Chapter 11: Credit Management

Long-outstanding, uncollectable receivables are never good for the financial health of an organization. If a customer defaults on paying outstanding amounts by the end of the allowed payment term, the company needs to monitor that customer’s allowed credit more closely in future transactions. The credit and risk management function in an organization is therefore responsible for creating policies and exercising continuous control in order to minimize credit risks. The Credit Management application in SAP allows you to map your organization’s credit policies at various stages of the order to the cash cycle such that the policies act as the determining rules and help in controlling the credit decision-making process.

In this chapter, we will cover how the credit management functionality available in the SAP SD application supports the credit management function in an organization. We will discuss the concepts of credit management, look closely at customization, and show you the process/setup with the help of the settings we have created for our imaginary company, Galaxy Musical Instruments.

Introducing Credit Management in SAP

SAP Credit Management is an application that helps organizations monitor, evaluate, and control credit situations and credit allocations. It allows you to grant credit terms to your customers and also perform credit checks on the sales transactions. When you implement Credit Management in your SAP instance, you map your organization’s credit policies into the Credit Management application. Customers are aligned with these credit policy rules on the basis of the information collected from various sources, such as the customer’s past transactional history, the customer’s credit reports available from credit agencies like Dun & Bradstreet (D&B), the customer’s financial stability in the market, the geographical and political situations of the regions where the goods are sold, and so on. Each credit-related sales transaction is then monitored and evaluated with respect to these rules or policies, and the results of the evaluation help your organization decide whether to sell the goods on credit.

A credit check is a comparison of the customer’s credit exposure with the customer’s available credit limit setup in the credit master records. Credit exposure is a sum total of the open orders, open deliveries, open billings, open receivables, and open special liabilities. Credit limit is the maximum amount for which you allow your customer to purchase goods from you on credit. You store credit limits in the customer’s credit master records.

Whenever you create a new document that is relevant for credit checks, SAP calculates the current credit exposure for the customer and compares it with the customer’s available credit limit that is maintained in the customer’s credit master. If the exposure is more than the credit limit, the credit check fails. Figure 11-1 shows an example of applying credit management in a sales cycle.

Figure 11-1: Example showing credit processing

As you can see, a new sales order for customer ABC was created with an order value of $15,000. Since credit management is active and the document is relevant for a credit check, the SAP system inquires for the current credit utilization and maximum credit limit for the customer from the customer credit master. The total credit exposure for this customer (current utilization + current order value = 12,000 + 15,000 = 27,000) is greater than the credit limit ($25,000), and therefore SAP blocks the customer order. The credit representative then analyzes the document using the credit-blocked order reports and, after carefully evaluating the risk involved in releasing the order, approves and releases the order. The order is picked up by delivery processing and billed, and the SAP system posts the receivables to accounting.

In SAP, a credit limit check is carried out whenever a document is created or changed. You can perform credit checks at three points, namely, when a sales order is created or changed, when a delivery document is created or changed, and at the time of PGI. When the check is performed at the time of the order or delivery, the resultant document gives a warning, triggers an error message, or may even be blocked, based on the customization settings defined in IMG. When a check is performed at PGI, it behaves a bit differently. Since PGI is the last step in delivery processing, a credit check failure at the time of PGI cannot block the delivery document. Rather, it triggers an error message and stops the PGI from posting.

The Link Between a Credit Check and the Pricing Procedure

A SAP credit check is linked to SD pricing via the Subtotal field. For SAP to be able to derive the credit value (VBAP-CMPRE) from the sales document, the net value (final price + tax) line in the pricing procedure must have selection A in the Subtotal field. Without this setting in the pricing procedure, the credit check will not work.

Setting Up Credit Masters

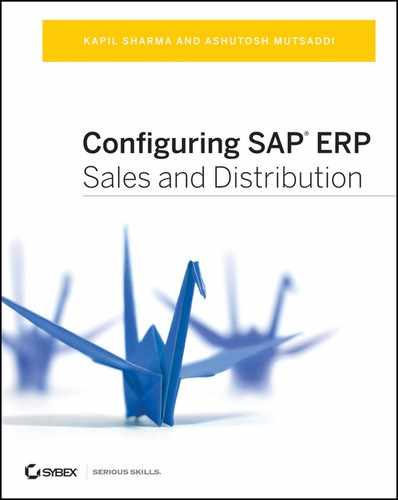

A customer credit master in SAP stores all the credit-related information for the customer. The credit master is set up for the combination of payer partner account and the respective credit control area. You can set up the credit master data by using the transaction FD32 or by following the SAP easy access menu path SAP Menu Accounting Financial Accounting Accounts Receivables Credit Management Master Data Change. Figure 11-2 shows the customer credit master data maintenance screen.

Figure 11-2: Customer credit master data

You maintain the customer credit limit in the Credit Limit field, and you maintain the risk category to which the customer belongs in the Risk Category field. The SAP system automatically calculates the sales value as a sum total of all the open orders, open deliveries, and open billing documents that are relevant for the credit check and that belong to the credit account. The open receivables value is taken from the customer A/R records, and the credit exposure is automatically calculated as the sum total of all the open values. The credit limit used is calculated by comparing the credit limit with the current credit exposure.

You can set the dates when the last internal credit review on the customer account was performed and when the next internal credit review for the customer account should be due. Using the Goto, Extras, and Environment menu paths in the menu bar at the top of the screen, as shown in Figure 11-2, you can pull up a variety of valuable information about the customer account, such as A/R summary, dunning summary, change log, and so on.

TIP Open orders are the orders that are not yet processed for deliveries, open deliveries are deliveries that are created but not yet processed for PGI, and billing and open billing are the billing documents that are generated but not yet posted to accounting.

Processing the Credit-Blocked Documents

SAP provides a set of five transaction codes to process documents that are blocked because of a credit check. You can use these transactions to generate a work list of credit-blocked documents. From the work-list screen, you can then do the following:

- Release the blocked documents so that they can be processed further for delivery and billing steps.

- Reject a credit-blocked document. The document is rejected and cannot be processed further.

- Reassign the documents to your peers.

- Forward the documents to another credit manager or credit representative for evaluation.

Table 11-1 discusses the five transactions for processing the blocked documents.

Table 11-1: Transactions to Process Blocked Sales Documents

| Transaction Code | Description | Use |

| VKM1 | List of blocked documents | Lists all the credit-blocked documents. |

| VKM2 | List of released documents | Lists all the documents that are manually released (status D). |

| VKM3 | Sales documents | Allows work-list generation based on sales document numbers. The list contains all the documents irrespective of whether the status is blocked (B), released (D), or approved (A). |

| VKM4 | List of all documents | Allows work-list generation including all the documents that are relevant for a credit check (i.e., deliveries and orders). The list contains all the documents irrespective of whether the status is blocked (B), released (D), or approved (A). |

| VKM5 | Delivery documents only | Allows work-list generation for delivery documents only. |

Important Notes and Programs Related to Credit Release Transactions

NOTE the following:

- So that a credit representative releases only the documents that they are eligible to release, SAP allows you to set authorization limits. Refer to SAP OSS note 1259643, which talks in detail about how to use authorizations.

- If you ever want to add new fields to the VKM* reports, you can use user exit DBKMVF02. Refer to SAP OSS note 779389, which talks about the details of how to add user-defined fields to VKM* reports.

- You can use programs RVKRED06 and RVKRED09 in the background job mode for automatic credit checks. This will reduce the load on credit representatives so they only have to deal with the scenarios that are exceptions and therefore need their approvals.

When you release a document manually using one of the VKM* transactions, the document’s overall credit status is set to D. This denotes that the document was under a credit block and has been manually released. Other document statuses used in SAP in Credit Management are as follows:

- A denotes the documents for which the credit check was successful.

- B denotes the documents that are in blocked status due to an unsuccessful credit check.

- Blank denotes the documents for which the credit check is not applicable.

To decide whether to release a document from a credit block, a credit representative needs information from various sources such as the customer’s past payment history, the customer’s A/R ageing, the oldest open item in A/R, the customer’s account summary, the dunning information on the customer, and so on. SAP provides this information to credit representatives via a set of reports available in the SAP FICO module (Table 11-2). For an SD consultant, it is good, but not essential, to know about these reports.

Table 11-2: Credit Information Reports

| Transaction Code/Program Name | Description |

| F.31/RFDKLI40 | Credit overview |

| F.33/RFDKLI30 | Brief credit overview |

| S_ALR_87012218/RFDKLI41 | Credit master sheet |

| FCV3 | Early warning list |

| F.32/RFDKLI10 | Missing data |

| F.28/RFDKLI20 | SD, FI: re-creation of credit data after organizational changes |

| S_ALR_87012215 | Changes to credit management |

| FDK43 | Master data list |

| FD11 | Account analysis |

| FD10N | Customer balances |

| FBL5N | Customer line items |

The credit management functionality in SAP spans SD and FICO and so does its customization. There is no predefined sequence that needs to be followed; the process we explain in the following sections is based on what we prefer to choose while configuring Credit Management in SD.

The customization at a high level involves the following steps:

1. Defining a credit control area

2. Assigning the credit control area to a company code and sales area

3. Defining the permitted credit control area for a company code

4. Defining credit risk categories

5. Setting up credit groups

6. Assigning credit groups to sales documents and delivery documents

7. Determining active receivables per item category

8. Setting up credit checks

The following sections cover these customization steps in detail.

Defining a Credit Control Area

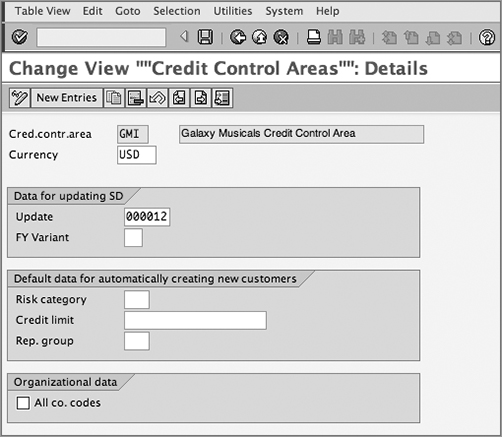

A credit control area is an organizational unit responsible for monitoring, evaluating, and controlling the credit management operations. Defining a credit control area is the first step in the customization of the credit managementfunctionality in the SAP SD application. You can define the credit control area by using the transaction code OB45 or by following the menu path IMG Enterprise Structure Definition Financial Accounting Define Credit Control Area. On the customization overview screen that appears next, click the New Entries button to define your credit control area. Figure 11-3 shows the customization screen that appears.

The fields on this screen are as follows:

Credit Control Area Here you provide the identifier key for your credit control area along with a meaningful description. The key can be up to four characters long. For Galaxy Musical Instruments, we defined the key as GMI.

Figure 11-3: Customization screen for setting up a credit control area

Currency Here you maintain the currency for the credit control area. Credit limits are maintained in the credit control area currency. In scenarios where the currency of the assigned company code is different from the credit control area currency, the credit exposure of the customers under such company codes is converted into the credit control area currency for the purpose of credit checks and related decision making.

Update rules In SAP, credit exposure is a sum of special liabilities, open receivables, open orders, open deliveries, and open billings. Update rules control when and how the data related to open orders, open deliveries, open billing, and open A/R is updated in the calculation of credit exposure. You can choose one of the following update groups that are available in standard SAP:

[Blank] If the field is left blank, the SAP credit management application ignores the SD documents and considers only open receivables and open special G/L items for calculating credit exposure.

000012 This update rule is available for a sales order cycle that involves delivery. In the event that a new order is created, the open order value is added to the exposure. When the order is delivered, the open order value is subtracted from the exposure, and the open delivery value is added to the exposure. On billing the delivery, the open delivery value is subtracted from the exposure, and the open billing value is added to the exposure. When the billing posts to accounting, the open billing value is subtracted, and the open A/R value is added to the exposure. The exposure is finally reduced when the cash is applied against the open A/R.

000015 Use this rule if you want SAP to calculate the exposure without considering the open sales order value. In this rule, when the order is delivered, the open delivery value is added to the exposure. On billing generation, the open delivery value is subtracted from the exposure, and the open billing value is added to the exposure. When the billing posts to accounting, the open billing value is subtracted, and the open A/R value is added to the exposure. The exposure is finally reduced when the cash is applied against the open A/R.

000018 This is relevant for nondelivery-relevant orders only. When a new order is created, the open delivery value is added to the exposure. When the order is billed, the open delivery value is subtracted from the exposure, and the open billing is added to the exposure. When the billing posts to accounting, the open billing value is subtracted, and the open A/R value is added to the exposure. The exposure is finally reduced when the cash is applied against the open A/R.

FY Variant In SAP, the fiscal or financial year of an organization is divided into a number of periods (a posting period and special periods). Fiscal year variant is the term used to represent and control these posting periods. When a document is posted into accounting, a fiscal year variant, along with a posting date, helps determine the posting period and fiscal year for posting the accounting entry into the correct period.

You should enter a fiscal year variant for your credit control area if the company codes that you will be assigning to your credit control area use different fiscal year variants. If they all use the same fiscal year variant, you can leave this field blank. The reason for this is that in SAP the credit values updated in the tables (S066) are recorded per posting period. In cases where the assigned company codes have different fiscal year variants, determining the correct posting period becomes difficult. The posting period in such scenarios can be determined only if you assign a default fiscal year variant to your credit control area.

Default Data For Automatically Creating New Customers The fields in this section of the customization screen are for creating the default credit check–related settings for new customers who have not yet been granted any credit terms. Provide default values in these fields if you want to perform credit checks on orders from new customers who have not yet been granted credit terms. We will discuss the credit check setup for new customers later in this chapter.

All Co. Codes Select this check box if you want to apply your credit control area to all the company codes that exist in your SAP instance.

CASE STUDY—Galaxy Musical Instruments Configuration Analysis: Credit Control Area Definition

Galaxy wanted centralized credit management and therefore decided to use centralized credit control area GMI with the USD currency. Galaxy wanted to perform credit checks by including open orders, open deliveries, and open billing values in the calculation of credit exposure and therefore chose update group 000012 to manage credit management for both the United States and Mexico. The Fiscal Year Variant setting is blank because both the company codes for Galaxy use the same fiscal year variant.

Assigning the Credit Control Area to a Company Code and Sales Area

Once defined, the credit control area needs to be assigned to the required sales areas and company codes. This way, you maintain a link between Credit Management, FI-A/R, and the SD application so you can monitor, evaluate, and control the credit transactions taking place in the assigned company codes and sales areas.

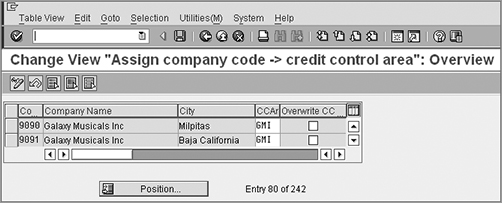

You assign a company code to a credit control area by using transaction code OBY6 or by following menu path IMG Enterprise Structure Assignment Financial Accounting Assign Company Code To Credit Control Area. Always remember that a credit control area can have multiple company codes, but a company code can be assigned to only one default credit control area. Figure 11-4 shows the customization screen for assigning company codes to a credit control area. The assignment is very simple. The company code data is already populated on the customization screen. You just need to maintain the corresponding credit control area in the CCAr field for all the required company codes.

Figure 11-4: Assigning a company code to a credit control area

NOTE Remember that this is the default assignment for a credit control area for the respective company codes. For example, company codes 9090 and 9091 will always have a default credit control area of GMI. If you want to have the flexibility to overwrite the default credit control area during document postings, you need to select the Overwrite CC check box for the particular company code for which you want this flexibility.

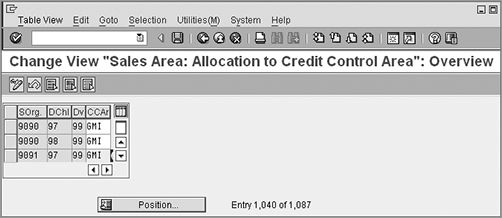

You can assign a sales area to a credit control area by using transaction code OVFL or by following menu path IMG Enterprise Structure Assignment Sales And Distribution Assign Sales Area To Credit Control Area. Figure 11-5 shows the configuration screen for assigning a sales area to a credit control area. As you can see, this assignment is also very simple. The sales area is automatically populated on the configuration screen. Use the Position button to position the cursor on the required sales area, and maintain the credit control area in the CCAr field for each required sales area.

CASE STUDY—Galaxy Configuration Analysis: Credit Control Area Assignment

Galaxy wanted to implement centralized credit management, and therefore both the company codes were assigned to the same credit control area, GMI (Figure 11-4). Since the credit management is to be used to perform credit checks on sales transactions, all the U.S. and Mexico sales areas were also assigned to the GMI credit control area (Figure 11-5).

The currency for the credit control area GMI is USD. Therefore, the credit limits for GMI can only be maintained in USD, and the credit checks will also be performed in USD, irrespective of the currency of the company codes. For performing credit checks on sales transactions belonging to 9091 (Galaxy Mexico), the SAP system will first internally convert the sales transaction value from Mexican currency into USD so as to calculate the credit exposure in USD and will then perform the credit check on the sales transaction.

Figure 11-5: Assigning a sales area to a credit control area

Centralized vs. Decentralized Credit Management

In SAP, credit management can be categorized as either centralized or decentralized.

Credit management is centralized when you assign all the relevant company codes to a single credit control area, as shown in following example:

| Credit Control Area | Company Code |

| 1000 | 1000 |

| 1000 | 1100 |

| 1000 | 1200 |

In this case, the credit limits assigned to the customer are valid across all the company codes assigned to the centralized credit control area. This chapter talks only about centralized credit management in SAP.

Credit management is decentralized when you have more than one credit control area to handle your credit operations. In decentralized credit management, you assign company codes to their individual credit control areas, as shown in the following example:

| Credit control area | Company Code |

| 1000 | 1000 |

| 1100 | 1100 |

| 1200 | 1200 |

Defining a Permitted Credit Control Area for a Company Code

In SAP, a credit control area can have multiple company codes, but a company code can have only one default credit control area. If you ever come across a situation where the business requirement demands use of an alternate credit control area instead of using the default credit control area assigned to the company code in OB38, you can configure an alternate credit control area using “permitted credit control areas for a company code” customizing. You can reach the customization screen by using transaction code OBZK or by following menu path IMG Financial Accounting Accounts Receivable And Account Payable Credit Management Credit Control Account Assign Permitted Credit Control Areas To Company Code.

As usual, use the New Entries button to maintain the customization entry, and maintain all the alternatives that you want to permit for a company code. For your alternate credit control area to work, the default credit control area assignment in OB38 must have the Overwrite CC check box selected. This selection tells SAP that the default credit control area can be overwritten.

Once both these settings are done, you can use your alternate credit control area in the transactions by manually replacing the default SAP-proposed credit control area with your permitted alternative credit control area. If you want to default this alternative credit control area for a specific customer, you can assign this on the Billing tab of the sales area data of the customer master as a default credit control area for that customer. You may also use user exit EXIT_SAPFV45K_001 to define your own determination rules, which will help overwrite the SAP-proposed default credit control area with your permitted alternative credit control area.

Defining Risk Categories

Risk categories help you group the customers based on their credit ratings. You can define separate controls for each risk category to monitor, evaluate, and control the credit situations and credit allocations.

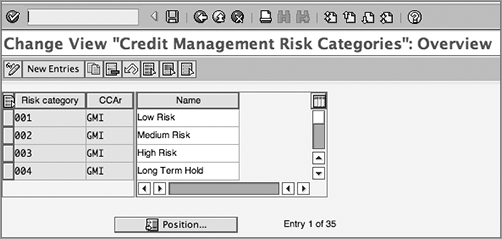

You define a risk category by using transaction code OB01 or by following menu path IMG Financial Accounting Accounts Receivable And Account Payable Credit Management Credit Control Account Define Risk Categories. Figure 11-6 shows the customization screen for setting up the risk categories.

To define your own risk categories, you just need to click the New Entries button, maintain an up-to-three-character identifier for the risk category with a meaningful description, and then assign the identifier to the appropriate credit control area. Figure 11-6 shows the risk categories that we set up for Galaxy Musical Instruments.

Figure 11-6: Defining risk categories

Determining Credit Control Area

A credit control area controls the credit operations. You assign a credit control area in customization to the company code and sales area. The credit control area is also assigned to the customer credit master record. You could even set up your own determination rules for your credit control area, as we just discussed. When you create a sales document, SAP uses these assignments to determine the credit control area for the sales transaction. For a sales transaction, a credit control area can be determined in the following sequence:

- Via user exit (EXIT_SAPFV45K_001)

- Customer master/sales area data (the Credit Control Area field on the Billing tab)

- Sales area (customization)

- Company code of the sales organization (customization)

CASE STUDY—Galaxy Configuration Analysis: Risk Categories

Every organization has its own way to rate its credit customers. For Galaxy, we grouped customers into four risk categories: Low Risk, Medium Risk, High Risk, and Long Term Hold. The Long Term Hold risk category was created to control credit allocations and credit checks for defaulters who have not paid off their long-outstanding receivables.

Defining Credit Groups

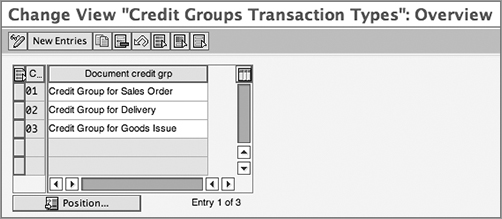

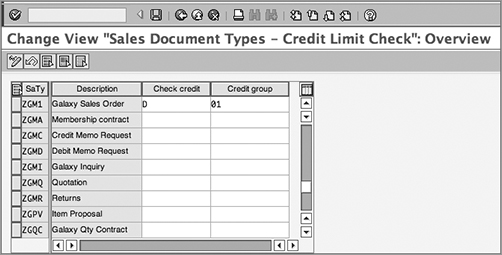

A credit group represents the business transaction where the credit check can be applied. Figure 11-7 represent the three credit groups that are provided in the standard SAP system to cover the three major business transactions in sales and distributions. You can reach this customization screen by using transaction code OVA6 or by following menu path IMG Sales And Distribution Basic Functions Credit Management/Risk Management Credit Management Define Credit Groups. As you can see, the available credit groups cover all three vital steps in sales order processing. It’s not very common that you have to define a new credit group for your credit management settings, but if the need arises, you can define one by clicking the New Entries button on the customization screen and providing a two-character identifier and a meaningful description.

Figure 11-7: Defining credit groups

Assigning Credit Groups to Sales Documents and Delivery Documents

In this step, you assign all the sales order and delivery document types that you would like to include in credit checks to their respective credit groups. To perform the assignments, you can use menu path IMG Sales And Distribution Basic Functions Credit Management/Risk Management Credit Management Assign Sales Documents And Delivery Documents. After you follow the menu, you will see a Choose Activity dialog box providing two options: Credit Limit Check For Order Types and Credit Limit Check For Delivery Types.

Credit Limit Check For Order Types Here you assign the sales document to the respective credit group. Figure 11-8 shows the customization screen for this assignment activity. You can also reach this screen using transaction code OVAK.

The assignment process is very simple. You just need to assign the sales document types to their respective credit groups. Galaxy is using credit group 01 to perform credit checks on sales order type ZGM1, as shown in Figure 11-8.

Another field visible here is the Check Credit field. This field controls whether the system runs credit checks during sales order processing and, if yes, whether it will be a simple credit check or an automatic credit check. We will discuss the selection value for this field later in the chapter, along with how to set up simple and automatic credit checks.

Figure 11-8: Defining credit groups

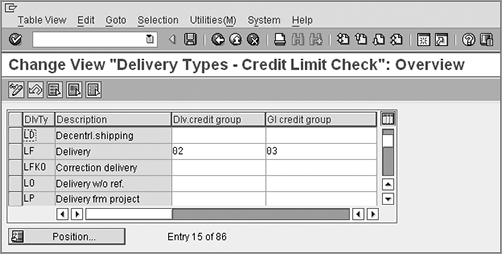

Credit Limit Check For Delivery Types This activity allows you to set up the credit groups for delivery documents. Figure 11-9 shows the customization screen for this assignment activity. You can also reach this screen using transaction code OVAD.

Here again, you just need to assign the delivery document types to their respective credit groups. Galaxy is using credit group 02 for performing credit checks at the delivery document (create/change) level for delivery type LF and is using credit group 03 to perform credit checks at the post goods issue (PGI) level for delivery type LF.

Figure 11-9: Defining credit groups

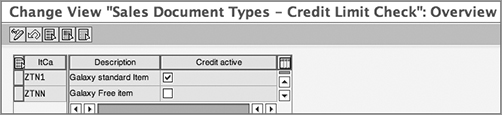

Determining Active Receivables per Item Category

In this step, you set up the item category relevancy for credit checks. This setting helps calculate the net order value that is relevant for the credit check. So, in the case of an order with four line items of $100 each, if three line items are set up as relevant to a credit check (based on their item categories credit check relevancy setup in OVA7), SAP considers only $300 as the net credit value for calculating the credit exposure for that sales order and excludes $100 for line 4, which is not relevant for the credit check.

To reach the customization screen, you can use transaction code OVA7 or follow menu path IMG Sales And Distribution Basic Functions Credit Management/Risk Management Credit Management/Risk Management Settings Determine Active Receivables Per Item Category. Figure 11-10 shows the customization screen for setting up item category relevancy for credit checks. To make the assignment, you need to select the check boxes for all the required item categories that you want to make eligible for credit checks.

Figure 11-10: Setting up item category relevancy for a credit check

Always remember that credit checks in SAP are performed against a payer partner after accumulating all the necessary financial figures and all the open order, open delivery, and open billing documents. When you create an order document, all the credit relevant line items from the order are summed up to calculate the total sales order credit value. SAP then searches the credit existing exposure for the payer account from the sales order by looking into the credit master data record for the payer and add the credit value from the sales order to the existing credit exposure to calculate the total credit exposure value. This total exposure value is then compared against the total credit limit available to the payer and accordingly SAP blocks or approves the credit check on the sales order and updates the credit status at the document header level.

Setting Up Credit Checks

SAP provides two types of credit check, namely, a simple credit check and an automatic credit check:

Simple credit check A simple credit check, as the name suggests, is very simple in nature. The functionality is limited and considers only open A/R items and open items from special G/L and sales orders for performing the credit checks. When you create/change a sales order that is relevant for a simple credit check, SAP calculates the payer/customer’s credit exposure by adding the open A/R balance for the customer, open item balances from the special G/L, and the net sales order value. This credit exposure is then compared against the customer credit limit maintained in the customer’s credit master. If the credit exposure is greater than the credit limit, the system sets the credit check status as “fail” and shows a warning, generates an error message, or performs a delivery block.

Automatic credit check An automatic credit check is more robust than a simple credit check. Unlike a simple credit check, where you apply a standard rule across all the credit check–relevant documents, an automatic credit check allows you to pick and choose from a variety of credit check rules available in the standard SAP system to base your credit checks on. You can specify when and when not to perform a credit check, can include seasonal factors, and can even define and use your own credit check rules.

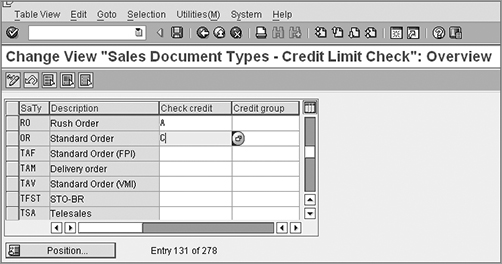

Setting Up a Simple Credit Check

You set up a simple credit check in customizing by using transaction code OVAK or by following menu path IMG Sales And Distribution Basic Functions Credit Management/Risk Management Simple Credit Limit Check. Figure 11-11 shows the configuration screen for maintaining simple credit checks.

Figure 11-11: Customization screen for configuring a simple credit check

To set up a simple credit check, you need to maintain values in the Check Credit field corresponding to each and every sales document type for which you want the simple credit check to happen. The Check Credit field specifies whether the system runs credit checks for sales documents and, if it does, what types of credit check the system would run and what impact it would have on the corresponding sales order document. Table 11-3 lists the possible values that you can maintain for the Check Credit field and their impacts.

Table 11-3: Possible Values for Simple Credit Checks and Their Impacts on Sales Orders

| Selection Value | Impact |

| Blank | No credit check occurs. |

| A | The system shows a warning message; the sales order can be delivered and allowed to perform further processing. |

| B | The system shows an error message; the sales order cannot be saved. |

| C | The system sets up a delivery block on the sales order; the order can be saved but cannot be delivered. |

Setting Up an Automatic Credit Check

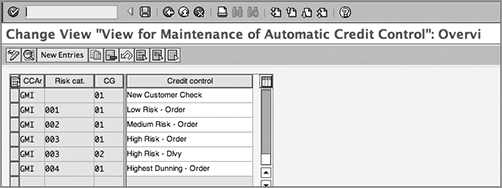

You set up the automatic credit check by using transaction code OVA8 or by following menu path IMG Sales And Distribution Basic Functions Credit Management/Risk Management Credit Management Define Automatic Credit Control. Figure 11-12 represents the overview screen for defining automatic credit checks. In SAP, each automatic credit check rule is defined for a unique combination of credit control area, risk category, and credit group. This provides you with the flexibility to assign different checks for different combinations, thus allowing new-customer sales order credit check rules to differ from a high-risk credit customer sales order. Take a look at Figure 11-12, and you will notice that we defined a couple of credit control rules for Galaxy, each identified on the basis of a unique combination of credit control area, risk category, and credit group field.

Figure 11-12: Defining automatic credit control, overview screen

As always, you can use the New Entries button to define your own automatic credit checks or you can use the Copy button to create one by copying from an existing one.

TIP If you are configuring an automatic credit check, in addition to OVA8 setup, make sure that the sales document types on which you would like to perform the automatic credit check are configured, as shown earlier in Figure 11-8.

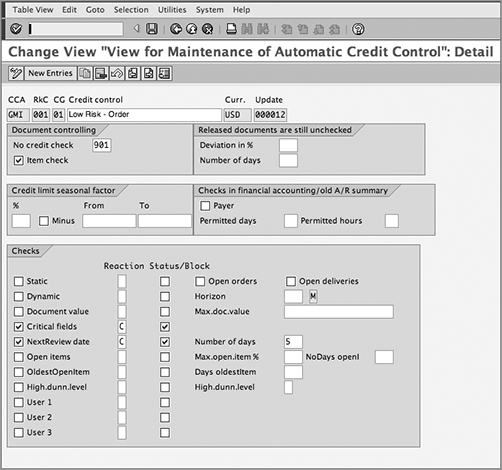

Figure 11-13 shows the customization detail screen for automatic credit control setup. For the purposes of this chapter, we will break this customization screen into logical sections and will show examples (wherever required) to explain the use and impact of section/field in the credit check. The first section on the customization screen shows the key combination that controls the credit check, which we already discussed. The Currency and Update settings in Figure 11-13 are automatically proposed by the system from the credit control area customization (from OB45 setup) and cannot be changed.

Figure 11-13: Defining automatic credit control, detail screen

The other sections of the screen are as follows:

Document Controlling Here you set the overall document-level controlling for your credit check rule. There are two fields:

No Credit Check Here you can set up your own requirement to not trigger credit checks on certain documents or in a certain situation. A common use of this field is for manually released documents. In standard SAP, manually released documents are rechecked when there is a substantial change. If you would like to not check the manually released documents with a credit check again, you can create a requirement using ABAP help and can assign the requirement number in this field.

Item Check If you select this check box, SAP takes into consideration the item category relevancy for credit checks. The credit check happens for all the items in the document that are relevant for credit checks. When this check box is not selected, the credit check is performed at the document header level.

Released Documents Are Still Unchecked Here you set the rule that controls when to recheck the documents for credit checks if they were originally released manually.

If the dollar value for any manually released document is changed beyond the threshold percentage defined in the Deviation In % field, the document is rechecked for credit check calculations.

If a manually released document has passed the threshold limit specified in the Number Of Days field, the document will be again rechecked for credit check calculations after taking into account whether the new value exceeds the calculation as per the Deviation In % field.

Checks In Financial Accounting/Old A/R Summary This check against the A/R summary helps you ensure that the credit checks are always happening against the latest open A/R summary for a payer. Here you define the permitted number of days and permitted number of hours for an A/R summary to be used for credit check calculations.

NOTE In SAP, you use transaction code FCV1 to generate an A/R summary. The A/R summary is beneficial for decentralized credit management where you have sales transactions happening in system X and you want to transfer the open A/R balances from system Y for performing credit checks on sales documents in system X. In the case of centralized credit management, an A/R summary is helpful in improving system performance because every time SAP checks open A/R balances for credit check calculations, it doesn’t need to go to various FI tables and instead can easily pick up information from the A/R summary table (KNKKF1). In SAP, you can define the validity for the A/R summary and can put the A/R summary program in periodic batch job runs for regular updates to the KNKKF1 table.

Role Of Seasonal Factors In Credit Check In SAP, you can add seasonal factors to your credit check. For example, during holiday seasons, if you wanted to relax or restrict your customer’s purchasing power by some percentage, you can do it using this customization check.

Reaction By making an appropriate selection in this field, you can control how the system reacts in situations where the credit check for a document is unsuccessful. The available options are as follows:

- Blank: No message is sent to the user.

- A: A warning message is issued to the user informing them that the credit check was unsuccessful.

- B: An error message is issued to the user with information about the unsuccessful credit check, and the document cannot be saved.

- C: This is just like A, but it tells the user the exact amount by which the credit exposure is above the credit limit.

- D: This is just like B, with the information provided to user about how much more the credit exposure is above the credit limit.

Status Using the Status field, you can set the document status as blocked or unblocked. When selected, the document will be blocked if it fails the credit check; otherwise, it will not be blocked.

Static Credit Checks As the name suggests, a static credit check is static in nature. There is no time factor in play when the credit check is calculated. SAP provides two check boxes, Open Orders and Open Deliveries, which control the credit checks. Based on whether you select only sales orders, only deliveries, or both sales orders and deliveries for a static check, SAP selects the documents.

Dynamic Credit Checks A dynamic credit check allows you to use horizon periods for calculating credit checks. Which documents should be picked for a credit check by SAP depends upon what horizon periods you set when customizing in this check. You can define a horizon in days, weeks, and months. So if you set a dynamic credit check in customization with a two-month horizon, SAP will only pick up documents for the customer that fall in this two-month horizon period to calculate the credit exposure. If there are any sales documents from the customer that fall outside this horizon period, they are excluded from the credit check. Dynamic credit checks can be performed only on sales order documents.

Document Value Check This field, in conjunction with the value in the field Max.Doc.Value, decides how the system behaves when the maximum allowable document value is exceeded. Figure 11-14 shows how the document value check impacts the credit check for a sales document.

Figure 11-14: Example showing the document value check

Critical Fields Check Payment Terms, Fixed Value Date, and Additional Value Days are the three predefined critical fields in the standard SAP system. With this check, the SAP system compares and ensures that the values for these critical fields in the sales document are exactly similar to what is maintained in the corresponding customer master record for the customer. If the values are the same, the document passes the credit check; otherwise, the credit check is unsuccessful.

Next Review Date Check The credit review is a periodic activity. Organizations do perform credit reviews on a regular basis and make sure that the credit terms in the customer master are appropriate with respect to the current credit analysis on the customer account. This check allows you to block the sales documents of a customer whose credit review information is old, such as if the next review date has already passed and the customer account is still pending credit review.

Open Items Check Long-open A/R balances often turn into bad debts if the proper controls are not in place to stop an A/R from falling into the long-term A/R bucket. This check helps you block customer sales orders if the customer open A/R balance has reached a certain threshold. This check works on the combined result of two fields: the number of days outstanding and the percentage of total A/R. If both the conditions hold true, only then the credit check is successful. Figure 11-15 shows how an open item check impacts the credit check for a sales document.

Figure 11-15: Example showing open items check

As you can see, customer ABC has a total A/R balance for $50,000. The overdue balance of more than 45 days is $35,000, which is 70 percent of the total A/R. As per the credit check rules, if the outstanding balance of more than 45 days is above 40 percent of the total A/R, the credit check will block the document, and thus the sales document gets a credit block.

Oldest Open Items Check Just like the previous check, this check takes into consideration a customer’s open A/R values. This check gives you control to block the customer’s sales document in situations where customer is defaulting for a particular invoice payment that is about to cross the threshold limit set in customizing and that may turn into a bad debt. For example, suppose customer X is a medium-risk customer and in customizing for medium-risk credit-check rule, you entered that the oldest open items allowed for a medium-risk customer is 90 days with status checkbox checked. Now the day customer X has any A/R item outstanding more than 90 days, SAP will start blocking the orders for customer X.

Highest Dunning Level Check In SAP, you send dunning letters to customers as a payment due reminder. Dunning level refers to the number of times you have sent a dunning letter to a customer for the same A/R. Level 1 may be configured as a friendly reminder sent one week before the payment is due, level 2 may be configured as a reminder one week after the payment was due, level 3 may be configured as a reminder one month after the payment was due, level 4 may be a reminder two months after the payment was due, and so on.

Using this check, you set a threshold for dunning letters when customizing. For example, you can set a credit check rule to block all the sales documents for the customer if they’ve been sent three letters of dunning and the payment for A/R is yet to be received.

Custom Defined Checks In SAP, you can define up to three user-defined credit check rules. For defining your own credit check rules, SAP provides the user exits LVKMPFZ1, LVKMPFZ2, and LVKMPFZ3 that correspond respectively to the User 1, User 2, and User 3 check boxes on the OVA8 screen.

To give you an idea of how you can use these rules in real time, Table 11-4 shows the credit rules configured for Galaxy Musical Instruments.

CASE STUDY—New-Customer Credit Check for Galaxy Musical Instruments

To have better credit controls, Galaxy felt a need to put all the newly opened accounts into one default category called New Customer. As a process in Galaxy, a new customer account is opened by a sales representative, and the credit allocation and processing is performed by a credit representative working in the finance department. The lead time for setting up the credit master for the new customer is one day. Galaxy wanted to have the flexibility to allow the creation of a sales order without waiting for a credit master to be set up in SAP, but at the same time Galaxy wanted these orders to be in a default credit block, which could later be released by the credit managers once they have set up the credit master for each new customer. To do so, Galaxy set up the credit rule (GMI + blank + 01) for new customers in Automatic Credit Checks. To make sure that this rule was called up in SAP while processing transactions for a new customer, Galaxy activated the new customer settings available in OB45 by assigning a default credit limit of $1.

As a result, Galaxy was able to provide parallel processing to the sales and credit teams: the sales team got the flexibility of creating orders for new customers without waiting for the credit team to set up their credit masters, and at the same time the credit team was not worried about a credit risk due to new customers because all the orders for new customers are under a default credit block.

Table 11-4: Galaxy’s Credit Rules

ZGMI is the centralized credit control area for Galaxy.

Risk category 01 is for low risk, 02 is for medium risk, 03 is for high risk, and 04 is for the highest dunning. New customers are taken care of by using a blank risk category.

Credit group 01 represents sales documents, and 02 represents delivery documents.

Requirement 901: Do not perform credit checks again for documents released manually from a credit block. Applicable only to orders.

Requirement 902: Do not perform credit checks again for documents released manually from a credit block. Applicable only to deliveries.

Troubleshooting Credit Management: Helpful OSS Notes

- 18613, Checklist for Credit Management: This OSS note provides a general customizing checklist that you can use if you face any customization-related trouble with credit management.

- 377165, Update Open Credit Values for Credit Management: This note provides valuable insight about how open values are updated in SIS structures S066 and S067 in SAP.

In this chapter, we discussed credit management in detail, including concepts, processes, and customization, and also used the Galaxy Musical Instruments case study to provide examples for customization. We discussed how credit management works in SAP and how can you customize it to suit your business needs. In the next chapter, we will discuss various material-related functionalities that are available in SAP SD.