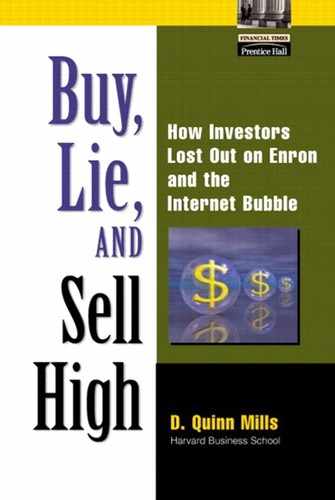

Diagramming the Financial Value Chain

Figure 4-1 is of the Financial Value Chain—the group of specialized companies that together cause the capital market to function and which translate the economic value of a firm into financial value.

Figure 4-1. The Financial Value Chain.

The chain begins with start-up firms and the entrepreneurs who run them. Next are the venture firms and/or angels who finance early-stage firms in return for an ownership stake (usually in the form of preferred stock) and who also have contacts to the investment banks. Accountants play a crucial role because they verify the honesty of the information upon which transactions are based. Without confidence that the representations of a seller about the financial condition of a company are correct, buyers would hesitate to buy, and a market would be difficult to create. But accountants have a divided, even ambiguous responsibility—partly to the company that pays their fees, and partly to the investors who depend on the veracity of their reports.

Entrepreneurs rely on investment banks (such as Goldman Sachs, Morgan Stanley Dean Witter, and Credit Suisse First Boston) to raise money through an initial public offering, or “going public.” Investment banks provide advisory financial services, and help a company sell itself to investors, often in the form of a road show. For these services, investment banks are paid a commission based on the amount of money that the company manages to raise in its offering, typically on the order of seven percent,[15] a very high-margin source of business for the investment banks.

During the IPO process, banks undertake a publicity campaign to potential investors and then sell the shares, at least for a fully marketed offering. (Other offerings might be made to only a small set of investors, and so not fully marketed.) During the dot-com bubble, Goldman Sachs and Morgan Stanley together did about 70 percent of all good (or so it seemed at the time) quality IPOs. It appears that entrepreneurs and venture firms gave great importance to the stronger brand names among the investment banks.

The banks, though they represent client firms, and are paid by them, also have some responsibility to investors to be sure that shares sold to investors do not immediately become worthless. So banks traditionally exercise a gatekeeping function controlling which companies get taken to the public market. It may be hard to believe that the banks actually turned anything down during the dot-com bubble—but not every company that applied to the banks was taken public, and there was tremendous competition among the banks to get the best of the bunch to take to IPOs.

At the end of the Financial Value Chain are the investors, both institutional (such as corporate or public employee pension funds, and mutual funds) and retail (individual investors via their savings or self-managed pension funds). Retail investors may buy shares in a new company directly from the banks via IPOs, or indirectly through buying shares in mutual funds that have bought IPO shares. Small investors may end up holding IPO shares via corporate pension funds by which they are covered, or via shares in their own companies if they work for firms which have IPOs.

The Financial Value Chain is complex, involving many participants with different functions, interests, and incentives, and with different relationships among one another. This book is not the place to discuss or describe it in great detail. Appendix B at the back of this book gives a tabular summary of the chain that is more detailed than our discussion here. The appendix gives a snapshot of the entire chain and of the influences exerted on and by each of the participants.

Figure 4-2 (The Ordinary Relationship of Economic and Financial Value) shows what should be the relationship between the growth of economic value in a start-up and the growth of the financial value of the firm. The start-up begins slowly and over years builds products, services, and customers, begins to generate revenues, and ultimately becomes profitable. This is a tale of success. Many start-ups, of course, fail along the way.

Figure 4-2. The ordinary relationship of economic and financial value.

While the start-up is building economic value, financial value is increasing also, and at roughly the same rate. In the ordinary course of events, a start-up gets successive infusions of capital from investors at points in its development which are milestones. At each of these times, the valuation of the company is typically increased. This is valuation via a step-function. When the company has an IPO, a valuation is placed on the company that is the last step of the step-function. After the IPO, the capital market values the company anew again each day. Again, if markets are reasonably efficient, financial value should be increasing at roughly the same rate as the company is building economic value via increased sales and profits.

The formal functioning of the Financial Value Chain during the Internet bubble was not unusual. The Financial Value Chain connected start-up companies to retail investors via investment banks and mutual funds, with the deep involvement of venture funds, financial angels, accountants, the financial press, and pension funds, and always—after the venture and angel investment stage—under the supposedly watchful eyes of government regulators. By virtue of the Financial Value Chain, the economic value being built by start-ups was converted into financial value for investors. The Financial Value Chain is intended to provide information to buyers for the purpose of facilitating investment, but during the bubble the system appears to have given out information that proved wrong about the financial situation and viability of dot-com and telecom businesses, and the consequences hurt both entrepreneurs and investors. How did the system generate results so out of whack?