In the 1980s, Congressional Republicans led an organized effort to get tax cuts through the Congress that were sold as tax cuts for everybody. But to the disappointment of the middle class, when the smoke cleared, most of the money went to the wealthy. One of the chief strategies used to convince the voters that tax reduction was good for everyone was “trickle-down economics” which theorized that the reduction of taxes on the wealthy would create more jobs and increased wages. Instead, it has led to inequality.

The Six Tax Laws

In the 1980s, Congressional Republicans organized an effort to get tax cuts through the Congress that was sold as tax cuts for everybody. But it wasn’t just a wealth transfer; people didn’t realize that during a time of deficit spending we increased the federal deficit without having the revenue to cover the additional costs.

1981—Economic Recovery and Tax Act: This bill was sold to the citizens as a recovery bill during the recession of 1981 to 1983 that would create jobs. This was the beginning of what would become supply side economics which was based on the assumption that tax cuts would somehow lead to jobs and growth.

The bill reduced the highest rate of taxation from 70 to 50 percent overnight and included an across the board decrease in marginal income tax rates by 23 percent. It also gave big businesses very generous depreciation rates, and it vastly expanded corporate tax loopholes which lowered taxes for corporations by $150 billion over five years.

1986—Tax Reform Act of 1986: A second tax act was passed which was supposedly designed to simplify the tax code, broaden the tax base, and eliminate many tax shelters. Senator Portman (R-Ohio) called on Congress to pass comprehensive tax reform to boost the economy. He refers to Reagan Administration tax cuts that “boosted American businesses by allowing them to compete on a level playing field and eased the financial burden of families.”

The reality was the 1986 Tax Act lowered the top tax rate from 50 to 28 percent, while the bottom rate was raised from 11 to 15 percent. Some middle-class citizens got a few bucks in the first years, but the vast majority of the money went to the top 10 percent. The low-class citizens were not represented in this Act and subsequently lost while the rich had a huge victory.

As a result of the 1981 and 1986 bills, the top income tax rate was slashed from 70 to 28 percent. Reagan focused his efforts on slashing taxes but paid little attention to the federal deficits. Reagan’s budgets tripled the national debt from $998 billion at the end of Carter’s last budget to $2.9 trillion at the end of Reagan’s last budget.

The problem was that the 1981 and 1986 tax cuts proved that cutting taxes when there is no offset and during times of deficits increases the deficit and creates serious problems for the country and the economy.

2001—Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA): Even though the country was sinking into a recession and deficits, it did not dissuade Republicans from pushing through more unbudgeted tax cuts. This tax cut was also sold to the citizens using supply side economics that promised jobs for tax breaks.

In the fine print of the bill was also included more itemized deductions for the wealthy as well as steep cuts in capital gains and dividend taxes. By employing “phase-ins,” it appeared that the average citizen would get proportionate cuts for ten years. But, instead, the average citizen would get a one-time $300 tax rebate, and as the phased in tax cuts grew through the decade, the top 1 percent of tax payers received a 51 percent tax cut.

2003—Jobs and Growth Tax Relief and Reconciliation Act: This bill was the second tax cut in the Bush Jr. administration and further lowered marginal tax rates—supposedly for all citizens. Since both the 2001 and 2003 bills were passed, the issue of who were the beneficiaries is still hotly debated. The Center on Budget and Policy Priorities concluded that “the largest benefits accrue to the highest income households.”1 President George W. Bush’s 2001 cuts were followed by continued job losses for about a year because of the recession, and it wasn’t until after 2003 that jobs were created.

The Bush forecast of jobs created by these tax cuts was 3.31 million jobs, but during his eight-year presidency, only 1.08 million jobs were created. The Clinton administration in the decade before Bush created 22.7 million jobs—without tax cuts.

The best analysis of the two Bush tax cuts was by the Center on Budget and Policy Priorities in 2008.2 They found the following myths and subsequent realities.

1. Tax cuts “pay for themselves.”

A study by the Treasury Department found that cutting taxes decreased revenues.

2. The economy grew strongly because of tax cuts.

The 2001 to 2007 economic expansion was subpar overall.

3. Extending the tax cuts is important for the economy’s long-run growth.

Extending the tax cuts without paying for them will reduce economic growth.

4. The tax cuts made the system more progressive.

The tax cuts led to more inequality.

5. The tax cuts made the tax system fairer to small businesses.

6. They provided large gains for those with high incomes and little benefit to others.

A New York Times editorial in 2011 said quite clearly, “The full Bush era tax cuts were the single biggest contributor to the deficit over the past decade, reducing revenues by about $1.8 trillion between 2002 and 2009.”3

2004: Another example is the special tax break President George Bush gave to large, public corporations in 2004 to repatriate $1 trillion stashed in overseas tax havens to avoid U.S. corporate taxes. He gave them a one-time tax deal of 5 percent taxes under the banner of creating more jobs and investment. Michael Mundaca, Assistant Secretary for Tax policy wrote, “Unfortunately, there is no evidence that it increased U.S. investment or jobs, and it cost tax payers billions.”

2017—The Tax Cut and Jobs Act (TCJA): The Tax Cuts and Jobs Act (TCJA) of 2017 was the fifth big tax cut since 1981, reducing corporate taxes from 35 to 21 percent, or by $1.5 trillion over 10 years. I think it is fair to say that the TCJA is the ultimate test of supply side economic theory because just like the previous four tax cuts it promised to create millions of jobs.

Treasury Secretary Steve Mnuchin said in October 2017 that tax cuts would push “GDP growth over 3 percent or higher leading to millions and millions of jobs.” Perhaps, the biggest blunder of the Trump administration was the claim that the TCJA “would add $1.8 trillion in new revenue that would more than pay for the $1.5 trillion cost of the tax cuts themselves.” The implication is that increased economic growth would boost tax revenues enough to offset the tax cuts. But this optimistic scenario simply did not happen.

To prove that the TCJA worked as proposed requires real investment. The Economic Policy Institute says, “If the TCJA’s corporate rate cuts are to even have a chance at reaching your paycheck, first investment has to boom. The results have been abysmal for the TCJA.” The data in Figure 9.1 provides no evidence for an investment boom from the TCJA year-over-year change in real, nonresidential fixed investment, from 2005 to 2019.

Figure 9.1 shows that “year-over-year real, nonresidential fixed investment growth continues to stagnate. If the TCJA was working, we should have seen an investment boom. Instead, after the passage of the TCJA, investment growth continued along its pre-TCJA trend for a couple quarters before falling all the way to 1.3 percent in 2019 Q3.”

Figure 9.1 Nonresidential fixed investment

Source: EPI analysis of data from table 1.1.6 from the National Income and Product Accounts (NIPA) from the Bureau of Economic Analysis (BEA).

Contrary to the Trump administration claims, the TCJA did not increase GDP over 3 percent, create millions of jobs, or add $1.8 trillion in new revenue that would than pay for the $1.5 trillion cost of the tax cuts; because tax receipts declined and growth did not pay for the tax cuts, the TCJA is simply increasing the federal deficit.

The fact is, prior to the TCJA, few corporations paid the 35 percent corporate tax. After the many deductions offered, 400 of America’s largest corporations paid an average federal tax rate of about 11 percent on their profits in 2019, roughly half the official rate established under President Trump’s 2017 tax law, according to The Washington Post.4

A 2017 study by the Institute for Policy Studies found that across-the-board corporate tax cuts don’t do much to create jobs. It compared 92 publicly held corporations who paid less than the 35 percent corporate tax rate. It found that, between 2008 and 2016, these corporations lost jobs while the overall economy increased jobs by 6 percent. Instead of paying taxes or hiring, these companies bought back their own stocks.5 The study also found that what does create jobs is extending unemployment and cutting payroll taxes.

CARES ACT: The Coronavirus Aid, Relief, and Economic Security Act, also known as the CARES Act, was a $2.2 trillion economic stimulus bill passed by the 116th U.S. Congress and signed into law by President Donald Trump on March 27, 2020. This was the 6th tax act that was passed without raising taxes to pay for it.

Overseas Tax Havens: Another tax avoidance scheme used by the U.S. MNCs is to keep their money in overseas accounts (tax havens) rather than bringing them into the United States. In 2017, according to The Institute on Taxation, the 500 largest American companies held more than $2.5 trillion in accumulated profits offshore to avoid U.S. taxes and would collectively owe an estimated $767 billion in U.S. taxes if they repatriated the funds.6

They lobbied Congress and the administration to give them a onetime corporate tax holiday at an income tax rate of 5 percent to bring the money into the country. Backers say that it will create thousands of new jobs and new investments, but the last time President Bush gave them a tax holiday in 2004, there was no evidence of new jobs and almost all of the money went to the shareholders.

Tax deductions for outsourcing jobs: In an incredible twist of fate, MNCs are able to get tax deductions when they close American factories and move them to foreign countries. This has been going on since outsourcing began, but it was one of those dirty little secrets not known by the public. A bill to eliminate these tax breaks called the “No Tax Breaks for Outsourcing Act” was introduced in the Congress in March 2021. It would remove incentives for companies to take their business abroad and close the corporate inversion loophole. As of August 2022 Congress hadn’t passed this bill.

Tax inversions: Another clever tax avoidance scheme was created by large pharmaceutical manufacturers. They buy or merge with a foreign company and move their headquarters to a foreign country like Ireland— which has a corporate tax rate of 12.5 percent. Many experts agree the only way to stem the tide of companies moving overseas would be to switch to a more equitable “territorial” system, which would tax corporations only on the income they earn in the United States. Most countries follow the territorial model.

The anti-inversion proposal, announced by the Treasury Department as part of a more detailed version of Biden’s new tax plan, would tighten the threshold at which companies lose the tax benefits of doing an inversion.

All of these tax avoidance schemes make me wonder how much tax reduction is enough? Corporations and the wealthiest American have had fantastic increase in total wealth over the last 42 years. Figure 9.2 shows that the gap between federal revenues and outlays continues to widen. Cutting federal deficits during a pandemic is politically impractical, but the logical conclusion is that taxes must be increased or economic problems will become dire.

Most of the gains for the middle class from the New Deal have gone away, and the top 1 percent of income earners have gone from 8 percent in 1978 to 37 percent of the total income of the country (See Figure 1.2 in Chapter 1).

According to the Institute for Taxation and Economic Policy in 2020, 55 American corporations paid 0 taxes, and in fact, they received a combined federal rebate of more than $3 billion for an effective tax rate of approximately a negative 9 percent. These corporations have lobbied hard for tax deductions such as tax breaks for stock options, credits for research and experimentation, and write-offs for renewable energy and capital investments. President Biden wants to change this and publicly said, “We are asking corporate America to pay their fair share.”

Figure 9.2 Federal outlays and revenues

Source: Summary of receipts, outlays, and surpluses or deficits in current dollars and a percentage of GDP: 1980 to 2013, White House, Office of Management and Budget, Historical tables, Table 1.3, June 7, 2021.

The Big Lie—Trickle-Down Economics

There has been a widely accepted economic concept that was created during the Reagan administration and has been used and abused in every election since 1980. It has been called trickle-down economics, supply side economics, and the Laffer Curve, and it assumes that there should be no or few barriers to the accumulation of wealth, because if the rich do well, benefits will trickle down to everybody else. Since the Laffer Curve days, the theory has expanded to suggest that lower tax rates, estate taxes, and capital gains on high-income people and corporations will benefit everyone by increasing GDP growth, wages, and jobs.

The idea of lower taxes that lead to more jobs became so popular that despite recessions and the decline of median income of the middle class, it is still regarded by conservatives as some kind of absolute truth.

For instance, during the vice-presidential debate in 2012, Congressman Paul Ryan said that “Republicans expect tax cuts to create somewhere between 7 and 12 million jobs, grow the tax and balance the budget.” If you take his plan literally, you can assume that cutting taxes for the wealthiest people would actually increase tax revenue for the government. The fact is, we have had five tax laws passed since 1981 that lowered taxes to the wealthy and corporations, and there is very little proof that tax reduction had anything to do with increasing the number of jobs or higher wages.

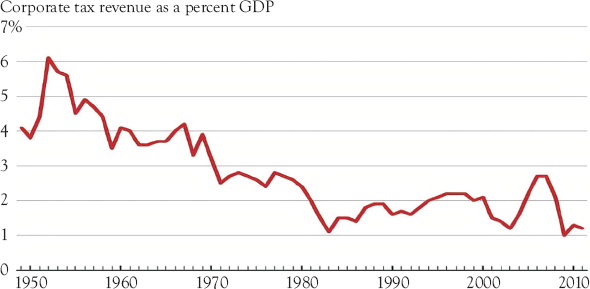

Even though corporations complain about the corporate tax rate, history shows that the effective corporate tax rate has been steadily declining for decades. Figure 9.3 shows that as a percentage of GDP corporate tax revenues dropped to a new low in 1984 after the first tax cut law and have stayed low ever since.

Figure 9.3 Corporate tax revenues are at historic lows

Source: Office of Management and Budget.

The corporate share of total federal tax revenue has dropped by two thirds in the last 60 years. The obvious conclusion is that corporations are simply not paying their fair share.

The Myth That Never Goes Away

The idea that wealthy people and corporations will create more jobs when paying lower tax is a myth that simply won’t go away. What the five tax cuts prove is that politicians can make any claim they want about the creation of jobs, growth, wages, and the budget, because they know that once the tax law goes through Congress there will be little, if any, follow-up and the public will lose interest. They now have proved historically that any time they want another tax cut, they only have to bring out another variation of trickle-down economics. It works every time. But in the past 40 years, both government agencies and independent economists have looked into the issue and found there is little or no supporting evidence of a correlation.

In recent years, quantitative studies have been showing up to measure the link between tax reductions, wages, and jobs. The Congressional Research Service (CRS) is a nonpartisan entity associated with the Library of Congress that does academic quality research to answer difficult policy questions.

In 2019, the CRS released a study that concluded that:

The reduction in top tax rates appears to be uncorrelated with saving, investment, and productivity growth. The top tax rates appear to have little or no relation to the size of the economic pie. However, the top tax rate reductions appear to be associated with the increasing concentration of income at the top of the income distribution. The report notes that tax rates were at the highest when growth was at its peak, and that the reduction in tax rates has not had any discernible impact on the types of investment that lead to growth.7

It is also notable that as soon as the CRS report was issued, Senator Chuck Grassley (Republican chairman of the Senate Finance Committee at the time) sent a letter to the CRS taking issue with its findings.

Other studies have also proved that tax rate reductions are correlated with the increasing concentration of income at the top of the income distribution and that supply side theory is flawed. David Stockman, one of the designers of supply side economics, admits that:

There is no realistic way for “Trickle-Down” economics to work and increase the income of the working classes of America. In fact, I am certain that the developers of the theory of “Trickle-Down” economics were fully aware of this and that “Trickle-Down” has in fact worked as intended. This means that the intent behind implementing “Trickle-Down” was to benefit the wealthiest Americans at the expense of working-class Americans.

Stockman said,

Giving small tax cuts across the board to all brackets was a “Trojan Horse” that was used to get approval for the huge top bracket cuts. Trickle down was a term used by Republicans that actually meant giving tax cuts to the rich.

I was always skeptical of the idea that tax reduction could create jobs, but I also wondered why this idea has pervaded our culture as an acceptable economic theory and had so much traction for so many years. I guess that if you say something often enough and treat it is an absolute economic truth people will accept it. There is now an enormous amount of evidence that proves that increases in jobs, wages, and investment in capital equipment are really driven by demand, not tax cuts, and we need to say this more often.

Politicians need to use this myth to justify selling their programs, and they will continue to use the tax reduction myth and sell it as an economic truth no matter what the evidence.

A good example was Congressman Paul Ryan’s Path to Prosperity plan in 2009. He says right in the introduction of his plan that “fixing our broken tax code will create jobs and increase wages.” He wanted to reduce taxes in most of the tax brackets, and he also wanted to eliminate capital gains taxes, inheritance taxes, and taxes on interest. He said that “these tax cuts will create nearly 1 million new private-sector jobs next year and result in 2.5 million additional private-sector jobs in the last year of the decade.”

He also claimed it spurs economic growth, increasing real GDP by $1.5 trillion over the decade, and it unleashes prosperity and economic security, yielding $1.1 trillion in higher wages and an average $1,000 per year in higher income for each family. However, an analysis of Paul Ryan’s tax proposal showed it would give people making around $30,000 per year about $246 per year. But those making more than $1 million a year would save $265,011 per year (according to the Center on Budget and Policy Priorities).

Many supporters of tax cuts are also critics of federal budget deficits, and they don’t seem to acknowledge that their tax reduction will increase the deficit (or they don’t care). In fact, all tax cuts from now on will increase the federal deficit unless they are passed with offsets.

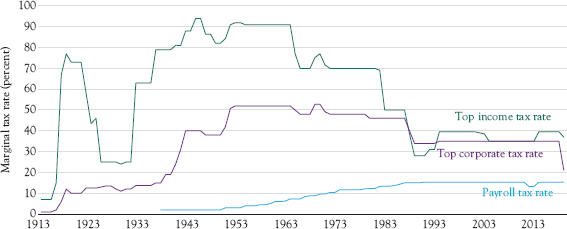

Figure 9.4 is as chart from the Brookings Institute Hamilton Project which provides context for the debate over tax cuts and tax revenue. It shows that both top income tax rates and corporate tax rates went down below 25 percent during the 1920s. After the crash of 1929, New Deal legislation pushed the top marginal tax rates as high as 90 percent and the corporate tax to 50 percent. It wasn’t until the Reagan administration that the top marginal tax rate was dropped from 70 to 35 percent and the corporate tax rate was dropped from 50 to 28 percent. These rates have varied little in the last 36 years and the wealthy have done exceedingly well for four decades. The only serious attempt by the government to find new taxes has been the rise of payroll taxes which was at the expense of working people.

Figure 9.4 Historical tax rates, 1913 to 2013

Source: Internal Revenue Service (IRS) 1913 to 2018; Social Security Administration (SSA) 1937 to 2018; Urban–Brookings Tax Policy Center (TPC) 1913 to 2018; authors’ calculations.

Note: Data for the top income tax rates are from the TPC. Data for the top corporate tax rates are from the IRS. Data for the payroll tax rates are from the SSA. Payroll tax includes both the employee and employer contributions.

The United States is a relatively lightly taxed economy compared to most Western Nations. High levels of inequality and rising deficits will probably force Congress to consider raising taxes on the wealthy and corporations. The question is whether the multinationals will be willing to “pay their fair share” or do another Dodd–Frank lobbying blitz to keep their taxes down at the expense of the country and maybe the economy? Or they may choose to move their corporations to a low tax country and export their products to the United States.

The specter of multinational corporations (MNCs) avoiding income taxes on billions in profits sends a bad signal to the average American that the tax system is stacked against them. U.S. MNCs have had a good 40-year run of low taxes, and all evidence shows that the tax cuts have not increased jobs or GDP growth. They can help their country and their stakeholders by paying their fair share.

1 J. Friedman and I. Shapiro. July 01, 2010. “Tax Returns: A comprehensive Assessment of the Bush Administration’s Record on Cutting Taxes, CBBP.

2 Tax cuts: Myths and Realities. May 09, 2008. Center on Budget and Policy Priorities.

3 Taxes the Deficit and the Economy. September 21, 2011. New York Times.

4 J. Stein, and C. Ingraham. December16, 2019. Corporations Paid 11.3 Percent Tax Rate Last Year After Steep Drop Under Trump’s Law.

5 K. Amadeo. October 30, 2021. “Do Tax Cuts Create Jobs, If so, How?” The Balance.

6 Fortune 500 Companies Hold a Record $2.6 Trillion Offshore. March 28, 2017. Institute on Taxation and Economic Policy, Washington, DC.

7 Professional Staff, Senate Finance Committee. May 31, 2019. The Economic Effects of the 2017 Tax Revision, Congressional Research Services Paper R45736.