Chapter 4

Cash

Cash is both an investment class in its own right, and of course the means of exchange that is used to pay for investments in the other asset classes such as securities and derivatives.

4.1 CASH AS A MEANS OF EXCHANGE

Cash is used to pay and receive funds as a result of trading in other instruments. In this context cash is a currency such as pounds sterling, United States dollars, Japanese yen, etc. Currencies are usually identified by a three character ISO currency code such as GBP, USD and JPY. Cash is held at bank accounts, and the location of these accounts is generally, but not exclusively, in the country that uses that particular currency as its own official currency. There are exceptions to this rule, for example all European Union countries offer bank accounts in euros, even if, like the United Kingdom, the euro is not the official currency of the country concerned.

The relationship between countries and currencies is a many (country) to one (currency) relationship. Even before the advent of the euro in 1999 there were examples (such as Panama which uses the United States dollar) of one country using the official currency of another country as its official currency.

For each currency there are associated working days and holiday calendars. Nearly all currencies use Monday to Friday as normal working days, and banks are closed at weekends. There are exceptions to this rule – some Islamic countries close their banks on Fridays and open them on Sundays.

Each currency is also linked to a calendar of public holidays when banks are closed and no transactions in that currency are able to settle across a bank account. For retail transactions there may be many such public holidays in the year; for wholesale transactions such as trading in securities and derivatives there may be very few. For example, the only days that are considered to be public holidays for settlement of trades using euros are 1 January and 25 December each year.

On a public holiday for the country concerned the following are generally true:

- Investment exchanges are closed, so that no new trades in instruments listed on those exchanges can take place.

- Banks are closed, so that:

– No trades of an earlier trade date may settle

– No coupons or dividends can be paid

– No “fixings” of benchmark interest rates such as LIBOR or EURIBOR can take place.

Chapters 10 and 23 will examine the requirement to hold calendars and holiday calendars as part of static data in business applications.

4.1.1 Interest calculation methods for currencies

When calculating interest for fractions of years for currency transactions, the following calculation methods are used:

- Actual number of days/360: This method is used for all currencies except pounds sterling and Japanese yen. Calculate the difference between two dates, and divide the answer by 360.

- Actual number of days/365: This method is used for pounds sterling and Japanese yen. Calculate the difference between two dates, and divide the answer by 365, or 366 if the year concerned is a leap year.

4.2 CASH AS AN INVESTMENT CLASS

Investment industry participants use cash as an investment class in two ways, foreign exchange transactions and money market loans and deposits.

4.2.1 Foreign exchange transactions

The FX (foreign exchange) market exists wherever one currency is traded for another. It is by far the largest financial market in the world, and includes trading between large banks, central banks, currency speculators, multinational corporations, governments, and other financial markets and institutions. The FX market is by far the largest investment market in the world. In 2004, the Bank of International Settlements (BIS) estimated that the average daily turnover of this market was worth USD 1.9 trillion, which is equivalent to

- More than 10 times the average daily turnover of global equity markets

- 40 times the average daily turnover of the New York Stock Exchange

- USD 300 a day for every man, woman, and child on earth

- An annual turnover more than 10 times the value of all the world’s goods and services combined.

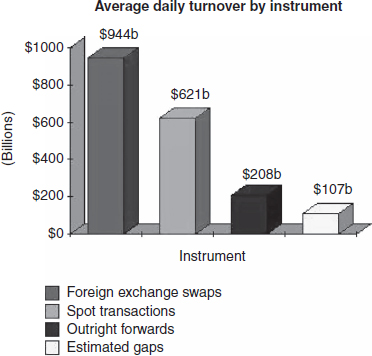

More than 50% of this turnover is carried out in the United Kingdom and the United States. The daily turnover by transaction type is shown in Figure 4.1.

Figure 4.1 FX daily turnover by transaction type

The different transaction types may be summarised as follows:

- Spot transactions occur when a trading party buys one currency with a different currency for immediate delivery, rather than for future delivery. The standard value date for foreign exchange spot trades is T + 2 days, i.e. two days from the date of trade execution. The price of a spot FX deal is known as the exchange rate of the transaction.

- Forward transactions are those where value date is greater than the standard two days for a spot transaction. The price of a forward FX transaction will be different to that of a spot transaction. The difference in price will reflect the fact that the two currencies concerned have different interest rates. The relationship between spot and forward prices is calculated by the following equation:

![]()

where:

F = forward price

S = spot price

rT = interest rate of the term (i.e. bought) currency

rB = interest rate of the base (i.e., sold) currency

T = tenor (calculated according to the appropriate day count convention – see section 3.2 for more details of the day count conventions).

Worked example

On 3 February 2008 a firm wishes to do a forward deal buying USD and selling GBP for value date 5 March 2008.

The normal spot value date for such a deal is 5 February 2008, so settlement is delayed for 29 days.

The spot exchange rate is USD 2.01 = GBP1.

The current interest rate for the US dollar is 5.5%, calculated on an actual/360 day basis. The current interest rate for the pounds sterling is 5.0%, calculated on an actual/360 day basis.

The calculation is as follows: F = 2.01 * (1 + 5.5 * 29/360)/ (1 + 5.0 * 29/365) = 2.75878

FX swaps consist of two legs which are executed simultaneously for the same quantity, and therefore offset each other:

1. A spot foreign exchange transaction

2. A forward foreign exchange transaction.

Investors use forex swaps to speculate on changes in the interest rate differentials between two currencies. If the forward exchange rate for a particular currency was lower than the spot rate, an investor might sell a currency at the spot rate and buy it back at the forward rate.

4.2.2 Money market loans and deposits

Banks offer their clients the ability to place deposits or to take out loans for periods of up to 13 months. Call and notice loans and deposits have no agreed maturity date when the transaction is first agreed, while time deposits and time loans and deposits have an agreed maturity date. What one of the parties considers a loan, the other party of course considers a deposit. The rule is that if funds are received by Party A from Party B on the commencement date of the transaction then Party A has attracted a deposit, and Party B has placed a loan.

Worked example

On 5 February 2008 Bank A agrees to lend Bank B USD 1 000 000 for 31 days between 8 February 2008 and 10 March 2008 at 5% interest.

The amount of interest that Bank B has to repay to Bank A on 10 March is therefore USD 4305.56; which is calculated as:

Interest = Principal amount * Interest rate * Days difference between start date and end date/360

= 1000 000.00*5%* 31/360

The divisor of 360 is used because the currency of the transaction is USD. If it had been GBP or JPY then a divisor of 365 would have been used

Because this is a time deposit/loan, two working days before the termination date of the transaction the two parties need to get in touch with each other and agree either that:

- They will terminate the transaction as originally agreed by Party B returning the principal amount plus the interest to Party A; or

- They may agree to roll over the transaction for a further period. In this case Party B needs to make payment of only the interest to Party A. Rolling over implies a renegotiation of the interest rate for the next period.

Some forms of loan and deposit transactions – known as sale and repurchase agreements or repos – involve the use of securities as collateral. These types of transactions will be examined in detail in Chapter 21.

4.3 MORE TRADE TERMINOLOGY

We now have some further trade terms from the FX and loan and deposit transactions (Table 4.1) to add to those that we have gathered from examining equity and bond trades.

Table 4.1 FX trade terminology

| Term | Explanation |

| Spot date | The value date of a spot FX transaction, or the value date of the start leg of an FX swap |

| Forward date | The value date of a forward FX transaction, or the value date of the end leg of an FX Swap |

| Spot price | The exchange rate used in a spot FX transaction or the start leg of an FX swap |

| Forward price | The exchange rate used in a forward FX transaction or the start leg of an FX swap |

| Exchange rate | The price of an FX transaction |

| Deposit | When a financial institution borrows money from another institution, it is said to “attract a deposit” |

| Loan | When a financial institution lends money to another institution, it is said to “place a loan” |

| Call or notice | A loan or deposit that has no agreed maturity date |

| Start date | The value date of the first leg of a loan or deposit transaction |

| Maturity date | The value date of the end leg of a loan or deposit transaction |