2

Opportunities and Challenges

Trust is the most important element that drives both a successful transaction in a business and a meaningful personal or social value exchange in a society.

—Jai Singh Arun

Aside from the Internet, which actually emerged at the end of the 20th century, blockchain is the most disruptive technology of the 21st century. It radically unravels the trust, transparency, and accountability issues in business, and opens endless opportunities for innovation across industries.

In recent decades, businesses and trade have crossed geographic boundaries and become global and open in many ways. Nevertheless, the most fundamental challenge remains trust. In many situations, would-be partners have either limited or no trust, which is why an intermediary is often required between two or more parties to complete their business transactions. Examples of such intermediaries are banks, insurance agencies, trade agencies, government agencies, credit agencies, and identity bureaus.

The transformational shift that blockchain delivers is a new way to forge trust among distrusted partners. This shift will disrupt the way that they—and you—do business. It brings many new opportunities and a shared or peer-to-peer economy for every industry and organization, including intermediaries, to reimagine and transform their business processes and business models. However, every opportunity comes with an initial challenge. Blockchain adoption is challenging when you try to address too large a scope, there are no motivations or incentives for participants, and the governance structure is cumbersome and has many stakeholders.

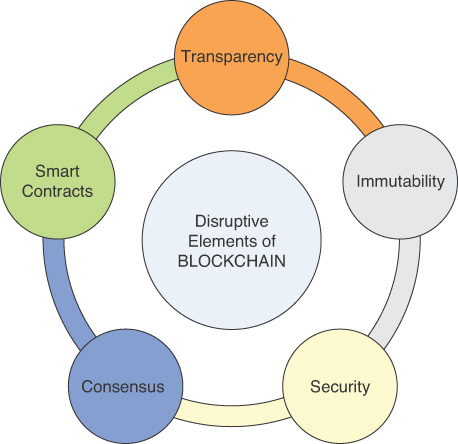

Disruptive Elements

What makes blockchain so disruptive? Blockchain intrinsically bridges the trust gap in our business networks and our societies by co-developing a shared copy of the truth. Five critical elements of the blockchain technology drive this disruption: transparency, immutability, security, consensus, and smart contracts (Figure 2.1). How you see these disruptive elements—that is, your perspective of each of them—suggests ways to transform your business.

Transparency

Blockchain provides end-to-end visibility of your business transactions with a single source of truth that is replicated or shared across the distributed ledger in your business network. Based on the permissions that are given in a private or public blockchain-based business network, you can see the full trail of a transaction. In the past, this transparency has not existed in business networks that involve multiple participants. Thus, the new transparency disrupts many intermediaries or third parties in your business network by enabling direct peer-to-peer connection and exchange.

Imagine a supply chain network with a single source of truth across the value chain.

It is difficult to get real-time visibility of shipments in a logistics and supply-chain business because such a complex network includes multiple participants (users of goods, retailers, distributors, manufacturers, suppliers, and brokers), each of which keeps its own record of a transaction, and whose records are never synchronized. A blockchain-based supply chain network provides greater visibility and transparency that drives efficiency and higher value.

Immutability

After you record a transaction into a blockchain, no one can delete it. If you try to modify the transaction, the blockchain appends another update record to the transaction, which is visible to the participants in the network. Each transaction in a blockchain is encoded into a data block and uniquely signed and timestamped. Each block is connected to the blocks before and after it. These blocks cannot be altered or modified; they are linked together to form a chain that is immutable and irreversible. An immutable history of transactions eliminates the counterfeiting and fraud challenges faced by many businesses.

The blockchain-driven provenance process eradicates counterfeiting by using immutability and transparency.

Counterfeiting is the biggest challenge globally for legal and financial documents and valuable goods, such as drugs, food products, luxury clothes, and jewelry. It costs companies more than 7 percent of their annual expenditures, amounting to almost $4 trillion each year on a global scale.1 The immutable digital record and history of transfer of an asset or good are identifiable and visible to the participants within the blockchain network, so this approach blocks fraud and tampering attempts in a system or process.

Security

Blockchain provides a highly secure transaction system that is almost impossible to hack. Every transaction record on a blockchain is cryptographically secured with digital signatures, along with a trail of the transaction updates. Participants in the network have their own private keys that are assigned to a transaction or any update to an existing transaction. Therefore, security vulnerabilities are easily identified and inherently prevented. Every transaction is replicated or shared across the distributed ledger, which means that hackers must look at every ledger and find the same data or record across all the ledgers, which is difficult.

Security, privacy, and compliance are bolstered by a distributed ledger, transaction integrity, high availability, and auditability.

The security of business-critical data and transactions is a primary concern in any organization and across all industries. Digital transformation of such data and transactions, in turn, is the key driving force of further complexity in today’s business world and brings up new security issues. Global cybersecurity spending was expected to exceed $114 billion in 2018, according to analyst firm Gartner,2 and Statista predicts that it will total more than $234 billion by 2022.3

Most organizations keep their business and customer information in a centralized system. Unfortunately, such centralized systems are vulnerable to attack. Blockchain applies a decentralized approach, in which the transaction data are replicated across the distributed ledger. Thus, even though one of the ledgers is not active, the other ledgers have a copy of the transactions and ensure availability. Each transaction is validated or consented to by network participants before it is posted in the ledger. Although you can identify the members in a blockchain, they can maintain their anonymity and privacy, which is important for organizations to ensure trust. Having an untampered transaction history in blockchain delivers readily available auditability for compliance and regulation purposes.

Consensus

The network participants in blockchain use a consensus mechanism to eliminate the need to rely on central authorities and third parties to validate business transactions. The foundation of cryptocurrency, for example, is a public blockchain that requires miners to validate the currency transactions. This process, which is called proof of work or mining overhead, involves a huge amount of computing power and energy. In contrast, permissioned blockchain includes trusted participants on the network and uses consensus algorithms that validate transactions anonymously without mining overhead, and with a fraction of the computing power and the energy costs that are used in a public blockchain.

Consensus drives fair participation in a business network with democracy.

On a global scale, unfairness is more than 50% in economic structures where benefits and burdens are not fairly distributed across the country government according to a BBC poll. Many businesses spend billions of dollars every year to deal with unfairness issues, while others lose billions of dollars every year without being aware of unfairness. Many intermediaries in the legal, business, and government arenas take advantage of unfairness and deceptive practices for their own economic or financial benefits. Blockchain technology has the potential to replace the unfairness in government and businesses with a truly democratic and transparent approach toward transactions.

Smart Contracts

You can think of smart contracts as self-executing electronic contracts that state the legal and business terms of an agreement between business partners. Smart contracts in blockchain are business logics that are programmed and embedded into a transaction record that enable business process automation. Such contracts allow transactions and agreements to be executed among various business participants without engaging the services of a central authority, legal system, or arbitrator. Business process automation is possible by using smart contracts because the transactions in blockchain are trusted, transparent, and immutable.

Smart contracts fuel business process innovation with automation, speed, and compliance without hefty costs and risks.

Even though automation and agility are increasing in business or legal contracts management, the average cost of processing and reviewing a basic contract has increased by 38 percent in the last six years and now averages $6900, according to the International Association for Contract and Commercial Management (IACCM).4 The global legal services market alone is expected to top $1 trillion by 2021, based on a Statista report.5 Think how much you are spending on your contract management services and how much potential smart contracts have to save money, enable contracts to be processed faster or almost instantaneously electronically, and reduce risks through application of transparency and immutability. Initial estimates suggest that blockchain technology can reduce the execution time of business contracts from days to minutes, from manual to automated, at a fraction of the current cost, essentially without any legal entity becoming involved.

Next, we’ll explore how these disruptive elements from blockchain can uncover new opportunities for your business’s transformation.

Opportunities

Many individuals and organizations (sometimes unintentionally) thwart positive changes in business due to their inability to see how new innovative technologies can revolutionize the future. Emerging technologies bring new opportunities and change our lives by changing the way that we think and operate. Two of the revolutionary technologies that we witnessed in the 20th century were personal computers and the Internet. The next significant transformative technology of the 21st century is blockchain.

Gartner forecasts that the business value that is driven by blockchain will amount to $3.1 trillion by 2030.6 The true business value will be driven by the new opportunities that users envision to transform their businesses in various use cases across a wide range of industries, from cryptocurrency to cross-border payments, food safety to provenance, supply chain to trade finance, clinical trials to healthcare exchanges, digital rights management to royalty settlements, digital identity to land registry, and many more. Blockchain presents endless opportunities.

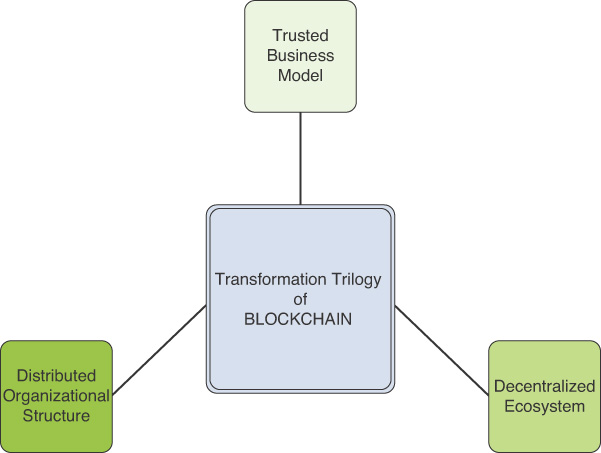

Transformative Power of Blockchain

Blockchain technology drives transformational opportunities in three ways so that enterprises, economies, and ecosystems flourish. This transformation trilogy is composed of new organizational structures, new business models, and new ecosystems (Figure 2.2).

Distributed Organizational Structure

Most modern organizations, whether public or private, are highly centralized, and they typically institute bureaucratic governance that benefits monopolies. Partners in that network are driven to compete adversely. All too frequently, a command-and-control–driven approach intended to gain short-term benefits disables the innovation agenda in these organizations. The centralized structure in such an organization has either limited or no visibility, trust, and transparency across the business. These challenges drive higher costs, reduce agility, add inefficiency in operations, and create an unhealthy and unsustainable culture within the economy.

Now imagine how you might use blockchain to revive a centralized organizational structure that drives freedom of innovation and autonomy in the participating business networks. The distributed nature of blockchain technology, along with the emphasis on consensus and smart contracts, delivers a self-governing business network with a greater autonomy that flattens traditional enterprise structures into a distributed and shared structure. Business transactions are managed in a distributed and shared ledger that offers transparency and visibility across the network without any complex and hierarchical nature. Imagine a new government structure for a country that is free from fraud and bureaucracy and transparent to its citizens.

This new distributed structure enables organizations to be highly cost-effective, efficient, and faster in delivering services and business results.

Trusted Business Model

Business models are primarily a construct indicating how organizations bring a set of capabilities to create and deliver value to their clients and partners by maintaining relationships, ensuring stickiness, and differentiating products and services from those of their competitors. The traditional business models are process-heavy and require the presence of many stakeholders, intermediaries, and third parties due to limited trust and transparency. These characteristics drive inefficiencies, higher costs, and sluggishness in the business. Recently, however, new models have emerged that have disrupted traditional models, such Uber (taxi service), Airbnb (short-term housing rental), and Netflix (movie rental).

Blockchain presents many opportunities beyond cryptocurrency for organizations to disrupt traditional business models by using peer-to-peer exchange with trust, digital and automated execution of business contracts, and agreements with smart contracts. The intermediation between third parties is handled by distributed ledger and transparency, and transaction integrity is ensured with security and cryptography.

Blockchain injects trust into business transactions. It fundamentally changes the state of trust in business models by making it dynamic, so that business models can be defined as either trusted, semi-trusted, or untrusted. A public, private, permissioned, or consortia blockchain establishes trust with the correct governance structure and policy.

Organizations’ brand and reputation systems that are built on blockchain can provide assurance of truth and transparency through their business records, which can visibly demonstrate trustworthiness to their potential clients and partners.

Examples of such business model transformations include the following:

A music distribution model in which music files are exchanged directly from creator to the listeners and monetized without any distributors

A remittance model in which money is transferred from a sender to a receiver without a financial institution acting as an intermediary

An open market model that connects buyers and sellers directly without an exchange intermediary

Decentralized Ecosystem

An open approach toward business transactions’ trust and transparency in a network that is driven by blockchain promotes a transformational journey for the network’s participants. In this approach, organizations and systems cooperate, and value is co-created and contained in the network.

As blockchain delivers distributed organizational structures and trusted business models, it fosters new emerging trusted marketplaces and economy-to-exchange value. Peer-to-peer models are driving the new ecosystem of players and eliminated the roles for intermediaries. This systematic change fosters the creation of new consumers, competitors, microeconomies, profit pools, and a distributed ecosystem. Decentralized, ecosystem-driven markets are impossible to compete with.

The following examples illustrate new ecosystems that can emerge as part of distributed environments:

Start-up funding is reinvented by using initial coin offerings (ICO) and tokens.

A “know your customers” (KYC) service is created and used within a business network and eliminates the traditional KYC that was redundant for each organization.

Assets and land registration in developing nations can leapfrog traditional rural and urban development and real estate governance ecosystems in developed nations.

A trading and investment model runs without a clearinghouse.

Achieving these kinds of advances is not a matter of mastering the blockchain technology; instead, it requires rethinking your current market role, value streams, and existing business ecosystems, and finding opportunities to transform your business. This is a new radical shift in businesses in which many elements must be redesigned, such as organizational structure, business model, and ecosystem.

Transformative Opportunities

This section examines some of the industry-specific transformational opportunities that may be driven by blockchain, beyond Bitcoin or cryptocurrency.

Banking and Financial Markets

Blockchain capabilities deliver banking innovations to revamp the experience for customers by reducing transaction times from hours to seconds, eliminating manual processes, and eradicating unnecessary intermediaries in trade finance, digital identities, and cross-border payments. With blockchain, you can conduct business rapidly and securely, moving from paper-based to blockchain-stored transaction records, which can enable easier expansion to underserved markets, such as small and medium enterprises.

Trade Finance

Banks continue to struggle with manual processes and stringent requirements for managing, tracking, and securing domestic and cross-border trade transactions. For example, processes for corporate trade financing letters of credit are typically paper based and fragmented, which can make financing more challenging for the 50 percent of smaller enterprises that might not have credit sources.

Blockchain-based smart contracts can automatically store, secure, and exchange contract details and financial terms; coordinate trade logistics and payments via an integrated real-time network; and streamline digital trade processes. With blockchain, ledger transactions can flow from one small enterprise to another one through a trusted bank. Larger firms can also benefit by better tracking of trade finance transactions.

For example, IBM and eight European banks have created We.Trade, which is a multiple-bank collaboration that is building trusted digital trade chain connections with smaller enterprises.

Digital Identity Verification

Requiring clients to repeatedly provide identifying information can erode customer satisfaction and cause transaction delays. Onboarding clients for checking accounts or mortgages or migrating them from one bank to another requires strict compliance with KYC standards.

On IBM Blockchain, identification documentation can be consolidated with managed access and permissions without storing the actual identifying information. This supports KYC due diligence, helps secure personal information, and enhances client satisfaction.

For example, IBM and SecureKey Technologies are building an identity-sharing ecosystem with Canadian banks that will enable clients to instantly verify identities when opening new accounts. Other uses include driver’s license applications and requests for utility services.

Insurance

Blockchain can simplify and secure multiparty operations at the heart of the insurance industry. Whether interacting with customers or dealing with other parties, blockchain can reduce the challenges that are presented by multiple parties that keep their own records.

As transactions occur, insurers can rely on blockchain’s distributed ledger technology to update and validate information against other records in the network; reduce management costs for policies, claims, and relationships; streamline operations; and enhance customer satisfaction. Companies can also capture opportunities and revenue through new business models or new insurance products.

Complex Risk Coverage

Employees, policy holders, adjusters, and agents who cannot view insurance policy information usually need human help, which increases the chance of errors, delays claims resolution, and increases costs. The challenge escalates with complex insurance programs or managing policies in multiple countries, which can involve strict legal and regulatory adherence. Blockchain can resolve many of these obstacles to smooth operations.

For example, using IBM Blockchain, AIG and Standard Chartered converted multiple policies into “smart contracts” that provided a single, consolidated view of policy data and documentation in real time. The solution enables visibility into coverage and premium payments, delivering automated notifications to network participants after payment events occur.

Group Benefits

Organizations offering group benefits often rely on a complex network of administrators, providers, employees, and others to manage those benefits. Different versions of the same data require consolidation to ensure eligibility and access to benefits.

For example, IBM Blockchain can be the vital link across a vast ecosystem of third-party administrators and service provider networks. Its shared ledger transparency can help employers reduce errors, which results in improved claims processing, better provider management, and lower operational expenses.

Healthcare

Blockchain can transform healthcare enterprises and increase the quality of care by enabling new ecosystems and new business models to evolve. Healthcare information that is stored on a blockchain can change the way that providers store clinical information and how they share information within their own organization as well as with other healthcare partners, payers, and patients.

Blockchain decentralizes healthcare information, increasing data availability, efficiency, transparency, and trust. However, it requires careful planning to make the most of the advantages it brings. The blockchain infrastructure that IBM is helping to build provides enterprises with a solid platform for both immediate and long-term business solutions.

Patient Consent and Health Data Exchange

Disparate record-keeping systems can result in patient consent forms and medical histories that are incomplete, conflicting, or ambiguous. By comparison, blockchain-stored records can be used to provide complete, longitudinal health records for individuals, giving all patients more control over their own information through verifiable consent. With blockchain, every patient record reflects the best-known medical facts, from genomics data to diagnostic medical imaging, and data can be reliably transferred when needed, with no need for a central gatekeeper.

Clinical Trials Management

Clinical trials of healthcare interventions generate mountains of data, which requires healthcare administrators to keep reliable and consistent records for peer review and to meet regulatory requirements. Blockchain tools, in concert with electronic data capture (EDC), allows clinical data to be automatically aggregated, replicated, and distributed among researchers and practitioners with greater auditability, provenance tracking, and control compared to complicated conventional systems.

Retail and Consumer Goods

Blockchain is removing obstacles and increasing visibility for consumer products and retail business transactions. Greater transparency through a shared and immutable ledger enables businesses to establish a climate of trust across areas such as invoicing and payments, the consumer supply chain, and global shipping. Through the use of a distributed and trusted database, a blockchain solution reduces barriers that might otherwise impede business, such as siloed management and regulatory systems, time-consuming settlement processes, and uncertainty between entities conducting transactions.

Blockchain speeds transactions, builds trust between participating members, and opens the door to cross-industry and global business opportunities.

Commerce

All too often, lengthy invoicing and payment processes across diverse systems lead to delays in verification and payments, triggering disputes and driving up the cost of doing business in today’s global markets. Blockchain helps remove friction from such commerce by providing a common chain of information visibility that is shared across vendors and purchasers.

For example, a major consumer goods company used IBM Blockchain to reduce the complexity and ambiguity it encountered in invoice processing. The solution cut processing times from five days to one and trimmed processing costs by 50 percent. The company plans to expand its new model to numerous other supplier relationships.

Supply Chain Management

Disparate systems that are used by multiple entities across a supply chain can block visibility across the ecosystem, creating an atmosphere of distrust and leaving all parties at risk. For example, trust in the food supply has suffered due to a lack of industry transparency between suppliers, processors, distributors, retailers, logistics providers, and consumers.

A blockchain-based food supply chain provenance like IBM Food Trust is a collaborative solution that unites growers, distributors, processors, retailers, and other food industry stakeholders to efficiently and securely trace food through every step of the supply chain. The IBM Blockchain–powered solution helps ensure food safety from farm to store through rapid end-to-end traceability of data and access to compliance certification.

For example, Walmart and IBM have partnered to help improve food safety by using IBM Food Trust. The first blockchain food safety solution to run production data for products across the food system, it allows early adopters to confidently and securely share data with their food supply chain partners.

In another supply-chain application, IBM and Maersk have announced a joint effort to streamline shipping through creation of an efficient and secure global trade digitization platform based on IBM Blockchain. The proposed venture will address needs for transparency, simplicity, and open standards as goods move across borders and trading zones.

Government

From issuing identification and registering property to administering elections and enforcing laws, government must ensure stringent data stewardship to protect citizen information, maintain trust, and ensure the accuracy of public records. Governments face challenges unlike those encountered in any other domain: Data architects, administrators, and privacy officers must protect citizens’ personal information, yet keep vital information accessible when needed. Scaling complicates life for government administrators, too: The vast scope of mandated services and the large workforces that are needed to provide them can lead to fraud, waste, and abuse, allowing significant errors to slip into vital public records.

Asset Registration

We rely on government to accurately record and track our homes, businesses, cars, and more, so as to verify ownership and ensure smooth financial transactions. Accurate and accessible registries are crucial to engender trust and transparency in government. Despite this need, today’s registries suffer from slow, duplicative processes and an overreliance on error-prone, incomplete, and manual data entry. Blockchain enables government agencies to increase the accuracy and efficiency of publicly held records by linking ownership of an asset to a single and shared ledger without disrupting the existing registry data.

Fraud Prevention and Compliance

All too often, fraud, information privacy abuse, and accidental data exposure plague government data transactions. Moreover, siloed legacy systems and processes within government frequently result in multiple versions of multiuser data sets. In the absence of a single version of the truth, the risk of fraud and the difficulty of ensuring compliance increases each time a data set is accessed, because there is no way to distinguish between correct and incorrect entries.

Blockchain creates a shared and trusted ledger that sequentially appends cryptographically secure data. This ledger is accessible only to trusted parties, giving government administrators the assurance that they are working with data that are up-to-date, accurate, and nearly impossible to manipulate.

Media and Entertainment

Blockchain is increasing transparency in digital transactions and removing complexity from the media and entertainment ecosystem by reducing the need for multiple stakeholders in advertising purchases and digital content management. With an immutable and shared ledger that records transactions as they occur, companies in media, advertising, entertainment, and others have complete visibility as content or data are purchased and used.

Blockchain is designed to accelerate the creation of “built for business” global blockchain networks across industries and use cases. The implications for media and entertainment can be profound, such as in digital rights management—trusted and transparent content distribution in a digital ecosystem.

Advertisement Settlement

Nearly 50 percent of ads fail to reach their intended audience.7 Moreover, antiquated rating and measurement systems can make it impossible to know the precise number of audience impressions achieved with a specific ad. Digital advertising fraud costs at least $7 billion annually,8 while intermediaries profit from 60 percent of ad spending. Discrepancies in systems of record typically lead to disputes, labor costs, leakage, and poor cash flow.

Using an immutable blockchain ledger can remove the need for intermediaries, thereby reducing advertising costs. By digitally recording transactions across the advertising ecosystem, advertisers, intermediaries, and advertising sellers have a shared knowledge of impressions and can use smart contracts to create a transparent system that proves spending is based on actual impressions. Inventory management can be streamlined, and billing and invoicing can become more efficient for agencies creating ads.

For example, Unilever, one of the world’s largest advertisers, partnered with IBM to build a blockchain solution to manage its advertising supply chain and create a trust-based and transparent solution that enables buyer verification, offering a way for all parties to visualize every part of the advertising process. The new transparency will make it easier for advertisers and advertising platforms to know how efficient campaigns are, justifying (or not) advertising expenses.

Loyalty Programs

Loyalty programs have been implemented in a variety of forums, spanning the hospitality, finance, entertainment, airline, and retail industries, among others. However, segmented systems can make it impossible for consumers to exchange their loyalty points across entities, including ones in the same industry, such as banks. This situation limits cross-marketing and revenue growth opportunities.

Blockchain solutions make it possible to provide complete visibility into a loyalty inventory to establish trust across the loyalty ecosystem, enabling, for example, a consumer to book a hotel, purchase a theme park ticket, or buy a cup of coffee by using frequent-flyer points. Conversely, the consumer can gain credit through loyalty points that are earned with other entities and use them with the airline.

For example, China UnionPay, which guarantees credit card usage across Chinese banks in more than 150 countries, uses IBM Blockchain to help bank customers exchange bonus points that are earned through purchases among disparate banks. The new peer-to-peer bank reward point trading system will allow points exchange between banks, credit card users, and gift shops.

Automotive

Every part of the complex automotive business ecosystem—from parts suppliers and manufacturers to customers and safety regulators—relies on a network of transactions and knowledge that starts long before a vehicle is manufactured and extends far beyond its purchase. That network is growing. From support for evolving hardware and services to understanding the provenance and location of defective or counterfeit parts, the amount of data that the automotive industry must track is exploding.

Blockchain can help build efficiency, transparency, and trust by using a shared and permissioned record of ownership, location, and movement of parts and goods. The versatility of blockchain records makes them perfect for keeping up with innovative new business models.

Mobility Service

Modern cars are more than transportation devices; they are complex and networked software platforms on wheels. Vehicles increasingly need to incorporate secure and seamless mobility services, including micropayments and other interactions with ride-sharing services, smart transportation infrastructure, and electric vehicle charging.

IBM has announced a partnership with ZF and UBS Bank to implement a blockchain-backed car eWallet service that is delivered through IBM Cloud, enabling cashless micropayments for tolls, congestion fees, electric charging fees, parking fees, and making payments between vehicles. The system also allows a vehicle to be used as a secure drop point for packages, when the vehicle owner gives the package delivery service permission to access its trunk.

Provenance Tracking

Auto manufacturing is truly global. Parts are sourced worldwide, and completed vehicles might be driven anywhere on earth. To contend with counterfeit parts and defect-driven product recalls, traceability is crucial in understanding a vehicle’s post-sale movements. To maintain safety and reliability, makers must track vehicle movements for both regulators and purchasers. If a component safety issue arises, blockchain technology can help both automobile makers and parts suppliers quickly discover where the parts are.

Analogous to the developments occurring in the auto industry, Boeing is implementing an IBM Blockchain–based solution that will make information from across the aircraft supply chain accessible to component vendors, aircraft owners and maintainers, and regulators.

Travel and Transportation

The travel and transportation environments have millions of moving parts. Blockchain technologies can help each part move in the safe, secure, efficient, and frictionless ways that are necessary for business success and customer satisfaction.

Consider the airline industry’s practice of interlining, also known as interline ticketing and interline booking, is a voluntary commercial agreement between individual airlines to handle passengers traveling on itineraries that require multiple flights on multiple airlines. As part of this practice, multiple business-to-business transactions occur between booking agents, air carriers, credit card companies, and airports. The results often lead to complexity, errors, or transaction disputes. In contrast, when all parties use the same data in a blockchain environment, common information visibility and sharing can eliminate inconsistencies. Whether used on land, at sea, or in the air, blockchain technology speeds transactions, eliminates fraud, and helps streamline transportation operations with an immutable, trustworthy, and secure system that builds trust among parties.

Personnel Coordination

Passenger and cargo safety are paramount in every form of transportation, but crew training and certification can involve multiple agencies over long periods. Every transport terminal is a hive of activity, with personnel who are employed by a wide range of companies with duties as diverse as fuel delivery, ticket taking, catering, shuttle-cart driving, cleaning, and more. Each employee requires vetting for security, and all of their activities must be coordinated.

With its shared and immutable ledger that prevents entries from being changed or falsified, blockchain can provide the verification and insight that transportation companies need. Certificates and licenses can be stored for each crew member and verified and updated as more training occurs. Blockchain provides a central management mechanism, with visibility into the common information that is necessary for settling disputes over pay, work status, or other issues that might arise.

Cargo Handling

Shipping goods involves multiple parties, including senders, receivers, carriers, and regulators. Given the involvement of so many entities, each with a different records system, blockchain can help track the location and condition of cargo. Using shared records of ownership, location, and movement, carriers can improve their load utilization, and senders and receivers can speed delivery by clearing customs in transit instead of waiting at the terminal.

For example, dnata (Dubai National Air Transport Association), a global provider of ground handling, cargo, travel, and flight catering services for more than 400 airlines, teamed with IBM to eliminate redundant data and improve visibility and transparency for cargo services by using blockchain. The results streamlined and simplified the processes from the point of origin to the final destination. The blockchain solution achieves this task by digitizing the supply chain and by using a peer-to-peer network to manage and track each cargo container’s path.

Challenges

The primary challenges with the application of blockchain are not about having a perfect and matured technology: The evolution of blockchain technology will undoubtedly continue, much as Internet technology continues to advance nearly four decades after its first introduction. Blockchain technology has been used for several years as an underlying foundation for cryptocurrency application, and lately many organizations have advanced it to ensure its enterprise readiness for other industries. The key challenges are choosing the right scope, having the right motivation for a business and its participants, ensuring the right governance structure, and having the correct team and technology in place. These challenges can be conquered if you make deliberate and diligent efforts to manage the blockchain network effectively and focus on driving the ultimate transformation that you envisioned.

As shown in Figure 2.3, addressing the challenges involves three aspects: The scope helps you determine what plan you should make for a blockchain network, governance defines how you should operate it, and motivation drives why you should build or participate in it.

Scope

Although blockchain has the potential to disrupt many businesses, current business policies and requirements might not immediately support the transformation. Also, blockchain might not be feasible for multiple reasons, such as existing government, business, and legal agreements and laws, exposure, global reputation, bureaucracy, and partnerships. Therefore, it is important to select the right scope so that you can deliver success incrementally, albeit with a big dream in mind for transformation.

The scope selection exercise reflects your vision and business outcome expectations. However, given that blockchain touches critical elements of an organization’s structure, business model, and ecosystem, it is important to consider the scope of each of these items in the context of your desired short-term and long-term business outcomes.

The success of a blockchain project is determined by the correct selection of scope, so define your minimal viable product (MVP) and minimal viable ecosystem (MVE) with a clear start state of your blockchain project; determine your Specific, Measurable, Achievable, Results-focused, and Time-bound (SMART) end goal; and identify key activities that must be performed to pinpoint the following items:

Vulnerabilities and inefficiencies to identify disruptive business use cases

Business network participants and ecosystem readiness

Business model and differentiation needed to compete

Governance plan and policy for cooperation and trust

Operational plan, including costs and responsibilities

Technology and vendor selection

Motivation

The right incentive plan drives motivation to establish the correct behavior, trust, and cooperation in any business network involving consumers and partners. A blockchain network includes both founders of the network and participants. However, because of the nature of the distributed organizations and the decentralized ecosystem that is ready for shared gain and shared pain, it is important to develop an appropriate incentive structure so that everyone is motivated and acts as a trusted partner in the network. Bad actors in a network can jeopardize your ability to achieve your goals within the planned time, costs, and resources conditions.

Incentives in blockchain business networks are not monetary, but might be instead visibility, access, share, and exchange rights. For example, a regulator might want access to and visibility of transactions for compliance purpose, a nonfounding member might want to participate and share its assets for exchange or return value in a network, and a founding member such as a government agency might want specific rights for a business policy or transaction while maintaining trust and transparency.

A token can be issued as an incentive to grow transactions, assets exchange, or the value of transactions in a network. Tokens represent equity or rewards in the systems, and the value of those rewards grow if everyone is performing at an expected or higher level. These tokens are used in managing the loyalty points in retail or consumer businesses, carbon credits in energy trading, credit scores in a financial system, course or merit certification in an educational system, or even a brand or a social image in a reputation system.

To drive sustained motivation in a blockchain network, you must evaluate the following aspects:

Who brings which data, knowledge, or assets to the network?

What is the value of their contributions to the network?

What do they expect in return?

What will keep them motivated to be trusted participants?

What incentives you can offer for short-term versus long-term engagement?

What policies can enable automated incentive allocation?

Governance

A good business depends on having a good governance structure and a team of trusted partners. The success and failure of a business entirely depends on its ability to develop an ecosystem that is properly governed and incentivized.

Governance is the most critical and compulsory requirement for a blockchain project’s success because it maintains a decentralized property with self-executable business and legal contracts that are embodied in the transactions as smart contracts. Although this approach drives automation, speed, and efficiency in a business network, it is critical to understand how the smart contracts are developed and managed as part of the governance structure. In unforeseeable situations, when you have trusted and motivated partners in a network, consensus building becomes much easier and occurs much faster.

The risk in a blockchain project is directly proportional to the governance complexity that drives increased uncertainty, delays, and costs. The public blockchain networks have higher risks than their private, permissioned, or hybrid counterparts due to the difficulty in governance efficacy. Although some use cases are perfect for public blockchain, others are not. Unless you plan carefully, having an open, public, and decentralized governance structure might not be feasible for many of your enterprise use cases because of privacy, compliance, and regulatory requirements. Because many industries’ regulators are investigating blockchain technology implications for their compliance requirements and addressing them, your network must adhere to the existing compliance policies.

A governance structure in a blockchain network can include multiple levels of workgroups that should have a dedicated focus to address the following specific concerns:

The disruptive nature of the envisioned business model and its impact on participants

The roles and accountability of participants

Decision rights

Shared incentives and disincentives

Intellectual property rights and liabilities

Existing regulatory and compliance policies and awareness of future changes

Technical design and architecture

Technology

Technology concerns are not the primary inhibitors of the adoption of blockchain. Indeed, many organizations, including IBM, have made deliberate efforts to make blockchain ready for enterprise usage by effectively addressing (or being in the process of addressing) implementation, deployment, integration, and operation concerns.

Many businesses might be overwhelmed by the technical challenges regarding privacy, scale, or throughput, such as the number of transactions, interoperability, consensus, contract verification, tools, support, and quantum computing threats. However, many of these concerns have already been addressed by many vendors in various implementations of blockchain technologies.

Permissioned and private blockchains can address the privacy concerns by maintaining the anonymity of a participant while ensuring the validation of a transaction from an authorized participant or by using obfuscation technology to restrict the exposure of private information. In public blockchain implementation, businesses can choose to implement off-chain execution—a practice in which they keep only transactional information recorded on the public ledger, while simultaneously maintaining a shadow ledger to keep identity information private.

The scalability or throughput of the blockchain network primarily depends on the levels of security and cryptography that are applied, as well as the efficiency of the consensus algorithm. If you loosen the security strength, the throughput increases. The proof-of-work module is the primary compute- and time-intensive task that drives the throughput, and many public blockchain implementations for cryptocurrency have single-digit transactions that are validated and recorded per second. By comparison, a robust, enterprise-ready, and permissioned blockchain like Hyperledger is ready to serve more than a thousand transactions per second without compromising any security.

Also, you can run multiple channels in a parallel peer-to-peer scheme. This model addresses throughput concerns and enables blockchain readiness for many enterprise use cases.

Interoperability is another concern, given the existence of different implementations of blockchain technologies, such as Ethereum, Hyperledger, R3’s Corda, and Ripple. Although business applications and networks are built on different blockchain bases, eventually they must interoperate in the broader economy. As an analogy, think about how we started with private and closed intranets, which were then called upon to interoperate on the Internet. In the blockchain world, standards and technology groups are already working to address these types of concerns.

Consensus mechanisms and corresponding algorithms are quite advanced in the current technology implementations. For example, Hyperledger addresses fault tolerance and resilience concerns by providing a modular foundation where peers are divided into separate groups that are based on their roles and smart contracts are tailored and run. Contract verifications are fairly managed by emerging smart contract programming languages. Tools, deployment, and operations support is provided by many vendors and open source communities.

To some extent, quantum computing poses a threat to blockchain security because quantum computers can hack any traditional system’s cryptography. Nevertheless, post-quantum cryptography, such as lattice cryptography techniques, is available to address quantum computing threats.

Although many technical challenges can be addressed with public, private, permissioned, or hybrid blockchain models, you should be able to clearly identify the following items in your environment:

The architectural needs of your business use case—that is, whether you use a public, private, permissioned, or hybrid blockchain network

Open and standard technologies requirements

Privacy requirements

Scalability and throughput needs

Integration capability with existing systems and applications

End-to-end support for implementation, deployment, and operations

Interoperability needs

Chapter Summary

This chapter covered blockchain technology’s disruptive elements that drive transformation across traditional organizational structures, business models, and ecosystems. These characteristics fundamentally open endless opportunities in many industries to innovate and challenge the status quo. The primary challenges for a blockchain project’s success are specific to the scope, motivation, and governance rather than to the technology.

References

1. Crowe’s Financial Cost of Fraud 2018 Report. www.crowe.com/uk/croweuk/insights/financial-cost-of-fraud-2018

2. Gartner, 2018 Worldwide Cybersecurity Forecast Report. www.gartner.com/en/newsroom/press-releases/2018-08-15-gartner-forecasts-worldwide-information-security-spending-to-exceed-124-billion-in-2019

3. Statista, Report: Size of the Cyber Security Market Worldwide, from 2017 to 2022. www.statista.com/statistics/595182/worldwide-security-as-a-service-market-size/

4. International Association for Contract and Commercial Management Report. blog.iaccm.com/commitment-matters-tim-cummins-blog/the-cost-of-a-contract

5. Statista, Report: Size of the Legal Services Market Worldwide from 2013 to 2021. www.statista.com/statistics/605125/size-of-the-global-legal-services-market/

6. Gartner, Forecast: Blockchain Business Value, Worldwide, 2017–2030. www.gartner.com/doc/3627117/forecast-blockchain-business-value-worldwide

7. Michael Burgi, “What’s Being Done to Rein in $7 Billion in Ad Fraud,” Adweek, February 21, 2016.

8. Lucy Handley, “Billions of Digital Marketing Dollars Are Being Wasted as Online Adverts Miss Their Intended Targets: Research,” CNBC, December 20, 2016.