Curve Finance’s AMM was originally designed to facilitate trades with low price impact between stablecoins or, more generally, between assets that have the same price—like ETH and sETH (Synthetix1 ETH). Curve’s AMM was launched in January 2020 and was initially called StableSwap. Its algorithm is more complex than those of the AMMs we have studied in the previous chapters.

In June 2021, Curve v2 was presented [12]. This new version of Curve’s AMM is called Crypto Pools, and although it is based on the previous one, it introduces a new algorithm to allow trading between nonpegged assets.2

Currently, both versions of the Curve AMM coexist. In this chapter, we will explain how the StableSwap AMM works and analyze the maths behind it. We will not cover Curve v2 in this book.

4.1 The StableSwap Invariant

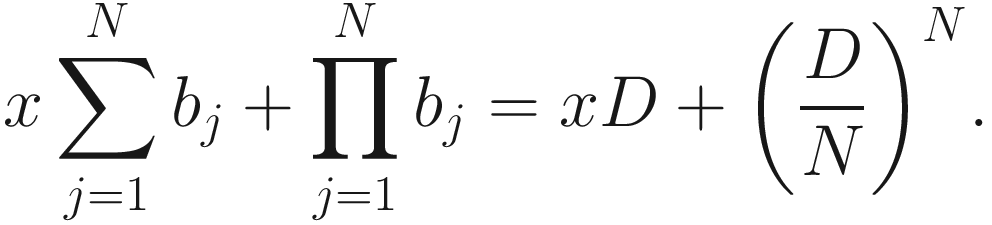

The StableSwap invariant is a combination of the constant product invariant and the constant sum invariant, which are defined as

and

and

and hence, bi + bo = bi + b + bo − a, from where it follows that a = b, which implies that the effective price paid per unit of token o in terms of token i is  . In particular, there is no difference between the spot price and the effective price paid by a trader; that is, there is no price impact.

. In particular, there is no difference between the spot price and the effective price paid by a trader; that is, there is no price impact.

for all j ∈ {1, 2, …, N}, and substituting these expressions in the constant product formula, we obtain that

for all j ∈ {1, 2, …, N}, and substituting these expressions in the constant product formula, we obtain that  . Thus, our constant product invariant will be

. Thus, our constant product invariant will be

Note that when t = 0, we obtain the constant product formula, and when t = 1, we obtain the constant sum formula.

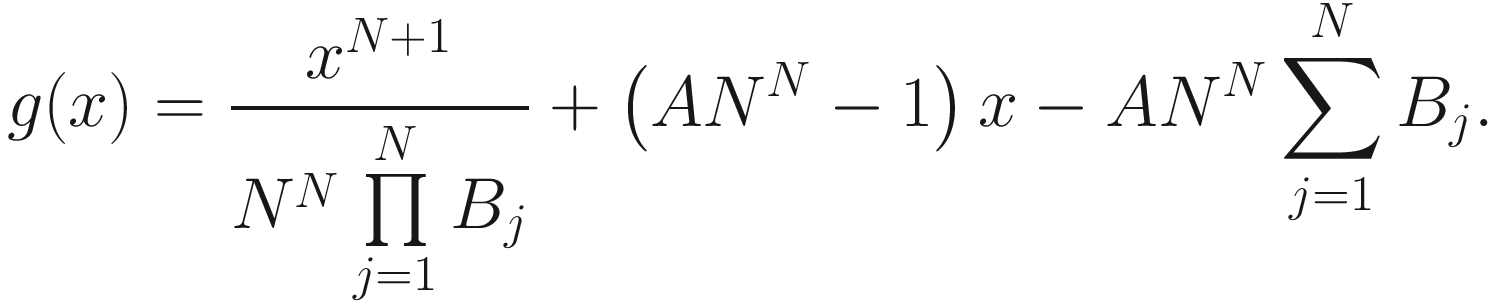

. Note that this function g satisfies thedesired properties and that 0 ≤ g(x) ≤ 1 for all x ≥ 0. Replacing t = g(x) in the preceding expression, we obtain

. Note that this function g satisfies thedesired properties and that 0 ≤ g(x) ≤ 1 for all x ≥ 0. Replacing t = g(x) in the preceding expression, we obtain

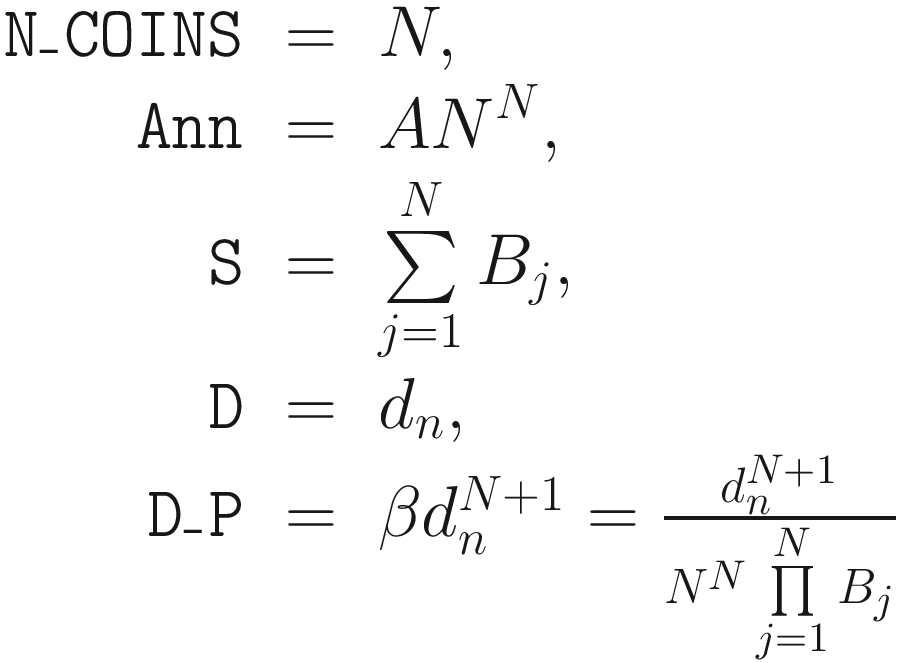

where A is a positive number that is called amplification coefficient. In the actual code, there is a parameter labeled A, which is a positive integer and is equal to ANN − 1. Therefore, from now on, we will assume that ANN − 1 is a positive integer—and this will indeed be needed later.

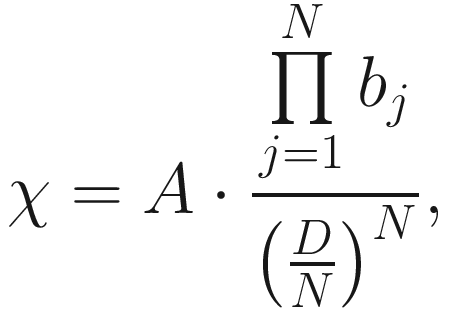

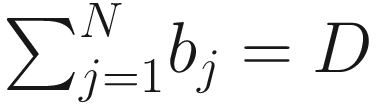

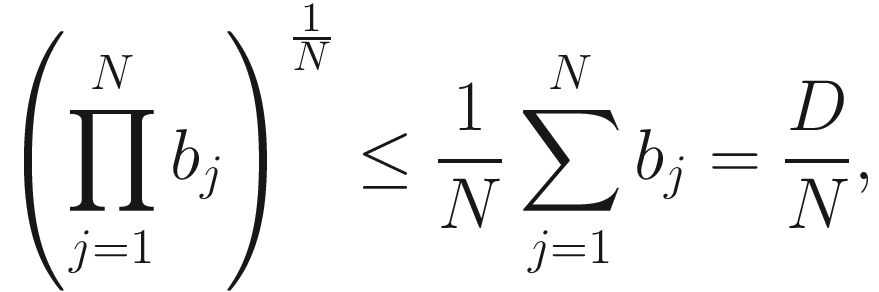

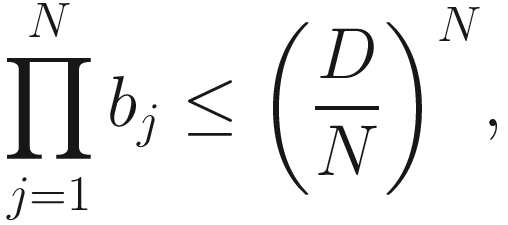

(which will not hold in general as the pool balances change), by the inequality of arithmetic and geometric means,3 we have that

(which will not hold in general as the pool balances change), by the inequality of arithmetic and geometric means,3 we have that

Graph of the function f

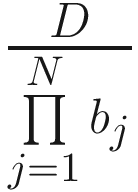

, we get

, we get

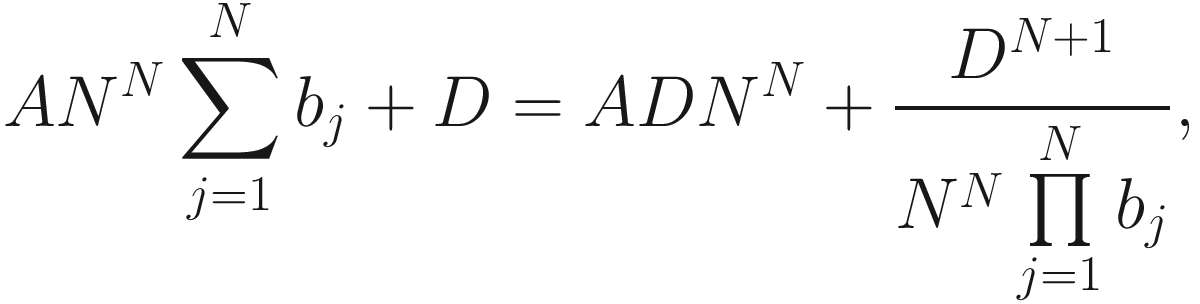

which is the StableSwap invariant [11].

Comparison between the StableSwap invariant, the constant product invariant, and the constant sum invariant

4.2 Mathematical Preliminaries

In this subsection, we will analyze several mathematical arguments that are used within the StableSwap AMM. We will also prove some results that will be needed later in order to explain the mathematical foundations of this AMM.

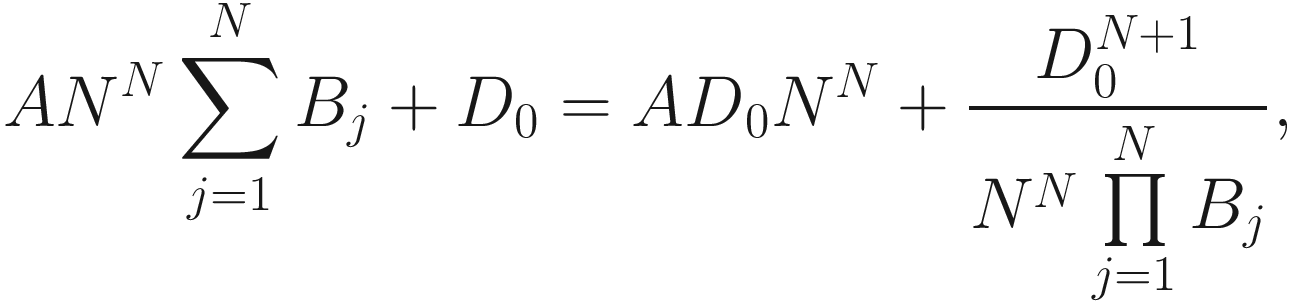

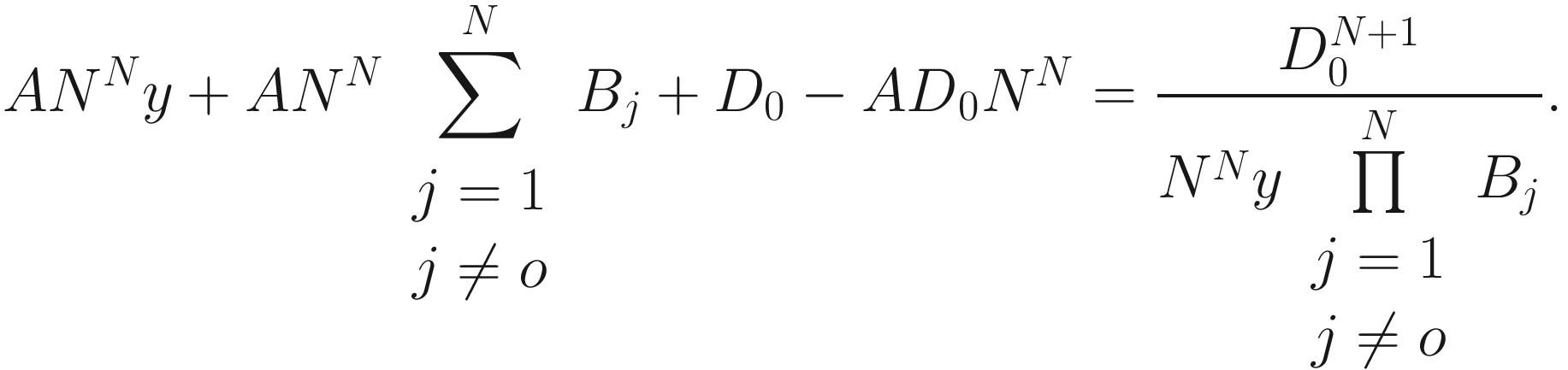

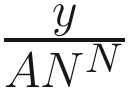

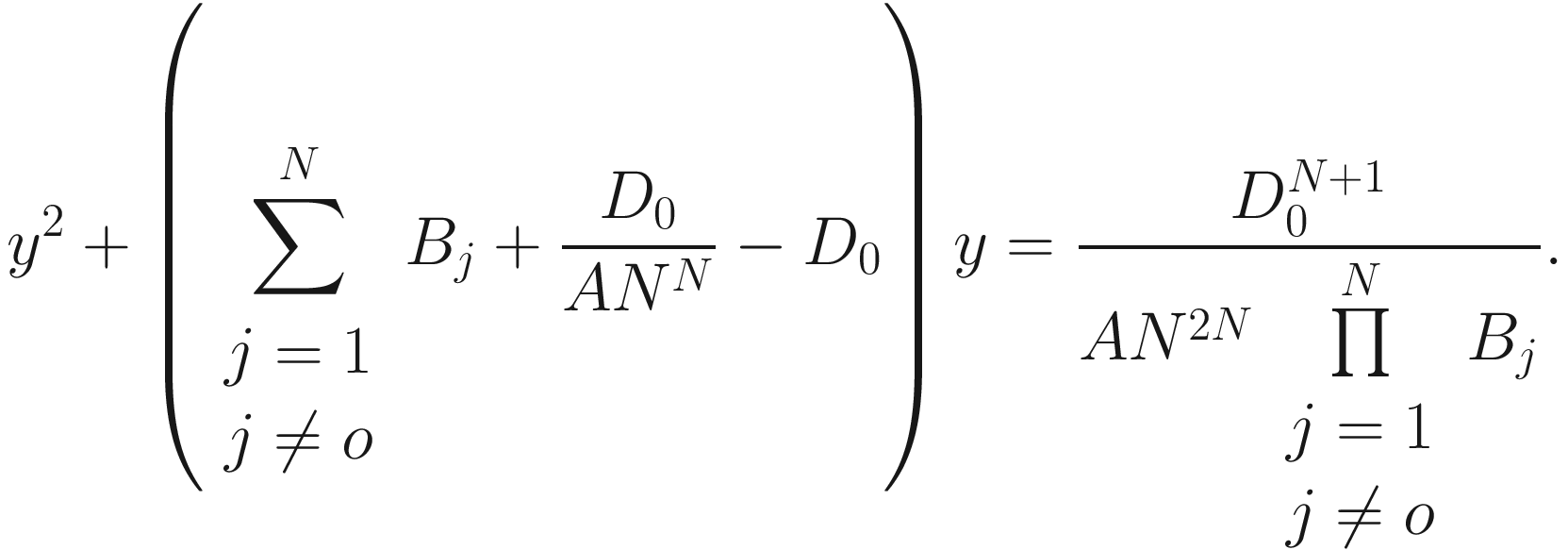

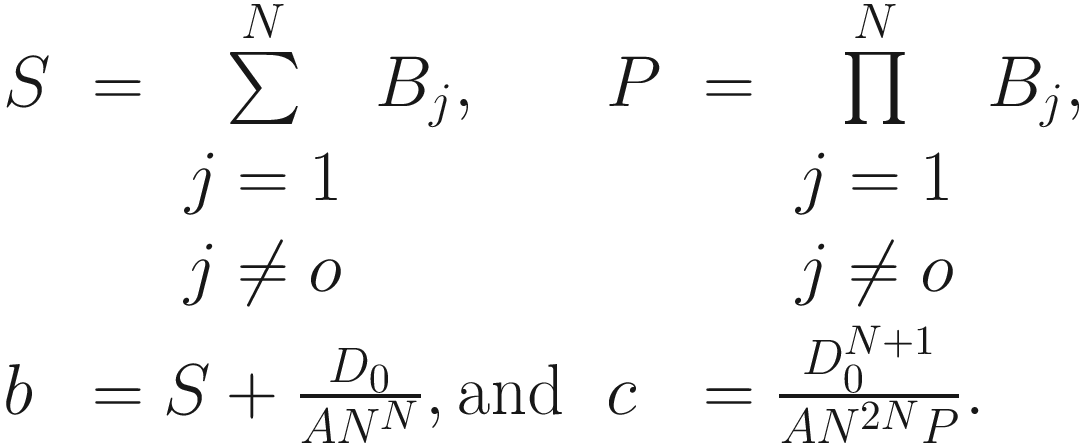

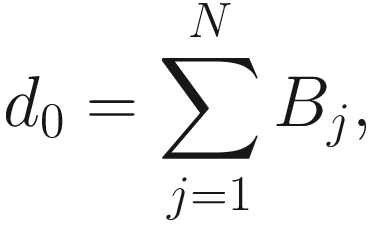

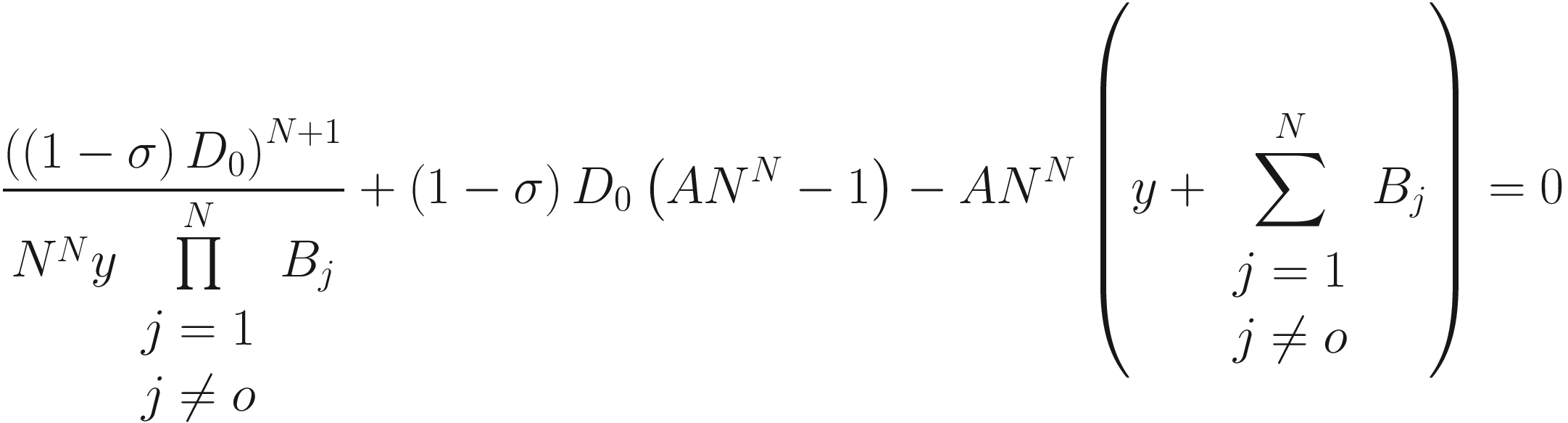

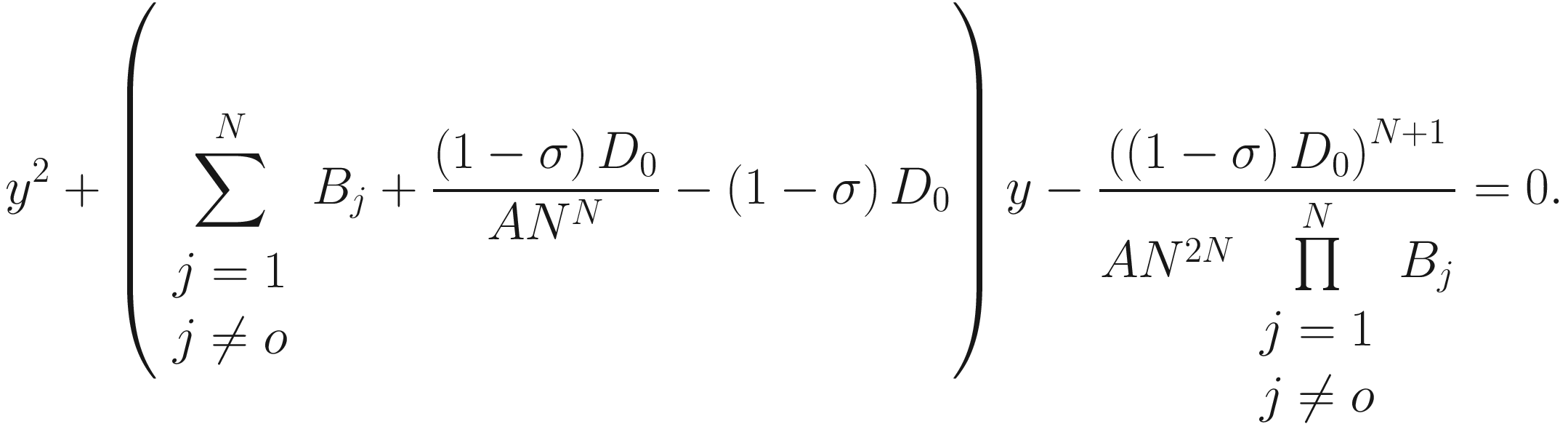

Consider a StableSwap liquidity pool consisting of N tokens. For each j ∈ {1, 2, …, N}, let Bj be the balance of token j in the pool. Let D0 be the value of the pool parameter D. Recall that D0 > 0. Let o ∈ {1, 2, …, N}. We will prove that the balance of token o is uniquely determined by D0 and the balances Bj, j ≠ o.

we get

we get

and the value of y can be obtained through solving the previous quadratic equation. Observe that if y1 and y2 are the solutions of the previous equation, then y1y2 = − c, and since c > 0, we obtain that y1y2 < 0. This means that one of the solutions of the previous equation is positive and the other is negative. Thus, the value of y that we are looking for is well defined since it is the only positive solution to the previous equation. Therefore, we have proved that the balance of token o is uniquely determined by D0 and the balances Bj, j ≠ 0.

The previous proof allows us to give the following definition.

as the only positive number that satisfies Equation 4.3. That is, the number  is the balance of token o if the balance of token j is Bj for all j ∈ {1, 2, …, N} − {o} and the value of the pool parameter D is D0.

is the balance of token o if the balance of token j is Bj for all j ∈ {1, 2, …, N} − {o} and the value of the pool parameter D is D0.

We will analyze now how  changes when we modify the balances Bj, j ≠ o, or the value of the pool parameter D.

changes when we modify the balances Bj, j ≠ o, or the value of the pool parameter D.

be positive real numbers. Let

be positive real numbers. Let

be positive real numbers. If

be positive real numbers. If  and

and  for all j ∈ {1, 2, …, N} − {o}, then

for all j ∈ {1, 2, …, N} − {o}, then

, or

, or  is strict, then

is strict, then

and that y > 0 and y´ > 0. Hence,

and that y > 0 and y´ > 0. Hence,

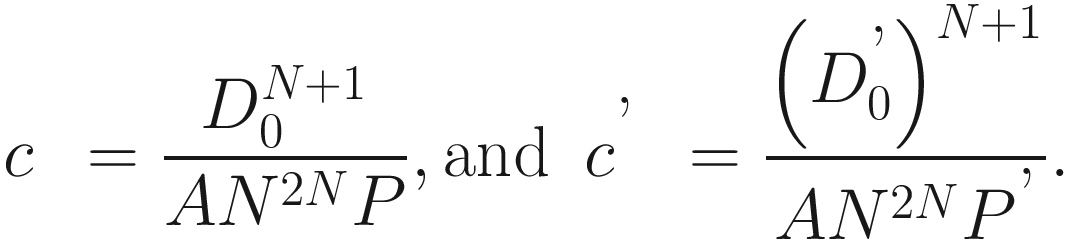

for all j ∈ {1, 2, …, N} − {o} and D0≥

for all j ∈ {1, 2, …, N} − {o} and D0≥  . Then S ≤ Ś and P ≤ P´. And since

. Then S ≤ Ś and P ≤ P´. And since  , we obtain that c ≥ c´. On the other hand, since ANN − 1 is a positive integer and N ≥ 2, it follows that

, we obtain that c ≥ c´. On the other hand, since ANN − 1 is a positive integer and N ≥ 2, it follows that  . Thus,

. Thus,

which entails a contradiction. Thus, y ≥ yʹ.

, or D0≥

, or D0≥  is strict, then c > cʹ. Suppose that y ≤ yʹ. Then

is strict, then c > cʹ. Suppose that y ≤ yʹ. Then

which entails a contradiction. Thus, y > yʹ. □

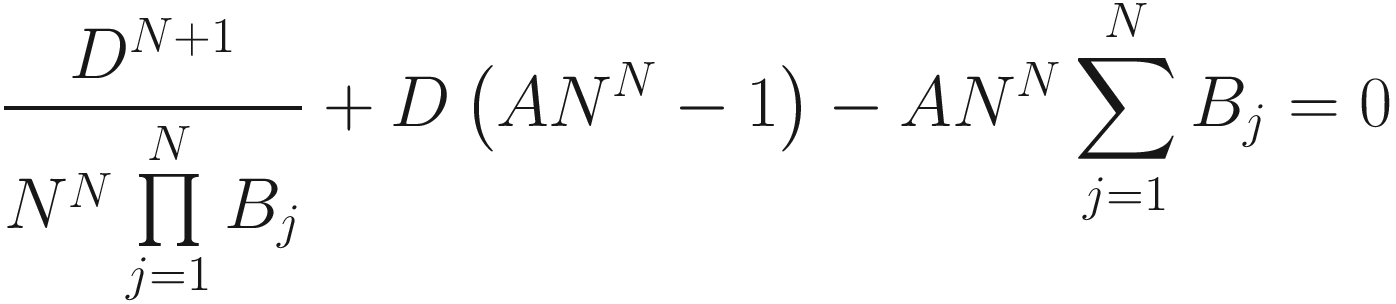

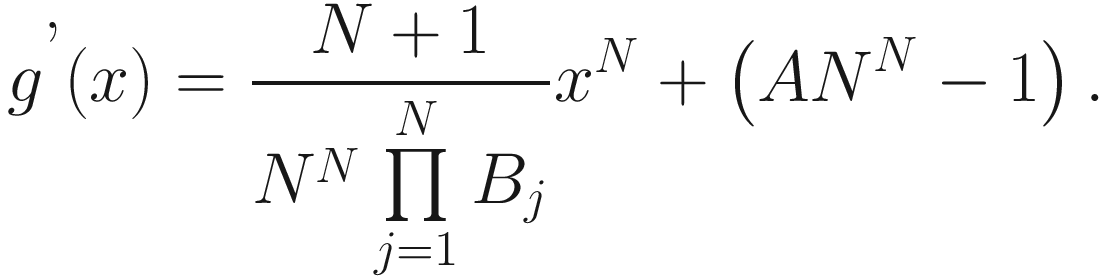

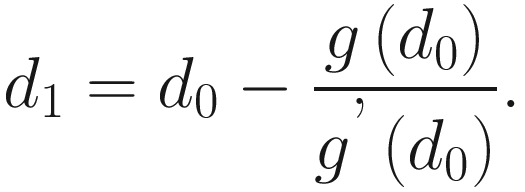

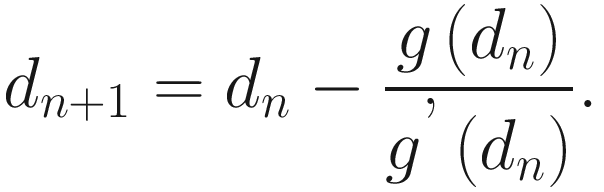

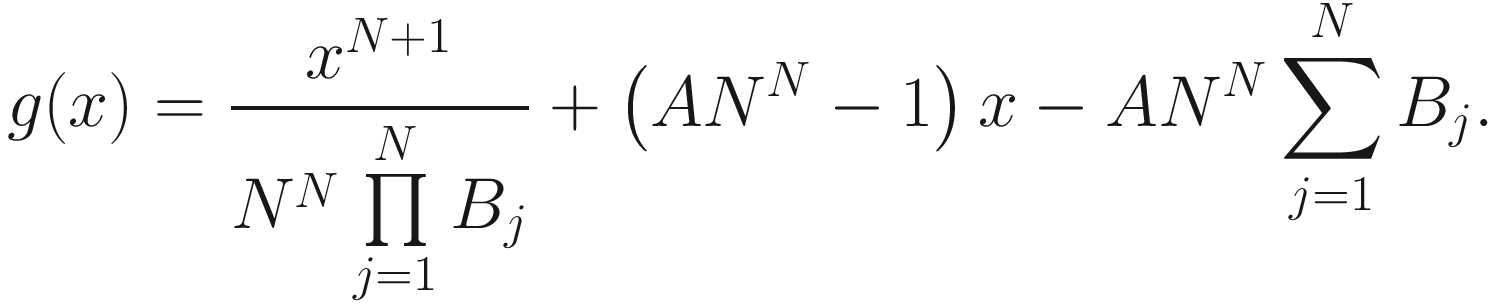

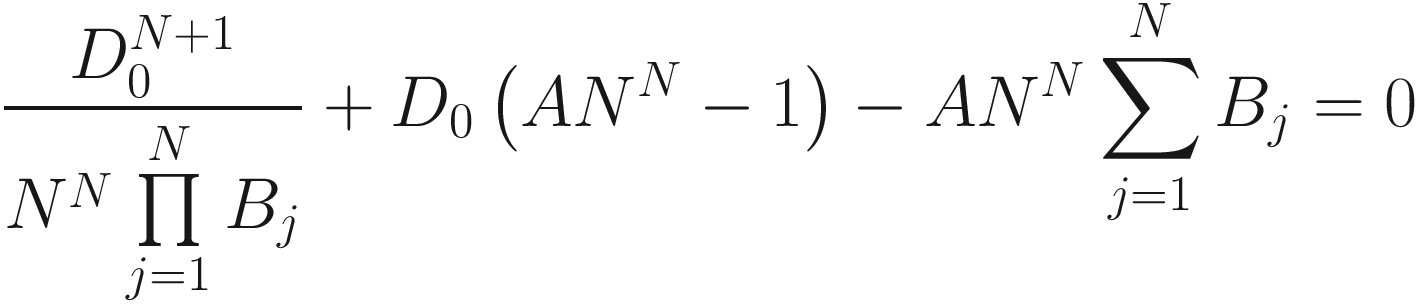

4.2.1 Finding the Parameter D

which follows from the invariant Equation 4.2.

(because the leading coefficient of g is a positive number), we obtain that g has at least one root in the interval (0, +∞). Therefore, g has exactly one positive root, and thus, the parameter D is well defined.

The process ends when the desired precision has been obtained, that is, when the difference between two consecutive terms, dk and dk + 1, is smaller than a certain number.

get_D function of the smart contract of StableSwap

4.3 Trading Formulae

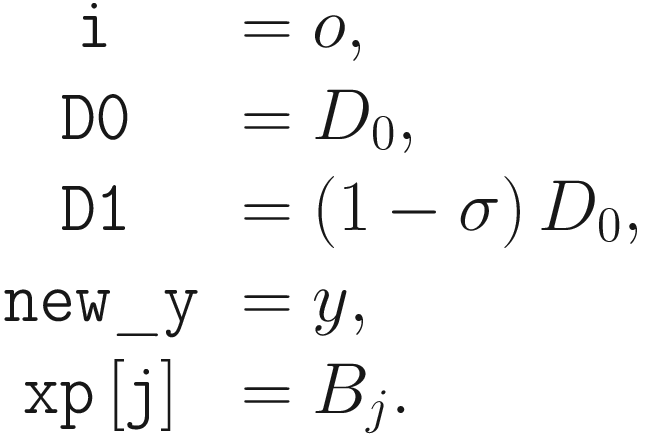

Consider a StableSwap liquidity pool of N tokens and no fees and let B1, B2, …, BN be the balances of the tokens in the pool. Let D0 be the value of the pool parameter D. Let i, o ∈ {1, 2, …, N}. As in the previous chapters, we want to compute the amount Ao of token o that a trader will receive when depositing a certain amount Ai of token i. For each j ∈ {1, 2, …, N}, let  be the balance of token j after the trade. Clearly,

be the balance of token j after the trade. Clearly,  and

and  for all j ∈ {1, 2, …, N} − {i, o}. For simplicity, let

for all j ∈ {1, 2, …, N} − {i, o}. For simplicity, let  . Note that Ao = Bo − y. We will compute y. From the previous section, we know that the value of y can be obtained by solving the quadratic Equation 4.3 and is given by

. Note that Ao = Bo − y. We will compute y. From the previous section, we know that the value of y can be obtained by solving the quadratic Equation 4.3 and is given by  following Definition 4.1.

following Definition 4.1.

get_y function of the smart contract of StableSwap

4.3.1 Taking Fee into Consideration

This last formula is the one that appears in the code of the StableSwap AMM, as we can see in Listing 4-3.

exchange function of the smart contract of StableSwap

Token 1 | Token 2 | Token 3 | |

USDC | DAI | USDT | |

Bj | 100,000 | 120,000 | 80,000 |

Suppose that the fee of the pool is 0.03%, that the pool administrative fee is 50%, and that the value of the amplification coefficient A is 500.

Applying the algorithm described by Equation 4.5, we obtain that the value of D is approximately 299,999. Observe that it is very close to the sum B1 + B2 + B3 of the balances of each token, which is 100,000+120,000+80,000=300,000.

Observe that the balance of USDC in the pool has decreased by approximately 100,000 - 90,001.21 = 9,998.79, and since just 9,997.29 USDC are given to the trader, we obtain that the difference between those amounts—1.5 USDC—has been charged as an administrative fee to the liquidity providers, since an additional amount of 1.5 USDC has been removed from the pool.

Note also that if there had been no fees, the trader would have received approximately 100,000 – 89,999.71 = 10,000.29 USDC (this is 3 USDC more than the amount they received when fees were considered), and thus, the balance of USDC in the pool would have been 100,000 - 10,000.29 = 89,999.71 (which is represented by y). Therefore, the pool now has 90,001.21 - 89,999.71 = 1.5 USDC more than it would have had if there were no fees. As we can see, the trader has been charged a fee of 3 USDC, and from this amount, 1.5 USDC goes into the pool, and the other 1.5 USDC is reserved separately as an administrative fee of the protocol.

USDC | DAI | USDT | |

Bj | 90,001.21 | 120,000 | 90,000 |

Also, after the trade, the parameter D is recalculated with the algorithm given by Equation 4.5, and we have that the new value for the parameter D is approximately 300,000.57.

4.4 All-Asset Deposit

In a similar way as with Uniswap and Balancer, liquidity providers can deposit assets into a StableSwap pool in order to earn trading fees. In exchange for their deposit, they receive StableSwap LP tokens, which represent ownership of the assets contained in the pool. During the pool trading activity, the fees from swaps accrue into the pool, resulting in added value for the StableSwap LP tokens. In this section, we will describe how the all-asset deposit works in the StableSwap AMM.

for all i, j ∈ {1, 2, …, N}.

be the share that the new liquidity provider adds to the pool. Hence, they will receive a share q of the amount of existent StableSwap LP tokens; that is, they will receive an amount qM of StableSwap LP tokens. Note also that for all j ∈ {1, 2, …, N},

be the share that the new liquidity provider adds to the pool. Hence, they will receive a share q of the amount of existent StableSwap LP tokens; that is, they will receive an amount qM of StableSwap LP tokens. Note also that for all j ∈ {1, 2, …, N},

and thus, xj = qBj for all j ∈ {1, 2, …, N}. Hence, in order to receive a share q of the existent StableSwap LP tokens, the liquidity provider has to deposit, for each j ∈ {1, 2, …, N}, an amount qBj of token j.

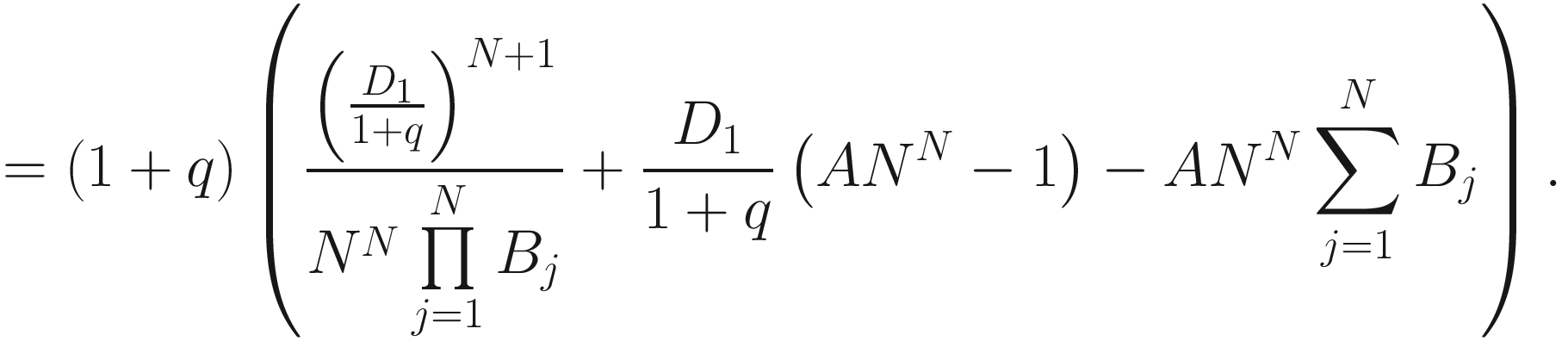

be the balances of the tokens in the pool after the deposit. Note that

be the balances of the tokens in the pool after the deposit. Note that  for all j ∈ {1, 2, …, N}. From Equation 4.4, we know that D0 and D1 satisfy

for all j ∈ {1, 2, …, N}. From Equation 4.4, we know that D0 and D1 satisfy

Note that both D0 and  are positive solutions of the equation g(x) = 0, and hence,

are positive solutions of the equation g(x) = 0, and hence,  since the map g has exactly one positive root (see subsection 4.2.1). Thus, D1 = (1 + q)D0.

since the map g has exactly one positive root (see subsection 4.2.1). Thus, D1 = (1 + q)D0.

Before deposit | After deposit | |

Balance of token j | Bj | (1 + q)Bj |

Value of parameter D | D0 | (1 + q)D0 |

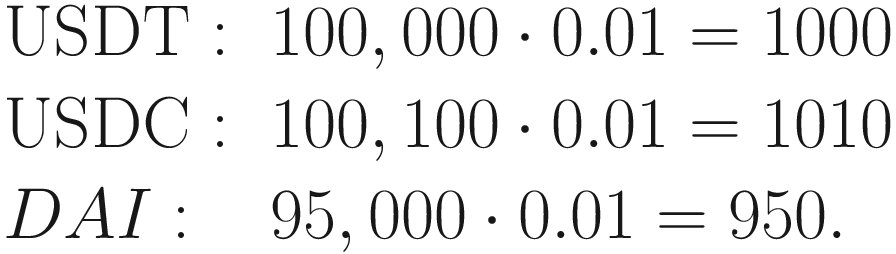

USDT | USDC | DAI | |

Bj | 100,000 | 101,000 | 95,000 |

Suppose, in addition, that the current number of StableSwap LP tokens in circulation is 10,000.

In addition, they will receive an amount of 10,000.0.01 = 100 StableSwap LP tokens.

4.5 All-Asset Withdrawal

We will now analyze the case in which a liquidity provider redeems StableSwap LP tokens. Suppose that the liquidity provider owns an amount m of StableSwap LP tokens, and let M be the amount of StableSwap LP tokens in circulation. Let  ; that is, σ is the share of the pool that the liquidity provider owns. Let B1, B2, …, BN be the balances of the tokens in the pool. Clearly, in return for the amount m of StableSwap LP tokens, the liquidity provider will receive, for each j ∈ {1, 2, …, N}, an amount σBj of token j.

; that is, σ is the share of the pool that the liquidity provider owns. Let B1, B2, …, BN be the balances of the tokens in the pool. Clearly, in return for the amount m of StableSwap LP tokens, the liquidity provider will receive, for each j ∈ {1, 2, …, N}, an amount σBj of token j.

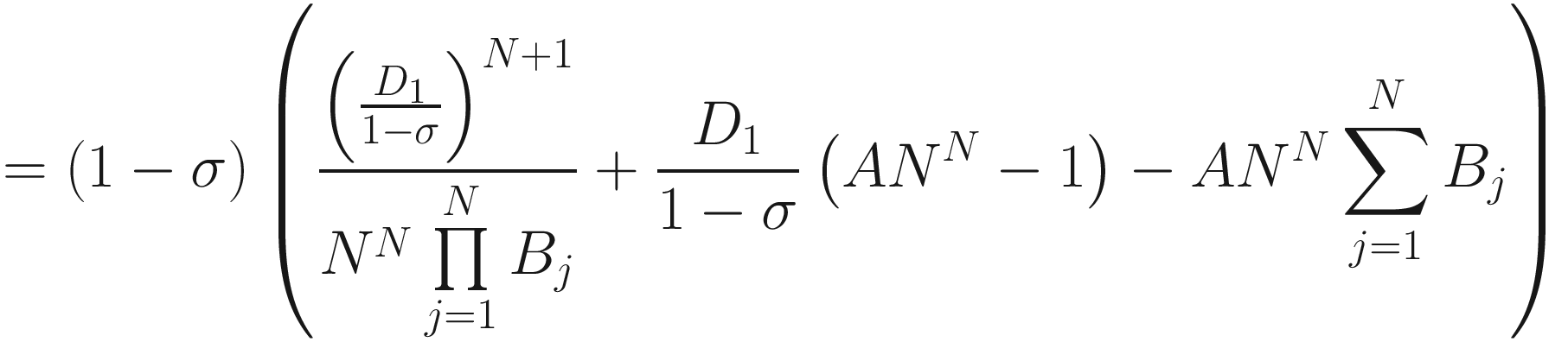

Note also that for all j ∈ {1, 2, …, N}, the balance of token j in the pool after the all-asset withdrawal is Bj − σBj = (1 − σ)Bj. As we did in the case of the all-asset deposit, we will prove that the parameter D changes in the same proportion as the balances of the tokens of the pool. That is, we will prove that if the value of the parameter D is D0 before the all-asset withdrawal, then its value after the withdrawal is (1 − σ)D0.

Note that both D0 and  are positive solutions of the equation g(x) = 0, and hence,

are positive solutions of the equation g(x) = 0, and hence,  since the function g has exactly one positive root (see subsection 4.2.1). Thus, D1 = (1 − σ)D0.

since the function g has exactly one positive root (see subsection 4.2.1). Thus, D1 = (1 − σ)D0.

Before withdrawal | After withdrawal | |

Balance of token j | Bj | (1 − σ)Bj |

Value of parameter D | D0 | (1 − σ)D0 |

Observe that the parameter D plays the same role as the parameter V in Balancer (and as the parameter L in Uniswap v2), meaning that for liquidity deposits (or withdrawals), the amount of tokens minted (or burned) is reflected in the change of the parameter D.

USDT | USDC | DAI | |

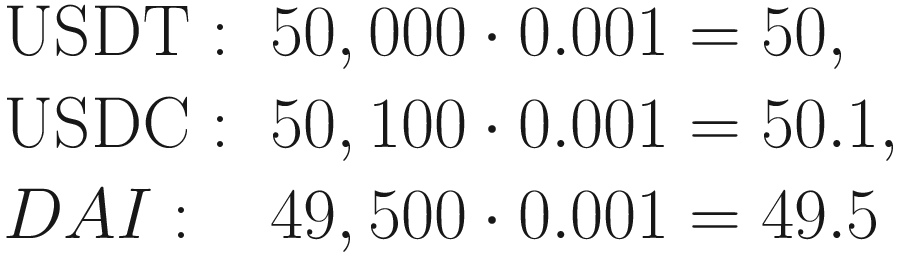

Bj | 50,000 | 50,100 | 49,500 |

; that is, the liquidity provider owns 0.1% of the pool. If they decide to redeem their StableSwap LP tokens by performing an all-asset withdrawal, they will obtain the following amounts of each token:

; that is, the liquidity provider owns 0.1% of the pool. If they decide to redeem their StableSwap LP tokens by performing an all-asset withdrawal, they will obtain the following amounts of each token:

4.6 Single-Asset Withdrawal

We will now tackle the single-asset withdrawal feature of Curve Finance. Suppose that we have a StableSwap pool that has N tokens with balances B1, B2, …, BN and that the pool has a nonzero fee ϕ. Assume that a liquidity provider owns a share σ of all the StableSwap LP tokens and that instead of redeeming a proportion σ of each of the tokens of the pool, they want to obtain all their share in terms of just one token of the pool, say, token o. Let D0 be the value of the parameter D before the withdrawal. If we were to perform an all-asset withdrawal, the value of the parameter D after the withdrawal would be (1 − σ)D0, as we saw in the previous section. Thus, it makes sense to use this value of D to calculate the amount of token o that will be left after the single-asset withdrawal since the parameter D also reflects the liquidity of the pool in a certain sense.

Before withdrawal | After withdrawal | |

Balance of token o | Bo | y |

Balance of token j, with j ≠ o | Bj | Bj |

Value of parameter D | D0 | (1 − σ)D0 |

Therefore, if there were no fees, the liquidity provider would have to receive an amount Bo − y of token o (note that y < Bo by Proposition 4.1). However, since the liquidity provider receives only one token, the proportions of the tokens in the pool are modified, and thus, several spot prices also change, as occurred with the Balancer AMM. Thus, a fee has to be charged, in a similar way as when a trade is performed.

After AAW | After SAW | |

Balance of token o | (1 − σ)Bo | y |

Balance of token j, with j ≠ o | (1 − σ)Bj | Bj |

Value of parameter D | (1 − σ)D0 | (1 − σ)D0 |

It will be reasonable to charge the fee on the difference between the balances of the tokens in both situations, since a direct single-asset withdrawal should be equivalent to an all-asset withdrawal followed by the corresponding trades, that is, trading, for each j∈ {1, 2, …, N} − {o}, the amount σBj of token j received in the all-asset withdrawal so as to obtain token o. Hence, for each j∈ {1, 2, …, N} − {o}, the fee on token j should be ϕσBj (note that here we are considering charging fees on the way in). Therefore, if we consider the situation of an all-asset withdrawal followed by the corresponding trades, for each j ∈ {1, 2, …, N} − {o}, the balance of token j in the pool after the trades will be (1 − σ)Bj + σBj = Bj as expected. However, in order to obtain the amount of token o that the liquidity provider should receive, we have to compute the balance of token o with respect to the balances of all the other tokens considering that the liquidity provider deposits an amount σBj − ϕσBj of token j, due to the fees that are charged. In addition, the value of the parameter D to be considered is (1 − σ)D0, that is, the same value as after the all-asset withdrawal, since in a trade, the value of D is preserved in order to compute the amount of tokens that should be given to the trader (as if there were no fees) and then when the fees are charged, the value of parameter D is updated. Observe that a similar situation occurs in Uniswap v2 and in Balancer’s AMMs.

State | |

Balance of token j, with j ≠ o | Bj − ϕσBj |

Balance of token o | yʹ |

Value of parameter D | (1 − σ)D0 |

where for each  .

.

Function used for the single-asset withdrawal in the smart contract of StableSwap

Performing a single-asset withdrawal

Performing an all-asset withdrawal followed by some trades to obtain the token they want

Token 1 | Token 2 | Token 3 | |

USDC | DAI | USDT | |

Bj | 1,800,000 | 1,400,000 | 800,000 |

Suppose that the fee of the pool is 0.03%, the administrative pool fee is 50%, and the value of the amplification coefficient A is 500.

We now apply the algorithm given by Equation 4.5 to compute the value of the parameter D at the state of the pool given by the previous table, obtaining D ≈ 3,999,947.93. This value will be called D0.

Suppose first that the liquidity provider decides to perform a single-asset withdrawal. By Equation 4.6, the amount of USDC that the liquidity provider receives is Bo − yʹ − ϕ((1 − σ)Bo − y), where Bo is the balance of USDC in the pool, σ = 0.01, and where y and yʹ are the amounts of USDC that correspond to the following states of the pool:

State A | State B | |

Balance of USDC | y | yʹ |

Balance of DAI | 1,400,000 | (1 − 0.0003 0.01)⋅1,400,000 = 1,399,995.8 |

Balance of USDT | 800,000 | (1 − 0.0003 ⋅ 0.01) ⋅ 800,000 =799,997.6 |

Value of parameter | 0.99D0 | 0.99D0 |

Suppose now that the liquidity provider decides to perform an all-asset withdrawal and then trade the received amounts of DAI and USDT to obtain more USDC. Clearly, they receive 18,000 USDC, 14,000 DAI, and 8,000 USDT from the all-asset withdrawal, and after it, the updated balances of the pool are as follows:

USDC | DAI | USDT |

1,782,000 | 1,386,000 | 792,000 |

and the new value of the parameter D is 0.99D0 ≈ 3,959,948.45.

of USDC that they receive is

of USDC that they receive is

and the updated balances of DAI and USDT are 1,400,000 and 792,000, respectively. Also, the new value of the parameter D, which is obtained by applying the algorithm given by Equation 4.5, is D1 ≈ 3,959,950.55.

of USDC that they receive is

of USDC that they receive is

. Thus,

. Thus,

that is, the liquidity provider receives 7,999.49 USDC more.

which is a bit more than the 39,989.44 USDC they obtain performing a single-asset withdrawal.

4.7 StableSwap LP Token Swap

As we did in the previous chapters, consider two different (Uniswap, Balancer, or StableSwap) pools, P1 and P2, respectively. Let LP1 and LP2 be the LP tokens of pools P1 and P2, respectively. We want to compute the fair swap price between LP1 and LP2. To this end, we will calculate the total value of each of the pools in terms of a chosen token Z, and then we will compute the value of tokens LP1 and LP2 in terms of token Z so as to find the fair swap price.

We will now give two examples where we will compute the fair swap price between StableSwap LP tokens and LP tokens of different pools.

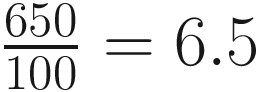

Alice | Bob | |

Pool | Balancer | StableSwap |

Supply of pool tokens | 10,000 | 20,000 |

Token X | ETH | USDC |

Token Y | BTC | USDT |

Balance of token X | 1,300 | 1,000,000 |

Balance of token Y | 25 | 1,000,500 |

Weight of token X | 0.8 | — |

Weight of token Y | 0.2 | — |

Thus, the price of each of Alice’s tokens in terms of Bob’s tokens is  , which means that if Alice gives Bob 1 of her tokens from the Balancer pool, she will get 6.5 of Bob’s tokens from the StableSwap pool in return.

, which means that if Alice gives Bob 1 of her tokens from the Balancer pool, she will get 6.5 of Bob’s tokens from the StableSwap pool in return.

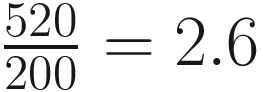

Alice | Bob | |

Pool | Uniswap v2 | StableSwap |

Supply of pool tokens | 20,000 | 10,000 |

Token X | ETH | USDC |

Token Y | BTC | USDT |

Balance of token X | 1,300 | 1,000,000 |

Balance of token Y | 100 | 1,000,500 |

Thus, the price of each of Alice’s tokens in terms of Bob’s tokens is  ; that is, if Alice gives Bob 1 of her Uniswap LP tokens, she will get 2.6 of Bob’s StableSwap LP tokens in return.

; that is, if Alice gives Bob 1 of her Uniswap LP tokens, she will get 2.6 of Bob’s StableSwap LP tokens in return.

4.8 Summary

In this chapter, we explained how the invariant formula for the StableSwap AMM is obtained and how trades are performed. We also showed how liquidity can be deposited and withdrawn and gave a detailed description of the single-asset withdrawal feature.

In the next chapter, we will study the Uniswap v3 AMM, which introduces concentrated liquidity. As we shall see, the design of the Uniswap v3 AMM is very different from those of the AMMs that we have described before.