Uniswap v2 is a decentralized exchange based on a system of smart contracts on the Ethereum blockchain and other networks (such as Polygon, Optimism, Arbitrum). It is formed by liquidity pools that enable automated market making; that is, they enable traders to buy and sell assets against the protocol without the need for a third party. Each Uniswap v2 liquidity pool consists of reserves of two ERC-20 tokens deposited by liquidity providers, who benefit from the fees that the protocol charges to traders. The collected fees are shared proportionally among all liquidity providers.

Uniswap v2 liquidity pools are based on a product formula that considers the amount of reserves of each of the two tokens of the pool. This product formula plays a crucial role in determining the amounts of each token involved in any trade. Consequently, the product formula determines the price of one of the pool tokens in terms of the other. Moreover, the price of an asset in a Uniswap v2 liquidity pool follows the actual market price of that asset due to the actions of external arbitrageurs, who detect price inconsistencies between the market price and the internal price of the liquidity pool and make a trade in order to gain an instant benefit from the difference between the said prices, making the internal price of the oracle once again equal to the market price.

In this chapter, we will explain in detail how the Uniswap v2 AMM works and delve into the mathematical concepts behind it. We will explain how the trading formulae and the spot price formula are derived from the product formula and show how liquidity providers can deposit and remove liquidity from the liquidity pools. In the process, we will analyze several interesting questions and give various illustrative examples.

2.1 Trading in a Uniswap v2 pool

where L is a positive number that is called liquidity parameter of the pool. For the moment, we will assume that L is a constant value. We will see later how the liquidity parameter L can change.

Pool states before and after the trade in a pool with no fees

We will now analyze how the constant product formula works in the general case in order to obtain several important formulae that will be used throughout this chapter. We will assume first that the liquidity pool has no fees.

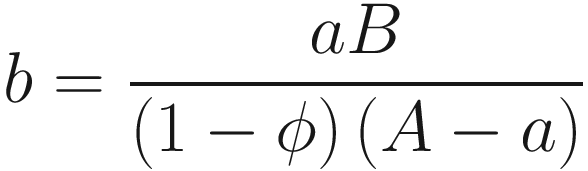

This means that in order to receive an amount a of token X, the trader must deposit an amount  of token Y.

of token Y.

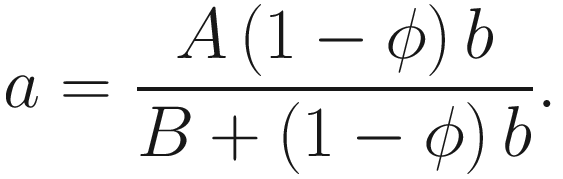

This means that if the trader deposits an amount b of token Y, they will receive an amount  of token X.

of token X.

2.1.1 Spot Price

A fundamental concept is that of the spot price. The spot price of token X in terms of token Y is defined as the price we pay per token X that we receive after depositing an infinitely small amount of token Y. In order to study the spot price and obtain a formula to compute it, we need to give a more formal definition.

Let A and B be the balances in the pool of tokens X and Y, respectively. Suppose that a trader deposits an amount b of token Y and receives an amount a of token X. Then, the price that the trader paid for each unit of token X is ![]() . We also say that

. We also say that ![]() is the effective price (of token X in terms of token Y ) paid by the trader.

is the effective price (of token X in terms of token Y ) paid by the trader.

Let p be the spot price of token X in terms of token Y and let pe(b) be the effective price (of token X in terms of token Y) paid by the trader when depositing an amount b of token Y.

(recall that a depends on b ).

Hence, the spot price when the pool state is (A, B) is equal to  , which coincides with the slope of the line that passes through the origin (0, 0) and the point (A, B).

, which coincides with the slope of the line that passes through the origin (0, 0) and the point (A, B).

which is small if the deposited amount b is small with respect to the balance A of token X. This means that for pools with large liquidity, this difference will be small.

by Equation 2.5.

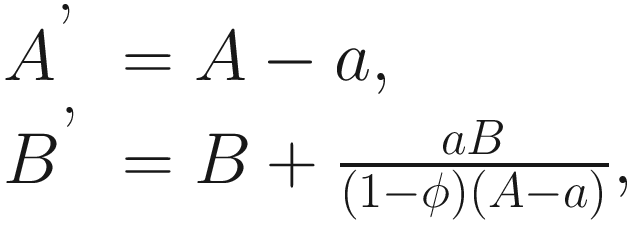

, which coincides with the slope of the line segment that goes from (0,0) to (A, B) (this is the dotted segment of Figure 2-2). Note also that if the state of the pool before a trade is P = (A, B) and the state of the pool after that trade is P′ = (A′, B′) = (A − a, B + b), then the effective price that the trader paid for each unit of token X is

, which coincides with the slope of the line segment that goes from (0,0) to (A, B) (this is the dotted segment of Figure 2-2). Note also that if the state of the pool before a trade is P = (A, B) and the state of the pool after that trade is P′ = (A′, B′) = (A − a, B + b), then the effective price that the trader paid for each unit of token X is

Geometric interpretation of the spot price and the price impact

as expected. We can also see this in Figure 2-2.

Regarding the price impact, since the slope of the tangent line is the opposite of the spot price p, it follows that in Figure 2-2, q = ap, and hence, q is the amount of token Y that would have been paid if the whole trade had been executed at the spot price. Therefore, we obtain that the price impact s is equal to b – q, and hence, it can be interpreted as the length of the dashed segment labelled r of Figure 2-2.

which is more than the spot price p. This means that the trader paid 5,000 USDC for each ETH.

is the price impact of the trade, which can be seen as a loss for the trader.

2.1.2 Accounting for Fees

Equations 2.2 and 2.3 are valid if the liquidity pool has no fees, but in general, traders are charged a fee for trading. The collected fees are added to the pool reserves and then paid to liquidity providers in a way that is proportional to the deposits they have made.

Trading mechanism with fees

This means that if the trader deposits an amount b of token Y, they will receive an amount  of token X.

of token X.

This means that in order to receive an amount a of token X, the trader has to deposit an amount  of token Y.

of token Y.

Equations 2.7 and 2.8 are covered by the portion of the Uniswap v2 code2 given in Listing 2-1, applying the following translation between the variables of the code and our notation:

reserveIn = B,

reserveOut = A,

amountIn = b,

amountOut = a,

Functions getAmountOut and GetAmountIn of the smart contract of Uniswap v2

Note that (L′)2 > L2 if ϕ > 0. That is, if the liquidity pool has nonzero fees, then the liquidity parameter will increase a bit after each transaction.

Change of the pool state when trading in a pool with no fees

On the other hand, if the liquidity pool has a nonzero fee ϕ, then the liquidity parameter increases after each trade (this is L′ > L with the previous notations). If the pool reserves before a trade are A and B, and a trader deposits an amount b of token Y and receives an amount a of token X, then

Change of the pool state when trading in a pool with fees

Note that the absolute value of the slope of the segment between the points P = (A,B) and P′ = (A − a, B + b) shown in Figure 2-5 is exactly the deposited amount of token Y per unit of token X, that is, the effective price paid by the trader.

2.2 Impact of the Trades on the Price

When a trade is executed, the balances of the tokens in the pool change, and as a consequence of the trade, the spot price also changes. In this section, we will perform several analyses to show how the spot price varies when trades occur.

2.2.1 A Simple Example

We will give first a simple example that shows how the spot price of a token increases after a trader purchases an amount of it.

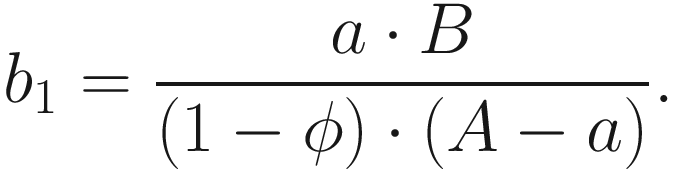

Example 2.2 (Shift in the average buy price). Consider a Uniswap v2 pool with ETH and USDC, having a fee of 0.3%. Suppose that the pool has reserves of 10,000 ETH and 40,000,000 USDC. Let A = 10,000 and B = 40,000,000. Note that the spot price is 4,000 USDC/ETH.

This means that the trader has to deposit approximately 2,346,573 USDC in order to obtain 500 ETH. This is equivalent to an average price of roughly 4,693 USDC/ETH. We find that the price of ETH in terms of USDC has increased due to the fact that the amounts of USDC and ETH have respectively increased and decreased reflecting a higher demand for ETH and thus a higher price for ETH in terms of USDC.

since B < B + b1 and A − a > A − 2a.

2.2.2 Analysis of Two Consecutive Trades

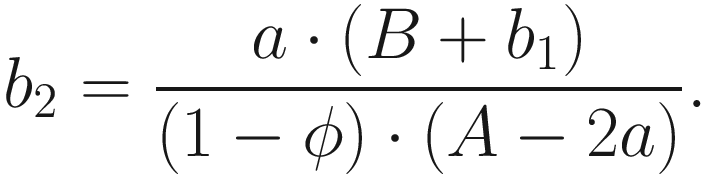

We will now extend the previous example to study if there is any difference between buying 500 ETH in only one trade and buying 500 ETH in two consecutive trades of 250 ETH each.

Example 2.3 (ETH purchase price comparison). Consider again a liquidity pool of 10,000 ETH and 40,000,000 USDC. Let A = 10, 000 and B = 40,000,000.

that is, the amount of USDC that has to be paid in order to buy 500 ETH in one step is the same as the amount of USDC needed to buy 500 ETH in two consecutive steps of 250 ETH each.

Comparison between making a trade in one step and dividing it into two trades in a pool with no fees

Hence, in order to buy 500 ETH in two steps, we need to pay approximately 1,028,727 + 1,082,952 = 2,111,679 USDC, which is more than the 2,111,598 USDC needed to buy 500 ETH in one step.

Comparison between making a trade in one step and dividing it into two trades in a pool with fees

The following proposition formalizes and generalizes the results of the previous example.

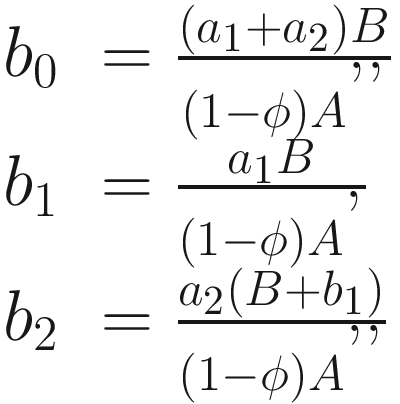

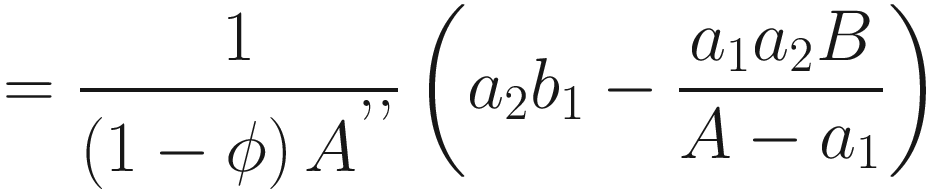

Proposition 2.1. Consider a liquidity pool with two tokens X and Y and with fee ϕ ∈ [0, 1). Let A be the balance of token X in the pool and let B be the balance of token Y in the pool. Let a1, a2 > 0 such that a1 + a2 < A. Let b0 be the amount of token Y needed to buy a1 + a2 tokens X, let b1 be the amount of token Y needed to buy a1 tokens X, and let b2 be the amount of token Y needed to buy a2 tokens X after a1 tokens X have been purchased. Then b0 ≤ b1 + b2 and the equality holds if and only if ϕ = 0.

Thus, b1 + b2 − b0 ≥ 0 and b1 + b2 − b0 = 0 if and only if ϕ = 0. The result follows. □

2.2.3 Impact of the Trade Size on the Average Purchase Price

In practice, traders often buy many tokens at once, and as we have seen in Example 2.2, every token costs more than the previous one. We will now analyze this in more detail. Consider a liquidity pool with tokens X and Y and trading fee ϕ. Let A and B be the balances of tokens X and Y in the pool. Suppose that a trader deposits an amount b of token Y and receives an amount a of token X (hence, they buy token X ).

We will study these formulae in the following example.

Price impact: impact of the traded amount on the purchase price

2.2.4 Impact of the Trade Size on the Average Sell Price

We will study these formulae in the following example.

Price impact: impact of the amount traded on the sell price

2.2.5 Impact of the Trade Size on the Price Growth Ratio

. We want to compute the growth of the spot price after a trader buys an amount a of token X. Note that the amount of token Y the trader has to deposit to buy an amount a of token X is given by Equation 2.8. The updated balances after the trade are

. We want to compute the growth of the spot price after a trader buys an amount a of token X. Note that the amount of token Y the trader has to deposit to buy an amount a of token X is given by Equation 2.8. The updated balances after the trade are

; that is, r is the fraction of token X that the trader is buying (with respect to the balance of token X in the pool). Using the fact that

; that is, r is the fraction of token X that the trader is buying (with respect to the balance of token X in the pool). Using the fact that  , we can write the updated spot price p′ in terms of p and r as follows:

, we can write the updated spot price p′ in terms of p and r as follows:

. In Figure 2-10, we plot (in solid line) the price increment as a function of the fraction r of token X bought (in percentage) in the range (0, 10], and we compare it with a linear function.

. In Figure 2-10, we plot (in solid line) the price increment as a function of the fraction r of token X bought (in percentage) in the range (0, 10], and we compare it with a linear function.

Percentage of price increment as a function of the percentage of token X bought

Percentage of price increment as a function of the percentage of token X bought

2.3 Providing Liquidity

In this section, we will explain how liquidity providers can add liquidity to a Uniswap v2 pool and how they can withdraw the liquidity they have deposited. We will also analyze the possible impermanent losses that a liquidity provider might face. In the last part of this section, we will explain how to set a fair price for a liquidity provider’s position.

2.3.1 Minting LP Tokens

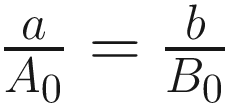

When a liquidity provider wants to provide liquidity to a Uniswap v2 pool, they need to deposit amounts of tokens X and Y that are in a proportion defined by the state of the pool. By doing so, they will be given specific tokens, called liquidity pool tokens—or LP tokens—which represent the share of the pool they own. The liquidity provider will also earn trading fees according to that share. Note that that share will vary when either new liquidity providers enter the pool or existing ones leave the pool.

that is, the amounts of tokens X and Y that the liquidity provider deposits have to be in the same proportion as that of the pool reserves. Observe that the spot price after the deposit is  , which is the same as the original spot price

, which is the same as the original spot price  since

since  (and thus, A(B + b) = B(A + a)).

(and thus, A(B + b) = B(A + a)).

Minting LP tokens

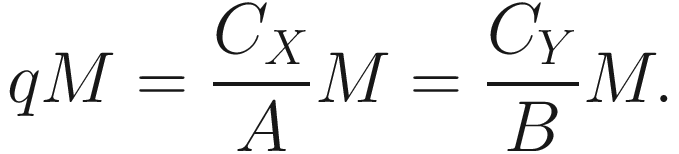

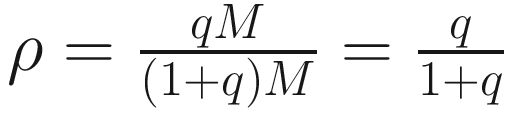

The new liquidity provider will receive an amount qM of LP tokens. This means that an amount qM of LP tokens will be newly minted and that the total amount of existent LP tokens will be updated to M + qM = (1 + q)M.

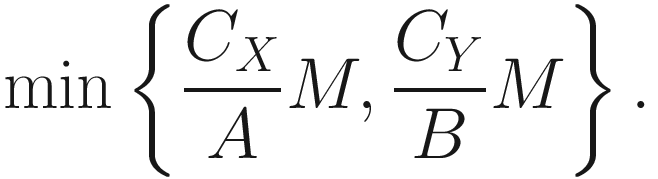

The Uniswap v2 AMM does not require the liquidity provider to find the exact amounts to deposit. Instead, given amounts CX of token X and CY of token Y that the liquidity provider has available for the deposit, the protocol computes the maximum amounts of tokens X and Y that the liquidity provider can deposit to preserve the pool proportions, and gives the remaining amount of either token X or token Y that was not deposited back to the liquidity provider, together with the LP tokens that correspond to the deposit. This feature is particularly useful due to the ever-changing nonpredictable pool state arising from the fact that the AMM is decentralized. Indeed, if a liquidity provider computes at a certain moment the amounts that they need to deposit, by the time the transaction is processed, the pool state could be different, since other pool transactions could have been processed first, and hence, the amounts needed for the liquidity deposit might have changed.

Case 1:

.

.

. Then, the liquidity provider will receive an amount qM of LP tokens. Note that

. Then, the liquidity provider will receive an amount qM of LP tokens. Note that

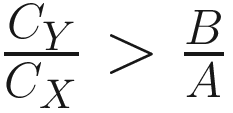

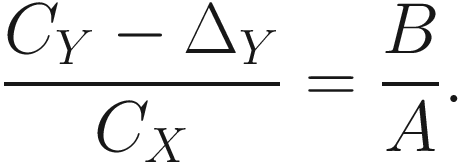

Case 2:

Since  , we obtain that

, we obtain that  . Then

. Then  .

.

, and hence,

, and hence,  . This means that the amounts CX and CY − ΔY are in the right proportions. We define then

. This means that the amounts CX and CY − ΔY are in the right proportions. We define then  . Hence, the liquidity provider will be given back an amount ΔY of token Y and will receive an amount qM of LP tokens. Note that

. Hence, the liquidity provider will be given back an amount ΔY of token Y and will receive an amount qM of LP tokens. Note that

Case 3:

Since  , we obtain that

, we obtain that  . Then

. Then  .

.

and hence

and hence  . This means that the amounts CX − ΔX and CY are in the right proportions. We define then

. This means that the amounts CX − ΔX and CY are in the right proportions. We define then  . Hence, the liquidity provider will be given back an amount ΔX of token X and will receive an amount qM of LP tokens. Note that

. Hence, the liquidity provider will be given back an amount ΔX of token X and will receive an amount qM of LP tokens. Note that

In the code given in Listing 2-2, we can find the previous formula.3 The translation between the variables of the code and our notation is

totalsupply = M,

amount0 = CX,

amount1 = CY,

_eserve0 = A,

_eserve1 = B,

liquidity = qM.

mint function of the smart contract of Uniswap v2

Starting the Pool

. In this case, the liquidity provider will receive an amount of LP tokens defined by

. In this case, the liquidity provider will receive an amount of LP tokens defined by

Portion of the mint function of the smart contract of Uniswap v2

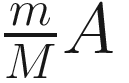

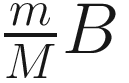

2.3.2 Burning LP Tokens

Burning LP tokens

We will now explain in detail how this works. Consider a Uniswap v2 liquidity pool with tokens X and Y. Let A and B be the corresponding amounts of tokens X and Y in the pool. Let M be the amount of existent LP tokens and let m be the amount of LP tokens that the liquidity provider wants to redeem. Clearly, the amount m of LP tokens corresponds to a share  of the pool. Therefore, in exchange for the amount m of LP tokens, the liquidity provider will receive an amount

of the pool. Therefore, in exchange for the amount m of LP tokens, the liquidity provider will receive an amount  of token X and an amount

of token X and an amount  of token Y. The amount m of LP tokens deposited by the liquidity provider will be burned, and the amount of existent LP tokens will be updated to M – m. Clearly, the pool reserves will also be updated to

of token Y. The amount m of LP tokens deposited by the liquidity provider will be burned, and the amount of existent LP tokens will be updated to M – m. Clearly, the pool reserves will also be updated to  for token X and

for token X and  for token Y.

for token Y.

The formula for the amount of each token that the liquidity provider has to receive when redeeming LP tokens is covered by the burn function of Uniswap v2,5 which is given in Listing 2-4, with the following translation between the variables of the code and our notation:

burn function of the smart contract of Uniswap v2

Distribution of Fees

Visualizing how liquidity providers earn trading fees

2.3.3 Pool Value and Impermanent Loss

, and hence, the value of the amount A of token X that the pool has in terms of token Y is

, and hence, the value of the amount A of token X that the pool has in terms of token Y is  . And since the value of the amount B of token Y in the pool is B, we obtain that the total value of the pool in terms of token Y is

. And since the value of the amount B of token Y in the pool is B, we obtain that the total value of the pool in terms of token Y is

that is, a fraction ρ of the whole pool value, as expected.

Computing Impermanent Loss Without Fees

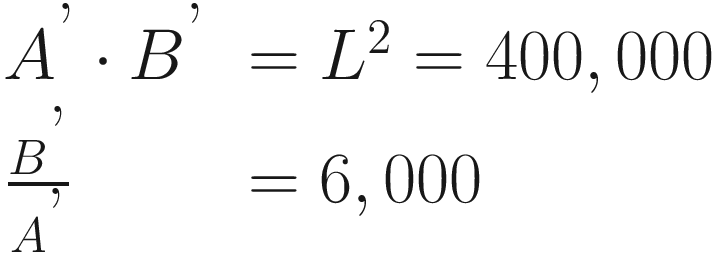

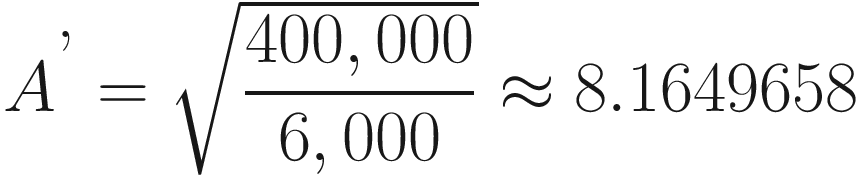

Consider a Uniswap v2 liquidity pool with no fees having 9 ETH and 36,000 USDC. Suppose that the existent amount of LP tokens is 90 and that a liquidity provider adds 1 ETH and 4,000 USDC to the pool. Thus, the pool balances after the deposit are 10 ETH and 40,000 USDC, and the liquidity parameter L satisfies L2 = 400,000. Note that the liquidity provider earns an amount of  tokens and that the total amount of existent LP tokens is now 100. Hence, the new liquidity provider owns a share of 10% of the existent LP tokens and thus of the total pool liquidity. Note that the spot price of ETH before and after the deposit is 4,000 USDC/ETH.

tokens and that the total amount of existent LP tokens is now 100. Hence, the new liquidity provider owns a share of 10% of the existent LP tokens and thus of the total pool liquidity. Note that the spot price of ETH before and after the deposit is 4,000 USDC/ETH.

Therefore, they are facing a loss of approximately 202.04 USDC, which amounts to a loss of approximately 2.02% with respect to holding the assets. This loss is called impermanent loss (or divergence loss) and is due to the fact that the amounts of the tokens are moving on a multiplicative inverse curve. It is called impermanent because if the ETH price reverts to the original 4,000 USDC/ETH (which is the spot price at the moment of the deposit), then the pool balances will be again 10 ETH and 40,000 USDC, and in consequence, the liquidity provider’s position will be the same as the one at the beginning and there will be no loss. But if the liquidity provider decides to withdraw their position when the price is 6,000 USDC/ETH, then the previous loss becomes permanent.

. Let

. Let  . We know that the liquidity provider receives an amount qM of LP tokens. In addition, after the deposit, the pool reserves are A = A0 + a for token X and B = B0 + b for token Y, and the total amount of LP tokens is (1 + q)M. Note that the liquidity provider owns a share

. We know that the liquidity provider receives an amount qM of LP tokens. In addition, after the deposit, the pool reserves are A = A0 + a for token X and B = B0 + b for token Y, and the total amount of LP tokens is (1 + q)M. Note that the liquidity provider owns a share  of the pool. Since

of the pool. Since  , we obtain that

, we obtain that

be the spot price after the deposit (which is the same as the spot price before the deposit, as we have previously proved). Hence,

be the spot price after the deposit (which is the same as the spot price before the deposit, as we have previously proved). Hence,

. And since the pool has no fees, we have that A′B′ = AB. Thus,

. And since the pool has no fees, we have that A′B′ = AB. Thus,

Losses of liquidity providers due to price variation compared to holding the funds supplied

Accounting for Fees

The previous analysis did not take fees into consideration. In a pool with a nonzero trading fee, all trading activities add liquidity to the pool in the form of collected fees, which increase the value of the liquidity providers’ positions and hence reduce their impermanent losses.

In order to understand how this works, we will analyze the following example. Consider a liquidity pool with ETH and USDC and with fee ϕ = 0.003. Assume that the pool has 1,000 ETH and 4,000,000 USDC. Note that the spot price is p = 4,000 USDC/ETH. Suppose that a liquidity provider owns a share of 10% of the pool.

and the new spot price is p′ ≈ 4,008.024 USDC/ETH.

In the case of a liquidity pool without trading fees (ϕ = 0) and considering the same situation as the previous one, we could perform similar computations to obtain that the liquidity provider would face an impermanent loss of approximately 0.4 USDC.

For liquidity pools with massive trading activity around the starting price, the trading fee becomes more significant for the value of the liquidity provider’s position, and the impermanent loss can sometimes be compensated, resulting in gains for the liquidity providers.

2.3.4 LP Token Swap

In this subsection, we will study the problem of swapping LP tokens of two different liquidity pools. To calculate the fair swap price, we will need to compute the values of those LP tokens.

Consider two liquidity providers, Alice and Bob, who are members of two different liquidity pools P1 and P2, which have liquidity pool tokens LP1 and LP2, respectively. Both Alice and Bob own a certain amount of LP tokens of their respective pools. Let N1 and N2 be the the total minted liquidity tokens in pools P1 and P2, respectively.

We will divide our analysis into two different cases: when the liquidity pools P1 and P2 have at least one common token and when they do not.

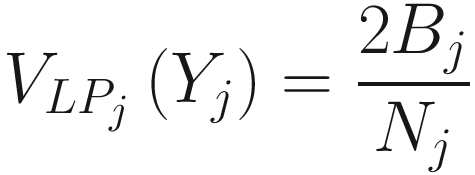

Common Token Case

Suppose first that the liquidity pools P1 and P2 have (at least) one common token Y. We want to compute the fair swap price between Alice’s and Bob’s LP tokens. In other words, we want to calculate how the values of the tokens LP1 and LP2 are related.

, and therefore,

, and therefore,

Summing up, this means that if Alice gives one LP token from pool P1 to Bob, Alice will get  tokens from pool P2 in return.

tokens from pool P2 in return.

Alice (Pool P1) | Bob (Pool P2) | |

|---|---|---|

Total LP tokens | 12,000 | 10,000 |

LP tokens owned | 100 | 100 |

Token X | ETH | ETH |

Token Y | USDC | USDC |

Amount of token X | 10,000 | 9,750 |

Amount of token Y | 40,000,000 | 39,000,000 |

Hence, if Alice swaps all her 100 LP tokens from pool P1, she will receive approximately 85.47 LP tokens from pool P2 in return. Note that, although the liquidity of pool P2 is less than that of pool P1, the amount of LP tokens minted in pool P2 is less than that of P1, resulting in a relatively higher price of the token of pool P2 compared with the token of pool P1.

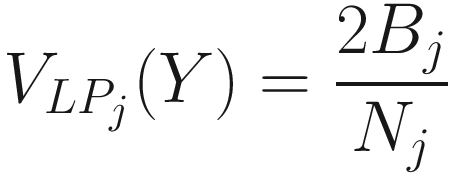

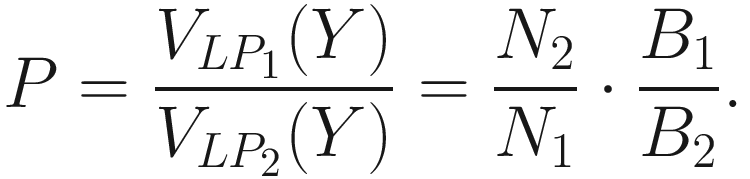

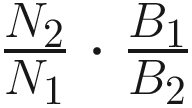

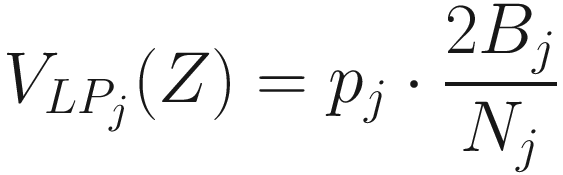

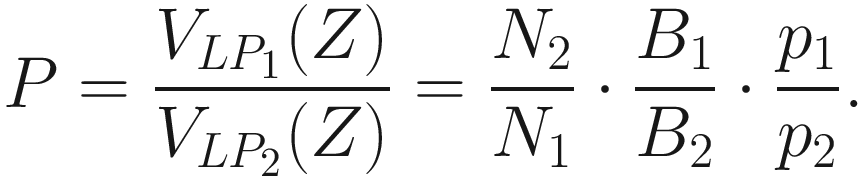

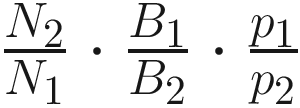

No In-Common Token Case: Oracle Swap

Suppose now that pools P1 and P2 do not have a common token. In that case, we will use external price data to express amounts of certain tokens Y1 ≠ Y2 in terms of amounts of a chosen token Z. We will need the corresponding exchange rates (or prices) to do so.

Let Y1 be a token of pool P1 and let Y2 be a token of pool P2. Suppose that Y1 ≠ Y2. For j ∈ {1, 2}, let Bj be the amount of token Yj in pool Pj. Let Z be a token, and for j ∈ {1, 2}, let pj be the price of token Yj in terms of token Z.

, and thus,

, and thus,

Summing up, this means that if Alice gives one LP token from pool P1 to Bob, Alice will get  tokens from pool P2 in return.

tokens from pool P2 in return.

Pool P1 | Pool P2 | |

|---|---|---|

Total LP tokens | 12,000 | 10,000 |

Token X | WBTC | XRP |

Token Y | ETH | DAI |

Amount of token X | 100 | 1,000,000 |

Amount of token Y | 1,200 | 800,000 |

We will use USDC as the token Z in which prices will be expressed, with exchange rates of 4,000 USDC/ETH and 1 USDC/DAI.

Thus, each LP1 token is worth 5 LP2 tokens. Note that although pool P2 has minted fewer LP tokens, the total value of pool P1 (2 ⋅ 1,200 ⋅ 4,000 = 9,600,000 USDC) is much higher than that of pool P2(2 ⋅ 800,000 ⋅ 1 = 1,600,000 USDC), resulting in a high exchange rate between the corresponding LP tokens.

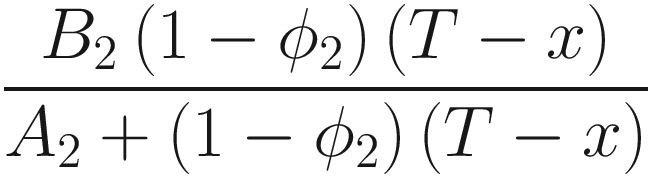

2.4 Motivating DEX Aggregators

A DEX aggregator is a blockchain-based service that functions as an explorer for the prices and liquidity offered by different Decentralized Exchanges and helps traders find the best price for their trades. In addition, DEX aggregators are equipped with an algorithm that allows users to split the trade they want to do in several trades against different AMMs so as to obtain the best possible price for that trade. Clearly, this is a very enticing service. We will develop a simple example to show why this makes sense and how one can split a trade between two different pools to obtain a better price.

Suppose that we want to trade an amount T of ETH among two different ETH/USDC pools. For example, these can be Uniswap v2 pools on two different networks or one Uniswap and one Sushiswap pool on the same network. We want to find the amount of ETH we should trade in each pool in order to receive the maximum possible amount of USDC.

and

and  . Note that

. Note that

Note that g(x) is just a polynomial of degree 2 and that for any x0 ∈ [0, T], f ′(x0) = 0 if and only if g(x0) = 0. Moreover, since the denominator of the last expression of f ′(x) is always positive, we obtain that for any x0 ∈ [0, T], f ′(x0) > 0 if and only if g(x0) > 0 (and f ′(x0) < 0 if and only if g(x0) < 0). Thus, in order to study the zeros and the sign of f ′, we can study the zeros and the sign of g. Recall that since g is a polynomial of degree 2, the zeros of g can be computed from the quadratic formula. Then the positive and negative regions of g can easily be obtained observing the concavity of g from its leading coefficient.

In the following example, we will show how the previous argument can be applied.

Pool 1 | Pool 2 | |

|---|---|---|

ETH | 10,000 | 10,300 |

USDC | 40,000,000 | 39,500,000 |

Φ | 0.3% | 0.3% |

Since the leading coefficient of g is negative, we obtain that g is positive on the interval (x1, x2) and negative on the intervals (−∞, x1) and (x2, +∞) (and we know that the same holds for f ′).

And since we are interested in computing the maximum of f on the interval [0, T], from the sign of f ′, we obtain that f is strictly increasing on the interval [0, x2] and strictly decreasing on the interval [x2, 1,500]. Thus, the function f attains a maximum on x2 ≈ 854.0514. Therefore, in order to maximize the amount of USDC received when trading 1,500 ETH, we have to sell 854.0514 ETH on pool 1 and 1,500 − 854.0514 = 645.9486 ETH on pool 2. By doing so, we will obtain f(854.0514) ≈ 5,463,115.24 USDC.

Observe that if we had performed the whole trade on pool 1, we would have received f(1,500) ≈ 5,203,775.39 USDC, and if we had performed the whole trade on pool 2, we would have received f(0) ≈ 5,008,032.72 USDC.

As we can see from the previous example, we can obtain a much better price if we split the trade between the two pools in a suitable way. However, in order to do so, we need to have all the information about the state of the two pools, and we also need to perform a lot of mathematical computations. DEX aggregators do all this work for us, and hence, they are a valuable and much appreciated tool.

2.5 Summary

In this chapter, we performed a thorough analysis of the Uniswap v2 AMM, introducing the concepts of spot price, effective price, price impact, and impermanent loss. We show how trades are performed in Uniswap v2 and how liquidity can be deposited and withdrawn.

In the next chapter, we will analyze the Balancer AMM, which is a generalization of the Uniswap v2 AMM and allows liquidity pools of more than two assets.