CHAPTER 13

BLOCKCHAIN TECHNOLOGY: A PARADIGM SHIFT IN INVESTMENT BANKING

R. Vedapradha,1,∗ Hariharan Ravi,1,∗ Arockia Rajasekar2

1 Department of Commerce and Management, St. Joseph’s College of Commerce (Autonomous), Bangalore, Karnataka, India

2 Department of Commerce, St. Joseph’s College (Autonomous), Trichy, India

Abstract

Purpose: Blockchain technology can have ramifications across the investment banking ecosystem due to their cryptographic distributed ledger. The aim of this chapter is to evaluate the adaptation feasibility and predict its performance for a regulatory framework when Blockchain technology is applied by investment banks.Design/Methodology/Approach: Random sampling is used with a sample size of 50 respondents from investment banks operating in urban Bangalore based on the primary data collected. Statutory impact (SI), compliance policy (CP), fiscal policy (FP), competitive edge (CE), and service-level agreement (SLA) are the variables. SPSS and SPSS AMOS are the statistical software used to test the structural equation model (SEM) with confirmatory factor analysis (CFA), multiple linear regression analysis and one-way ANOVA (analysis of variance).

Findings: The model fits perfectly based values to fit indices. SI is the most influencing variable and has a greater impact on acceptability with beta value 0.899 at 0.001 percent significant level with Chi-square value being 3.14 and the estimated reliability post-adoption is 81 percent. SI, CP, SLA, and CE are the significant predictors of performance with a greater association between the performance of the banks and regulatory framework indicators with significance at 0.01 percent level.

Originality/Value: The technology can reduce the operating cost from the middle and backend, improves transparency, and prevents money laundering, as it is tamper-proof and accessed by all the parties at the same time.

Keywords: Service-level agreement (SLA), anti-money laundering (AML), investment banking cycle, competitive edge

13.1 Introduction

Blockchain technology facilitates investment banks to create a cryptographic distributed ledger amongst the various parties involved in investment banking to validate the transactions. The transactions consist of the data, which is very prevalent and constantly creates more efficient information transactions, enhances regulatory controls, and improves reliability by eliminating the intermediaries. It can be applied in KYC (Know Your Customers) of clients, AML of data sharing, collateral management, trading and settlements of trades, and clearing through a transaction cloud.

Blockchain technology can help banks reduce their infrastructure cost as a network of computers maintains the transactions on the internet platform without any approval from the central authority. It also helps in reducing the operational cost based on their back-office processes such as clearing, trade support, compliance and settlement of securities, as it can remove the reconciliation since the transactions are distributed and virtually tamper proof.

Banking costs can be reduced with integrated database management by the investment banks as they invest a tremendous amount of money in the maintenance of databases. Databases are created to store, validate, and transform information regarding clients, financial transactions, and documents. Blockchain technology plays a pivotal role in rendering quality service with more transparency and efficiency by offering a centralized platform to the database, permitting access to data between the counterparties along with a highly secured access system [1].

13.1.1 Evolution of Technology

The concept of the technology has created an edge for the various industries to improve efficiency, productivity and channelize a game plan to sustain in the long run. Wei Dai is the eminent researcher who launched the digital money concept through Bitcoin, which focused on offering solutions to various issues on a technological platform that can also generate money based on decentralized consensus. Satoshi Nakamoto created a revolution in the digital world by familiarizing the world with Blockchain technology in 2008 in the form of cryptocurrency, where it is a peer-to-peer electronic cash system. It was developed to design a decentralized ledger that works on trustable sources of networks which are not controlled by individuals. The preferred languages to be used for this technology are C++, Java, Python, Solidity, and Ruby. Initially, the concept of Bitcoin was only in the news but it began to transform due to the enormous opportunities it offered and it started creating a buzz post-2014, finally gaining importance post-2017 [2].

13.1.2 Scope of Applications

The application of this transforming technology is suitable for all possible industries and can be customized based on their requirements. The infrastructure creates a database through which data can be shared, stored, and transferred through a mechanism, as it has various levels of permissions. These tasks performed by the users can only be accessed to read and execute, but some can just read the transactions, promoting security and privacy.

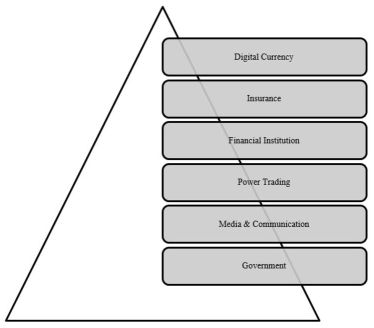

Some of the areas of its magical applications which are creating a greater impact are discussed below. In addition to financial institutions, it is applicable in many more industries as well. Here, a few of the applications are discussed in detail based on Figure 13.1.

Figure 13.1 Applications of blockchain technology.

- Digital Currency: Bitcoin was limited in its usage due to the failures in the regulatory framework. However, the advanced technology creates room for the next level where the reliability of the digital identity has been approved, applied and tested for knowing the customers based on online authentication standards across the service industries.

- Financial Institutions: Banks and other financial institutions are highly prone to money laundering, identity theft, digital transfer of funds and many more attacks that can hamper customer relationships and affect the services rendered. Now, financial institutions are being transformed by a robust technology, enabling them to reduce costs, increase efficiency, and provide more secure transactions.

- Insurance: Insurance protection against uncertain damages can put a business in trouble by collapsing in a second if there is no coverage for the same. The insurance companies are vulnerable to illegal claims and manipulation of data. Hence, blockchain technology can be a boon to them as it facilitates in the streamlining of the documentation process and the payments of premiums and claims, due to complete digital transformation which reliably handles data in the form of documents.

- Government Bodies: There are often setbacks in government systems due to corruption and nonproductive operations as a result of various political and economic factors. In order to render better civil services to civilians, blockchain technology can be used to create a transparent platform connecting the governing authorities with the general public through the digital world, thereby processing transactions which promote the conversion of ineffective services into effective public service delivery along with the promise of optimum utilization of resources.

- Media and Communications: Internet of things (IoT) has opened the gates to countless users easily accessing the information from the internet platform, which calls for protection of the different parties involved in the development of the arts and mass media, like research authors, actors, musicians, singers, and theater artists whose work and contributions are pirated without permission or acknowledgment. Blockchain technology can solve this problem of access and use by bringing all the parties in direct contact with consumers.

- Power Trading: Various commodities are traded across the exchanges by industries, from products to asset classes, involving cash transactions and digital documents during the process of transfer of ownership to ensure transparency. Blockchain technology is applied to the settlement process for trading and transferring resources flawlessly.

13.1.3 Merits of Blockchain Technology in Banks

Blockchain is one the most robust disruptive technologies that can facilitate in revamping the entire business of the banks. Figure 13.2 shows some of the merits of adopting this technology.

Figure 13.2 Blockchain technology for better customer experience.

Blockchain technology can help to increase transparency and effectiveness at a larger scale due to the following attributes:

- Robustness: It can improve the quality of transactions with strong reliability due to the distributed ledger based on cloud transactions.

- Regulatory Framework: It enables creating better transparency and security with “know-your-customer” documentation which prevents money laundering activities.

- Cost Reduction: It can reduce cost by utilization of resources and streamlining few operational processes in the areas of middle-office and back-office segments.

- Automation: The added advantage of blockchain technology is that it has better implications for creating innovative and customized products and services for better customer relationship management.

- Secured and Shared Transactions: The transactions are based on the validation from all the parties involved and are tamper-proof unless approved by all. It ensures better data security due to cloud computing [3].

13.1.4 Investment Banks

Specialized banks often focus on the operations of offering asset management, wealth management, advisory services, and consultancy service to various clients ranging from financial institutions through central banks to manage their portfolios under three segments, namely front-end, middle and back-end operations. It is one of the most critical divisions in banking apart from commercial and retail because they promote capital formation, generate foreign exchanges, facilitate foreign direct investments, and create employment opportunities. Some of the key players of this division are financial institutions, financial markets, authorized brokers, clearing houses, and legal agencies. They are investing a lot of money on the middle and back-end operations by setting up a captive firm across emerging countries to obtain a cost advantage and time lag. Some of the leading banks, like Morgan Stanley,1 Goldman Sachs,2 Northern Trust,3 State Street,4 and Wells Fargo,5 have their headquarters based in the U.S., U.K., and various other European countries [4].

13.1.5 Theoretical Framework

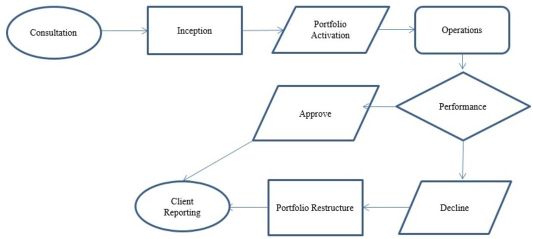

Investment banks play a pivotal role in capital formation, generating foreign direct investments, and promoting foreign exchange reserves of a nation. They have proved to be a ray of hope in the development of emerging countries moving in the direction of growth and development. An investment bank has various operational services offered at different levels to multiple clients, which are front-end, middle, and back-end operations. The theoretical framework of an investment bank is shown in Figure 13.3.

Figure 13.3 Theoretical framework of investment banks.

- Consultation: The clients are mostly financial institutions, central banks, and high-net-worth individuals who approach these banks to avail the asset management services. Some clients seek the guidance of only consultation services. Most of them look forward to investments at this stage. They often come in direct contact with the front-end desk through productive interaction.

- Inception: The marketing consultants create an avenue to the clients who are interested in the investments. The concerned staff assists the clients in going through the initial document verification before proceeding. There is effective integration of different departments responsible for the initialization, who are involved during the decision-making process to validate and evaluate the activation. The client will confirm the percentage of the portfolio comprised of different proportions of asset classes to be invested.

- Portfolio Activation: The portfolio manager designs a customized portfolio for the clients based on their requirements with suitable currency, quantum of the amount, base currency, and local currency. All departments will be informed to ensure preparations are made before the fund gets traded in the financial markets.

- Operations: It consists of reconciliation of the portfolio, preparation of accounting statements, calculation of net asset value (NAV), making accounting adjustments in the accounting systems for the authentic proof of the record kept between the custodian and the IBs.

- Performance: The performance of the portfolio is calculated in comparison with the benchmark or index, like S&P and NIFTY 50, to examine the portfolio floated by the IBs across the asset class. There are two major types of strategies, namely Active strategy and Passive strategy. An active strategy is adopted when the portfolio floated by the IB is expected to outperform or reflect results above the level of the benchmark of the market portfolio. A passive strategy focuses on balancing the portfolio drafted by the investment bank only to mimic the market index.

- Approve/Decline: When the portfolio performance matches the expected market index’s performance, the portfolio manager approves the results for further reporting. In the case of the reverse situation, then the manager declines the reporting immediately.

- Portfolio Restructures: The portfolio manager rearranges the combination of different asset classes in the current portfolio structure when the expected performance of the fund is less than (in case of active strategy) and above (in case of passive strategy) the performance of the market index.

- Client Reporting: The final report is generated and formatted as per the requirements of the clients based on SLA, like weekly, quarterly, monthly, semi-annually or annually, and dispatched to the clients, which gives them a summarized view of their investments, fund allocation, portfolio combination, and revenue generation [5].

13.1.6 Investment Banking Operational Levels

The banks are broadly divided into various operational levels, namely front-end, middle and back-end operations, based on the nature of service rendered. These levels are interconnected, where the output of the first level becomes the input of next level.

13.1.6.1 Front-End Operations

This level is confined to direct interaction between the authorized personnel of banks with clients who seek advice and guidance for their investments. They approach the new business team who are involved in the promotion of the customized products and services offered by the banks. Professional staff briefs the various clients about the products and services. Once after the client’s confirmation, they proceed towards verification of their KYC documents to process further. The papers are either approved or rejected based on their reliability and authenticity status. The last step is to incept the portfolio once the reports are legally authorized.

Figure 13.4 reflects the flow of the operations at the front-end desk.

Figure 13.4 Process in front-end operations.

13.1.6.2 Middle Operations

The inception portfolio designed as per the requirements of the clients is further processed by the portfolio administration department, who are responsible for activation of the fund, trading to integrate with trade and shareholder service departments. Figure 13.5 shows the trade department intimates the custodian and brokerage firms for all the trades booked (buy & sell) so that the custodian keeps the physical stock and cash ready during the settlements. Brokerage firms are responsible for executing the trades as an authorized agent who charges a specific fee for the service rendered.

The risk management department always thrives on monitoring the risk associated with the transactions arising across the portfolios to protect the banks from going bankrupt, portfolios getting overdrawn, idle cash and many more measures. The department plays a significant role in promoting the smooth functioning of the activities. The shareholder’s service department is responsible for record keeping of the cash contributions and withdrawals made by the clients from their portfolio. The clients will contribute a specific quantum of cash for a portfolio traded live in the financial market for the first time. This amount is based on the currency of the client’s domicile country towards the fund activation. These activities are of a different nature involving multiple services rendered by the banks to their clients playing a significant role in the business. However, it also is very challenging and risky if there is any negligence by the analysts or risk management team. Examples of risky situations could be idle cash in the portfolio contributed by the client without being invested or overtrading, or evaluating the cash balances available in the portfolio at the closure of the markets. A large risky transaction consists of a large quantum of the amount with globally accepted currencies like US Dollar, Euro, British Pound, Japanese Yen still not settled at the clearing houses, a failed trade due to insufficient funds at the third party and many more.

Figure 13.5 Process in middle operations.

13.1.6.3 Back-End Operations

Figure 13.6 reflects the flow of back-end operations, which is one of the most important and robust levels of services where the banks can generate efficiency and transparency that leads to approved client reporting. Once the portfolio is activated, there must be a reconciliation performed within the portfolio at different currency and security levels to check the accuracy of transactions and books of accounts maintained between custodian and IBs. NAV reconciliation follows after the portfolio reconciliation on the reconciliation tool in accounting systems.

Banks maintain their accounting systems based on the contractual whereas the custodian reflects the transaction based on actual settlements. Hence, there will always be the difference in settlement of transactions between custodian and banks due to reasons like failed trades, delay at a third party, and time lag. Portfolio reconciliation is concerned with operations related to cash and stock. NAV reconciliation is confined to computing the total NAV of the portfolio based on each security level, currency level, trades, and income separately between custodian records and IB’s records. The portfolio administration department confirms the NAV after closing the books of the accounts on the last working day of every month. Performance of the fund will be computed to verify the results have matched, outperformed or underperformed the market index. The portfolio manager adjusts the composition of the securities in the fund to match the requirements of the clients. Client reporting is the last phase of the operation where the summary of the investments and the performance of the portfolio created for the clients will be dispatched to them to meet the requirements of the SLA [6].

Figure 13.6 Process in back-end operations.

13.1.7 Conceptual Framework

Blockchain technology can transform the business process with a strategic, operational model finely tuned within the regulatory framework. It has the potential to replace the current infrastructure by adopting the distributed ledger process focused on improving the operational process either in the short-term or long-term goals. A dedicated team must be approved to learn the new technologies, explore their potential and evaluate the positive results upon implementation. The banks must prioritize their immediate pain points by studying the feasibility and preparedness of transforming processes that can create an edge. A blueprint must be developed and simulated in measuring the possible success or failures to ensure the maximum scalability and reduce the disruptions towards clients, operations and players of the market. Most of the banks are spending an exorbitant amount on the activities in the areas of middle and back-end operations to take advantage of the resources, cost element, and availability of labor that is also forcing them to set up subsidiary units or captive firms in the developing nation. This technology is still at the acceptance stage since there is anonymity at the other end when there are smart contracts entered between the parties traded on the financial markets, and identification becomes very challenging. Hence, the scope of its application must be validated before implementation and looking forward towards the execution.

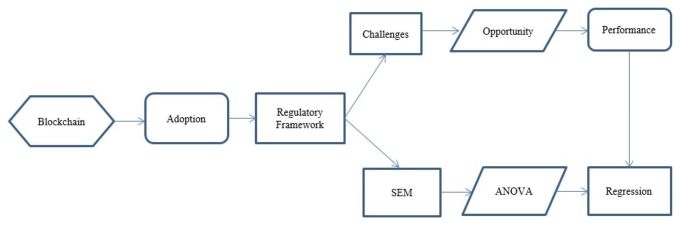

Figure 13.7 describes the conceptual framework of an investment bank. Some software companies are working towards developing a foolproof mechanism to overcome the barrier of identity [7].

The flowchart in Figure 13.7 reflects the conceptual framework of the application when adopted; it has higher acceptability through its implications on curbing the client-related process, money laundering, compliance, and legal practices, which are prone to various challenges. The drawbacks can be changed into opportunities if the investment banks chalk up their ground-level research to addressing the obstacles, and will definitely face difficulties in the short run but can surely prove to be effective. Hence, this study attempts to test the model of adaptability through the structural equation model, verifying the results through one-way ANOVA and Multiple Linear Regression models towards the overall performance of the banks’ post-implementation [7].

Figure 13.7 Flowchart representation of a conceptual framework.

13.1.8 Challenges

Every opportunity creates room for challenges to be faced and addressed, prompting the achievement of goals. Adoption of Blockchain technology consists of a few problems that have to be analyzed before implementation. Some of them are as follows:

- Standards: The route of software calls for identification of rules as authorized operating technology within the framework by combining the authority and responsibility.

- Governance Models: There must be a well-structured model developed and tested before the actual implementation of the technology to validate the challenges and consequences to ensure the suitability and scalability.

- Transfer of Assets: The logical transactions of the assets in the market when there are dual flows off and on between the parties, the management of which must be answered and decided.

- Regulators: There must be a balanced plan designed to ensure both privacy and transparency among the transactions of the players.

- Acceptance: Most of the employees do not accept the changes due to structural changes, technological changes and their efforts towards the training and development. There may be a few employees who always are reluctant to take the changes. The banks must address these issues.

- Positioning: Identification of the perfect time and process which is most suitable for the technological implementation must be forecasted and tested, and only then must be adopted, which requires time, cost and energy.

- Location: The area of improvement that facilitates a process, resulting in cost-effectiveness and optimization of resources, must be analyzed and placed in the right process by a suitable strategy.

- Digital Talent: Hunting down suitable talented employees for investment banks is very challenging as they are expected to be acquainted with both technology and investment banking concepts.

- Client Experience: The clients may have mixed reactions towards the acceptance of this technology as they might not be aware of it and might feel it is redundant when compared to an earlier technology or process, and it is an arduous task for banks to convince their clients to have confidence in the technology.

- Cloud Concept: The banks must be willing to move towards the cloud concept where all the transactions are secure and transparent, which means no hidden cost can be applied to the client’s service charges.

- Research: Research and development is the lifeblood of any business, and investment banks are always striving to create new products and services to gain an edge on the competition. It involves cost, time and resources [8].

13.2 Literature Review

Researchers have attempted to explore whether the impact of implementing integrated cloud and blockchain platforms will deliver better solutions to citizens by establishing a smart collaboration between them and their local government by offering a secure communication platform in a smart city [9]. The application of innovative technologies in the Internet of Things offers services which have been tested for their performance using cloud technology to enhance storage capacity, payment systems and ensure that transactions are tamper-proof [10]. Data can be stored and secured through networked cloud-based systems to ensure the validation of transactions. The computer networks operate with innovative infrastructures for companies and individuals to handle and manage their data. Data plays a pivotal role in cloud computing and promotes safety with a combination of hardware and software to better safeguard records, especially in commercial and military groups. A study by Liang et al. showed that a blockchain-based data provenance architecture in cloud environment ensured data operations and enhanced the security and privacy of users [11]. It enables dealing with smart contracts, offering better security and transparency with the third party during the transactions, promoting lower cost of operations, and better cybersecurity, especially when applied in industrial sectors with scalability and improved efficiency [12]. A disruptive technology has been proposed which is capable of revolutionizing the transportation industry with road network planning and facilitating drivers by offering security measures and comfortable driving based on the network models used to build an intelligent, secure and self-determining transport system for optimum utilization of resources. The authors have proposed that the vehicle network architecture operate in a smart city [13].

Tosh et al. have stated that there are practical concerns during the adaptation process of the technology based on the cloud concept and its performance handling the security concerns within the structured framework. The technology assures that data is secure and private through the cloud platform that enhances the performance [14]. A study be Stanciu attempted to evaluate distributed and hierarchical control systems based on smart contracts at the monitoring level, integrating the edge nodes at a micro-level in service architectures [15]. E-government is the emerging concept adopted to ensure decentralized and standardized models to facilitate in addressing the nation’s issues based on the cloud infrastructure in combination implementation which promotes effective and optimal resource management that focuses on analyzing the national data centers [16]. The introduction of an intelligent vehicle trust point mechanism applied in communication focuses on improving credibility, reliability and data accuracy. It has resulted in a better legal consensus due to the reward-based system in the communications [17].

Singh and Lee propose that emerging innovative technologies can be applied in meeting the standards of service-level agreement in business which ensures data accuracy, security and better improves the quality of standards. The comparative study has offered a solution to security concerns through a trusted third party [18]. Risk management, money laundering, and many other problems are addressed with the integration of active and eminent systems for improving authentication, validation and security across the financial institutions [19]. Kocsis et al. highlight the implementation of the technology applied to various complex systems to evaluate the performance outcome, attempting to venture into the novelty of hyperledger fabric services [20]. Experiments were conducted to confirm the secured and shared transactions that can also facilitate useful trades by various players in the market based on the Paillier cryptosystem to assure the confidentiality of data sharing [21]. Smart contracts have proven to be very influential in decentralized sharing of information among the various parties involved in trading, securing the information in consensus with application of this innovative technology which enables sustainable financial markets covering the vast area of economic performance retaining the quality of the data [22]. Biais et al. tested the application of technology in the form of a protocol game to evaluate the strategies of rational and strategic miners in the chain, ensuring the retention of foundational technological concepts resulting in orphaned and persistent divergence chains with excessive calculation ability [23]. Data can be stored and secured through networked cloud-based systems to ensure the validation of transactions. The computer networks operate with innovative infrastructures for companies and individuals to handle and manage their data [24-28].

13.3 Statement of the Problem

Investment banks are vulnerable to theft of critical data related to clients, money laundering, settlements and clearance of the securities, which plays a crucial role in the risk management and auditing that creates a benchmark in the industry. The regulations are stringent to arbitrate and mitigate frauds and risk of a trade or when a counterparty fails. Banks must adhere by law to perform KYC before bringing the clients on board. Hence, adopting the proposed technology can curb many regulatory-related obstacles and improve the performance of the investment banks, promoting better customer relationship management. It also ensures a reduction in operating cost and resources with maximum productivity.

13.3.1 Objectives

The study focuses on the below objectives:

- Evaluation of adaptability of Blockchain technology on a regulatory framework by investment banks.

- Assessment of performance by investment banks with the implementation of Blockchain technology.

13.3.2 Hypothesis

- H0: There is no association between the adaptation and regulatory framework by investment banks.

- H0: There is no significant impact of adoption on performance in investment banks.

13.3.3 Sampling

Random sampling technique has been implemented to obtain the sample size of 50 respondents based on the probability.

13.3.4 Data Collection and Source

The research is exploratory and based on the primary data obtained through a standard questionnaire. The respondents are the employees of various foreign investment banks operating in urban Bangalore.

13.3.5 Variables and Statistical Tools Used

Statutory impact, compliance policy, fiscal policy, auditing, and service-level agreement are the variables. Statistical package for social science (SPSS) and SPSS AMOS (analysis of moment structures) are the statistical software applied for the study. Structural equation model (SEM) with confirmatory factor analysis (CFA), multiple linear regression analysis and one-way ANOVA (analysis of variance) are the statistical tests performed.

13.3.6 Limitations

The research is limited within the geographical location of urban Bangalore based on the foreign investment banks. There is the further scope of venturing into comparative study pre- and post-implementation of artificial intelligence, machine learning and cloud computing technology enabled techniques of operations in back office and middle office.

13.4 Results

Structural equation modeling (SEM) is one of the multivariate analysis techniques applied to evaluate the structural relationship between the dependent and the independent variables. The model designed is based on the conceptual framework to test the adaptability of the Blockchain technology within their regulatory framework.

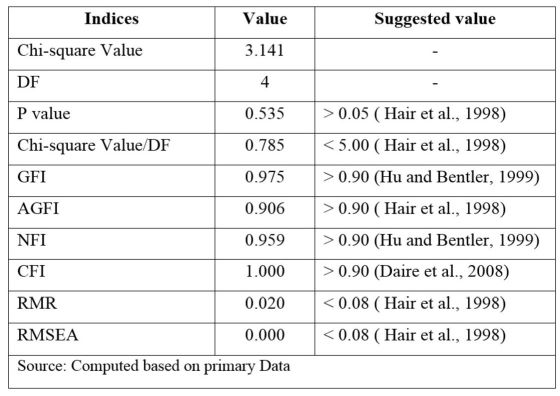

Table 13.1 reveals the components of a model fit based on the adaptability in the investment banks. Since all the parameters of model fit reflect the value within the threshold values, it is a perfect model to evaluate the adaptability of innovative technology. SEM model reflects the calculated value of P is 0.535 (> 0.05), reflecting the model fits perfectly. The Goodness of Fit Index (GFI) value is 0.975 and Adjusted Goodness of Fit Index (AGFI) is 0.906, confirming a good fit. The computed Normed Fit Index (NFI) value is 0.959, and the Comparative Fit Index (CFI) value is 1.000. It also shows that the Root Mean Square Residual (RMR) value is 0.020 and Root Mean Square Error of Approximation (RMSEA) value is 0.000.

Table 13.1 Model fit summary of the structural equation model of adaptability of blockchain technology in investment banks.

Figure 13.8 shows the SEM model applied for the testing of the goodness of fit in the adaptability in their regulatory framework to create more transparency in the business transactions. This model consists of 5 observed variables, namely RF1 (Statutory impact), RF2 (Compliance policy), RF3 (Competitive edge), RF4 (Fiscal policy) and RF5 (Service-Level Agreement) measuring the construct variable regulatory framework. The measurement error represents other variations for a particular observed variable and their estimation. A factor loading represents the relationship between the factor and its indicator. e1 (Legality), e2 (Ownership), e3 (Cost), e4 (Access), and e5 (Clients) represent that those factors having an impact are treated as error terms by running the model.

Figure 13.8 Path diagramwith standardized estimates displayed based on the regulatory framework in investment banks.

A variance in Statutory Impact of 81 percent is accounted for by the Regulatory framework; the rest of the difference of 19 percent is due to the unique factor legality (e1). Hence, 0.81 is the estimated SI reliability of the banks adopting the technology. A variance of 40 percent in Compliance policy is accounted for by the Regulatory framework; the deviation of 60 percent is due to the unique factor ownership (e2). Hence, 0.40 is the estimated reliability of CP if the banks adopt the technology. A variance of 63 percent in Competitive edge accounts for the Regulatory framework, the balance of the variation 37 percent is due to the unique factor cost (e3). Hence, 0.60 is the estimated reliability of CE if the banks adopt the technology. A variance of 74 percent in Fiscal policy is accounted for by the Regulatory framework; the remaining variance of 26 percent is due to the unique factor access (e4). Hence, 0.74 is the estimated reliability of FP if the banks adopt the technology. A variance of 10 percent in Competitive edge is accounted for by the Regulatory framework; the other variance of 90 percent is due to the unique factor clients (e5). Hence, 0.10 is the estimated reliability of SLA if the banks adopt the technology.

Adaptability defining factors statutory impact (81%), fiscal policy (74%), competitive edge (63%) and compliance policy (40%) reflect successful and higher levels of acceptance when the investment banks implement Blockchain technology. However, the factor client-based reliability towards acceptance and adaption by these banks is just 10%. Hence, it can be concluded that the overall adaptability is 65%, offering a platform that is reliable and secure networks to ensure better customer relationships and transparency.

The results in Table 13.2 show that unstandardized coefficients (B) based on RF1 is 1.000, RF2 is 0.948, RF3 is 0.878, RF4 is 1.112, and RF5 is 0.104. The p values of RF1, RF2, RF3, and RF5 are significant at 0.001 percent level and have a positive impact on the adaptability of the technology. However, RF2 shows a negative impact as the banks are expected to permit access to their customers, creating ownership to view their financial data which can be shared by them across banks and financial institutions to avail better services and deals. As per the standardized coefficient (Beta) values from Table 13.2 below, statutory impact has the maximum effect with 0.899, which is the most influencing factor in the model, followed by fiscal policy (0.737), competitive edge (0.633), SLA (0.104), and least influencing factor is compliance policy (-0.632).

Table 13.2 Confirmatory factor analysis of the impact of the adoption of technology on the performance based on the SEM model.

RF3 predicts 87.8 percent, RF4 predicts 112 percent, and RF5 predicts 10.4 percent, and RF2 diverges from the impact prediction because of the compliance policy which discloses the trades performed by the employees in the banks. RF1 predicts 100 percent success post-adaptation.

RFW reflects the regulatory framework which is considered as the latent construct variable on the acceptance of the technology.

ANOVA is a statistical tool applied to estimate the difference of variances among the group means of the variables selected for the study based on the sample size. The results from Table 13.3 show that there is a more significant association between the performance of the investment banks and regulatory framework, indicating variables when Blockchain technology is adopted, which are significant at 0.01 level in regard to RF1, RF3, RF4, and RF5.

Table 13.3 Regulatory framework and performance on the adaptability of the blockchain.

One-way ANOVA was executed to compare the ramification of regulatory variables with the performance of the investment banks. The outcome reflects that there is significant effect of the mentioned technology, RF1 (F =4.337, p = 0.000), RF3 (F = 3.633, p = 0.001), RF4 (F = 2.074, p = 0.036), RF5 (F = 3.479, p = 0.001). However, RF2 is not significant as the p value is 0.335, and the F value is 1.178. Hence, there is a higher level of association between the regulatory variables based on technology and the performance of the banks.

A linear regression model is used to predict the dependent variables based on the independent variables to evaluate and predict the linear relationship existing between the variables chosen for the study.

Table 13.4 shows the model fit summary details of the multiple linear regression model evaluated for testing the impact of performance on the banks when innovative technology of Blockchain is adopted. Hence, 77 percent of the prediction of the dependent variable can be successful based on the known independent variables.

Table 13.4 Model fit summary of the multiple linear regression model.

Table 13.5 reflects the performance predictors in the regression model adopted to test the performance of these investment banks based on the independent variables, namely statutory impact, compliance policy, competitive edge, fiscal policy, and service-level agreement. The dependent variable is the performance of the bank.

Table 13.5 The performance predictors in the regression model.

Performance is the dependent variable while the independent variables of the regulatory framework are X1, X2, X3, X4, and X5. The prediction was based on the model of regression developed using “Enter” method as per Table 13.5. A multiple linear regression equation was applied to forecast the performance of the banks based on technology-enabled indicating variables. The following is the equation:

Where,

- Y = Dependent variable, X1, X2, X3, X4 and X5 are independent variables.

- X1 = Statutory impact

- X2 = Compliance policy

- X3 = Competitive edge

- X4 = Fiscal policy

- X5 = Service-level agreement

Y reflects the performance of the investment banks and 16.790 is the constant value. A significant regression equation was (F (5, 44) = 13.027, (p < .000), with an R2 of 0.597. Hence, the forecasted performance is equal to 16.790 + 5.594 (Statutory impact) + 4.311 (Compliance policy) + 1.631 (Competitive edge) −0.463 (Fiscal policy) + 3.908 (Service-level agreement).

The performance of the banks increases for every 5.594 strategies of legal decisions, 4.311 compliance strategies, 1.631 competitive advancements, and 3.908 percent of quality reporting as per service-level agreement. However, the quality of decisions based on the fiscal policy is reduced by 0.463 for every decision. The error terms are implementation cost, the reluctance of employees, and resources involved in training the employees to adopt this technology. Hence, statutory impact, compliance policy, service-level agreement, and competitive edge are significant predictors of the bank’s performance having a positive impact due to the adoption of a crypto ledger. However, fiscal policy is not a significant predictor as the value of p is 0.612. The impact of execution for the regulatory network has a significant impact on the output performance as the value of R is 0.773.

13.5 Discussion of Findings

The statutory impact has been by the error term e1 based on the scope for legal identification amongst the counterparties involved in the Blockchain; computer codes generated in the form of smart contracts for the financial assets question its application, raising concerns about the legal entity. Compliance policy influences the error term e2 which calls for giving ownership to the customers, providing access to their financial data and allowing it to be shared across financial institutions; there are concerns regarding the ownership of non-cryptocurrency-based financial assets being transferred on this platform with certainty.

Banks can create a competitive edge with the adoption of this technology, which can reduce their operating cost by almost 50 percent, but the cost of implementation (e3) influences the outcome. The cost of training human resource to adapt to the existing systems and implementation cost is expensive. It also depends upon banks being able to afford to invest such a considerable amount in revamping their business. They must consider the cash inflows that pay back their investment.

The fiscal policy of investment banks is focused on generating cash flows through various services rendered to different groups of clients and also consists of their investments for the capital requirements. The artificial intelligence-enabled technology promotes trade settlements; transparent contracts compute the gains or losses, adjusting the collaterals accordingly and increasing transparency. The error term (e4) influences the adjustability as there are questions related to access and control of the technology based on the ledger versions being kept open or controlled.

SLA is a legal contractual agreement between the service provider and the clients defining the level of service expected, reporting, monitoring, consequences on failing to meet the standards, reliability, service standards, quality, availability, and responsibilities within a specified timeframe. It is affected by the error term (e5), which can be due to issues like client privacy and security, process speed on scalability, and cyber risks involved when the Blockchain technology is adapted. The impact of technology enabled with Blockchain in the regulatory network has a significant impact on the output performance as the value of R is 0.773. The ANOVA test has proved that there is a more significant association between the adaptability and the performance. Regression analysis has confirmed that statutory impact, compliance policy, service-level agreement, and competitive edge are indeed significant predictors of the bank’s performance. The SEM model has fitted perfectly within the regulatory framework of the banks. All the parametric tests performed have proved positively that the adaptation of the technology is very impressive and brings a tremendous change in the operations of the investment banks.

13.6 Conclusion

Blockchain is a promising technology for reducing the cost of operations, infrastructure, and human capital in the service industry. It has an enormous implication on the compatibility of infrastructure, expertise skill sets, computing power, and datacenter management. Hence, this chapter has shown that the investment banks can adopt this technology in their regulatory framework because data sharing, secured transactions, and contracts for tamper-proof digital agreements which promote authenticity. Blockchain improves with time based on the scalability of the technology.

REFERENCES

- 1. Are you exploring the Blockchain technology for your investment bank? (2019). Retrieved from https://www.accenture.com/in-en/insight-perspectives-capital-markets-blockchain.

- 2. Narayanan, V. (2018). A brief history in the evolution of Blockchain technology platforms. Retrieved from https://hackernoon.com/a-brief-history-in-the-evolution-of-blockchain-technology-platforms-1bb2bad8960a.

- 3. Accenture Consulting Report. (2017). Top 10 challenges for Investment banks. (Accessed on 4th February 2019). https://www.accenture.com/t20180418T063906Z_w_/us-en/_acnmedia/Accenture/Designlogic/16-3360/documents/Accenture-2017-Top-10-Challenges-10-Distributed-Ledgers-Blockchain.pdf.

- 4. Vedapradha, R., et al. (2016). Investment banking - A panacea for economic development in banking sector. International Journal of Business Quantitative Economics and Applied Management Research, 3(4), 46-48.

- 5. Guo, Y., & Liang, C. (2016). Blockchain application and outlook in the banking industry. Financial Innovation, 2(1), 24.

- 6. Vedapradha, R., & Ravi, H. (2018). Application of artificial intelligence in investment banks. Review of Economic and Business Studies, 11(2), 131-136.

- 7. Nead, N. (June). The Impact of Blockchain on Investment Banking. Retrieved from https://investmentbank.com/blockchain/.

- 8. Shrivastava, G., Kumar, P., Gupta, B. B., Bala, S., & Dey, N. (Eds.). (2018). Handbook of Research on Network Forensics and Analysis Techniques. IGI Global.

- 9. Biswas, K., & Muthukkumarasamy, V. (2016, December). Securing smart cities using blockchain technology. In High-Performance Computing and Communications; IEEE 14th International Conference on Smart City; IEEE 2nd International Conference on Data Science and Systems (HPCC/SmartCity/DSS), 2016 IEEE 18th International Conference (pp. 1392-1393). IEEE.

- 10. Samaniego, M., & Deters, R. (2016, December). Blockchain as a service for IoT. In Internet of Things (iThings) and IEEE Green Computing and Communications (GreenCom) and IEEE Cyber, Physical and Social Computing (CPSCom) and IEEE Smart Data (SmartData), 2016 IEEE International Conference (pp. 433-436). IEEE.

- 11. Liang, X., Shetty, S., Tosh, D., Kamhoua, C., Kwiat, K., & Njilla, L. (2017, May). Provchain: A blockchain-based data provenance architecture in cloud environment with enhanced privacy and availability. In Proceedings of the 17th IEEE/ACM International Symposium on Cluster, Cloud and Grid Computing (pp. 468-477). IEEE Press

- 12. Ahram, T., Sargolzaei, A., Sargolzaei, S., Daniels, J., & Amaba, B. (2017, June). Blockchain technology innovations. In Technology & Engineering Management Conference (TEMSCON), 2017 IEEE (pp. 137-141). IEEE.

- 13. Sharma, P. K., Moon, S. Y., & Park, J. H. (2017). Block-VN: A distributed block chain based vehicular network architecture in smart city. Journal of Information Processing Systems, 13(1), 84.

- 14. Tosh, D. K., Shetty, S., Liang, X., Kamhoua, C., & Njilla, L. (2017, October). Consensus protocols for blockchain-based data provenance: Challenges and opportunities. In Ubiquitous Computing, Electronics and Mobile Communication Conference (UEMCON), 2017 IEEE 8th Annual (pp. 469-474). IEEE.

- 15. Stanciu, A. (2017, May). Blockchain based distributed control system for edge computing. In 2017 21st International Conference on Control Systems and Computer Science (CSCS) (pp. 667-671). IEEE.

- 16. Chibuye, M., & Phiri, J. (2017). Blockchain – it’s practical use for national data centres. Zambia ICT Journal, 1(1), 57-62.

- 17. Singh, M., & Kim, S. (2017, November). Introduce reward-based intelligent vehicles communication using blockchain. In SoC Design Conference (ISOCC), 2017 International (pp. 15-16). IEEE.

- 18. Singh, I., & Lee, S. W. (2017, November). Comparative requirements analysis for the feasibility of blockchain for secure cloud. In Asia Pacific Requirements Engeneering Conference (pp. 57-72). Springer, Singapore.

- 19. Cong, L. W., & He, Z. (2019). Block chain disruption and smart contracts. The Review of Financial Studies, 32(5), 1754-1797.

- 20. Kocsis, I., Klenik, A., Pataricza, A., Telek, M., De, F., & Cseh, D. (2018). Systematic performance evaluation using component-in-the-loop approach. International Journal of Cloud Computing, 7(3-4), 336-357.

- 21. Zhang, Y., Deng, R., Liu, X., & Zheng, D. (2018). Outsourcing service fair payment based on blockchain and its applications in cloud computing. IEEE Transactions on Services Computing.

- 22. Cong, L. W., & He, Z. (2018). Blockchain disruption and smart contracts (No. w24399). National Bureau of Economic Research.

- 23. Biais, B., Bisiere, C., Bouvard, M., & Casamatta, C. (2019). The blockchain folk theorem. The Review of Financial Studies, 32(5), 1662-1715.

- 24. Ahmad, F. A., Kumar, P., Shrivastava, G., & Bouhlel, M. S. (2018). Bitcoin: Digital decentralized cryptocurrency. In Handbook of Research on Network Forensics and Analysis Techniques (pp. 395-415). IGI Global.

- 25. Sharma, K., & Shrivastava, G. (2014). Public key infrastructure and trust of Web based knowledge discovery. Int. J. Eng., Sci. Manage., 4(1), 56-60.

- 26. Srivastava, S. R., Dube, S., Shrivastaya, G., & Sharma, K. (2019). Smartphone triggered security challenges – issues, case studies and prevention. In Cyber Security in Parallel and Distributed Computing: Concepts, Techniques, Applications and Case Studies. (pp. 187-206). John Wiley & Sons.

- 27. Sharma, K., Rafiqui, F., Attri, P., & Yadav, S. K. (2019). A two-tier security solution for storing data across public cloud. Recent Patents on Computer Science, 12(3), 191-201.

- 28. Kumar, P., Shrivastava, G., & Tanwar, P. (2020). Demistifying Ethereum technology: application and benefits of decentralization. In Forensic Investigations and Risk Management in Mobile and Wireless Communications (pp. 242-256). IGI Global.