale of Product A to Company S. The seller of the inventories involved foreign-related transactions. The taxpayer looked to traditional transaction methods to determine the arm’s length price and determined that it was appropriate to apply the cost plus method to Company P pursuant to ASMT Article 66-4(2), Item 1(c). See the explanation for Case 1 as to the points to note regarding the applicability of traditional transaction methods, including methods that are equivalent to the traditional transaction methods, in judging whether transactions correspond to comparable transactions.

CASE 4: METHODS CONSISTENT WITH THE COMPARABLE UNCONTROLLED PRICE METHOD

Case 4 examines the situation in which the taxpayer considered applying the traditional transaction methods or methods equivalent to the traditional transaction methods but determined that it could not do so.

Nevertheless, the taxpayer found that it was appropriate to apply a method that is “consistent with” the comparable uncontrolled price method or is “consistent with” a method that is consistent with the comparable uncontrolled price method. Case 4 describes two such situations, a sale of inventories fact pattern and a loan transaction fact pattern.

Schematic

The schematic for the inventory fact pattern indicates:

- Company S, in Country X, a foreign-related person to Japanese Corporation P, supplies raw material “a” to Japanese Corporation P in Japan.

- Japanese Corporation P, a manufacturer and distributor of Product A, obtains raw material “a” from related party S in Country X, manufactures Product A, and sells Product A to third-party agents in Japan.

- Japanese Corporation P previously established Company S in Country X ten years ago as a subsidiary to supply raw material “a” for Product X.

- Company S sells its entire output of raw material “a” to Japanese Corporation P.

- Japanese Corporation P manufactures Product A and sells Product A to third-party agents in Japan.

- Japanese Corporation P receives no supplies of raw material “a” from any source except from Company S.

- Raw material “a,” which contains Product A, is sold worldwide on the commodity exchanges.

- The commodity exchanges reflect a quoted price for raw material “a.”

Applicability of Traditional Transaction Methods

Japanese transfer pricing gives preference to the traditional transaction methods when selecting a method of calculation that gives rise to the arm’s length price pursuant to ASMT Article 66-4(2), Item 1. An examination of comparable transactions the taxpayer undertakes in accordance with ASMT Directive 66-4(2)-1 and ASMT Directive 66-4(2)-3 and other relevant provisions produces these findings:

- Japanese Company P receives no supply of raw material “a” except from Company S.

- Company S supplies its entire output of raw material “a” to Japanese Company P.

- It is therefore not possible to find any comparable transactions in applying the comparable uncontrolled price method.

- It also was not possible to find any comparable transactions from publicly available information in applying the comparable uncontrolled price method.

- It is not feasible to apply the resale price method in this situation because Company P performed the manufacturing function in producing Product A from raw material “a.”

- Of the three traditional transaction methods, one possible option would be to apply the cost plus method to Company S. The comparable transactions in such a case would be the uncontrolled transactions in Country X. The taxpayer cannot apply the cost plus method because Japanese Company P and Company S cannot obtain sufficient information to adjust for such differences. Company S would have needed to adjust for profit margin differences for the gross profit on sales.

Based on the foregoing analysis, the taxpayer determines that it could not apply the traditional transaction methods. The taxpayer then considers the application of methods that are “consistent with” the traditional transaction methods as prescribed in ASMT 66–4(2), Item 1(d). The taxpayer concluded that worldwide transactions are present on commodity exchanges, that there exists a market price for raw material “a,” and that the taxpayer could apply the CUP after adjusting for differences in particular transaction terms, such as for transportation costs, to calculate the arm’s length price. See ASMT Article 66-4(2), Item 1(d).

Explanation

At the outset, the reader should consider the applicability of the traditional transaction methods, including methods equivalent to the traditional transaction methods, and in judging whether the transactions correspond to comparable transactions, as reflected in the explanation of Case 1. If there are no transactions that exist between unrelated persons that are comparable to the foreign-related transaction and the taxpayer cannot apply the traditional transaction methods, it might be possible to apply a method that is “consistent with” the traditional transaction methods. Objective and realistic indicators of variables may exist, such as market prices (e.g., the quoted market price in this instance). These methods may be available using these transactions as comparable transactions in order to calculate the arm’s length price.

Money-Lending Transactions

The schematic indicates that these transactions have taken place:

- Japanese Corporation P lends funds to foreign-related person S in Country X.

- The Japanese Corporation P–foreign-related person S loan is for ten years at 3% interest per annum.

- Bank T loans funds to Bank T at a 0.7% spread.

- Both Japanese Corporation P and foreign-related person S manufacture and sell Product A.

- There are no bank transactions.

- Japanese Corporation P is manufacturer and distributor of Product A.

- Company S, a subsidiary of Japanese Corporation P, manufactures and distributes Product A.

- Both Japanese Corporation P and Company S manufacture and distribute Product A.

- Neither Japanese Corporation P nor Company S engages in money laundering or in similar activities.

- Company S is doing well, and Company S has no need for support from Japanese Company P.

Past Fundraising Activities

Japanese Corporation P extended a loan to Company S seven years ago, denominated in Country X’s currency, to fund Company S’s investment in the expansion of S’s manufacturing capacity. Japanese Corporation P funded its loan to Company S from Japanese Corporation P’s funds on hand. This loan was for 10 years, bearing an interest rate of 3%.

Neither Japanese Corporation P nor Company S is engaged in money-lending transactions with related persons apart from financial institutions. Company S had never previously borrowed from banks or from similar institutions. As a result, there is no prospect that either the Japanese Corporation P or Company S could obtain information concerning spreads.

Japanese Corporation P previously took out a long-term loan from its main bank, Bank T. Bank would have loaned the funds to Japanese Corporation P to fund the loan to foreign-related Company S at a 0.7% spread. Japanese Corporation P and Company S could obtain swap data from a financial services provider. The financial data provider provided information to Japanese Corporation P and to Company S that the interest swap rate involving Country X’s currency for the ten-year time period would be 5%.

The Reference Case Studies define the “spread” as the interest rate corresponding to the profit that a financial institution can expect to earn. The spread includes the portion corresponding to the administrative expenses of the financial institution and the portion corresponding to the credit risk of the borrower. The “swap rate” of an interest rate swap indicates the level of the long-term interest rate that is exchangeable for the short-term interest rate, as indicated by the international financial markets.

Applicability of Methods that Are Equivalent to the Traditional Transaction Methods

Japanese transfer pricing provisions give preference to the taxpayer’s use of methods that are equivalent to the traditional transaction methods pursuant to ASMT Article 66-4(2), Item 2, when the taxpayer selects an arm’s length price for the money-lending transaction between Japanese Corporation P and Company S. An examination of comparable transactions pursuant to ASMT Directive 66-4(6)-4 and ASMT Directive 66-4(2)-3 and other relevant provisions produces these findings:

- Given the information available, the taxpayer is unable to find comparable transactions to apply a method that is equivalent to the CUP or to a method that is equivalent to the cost plus method.

- It was impossible to apply the methods prescribed in ASMT Directive 66-4(6)-4 as Company S had no bank loans.

- The taxpayer was unable to obtain information as to the interest rate that a lender would apply where the company had taken out a loan from a bank or similar institution under the same terms and conditions.

Selection of the Arm’s Length Price for Interest Rate Spreads

The calculation of interest rate was:

- Japanese Corporation P had determined the bank loan.

- The bank could provide spread information as to Corporation P.

- The taxpayer is to determine the arm’s length price using the interest rate pursuant to Administrative Guideline 2-7(1) and ASMT 66-4(2), Item 2(b), methods equivalent to methods consistent with the comparable uncontrolled price method.

- The arm’s length price is the interest rate for the money-lending transactions between Japanese Corporation P and Company S.

- The arm’s length rate is 5.7%, the objective interest rate of 5% plus the 0.7% spread.

Explaining the Arm’s Length Interest Rate Determination

As a general matter, see Case 1 for such transfer pricing analysis that concerns the applicability of traditional transaction methods. This analysis includes methods equivalent to the traditional transaction methods and pertains to the judging whether transactions correspond to comparable transactions.

There might be situations in which the taxpayer cannot find any transactions with unrelated persons that are comparable to foreign-related transactions, and, for that reason, the taxpayer cannot apply the traditional transaction methods. In that situation, it might be possible for the taxpayer to calculate the arm’s length price by a transfer pricing method that is “consistent with” the traditional transaction methods or a transfer pricing method that is “equivalent to” a method that is “consistent with” the traditional transaction methods that use such transactions as the comparable transaction. The prerequisite for applying the “consistent with” method or the “equivalent to” method is the existence of “objective and realistic indicators” pertaining to market prices or similar variables, such as the market interest rate, as in the present case.

The taxpayer is to use the next four-step procedure for calculating the arm’s length price for money-lending transactions by corporations by themselves providing that they do not engage in the money-lending business:

The interest rate that this methodology provides is the same regardless of whether the lender provides the loan through its funds at hand or through borrowed funds. The situation might exist where a financial transaction occurs under the same terms and conditions and under the same currency. In that situation, there is no fundamental need to allow for differences due to markets because the level of interest rates in each financial market is mostly the same.

CASE 5: METHODS CONSISTENT WITH THE COST PLUS METHOD

If the taxpayer determines that it cannot apply a transfer pricing method that is “equivalent to” the traditional transaction methods, the taxpayer can apply a transfer pricing method that is “consistent with” the cost plus method. The fact pattern for Case 5 is:

- Japanese Corporation P is engaged in the manufacture of Product A and the sales of Product A and part “a.”

- Japanese Corporation P undertakes sales relationships with foreign-related person S in Country X and with third-party T in Country X.

- Japanese Corporation P sells part “a” to foreign-related person S in Country X and third-party T in Country X.

- Japanese Corporation P provides maintenance services to foreign-related person S and maintains and inspects production facilities for foreign-related person S.

- Foreign-related person S manufactures Product A and sells Product A to third parties.

- Third-party T manufactures Product B and sells Product B to third parties.

The additional facts pertaining to Case 5 are:

- Japanese Corporation P established Company S ten years ago in Country X as a subsidiary to manufacture Product A and distribute Product A.

- Company S buys part “a” from Japanese Corporation P, which Japanese Corporation P manufactures.

- Company S combines part “a” with other parts to produce Product A for sale to third parties in Country X.

- Japanese Corporation P sells part “a” to Company T, a third party located in Country X.

- Company T purchases part “a” from Japanese Corporation P.

- Company T combines part “a” with other parts to manufacture Product B for sale to third parties in Country X.

- The providing of services is not a “core business” to Japanese Corporation P.

- Japanese Corporation P sells part “a” to Company A and to Company T at the same price.

- The market level, transaction terms, and transaction volumes for part “a” are the same.

Services Transactions

Japanese Corporation P performs two functions for Company S. Japanese Corporation P provides three engineers from its manufacturing division, for a total of two months per year, to maintain and inspect Company S’s facilities to manufacture Product A and to train Company S’s equipment operators. The maintenance, inspection, and other services that Japanese Corporation P undertake through its three engineers are not independent. However, the maintenance, inspection, and other services do not make use of Japanese Corporation P’s manufacturing know-how and so forth. Company S does not provide any consideration to Japanese Corporation P for the maintenance, inspection, and other services.

Neither Japanese Corporation P nor Company S engages in similar services transactions with unrelated parties. Furthermore, the taxpayer is unable to find similar services transactions between unrelated parties.

Applicability of the Traditional Transaction Methods for the Sale of Part “a”

The Japanese transfer pricing provisions give preference to the traditional transaction methods when selecting an arm’s length price pursuant to ASMT Article 66-4(2), Item 1. The taxpayer undertakes an examination of comparable transactions in accordance with ASMT Directive 66-4(2)-1, ASMT Directive 66-4(2)-3, and other provisions. The taxpayer finds that there are no problems from the point of view of transfer pricing taxation arising from the CUP as to the sale of part “a.” Japanese Corporation P and Company C use the sale of part “a,” using as a comparable transaction Japanese Corporation P’s sale to Company T.

Applicability of “Equivalent Methods”

The Japanese transfer pricing provisions give preference to the traditional transaction methods, and to method equivalent, when selecting an arm’s length price pursuant to ASMT Article 66-4(2), Item 2. An examination of comparable transactions in accordance with ASMT Directive 66-4(6)-5, ASMT Directive 66-4(6)-3, and other relevant provisions produce these findings:

- The taxpayer is unable to find any comparable transactions as to methods that are equivalent to the CUP or to the cost plus method as to Japanese Corporation P because the scope of the information is limited.

- Due to the content of the transaction, the taxpayer found it unfeasible to apply a transfer pricing method that is equivalent to the resale price method.

Applying the Services Method

The taxpayer determined that the providing of services by Japanese Corporation P to Company S was incidental to Japanese Corporation P’s core business, which is the sale of part “a,” and that the cost of providing the services did not account for a significant portion of Japanese Corporation P’s costs in the taxable year in which the services activities took place. Japanese Corporation P made no use of intangible properties in providing services.

Based on the preceding facts, the taxpayer rejected the use of the cost plus method. Instead, the taxpayer found it appropriate to apply a transfer pricing method that is “consistent with” the cost plus method (i.e., by applying the final cost of services provision as being the arm’s length price pursuant to Administrative Guidance 2–9).

The final service cost is the sum of:

- Salaries, bonuses, and retirement expenses during the dispatch period

- Engineers’ travel, transport, and accommodation costs

- Other costs to dispatch the engineers

- Indirect costs allocated on a reasonable basis, such as the general expenses of the division concerned and associated divisions

The reader should review the explanation for Case 1 as to the applicability of the traditional transaction methods, including methods that are “equivalent to” the traditional transaction methods, and in judging whether the transactions correspond to comparable transactions. The reader should review the explanation for Case 1 as to the traditional transaction methods, including methods that are “consistent with” the traditional transaction methods.

ASMT Directive 66-4(6)-5 addresses transfer pricing methods that are “equivalent to” the comparable uncontrolled method or a method that is “equivalent to” the cost plus method for services transactions. The application of the cost plus method necessitates a markup in the expenses required to provide the services. Nevertheless, it generally will be difficult for the taxpayer to find “comparable transactions” among the uncontrolled transactions as services transactions that are incidental to the corporation’s core business. Thus, the Reference Case Studies recognize that there may some cases where the ASTM Directive provides transfer pricing methods the taxpayer cannot apply. As a result, pursuant to Administrative Guideline 2-9, the final services cost might include the cost without markup for the expenses required.

Administrative Guideline 2-9 provide that the final service cost is not the arm’s length price if:

- The services activities are “not incidental to” the core business

- The cost of providing the services “does not” account for a significant proportion of the cost or expenses of a corporation of a foreign-related business

- The taxpayer uses intangible property in providing services

These provisions would suggest that the taxpayer consider other calculation methods in this instance.

The Reference Case Studies, in applying the second of these three tests, makes use of the term “does not” in reference to the costs or expenses involved. As transfer pricing practitioners, we suggest that the Reference Case Studies contain an error, and that “does” is the word that the Reference Case Studies would require.

The next four points specify the differences as to whether the final services costs can be treated as the arm’s length price where these costs are incidental to the core business between the corporation and the foreign-related business:

The Reference Case Studies caution that a corporation might engage in an inventory transaction and a services transaction, both with a foreign-related person. In that event, the taxpayer should consider that transfer pricing issues can apply to both situations.

CASE 6: TRANSACTIONAL NET MARGIN METHOD

In the case at hand, the taxpayer considered the applicability of the traditional transaction methods. The taxpayer determined that it could not apply the traditional transaction methods in this instance. The taxpayer then ascertained that it could obtain comparable transactions that would enable it to apply the transactional net margin method, making the transactional net margin method appropriate. The taxpayer then considered the applicability of transfer pricing methods that are “equivalent to” the traditional transaction methods and determined that the transactional net margin method was appropriate as being “equivalent to” the traditional transaction methods.

Case 2 considers two situations in which the transactional net margin method might be appropriate: the first addresses the sale of inventories; the second addresses the licensing of intangible properties.

Sale of Inventories

Consider this fact pattern:

- Japanese Corporation P purchases raw materials and so forth in Japan.

- Japanese Corporation P established Company S in Country X ten years ago to distribute Product A.

- Japanese Corporation P manufactures Product A in Japan.

- Japanese Corporation P sells Product A to foreign-related party S in Country X.

- Foreign-related party S, in Country X, purchases Product A from Japanese Corporation P.

- Foreign-related party S, in Country X, sells Product A to a dozen or so third-party companies as agents in Country X.

- Japanese Corporation P manufactures Product A using its original technology it developed through its R&D process.

- Company S does not engage in any advertising or sales promotion activities.

- Country X does require that companies disclose financial data, but Country X does not require the company to disclose cost items.

- Japan does require the company to disclose operating income.

Potential Applicability of the Traditional Transaction Methods

The Japanese transfer pricing provisions give preference to the traditional transaction methods to determine the arm’s length price. ASMT Article 66-4(2), Item 1, provides that the taxpayer must examine comparable transactions in accordance with ASMT Directive 66-4(2)-1, ASMT Directive 66-4(2)-3, and other relevant provisions. These findings are:

- Product A, which Japanese Corporation P manufactured and sold to Company S, is a product that utilizes Japanese Corporation P’s technologies resulting from its R&D activities.

- The taxpayer was unable to find comparable transactions from the available data in applying the CUP or the cost plus method to Japanese Corporation P.

- Company S was not engaged in original advertising or in sales promotion activities.

- Company S has no intangible properties that provide a source of income.

- See Cases 10 to 15 regarding the relationship between intangible properties and sources of income.

- It was not possible to ascertain gross profit on sales, or cost of sales, from publicly available information in Country X.

- The taxpayer was unable to obtain the information it would need to adjust the differences affecting the ratio of gross profit to sales.

- As a result, the taxpayer could not find comparable transactions to apply the resale price method to Company S.

Methods that Would Substitute for the Traditional Transaction Methods

The taxpayer found that it could not apply the traditional transaction methods. The taxpayer considered applying methods that are “consistent with” the traditional transaction methods, as prescribed by ASMT Article 66-4(2), Item 1(d), and other methods prescribed in the ASMT Cabinet Order, with these results. The taxpayer was unable to find comparable transactions in applying methods that are consistent with the traditional transaction methods. It was possible for the taxpayer to identify comparable transactions for Company S from publicly available information based on the operating margin. As a result, it was deemed to be appropriate in this case to calculate the arm’s length price by applying the transactional net margin method to Company S pursuant to ASMT Cabinet Order, Article 39-12(8), Item 2.

Transactional Net Margin Method and the Profit Split Method

The reader should examine the examination process applicable to Case 1, including traditional transaction methods, including methods “equivalent to” methods consistent with the traditional transaction methods. The transactional net margin method calculates the arm’s length price by selecting comparable transactions for one of the counterparts to the transaction concerned. There may be, however, cases in which the profit split method is more appropriate, based on the corporation’s role and functions, in order for the taxpayer to calculate arm’s length price based on the contributions of both the corporation and the foreign-related person to generate profit.

Transactional Net Margin Method

These factors apply to the transactional net margin method:

- The transactional net margin method is a comparison of net incomes. Taxpayers might apply the transactional net margin method to calculate the arm’s length price for foreign-related transactions. They can focus on the level of operating income from these foreign-related transactions. When considering the application of the transactional net margin method, taxpayers need to consider the similarity of factors listed in ASMT Directive 66-4(2)-3 when selecting comparable transactions.

- The comparable uncontrolled cost method compares the prices of goods themselves and requires the taxpayer to apply strict similarity or homogeneity of inventories. In contrast, the resale price method or the cost plus method focuses on gross profit on sales. These traditional methods require the taxpayer to determine whether those activities are similar, as performed by the buyer and by the seller.

- Differences in products tend to affect prices. Differences in functions tend to affect the profit margin (i.e., the gross profit on sales). However, many knowledgeable practitioners view the operating margin as being less susceptible to the effects of such differences. Nevertheless, the taxpayer might find that such transactions may be usable as a source of comparability with transactional net margin method transactions. The taxpayer might reach that conclusion even where the comparability that traditional transaction methods would require is not available.

- The Japanese tax authorities introduced the transactional net margin method for fiscal 2004. Taxpayers can apply the method for taxable years commencing in or after April 1, 2004.

Profit Split Method

The Japanese transfer pricing methodology provides for three specific profit split methodologies:

Profit Split Method and the Transactional Net Margin Method

The Japanese transfer pricing provisions treat the transactional net margin method and the profit split method as being of equal importance. Neither of the two methods has more importance than the other in deciding which transfer pricing method to apply.

As a general matter, the Japanese transfer pricing provisions view transfer pricing taxation as a system of taxation concerning transactions between a corporation and a foreign-related person. The Japanese transfer pricing provisions suggest that the taxpayer should pay attention to whether the profit arising from a foreign-related transaction is commensurate with the roles and function of each party to the transaction. Pursuant to Administrative Guideline 2-1(3), the taxpayer is to indicate whether it has problems concerning transfer pricing taxation.

The Japanese transfer pricing provisions require the taxpayer to select “the most reasonable” transfer pricing method, making that determination in keeping with the actual situation in each particular case. The taxpayer must consider this point when making the selection.

Licensing Activities

The Reference Case Studies provide this scenario concerning the licensing of patents and manufacturing know-how:

- Japanese Corporation P manufactures and sells Product A in Japan.

- Japanese Corporation P established foreign-related person S as a subsidiary to manufacture and distribute Product A.

- Japanese Corporation P manufactures Product A through applying its own original R&D technologies.

- Japanese Corporation P licenses patents and manufacturing know-how to foreign-related person S in Country X, using Japanese Corporation P’s own technologies.

- Foreign-related party S purchases raw materials.

- Foreign-related party S licenses patents and manufacturing know-how from Japanese Corporation P.

- Foreign-related party S manufactures Product A in Country X.

- Foreign-related party S sells Product A to third parties in Country X as agents.

- No trading of inventories takes place between Japanese Corporation P and Company S.

- Company S has no R&D operations.

- Company S licenses Japanese Corporation P’s technology to manufacture Product A.

Treatment of the License for Transfer Pricing Purposes

The Japanese transfer pricing provisions give preference to the traditional transaction method and to transfer pricing methods that are “equivalent to” these methods when the taxpayer selects an arm’s length price. The taxpayer would apply ASMT Article 66-4(2), Item 2, in examining comparable transactions in accordance with ASMT Directive 66-4(6)-6, ASMT Directive 66-4(2)-3, and other relevant provisions. This analysis produced these findings:

- The patents and know-how that Japanese Corporation P licensed to Company S are Japanese Corporation P’s original R&D technologies.

- Based on the information available, it is not possible for the taxpayer to find comparable transactions for applying a transfer pricing method that is “equivalent to” the CUP or to a method that is “equivalent to” the cost plus method to Japanese Corporation P.

- The taxpayer was unable to apply a method that is “equivalent to” the resale price method given the content of the transaction.

Finding a Method to Substitute for the Traditional Transaction Methods

In this situation, the taxpayer found that it was impossible to apply a transfer pricing method that was “equivalent to” the traditional transaction methods. Further, the taxpayer found that it was impossible to apply methods that are “equivalent to” methods that are “consistent with” the traditional transaction methods. The taxpayer considered applying the transfer pricing methods prescribed in ASMT Article 66-4(2), Item 2(b), and other methods prescribed in the ASMT Cabinet Order, and obtained these results:

- The taxpayer was unable to identify comparable transactions in seeking to apply the “equivalent to” methods that are “consistent with” the arm’s length results.

- The taxpayer can obtain operating margins on comparable transactions from publicly available information that are comparable with manufacturing and sales transactions that Company S undertakes.

- The taxpayer could be able to calculate the arm’s length price indirectly, doing so by calculating the “normal profit” that is “commensurate with” Company S’s functions operating margin.

- The taxpayer could then treat Company S’s residual profit in excess of the normal profit amount as being the consideration for licensing of patents and manufacturing know-how.

- The taxpayer can apply the preceding indirect arm’s length approach by directly calculating the consideration for licensing intangible properties between Japanese Corporation P and Company S.

- In this particular case, the taxpayer found it appropriate to calculate the arm’s length price by applying a transfer pricing method that is “consistent with” the transactional net margin method as applied to Company S, pursuant to ASMT Cabinet Order Article 39-12(8), Item 4.

Explanation for the Transactional Net Margin Method Determination

The reader should review the explanation to Case 1 as to the applicability of the traditional transaction methods and the applicability of transfer pricing methods that are “equivalent to” the traditional transaction methods.

It may be possible for the taxpayer to apply the transactional net margin method and to indirectly calculate the amount of consideration for the furnishing of intangible properties. The taxpayer might be able to apply this approach when the corporation furnishes intangible properties to a foreign-related person through the licensing of patents or of similar property. The taxpayer can calculate the normal profit that is “commensurate with” the functions of the foreign-related person and then treat the residual profit of the foreign-related person as the excess amount.

It is possible for the taxpayer to apply this profit split approach if the foreign-related person engages in the same category of business as that of the foreign-related transaction. It is possible for the taxpayer to apply this profit split approach if the corporation has comparable manufacturing functions or sales functions to other corporations in similar markets of a similar size. This procedure does not apply to corporations that have material intangible properties. This method of calculating the arm’s length price is “a method that is equivalent to” a transfer pricing method that is “consistent with” the transactional net margin method.

The case at hand is premised on the license of intangible properties under contract. This situation can apply even if Japanese Corporation P and Company S do not have an agreement between them. The taxpayer might be able to apply the intangible arrangement if the facts and circumstances would deem a license to be created based on the actual state of the transactions, pursuant to Administrative Guideline 2-13.

The transactional net margin method is a method of calculating the arm’s length price by selecting comparable transactions. These comparable transactional net margin transactions would involve one or the other counterparts to the underlying transaction. There may be cases in which the profit split method is a more appropriate method that is the transactional net margin method in determining the arm’s length price. The method selection depends on the contribution of the corporation and the foreign-related party to the generation of profit, determined in light of the roles and functions of the corporation and the foreign-related party.

CASE 7: CONTRIBUTION PROFIT SPLIT METHOD

In the case at hand, the taxpayer considered the applicability of the traditional transaction methods and found that it could not apply the traditional transaction methods. The taxpayer determined that the profit split method was appropriate.

First Application of the Contribution Profit Split Method

The first application of the contribution profit split method is shown next.

- Japanese Corporation P purchases raw materials and other items in Japan.

- Japanese Corporation P manufactures Product A in Japan.

- Japanese Corporation P established Company S in Country X ten years before.

- Japanese Corporation P sells Product A in Japan.

- Japanese Corporation P sells part “a” to foreign-related person S in Country X.

- Foreign-related person S combines part “a” with other parts to produce Product A.

- Foreign-related person S manufactures Product A in Country X.

- Foreign-related person S sells Product A to third-party agents in Country X.

- Foreign-related person S has no R&D operations.

- Foreign-related person S does not engage in original advertising or sales promotion activities.

- Foreign-related person S does not use its own trademark or other properties in its distribution activities.

Other Conditions of the Transfer

Company S sells Product A to third parties located in Country X. However, two other corporations manufacture products that are similar to Product A and sell these products in Country X. These two corporations are manufacturing subsidiaries whose parent companies are located outside Country X. The market for such products in Country X is an oligopoly of these three companies. These two companies have similar products as Product A.

Product A has an equal share of the market compared with these two companies. Product A is almost the same as the similar products of the same companies in terms of product and price. In Japan, only one corporation manufactures and sells a product similar to Japanese Corporation P’s Product A. Transactions involving the similar product are controlled transactions.

Inapplicability of the Traditional Transaction Methods

The Japanese transfer pricing provisions give preference to traditional transfer pricing transaction methods when the taxpayer selects an arm’s length price pursuant to ASMT Article 66-4(2), Item 1. ASMT Directive 66-4(2)-1, ASMT Directive 44-4(2)-3, and other relevant provisions produce these findings:

- Regarding Japanese Corporation P, one corporation is manufacturing and selling a product that is similar to Product A in Japan. All transactions involving that product are controlled transactions. As a result, based on the information available, it is not possible for the taxpayer to identify comparable transactions in seeking to apply the CUP or the cost plus method.

- Regarding Company C, the transactions of the two companies deal in similar products, but they are controlled transactions. As a result, the taxpayer cannot find comparable transactions in applying the resale price method to Company S’s sales transactions.

Substituting for the Traditional Transaction Methods

The taxpayer cannot apply the traditional transaction methods in the present case. The taxpayer considered applying methods that are “consistent with” the traditional transaction methods, as prescribed by ASMT Article 66-4(2), and other methods, as prescribed by the ASMT Cabinet Order. The taxpayer was unable to find comparable transactions in applying methods that are “consistent with” the traditional transaction methods. The taxpayer then considered it appropriate in this case to calculate arm’s length amount pertaining to foreign-related transactions between Japanese Corporation P and Company S by applying the profit split method.

The taxpayer was unable to identify any comparable transactions in applying the transactional net margin method. Neither Japanese Corporation P nor Company S had material intangible property. As a result neither party could apply the residual profit split method.

Explaining the Selection of a Transfer Pricing Method

The reader should note that Case 1 addresses the applicability of the traditional transfer pricing transaction methods, including methods that might be considered as methods “equivalent to” the traditional transaction methods, and for judging whether these transactions correspond to comparable transactions. There might be situations in which it is difficult for the taxpayer to find comparable transactions due to the state of the market, such as the existence of an oligopoly. A taxpayer might be better off in that situation in using the contribution profit split transfer pricing method but without seeking to use comparable transactions as the method of arm’s length price. The contribution profit split method might be the method that is “more appropriate.” The taxpayer cannot apply the residual profit split method if neither the corporation nor the related person has material intangible properties. The reader should see the explanation to Case 8 to determine whether the residual profit split method is compatible.

The issue in applying the contribution profit split method can be the selection of factors the taxpayer is to use. The taxpayer is to make use of the factors that are suited to estimating the extent of the contribution to the profit that is to be split, depending on the content of the foreign-related transaction. These factors might include, for instance, the amount of the expenses incurred, such personnel costs, and the amount of capital the corporation or the foreign-related person employ pursuant to ASMT Directive 66-4(4)-2.

For instance, in applying the contribution profit split method, the taxpayer might consider if the function the taxpayer ordinarily performs (e.g., in manufacturing or in distribution) contributes to the generation of profit. In such a case, it would be logical for the taxpayer to use the human resource expenditures and depreciation expenses that reflect that function.

Financial Institutions with International Operations

Japanese Corporation A is a financial institution having international operations in Country X and in Country Y:

- Japanese Corporation A does business with foreign-related person XA in Country X.

- Japanese Corporation A does business with foreign-related person YA in Country Y.

- Japanese Corporation A, foreign-related person XA, and foreign-related person YA all engage in derivative transactions as a single group.

- Japanese Corporation A markets derivative products to customers.

- Japanese Corporation A takes orders from customers.

- Japanese Corporation A, a front-end company, creates, develops, and markets derivative products to meet customer demands.

- Foreign-related person XA provides Japanese Corporation A with pricing these derivative products.

- Foreign-related person XA, according to Japanese Corporation A’s request, engages in interbank market transactions.

- Foreign-related person XA engages in trading operations, including revenue and risk management concerns as to all financial products that foreign-related person XA handles.

- Foreign-related person YA is a party to contracts with customers, according to customer needs, and engages in trading operations.

Determination of Transfer Pricing Methods

The Japanese transfer pricing provisions give the taxpayer preference to transfer pricing methods that are “equivalent to” the traditional transfer pricing methods when the taxpayer selects an arm’s length price pursuant to ASMT Article 66-4(2), Item 2. An examination of comparable transactions pursuant to ASMT Directive 66-4(6)-5, ASMT Directive 66-4(2)-3, and other provisions produces these findings:

- The taxpayer was unable to ascertain comparable functions as to front-end operations, marketing, and trading, as the taxpayer dispersed these functions among related parties through services transactions with unrelated parties.

- Given the data available, the taxpayer was unable to identify uncontrolled transactions in the same or similar category of business that Japanese Corporation A, foreign-related person XA, and foreign-related person YA undertook with the same terms of service provision.

- The taxpayer was not able to find any comparable transactions in applying methods that are equivalent to the traditional transaction methods.

Selection of a Transfer Pricing Method that Determines the Arm’s Length Price

In this particular case, the taxpayer found that it could not apply a transfer pricing method that is “equivalent to” the traditional transaction methods. The taxpayer considered applying transfer pricing methods that are “equivalent to” transfer pricing methods that are “consistent with” the traditional transaction methods pursuant to ASMT Article 66-4(2), Item 2(b), and to other transfer pricing methods that are “equivalent to” other methods, as prescribed in the ASMT Cabinet Order. The taxpayer determined:

- The taxpayer was unable to find comparable transactions to the application of a transfer pricing method that is “equivalent to” a transfer pricing method that is “consistent with” the traditional transaction methods.

- The taxpayer concluded that the Japanese Corporation A performed its operations as a single set of functions concerning the sale of derivative products to customers by the business group as a unit.

- Based on the foregoing, the taxpayer found it appropriate to apply the profit split method by apportioning the profit that arose from Japanese Corporation A, foreign-related person XA, and foreign-related person YA.

- The taxpayer was to apportion the combined profit “according to the level of each foreign-related person’s contribution.”

- The taxpayer found no comparable transactions in considering whether to apply the transactional net margin method.

Explaining the Choice of Transfer Pricing Method

The reader should consider that the explanation to Case 1 discusses the applicability of traditional transaction methods, including transfer pricing methods that are “equivalent to” traditional transaction methods, and in judging whether the transactions correspond to comparable transactions.

Transactions might be highly integrated and might be global in nature. The company’s functions can be dispersed among a corporation and foreign-related persons that do business together cooperatively as a single unit. In such situations, it is difficult for the taxpayer to determine the revenues of each of the related persons by means of a transfer pricing method that is equivalent to the traditional transaction methods. In such situations, the taxpayer should consider applying transfer pricing methods that are “equivalent to” methods “consistent with” the traditional transaction methods, as prescribed by ASMT Article 66-4(2), Item 2(b), and to methods that are “equivalent to other methods,” as prescribed in the ASMT Cabinet Order.

The taxpayer will find that the application of transfer pricing methods that are consistent with the traditional transaction methods is difficult for the same reasons as applying methods that are “equivalent to” the traditional transaction methods. The taxpayer, then, needs to consider the application of a transfer pricing method that is “equivalent to” the profit split method or a transfer pricing method that is “equivalent to” the transaction net margin method. In the case of transactions such as those described in this case, however, it is generally appropriate for the taxpayer to apply a transfer pricing method that is “equivalent to” the profit split method. The taxpayer, in applying the profit split method, can allocate the profit arising from the overall transactions to each of the operations concerned according to their contributions. This method would be a transfer pricing method that is “equivalent to” the contribution profit sharing method. This profit split method might be feasible due to the frequent infeasibility of finding comparable transactions when applying the transactional net margin method.

CASE 8: RESIDUAL PROFIT SPLIT METHOD

In the case at hand, the taxpayer found that it could apply the traditional transaction transfer pricing methods. The taxpayer reached this determination after considering the applicability of the traditional transaction methods, including methods that are “equivalent to” the traditional transaction methods. Here the taxpayer found the residual profit split approach to be appropriate because the corporation and the foreign-related person create intangible properties through R&D, sales promotion, and other activities that serve as a source of income.

The business relationships are:

- Japanese Corporation P purchases raw materials and other items.

- Japanese Corporation P manufactures Product A in Japan.

- Japanese Corporation P sells Product A.

- Japanese Corporation P established foreign-related person S as a subsidiary ten years ago to manufacture and distribute Product A.

- Japanese Corporation P and foreign-related person S manufacture Product A using original technologies that result from Japanese Corporation P’s R&D activities.

- Japanese Corporation P supplies part “a” to foreign-related person S in Country X.

- Part “a” is a core part that aggregates original technologies that Japanese Corporation P produces.

- Foreign-related person S combines part “a” with other parts to manufacture Product A.

- Foreign-related person S manufactures Product A based on original technologies that Japanese Corporation P furnishes to foreign-related person S.

- Japanese Corporation P licenses patents and manufacturing know-how to related-person S in Country X.

- Foreign-related person S manufactures Product A in Country X.

- Foreign-related person S sells Product A to approximately 200 third-party retailers.

- Foreign-related person S has no R&D operations.

- Foreign-related person S has numerous sales representatives.

- Foreign-related person S engages in original advertising and sales promotion activities that foreign-related person S targets to retailers and to end consumers.

Product A has achieved a certain market share in Country X. Product A achieved this market share because of:

- Product A’s unique technical performance

- Strong product recognition

- A well-developed network of retailers, built up through advertising and sales promotion activities

- Foreign-related person S selling Product A at a stable price

Traditional Transaction Methods and Methods “Equivalent to” Traditional Transaction Methods

The Japanese transfer pricing provisions give preference to traditional transaction methods and to methods “equivalent to” transaction methods for purposes of ascertaining the arm’s length price pursuant to ASMT Article 66-4(2). An examination of comparable transactions in accordance with ASMT Directive 66-4(2)-1, ASMT Directive 66-4(6)-6, ASMT Directive 66-4(2)-3, and other provisions produced these findings:

- Japanese Corporation P licensed patents and know-how to foreign-related person S. Japanese Corporation P created these patents and know-how as original technologies emanating as a result of its R&D activities.

- Japanese Corporation P manufacturers part “a” as a result of these original technologies.

- Based on the information available, the taxpayer found it impossible to find any comparable transactions for purposes of applying the CUP or any equivalent method.

- Based on the information available, the taxpayer found it impossible to find any comparable transactions for purposes of applying the cost plus method or any equivalent method.

- The hallmark of transfer pricing taxability then becomes the delineation between a “corporation engaging solely in basic activities” and a corporation that exceeds this basic activities threshold.