Epilogue

Twelve Pillars of Wisdom

Wisdom excelleth folly

“Wisdom excelleth folly as far as light excelleth darkness.” My epilogue begins with this apt quotation from Ecclesiastes, and I must warn you that I shall end it with what I think is an equally apt quotation. Throughout this book I have tried to impart some wisdom to the intelligent investor in mutual funds and delineate some folly that should be avoided. And I hope that I have succeeded in shedding light on mutual fund issues previously shrouded in darkness. By way of summary, I close with the following “twelve pillars of wisdom” as lamps to guide you in your search for a sensible, productive investment program.

- Investing is not nearly as difficult as it looks. The intelligent investor in mutual funds, using common sense and without extraordinary financial acumen, can perform with the pros. In a world where financial markets are highly efficient, there is absolutely no reason that careful and disciplined novices—those who know the rudiments but lack the experience—cannot hold their own or even surpass the long-term returns earned by professional investors as a group. Successful investing involves doing just a few things right and avoiding serious mistakes.

- When all else fails, fall back on simplicity. If you have a major investment decision to make, there are an infinite number of solutions that would be worse than this one: commit, over a period of a few years, half of your assets to a stock index fund and half to a bond index fund. Ignore interim fluctuations in their net asset values. Hold your positions for as long as you live, subject only to infrequent and marginal adjustments as your circumstances change. Occam's razor—a thesis set forth 600 years ago and often affirmed by experience since then— should encourage you: when there are multiple solutions to a problem, choose the simplest one.

- Time marches on. Time dramatically enhances capital accumulation as the magic of compounding accelerates. At an annual return of +10%, the additional capital accumulation on a $10,000 investment is $1,000 in the first year, $2,400 by the tenth year, and $10,000 by the twenty-fifth year. At the end of 25 years, the total value of the initial $10,000 investment is $108,000, nearly a tenfold increase in value. Give yourself the benefit of all the time you can possibly afford.

- Nothing ventured, nothing gained. It pays to take reasonable interim risks in the search for higher long-term rates of return. The magic of compounding accelerates sharply with even modest increases in annual rate of return. While an investment of $10,000 earning an annual return of +10% grows to a value of $108,000 over 25 years, at +12% the final value is $170,000. The difference of $62,000 is more than six times the initial investment itself.

- Diversify, diversify, diversify. It is hard to imagine that a principle as basic as investment diversification can be so valuable. By investing in mutual funds you can eliminate the risk of owning the stock or bond of a single enterprise that may deteriorate and never fully recover, or even fail altogether. The passage of time has no impact on this specific security risk. By owning a broadly diversified portfolio of stocks and bonds, only market risk remains. This risk is reflected in the volatility of the total value of your portfolio and should take care of itself over time as reinvested dividends and interest are compounded.

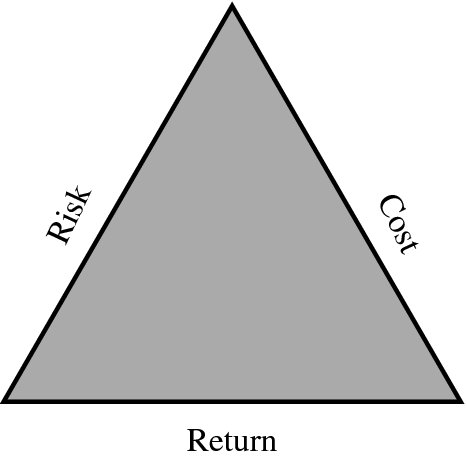

- The eternal triangle. Never forget that risk, return, and cost are the three sides of the eternal triangle of investing. Remember also that the cost penalty may sharply erode the risk premium to which an investor is entitled. This is not to say that you should necessarily seek out the lowest-cost mutual fund option. Rather, you should understand unequivocally that investing in a fund with a relatively high expense ratio—more than 0.50% per year for a money market fund, 0.75% for a bond fund, 1.00% for a regular equity fund, or 0.30% for an index fund—bears careful examination. Unless you are confident that the higher costs you incur are justified by higher expected returns or enhanced value of service, select your investments from among the lower-cost no-load funds.

- The powerful magnetism of the mean. In the world of investing, the mean is a powerful magnet that pulls financial market returns toward it, causing returns to deteriorate after they exceed historical norms by substantial margins and to improve after they fall short. The mean is also the powerful magnet that pulls the returns achieved by portfolio managers toward it, causing a fund's return to move, over time, ever closer to the average returns achieved by other funds. Regression to the mean is a manifestation of the immutable law of averages that prevails, sooner or later, in the financial jungle.

- Do not overestimate your ability to pick superior equity mutual funds, nor underestimate your ability to pick superior bond and money market funds. In selecting equity funds, no analysis of the past, no matter how painstaking, assures future superiority. In general, you should settle for a solid mainstream equity fund in which the action of the stock market itself explains about 85% or more of the fund's return. Combining several low-cost equity funds to achieve this diversification is equally sensible; so is the holding of a single low-cost index fund. But do not approach the selection of bond and money market funds with the same skepticism. Selecting the better funds in these categories on the basis of their comparative costs holds remarkably favorable prospects for success.

- You may have a stable principal value or a stable income stream, but you may not have both. Nothing could make this proposition more obvious than the contrast between a 90-day U.S. Treasury bill—with its volatile income stream and fixed value—and a 30-year U.S. Treasury bond—with its fixed income stream and extraordinarily volatile market value. Intelligent investing involves choices, compromises, and trade-offs, and your own financial position should determine which type of stability—or, more likely, which combination of the two—is most suitable for your portfolio.

- Beware of “fighting the last war.” Too many investors—individuals and institutions alike—are constantly making investment decisions based on the lessons of the recent, or even the extended, past. They seek stocks after stocks have emerged victorious from the last war, bonds after bonds have won, Treasury bills after bills have won. And they worry about the impact of inflation after inflation, having turned high real returns into so-so nominal returns, has become the accepted bogeyman. You should not ignore the past, but neither should you assume that a particular cyclical trend will last forever. None does.

- You rarely, if ever, know something the market does not. It is really not possible to do so. If you are worried about the coming bear market, excited about the coming bull market, fearful about the prospect of war, or concerned about the economy, the election, or indeed the state of mankind, in all probability your opinions are already reflected in the market. The financial markets reflect the knowledge, the hopes, the fears, even the greed, of all investors everywhere. It is nearly always unwise to act on insights that you think are your own but are in fact shared by millions of others.

- Think long term. Do not let transitory changes in stock prices alter your investment program. There is a lot of noise in the daily volatility of the stock market, which too often is “a tale told by an idiot, full of sound and fury, signifying nothing.” (Macbeth would doubtless agree.) Stocks may remain overvalued, or undervalued, for years. Patience and consistency are valuable assets for the intelligent investor. The best rule is: stay the course.

As you go about investing for the future—a future surely filled with a full measure of reward and peril, optimism and pessimism, hope and fear—a final touch of philosophy may help you and other intelligent investors through the rough patches that inevitably lie ahead. As Ecclesiastes tells us:

I returned, and saw under the sun, that the race is not to the swift, nor the battle to the strong, neither yet bread to the wise, nor yet riches to men of understanding, nor yet favor to men of skill; but time and chance happeneth to them all.