Inactivity Based Cost Management

An Activity has a cost incidence whereas Inactivity a cost consequence. Measure Cost Consequence, Now, Now, Now.

—Jayaraman Rajah Iyer*

Inactivity Based Cost Management1 (IBCM) functions on the following five principles:

- Principle #1: What gets measured, gets managed

- Principle #2: Measure Qualitative Elements of Management

- Principle #3: Corporate Atomic Structure

- Principle #4: Return on Intangible

- Principle #5: Emergent Property Phenomenon

Principle #1: What Gets Measured, Gets Managed

Some of the notable events in corporate history provide evidence of this. Lockheed, an American aerospace company, was the first major financial scandal that rocked the corporate world, in 1976. Then secretary of state Henry Kissinger maintained that disclosure would harm other governments and damage U.S. relations with them.2 There was one minor consolation: Reports of rampant payoffs by Exxon, Gulf, Mobil, Northrop, United Brands, and other corporate giants had not directly implicated any major world leaders.3 Ashland Oil Inc. argued that securities laws did not require public disclosure of the recipients of questionable payments the company claimed to have made in Nigeria, Gabon, Libya, and the Dominican Republic. Ashland had already supplied the names to the SEC. Lockheed went further. It stated that identifying its beneficiaries could hurt its $1.6 billion backlog of unfilled foreign orders, presumably by causing embarrassed foreign governments to cancel contracts, and also damage prospects for future sales. Nor would Lockheed promise to make no more political payments. Such payments, it said, are a normal and necessary feature of doing business in certain parts of the world, are essential to sales, and “are consistent with practices engaged in by numerous other companies abroad.”4

A report from the Reserve Bank of Australia Bulletin February 19955 analyses the collapse of Barings Bank, thanks to the reckless actions of Nick Leeson. The Board of Banking Supervision concluded that the failings at Barings could not be attributed to the complexity of the business carried out within BFS (Baring Futures [Singapore]) but were primarily a failure on the part of a number of individuals within the Barings Group to do their jobs properly. Against that background, the board outlined five main lessons for management flowing from the Barings failure:

- Management teams have a duty to understand fully the businesses they manage.

- Responsibility for each business activity has to be clearly established and communicated to all relevant parties.

- Clear segregation of duties is fundamental to any effective control system.

- Relevant internal controls, including independent risk management, have to be established for all business activities.

- Top management and the audit committee have to ensure that significant weaknesses, identified to them by internal audit or otherwise, are resolved quickly.

What emerges from these findings is that there’s no measurement system for ethical behavior within these companies. That concept is completely missing. The range of such wrongdoings has only increased from 1976 to 1995 to 2019. This period has witnessed the downfall of firms such as Enron, Robert Maxwell, Madoff, IL&FS, and the slow but sure diminishing of the Big 8 audit firms to the Big 4 firms. Referring to the audit committee seems to be the standard panacea for such ongoing corporate ills. A common streak is that these downfalls have each been caused by the actions of a single individual freely running amok with a license of hedonism akin to that in the 007 James Bond movie Goldfinger. Charles Ferguson’s Inside Job reveals a lot about these perpetrators. Some of the interviewees have described the lavish lifestyle of Richard Fuld, CEO of Lehman Brothers, replete with mansions, private elevators, an art collection filled with million-dollar paintings, a bunch of corporate planes. Jeffrey Lane, vice chairman of Lehman Brothers (2003–2007), says, “Fifty-billion-dollar deals were not large enough, so we do hundred billion-dollar deals.” Willem Buiter, chief economist of Citigroup, says, “Banking became a pissing contest, you know; mine’s bigger than yours; that kind of stuff. It was all men that ran it, incidentally.” It is also worthy of note that none of the errant bosses in each of these scandals were women. The intangible, a force that converts mass into energy and vice versa, does not have a gender bias. In fact, when applying the measure to management, it is more likely that women will reach board-level appointments by their sheer performance on intangible measurements than men.

Illustratively, in the Government Auditing Standards January 2007 Revision issued by the U.S. Government Accountability Office,6 the word “governance” has been used 60 times and barring two, it is prefixed with the phrase “those charged with.” It implies (1) governance is a staff function and there are individuals who are not entrusted with governance and (2) audits are undertaken in the same pattern as balance sheet audit. “Performance audit objectives may vary widely and include assessments of program effectiveness, economy, and efficiency; internal control; compliance; and prospective analyses.”7 In both the cases understanding of governance needs further explanation. The expression “those charged with governance” is akin to “those who are charged with breathing.”

The simple fact is what gets measured, gets managed. This is the first resolution an organization should believe in, for other benefits to follow. Governance needs to be measured, only then can governance be managed.

Principle #2: Measure Qualitative Elements of Management

A global survey of 378 senior executives, jointly conducted by KPMG International with the Economist Intelligent Unit (EIU), on corporate sustainability, concluded,

Many firms are grappling with the problem of deciding exactly what and how to measure, and appropriate benchmarks are scarce. Deciding how to measure is more difficult than deciding what to measure with 78% of respondents considering creating or finding reliable internal data, 76% finding a meaningful benchmark, and 65% determining what to report on, a “major” or “moderate” challenge.8

Corporate needs to scrutinize their buzzwords carefully. “Sustainability” is another such that remains unexamined. A way to bypass this is to first apply the #1 Principle test, that is, what gets measured, gets managed. In the KPMG–EIU survey, the respondent base was highly placed: 26 percent were CEOs, presidents, or managing directors of their firms; half represented the C-suite or board, and all respondents were in a management position. Measuring qualitative elements of management will have to be addressed squarely.

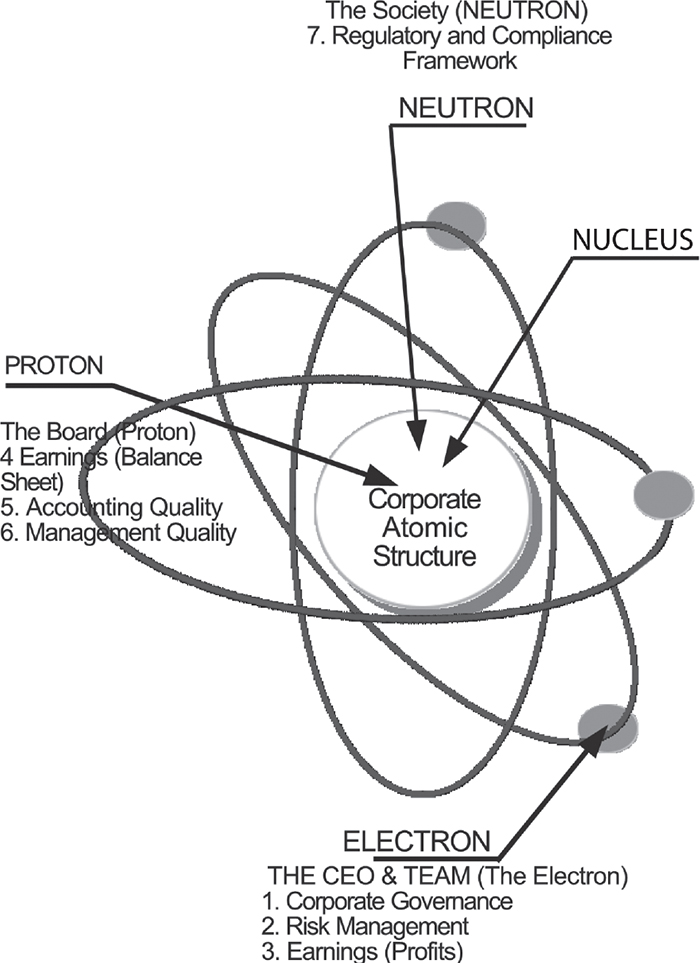

Principle #3: Corporate Atomic Structure (Figure 6.1)

Figure 6.1 3-D corporate atomic structure

Restructure the Organization

The intangible is the energy force that pervades corporate. In the Subject–Object distinction between the Qualitative and Quantitative elements of corporate management, the Subject, a person possessing the pulsating energy, delves into matters of metaphysics. The Object is inert, but its logical structure is unique with Quality and Action integrated. The Subject is the driver of movement in man-made Objects. By the second principle, we found many corporate managers knew what to measure but struggled with how to measure. What Galileo said could be meaningful: “Measure what is measurable, and make measurable what is not so.” Organizational restructuring is called for to accommodate issue areas we find difficult to measure.

Redesign with a 3-D Corporate Atomic Structure

Corporate needs to discard the 2-D spreadsheet organization structure currently in use. When the intangible is placed in the pivotal position, the organization structure revolves around it. The intangible is a metaphysical concept. The Kantian ideal of the science of metaphysics with a logical structure like that of the well-established mathematical and natural sciences is now made possible. A 3-D Corporate Atomic Structure reflects the natural formation of atomic structure, with only two processes in the making. By connecting the laws of physics to metaphysics, lasting metrics, measures of quantitative assessment, are established. Martin Rees, a British cosmologist and astrophysicist, talking about aliens says, though they may come from planet Zog and have seven tentacles, they would be made of similar atoms to us. That’s not an issue here, for corporate has not thought about being one with nature. They stand aloof from the laws of physics; rather corporate structure as of now is alien to the entire universe, indeed. First of all, let corporate gather momentum to sync with physics, by creating a Corporate Atomic Structure. Let us compare the similarities between the Atomic Structure and Corporate Atomic Structure (Table 6.1):

Table 6.1 Similarity between atomic structure and corporate atomic structure

|

Atomic structure |

Corporate atomic structure |

|

1. Every atom is made from three kinds of elementary particles: protons, which have a positive electrical charge; electrons, which have a negative electrical charge; and neutrons, which have no charge. |

1. Every substance is made up of three kinds of elementary particles: policies, which have a positive charge; practices, which have a negative charge; and the society, which has no charge. |

|

2. Protons and neutrons are packed into the nucleus, while electrons spin around outside. |

2. Policies and the society are packed into the nucleus, while practices spin around outside. |

|

3. The number of protons in an atom is always balanced by an equal number of electrons. |

3. The number of categories of personnel in policies is always balanced by an equal number of categories in practices. |

|

4. Neutrons don’t influence an atom’s identity, but they do add to its mass. |

4. Society doesn’t influence the identity of a company, but it does add to its mass. |

|

5. (e = mc2): e in the equation stands for energy, m for mass, and c square for the speed of light squared. |

|

|

In the simplest term, what the equation says is that mass and energy have an equivalence. They are two forms of the same thing: Energy is liberated matter; matter is energy, waiting to happen. |

|

|

Since c2 (speed of light by itself) is a truly enormous number, what the equation is saying is that there is a huge amount, a REALLY huge amount, of energy bound up in every material thing. |

|

What Corporate Atomic Structure Means

Every Substance is made up of three kinds of elementary particles: policies, which have a positive charge; practices, which have a negative charge; and society, which has no charge.

- The most significant part of a 3-D Corporate Atomic Structure is that society is brought into the structure. This means it is integrated into the Corporate Management Operating System. The impact on the Corporate Value System would be immense.

- Policies and society are packed into the nucleus, while practices spin around outside.

- The day the registrar of companies approves, a company is dragged into society, with all the paraphernalia of regulators joining in.

- The board and society form a nucleus.

- In the Atomic Structure, protons and neutrons form a nucleus. Protons are 1,837 times the mass of an electron. Electrons spin pretty fast, nearly three-fourth of the speed of light. So fast that they can go off tangent. It’s the neutrons that stabilize the electron from spinning off the nucleus.

- In the Corporate Atomic Structure it’s society that prevents the CEO from spinning off its nucleus. It greatly stabilizes the functioning of a company.

- The number of categories of personnel in policies is always balanced by an equal number of categories in practices.

- In the Subject–Object Distinction of Qualitative and Quantitative Elements of Management, in the CREAM Report Framework Refer Figure 6.2, the number of people for each task as a team is five, one from the Corporate Ethical Responsibility Force and four from the Corporate Fiscal Responsibility Force. It is irrespective of, for policies or practices that may be under scrutiny of any Process Block.

- Society doesn’t influence the identity of a company, but it does add to its mass.

- The neutrons of an organization impact its stability factor. The Ethical Motive triggers the Profit Motive, not the other way around.

- (e = mc2): e in the equation stands for energy, m for mass, and c2 for the speed of light squared.

- Profits are the energy created by a company. We normally calculate only the fiscal assets, which constitute the mass. Profits are the result of using fiscal assets to the optimum.

- Energy is created mainly from ethical assets. What we call c2 is that it refers to the ethical asset usage. A team of five for each task is backed by an undertaking on ethical responsibility to optimize results.

- Sustainability of efficiency, which arises from the best use of fiscal assets, results in profits. Sustainability of Value System, which arises from the best use of ethical assets, adds energy and therefore greater results.

- Corporate lives in Plato’s cave must go out and find out how ethical standards are practiced and measured, which is not happening, so as to maintain the sustainability of profits and growth. In the simplest term, what the equation says is that mass and energy have an equivalence. They are two forms of the same thing: Energy is liberated matter; matter is energy, waiting to happen.

- Cost of Inaction is wasted energy and time, where mass is waiting to be used.

- In reality, an electron cannot be stopped as it continuously spins around the nucleus at an unimaginable speed.

- Neither should the CEO team, who should never allow fiscal and ethical assets to fall into a state of insentience.

- Since c2 (speed of light by itself), is a truly enormous number, what the equation is saying is that there is a huge amount, a really huge amount, of energy bound up in every material thing.

- That optimum is very huge, represented by c2. It refers to the Subject; the capability of each individual is truly huge to create a prodigious amount of energy for an organization.

- If so, then the profits for a company are indeed huge. Speed of light times the speed of light.

- Energy is bound up in every material thing. Release it for the good of society. An organized approach is what is needed for corporate.

007 Factor—The Corporate Benchmark

For corporate to exist as they should requires Corporate Hydrogen, made up of fiscal and ethical assets, be governed in a way that converts mass into energy at the optimized level of performance. Corporate does not do anything more than the universe does: Creative Process and Action Process, creation and destruction. Nothing else, kicking matter from one space to another. Newton’s First Law of Motion applies here: “An object will remain at rest or in uniform motion in a straight line unless acted upon by an external force.” We may add two steps to it: First, recognize the creation of ethical assets as matter or substance, and second, kick the matter thus created to send it from one plane to the other. This process takes place as routinely as operating a piece of machinery. Machinery produces a product and an ethical asset produces energy. The 007 factor will be the corporate benchmark applied to both Fiscal and Ethical Assets. Rees defines the composition of the universe. When we apply the same attributes to corporate, the results would be similar. It creates a “Goldilocks effect” for corporate (Table 6.2).

Table 6.2 Benchmarking corporate atomic structure aligning with atomic structure

|

Atomic Structure* |

Corporate Atomic Structure |

|

1. For the universe to exist as it does requires that hydrogen be converted into helium in a precise but comparatively stately manner, specifically, in a way that converts seven one-thousandths [.007] of its mass into energy. |

1. For the corporate to exist as they should, requires Corporate Hydrogen, made up of fiscal and ethical assets, be governed in a way that converts mass into energy at the optimized level of performance and use. |

|

2. Lower that value very slightly, from seven one-thousandths [.007] to six one-thousandths [.006], say, and no transformation could take place: The universe would consist of hydrogen and nothing else. |

2. Lower the level of performance and use, even slightly, and no transformation takes place—the company would consist of nonmoving Ethical and Fiscal assets and nothing else. |

|

3. Raise the value very slightly, to eight one-thousandths, and bonding would be so wildly prolific that the hydrogen would long since have been exhausted. |

3. Raise the value of use, rather misuse, of any one of the assets, such as diversion of funds, assets base would long since have been exhausted. |

|

4. At .007 state, gravity is perfectly pitched—“critical density” is the cosmologists’ term for it—and will hold the universe together at the just-right dimensions to allow things to go on indefinitely. Cosmologists, in their lighter moments, sometimes calls this the “Goldilocks effect”—that everything is just right. |

4. At 007 factor of governance, gravity is perfectly pitched between the board of directors, the CEO team, and society, such that it will hold a company together at the just-right dimensions to allow things to go on indefinitely. This would be the “Goldilocks Effect” of Corporate Governance, where everything is Just Right. |

*Martin Rees.

Principle #4: Return on Intangible

Return on Intangible shall be seen in the background of what American neuroscientist David Eagleman says,

If we take a cubic centimeter of one’s brain tissue, there are as many connections between them9 as there are stars in the milky ways in the galaxy. These strange alien landscapes of neurons and synapses, somehow with strange materials, map on to decision making.

The cubic centimeter of each brain, not of a team or a group of elite people who run an organization, but of every human we come across on this planet. Return on intangible is an equation when applied to corporate affairs will have a significant impact on the growth and reaching targets, for it encompasses the capability of every individual with an organization. Truly, return on intangible is a capability model. The equation is as follows:

Return on Intangible = (Action or Inaction)/Intangible.

Action or Inaction in the numerator and Intangible the denominator.

Action is 1 and Inaction is 0. Intangible is always 1, for Intangible reveals human capability that is common to all.

This is the same formula as Newton’s Second Law of Motion: Force = mass x acceleration.

The purpose of what the Second Law states is not to keep the mass static, but to keep it moving. That’s what a CEO team does, not allowing any substance to rest in a static position. In the Six Stages of Transformation during the Creative Process, there’s a continuous movement of linear growth toward creating a substance. In the Action Process, the same Six Stages are replicated toward task accomplishment. In the case of an electron in an atom, there’s a continuous movement spinning around the nucleus. It’s not so in the case of the corporate electron—the CEO team. So, we have conveniently divided the entire Action Process into six sections. When targets are met the numerator is 1. That is to say, 100 percent task accomplishment gets Action rating to 1, which ensures the mass is moved out and the energy is created.

There’s a possibility some may or may not reach their targets. Accordingly, the stage for each task would indicate two factors: (1) stage completed and (2) simultaneous gap between the target and the stage completed. In an organization, there are millions of such tasks assigned to every individual that would be identified as to dT/dT, series of tasks in respective series of Time. This holds good both in the Creative Process and the Action Process. The Creative Process has six stages of development from the domain of the intangible through to a substance in the tangible field. IPR is one such tangible substance. The unavoidable six stages of the Creative Process vary, moving from one phase to another linearly. There is no quantum jump in the Creative Process. These six stages of transformation in the creative process will be useful by setting targets for innovation to quicken or broaden each phase accordingly. Illustratively, in the recent outbreak of COVID-19, The Economist in its 6th May 2020 edition states: More than 7,000 papers on the pandemic - covering everything from virology to epidemiology - have appeared in the past three months. A fifth of them has come out in the past week alone.12 Innovation is individual-centric and therefore participants in the six stages are made accountable. This book is emphatic about the six stages being completed, stage by stage, lest the end product ends up lacking quality and accountability. Since the denominator is 1 and the binary value makes it clear as to the stage reached, a corporate rating of active elements and simultaneously of inactive elements is obtained. Return on intangible, therefore, for a company as a whole is a single-digit figure between 0 and 5. When it is below 5 an Index of Inactivity furnishes by process area as well as by resource area, only resource is intangible.

Traditional return on investment (RoI) is replaced by return on intangible (RoI). It triggers the capability of every individual and tracks it.

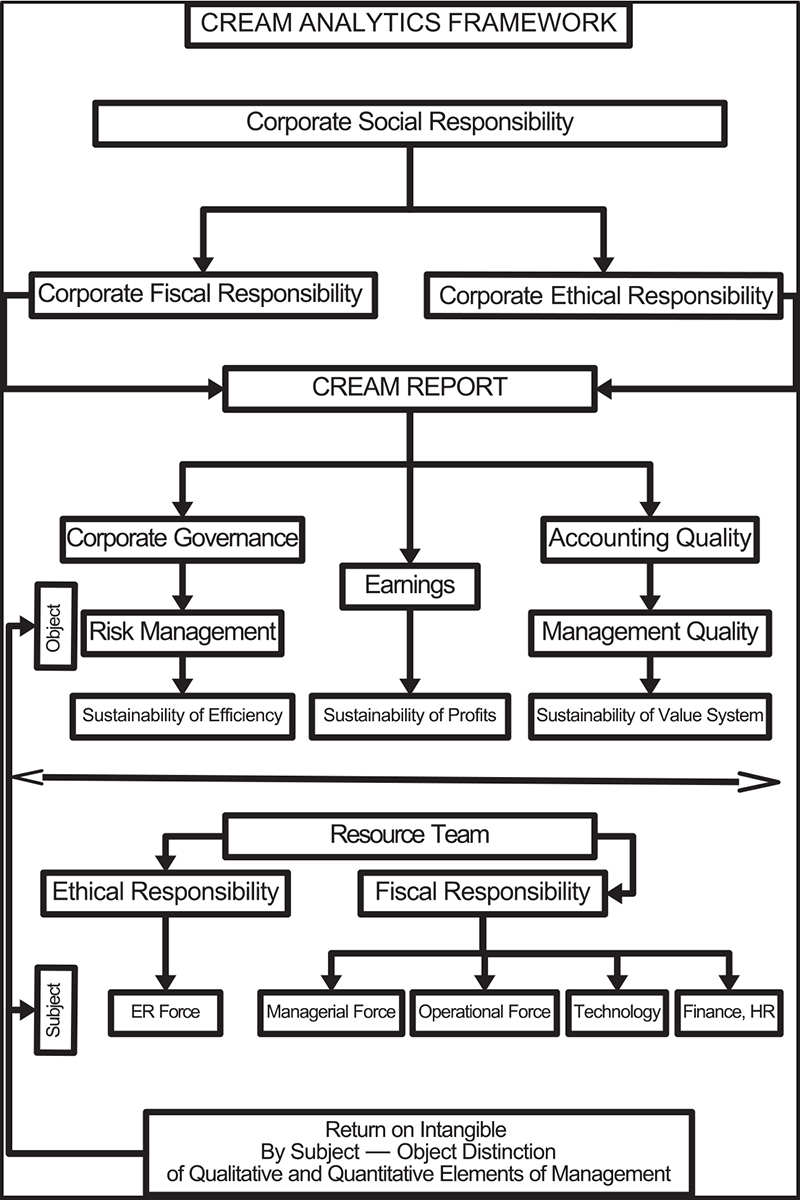

CREAM Analytics Framework (Figure 6.2)

Figure 6.2 CREAM analytics framework

CREAM stands for the following:

- C—Corporate Governance

- R—Risk Management,

- E—Earnings: split into (i) P&L and (ii) Balance Sheet

- A—Accounting Quality

- M—Management Quality

Each Process Block has a team of five representing the Ethical and Fiscal Responsibility group. Create Process Blocks for the organization. There are about 170 Process Blocks, as the case study of HUL in Chapter 8 shows—CREAM Report. These open-ended Process Blocks consist of both Qualitative and Quantitative elements of management. Each is manned by a team of five members, one Ethical Responsibility and Four of Fiscal Responsibility.

These Process Blocks come under two categories: Creative Process and Action Process. Nothing more. Each Process Block would fit into either of the two categories. Process Blocks are governed by the CREAM Framework.

Team Formation

It is essential to establish resource owners who would be taking responsibility for all actions of corporate. The resource owners who are classified for the purpose of governance standards are grouped as under:

(1) One Member from the Ethical Responsibility (ER) Group and (2) Four Members from the Fiscal Responsibility Group, consisting of (i) Operational Force, (ii) Managerial Force, (iii) Finance, HR, and other service providers, and (iv) Technology.

ER Force is shown separately, as Governance is for all and Ethical Responsibility is for all. Fiscal Responsibility aligns with Ethical Responsibility.

At a more matured state of Governance, there would be no need to have an ER Force, or for that matter, an Internal Audit Force, separately, as each Process Block is managed by four persons independently well trained in the art of converting their Fiscal and Ethical Assets into pure energy. Each performance is tracked and monitored by return on intangible. Self- Governance must be the ultimate goal of Corporate Ethics. Each task is owned by its team, is entrusted with targets of CAGR converted into CDGR, Daily growth rate. Also, CARR converted into CDRR Daily Reduction Rate, deconstructing what is valueless. Leadership is at the level of organizing the workforce that is entrusted with responsibility, both in the Creative and Action Processes.

The hierarchical one-man call center is no more.

There’s no VIP boss anymore, only a foot soldier. In a maintenance team, a cleaner is the foot soldier, in an airplane a pilot is the foot soldier, in a nuclear reactor a doctorate is the foot soldier, in a research lab an innovator is the foot soldier. A hierarchical one-man call center is the bane of corporate development. Risk appetite trickles down from the top. Risk culture travels up from the foot soldier. Remove the distinctions of money from the highest to the lowest paid and compare all as equal. Now, a lowly paid individual can challenge the highest paid on the use of the ethical assets of a company. All have the same cubic centimeter of brain tissue capability, which must be measured and enhanced. That’s the principle behind return on intangible. A foot soldier is the surgeon in the operating theatre, and all others readily give the worker what is needed to obtain the desired optimum results. While operating a machine or selling a product, the foot soldier cannot look around in search of a tool, essential for his or her task accomplishment. Remember the adage set by Robert Townsend in Up the Organization—“True leadership must be for the benefit of the followers, not the enrichment of the leaders. In combat, officers eat last.” The five members in a team during the Action Process are organized to provide that support. If a worker or a salesperson does get the optimum score of five, as well as each person at each step above, there ends the company’s woes. CEO rating is arrived at by accumulated ratings of each employee. That is to say, the CEO is concerned about the best ratings of each employee and works toward optimum performance. Intangible is the energy force, and as Polman says, “Leadership is not about giving energy, but unleashing others’ people energy”—that fits well with the return on intangible formula. In return on intangible the denominator is the energy force. The optimum score for each person is five. An index of inactivity for the company as a whole identifies a single task by a single person who has not achieved the optimum level of performance. It means the energy force is lacking, which causes the governance deficit, enabling the CEO to take corrective action instantly

Principle #5: Emergent Property Phenomenon

The three principles of emergent property according to Nobel laureate Murray Gellmann are as follows: (1) conformability of nature to herself, (2) applicability of simplicity, and (3) unreasonable effectiveness. By “Emergent Property” he means you don’t add something more to get something more. Rather, shed your inhibitions and focus on using your ethical assets. Emergent Property means it’s Corporate Yoga.

- Conformability of nature to herself: “For Nature is very consonant and conformable to herself,” says Isaac Newton.10,11 With Corporate Atomic Structure, the first principle “conformability of nature to herself” is met.

- Applicability of simplicity: It is ensured by limiting the entire management process to only two: the Creative Process and the Action Process. The second principle of Emergent Property, the applicability of the criterion of simplicity, is met. There are six stages of development and only two processes, the Creative Process and the Action Process. It’s simple enough for school children to learn governance by way of a game such as hopscotch.

Data explosion: Data retained in various forums, the OECD, The Global Competitiveness Report, Central Bureau of Statistics, GDP Growth comparison, World Bank, IMF, National Expenditure on XYZ, is all a nightmare for absorption and comparison. In this work, data is shrunk to the root level. Entire corporate performance by even a single task, by a single individual, can be exploded but yet does not exceed five, and is made meaningful. One is comparable with another. Corporate Atomic Structure is aligned with every other universal benchmark, with the same optimized results. Furthermore, the return on intangible can be calculated not just for one company but for the entire corporate by process area and by resource area, to produce a single result of 0 to 5, with the ready reckoner for Index of Inactivity for each person connected. - Unreasonable effectiveness: In return on intangible, covering the entire gamut of management with a single formula, the unreasonable effectiveness principle is met. Unreasonable effectiveness is the art of resolving a paradox with the least number of mathematical calculations. The simplest one is the Opposite Value Analysis, which can resolve any such mental aberrations. It is a truth serum. Return on intangible is a simple process once CAGR is brought to a CDGR level and allocation of duties to individuals part of a team of five is done. Daily performance with task accomplishments and deriving an Index of Inactivity converts the n-dimensional problems to n-problems of one dimension. That one dimension is the denominator, Intangible.

Consider the Organization as Human.

Six Limbs and Four Auxiliary Limbs of a Corporate Body

Let us attribute to a corporate body, a human form. After all, it is made up of people, not inanimate objects. Corporate Returns on Intangible Intellectual Value Capital, of Creative Process, and Action Value Capital, of Action Process, together make the Intangible Value Capital of a company. This is better understood in human terms rather than clinical inanimate ones. Today, an entity is considered an Object with no human involvement, and quantification loses the necessary insight into what human engagement brings to the table. Return on intangible statement of Active Index taken to Wall Street would reveal how vibrant an organization made and run by people actually is.

Six Limbs of the Corporate Body:

- Nose is the intangible. It converts mass into pure energy.

- Mouth is the grammar of the Corporate Atomic Structure.

- Feet are the measurement through Powerful Metrics.

- Ear is the dictionary of the learning management system (LMS).

- Eye is the Long-Range Planning and Short-Range Action—CAGR brought to CDGR—Compound Daily Growth Rate, CARR converted into CDRR Daily Reduction Rate.

- Hand is the work.

Four Auxiliary Limbs of the Corporate Body:

- Explication of corporate laws and management quality

- Science of reasoning—sustainability of efficiency

- Strategies—sustainability of profits

- Ethical responsibility—sustainability of value system

With six limbs and four auxiliary limbs, the corporate body in human form may call for attention from a medical team to attend and optimize energy force in respective limbs for an overall health check, limb by limb.

I IBCM—The Five Principles

- Principle #1: What gets measured, gets managed

- Principle #2: Measure qualitative elements of management

- Principle #3: Corporate atomic structure

- Principle #4: Return on intangible

- Principle #5: Emergent property phenomenon

II Corporate in Human Form

- Six limbs of the corporate body

- Four auxiliary limbs of the corporate body

Notes

1. J.R. Iyer. Inactivity Based Cost Management—Copyright REGN. NO. L-27490/2006 dated December 1, 2006 Govt. of India, Copyrights Office.

2. R. Halloran. 1976. “Japanese Raid Lockheed And Others in Bribe Case.” https://www.nytimes.com/1976/02/24/archives/japanese-raid-lockheed-and-others-in-bribe-case-japanese-raid-in.html

3. The Big Payoff: TIME: Monday, February 23, 1976.

4. Lockheed’s Defiance: A Right to Bribe? TIME: Monday, August 18, 1975.

5. Reserve Bank of Australia. 1995. “Implications of the Barings Collapse for Bank Supervisors.”

6. United States Government Accountability Office. 2007. “By the Comptroller General of the United States,” Government Auditing Standards. January 2007 Revision.

7. Ibid., 1.28.

8. KPMG International. “Corporate Sustainability A Progress Report,” kpmg.com. https://www.sustainabilityexchange.ac.uk/files/corporate-sustainability-a-progress-report_1.pdf.

9. D. Eagleman. 2013. “ Brain over Mind?” https://www.youtube.com/watch?v=UWBtT-Gl4vQ.

10. Quote from TED talk by M. Gell-Mann. 2007. “ Beauty, Truth…. and Physics?” https://www.ted.com/talks/murray_gell_mann_beauty_truth_and_physics#t-872257.

11. Also quote from https://libquotes.com/isaac-newton/quote/lbf0m1n.

12. Scientific research on the coronavirus is being released in a torrent: https://www.economist.com/science-and-technology/2020/05/06/scientific-research-on-the-coronavirus-is-being-released-in-a-torrent

*Inactivity Based Cost Management